During the COVID-19 pandemic, Initial Public Offerings (IPOs) and Special Purpose Acquisition Companies (SPACs) gained considerable popularity as ways to take a company public. During the multiple lockdowns, companies had lots of time to streamline their business plans and strategize to get them to the next level. As a result, many found 2020 to be the perfect time to take their company public via IPOs or SPACs to help respond to the uncertainty created by the world health crisis and raise funds for their business.

Although there was a slight SPAC slowdown in April 2021, numbers are settling out post-COVID going into the third quarter, and there are still lots of market opportunities for companies looking to show their growth and go public through IPOs and SPACs. Before opening up your business to a national exchange, it’s critical to understand how IPOs and SPACs evolved through COVID and what to expect post-pandemic.

IPOs and SPACs Post-Pandemic

The pandemic has seen its ups and downs for IPOs and SPACs, and in January 2021, issuances of SPACs, in particular, were once again on the rise. SPACs were so popular that by the end of March 2021, there were already 292 issuances, and they had raised $87.9 billion, which exceeded the $83.4 billion total raised in 2020. However, in April 2021, the Securities and Exchange Commission (SEC) announced it was considering new guidelines that would change the way SPACs report information on financial statements for investors. The rate of issuances dropped by almost 90% that month.

Thankfully, as we move into the third quarter of 2021, later in the pandemic, we see these numbers settling back to normal. For example, there was a rush at the end of the second quarter, with 13 SPACs pricing and going public in the last week of June alone. As of September 27, 2021, the total amount raised by SPAC issuances in 2021 so far was $127.1 billion according to the website SPAC Research. SPACs are transforming the entrepreneurial landscape of the world, and there are hundreds of SPACs from 2020 and 2021 still looking for targets as well as new market opportunities for companies to go public. Overall, COVID has had a stimulating effect on financial markets, since they have experienced breakneck growth over the past 15 months, with relatively few roadblocks or downturns and no signs of stopping post-pandemic.

When the SEC announced it was considering new restrictions on SPACs in early April 2021, many companies turned their attention back to the traditional IPO route. Going into the third quarter of 2021, IPOs alone in the U.S. had raised $79.9 billion in proceeds. This number is higher than every year in the past decade except for one, which means that 2021 is on track to go down as the most prolific year for IPOs on record. With the lockdowns over the past 18 or so months, bankers have been laser-focused and able to push as many deals through as possible, taking advantage of stock market highs. Furthermore, between institutional and retail investors, there is lots of money in the market right now, pushing many companies to go public earlier than they originally planned. With 761 offerings as of September 27, 2021, this year has already beaten 2020 in IPO frequency, surpassing its 480 IPOs, and had more than three times as many as 2019, which saw 232. As we look to the last two quarters of 2021, the trend of businesses taking advantage of IPOs to take their companies public is still on the rise.

Business as Usual

Although there will be some changes to the post-pandemic landscape, if you are looking to take your company public through IPOs or SPACs, now may be the perfect time, since the market of potential buyers has perhaps never been bigger. Not to mention, both SPACs and IPOs have proved their resiliency when faced with potential roadblocks such as the pandemic and the SEC statement on potential SPAC restrictions in April 2021. In fact, since April, the issuances of SPACs and IPOs continue to increase each quarter, and numbers are set to be record-breaking yet again in 2021.

This doesn’t mean there are no complications. Currently, one thing that adds a layer of complexity to due diligence efforts would be possible travel restrictions. In these cases, meetings or on-site visits would need to be done virtually, and in an international transaction, one would need to rely more heavily on local counsel. Of course, another thing to be aware of is that because of how hot the market is, the risks involved with IPOs and SPACs increase as well.

However, with so many buyers and so much money to be had within the market, the rewards outweigh the risks for most investors. Thus, the current IPO and SPAC landscape could be an ideal market for companies looking to go public. For many companies, it is no longer a question of if they should go public, but rather how and when.

Sophisticated clients’ expectations of their M&A deal attorneys have not slackened in the age of remote working and back-to-back Zoom meetings in the wake of the pandemic.

Given that reality, the recent publication of the latest edition of Using Legal Project Management in Merger and Acquisition and Joint Venture Transactions is particularly timely. This unique guidebook contains downloadable and customizable checklists and other tools providing an arsenal of resources for deal lawyers seeking to drive efficiency for and deliver value to their clients. The new edition adds to that arsenal and responds to new developments in the evolving M&A marketplace. It also breaks new ground with an entirely new battery of resources focused on joint venture transactions.

The new edition marks the third iteration of the guidebook to be published in just five years. Several factors have driven the number of editions in this short period.

First, there has been an explosion in the field of legal project management generally as law firms and corporate law departments alike have added legions of project and pricing managers to their ranks. The editors recently participated in a global summit of such managers, something that would have been unthinkable just a few years ago.

Second, corporate law departments and other sophisticated clients are issuing RFPs with increasing frequency that require bidding law firms to include meaningful explanations of how they would use legal project management (LPM) in carrying out their engagement.

Third, the COVID-19 pandemic catalyzed the need for the tools in the field. In a remote work world with lawyers working from various venues, having an organized and coordinated team can be a challenge, but at the same time remains a necessity. The LPM tools found in the guidebook can go a long way to helping distributed legal deal teams stay in sync.

Finally, the 100+ deal lawyers from around the world who comprise the American Bar Association’s M&A Legal Project Management Task Force kept coming up with new and creative ideas as to how LPM might be used in particular types of transactions to respond to new ways of handling deal risks and other matters. As editors of the guidebook, we owe them our thanks for their seasoned perspectives and invaluable input.

As a consequence, the Third Edition includes eight new M&A tools that are particularly relevant to the tumultuous and ever fast-moving world in which deal lawyers find themselves. The following are thumbnail descriptions of the eight new tools:

Cataclysmic Event Due Diligence Questionnaire: This is a list of due diligence and document requests triggered by or related to a cataclysmic or force majeure-like event, incident, occurrence or circumstance such as a pandemic, an Act of God, or anything else that is or has the potential to be, material, major and disruptive.

Limited Auction Checklist: This is a checklist of key items to consider in connection with a limited auction process. Such a process entails a higher degree of complexity than transactions with only one potential buyer, given the need to coordinate and stage the disclosure of information to various interested parties and handle parallel negotiations with multiple bidders.

Deal Cycle Capture Tool: This tool captures and communicate significant matters identified during the deal cycle, particularly during due diligence, where such matter requires later consideration or action, including in connection with the drafting of representations and warranties.

Section 363 Bankruptcy Sale Checklist: This is a checklist of important items to consider in connection with the sale of distressed company pursuant to Section 363 of the U.S. Bankruptcy Code.

M&A Escrow Agreement Checklist: This tool identifies issues to be considered in the negotiation of an escrow arrangement to satisfy a seller’s post-closing obligations, including purchase price adjustments and indemnification claims.

Representation and Warranty Insurance (“RWI”) Tool: This tool provides practical advice and guidance on securing and structuring representation and warranty insurance as a means to make a buyer whole for seller breaches. The tool helps you consider these key questions: What is covered? What is excluded from coverage? What is the process for putting RWI in place?

Post-Closing Reference Checklist: This tool consists of a client alert letter and accompanying list of important post-closing action items and deadlines, including items related to the bringing of indemnification claims.

Post-Acquisition Integration Checklist: While deal making is hard, integration is even harder. Oftentimes, the projected synergies and value to be realized from M&A are lost on integration. One leading contributing factor can be buyer’s failure to consider and plan how the acquired business is to be integrated into its own business after closing. This tool provides a list of questions and action items for a buyer to consider in developing and implementing a post-closing integration plan.

The Third Edition moves beyond M&A by adding four new tools developed by lawyers from around the globe who are members of the International Subcommittee of the M&A Committee of the Business Law Section. Joint ventures are complicated transactions involving sophisticated parties, and raise a number of issues in thorny areas including government, intellectual property, tax, employment law, and regulatory law. As such they are perfect candidates for LPM. The new joint venture tools leverage tools that were developed for M&A transactions, including a task checklist, a scoping tool, a drafting guide and a negotiating tool.

Now more than ever, the Guidebook serves as an indispensable tool not just for driving efficiency and client value, but also for training young lawyers and managing risk.

In a June 14, 2021, Settlement Order[1] (the “Order”), the Securities and Exchange Commission (“SEC”) alleged certain cybersecurity disclosure controls failures at First American Financial Corporation (“FAFC”).

Without admitting or denying the SEC’s findings, FAFC agreed to (1) cease and desist from further violations of SEC Exchange Act Rule 13a-15(a); and (2) pay a $487,616 penalty. Rule 13a-15(a) mandates that every issuer of a security registered pursuant to Section 12 of the Exchange Act must maintain disclosure controls and procedures to ensure that information the issuer must disclose in reports it files or submits pursuant to the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in the SEC’s rules and forms. FAFC provides products and services in connection with residential and commercial real estate transactions, including title insurance and escrow services. In connection with that business, FAFC issues common stock registered with the SEC pursuant to 12(b) of the Exchange Act. Many months before this SEC action arose, FAFC’s IT security personnel had identified a computer system vulnerability that they failed to remedy in accordance with the company’s policies, and about which they failed to inform the company’s senior management.

On May 24, 2019, a cybersecurity journalist notified FAFC that its “EaglePro” application for sharing document images related to title and escrow transactions had a cybersecurity vulnerability. The vulnerability exposed over 800 million title and escrow document images dating back to 2003. These images included Personal Identifiable Information (“PII”) such as social security numbers and financial information. In response to this notification, FAFC issued the following statement to the journalist: “First American has learned of a design defect in an application that made possible unauthorized access to customer data. At First American, security, privacy and confidentiality are of the highest priority and we are committed to protecting our customers’ information. The company took immediate action to address the situation and shut down external access to the application.” The journalist quoted this statement verbatim in his cybersecurity blog report published on the evening of May 24, 2019.[2]

FAFC then furnished a Form 8-K to the SEC on May 28, 2019, attaching an additional press release stating, in part, that there was “[n]o preliminary indication of large-scale unauthorized access to customer information.” The press release also stated: “First American Financial Corporation advises that it shut down external access to a production environment with a reported design defect that created the potential for unauthorized access to customer data.”

The June 2021 SEC Order arose in part because FAFC’s senior executives responsible for the press statement and Form 8-K were not apprised of certain information concerning the company’s information security personnel’s prior knowledge of a vulnerability associated with FAFC’s EaglePro system before making those statements – information that would have been relevant to management’s assessment of the company’s disclosure response to the vulnerability and the magnitude of the resulting risk. In particular, FAFC’s senior executives were not informed that the company’s information security personnel had identified a vulnerability several months earlier in a January 2019 manual penetration test of the EaglePro application (“January 2019 Report”), or that the company had failed to remediate the vulnerability in accordance with its policies. As discussed in the Order, FAFC did not maintain disclosure controls and procedures designed to ensure that senior management had this relevant information about the January 2019 Report prior to issuing the company’s disclosures about the vulnerability.

As evidenced by the FAFC Order, and several additional recent enforcement actions, the SEC is viewing cybersecurity threats to businesses subject to SEC rules as a growing business risk. One such enforcement action concerned Pearson plc, a London-based public company listed on the New York Stock Exchange (with Pearson’s ordinary shares registered under Section 12(b) of the Exchange Act). In August 2021, Pearson agreed to pay $1 million to settle charges that it misled investors about a 2018 data breach involving the theft of millions of student records, including dates of births and email addresses, and lacked adequate disclosure controls and procedures.[3]

Other recent SEC enforcement actions include sanctions against eight firms in three actions filed August 30, 2021, “for failures in their cybersecurity policies and procedures that resulted in email account takeovers exposing the personal information of thousands of customers and clients at each firm.” The eight firms, which have agreed to settle the charges, are: Cetera Advisor Networks LLC, Cetera Investment Services LLC, Cetera Financial Specialists LLC, Cetera Advisors LLC, and Cetera Investment Advisers LLC (collectively, the Cetera Entities) – $300,000 penalty; Cambridge Investment Research Inc. and Cambridge Investment Research Advisors Inc. (collectively, Cambridge) – $250,000 penalty; and KMS Financial Services Inc. – $200,000 penalty. All were Commission-registered as broker dealers, investment advisory firms, or both. Kristina Littman, Chief of the SEC Enforcement Division’s Cyber Unit, is quoted[4] as saying, “Investment advisers and broker dealers must fulfill their obligations concerning the protection of customer information…. It is not enough to write a policy requiring enhanced security measures if those requirements are not implemented or are only partially implemented, especially in the face of known attacks.”

Collectively, these SEC enforcement actions underscore the importance of a business:

Having appropriate privacy and cybersecurity policies;

Educating/training employees about these policies;

Ensuring the business’s contracting practices contain appropriate provisions consistent with these policies; and

Conducting periodic legal audits for compliance to these policies.

The FAFC Order also highlights the importance of executives maintaining an awareness of all material internal and external communications of the privacy and cybersecurity threats facing the business, and providing leadership from the top as to the importance of privacy and cybersecurity issues to the business’s risk management.

Special Purpose Acquisition Companies (SPACs) have become a popular way to raise funds for public mergers and acquisitions in recent years. However, the directors and officers of a SPAC can face unique exposures. These liabilities can include direct risks to personal assets because the funds the SPAC raises through a public offering must be held in a trust. A SPAC’s trust funds cannot be used to cover its defense and settlement costs and its at-risk capital may not be sufficient to cover these kinds of costs.

The right insurance can offer valuable peace of mind, but there is often some confusion about how it all works. This article will review two recent SPAC lawsuits and examine how an insurance policy—a Representations and Warranties (RWI) Policy or a Directors and Officers (D&O) Policy—would respond in each situation.

RWI Insurance and the Immunovant Case

Although SPACs are an exciting way of fundraising and going public, a SPAC is still, at heart, an M&A deal, making RWI insurance useful.

Let’s look at a recent case involving the biopharmaceutical company Immunovant. In Pitman v. Immunovant, Inc.,[1] a company developing a new drug to help with a common and debilitating disease connected with a SPAC looking for such a company. The two merged and went public.

However, when Immunovant announced it had “become aware of a potential problem” and “out of an abundance of caution” was placing a voluntary hold on its ongoing clinical trials, its stock price plunged 42%.

Shareholder Plaintiffs’ attorneys multiplied the 42% stock drop by the number of shares in open circulation and felt that the resulting amount was a large enough “pot of gold” to be worth the trouble of bringing a lawsuit. They united enough shareholders for a securities class action lawsuit with multiple allegations, including:

The SPAC failed to perform adequate due diligence.

The SPAC failed to disclose safety issues associated with the drug.

Because of either of these two factors, the prospects for approval, viability and profitability were diminished.

As a result, the company’s public statements were materially false and misleading.

Let’s first focus on the allegations of inadequate due diligence. These kinds of allegations typically assert that the SPAC team was incentivized to close a deal by a specific deadline and did not take the time or the effort to perform sufficient due diligence. The first implication here is that if the SPAC had made a proper effort to diligence the business and operations of the target company, it would have uncovered the problems being called out by the plaintiffs and would have been able to disclose them. The second implication is that if the SPAC’s diligence had been thorough, but had not uncovered problems, those problems were so well and intentionally hidden by the target company that they amounted to fraud on the part of the target company.

Putting aside the fraud implication for a moment, how does a SPAC refute the first implication of inadequate due diligence? The SPAC is responsible for establishing that it did, in fact, perform adequate diligence. To do so, an RWI policy, similar to the one used in the Immunovant deal, could be of great use. The process the buyer of the RWI policy (in this case, the SPAC) undertakes to secure the policy includes an intensive review by the insurer of the diligence the buyer conducted. The insurer usually engages specialized counsel from big law firms to review the diligence and probe areas that the insurer and its counsel (who see dozens of similar kinds of deals in the same industry on a weekly basis) believe to be particularly risky. In a way, this process serves as a safety net for anything the SPAC’s diligence team could have missed while reviewing the target’s business and operations. The insurer is incentivized to be extremely thorough because it will be the one paying the bills if diligence is patchy.

So in the Immunovant case, if—hypothetically—there were representations given as to the accuracy of Immunovant’s records of previous clinical drug trials, the RWI policy defenses would include:

The assertion that since the company has gone through the process of acquiring an RWI policy, which requires third parties to review the diligence and probe the adequacy of the work done. Thus the Plaintiffs have a much more difficult argument that that diligence was inadequate.

The argument that RWI speaks very clearly to what was known and not known by the SPAC. In essence, RWI provides the Immunovant parties with a third-party paper trail showing how much Defendants knew, how hard they worked to get to the information, and how innocent they were.

Coming back to the second implication of fraud, a RWI policy covers seller’s fraud. So if the diligence efforts fail in the face of fraud by the target company, the RWI policy would step in to cover losses resulting from such fraud. This means that the SPAC could potentially recoup some lost money and return it to the SPAC investors (Plaintiffs), which would diminish their losses and consequently the amount claimed by Plaintiffs’ attorneys in their lawsuit against the SPAC.

The Importance of RWI to SPACs

Representations and warranties insurance can hedge the risk for both the buyer and the seller in SPACs. There’s a common misperception that RWI is not useful in a public company style deal because in a public company deal the seller typical provides very limited or no representations and warranties in the purchase agreement and no indemnification. This reasoning is flawed. When there is lack of indemnification from the seller, the buyer is saddled with all of the risk with no avenue for a recourse. That is exactly the situation where RWI coverage is even more critical. In these kinds of cases, synthetic representations and warranties can be put in place through the use of a RWI policy and at least some of the risk can be transferred to the insurer. The definition of loss in these situations essentially comes from the insurance policy and not from the indemnification section of the agreement, and the buyer is insured against that loss.

D&O Insurance and the Lucid Motors Case

D&O insurance is on everyone’s minds these days because of its rising cost. Naturally, many companies are asking about ways they can save on their D&O premiums by reducing coverage.

Clients often ask if they need D&O coverage at the time of the SPAC’s IPO and whether they can get away with buying the least possible amount. There’s a myth out in the SPAC market that SPACs are not really subject to risk between the time of their IPO and their de-SPAC. Unfortunately, the common belief that all litigation comes after the de-SPAC is just not true and can cause some serious problems for the SPAC and its team of directors and officers. In fact, it is crucial to have coverage between the IPO and the de-SPAC.

Now, let us examine a case study that illustrates the importance of D&O insurance: Churchill Capital Corporation IV SecuritiesLitigation.[2] The Complaint alleges that Rumors spread that Churchill Capital Acquisition Corporation IV was going to acquire Lucid Motors, an electric vehicle company, which caused the price of the SPAC’s shares to jump from $10 to $22 per share. Then, the Lucid Motors CEO spoke to the media and mentioned a plan to deliver 6,000 vehicles in 2021. After several other statements to the media, the SPAC shares climbed to over $57 a share. The merger was finally announced on February 22, 2021, and on the same day the Lucid Motors CEO told the media that, in fact, the production of the vehicles would be delayed.

Documentation filed with merger announcement revealed that only 557 vehicles were planned versus the 6,000 that were previously mentioned and, not surprisingly, the price of the SPAC’s shares tanked. By the time the lawsuit was filed on April 18, 2021, the SPAC’s shares were trading at $18 per share.

What is interesting to note here is that this lawsuit is not your garden variety merger objection suit in which the plaintiffs allege insufficient disclosure and argue for the merger to be halted. These kinds of allegations and demands are typically addressed through additional SEC filings to close any gaps in the disclosure, and the plaintiff usually goes away for a few thousand dollars in mootness fees. These merger objections suits are not looked upon kindly by Delaware courts, which is why they are often filed in New York and have been commonly referred to as an M&A (and now a SPAC) “transaction tax.”

The Lucid Motors case, however, is a full-blown securities class-action lawsuit brought in federal court in Alabama against the SPAC, its CEO and CFO, and the target and its CEO. It alleges that these parties made or were involved in making false statements and omissions that drove the wild price fluctuations, which then resulted in losses for the SPAC’s shareholders. What’s even more interesting is that this lawsuit is being brought in advance of the merger for statements made prior to even the merger announcement.

When lawsuits of this type are brought, defendants’ thoughts automatically turn to insurance. The questions typically are:

Is there an insurance policy in place to protect my SPAC and my directors and officers?

Will the limits of that policy be sufficient to cover litigation defense and settlement costs?

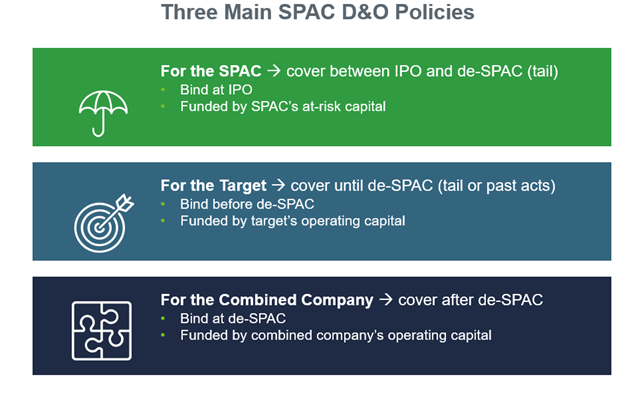

Here we should take a short detour and understand the kinds of policies that a SPAC team will encounter as it proceeds through the life cycle of the SPAC. There are three main types of D&O policies and it is essential to understand which D&O policies are in play before, during, and after the SPAC merger.

The first policy is the one that covers the SPAC and its directors and officers between the SPAC’s IPO and its business combination. This policy binds at the IPO and is funded by the SPAC’s at-risk capital. It typically has a tail component, which is essentially an extended reporting period for claims that come after the merger. Because a SPAC’s at-risk capital is usually very limited and the current SPAC D&O insurance pricing is quite high, these policies, if not planned and budgeted for properly, can cause a lot of aggravation to SPAC teams.

The second policy is the private company policy that covers the target company and its directors and officers until the company mergers with the SPAC. This policy can also have a tail component but is quite different from the public company D&O policy. It is a lot less complex and a lot less expensive than the public company D&O policy placed for a SPAC and for the combined company after the merger. This policy is typically in place ahead of the de-SPAC and is funded out of the target company’s operating capital.

The third policy covers the combined company and its directors and officers after the merger. It binds at the time of the merger and looks and feels very much like any traditional public company D&O policy. It is also considerably more expensive than the SPAC D&O policy and usually renews on an annual basis.

The Importance of Choosing the Right D&O Coverage

The first lesson we can learn from the Lucid Motors case is that serious, expensive lawsuits can and do occur before the de-SPAC and that the period between the SPAC IPO and its business combination is not risk-free. Consequently, the terms and limits of that first policy that covers the SPAC and its directors and officers between the IPO and the de-SPAC should be considered very carefully.

The second lesson is that lower limit of coverage may not be sufficient to cover defense and settlement costs and can put you at risk. Last year, SPAC teams usually considered $20 million in coverage limits for their SPACs because premium pricing was low and affordable. In recent months, however, increases in D&O premium pricing have forced SPAC teams to gravitate towards much lower limits. The majority now purchase between $5 million and $10 million in coverage, and some have even considered limits as low as $2.5 million. While D&O insurance costs are high and at-risk capital is restricted, going for the least expensive policy may not be the right decision for your SPAC and your team.

The importance of risk mitigation is another great lesson to take away from the Lucid Motors case. It is incredibly critical for all SPAC executives and the executives of the target company to pay very close attention to public messaging around deal time. They must be especially careful when making any statements on social or other media because getting sued for even inadvertent misrepresentations can be extremely painful, time consuming, and distracting in the midst of a deal and, without proper insurance coverage, can lead to serious financial losses.

Conclusion

The SPAC market is extremely dynamic and has grown dramatically in size and sophistication over the last few months. SPAC teams and teams aiming to merge with a SPAC must keep on top of the latest developments in the financial, regulatory, and legal aspects of this market.

Allegations and complaints in the lawsuits like the ones discussed above, while novel now, may become standard in the future. Having advisers who can steer you away from traps and anticipate risks and pitfalls, including guiding you through the most efficient and effective use of RWI and D&O policies is a must have for any SPAC team.

[1] Case No. 1:21-cv-00918, U.S. District Court for the Eastern District of New York.

[2] Case No. 21-cv-00539, U.S. District Court for the Northern District of Alabama, Eastern Division. See also, Arico v. Churchill Capital Corporation IV, Case No. 21-cv-12355, U.S. District Court for the District of New Jersey.

Amidst all of the tributes on 9/11, there are two more public servants who deserve America’s thanks. They are not among the first responders, such as firefighters or police officers, who ran towards the burning buildings. They protected America’s financial system on that terrible day and during the days thereafter. They served the public with courage and distinction.

The first is Roger W. Ferguson, Jr., who was Vice Chairman of the Board of Governors of the Federal Reserve System. As the Federal Reserve website notes, “When the terrorist attacks occurred on September 11, 2001, Ferguson was the only member of the Board of Governors in Washington (others were traveling). He quickly moved to assure bankers and investors that the Fed would provide the lending necessary to keep the economy going in the aftermath of the crisis.”

As Mr. Ferguson later explained, the attack “could prompt a chain reaction drying up liquidity, which, unchecked, could lead to real economic activity seizing-up. The shocks to the financial system and the economy that were possible could have been disastrous to the confidence of businesses and households in our country and, to a significant degree, the rest of the world.”[1] It was critical for the Fed to demonstrate leadership in the face of this vicious attack.

First, Mr. Ferguson made sure that the financial system maintained liquidity, the lifeblood of our economy.

Why were we so concerned about maintaining liquidity in the financial system? Liquidity, as you know, serves as the oil lubricating the engine of capitalism to keep it from burning itself out. The efficiency of our financial system at maintaining adequate liquidity is often taken for granted. But on September 11, it could not be taken for granted. The bottlenecks in the pipeline became so severe that the Federal Reserve stepped in to ensure that the financial system remained adequately liquid. In other words, our massive provision of reserves made sure that the engine of finance did not run out of oil and seize up.[2]

Vice Chairman Ferguson and his Fed colleagues made sure that the Fed discount window was open and lending to banks.

On September 12, lending to banks through the discount window totaled about $46 billion, more than two hundred times the daily average for the previous month. The flood of funds released into the banking system reduced the immediate need for banks to rely on payments from other banks to make the payments they themselves owed others.[3]

These and other actions that Mr. Ferguson spearheaded prevented the American economy from going into a tailspin. I don’t know what went on behind the scenes at the Fed. But as the senior Fed governor, Roger acted with focus and determination. He didn’t dither. He demonstrated leadership and patriotism under extraordinary circumstances. If I had an opportunity to whisper in President Biden’s ear, I would urge him to award the Medal of Freedom to Roger Ferguson for his extraordinary service on that day.

A second person who deserves our thanks is Annette L. Nazareth. Ms. Nazareth was the Director of the SEC’s Division of Market Regulation (now known as the Division of Trading & Markets). (President George W. Bush later appointed her to be an SEC Commissioner.) After the attacks, there was enormous political pressure for Wall Street to reopen immediately. Notwithstanding the terrible loss of life and physical damage in lower Manhattan, many in Washington felt it was important to show the nation and the world that Wall Street could keep functioning.

The exchanges and broker-dealers appreciated the need to reopen, but they knew that they were not ready. For those firms whose personnel survived the attack, it was not easy to resume trading. Many firms’ offices were destroyed or were inaccessible. The attack knocked out communications lines and other systems. No one had considered disaster planning for a terrorist attack. Working from home wasn’t a possibility in those days. A premature opening would have resulted in failures and would have done more damage to the public’s confidence, rather than enhancing it.

On 9/11, I was general counsel of the Securities Industry Association (now called SIFMA), the trade group for broker-dealers. My members asked me to deliver one message to Ms. Nazareth at the SEC: don’t force the markets to open before they are ready. Of course, many others offered the same advice to others at the SEC, including Chairman Harvey Pitt.

Fortunately, the SEC took the advice that so many offered. As TheWall Street Journal recently described it, “The stock market stayed closed for four trading days—its longest shutdown since 1933—as crews worked to fix the damage.”[4] The subsequent reopening went reasonably well.

* * * * *

The financial markets are very different today than they were in 2001. Physical trading floors are much less important today than they were twenty years ago. Financial markets face different challenges, such as cyberattacks.[5] Those changes don’t diminish the leadership and heroism of the numerous individuals who worked so hard to restore America’s financial system after the 9/11 attacks.

Both Annette Nazareth and Roger Ferguson deserve our thanks for keeping their heads cool and acting sensibly in the face of a crisis. They prevented a terrible attack from cascading into a financial calamity. And for those of you who don’t know, Roger and Annette are husband and wife.

[1]Remarks by Vice Chairman Roger W. Ferguson, Jr. At Vanderbilt University, Nashville, Tennessee, February 5, 2003.

The folk rock group The Mamas and the Papas’ first hit and Grammy Hall of Fame song, “California Dreamin’,” expressed the hopes and dreams of leaving behind the cold of a winter’s day for the warmth of Los Angeles.[1] Under a recent decision of the California Court of Appeal that reversed the judgment of an L.A. trial court, whether a hit song means that the songwriter realizes the hopes and dreams of the warmth of financially sharing in the song’s success, or bears the cold of a winter’s day in not so sharing,[2] turns on the grant of discretion in the songwriter’s contract with the music publisher.

THE GRANT OF DISCRETION UNDER CALIFORNIA LAW

In Gilkyson v. Disney Enterprises, Inc.,[3] the children of the late songwriter Terry Gilkyson sued Disney Enterprises, Inc. and its music publishing subsidiary, Wonderland Music Company, Inc. (collectively, “Disney”), over royalties for the use of Gilkyson’s songs in the home entertainment releases of the 1967 animated film, The Jungle Book. One of the songs was “The Bare Necessities,” a song that has warmed the hearts of children around the world, whose laughter then warmed the hearts of their parents.

In 1963, Gilkyson entered into a contract with Disney that provided for a royalty equal to 50% of the net amount received by the Disney music publisher on account of licensing or other disposition of the mechanical reproduction right in and to material written by Gilkyson.

In another section of the contract, Disney reserved all revenue and receipts received by and paid to Disney by virtue of the exercise of grand, dramatic, television, and other performance rights, including the use of the material in motion pictures, photoplays, books, merchandising, television, radio, and endeavors of the same or similar nature.

Finally, another section of the contract provided that Gilkyson had no interest in any of the material other than his right to receive the royalties specifically set forth in the contract. In addition, nothing contained in the contract was to be construed as obligating Disney “to publish, release, exploit or otherwise distribute any of the material, and the same shall be always subject to [Disney’s] sole discretion.”

The jury returned a verdict of $350,000 in favor of the Gilkyson children for Disney’s breach of the contract. The trial judge then awarded an additional $699,316.40 as damages for the period after the date of the verdict through the duration of the songs’ copyrights.

Disney appealed the trial court’s judgment. The California Court of Appeal reversed and held that, under the language of the contract, Disney did not have any obligation to pay royalties to the Gilkyson children during the contract’s limitations period. Since the Disney music publisher was not paid for digital downloads of the motion picture or other audiovisual reproductions, it did not receive any amounts for which royalties were due.

Furthermore, nothing in the contract required Disney to exploit the mechanical reproduction rights at all or, if it elected to do so, exploit them in any particular manner. Rather, exploitation of these rights was in Disney’s sole discretion. Accordingly, the Disney music publisher had the right to permit its home entertainment affiliate to use the songs without charging an intercompany license fee and without incurring any liability to Gilkyson. The court keenly observed, “Had the parties intended that Disney would use its best efforts to exploit the mechanical reproduction rights in a manner that generated royalties for Gilkyson, the contracts would not have expressly granted Disney such unfettered discretion.”[4]

Since the trial court had denied the Gilkyson children’s motion for leave to file a second amended complaint that would have added a cause of action for breach of the implied covenant of good faith and fair dealing, and their appeal did not raise this issue, the covenant was not before the Court of Appeal. However, the Court of Appeal rejected the Gilkyson children’s argument that several general provisions of California law required the payment of royalties. Their argument would effectively require the court to rewrite the express language of the contract, which granted Disney the sole discretion on how to exploit the rights it obtained from Gilkyson and limited his right to royalties to Disney’s net receipts. The court was not authorized to engage in such an endeavor.

THE GRANT OF DISCRETION UNDER DELAWARE LAW

The reasoning of the court in Gilkyson is not unique to the jurisprudence of California. Delaware, the venerable bastion of corporate law, has used similar reasoning in its jurisprudence. In Oxbow Carbon & Minerals Holdings, Inc. v. Crestview-Oxbow Acquisition, LLC,[5] the Delaware Supreme Court’s most recent guidance on the implied covenant of good faith and fair dealing, the court rejected the use of the covenant in the face of a grant of discretion.

In Oxbow Carbon, two minority investors, Crestview Partners, L.P. and Load Line Capital LLC, became members (the “Minority Members”) of Oxbow Carbon LLC (“Oxbow”) in 2007. Oxbow was the leading third-party provider of marketing and logistics services to the global petroleum coke market. Crestview made a $190 million capital contribution in exchange for a 23.48% membership interest, and Load Line made a $75 million capital contribution in exchange for a 9.27% membership interest.

The majority investor, Oxbow Carbon & Minerals Holdings, Inc. (“Oxbow Holdings”), made a $483,038,499.86 capital contribution in exchange for an almost 60% membership interest. Oxbow and Oxbow Holdings were controlled by William I. Koch. Several of Koch’s family members and affiliates also invested in Oxbow, which meant that the Koch group owned a combined 67% of Oxbow’s equity.

The Minority Members bargained for the following exit rights. First, they received a put right that could be exercised after seven years. Second, if Oxbow rejected the put, the party exercising the put could force an exit sale of all of Oxbow’s equity interests. However, a member could not be forced to sell its equity interest unless it received total distributions from operations and the exit sale was equal to or greater than 1.5 times the member’s aggregate capital contribution (the “1.5x requirement”). The LLC agreement provided that all distributions were to be made pro rata in accordance with each member’s percentage interest and that any exit sale must be on equal terms and conditions for all members.

In 2011 and 2012, Oxbow admitted additional minority members, Ingraham Investments LLC and Oxbow Carbon Investment Company LLC (collectively, the “Small Holders”). The Small Holders received a combined 1.4% membership interest. The members of Ingraham were members of Koch’s family, and the members of Oxbow Carbon Investment Company were executives of a large sulfur trading company acquired by Oxbow. Ingraham made a $20 million capital contribution, and Oxbow Carbon Investment Company made a $15 million capital contribution. Oxbow distributed approximately $8.2 million to Crestview and $3.2 million to Load Line from these capital contributions.

The board of directors of Oxbow unanimously approved the admission of the Small Holders, including the directors appointed by Crestview and Load Line, who otherwise had the right to block their admission. Although their admission did not comply with the LLC operating agreement’s preemptive rights provisions and the special approval requirements for related party transactions,[6] and the Small Holders did not deliver signed counterpart signature pages, the Court of Chancery found that in their course of dealing, the parties treated the Small Holders as members.

On September 28, 2015, Crestview exercised its put. When Oxbow rejected the put, on January 20, 2016, Crestview exercised its right to an exit sale. However, at the price offered by the bidder, the sale proceeds were insufficient to distribute to the Small Holders an amount equal to or greater than the 1.5x requirement.

Litigation then ensued. The Court of Chancery held that although the 1.5x requirement prevented an exit sale, under the implied covenant of good faith and fair dealing, the exit sale should go forward. Since the board of directors did not expressly determine the rights, powers, and duties of Small Holders at the time of their admission, in particular whether the Small Holders would have the benefit of the 1.5x requirement, there was a gap in the contractual rights of the Minority Members and Small Holders. According to the Court of Chancery’s summary judgment opinion, had the Minority Members realized that the Small Holders would have the ability to block an exit sale due to the 1.5x requirement, the Minority Members would not have consented to their admission. In addition, had the parties recognized this gap, they most likely would have agreed that the Minority Members could satisfy the 1.5x requirement by making additional payments to the Small Holders from the proceeds the Minority Members received from the sale.

The Delaware Supreme Court reversed and held that there was no gap and the implied covenant of good faith and fair dealing did not apply. Therefore, under the plain language of the LLC operating agreement, the Small Holders had the benefit of the 1.5x requirement and could block the exit sale.

Under the LLC agreement, the terms of admission of new members were left to the discretion of the board of directors.[7] Since the board chose not to specify different rights for the Small Holders, the terms of the LLC agreement applied with equal force to them. The court would not imply new contract terms merely because the contract granted discretion to a board of directors.[8] Conferring discretion on the board was a contractual choice to grant authority to the board and not a gap. Although the grant of discretion did not relieve the board of its obligation to use that discretion consistent with the implied covenant of good faith and fair dealing, the Minority Members did not argue that the board exercised its discretion in bad faith in admitting the Small Holders.

The court found that in light of the absence of a gap, and since the admission of new members and its effect on the exit sale process could have been anticipated, the court would not apply the covenant. The court observed that the parties could have limited the 1.5x requirement to certain members, excluded subsequently admitted members, amended the exit sale right to permit distributions by Oxbow to the Small Holders to satisfy the 1.5x requirement before distributions were made pro rata to the members, or amended the exit sale right to permit the Minority Members to make payments to the Small Holders to satisfy the 1.5x requirement.

The court then described the limited use of the implied covenant of good faith and fair dealing. The covenant was a cautious enterprise best understood as a way of implying terms in a contract, whether employed to analyze unanticipated developments or to fill gaps in the contract. It was not an equitable remedy for rebalancing economic interests after events occurred that could have been anticipated but were not, which later adversely affected a party to the contract. Rather, the covenant was a limited and extraordinary legal remedy.

The covenant did not apply when the contract addressed the conduct at issue, but only when the contract was truly silent concerning the matter at hand. Even when the contract was silent, an interpreting court could not use an implied covenant to rewrite the parties’ agreement and should be most chary about applying a contractual protection when the contract could easily have been drafted to expressly provide for that protection.

Finally, the court pointed out the two situations in which the covenant generally would apply. First, a situation has arisen that was unforeseen by the parties, and the agreement’s express terms do not cover what should happen. Second, a party to the contract is given discretion to act as to a certain subject, and the discretion has been used in a way that is impliedly proscribed by the contract’s express terms.

THE TAKEAWAY

The takeaway from Gilkyson and OxbowCarbon is that in drafting contracts, the grant of discretion usually wins the day. If a party wants to avoid or lessen the risk of another party’s exercise of discretion to deprive it of a benefit, then to the extent that the party has the leverage, it should bargain for the contract to clearly set forth nondiscretionary obligations of the other party or well-defined parameters on the other party’s exercise of discretion. To rely on the implied covenant of good faith and fair dealing is likely no more than a vain hope and dream.

[1] The Mamas and the Papas, “California Dreamin’,” Music and lyrics by John E.A. Phillips and Michelle Gilliam Phillips, on If You Can Believe Your Eyes and Ears (Dunhill 1966).

[2]Cf. Gladys Knight & the Pips, “Midnight Train to Georgia,” Music and lyrics by Jim Weatherly, on Imagination (Buddah 1973) (“L.A. proved too much for the man (too much for the man, he couldn’t make it). So he’s leaving a life he’s come to know, ooh (he said he’s going). He said he’s going back to find (going back to find), ooh, what’s left of his world, the world he left behind not so long ago. . . . He kept dreaming (dreaming), ooh, that someday he’d be a star (a superstar, but he didn’t get far). But he sure found out the hard way that dreams don’t always come true, oh no, uh uh (dreams don’t always come true, uh uh, no, uh uh). So he pawned down his hopes (woo, woo, woo-woo), and even sold his old car (woo, woo, woo-woo). Bought a one way ticket back to the life he once knew, oh yes he did, he said he would.”).

[3] 2021 WL 3075699 (Cal. Ct. App. July 21, 2021).

[5] 202 A.3d 482 (Del. 2019) (en banc) (Valihura, J.).

[6] The LLC operating agreement provided for the admission of new members “on such terms and conditions as the Directors may determine at the time of admission. The terms of admission may provide for the creation of different classes or series of Units having different rights, powers and duties.”

[7]Seealso Kenneth A. Adams, A Manual of Style for Contract Drafting 3.188 (ABA 4th ed. 2017) (“Discretion is primarily conveyed by means of may, which expresses permission or sanction.”).

[8]See also Mohsen Manesh, “Express Contract Terms and the Implied Contractual Covenant of Delaware Law,” 38 Delaware Journal of Corporate Law 1, 35 (2013) (“[W]hen the express terms of a contract unambiguously grant one party unfettered, sole, and absolute discretion, the court will readily construe the express terms to permit the discretion-exercising party to act under any circumstances and for any reason, free of judicial intervention. It is because the Implied Covenant notwithstanding, such language in the contract permits only that reasonable expectation.”) (footnote omitted).

In decisions that may signal things to come for employee plaintiffs in the wake of the Supreme Court’s decision in Alston,[1] two federal courts applying the rule of reason have denied class certification in two pending no-poach antitrust franchise claims for a failure to show the predominance of common questions. On July 28, a Chicago federal judge declined to certify a class action against McDonald’s for violating Section 1 of the Sherman Act.[2] Two days later, a Southern District of Illinois judge also declined to certify a class against Jimmy John’s due to several Rule 23(a) and (b) failures of proof, including the predominance of individual questions.[3]

Both class actions challenged no-poach clauses in the fast food giants’ franchise agreements, which prevented their franchisees from hiring employees of other franchises or company-operated restaurants. Although the courts denied class certification on varied bases, both found that the alleged unlawful restraint — the no-poach provisions — should be evaluated under the rule of reason and not the quick-look analysis sought by the plaintiffs, and the plaintiffs who sought to certify nationwide classes did not present evidence that the relevant geographic market where they offered their labor services was national in scope. The courts suggested instead that the relevant geographic markets for fast-food employees like the plaintiffs could be the hundreds or thousands of markets near where the employees lived and worked, and that they would include all quick-service restaurants in the markets, not just the defendants’ branded restaurants.

Background

Until July 2018, both McDonald’s and Jimmy John’s had provisions in their franchise agreements generally prohibiting their franchisees from employing or seeking to employ individuals who work for other franchisees or restaurants operated by the company. While most of the fast-food giants’ branded restaurants are franchised, they both operate a small portion of the restaurants themselves. The plaintiffs in Deslandes v. McDonald’s and Conrad v. Jimmy John’s Franchise LLC are current or former employees of McDonald’s and Jimmy John’s restaurants, who allege that the no-poach provisions violate Section 1 of the Sherman Act by limiting competition and suppressing their wages.

While the proposed classes — nationwide classes of all persons employed at the defendants’ branded restaurants from roughly 2013 through July 12, 2018 — were sufficiently numerous under Fed. R. Civ. P. 23(a), both courts found, among other things, that common questions did not predominate under Rule 23(b)(3), thus barring certification. Although not discussed in this article, both courts denied class certification on other grounds factually specific to the claims raised in their respective cases.[4]

Rule of Reason v. Quick-Look Analysis

Before assessing whether common questions predominated, both courts decided whether the alleged anticompetitive effects should be analyzed using the rule of reason or a quick-look analysis. Relying on the Supreme Court’s recent decision in Alston, which involved a similar Section 1 Sherman Act claim against the NCAA and 11 Division 1 conferences for allegedly wielding monopsonist power in the market for student athletes, the courts held that a quick-look analysis applies only in rare situations, where the court has “considerable experience with the type of restraint at issue.”[5]

The McDonald’s court did not have enough experience with no-poach provisions in franchise agreements to say with confidence that the practice must always be condemned. Thus, with Alston as precedent, the McDonald’s court applied the rule of reason, as opposed to the quick-look analysis.

The Jimmy John’s court relied on Alston to answer the question it had punted at the motion to dismiss stage and found that the rule of reason applies “in this monopsony case challenging a nationwide franchise’s use of intrabrand restraints that were arguably ‘designed to help [the company] more effectively compete with other brands by ensuring cooperation and collegiality among franchisees, and by encouraging investment in training.’”[6] In addition to following the Supreme Court’s precedent in Alston, the Jimmy John’s court also found that the plaintiffs had failed to present common proof that will show that each franchisee conspired with Jimmy John’s to suppress labor mobility and wages.[7]

The rule of reason applied for several other important reasons. First, Defendant McDonald’s put forth sufficient evidence of the pro-competitive effects of the alleged restraint — preventing free riding and encouraging training — warranting the application of the rule of reason.[8] Second, because Defendant McDonald’s operates far fewer restaurants than its franchisees, franchises do not compete with restaurants McDonald’s operated for employees in many areas of the country, establishing that in many geographic markets, the restraints are vertical not horizontal.[9] Vertical restraints are judged under the rule of reason.[10] Third, Jimmy John’s presented expert opinion that the no-poach provision actually benefited the members of the putative class by encouraging their employers to invest in training, and the relevant labor market was not nationwide in scope and not limited to employment with the Jimmy John’s branded restaurants.[11] Rather, it encompassed employment at all quick-service restaurants within a local relevant market.[12]

Rule of Reason Application Creates Individual Questions Preventing Class Certification

The first question under the rule of reason analysis is whether the challenged restraint of trade has a substantial anticompetitive effect in the relevant market.[13] Both courts rejected the plaintiffs’ characterization of the relevant market as a national service market for McDonald’s or Jimmy John’s restaurant workers. The McDonald’s court said “it defies logic to suppose” that McDonald’s employees sell their labor in a national market.[14] According to the court, employees that compete in national markets are “highly skilled or highly paid” like CEOs — not fast-food employees.[15] This conclusion is buttressed by Defendant McDonald’s evidence: the deposition testimony from lay and expert witnesses demonstrated that McDonald’s restaurants experience local, not national, competition.[16] As such, the court found that proposed class members competed in different relevant geographic markets, making the rule of reason antitrust questions predominantly individual for purposes of Rule 23(b)(3).

Similarly, the Jimmy John’s court found, based on expert testimony, that competition from other quick-service restaurant employers and others would “push the worker’s wages … up to the competitive level associated with the worker’s skills.”[17] As such, individual questions as to whether individual plaintiffs suffered injury because of the alleged restraints existed, given the “varied and dynamic labor markets across the country.”[18]

Because the predominate question of whether the restraint causes an anticompetitive effect in the relevant market is not common to class members, the McDonald’s court did not decide whether the question of antitrust injury or impact is common.[19] But the court did say that it would be “difficult … to imagine that it could be a common question … ” since the question is based on wages, and “[t]he amount each person’s wages are suppressed,” which “will almost certainly vary depending on the amount of labor market power McDonald’s possessed in each relevant market.”[20]

Takeaways

While other courts could disagree,[21] these decisions represent big wins for employers and franchisors after the Alston decision, representing persuasive authority for limiting the use of quick-look analysis in franchise no-poach antitrust claims. Further, to the extent the rule of reason applies, the decisions illustrate the difficulty class plaintiffs and their counsel will face in trying to establish the predominance of common questions under the rule of reason when alleging both horizontal and vertical restraints.

[1]National Collegiate Athletic Association v. Alston, 594 U.S. ___.

[2]Deslandes v. McDonald’s USA LLC, No. 17 C 4857, 2021 WL 3187668 (N.D. Ill. July 28, 2021).

[4] The McDonald’s court found the class was not fairly and adequately represented by counsel due to its litigation tactics, including waiving the right to pursue a rule of reason antitrust claim. The Jimmy John’s court denied class certification for a number of reasons beside predominance, including a failure of typicality and adequacy, and a class was not a superior method of adjudicating the claims.

[5] McDonald’s, 2021 WL 3187668 at *11 (quoting Nat’l Collegiate Athletic Ass’n v. Alston, 141 S. Ct. 2141, 2156 (2021)): Jimmy John’s, 2021 U.S. Dist. 142272, at 25-6 (quoting Nat’l Collegiate Athletic Ass’n v. Alston, 141 S. Ct. 2141, 2156 (2021)).

[8]McDonald’s, 2021 WL 3187668 at *12-16. Even the plaintiffs’ experts echo this point, saying “for the restaurant employees in particular, the crew employees, there may be labor markets of different geographic size and that the key issue there might not even be size, it might be commuting distance.” Id. at 13.

[21]See e.g., Jarvis Arrington, et al v. BKW, et al., No. 20-13561 (11th Cir.). Oral arguments in the appeal of this franchise no-poach agreement case against Burger King have been scheduled for September 22, 2021.

On July 9, 2021, President Biden signed a broad Executive Order on Promoting Competition in the American Economy. This Executive Order—along with the related Fact Sheet and the President’s remarks at its signing—suggest that the administration is committed to an aggressive and coordinated approach to competition issues, especially in the areas of labor markets, agriculture, healthcare, and the tech sector. While many are skeptical that the Executive Order will change anything, the ability of the antitrust enforcement agencies to tie up mergers, challenge business decisions, and influence the courts—and the ripple effect on private actions—should not be ignored or underestimated. After summarizing the Executive Order, we recommend certain steps aimed at mitigating antitrust risks in the current political environment.

The White House was critical of past corporate consolidation across 75% of U.S. industries and argued that consolidation had increased prices for consumers, decreased wages for workers, and even hindered growth and innovation by making it more difficult for small and independent businesses. The Executive Order establishes what the White House refers to as a “whole-of-government effort to promote competition in the American economy,” encouraging 72 initiatives by more than a dozen agencies.

The Executive Order creates the White House Competition Council (the “Council”) within the Executive Office of the President as part of the plan to institute the coordinated and aggressive approach to competition-related matters across federal agencies.[1] The Council will work to implement the policies and the specific initiatives described in the Executive Order.

1. Labor and Noncompetes

The executive order places particular focus on labor issues and encourages the Federal Trade Commission (“FTC”) to ban or limit employee noncompete arrangements to increase economic mobility by making it easier for employees to change jobs. This effort builds on the Department of Justice’s (“DOJ”) recent efforts to challenge employee no-poach agreements as criminal antitrust violations. Companies considering business noncompetes should continue to ensure that such agreements are narrowly tailored for a legitimate business purpose. Similarly, the executive order encourages the FTC to ban unnecessary occupational licensing requirements.

2. Merger Enforcement

The executive order introduces uncertainty for businesses planning mergers or other actions that may raise competition issues. In fact, the order appears to invite such uncertainty by, among other things, supporting the “challenge [of] prior bad mergers that past administrations did not previously challenge.”

The executive order also urges the FTC and DOJ to review and revise their Merger Guidelines, which the FTC and DOJ immediately took up by announcing their plan to review the guidelines “to determine whether they are overly permissive.” The executive order also specifically asks the agencies to scrutinize and reconsider their approach to mergers in the hospital, banking and consumer finance, and Big Tech spaces. Some anticipated changes include lowering the concentration thresholds for presumptively anticompetitive mergers, refining potential competition prohibitions, and eliminating or greatly limiting the efficiencies defense.

The Executive Order also directed a number of actions aimed at specific sectors of the economy and even set short deadlines for some:

Labor Markets

Use FTC rulemaking authority to limit the use of non-compete clauses.

Use FTC rulemaking authority to limit unfair occupational licensing restrictions.

Food and Drug Administration (“FDA”) to work with states and tribes to import drugs from Canada.

Within 120 days, Department of Health and Human Services (“HHS”) to propose rules to make hearing aids available over the counter.

Within 45 days, HHS to increase support for generic drugs and issue a plan to combat high prescription drug prices and price gouging.

HHS to implement federal legislation to address surprise hospital billing.

HHS to standardize plan options in the National Health Insurance Marketplace to make it easier for people to comparison shop.

FTC to implement a rule that bans “pay for delay” agreements.

DOJ and FTC to revise merger guidelines so that patients are not harmed by hospital mergers.

Transportation

Within 45 days, Department of Transportation (“DOT”) to propose rules that require airlines to refund fees for services that are not provided, such as baggage fees when luggage is substantially delayed.

Within 90 days, DOT to consider rules that require airlines to clearly disclose to customers any ancillary fees, such as for baggage, ticket changes, or cancellations.

Agriculture

Department of Agriculture (“USDA”) to consider new rules under the Packers and Stockyards Act to address the unfair treatment of famers and improve competition in markets for their products.

USDA to consider new rules regarding when meat products can have “Product of USA” labels.

Within 300 days, USDA to develop a plan to increase farmers’ and small food processors’ access to retail market and submit a report to the Chair of the Council.

FTC to propose rules that limit equipment manufacturers from restricting farmers from repairing their own equipment.

Internet Service

Federal Communications Commission (“FCC”) to conduct future spectrum auction under rules that avoid excessive concentration of spectrum licenses.

FCC to prohibit internet service providers from charging excessive early termination fees.

FCC to establish rules that prevents landlords from making deals with ISPs to limit tenants’ choices.

FCC to restore Net Neutrality rules.

FCC to establish rules that requires broadband providers to provide a consumer label with clear information about prices and fees, performance, and network practices and to require those providers to report broadband price and subscription rates to the FCC for dissemination to the public.

Technology

Make it Administration policy to enforce antitrust laws in the area of new industries and technologies, and to scrutinize mergers by dominant internet platforms when they “stem from serial mergers, the acquisition of nascent competitors, the aggregation of data, unfair competition in attention markets, the surveillance of users, and the presence of network effects.”

FTC to establish rules pertaining to data collection and surveillance that may damage competition, consumer autonomy, and consumer privacy.

FTC to establish rules against unfair competition in major internet marketplaces.

Banking and Consumer Finance

Within 180 days, DOJ and federal banking agencies to review current practices and adopt for greater scrutiny of mergers under the Bank Merger Act and the Bank Holding Company Act of 1956.

Consumer Financial Protection Bureau (“CFPB”) to use rulemaking to make consumer financial data more portable and make it easier for consumers to switch banks.

The Executive Order does not immediately change the existing antitrust framework, but businesses should be prepared for a near-term change in enforcement by the relevant agencies. Companies should consider or be prepared to take steps such as those identified here:

Agreements or policies affecting employee freedom of movement should be assessed for less restrictive alternatives and focused as narrowly as possible to accomplish procompetitive objectives.

Compliance programs should be updated to shift focus from only or primarily customers/consumers to include competitors.

Given calls to abandon proof of a relevant product market, companies that have previously relied on a broad market definition when assessing the lawfulness of their actions should reexamine such actions to determine how their actions have affected their competitors.

Existing or contemplated discount, rebate, pricing, or other promotional allowance programs that cover 30% or more of the total U.S. market, particularly those that go back to dollar zero, apply retroactively, or allow for the claw back of credits already awarded, should be reassessed.

Agreements or programs that require or strongly encourage exclusive or bundled purchases should be reviewed.

Practices or programs that have generated multiple or significant complaints of foreclosure from customers or critical inputs should be examined.

[1] The Council will be led by the Assistant to the President for Economic Policy and Director of the National Economic Council as Chair, and includes the Secretaries of the Treasury, Defense, Agriculture, Commerce, Labor, Health and Human Services, Transportation, the Attorney General, and the Administrator of the Office of Information and Regulatory Affairs.

Judgment enforcement requires a combination of strategy, creativity, diligence, and patience. With a valid judgment in hand, what do you do next?

Assessing Collectability and Informing the Client

The collection of a judgment is a significant engagement for both an attorney and their judgment creditor client. Judgment collection requires the collecting attorney to assess the collectability of the judgment and to discuss the prospect of collection and the likely cost of collection with the judgment creditor client so the client can make well-informed decisions about collection strategies.

To avoid a dissatisfied client, any discussion about judgment collection must include a candid and realistic assessment by counsel of the various challenges inherent in the process and a recognition that having a judgment does not guarantee it will be collected, even with diligent enforcement efforts. Any candid assessment of the collectability of a judgment should include:

an assessment of available asset information and a plan to obtain further information about the existence of potential assets from which the judgment can be collected;

an analysis of the jurisdiction from which the original judgment arose (whether it is the local jurisdiction, from a sister state, or a foreign country) and any process required to cause the judgment to be enforceable in the jurisdiction in which any of judgment debtor’s located assets exist;

an assessment of the likelihood of further challenge to the validity and finality of the judgment;

the likely timeline for collection activities;

any applicable legal issues, such as applicable statutes of limitations; and

the likely cost of various collection activities, broken out by collection phase.

When preparing this analysis, counsel must also take into account a number of practical factors, including the amount of the subject judgment, the client’s willingness and ability to invest further resources in the collection process, and the client’s time horizon for recovery upon the judgment. With careful attention to these aspects of a judgment enforcement engagement, the attorney and client can formulate a clear, consensual, and preliminary collection plan that is practical based upon the circumstances and available information.

Gathering Information, Identifying Assets, and Conducting Discovery

Given the time and expense often involved in enforcing judgments, efficient asset recovery requires a targeted approach. There are often significant opportunities to gather information about the judgment debtor’s assets from third parties through domestic legal processes, even where the judgment debtor is based overseas. Gathering timely, specific intelligence about the debtor’s assets before initiating enforcement efforts is essential to combatting the myriad evasions typically employed by judgment debtors.

As an initial step, judgment creditors should attempt to identify assets of the judgment debtor located in the jurisdiction in which the judgment was entered. Such assets can be attached directly using the judgment jurisdiction’s available enforcement mechanisms. Where no assets can be readily located in the judgment jurisdiction, judgment creditors can pursue domestic judgment enforcement in state courts through the Uniform Enforcement of Foreign Judgments Act (“UEFJA”), as adopted, or in federal courts through Rule 69 of the Federal Rules of Civil Procedure and 28 U.S.C. § 1963.

Where no assets can be located domestically and reason exists to believe that the judgment debtor may own assets abroad, counsel for judgment creditors can expand their search overseas. The two primary means of procuring discovery abroad are: (a) to sue on the judgment in order to domesticate it in the target jurisdiction and then issue discovery from that proceeding; or (b) to utilize the processes of the Hague Convention on the Taking of Evidence Abroad in Civil or Commercial Matters (the “Hague Evidence Convention”). Both options present their own distinct challenges and often require retention of local counsel. Suing to register the judgment overseas often requires judgment creditors to initiate plenary proceedings, and foreign tribunals are typically reticent to recognize foreign judgments entered by default or otherwise lacking due process. Similarly, utilizing the Hague Evidence Convention can be notoriously cumbersome. Both avenues are constrained by the scope of discovery available in the target jurisdiction, which is generally significantly more limited than what is available in state and federal courts in the United States.

Given the difficulties of procuring discovery through foreign tribunals, targeting judgment debtor assets through United States banking channels can also be an attractive option. Issuing state or federal subpoenas to stateside financial institutions can often yield critical information about both domestic and foreign assets of the judgment debtor. Thanks to the centrality of the United States banking system to world financial markets, a significant portion of global financial transactions are routed through banks with footprints in the United States (read: subject to the jurisdiction of domestic state and federal courts). Accordingly, by serving carefully targeted subpoenas on such financial institutions, one can often identify crucial information regarding judgment debtors’ domestic and overseas assets, without the need to petition a foreign court.

In short, counsel must consider all available domestic and international discovery options with an emphasis on efficiently enforcing judgments and maximizing return on legal investment.

Enforcement Litigation in the United States

Domestic state and federal courts are busy, to say the least. Constitutional considerations frequently require courts to prioritize the management of criminal dockets and trials. Moreover, the practical impact of budget and resource constraints, as well as the COVID-19 pandemic, are daily considerations for prioritizing the work of the courts. The net effect can be that judgment collection and enforcement litigation may not proceed at the pace a judgment creditor would prefer.

In state courts, debt collection challenges may arise out of commercial, business or consumer transactions or, more commonly, in the collection of money judgments obtained after trial or pursuant to default judgments. Counsel must understand and be prepared to stay within the laws relating to fair debt collection practices, including key state and federal fair debt collection laws. Counsel must also understand the specific discovery tools available in the state where collection and enforcement are pursued, as well as any exemption statutes.

In federal courts, a money judgment—whether originating in the same district or registered in another district under 28 U.S.C. § 1963—is enforced by a writ of execution under Rule 69 of the Federal Rules of Civil Procedure, unless the court directs otherwise. Rule 69(a)(1) provides, however, that the procedure on execution—and in proceedings supplementary to and in aid of judgment or execution—must accord with the procedure of the state where the federal court is located, though a federal statute will govern to the extent that statute applies. With regard to discovery specifically, Rule 69(a)(2) provides that a judgment creditor may obtain discovery from any person, including the judgment debtor, as provided by the Federal Rules of Civil Procedure or by the procedure of the state where the court is located. So, a judgment creditor must take into account any federal statute that may govern, the full array of enforcement procedures and options otherwise available in the forum state, and the discovery mechanisms provided in the federal rules. In many cases involving a default judgment debtor, enforcement efforts may culminate in a motion for a finding of contempt and sanctions against the judgment debtor for failing to comply with court orders governing discovery in aid of execution. In such instances, counsel may also need to understand the requirements of 28 U.S.C. § 636 as they relate to proceedings before United States Magistrate Judges and the special procedures therein concerning contempt proceedings.

Considering that judgment collection and enforcement can be every bit as complex and challenging as the proceedings that gave rise to the judgment in the first instance, if not more, it should come as no surprise that effective judgment collection is fairly characterized as an art that necessitates a degree of mastery from practitioners.