The key challenge for regulating crypto assets is whether they can be classified as commodities or securities and, hence, whether the U.S. Securities and Exchange Commission (“SEC”) and/or the Commodity Futures Trading Commission (“CFTC”) has oversight. The collapse of FTX has highlighted the need to set clear guidelines on how the CFTC and SEC should divide the regulation of crypto assets.[1] Following the collapse of FTX, the CFTC’s chairman, Rostin Behnam, said that the CFTC had limited authority for enforcement action because it lacks direct oversight.[2] He stated the “CFTC does not have direct statutory authority to comprehensively regulate cash digital commodity markets.”[3] Behnam asked for “bills that contemplate shared responsibility for the CFTC and the SEC” so that “the SEC would utilize its existing authority and reporting regime requirements for all security tokens, while the CFTC would apply its market-based rules for the more limited subset of commodity tokens, which do not have the same characteristics as security tokens.”[4] Classification of crypto assets and subsequent regulation are important factors in the market. This article demonstrates that market participants’ classification of crypto assets as securities (or not) has been consistent with SEC and CFTC enforcement actions, with the notable exception of Ripple (“XRP”).

Ripple’s price movement following the SEC’s 2017 disclosure of the guidelines to identify crypto assets that are securities was in line with Bitcoin and Ethereum—crypto assets that the SEC has ruled are not securities.[5] Iconomi and other crypto assets with equity-like features experienced a more pronounced price decline than Ripple following the SEC’s guidelines disclosure. Despite arguments by industry participants that Ripple was “very unlikely” to be identified as a security by the SEC because “there is no expectation of profit (dividends or payouts) expected for Ripple holders,” the agency filed a lawsuit against Ripple in December 2020 for allegedly conducting an unregistered securities offering.[6] Ripple’s status as a commodity or security, and whether the SEC or industry players are correct about it, will soon be resolved as a court decision is expected soon.[7]

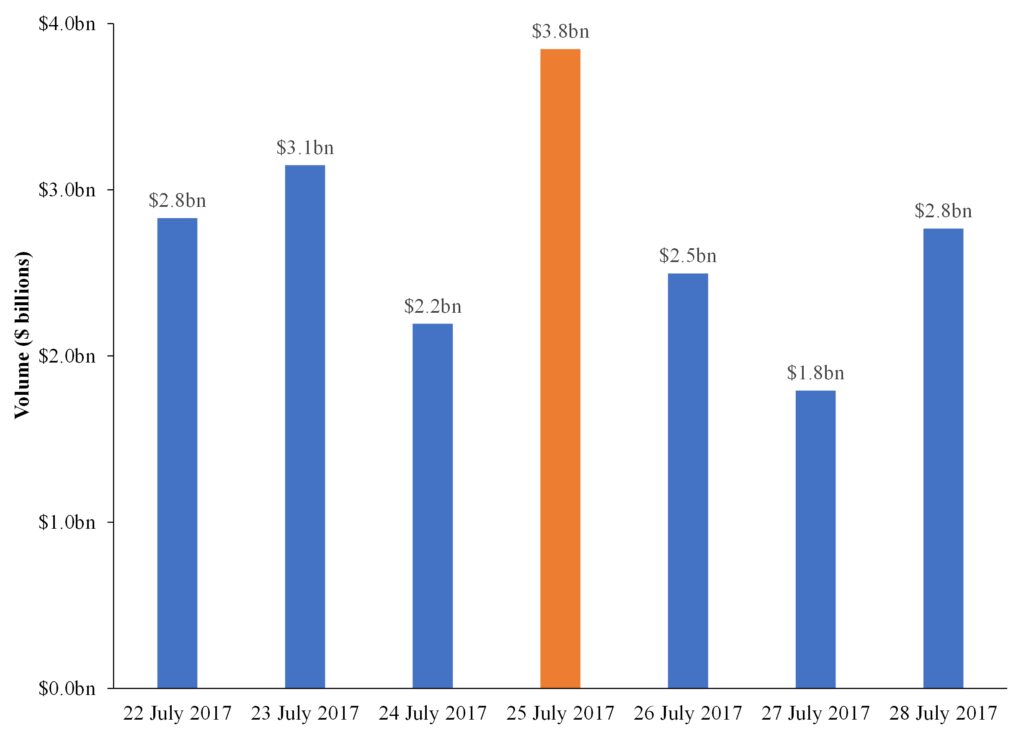

On July 25, 2017, the SEC issued an investigative report concluding that tokens sold by a decentralized autonomous organization that used blockchain technology were securities (“the DAO report”). The DAO report identified for the first time a crypto asset as a security and outlined the factors the agency would consider in determining whether crypto assets are securities. In the DAO report, the SEC stated that a key feature of a security is being an investment of money in which the investor has an expectation of profits based on the efforts of others regardless of whether the securities “are distributed in certificated form or through distributed ledger technology.”[8] The release of the DAO report had a notable impact on the crypto market, which we examine in this article to compare the regulatory decisions to the views of market participants regarding the classification of the crypto assets. The figure below presents the volume of crypto assets trading in the days immediately before and after the DAO report was issued. Daily trading volume increased from $2.2 billion the day prior to the report disclosure to $3.8 billion the day that the report was released, about a 75% increase.

Volume of Crypto Trading Following the Release of the DAO Report

The impact of the DAO report on the prices of crypto asset differed in that some prices remained stable while others dropped by more than 20% in a single day. In the discussion that follows, we demonstrate that the price of crypto assets reacted to the DAO report in a manner consistent with the market’s views about the type of crypto asset at issue. That is, the prices of certain crypto assets dropped notably for tokens that were viewed by market participants as likely to be securities, while the reaction of other assets was less noticeable or completely absent.

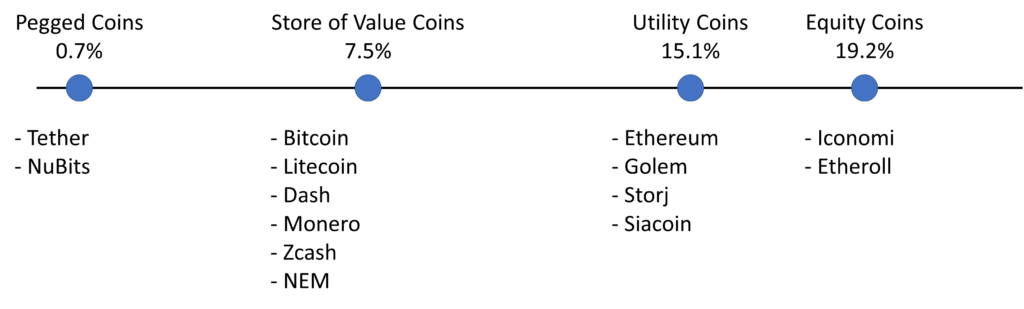

In analyzing market views regarding the classification of the crypto assets, we relied on two articles by Steemit, among other sources. The 2017 Steemit article “Is Your Crypto Digital Gold, Gas, or Something Else?” classified several crypto assets into four categories: pegged coins, store of value coins, utility coins, and equity coins.[9] We examined the crypto assets considered in the Steemit article and their classification to examine the price reaction to the DAO report on various crypto assets. The prices for crypto assets identified as pegged coins remained stable. Pegged coins are crypto assets that aim to peg their market value to some other assets, including the US dollar or the price of gold.[10] The prices for crypto assets identified as equity coins declined by about 20% following the DAO report. Equity coins are crypto assets that grant ownership rights to the token holders from profits generated by a project or product.[11] Iconomi is an example of a crypto asset identified as an equity coin, based on its white paper, which asserts that “ICN tokens represent ownership of the ICONOMI platform, allowing their holders to receive dividends and vote on ICONOMI related issues.”[12] Price declines for crypto assets that are considered to be store of value or utility tokens were not as pronounced. The purpose of store of value coins is to serve as a medium for transactions.[13] Utility coins are meant to offer additional network utility by providing access to resources to build block-chain-based applications or to execute smart contracts or provide access to remote computing power.[14]

The figure below presents the average price decline on the date that the DAO report was released across all crypto assets which were classified in the Steemit article. It is unlikely that pegged coins and store of value coins would be classified as securities “given their strong currency-like characteristics,” and “it is equally apparent” that equity coins are securities.[15] The Steemit article stated that it is less clear whether utility coins are securities or not.[16] The price decline of the coins classified as utility coins following the DAO report is consistent with the market’s view on the classification of the crypto assets. The average price decline was only 0.7% for the pegged coins and 7.5% for store of value coins, but it was 15.1% for utility coins and 19.2% for equity coins.

Price Decline Following the Release of the DAO Report by Type of Crypto Asset as Classified by the Steemit Article

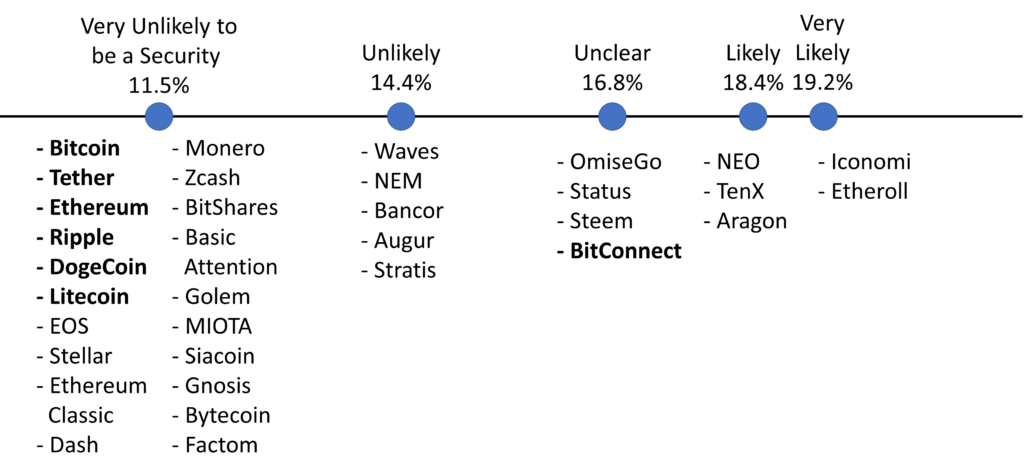

A second 2017 Steemit article, “Which Cryptocurrencies Will Be Regulated by the SEC/CFTC?” categorized a larger set of crypto assets as very unlikely, unlikely, unclear, likely, and very likely to be classified as securities per the SEC.[17] The figure below presents the average price decline on the date that the DAO report was released across all rating categories established in the second Steemit article. The price decline following the DAO report is again consistent with the market’s view on the likelihood of crypto assets being classified as securities by the SEC. The price decline was 11.5% for crypto assets classified as very unlikely to be deemed securities, 14.4% for unlikely, 16.8% for unclear, 18.4% for likely, and 19.2% for very likely.

Differences in Price Decline Following the Release of the DAO Report as Classified by the Steemit Article

The figure above lists the crypto assets under each rating category as identified in the second Steemit article. We identify in bold the subset of crypto assets that were later included in an enforcement action by the CFTC or the SEC. Bitcoin, Tether, Ethereum, DogeCoin, and Litecoin were included in enforcement actions by the CFTC, which oversees commodities and derivatives. Each had been classified by the Steemit article as very unlikely to be deemed securities.

Ripple and BitConnect were included in enforcement actions by the SEC, which oversees securities.[18] While BitConnect was given an unclear rating by the second Steemit article, Ripple received a very unlikely chance of being classified as a security by the SEC. Regarding BitConnect, the Steemit article stated:

It’s somewhat difficult to find information on how this coin works. We have not been able to find a white paper describing it. We suspect it would be considered a security as its purpose is to earn interest by paying it back to BCC developers, but it is very unclear.[19]

Regarding Ripple, the Steemit article said, “At this time there is no expectation of profit (dividends or payouts) expected for Ripple holders. It is used as a value holder for transactions in the Ripple ecosystem.”[20]

Conclusion

Since the DAO report release, the CFTC and SEC have conducted numerous enforcement actions. The agencies’ decisions on whether particular crypto assets were securities have been generally consistent with the market price reaction of the crypto assets following the DAO report with the notable exception of Ripple. Following the DAO decision, the market classified Ripple as “very unlikely” to be considered a security, and its price movement was in line with other crypto assets that were not considered securities using the same market classification, including Bitcoin and Ethereum.[21] Nevertheless, on December 22, 2020, the SEC charged Ripple with conducting a $1.3 billion unregistered securities offering. [22] The SEC argued there was no significant use for Ripple other than as an investment. The agency argued that the first potential use Ripple claimed for the token—to serve as a universal digital asset for banks to transfer money—never materialized. The SEC further argued that to date, the only product that permits Ripple use for any purpose is on-demand liquidity (“ODL”). ODL allows for cross-border payments to be settled in seconds, not days.[23] The SEC claimed, however, that ODL has gained little traction and that “ODL transactions comprised no more than 1.6% of XRP’s trading volume during any one quarter.”[24] The SEC has repeatedly clarified that “merely calling a token a ‘utility’ token or structuring it to provide some utility does not prevent the token from being a security.”[25] Both Ripple and the SEC submitted reply briefs in the ongoing lawsuit on December 2, 2022, and a court decision nears regarding whether Ripple can avoid the lawsuit.[26]

As more information is disclosed about the various crypto assets, one can examine the price reaction to regulatory and litigation rulings to evaluate the likelihood that assets will be classified as securities, as reflected by the views of market participants.

The authors are with NERA Economic Consulting. The views in this article represent those of the authors and not NERA. Please do not cite without permission from the authors.

Fran Velasquez, Former SEC Official Doubts FTX Crash Will Prompt Congress to Act on Crypto Regulations, COINDESK, Nov. 16, 2022. ↑

Why Congress Needs to Act: Lessons Learned from the FTX Collapse: Hearing Before the S. Comm. on Agric., Nutrition, & Forestry 117th Cong. (Dec. 1, 2022) (testimony of Rostin Behnam, Chairman, Commodity Futures Trading Comm’n). ↑

Id. ↑

Id. ↑

William Hinman, Dir., Div. of Corp. Fin., Sec. & Exch. Comm’n, Remarks at the Yahoo Finance All Markets Summit: Crypto: Digital Asset Transactions: When Howey Met Gary (Plastic) (June 14, 2018). ↑

Basic Crypto, Which Cryptocurrencies Will Be Regulated by the SEC/CFTC?, STEEMIT, Aug. 14, 2017; Complaint, Sec. & Exch. Comm’n v. Ripple Labs Inc., Case No. 1:20-cv-10832 (S.D.N.Y. Dec. 22, 2020). ↑

Jessica Corso, SEC, Ripple Issue Final Salvos As Crypto Decision Nears, LAW360, Dec. 5, 2022. ↑

Press Release, Sec. & Exch. Comm’n, SEC Issues Investigative Report Concluding DAO Tokens, a Digital Asset, Were Securities (July 25, 2017). ↑

Basic Crypto, Is Your Crypto Digital Gold, Gas, or Something Else?, STEEMIT, Aug. 12, 2017. ↑

Id. ↑

Id. ↑

Id. ↑

Id. ↑

Id. ↑

Adrian Parlow, Securities Liability and the Role of D&O Insurance in Regulating Initial Coin Offerings, 167 U. PA. L. REV. 211, 223 (2018). ↑

Basic Crypto, Which Cryptocurrencies Will Be Regulated by the SEC/CFTC?, STEEMIT, Aug. 14, 2017. ↑

Id. ↑

Complaint, Sec. & Exch. Comm’n v. BitConnect, Case No. 1:21-cv-07349 (S.D.N.Y. Sept. 1, 2021). ↑

Basic Crypto, Which Cryptocurrencies Will Be Regulated by the SEC/CFTC?, STEEMIT, Aug. 14, 2017. ↑

Id. ↑

The Ripple price dropped by 8.7% following the DAO report, similar to the 7% decline for Bitcoin and the 9.7% decline for Ethereum and less pronounced than the 23.2% price decline for Iconomi. While Iconomi was deemed an equity coin by the Steemit article, Bitcoin was categorized as a store of value coin, and Ethereum was identified as a utility coin that also has store of value coin features. ↑

Jessica Corso, SEC, Ripple Issue Final Salvos As Crypto Decision Nears, LAW360, Dec. 5, 2022. ↑

Cross-Border Payments: Settlement in Seconds, Not Days, RIPPLE (last visited Dec. 29, 2022). ↑

Complaint, Sec. & Exch. Comm’n v. Ripple Labs Inc., Case No. 1:20-cv-10832 (S.D.N.Y. Dec. 22, 2020). ↑

The Roles of the SEC and CFTC: Hearing Before the S. Committee on Banking, Hous., & Urb. Affs. 115th Cong. (Feb. 6, 2018) (testimony of Jay Clayton, Chairman, Sec. & Exch. Comm’n). ↑

Id. ↑