The MAC Cup II law student M&A negotiation competition has launched! Sixty-four student teams from forty-six schools across the US and Canada are squaring off in multiple qualifying rounds to join the “Final Four” in-person championship in Laguna Beach, California, and to win awards for best agreement mark-ups, all while learning to advocate their (made-up) clients’ positions.

The ABA Business Law Section’s M&A Committee launched the inaugural MAC Cup last year, with Nada Abousena and Grace Baer of American University taking top honors in front of the membership of the M&A Committee and a panel of invited judges. The M&A Committee has expanded this year’s MAC Cup to include more teams, more negotiations, and more awards, with continued access for students to M&A practitioners and professional M&A resources, promising to make the MAC Cup the premier hands-on transactional learning experience for law students with a passion for M&A.

“We’re giving law school students opportunities to learn about and apply M&A negotiation skills, like the litigation opportunities they get during the more traditional moot court,” said Mike O’Bryan, immediate past chair of the M&A Committee. “We want students to think about M&A as a significant part of their legal careers and to develop some practical skills to get them started.”

Nada Abousena and Grace Baer of American University Washington College of Law, coached by David Albin, won the inaugural MAC Cup in January 2024. Photo by Baldemar Fierro.

Building on Past Success

This year’s participation figures highlight the growing importance and reach of the competition.

“This year, we had eighty-nine applications,” said Thaddeus Chase, a member of the M&A Committee subcommittee that runs the MAC Cup. “This represents a 75 percent increase in submissions. And our targets will be even more aggressive for MAC Cup III.”

Other members of the MAC Cup subcommittee are O’Bryan, Wilson Chu, Glenn West, Tom Romer, Caroline Shinkle, and Sacha Jamal. All are members of the M&A Committee and practicing M&A attorneys, though Romer recently left the practice to form Dexterity, a digital negotiation platform designed for M&A (and now hosting the MAC Cup documents). Curtis Anderson, a professor at BYU Law School and former practicing outside and in-house M&A counsel, also is on the subcommittee and brings experience in organizing law school competitions.

“This year, by expanding the field, we’ve provided more students/law schools the opportunity to gain experience from the competition and the chance to compete,” said Chase. “It allows for more students to become connected and build a network across law schools and the M&A Committee. We’ve also built in the wrinkle that students may need to switch sides (i.e., from Buyer to Seller or from Seller to Buyer) with a week’s notice—we think this pushes students to think critically and drives home the point that the best outcome for a deal is usually somewhere in the middle (not everyone wins every point/issue).”

Learning New Skills

What do students learn?

M&A concepts; critical thinking; understanding the meaning of a “win” in M&A transactions; and the knowledge that this competition is not done in isolation: students can leverage the advice, guidance, and support of participating legal practitioners.

“The synergy between the law students and our members (whether as judges or coaches) is really dynamic and reflects the M&A Committee’s commitment to provide practical training to a new generation of M&A lawyers,” said Caroline Shinkle, a subcommittee member who has witnessed the excitement and rewards of this competition.

“Without a doubt, there is a level of seriousness that permeates student participation,” said Shinkle. “And yet this seriousness is tempered by the excitement created by the coaches and judges—generating a level of interaction rarely seen at this level.”

2024’s winners were announced at the M&A Committee’s annual meeting in Laguna Beach after facing off in a mock negotiation in front of attendees. Photo by Baldemar Fierro.

The Challenge of a Competitive Path

For students to make the “Final Four” is an indication of their hard work and negotiation skills—but also the strategic planning and coping skills needed to survive all phases of the competition.

The MAC Cup II schedule is intense:

Initial issues list and Acquisition Agreement mark-up due: October 21, 2024

First Open Round: October 26–27, 2024 (virtual)

Second round issues list and Acquisition Agreement mark-up due: October 30, 2024

Second Open Round: November 2–3, 2024 (virtual)

Elite 8 Quarterfinal Negotiation Matches: January 25, 2024 (virtual)

Semifinals: January 30, 2025 (in person), Laguna Beach, California

Finals: January 31, 2025 (in person), Laguna Beach, California

Opportunities for Lawyers

The competition provides opportunities for M&A practitioners to work with the students as judges or coaches. For the MAC Cup II, while the qualifying rounds are completed, lawyers still can act as judges in the virtual “Elite Eight” or the in-person “Final Four” rounds in January—if you’re interested, contact Thaddeus Chase (at [email protected]). In the longer run, there also will be opportunities for lawyers to recruit competitors and to coach or judge in next year’s MAC Cup III.

“At each stage, from initial issue spotting through final negotiations, students benefit from the legal talents of M&A Committee members who serve as judges and coaches,” said Romer.

Wendy Li and Alexis Brugger of University of Pennsylvania Carey Law School, who took second place in 2024, were coached by Debra Gatison Hatter. Photo by Baldemar Fierro.

Line Up to Be a Part of MAC Cup II

An impressive list of sponsors has already lined up to be part of MAC Cup II: M&A supporting companies Thomson Reuters, Hotshot, and Dexterity, and law firms Sullivan & Cromwell, Ropes & Gray, McDermott Will & Emery, Freshfields, Goodwin, Morrison Foerster, and Morris James. And the list is only getting longer!

“The sponsors have recognized that transactional skills have been sadly lacking in law student graduates. We’re changing that with the opportunities provided by the MAC Cup,” said Wilson Chu, former M&A Committee chair. “The transactional skills learned by students are invaluable.”

As the excitement leading up to the Laguna championship heats up, it has been proven, once again, that the BLS M&A Committee is at the forefront in its commitment to improving the knowledge and skills of law students throughout the nation.

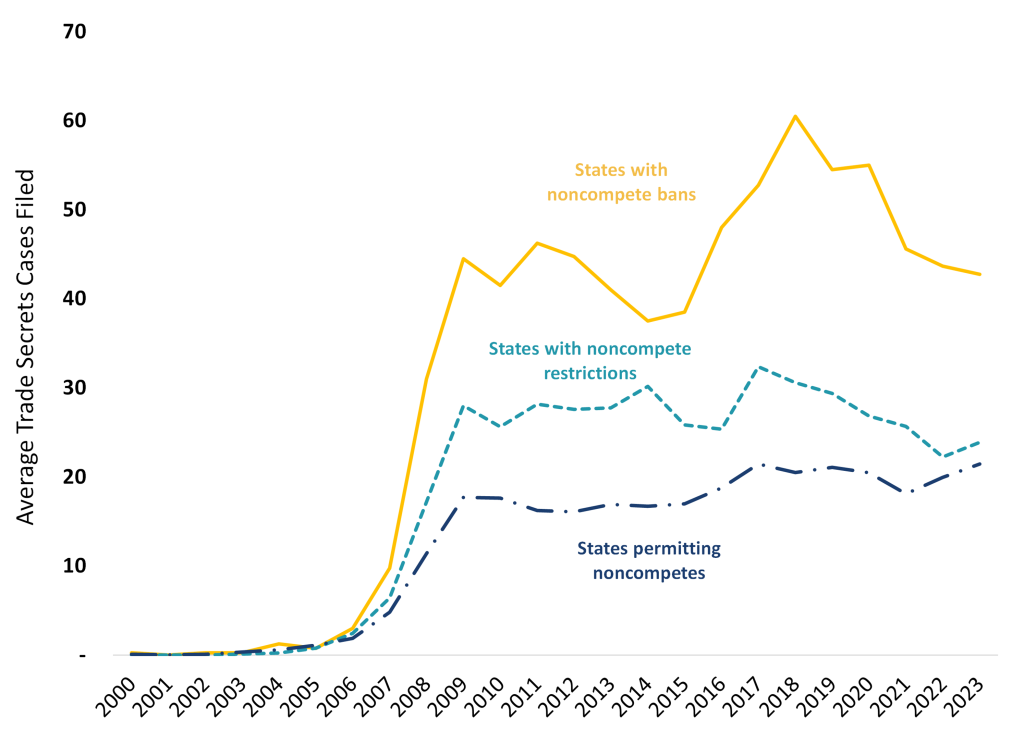

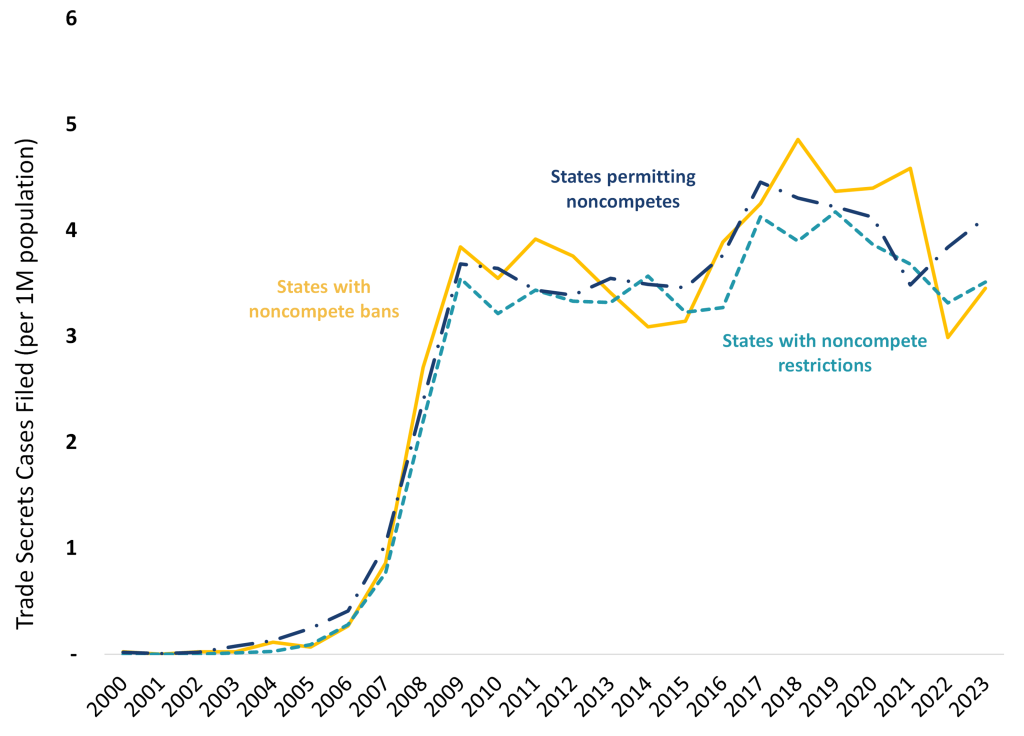

Contractual covenants not to compete, or “noncompetes,” restrict “a man’s natural right to follow any trade or profession anywhere he pleases and in any lawful manner.”[1] Delaware courts “frown on or disfavor restrictive covenants,” particularly in employment contracts, but such provisions have historically been enforced.[2] While the applicable standard has remained nominally consistent, recent case law suggests that these provisions are being scrutinized more closely.

The Reasonableness Test

Delaware courts “do not mechanically enforce or deny noncompetes but closely scrutinize[] them as restrictive of trade.”[3] A noncompete will be enforced only if it “(1) [is] reasonable in geographic scope and temporal duration, (2) advance[s] a legitimate economic interest of the party seeking its enforcement, and (3) survive[s] a balancing of the equities.”[4]

These requirements must be reviewed “holistically and in context.”[5] As Vice Chancellor Laster explained,

[a] court must not tick through individual features of a restriction in isolation, because features work together synergistically. For example, “a court must consider how the temporal and geographic restrictions operate together” because the “two dimensions necessarily interact.” A covenant that restricts employment in a similar industry for two years might be reasonable if it only applies within a single town or county, and vice versa. All else equal, a longer restrictive covenant will be more reasonable if geographically tempered, and a broader restrictive covenant will be more reasonable if temporally tailored.[6]

When a noncompete is entered into in connection with the sale of a business, the court must still evaluate its reasonableness, but the “inquiry is less searching than if the covenant had been contained in an employment contract.”[7]

The fact-intensive nature of this inquiry does not lend itself to bright-line tests; however, the case law has revealed some common themes.

Geographic Scope

“[T]he reasonableness of a covenant’s scope is not determined by reference to physical distances, but by reference to the area in which a covenantee has an interest the covenants are designed to protect.”[8] Courts have found noncompetes to be reasonable when limited to the areas where a company does business.[9] Provisions that apply beyond the company’s area of operations, have worldwide or nationwide application, or include the company’s affiliates or subsidiaries have been heavily criticized.[10]

While nationwide or worldwide restrictions are often considered overbroad, courts have enforced them when they are entered into in connection with the sale of a business.[11]

A lack of geographical restrictions is unusual, but it does not render the restriction unenforceable per se.[12] If the other aspects are reasonable, Delaware courts may still enforce the noncompete.[13]

Duration

As a general matter, the longer a restrictive covenant applies, the narrower its geographic and subject matter scope must be.[14] Delaware law does not provide a specific reasonable duration. Noncompetes lasting two years are the most commonly approved.[15] However, Delaware courts have found that restrictions lasting one year and three years were reasonable.[16]

In Ainslie v. Cantor Fitzgerald, Limited Partnership, the Delaware Court of Chancery found that a four-year noncompete contained in a partnership agreement was unreasonable, but it suggested that such a duration may be “in the range of reasonable” if the scope of the restriction were appropriately narrowed.[17]

Delaware courts have upheld longer durations when the provision arises in connection with the sale of a business or stock.[18]

Legitimate Economic Interest

Like the other aspects of this analysis, the existence of a legitimate economic interest is highly fact intensive. In evaluating the alleged economic interest, courts have considered a variety of factors, including (i) the employee’s exposure to confidential information, proprietary technology, and other trade secrets; (ii) the level of training and skill that was required to perform the work; and (iii) the employee’s general role with the company.[19]

The specificity of the applicable language is also important. Vague terms such as similar to or substantially the same as when referring to the company’s business have been found to be too vague to demonstrate a legitimate economic interest.[20] Noncompetes prohibiting conduct that directly competes with, or is similar to, the business of the company, and only the company, have been found to be enforceable.[21]

Finally, the breadth of the restriction is also considered. As the court in Fortiline, Inc. v. McCall held, a broader restriction requires a broader legitimate interest. Noncompetes that cover a company’s affiliates or that broadly define a company’s business have been routinely rejected as not being “tailored to the employee’s role while employed.”[22]

Delaware courts have held that protecting a company’s goodwill, confidential information, customer base, and/or competitive advantage gained through the employee’s efforts may each be a legitimate economic interest.[23] The identity of a company’s referral sources may be protectable provided that those sources are not transient in the industry.[24] A company’s desire to prevent its employees from working directly for its clients (known as disintermediation) may constitute a legitimate economic interest in appropriate circumstances.[25]

However, courts have rejected claims that a noncompete was necessary when the interests being protected were “vague and everyday concern[s],”[26] including that (i) the employee was generally “responsible for many . . . customer relationships,”[27] or involved in “finding deals and fostering relationships” with customers;[28] (ii) the employee would be able to use the technical expertise or general industry knowledge they gained while employed by the company against it;[29] and (iii) the employee could use an important certification the company paid for them to get against it.[30]

Balancing of the Equities

Finally, Delaware courts balance the company’s interest in preventing competition with the harm that would befall the employee if the covenant were enforced.

The recent case law suggests that this balance focuses on an employee’s ability to earn a living and the role the employee played in the company. Given Delaware’s concern for employees’ well-being, it is not surprising that courts have been critical of provisions that will prevent a person from earning a living.[31] The role that the employee had with the company is also an important factor. Given the typically disparate bargaining power between a company and its employees, noncompetes with lower-level employees are routinely rejected as unreasonable. However, Delaware courts have been less critical of provisions applying to senior executives who received significant compensation or who were critical to the negotiation of the transaction that led to the creation of the noncompete.[32]

The “Blue Pencil” Rule

As a court of equity, the Delaware Court of Chancery in the past has revised the scope and/or duration of a noncompete.[33] But this process, known as using a “blue pencil,” has been criticized and rarely applied in recent years. As Vice Chancellor Laster explained in Sunder Energy, LLC v. Jackson,

revising an overbroad restrictive covenant creates a no-lose situation for employers because businesses can draft the covenant as broadly as possible, confident that the scope of the restriction will chill some individuals from departing. If someone does challenge the provision, then the worst case is that the court will blue-pencil its scope so it is acceptable. It also enables employers to extract benefits at the expense of employees by including unenforceable restrictions in their agreements.[34]

In Labyrinth, Inc. v. Ulrich, the court denied a motion to dismiss because, even though the ten-year-long restrictive covenant was overbroad in several ways, the fact that the employee was personally and deeply involved in negotiating the covenant in connection with the sale of his business “may conceivably present a rare instance where equity and public policy might require blue penciling.”[35]

Contractual Provisions Regarding Reasonableness

The “reasonableness” analysis cannot be avoided via contractual provisions. Companies may attempt to contract around the reasonableness requirement by including provisions pursuant to which the employee (i) agrees that the restrictions are reasonable, (ii) waives any defense that they are not, and (iii) agrees that a court may modify the provision if it is deemed unreasonable as drafted. However, Delaware courts have repeatedly held that such provisions are ineffective and do not relieve the court of its obligation to determine the reasonableness of the provision.[36]

“Forfeiture for Competition” Provisions Recently Upheld

As the Delaware Supreme Court recently explained in Cantor Fitzgerald, Limited Partnership v. Ainslie, so-called “forfeiture for competition” provisions are not evaluated for “reasonableness.”[37] Forfeiture for competition provisions are contract provisions that relieve the company of obligations to pay an employee deferred financial benefits if the employee breaches a noncompetition provision in the contract. As the Delaware Supreme Court held in Cantor, such provisions “stand on different footing” than noncompetes because they do not “limit a [person’s] ability to compete or otherwise obtain employment.”[38] Unlike noncompetes, forfeiture for competition provisions are “a condition precedent that excuses [the company] from its duty to [make future payments] if the [employee] fail[s] to satisfy a condition to which they agreed to be bound in order to receive a deferred financial benefit.”[39] As a result, forfeiture for competition provisions are not reviewed for reasonableness but rather enjoy the “court’s deference on equal footing with any other bargained-for-term” in a contract.[40]

Statutory Limitations

Even if the provision satisfies the reasonableness standard, Delaware law prohibits the use of noncompetes in some narrow circumstances. By way of example, noncompetes between physicians that restrict the physician’s right to practice medicine in a particular area or for a particular time period are void (although provisions requiring the payment of money damages for a breach of such provision are enforceable).[41]

Other states have gone even further than Delaware and enacted statutes prohibiting or strictly limiting the enforceability of such provisions.[42]

The FTC’s Effort to Ban the Use of Noncompetes

Earlier this year, the Federal Trade Commission (“FTC”) issued a final rule (“Final Rule”) that, subject to certain specific exceptions, made it a violation of section 5 of the Federal Trade Commission Act for employers to enter into new noncompete agreements with workers of any level on or after September 4, 2024 (“Effective Date”).[43] However, the Final Rule was barred from taking effect, and its future is uncertain.

Under the Final Rule, noncompetes in effect on the Effective Date are only enforceable against employees considered to be “Senior Executives”—that is, those in a “policy-making position” who meet or exceed a minimum compensation requirement.[44] If an employee does not qualify as a Senior Executive, existing noncompetes are no longer enforceable. The Final Rule imposes strict time limits for companies to notify non–Senior Executives of that change.

While the Final Rule is a broad prohibition, there are several limitations and exceptions. First, it only applies to noncompetition provisions in employment contracts; it does not apply to noncompetes entered into in connection with the bona fide sale of a business or a franchise. Second, it does not prohibit causes of action for breaches of a noncompete that occurred prior to the Effective Date. Finally, enforcement of a noncompete does not violate the Final Rule if the company has a good-faith basis to believe that the Final Rule does not apply to that situation.

The Final Rule did not go into effect on September 4, 2024, as expected. On August 20, 2024, Judge Ada Brown of the U.S. District Court for the Northern District of Texas issued a permanent injunction setting aside the Final Rule and declaring that it “shall not be enforced or otherwise take effect on September 4, 2024, or thereafter.”[45] Litigation regarding enforceability of the Final Rule is ongoing. Therefore, it remains possible that the Final Rule, or some modified version thereof, may still become law.

In sum, while Delaware is a contractarian state that defers to people’s right to privately order their affairs, that deference is tempered when a contract restricts a person’s ability to work. Noncompete agreements (unlike forfeiture for competition provisions) are judged by a “reasonableness” standard. Reasonableness, however, does not lend itself to a bright-line test, but requires analysis of several interrelated considerations—the agreement’s geographic scope and duration, the existence of a legitimate economic interest, and a balancing of the equities. While no one factor is determinative, Delaware courts have issued some guideposts (discussed above) and made it clear the concept is so important that parties cannot contract around the inquiry and that courts are hesitant to change an otherwise unenforceable contract. The time may come that the FTC’s final rule goes into effect and companies are prohibited from entering into noncompetes altogether. However, until then business leaders and legal practitioners must ensure that noncompetes are “reasonable” if they are to be enforced under Delaware law.

Labyrinth, Inc. v. Ulrich, 2024 Del. Ch. LEXIS 78, at *52 (Del. Ch. Jan. 26, 2024). ↑

TriState Courier & Carriage, Inc. v. Berryman, 2004 Del. Ch. LEXIS 43, at *41 (Del. Ch. Apr. 15, 2004). ↑

Weichert Co. of Pa. v. Young, 2007 Del. Ch. LEXIS 170, at *12 (Del. Ch. Dec. 7, 2007). ↑

See, e.g., id. (twenty-five miles from the company’s main operations); TriState Courier & Carriage, 2004 Del. Ch. LEXIS 43, at *43 (anywhere the company operated or has operated for the previous three years); All Pro Maids, Inc. v. Layton, 2004 Del. Ch. LEXIS 116, at *17–18 (Del. Ch. Aug. 9, 2004) (limited to the specific zip codes where the majority of the company’s clients are located); Kan-Di-Ki, LLC v. Suer, 2015 Del. Ch. LEXIS 191, at *69 (Del Ch. July 22, 2015) (the twenty-three states the company operated in); COPI of Del., Inc. v. Kelly, 1996 Del. Ch. LEXIS 136, at *12 (Del. Ch. Oct. 25, 1996) (within twenty miles of the company’s operations). ↑

See, e.g., Fortiline, Inc. v. McCall, 2024 Del. Ch. LEXIS 317, at *9–10 (Del. Ch. Sept. 5, 2024) (finding a noncompete unreasonable because it applied at least nationwide); Hub Grp., Inc. v. Knoll, 2024 Del. Ch. LEXIS 250, at *23 (Del. Ch. July 18, 2024) (finding a noncompete unreasonable because it applied to the contiguous United States and potentially Canada, Mexico, and India, including geographic locations that the employee had no responsibility for); Labyrinth, Inc. v. Ulrich, 2024 Del. Ch. LEXIS 78, at *52 (Del. Ch. Jan. 26, 2024) (a noncompete was overbroad because it spanned the areas in which both the company and its affiliates operated); Sunder Energy, 305 A.3d at 754–56 (rejecting a noncompete that applied to forty-six states when the employee only operated in Texas); Centurion Serv. Grp., LLC v. Wilensky, 2023 Del. Ch. LEXIS 354, at *8–10 (Del. Ch. Aug. 31, 2023) (finding a noncompete was unreasonable because it applied to any “area” in the United States or abroad in which the company was operating or was planning to operate); Intertek Testing Servs. NA, Inc. v. Eastman, 2023 Del. Ch. LEXIS 66, at *8 (Del. Ch. Mar. 16, 2023) (a restrictive covenant applying anywhere in the world was overbroad because the company operated primarily in Texas); Kodiak Bldg. Partners, LLC v. Adams, 2022 Del. Ch. LEXIS 288, at *18–20 (Del. Ch. Oct. 6, 2022) (rejecting a noncompete that included the states of Idaho and Washington and anywhere within one hundred miles of any other location served by the company or its affiliates); FP UC Holdings, LLC v. Hamilton, 2020 Del. Ch. LEXIS 110, at *15–17 (Del. Ch. Mar. 27, 2020) (rejecting a provision applying anywhere in the United States the company operates or may operate). ↑

See, e.g., Centurion Serv. Grp., 2023 Del. Ch. LEXIS 354, at *10 (“[T]his Court has enforced non-competes with a nationwide scope, but only in instances where the competing party agrees, in connection with the sale of a business, to stand down from competing in the relevant industry anywhere for a stated period of time after the sale.”); see also Brace Indus. Contracting, Inc. v. Peterson Enters., Inc., 2015 Del. Ch. LEXIS 229, at *7 (Del. Ch. Aug. 28, 2015) (a restriction covering the entire United States and Canada was appropriate in connection with the sale of a business because the entity that was sold did business worldwide); O’Leary v. Telecom Res. Serv., LLC, 2011 Del. Super. LEXIS 36, at *1 (Del. Super. Jan. 14, 2011) (upholding a nationwide restrictive covenant entered into in connection with the sale of a business because the business operated across the nation). ↑

See Del. Express Shuttle v. Older, 2002 Del. Ch. LEXIS 124, at *45 (Del. Ch. Oct. 23, 2002). ↑

See, e.g., id. at *41–51 (enforcing a three-year noncompete that lacked a geographical restriction because it was expressly negotiated by the parties immediately before it went into effect and the restricted territory was implicitly limited to places the company could and did serve from its Newark, Delaware, facility); Rsch. & Trading Corp. v. Pfuhl, 1992 Del. Ch. LEXIS 234, at *12 (Del. Ch. Nov. 18, 1992) (enforcing a one-year noncompete that lacked a geographical limitation because the company enjoyed widespread goodwill and the relief sought was narrow in scope). ↑

See, e.g., Weichert Co. of Pa. v. Young, 2007 Del. Ch. LEXIS 170 (Del. Ch. Dec. 7, 2007); All Pro Maids, Inc. v. Layton, 2004 Del. Ch. LEXIS 116 (Del. Ch. Aug. 9, 2004); TriState Courier & Carriage, Inc. v. Berryman, 2004 Del. Ch. LEXIS 43 (Del. Ch. Apr. 15, 2004); Del. Express Shuttle, 2002 Del. Ch. LEXIS 124; COPI of Del., Inc. v. Kelly, 1996 Del. Ch. LEXIS 136 (Del. Ch. Oct. 25, 1996). ↑

See RHIS, Inc. v. Boyce, 2001 Del. Ch. LEXIS 118, at *23–24 (Del. Ch. Sept. 26, 2001) (upholding a one-year restriction); Rsch. & Trading Corp., 1992 Del. Ch. LEXIS 234, at *31 (upholding a one-year restriction); Faw, Casson & Co. v. Cranston, 375 A.2d 463, 469 (Del. Ch. 1977) (a three year noncompete was reasonable but only to the extent it applied in northern Delaware). But see Fortiline, Inc. v. McCall, 2024 Del. Ch. LEXIS 317, at *2, *10 (Del. Ch. Sept. 5, 2024) (holding that a one-year noncompete was overbroad); Del. Express Shuttle, 2002 Del. Ch. LEXIS 124, at *54 (a three-year noncompete was unreasonable). ↑

Ainslie v. Cantor Fitzgerald, Ltd. P’ship, 2023 Del. Ch. LEXIS 22, *41 (Del. Ch. June 4, 2023), rev’d on other grounds, Cantor Fitzgerald, Ltd. P’ship v. Ainslie, 312 A.3d 674 (Del. 2024). ↑

See, e.g., Kan-Di-Ki, LLC v. Suer, 2015 Del. Ch. LEXIS 191 (Del Ch. July 22, 2015) (upholding a five-year noncompete covering twenty-three states entered into in connection with the sale of the company); O’Leary v. Telecom Res. Serv., LLC, 2011 Del. Super LEXIS 36 (Del. Super. Jan. 14, 2011) (upholding a four-year noncompete covering the entire United States entered into in connection with the sale of the company); Hough Assocs. v. Hill, 2007 Del. Ch. LEXIS 5 (Del. Ch. Jan. 17, 2007) (upholding a noncompete in a stock purchase agreement that applied for five years following the date of the agreement or three years after the employee left the company, with a geographic scope of fifty miles). But see Labyrinth, Inc. v. Ulrich, 2024 Del. Ch. LEXIS 78 (Del. Ch. Jan. 26, 2024) (rejecting a ten-year noncompete contained in a stock purchase agreement). ↑

See Elite Cleaning Co. v. Capel, 2006 Del. Ch. LEXIS 1105, at *26–27 (Del. Ch. June 2, 2006). ↑

Hub Grp., Inc. v. Knoll, 2024 Del. Ch. LEXIS 250, at *25 (Del. Ch. July 18, 2024); Del. Express Shuttle, 2002 Del. Ch. LEXIS 124, at *48–50; Norton Petroleum Corp. v. Cameron, 1998 Del. Ch. LEXIS 32, at *12 (Del. Ch. Mar. 5, 1998). ↑

See, e.g., Gener8, LLC v. Castanon, 2023 Del. Ch. LEXIS 380 (Del. Ch. Sept. 29, 2023); Lyons Inc. Agency Inc. v. Wilson, 2018 Del. Ch. LEXIS 317, at *15 (Del. Ch. Sept. 28, 2018); Kan-Di-Ki, 2015 Del. Ch. LEXIS 191; TriState Courier & Carriage, Inc. v. Berryman, 2004 Del. Ch. LEXIS 43,*43 (Del. Ch. Apr. 15, 2004); All Pro Maids, Inc. v. Layton, 2004 Del. Ch. LEXIS 116 (Del. Ch. Aug. 9, 2004); COPI of Del., Inc. v. Kelly, 1996 Del. Ch. LEXIS 136 (Del. Ch. Oct. 25, 1996); Faw, Casson & Co., 375 A.2d at 468–69. ↑

Fortiline, Inc. v. McCall, 2024 Del. Ch. LEXIS 317, at *7 (Del. Ch. Sept. 5, 2024); see alsoLabyrinth, 2024 Del. Ch. LEXIS 78, at *53–54; Sunder Energy, LLC v. Jackson, 305 A.3d 723, 753 (Del. Ch. 2023); Centurion Serv. Grp., LLC v. Wilensky, 2023 Del. Ch. LEXIS 354, at *8–10 (Del. Ch. Aug. 31, 2023); Frontline Techs. Parent, LLC v. Murphy, 2023 Del. Ch. LEXIS 336 (Del. Ch. Aug. 23, 2023); Kodiak Bldg. Partners, LLC v. Adams, 2022 Del. Ch. LEXIS 288, at *18–19 (Del. Ch. Oct. 6, 2022) (rejecting a provision applying to the business of the company and its affiliates). ↑

See Fortiline, 2024 Del. Ch. LEXIS 317, at *6; Rsch. & Trading Corp. v. Pfuhl, 1992 Del. Ch. LEXIS 234, at *12 (Del. Ch. Nov. 18, 1992).↑

RHIS, Inc. v. Boyce, 2001 Del. Ch. LEXIS 118, at *20–21 (Del. Ch. Sept. 26, 2001). ↑

Elite Cleaning Co. v. Capel, 2006 Del. Ch LEXIS 105, at *23–24 (Del. Ch. June 2, 2006). ↑

Hub Grp., Inc. v. Knoll, 2024 Del. Ch. LEXIS 250, at *30 (Del. Ch. July 18, 2024); Centurion Serv. Grp., 2023 Del. Ch. LEXIS 354, at *10–11. ↑

Sunder Energy, LLC v. Jackson, 305 A.3d 723, 757–58 (Del. Ch. 2023) (finding a provision was unenforceable because, among other things, it barred the employee from participating in any business that sells to any homeowner in any states where Sunder did business . . . [meaning the employee] could not take a job at a Best Buy . . . or a McDonalds”); Centurion Serv. Grp., 2023 Del. Ch. LEXIS 354 (criticizing the impact of the provision on the employee’s ability to work). ↑

See, e.g., Labyrinth, Inc. v. Ulrich, 2024 Del. Ch. LEXIS 78, at *52 (Del. Ch. Jan. 26, 2024); Sunder Energy, 305 A.3d at 753. ↑

See, e.g., Del. Express Shuttle, Inc. v. Older, 2002 Del. Ch. LEXIS 124 (Del. Ch. Oct. 23, 2002) (adjusting the duration of a noncompete from three years to two years); Faw, Casson & Co. v. Cranston, 375 A.2d 463, 468–69 (Del. Ch. 1977) (revising the geographic reach of a noncompete). ↑

See e.g., Ainslie v. Cantor Fitzgerald, L.P., 2023 Del. Ch. LEXIS 22, at *36, rev’d on other grounds, Cantor Fitzgerald, Ltd. P’ship v. Ainslie, 312 A.3d 674 (Del. 2024) (“[T]he fact Plaintiffs signed an agreement stipulating to its own reasonableness does not insulate that agreement from a reasonableness review under Delaware law.”); Kodiak Bldg. Partners, LLC v. Adams, 2022 Del. Ch. LEXIS 288, at *8 (Del. Ch. Oct. 6, 2022) (“[L]anguage stating its restrictive covenants are reasonable, and waiving a defense that they are not, does not preclude this Court from performing the reasonableness analysis our law mandates.”). ↑

Del. Code tit. 6, § 2707 (2024); see alsoDel. Code tit. 6, § 4914 (prohibiting the use of noncompetes in motor vehicle franchise agreements); Del. Code tit. 24, § 4109 (2023) (prohibiting a requirement that a home inspector trainee be required to execute a noncompete with a supervising inspector). ↑

See, e.g., Ala. Code § 8-1-190(a) (2015); Cal. Bus. & Prof. Code §§ 16600 et seq. (2024); and Neb. Rev. Stat. § 59-1603 (2024). ↑

Following the regional bank crisis in March of 2023,[1] many businesses started to review their treasury-management procedures for cash deposits out of safety concerns in the event of an insolvency of their depository bank. The reviews brought new attention to deposit programs designed to maximize access to insurance coverage provided by the Federal Deposit Insurance Corporation (“FDIC”) for deposits larger than the current $250,000 standard maximum deposit insurance limit per account at a depository bank. This article focuses on the IntraFi Cash Service of IntraFi LLC (“IntraFi”) as an example of such a program. The article will respond to frequently asked questions about how the IntraFi program works and how the depositors and their lenders are protected in the program.

How Does the IntraFi Program Work?

When placing funds on behalf of a customer through the IntraFi program, the customer’s relationship institution, which may be a bank, broker-dealer, or other eligible financial institution (“Relationship Institution”), and the customer enter into a deposit placement agreement (“DPA”) and a custodial agreement with the Relationship Institution as the custodian. The DPA states that the Relationship Institution will act as the customer’s agent in placing deposits. The custodial agreement further authorizes the Relationship Institution to maintain a custodial account[2] for the customer for the purpose of crediting the deposits placed through the program.

The Relationship Institution, in turn, will have entered into a Participating Institution Agreement with IntraFi and a sub-custody agreement (“Sub-Custody Agreement”) with a large money-center bank as a sub-custodian (“Sub-Custodian”) for the IntraFi program. The funds the Relationship Institution places for the customer are then, as described below, deposited with various FDIC-insured deposit-taking financial institutions (“Destination Institutions”) that enter into Participating Institution Agreements with IntraFi and are eligible to receive funds through the IntraFi program.

The placements are in amounts and pursuant to arrangements that make the funds eligible for deposit insurance provided by the FDIC ($250,000 per owner, per Destination Institution for each account ownership category). Specifically, the benefits of that insurance for the deposits at the Destination Institutions may be passed on to the customer under the “pass-through” rules established by the FDIC, which enable funds deposited by a custodian on behalf of the customer to be insured as if the customer had made the deposit with the Destination Institution itself.[3] Notably, customers can instruct the Relationship Institution not to deposit funds with certain Destination Institutions where the customer already maintains accounts, so as not to exceed coverage limits at that insured bank. The IntraFi program allows depositors to access millions in aggregate FDIC insurance across network banks.

The Sub-Custodian acts under the Sub-Custody Agreement as an intermediary to have the funds deposited with the Destination Institutions. The funds are then placed into deposit accounts at each Destination Institution, with the deposit accounts being in the name of the Sub-Custodian at the Destination Institution.

The Relationship Institution, the Destination Institutions, and the Sub-Custodian maintain appropriate books and records. These books and records, when considered together, reflect that the customer is the ultimate beneficiary of the funds placed in a deposit account at the relevant Destination Institution. Each deposit is recorded (a) on the records of the Destination Institution, in the name of the Sub-Custodian as the Relationship Institution’s sub-custodian; (b) on the records of the Sub-Custodian, in the Relationship Institution’s name as the customer’s custodian (showing that the Sub-Custodian is holding any claims with respect to the funds against the Destination Institution for the benefit of the Relationship Institution); and (c) on the records of the Relationship Institution, in the customer’s name (showing that the Relationship Institution is holding its claims with respect to the funds against the Sub-Custodian for the benefit of the customer).

In addition, under the DPA, the Relationship Institution agrees with the customer that it is acting as a “securities intermediary” under Article 8 of the UCC with respect to the custodial account established for the customer and that it will treat as “financial assets” under Article 8 of the UCC all of the Relationship Institution’s rights against the Sub-Custodian with respect to the deposit accounts placed by the Sub-Custodian. Financial asset means, among other things, “any property that is held by a securities intermediary for another person in a securities account if the securities intermediary has expressly agreed with the other person that the property is to be treated as a financial asset under [Article 8].”[4] The custodial account is a “securities account” under the UCC. Once the rights to payment with respect to the deposit accounts are financial assets credited to the custodial account, the customer acquires a security entitlement to them, which is a combination of contractual rights against the Relationship Institution, as securities intermediary, and a property interest in the financial assets. The customer’s rights include obtaining payments and distributions on the financial assets, exercising rights with respect to those financial assets, changing the form of holding of those financial assets, and causing the Relationship Institution to comply with entitlement orders to transfer or redeem those financial assets.[5]

How Is the Customer Protected in the Event of Insolvency of the Relationship Institution?

As noted above, the claims against the Sub-Custodian are credited to the customer’s account and treated as financial assets, giving the customer security entitlements against the Relationship Institution. Under Article 8, financial assets so credited, with exceptions not relevant here, are not property of the Relationship Institution and are not subject to the claims of the Relationship Institution’s creditors. As a result, the financial assets—the claims of the Relationship Institution against the Sub-Custodian—would not be included in the insolvency estate of the Relationship Institution. Practically, in most cases when a Relationship Institution has failed, its deposits and the custodial account have been assumed by another Relationship Institution, and business has continued as usual.

How Is the Customer Protected in the Event of Insolvency of the Sub-Custodian?

Similarly, under the Sub-Custody Agreement, the parties agree that the Sub-Custodian is acting as a securities intermediary and that the claims of the Sub-Custodian against the Destination Institutions are treated as financial assets under Article 8. Accordingly, such claims against the Destination Institutions are treated as security entitlements of the Relationship Institution against the Sub-Custodian. As with the Relationship Institution, financial assets, with exceptions not relevant here, are not property of the Sub-Custodian, are not subject to the claims of the Sub-Custodian’s creditors, and would not be included in the insolvency estate of the Sub-Custodian.

How Is the Customer Protected against the Exercise of Setoff by the Sub-Custodian in Case the Sub-Custodian Has an Unrelated Claim against the Relationship Institution?

The only contractual right of setoff that the Sub-Custodian has under the Sub-Custody Agreement against the Relationship Institution is for certain limited charges due to the Sub-Custodian as compensation in the Sub-Custody Agreement.

The Sub-Custodian would likely not have a noncontractual common-law right of setoff against the funds placed with it under the IntraFi program for amounts owed to the Sub-Custodian unrelated to the IntraFi program. Under the common law of most states, noncontractual common-law setoff is permitted only when the debts owed are “mutual.”[6] Mutuality requires that both parties be acting in the same capacity. Under the Sub-Custody Agreement, though, the Sub-Custodian is acting as a securities intermediary under Article 8 for the ultimate benefit of customers of the Relationship Institution. The Sub-Custodian would likely be acting in a different capacity as a creditor of the Relationship Institution for amounts owed unrelated to the IntraFi program. (The analysis would be similar if the Destination Institution were to consider exercising a setoff right for unrelated claims against the Sub-Custodian.)

How Does a Lender to the Customer Obtain a Perfected Security Interest in the Customer’s Rights to Payment under the IntraFi Program with the Desired Priority?

The lender’s security agreement needs to reasonably identify the collateral. The collateral description in a security agreement may refer to security entitlements or investment property, which is the generic UCC Article 9 category into which security entitlements fall. Alternatively, the collateral description could be even more specific while using one of those terms, such as “all of the debtor’s right, title, or interest in security entitlements to financial assets consisting of rights to payment under the IntraFi program maintained by [the Relationship Institution] for the benefit of the debtor, and the proceeds thereof.”

The security interest may be perfected by the lender filing in the appropriate UCC filing office a properly completed UCC financing statement against the customer and indicating as the collateral the security entitlement or investment property or a more specific description of the security entitlement or investment property using those terms, and the proceeds thereof.

The security interest granted by the customer may also be perfected by the Relationship Institution obtaining “control” of the security entitlements. If the lender is also the Relationship Institution, the lender obtains control automatically because the Relationship Institution is the customer’s securities intermediary. If the lender is not the Relationship Institution, the lender should enter into a securities account control agreement with the Relationship Institution and the customer, which will require the Relationship Institution to follow, without further consent of the customer, the entitlement orders of the lender, rather than the customer, under certain circumstances. If the lender perfects the security interest by control, there is no need for the lender to file a financing statement against the customer to perfect the lender’s security interest in the customer’s rights to payment under the IntraFi program.

Perfection of the lender’s security interest by control is the preferable method of perfection for the lender.[7] A security interest in a security entitlement or investment property perfected by control will have priority over a security interest in the same collateral perfected by the filing of a financing statement. This is the case even if the perfection of the security interest by control occurred after the filing of the financing statement and even if the secured party perfected by control knew of the financing statement filing.

Additional Considerations

Notably, the DPA provides that the customer has the right to dismiss the Relationship Institution as custodian and request that any of the funds placed for the benefit of the customer with a Destination Institution be retitled by the Destination Institution in the name of the customer directly. This process has the effect of unwinding the securities account held by the Relationship Institution and the Relationship Institution ceasing its role as a securities intermediary with respect to the funds.

If the customer exercises this right and the funds are so retitled, (a) there would no longer be a security entitlement with respect to the customer’s right to payment of the funds, and (b) the Relationship Institution’s security interest with respect to the right to the funds would no longer be perfected by control or may not be entitled to the priority afforded by control. The Relationship Institution may then need to take any additional steps necessary to preserve the perfection and priority of the security interest. As a result, a Relationship Institution that is also a lender may wish to include a provision in its credit documents providing that the customer shall postpone the exercise of its rights under the DPA while any obligations under the credit documents are outstanding or while the Relationship Institution has any obligation to extend credit under the credit documents. A third-party lender will want to address this issue in its account control agreement with the customer and the Relationship Institution.

Concluding Comments

This article provides only a brief summary of the IntraFi program and does so as an example of similar programs. It does not respond to all questions that may arise under these types of FDIC insurance maximization programs and is not a substitute for a careful review of the documentation for each program.

The custodial account will be a securities account for purposes of Article 8 of the Uniform Commercial Code (“UCC”), which is an account to which securities or other financial assets may be credited. The crediting of the deposit to the custodial account does not in and of itself render the deposit a security for purposes of federal securities laws. ↑

This article is Part IV in the Many Splendors of Fraud Claims series by Glenn D. West, which explores recent cases that affect drafting practices for avoiding fraud claims in private company M&A.

In Delaware, as in most states,

any person or entity that is alleged to have knowingly participated in the making of a fraudulent misrepresentation can be liable for that misrepresentation to the same extent as the person or entity that actually makes the misrepresentation; and the persons or entities potentially liable can include affiliates of the entity making the representation, as well as the human officers and owners of that entity or its affiliates, to the extent they knowingly cause or permit that entity to make a fraudulent misrepresentation.[1]

This concept applies to both intra-contractual and extra-contractual fraud claims.

Importantly, however, ABRY PartnersV, L.P. v. F & W Acquisition LLC[2] and its progeny permit (1) extra-contractual fraud to be taken off the table for both parties and nonparties to an agreement, through a properly worded disclaimer-of-reliance provision (to which the nonparties are made third-party beneficiaries); (2) liability for intra-contractual fraud to be limited to deliberate or knowing falsehoods stated in the express representations and warranties contained in the written agreement only, through an exclusive remedy provision (to which the nonparties are made third-party beneficiaries); and (3) the elimination of liability, through an exclusive remedy and nonrecourse provision, for parties and nonparties from “reckless, grossly negligent, negligent, or innocent misrepresentations of fact”[3] in a purchase agreement (all of which are potential states of mind supporting tort-based claims, including, potentially, common-law or equitable fraud).

What no contractual provision can accomplish, however, whether it is an exclusive remedy provision or a nonrecourse provision, is the elimination of liability of either a party or a nonparty for knowingly making or causing another person to make a deliberately false statement in a purchase agreement. I have written about this several times,[4] but it appears that deal lawyers continue to negotiate fraud definitions and nonrecourse provisions as if nonparties could avoid liability for deliberate and knowing participation in the conveyance of falsehoods in the express representations in a purchase agreement.

Matrix Parent: Deficient Fraud Definition

Fraud is frequently defined with the aim of purportedly limiting liability for fraud to only the party that is actually making the representations and warranties in the purchase agreement. An example of this approach is the following definition of Fraud from the recent Delaware Superior Court decision Matrix Parent, Inc. v. Audax Management Company, LLC:[5]

[“Fraud” means] intentional and knowing common law fraud under Delaware law in the representations and warranties set forth in this Agreement, any Contribution Agreement and the certificates delivered pursuant to Section 2.02(f)(i) and Section 2.03(d)(i). A claim for Fraud may only be made against the Party committing such Fraud. “Fraud” does not include equitable fraud, constructive fraud, promissory fraud, unfair dealings fraud, unjust enrichment, or any torts (including fraud) or other claim based on negligence or recklessness (including based on constructive knowledge or negligent misrepresentation) or any other equitable claim.[6]

But as noted by Aveanna Healthcare, LLC v. Epic/Freedom, LLC,[7] one of ABRY Partners’ many progeny, “if a seller ‘knew that the company’s contractual representations were false,’ the seller cannot ‘insulate’ itself from contractual fraud by hiding behind the company’s representations.”[8] In other words, it does not matter who technically made the representations—it matters who participated in their making or in causing them to be made.

And just as nonparties cannot hide behind the party that technically made the contractual representations, you cannot use a nonrecourse provision to exonerate nonparties from their participation in the conveyance of intentional lies in a written purchase agreement either. Nonrecourse provisions are not permitted to go so far—any attempt to do so is famously considered “too much dynamite.”[9]

Matrix Parent not only rejected the effort of defendants to limit Fraud, as it was defined, to just the parties to the purchase agreement, but also rejected the reliance upon a very broadly worded nonrecourse clause to exonerate nonparties who were alleged to have knowingly participated in intentional intra-contractual fraud. The court further rejected a very explicit provision that actually had the parties waiving “any claim against any Non-Recourse Party for conspiracy, aiding or abetting or other theory of liability.”[10] According to the court, “under Delaware law, the terms of a fraudulently procured contract [even though limited to claims based ‘solely on the falsity of express contractual representations’] cannot exempt from liability entities that were knowingly complicit in the fraud, including entities that aided, abetted, or conspired to commit such fraud.”[11] And, similar to the holding in Online Healthnow, Inc. v. CIP OCL Investments, LLC,[12] “[b]ecause Plaintiff has well pled that [a non-recourse party] did, in fact, know of and facilitate the fraudulent misrepresentations in the SPA . . . [the non-recourse party] cannot invoke the non-recourse provision to avoid liability under ABRY Partners and its progeny.”[13]

Crafting an Agreement with the Matrix Parent Decision in Mind

So, knowing this, you can easily agree as a seller to carve out intentional inter-contractual fraud from the nonrecourse clause, and define Fraud by reference to “Persons” rather than “Parties.”

The July 15, 2024, Merger Agreement governing Perdoceo Education Corporation’s $135 million acquisition of University of St. Augustine for Health Sciences, LLC, contains an example of a Fraud definition that appears to understand that you cannot limit intentional intra-contractual common-law fraud to just the party actually making those representations:

“Fraud” means actual and intentional common law fraud under Delaware law with respect to the representations and warranties set forth in this Agreement (including Article V or Article VI), any of the Related Documents, or any certificate delivered pursuant to this Agreement or any of the Related Documents. For the avoidance of doubt, (a) the term “Fraud” does not include any claim for equitable fraud, promissory fraud, or unfair dealings fraud, or any claim for fraud or misrepresentation based on negligence or recklessness and (b) only a Person who had actual knowledge of or knowingly and intentionally participated in such Fraud shall be responsible for such Fraud and only to a Person who actually relied on such representations and warranties and was actually damaged or harmed by such Fraud.[14]

Keep in mind that clause (b) does not actually do anything that the law of Delaware doesn’t already do, but sometimes saying it out loud helps the other side—and it’s sleeves off the seller’s vest to acknowledge that nonparties can be liable for the knowing participation in the conveyance of falsehoods in the express representations and warranties set forth in an acquisition agreement.

Section 5 of the Securities Act of 1933 (“Securities Act”) prohibits the offer or sale of unregistered securities, absent an exemption. However, Section 4(a)(1) of the Securities Act explicitly states that the prohibition in Section 5 only applies to transactions by an issuer, underwriter, or dealer.[1]

The Securities and Exchange Commission (“SEC”) has been relatively undaunted by that limitation. Through a long series of SEC enforcement actions, appellate courts have expanded the plain language of Section 4(a)(1) by developing the “necessary participant” doctrine, widening the scope of the “issuer, underwriter, or dealer” language to hold defendants liable when they have been a “necessary participant” in the offer and sale of alleged unregistered securities. In an SEC enforcement action dating back to 1941, SEC v. Chinese Consolidated Benevolent Ass’n, the U.S. Court of Appeals for the Second Circuit found that a person not directly engaged in transferring title of the security nevertheless can be held liable under Section 5 if that person “engaged in steps necessary to the distribution of [unregistered] security issues.”[2] The Second Circuit’s interpretation is judge-made law that departs from the plain language of the statute.

This article explores the advent and evolution of the “necessary participant” doctrine and discusses some of the dangers of expanding the plain language of Section 4(a)(1).

Section 4(a)(1): The “Ordinary Trading” Exemption

Section 5 of the Securities Act makes it unlawful, directly or indirectly, to publicly offer or sell unregistered securities, unless the offering is covered by an exemption.[3] Several potential exemptions are available to market participants, depending upon the nature of the transaction, amount of the offering, and participants involved. One of those exemptions is codified under Section 4(a)(1),[4] sometimes known as the “ordinary trading” exemption, which states that Section 5 does not apply to transactions by any person other than an issuer, underwriter, or dealer.[5]

Underwriter is statutorily defined in Section 2(a)(11) of the Securities Act as

any person who has purchased from an issuer with a view to, or offers or sells for an issuer in connection with, the distribution of any security, or participates or has a direct or indirect participation in any such undertaking, or participates or has a participation in the direct or indirect underwriting of any such undertaking.[6]

For example, an investment bank that has an arrangement with a securities issuer to facilitate the public sale of its securities is typically considered an “underwriter.”

On its face, Section 2(a)(11) defines underwriter broadly enough such that, theoretically, it could be construed to encompass persons other than the traditional investment bank that underwrites a registered securities offering. However, “while the definition is indeed broad, ‘[u]nderwriter’ is not . . . a term of unlimited applicability that includes anyone associated with a given transaction.”[7] Courts have found that “[i]t is crucial to the definition of ‘underwriter’ that any underwriter must participate in the distribution of a security.”[8] This participation notion was expressly contemplated by Congress, which “ma[de] clear that a person merely furnishing an underwriter money to enable him to enter into an underwriting agreement is not an underwriter. . . . The test is one of participation in the underwriting undertaking rather than that of a mere interest in it.”[9] The rationale for subjecting underwriters to potential liability is “because they hold themselves out as professionals who are able to evaluate the financial condition of the issuer,” and “[t]he public relies on their expertise and reasonably expects that they have investigated the offering with which they are involved.”[10]

If a holder of securities is not an issuer, underwriter, or dealer, they may sell their existing securities without registration pursuant to Section 4(a)(1).[11] Section 4(a)(1) was “designed to exempt routine trading transactions with respect to securities already issued”—not necessarily to exempt initial distributions by issuers.[12] Importantly, Section 4(a)(1) exempts transactions, not persons.[13]

SEC v. Chinese Consolidated Benevolent Ass’n

In 1941, the Second Circuit seemingly expanded the statutory limitations of Section 4(a)(1), not only by construing the Section 2(a)(11) definition of underwriter broadly, but by holding that even if a defendant was not an issuer, dealer, or underwriter itself, the Section 4(a)(1) exemption would not apply if the defendant was engaged in “steps necessary” to the distribution of unregistered securities.

In Chinese Consolidated, the SEC sued a New York corporation to enjoin it from using any instruments of interstate commerce or of the mails in attempting or offering to sell or dispose of Chinese government bonds.[14] The defendant was a benevolent association with a membership of 25,000 Chinese individuals. Without any official or contractual relationship with the Chinese government, this New York corporation urged members of Chinese communities in New York, New Jersey, and Connecticut to purchase Chinese government bonds, and offered to accept funds from prospective purchasers and deliver those funds to the Bank of China in New York. Neither the defendant nor its members were ever charged for their activities, and they did not receive any compensation. The SEC sought to enjoin the defendant from disposing of, or attempting to dispose of, these Chinese government bonds, which it alleged were unregistered securities.

The defendant was concededly neither the issuer of the Chinese government bonds nor a dealer. Accordingly, under Section 4(a)(1) of the Securities Act, the defendant would be exempt from registration requirements if it was also not an underwriter, as defined in Section 2(a)(11). The district court indeed found that the defendant was not an underwriter and was therefore exempt because the defendant did not sell or solicit offers to buy the Chinese government bonds for an issuer, as the Section 2(a)(11) definition of underwriter specifies. The district court found that the defendant’s actions in attempting to dispose of the bonds were not for the Chinese government; indeed, there was no contractual arrangement or even understanding with the Chinese government.

The Second Circuit reversed, pointing to the facts that the “defendant solicited the orders, obtained the cash from the purchasers and caused both to be forwarded so as to procure the bonds.”[15] The court noted that “the aim of the Securities Act is to have information available for investors[,] [and] [t]his objective will be defeated if buying orders can be solicited which result in uninformed and improvident purchases.”[16] Ultimately, the court, noting the aim of the Securities Act to furnish the public with adequate information, and the purported aim of the issuer (here, the Chinese government) to promote the distribution of the securities, broadly interpreted the plain language of the definition of underwriter. The court held that “[a]ccordingly the words ‘(sell) for an issuer in connection with the distribution of any security’ ought to be read as covering continual solicitations.”[17] The court ultimately found that the defendant acted as an underwriter in the distribution of unregistered securities.[18]

Crucially, the court went on to find a “further reason” for holding that the defendant’s activity was prohibited.[19] The court noted that Section 4(a)(1) was not intended to exempt distributions by issuers, and that here,

[t]he complete transaction included not only solicitation by the defendant of offers to buy, but the offers themselves, the transmission of the offers and the purchase money through the banks to the Chinese government, the acceptance by that government of the offers and the delivery of the bonds to the purchaser or the defendant as his agent.[20]

The court held that “[e]ven if the defendant is not itself ‘an issuer, underwriter, or dealer’ it was participating in a transaction with an issuer, to wit, the Chinese Government.”[21] The court explained that the Section 4(a)(1) exemption does not “protect those who are engaged in steps necessary to the distribution of security issues.”[22]

In sum, the court found that the defendant’s actions fell under the definition of underwriter under Section 2(a)(11) such that the defendant was liable for its attempts to dispose of the Chinese government bonds without registration; and, significantly, that even if the defendant was not an underwriter, it “engaged in steps necessary to the distribution” of the unregistered securities such that it did not qualify for the Section 4(a)(1) exemption. Thus, the “necessary participant” doctrine was born, making it possible for a defendant to be liable under Section 2(a)(11) even if it is not an issuer, underwriter, or dealer.

The Second Circuit’s Expansion of Necessary Participant

Stemming from Chinese Consolidated in 1941, courts have adopted and expanded the necessary participant language from that case to create myriad other tests that purportedly help explain what a “necessary participant” is—and when a person who is not an issuer, underwriter, or dealer can nevertheless be liable under Section 5.[23]

Perhaps realizing that Chinese Consolidated was unmoored from the statute, the Second Circuit later tried to put the genie back in the bottle, but without actually overturning Chinese Consolidated. In SEC v. Kern, the Second Circuit cited the “steps necessary” language from Chinese Consolidated to hold that “underwriters . . . include any person who is ‘engaged in steps necessary to the distribution of security issues.’”[24] But later, in SEC v. Sourlis, with somewhat cursory analysis, the Second Circuit held that Section 5 liability extends to “those who have ‘engaged in steps necessary to the distribution of [unregistered] security issues’”—quoting and relying on Chinese Consolidated without even mentioning the word underwriter.[25]

District courts within the Second Circuit, springboarding from Chinese Consolidated’s departure from the statutory text, developed the “necessary participant” doctrine by introducing additional considerations beyond the plain language of Section 4(a)(1). Under these cases, defendants may be liable for violating Section 5 even if they do not offer or sell a security, provided that they were a “necessary participant” in the unregistered distribution.[26]

But then how is a court to determine who is a “necessary participant”? As one court frames it, “[t]he ‘necessary participant test . . . essentially asks whether, but for the defendant’s participation, the sale transaction would not have taken place.’”[27] This “but for” formulation significantly expands the range of whom the SEC can sue for Section 5 liability to include anyone or any entity that the SEC asserts had a necessary role in the unregistered securities transaction.

In other words, in an attempt to define limitations on what a “necessary participant” is, courts have articulated a “substantial factor” test—that is, “whether the defendants’ acts were a ‘substantial factor in the sales transaction.’”[28] However, the concept of a “substantial factor” in a securities transaction is as ill-defined as other terms within this discussion.[29]

And as the SEC v. Genovese court pointed out, the “but-for” test raises its own problems. It “would require finding innumerable necessary participants to every unregistered securities offering—everyone who played an intermediate role, no matter how small, in the chain of causation leading to the sale.”[30] Indeed, “[a] strict ‘but-for’ test also is at odds with the Commission’s guidance, which provides that not every individual in the causal chain is a necessary participant.”[31]

Ultimately, in Genovese, the court organized the defendant’s activities into two categories: (1) those showing “direct involvement” in the sale and (2) those “activities ancillary” to the sale.[32] Examples of direct involvement, which implicate substantial participation, include where defendants “directly prepared . . . corporate resolutions and documentation”;[33] “formed entities for use in sale, solicited investments, provided subscription agreements, communicated with buyers and sellers, and directed broker action”;[34] and “found private parties as clients for deals, filed paperwork with regulators, served as president, CEO and director of transfer agency and handled promotion of stock.”[35] In contrast, the Genovese court ultimately found that “activities ancillary” were “too remote from the actual sale to rise to the level of necessary or substantial participation”—creating yet another criterion for considering what “necessary participation” is.[36]

Thus, in the Second Circuit alone, the new category of “necessary participant” created by Chinese Consolidated—explicitly described as being separate from the definition of underwriter in Section 2(a)(11)—has spawned a slew of tests, some of which appear to be attempting to shoehorn the classification back into the underwriter definition, and some of which follow Chinese Consolidated more strictly (and thus follow the statute far more loosely).

Other Circuit Courts’ Interpretation of Necessary Participant

In the wake of Chinese Consolidated, other circuit courts, including the U.S. Courts of Appeals for the Seventh and Ninth Circuits, also adopted a new, atextual “necessary participant” doctrine, often tempered by the “substantial factor” doctrine, to hold that defendants need not be issuers, underwriters, or dealers to be held liable for a Section 5 violation.[37] These courts often recognize the risk that a party whose minimal acts assisted in the unregistered securities distribution could be held liable for registration violations, but they have found that, “in practice, the standards differ little, for no court using the ‘necessary participant’ test has found liable a defendant whose acts were not a substantial factor in the sales transaction.”[38]

In SEC v. Holschuh, the Seventh Circuit formulated the test differently, explicitly finding that persons who were not underwriters may nevertheless be liable on the grounds that the statute refers to the transactions by people, not the people themselves.[39]Holschuh found that the defendant “was a ‘necessary participant’ and ‘substantial factor’ in the unlawful sales transactions,” and thus liable even though not an underwriter.[40] Thus, other circuits have used this “substantial factor” test as well—sometimes articulated somewhat differently from the Second Circuit, but still addressing the concept of a “necessary participant” rather than strictly an issuer, underwriter, or dealer.

Back to the Second Circuit: In re Lehman Brothers

After the adoption of the “but-for” test and “substantial factor” test, which both provided gloss on the “necessary participant” doctrine, the Second Circuit provided further guidance in a 2011 case, In re Lehman Brothers Mortgage-Backed Securities Litigation.[41] There, investors brought putative class actions to hold credit ratings agencies liable under the Securities Act, in part as underwriters. The plaintiffs attempted to argue that Second Circuit precedent construed the term underwriter broadly to include any person who is “engaged in steps necessary to the distribution of security issues.”[42] According to the plaintiffs’ logic, “any persons playing an essential role in a public offering . . . may be liable as underwriters.”[43] The court disagreed, stating that its “prior cases do not hold that anyone taking steps that facilitate the eventual sale of a registered security fits the statutory definition of underwriter.”[44] Rather, the court “stated that ‘underwriter’ references those who take ‘steps necessary to the distribution’ of securities.”[45]

Further elaborating on Chinese Consolidated, Kern, and other Second Circuit progeny, the court clarified that “this precedent cannot be read to expand the definition of underwriter to those who participate only in non-distributional activities that may facilitate securities’ offering by others.”[46] Rather,

the participation must be in the statutorily enumerated distributional activities, not in non-distributional activities that may facilitate the eventual distribution by others. This approach avoids the implausible result of transforming every lawyer, accountant, and other professional whose work is theoretically “necessary” to bringing a security to market into an “underwriter” . . . , a dramatic outcome that Congress provided no sign of intending.[47]

In its elaboration, the court corrected a common misinterpretation of Chinese Consolidated, remarking that “we note that the ‘steps necessary to the distribution’ language relied on by plaintiffs was originally employed by this court [in Chinese Consolidated] to explain a registration exemption, not the underwriter definition.”[48] The court noted, “[W]e stated [in Chinese Consolidated] that ‘[i]t,’ meaning the [4(a)(1)] exemption, ‘does not . . . protect those who are engaged in steps necessary to the distribution of’ securities because it is limited to transactions between individual investors.”[49]

On the one hand, Lehman Brothers clarified that Chinese Consolidated first employed the “steps necessary” language to carve out “necessary participants” from the Section 4(a)(1) exemption. On the other, Lehman Brothers clarified that underwriter references those who take “steps necessary to the distribution” of securities, despite that language not existing in the Section 2(a)(11) statutory definition of underwriter. In doing so, Lehman Brothers reconfirmed the departure from the text first set out in Chinese Consolidated: under these cases, a “necessary participant” is not just a type of underwriter; it’s a new category entirely—one that does not exist in the text of the 1933 Securities Act.[50]

Where to, from Here?

The rationale of the Securities Act was to provide the public accurate and complete information by the people or entities responsible for distributing securities to the public.[51] Yet, despite Congress’s circumscribed application of registration requirements to issuers, dealers, and underwriters, the Second Circuit expanded the group responsible for registration requirements to include “necessary participants” to the distribution of securities, even if they are not underwriters.

That expansion, initiated in a few lines in Chinese Consolidated in 1941 and expounded on over a period of decades by multiple circuit and district courts, stretches the plain language of Section 4(a)(1). Not only can the Section 2(a)(11) definition of underwriter include those who indirectly participate in the distribution of securities (already, arguably, at the outer reaches of Section 2(a)(11)), but even those who are not underwriters may not fall under the Section 4(a)(1) exemption if they are “necessary participants” and take “steps necessary” to the distribution of unregistered securities.

Chinese Consolidated opened the door for a nebulous “necessary participant” to include myriad individuals or entities other than issuers, underwriters, or dealers in the chain of a securities distribution. The Ninth Circuit’s discussion in Murphy raised the concern that “this broader standard could encompass a party whose acts in furtherance of the distribution were de minimis and who should not be held liable for registration violations.”[52]

In the era of digital assets trading over complex and interconnected computer networks, it might be a struggle to draw the appropriate limiting principle on who could be deemed a “necessary participant,” and an expansive interpretation could apply to innumerable persons and entities. No longer are we only concerned with a single newspaper editorial, as Judge Swan pointed to in his Chinese Consolidated dissent, but courts will be asked to consider: Websites that host front ends? Participants in a blockchain network, such as validators, stakers, or decentralized exchanges? Noncustodial wallet providers? Blockchains themselves?

For many (and perhaps all) of these categories, it would make no sense to hold the persons or entities creating or operating these technologies responsible for issuances of unregistered securities—not from a policy point of view, and certainly not under the plain language of the Securities Act. Indeed, given the free-flowing and permissionless nature of the internet and Web 3.0, participants may not even be aware of the role they play in the distribution chain—perhaps they simply publish software on the internet that could be used to ultimately purchase an alleged unregistered security.

Eighty years of case law has developed to suggest that a “necessary participant” is its own category, apart from issuers, underwriters, and dealers. That alone is a departure from the plain text of the Securities Act. Worse, as explained above, district courts have struggled to interpret the “necessary participant” language from Chinese Consolidated to apply some limiting principle, such that underwriter is not too broadly construed to include any person who is engaged in “steps necessary” to the distribution of securities.

Without the “necessary participant” doctrine’s advent in Chinese Consolidated, district courts would merely have to interpret the plain language of Section 4(a)(1) that applies to issuers, underwriters, and dealers—and perhaps Section 2(a)(11)—to determine who would be considered an underwriter. While some of the same analytical tools might be useful, such tools would be used within the context of Section 2(a)(11) and the rest of the underwriter definition, which—in context—might serve to limit some of the more expansive interpretations of which parties may be liable.

Ultimately, the “necessary participant” doctrine as first stated in Chinese Consolidated would be unlikely to survive a strict textualist Supreme Court review. Chinese Consolidated created a new category for liability, even if a person was not an underwriter. A textualist review would likely limit Section 4(a)(1)’s application to its plain language of only issuers, dealers, or underwriters (as defined in Section 2(a)(11)), not issuers, dealers, underwriters, or those who have engaged in “steps necessary” to the distribution of securities, as in Chinese Consolidated.

Further, a textualist review, grounded in the remainder of Section 2(a)(11) (and taking into account the context of that language), would be narrower. For example, such a review would not eliminate the words “for an issuer” from the Section 2(a)(11) definition of underwriter, meaning that an entity with no contractual arrangement or understanding with the issuer likely would not be considered an underwriter. Deeming an individual or entity integral to distributing an alleged security, and thus liable under Section 5, simply because it provides information about or access to that security, despite no relationship or understanding with the issuer, is unmoored from the plain language of Section 5.

Unless the Supreme Court, other courts of appeal not bound by prior circuit law, or Congress weighs in and ends this eighty-year-long (and counting) detour away from the plain statutory language of the Securities Act, the definition of necessary participant, and the myriad considerations that influence what a “necessary participant” is, will remain unclear for individuals and entities operating in the securities industry and beyond.

15 U.S.C. § 77b(a)(11); see Fed. Deposit Ins. Corp. v. Credit Suisse First Bos. Mortg. Sec. Corp., 414 F. Supp. 3d 407, 413 (S.D.N.Y. 2019). ↑

In re Refco, Inc. Sec. Litig., No. 05-cv-8626, 2008 WL 3843343, at *4 (S.D.N.Y. Aug. 14, 2008) (citing Ackerberg v. Johnson, 892 F.2d 1328, 1335 (8th Cir. 1989)). ↑

McFarland v. Memorex Corp., 493 F. Supp. 631, 644 (N.D. Cal. 1980). ↑

Circuit Judge Swan dissented, pointing out that “the majority opinion has construed the statute more broadly than its language will permit.” Id. at 742. In his interpretation, including the defendant within the definition of an underwriter “gives no meaning to the words ‘for an issuer.’” Id. He pointed out that under the majority’s construction, “a single newspaper editorial, published without instigation by the Chinese Government and merely urging the purchase of the bonds in the name of patriotism, would make the newspaper an ‘underwriter,’” and that he “cannot believe the statute should be so interpreted.” Id.↑

See SEC v. N. Am. Rsch. & Dev. Corp., 424 F.2d 63, 82 (2d Cir. 1970) (noting that Chinese Consolidated “make[s] it clear that being an underwriter is not a prerequisite to a finding of violation of Section 5”); SEC v. Culpepper, 270 F.2d 241, 246 (2d Cir. 1959) (“In [Chinese Consolidated] we noted the underlying policy of the [Securities] Act, that of protecting the investing public through the disclosure of adequate information, would be seriously impaired if we held that a dealer must have conventional or contractual privity with the issuer in order to be an ‘underwriter.’”). ↑

425 F.3d 143, 152 (2d Cir. 2005) (citing Chinese Consolidated). Ironically, the citation of Chinese Consolidated’s “steps necessary” language to define underwriter in Kern “was arguably dictum because the transaction in that case unquestionably ‘involved underwriters,’ rendering [Section 4(a)(1)] inapplicable.” In re Lehman Brothers Mortg.-Backed Sec. Litig., 650 F.3d 167, n.7 (2d Cir. 2011). ↑

See SEC v. Mattera, No. 11-cv-8323, 2013 WL 6485949, at *10 (S.D.N.Y. Dec. 9, 2013) (holding that “necessary participants” in unregistered distributions may be liable under Section 5); SEC v. Sason, 433 F. Supp. 3d 496, 513 (S.D.N.Y. 2020). ↑

SEC v. Universal Express, Inc., 475 F. Supp. 2d 412, 422 (S.D.N.Y. 2007) (quoting SEC v. Murphy, 626 F.2d 633, 651–52 (9th Cir. 1980)). ↑

Id. (quoting Murphy, 626 F.2d at 651–52); see also SEC v. Genovese, No. 17-cv-5821, 2021 WL 1164654 (S.D.N.Y. Mar. 26, 2021) (noting that Sason and Mattera qualify the “necessary participant” test “with statements that the defendants’ acts must be a ‘substantial factor in the sales transactions’”). ↑

See SEC v. Elliott, No. 09-cv-7594, 2011 WL 3586454, at *7 (S.D.N.Y. Aug. 11, 2011) (“As for substantial participation, to be sure it is a concept without precise bounds. . . .”). ↑

Id. (quoting In re Owen v. Kane, Exchange Act Release No. 23827, 1986 WL 626043, at *3 (1986) (reinforcing that “not everyone in the chain of intermediaries between a seller of securities and the ultimate buyer is sufficiently involved in the process to make him responsible for an unlawful distribution”). ↑

See, e.g., SEC v. Murphy, 626 F.2d 633, 648 (9th Cir. 1980) (“Although we have rejected Murphy’s exemption argument because he need not be an issuer, underwriter or dealer to be held liable for a § 5 violation, we recognize that Murphy’s role in the transaction must be a significant one before liability will attach.”). ↑

Id.; see also SEC v. CMKM Diamonds, Inc., 729 F.3d 1248, 1255 (9th Cir. 2013) (“Prior to the issuance of a security, numerous persons perform mechanical acts without which there could be no sale. . . . [B]ut these acts nonetheless do not render the defendants sellers” because their “acts must also be a substantial factor in bringing about the transaction.”). ↑