To mark the forty-year anniversary of the Business Law Section’s Mergers & Acquisitions (“M&A”) Committee, Ann Beth Stebbins, one of the cochairs of the Committee’s Acquisitions of Public Companies Subcommittee, reflects on developments in public company M&A in the last forty years.

The Transformational Impact of the Revlon Decision

In October 1986, the Delaware Supreme Court issued its opinion in Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc., defining the duties owed to shareholders when a board determines to sell a company. Revlon came on the heels of several seminal Delaware decisions in 1985, most notably Smith v. Van Gorkom and Unocal Corp. v. Mesa Petroleum Co., which focused on defensive measures a board could reasonably adopt to address perceived threats to corporate policy. The Revlon decision established a critical limitation on the board’s ability to implement defensive measures once the sale or breakup of a company is inevitable, with the board’s role shifting from defender of corporate policy to that of an auctioneer charged with securing the best price reasonably available for shareholders. Revlon imposes enhanced scrutiny on board conduct in a sales context, and directors must demonstrate that they acted to obtain the highest value reasonably available for shareholders.

The Revlon decision ushered in the modern era of M&A practice, with a focus on process design and board conduct. Following Revlon, market practice evolved to include competitive auctions, an increased reliance on financial advisers to identify interested buyers and assist in price negotiations, and procedural safeguards such as special committees to insulate a process from conflicts. Since Revlon, deal protections have become a focal point of merger agreement negotiations, with buyers pressing for terms that secure deal certainty while target boards must justify that deal protections do not impede competitive offers that could result in greater value for shareholders. Revlon also spawned a flood of fiduciary duty litigation focused on process and whether a board had satisfied its duty to obtain the highest value reasonably available for shareholders. The litigation landscape prompted more formalized board processes, as well as extensive disclosure of merger negotiations and board deliberations.

The Globalization of M&A Activity

Beginning in the 1990s, strategic buyers ramped up geographic expansion on a global scale through cross-border M&A. The privatization of state-owned assets and deregulation in sectors such as telecom, utilities, and airlines created more cross-border targets. Trade liberalization and regional integration, including the formation of the European Union, the North American Free Trade Agreement, and the Association of Southeast Asian Nations, reduced barriers for foreign buyers and liberalized inbound and outbound investment. Many companies pursued a multinational M&A strategy to achieve scale, global market access, local distribution channels, and supply chain diversification. Law firms and investment banks expanded their global capabilities to structure and negotiate multijurisdictional deals, which often involved complex legal, regulatory, and tax issues. Cross-border M&A activity has been cyclical during the period, reflecting macroeconomic conditions, interest rate and foreign exchange fluctuations, and geopolitical shifts. Deal activity in recent years has been influenced by government priorities, balancing cross-border investment with national interests.

The Regulatory Environment

Global regulatory regimes have become an important part of the M&A landscape. The rise of national security and foreign investment screening has been a significant trend over the past few decades. Governments across the globe have broadened the scope of reviews and are applying stricter approval standards, especially in sectors involving technology and personal data. The expansion of the Committee on Foreign Investment in the United States and the proliferation of similar international regimes have lengthened transaction approval timelines, imposed conditional remedies, and introduced deal uncertainty.

Antitrust scrutiny has also intensified. Following years of antitrust enforcement based on a “consumer welfare” framework, U.S. regulators adopted a more aggressive posture in the last decade, scrutinizing transactions in the technology sector, introducing new theories of competitive harm, and litigating to block transactions. The regulatory agencies have recalibrated their priorities under the Trump administration and are generally viewed as taking a more pragmatic approach to mergers; however, high-profile transactions may draw attention from politicians on the state and national levels. Disclosure obligations have increased dramatically, with filings requiring extensive document production, expanded narrative explanations, and granular line-item detail. Sophisticated merger control regimes have developed worldwide, and global cooperation has intensified, beginning with the centralization of EU merger control in the 1990s. Competition authorities routinely share information and coordinate challenges; however, differing timelines, remedies, and outcomes may complicate deal execution. Multijurisdictional planning and coordination have become essential to successful completion of a transaction.

The Rise of Private Equity

Private equity was a niche alternative asset class forty years ago. It is has grown to be a huge financial pool, fueled by investment from pension funds and sovereign wealth endowments. Private equity has become a driver of deal volume, and sponsors are active buyers of public companies in large take-private transactions, as well as carve-out sales from strategic sellers. From its genesis in the 1980s in highly leveraged hostile takeovers (e.g., KKR’s takeover of Nabisco), private equity has adopted an operational focus. The private equity playbook continues to feature debt financing, cost rationalization, and exit via a sale or initial public offering; however, the model has evolved from financial engineering to value creation, with private equity owners driving growth organically and through add-on acquisitions. Private equity sponsors continue to use leverage to finance their M&A activity; however, the sources of leverage have evolved to include private credit and direct lending, with covenant-lite debt available in certain cycles.

Expansion of Shareholder Activism

Activist hedge funds, with professional teams and dedicated capital, began appearing in the late 1990s and have become an important driver of M& A activity. It is now common practice for activists to publicly or privately push boards to initiate a sales process, break up a company, or spin off a business unit, employing diverse tactics such as board campaigns, shareholder proposals, and media efforts. Activists may advocate for transformational deals or divestment of noncore businesses to unlock value.

Installing directors aligned with its M&A strategies increases the likelihood of the activist’s desired transaction being approved and executed. The introduction of the universal proxy card, which allows shareholders to use a single ballot at a contested meeting to mix and match director candidates, has had the practical effect of lowering the cost for an activist to elect its nominees and increases the probability that the activist will win some board seats in furtherance of its agenda. Companies targeted by an activist often enter into settlement agreements that provide the activist with one or more board seats to avoid a costly proxy fight. Activists often seek the support of institutional investors, which are less likely to agitate on their own but wield significant influence because of their size and voting power.

To mark the forty-year anniversary of the Business Law Section’s Mergers & Acquisitions Committee, Samantha Horn and Bianca Levin-Soler, cochairs of the Committee’s Private Equity M&A Subcommittee, reflect on developments in private equity M&A in the last forty years.

Over the last forty years, private equity has evolved from an upstart “corporate raider” model into a dominant force in global capital markets, with global assets under management growing to over $9 trillion as of 2025. This growth has been driven by a shift from pure financial engineering to operational value creation, fueled by structural macroeconomic, regulatory, and market trends. Certain practice changes and legal developments have contributed to the incredible growth in private equity M&A activity.

Affordable Credit

On a macroeconomic level, the cost and availability of debt financing have significantly influenced private equity dealmaking levels. Interest rates remained consistently low from 2009 to 2022, making debt significantly less expensive. Consequently, the use of borrowed money was a key driver of acquisitions by private equity firms. Through the use of debt financing, a fund could carry out many more M&A transactions while committing significantly less of its own capital to each deal by leveraging the remainder with debt, often in the range of five to six times EBITDA (earnings before interest, taxes, depreciation, and amortization).

In addition to the low cost of borrowing, the proliferation of a wider range of debt providers, including not only traditional banks but also nontraditional private capital debt investors, has allowed for larger, more diversified, and more sophisticated leveraged buyouts.

Decrease in Public Company Listings

Due to volatility in the public markets and the availability of capital in the private equity ecosystem, the number of public companies has approximately halved over the past twenty years as the market increasingly turns to private equity firms and pension funds to provide an exit or a path to liquidity. In the past, a strategic M&A transaction or an initial public offering were the most common exit options. With a more robust and diversified private equity market, many companies choose not to go public in order to avoid the significant expense and scrutiny of being publicly listed.

In addition, we now see longer hold periods for investments (hold periods are on average over six or even seven years at present); and in transactions held by pension funds, hold periods can sometimes be significantly longer, sometimes reaching ten years or more.

Expansion in Private Equity Investment

The amount of capital dedicated to private equity has steadily increased over the last four decades as a result of a significant positive return history, a growing number of private companies in which to invest (as discussed above), and the proliferation of various additional players in the private equity ecosystem—including sovereign wealth funds, endowments, high-net-worth individuals, and family offices. In addition, the more traditional private equity investors such as pension funds have steadily increased their allocation to the private equity asset class. Certain private equity funds also went public, allowing an even more diversified group of investors to enter the private equity market.

Representation and Warranty Insurance Products

The introduction of representation and warranty insurance (“RWI”) products in the 2000s also provided an advantage to both buyers and sellers of companies in an already frothy sell-side market by allowing sellers to reduce or eliminate exposure for post-closing indemnity claims and escrowed funds. This was of particular importance to private equity sellers, who prefer to be able to distribute all funds from a sale immediately after closing to their limited partners, and was particularly important in late-stage funds that may otherwise have had long escrow periods due to the fact that a fund’s assets were minimal at the end of the fund’s life.

In addition, RWI allowed for the preservation of relationships with the sellers, who are often involved in managing the business after closing, by removing or limiting the potential for indemnity claims against them and moving the liability for those claims to an insurance company. This often has the added effect of making negotiations of representations and warranties and indemnities less contentious.

Conclusion

The incredible growth in the private equity M&A space has many contributors and sources, but some of the most influential include the availability of affordable credit on beneficial terms, the increase in allocation to this asset class, the expansion of the group of investors investing in this asset class, and the introduction and widespread adoption of RWI.

In successful societies, the link between legal institutions and economic performance is undeniable. The rule of law and an independent judiciary form the bedrock upon which thriving economies are built. For businesses, these legal foundations provide the stability, predictability, and fairness necessary to operate and grow. Around the globe, countries that uphold these principles tend to experience greater investment, innovation, and prosperity. Conversely, where the rule of law is weak or judicial independence is compromised, economic stagnation, corruption, and instability often follow.

This article explores how the rule of law and judicial independence are indispensable to business success and economic development, which, in turn, contribute to an environment in which individuals can pursue their version of the American Dream.

Understanding the Rule of Law and Judicial Independence

Before exploring the importance of the rule of law and judicial independence for business and economics, it is helpful to explain these concepts.

The Rule of Law

The World Justice Project—a leading independent, nonprofit organization that has for nearly twenty years worked to advance the rule of law around the world—states the rule of law is “a durable system of laws, institutions, norms, and community commitment that delivers four universal principles: (1) accountability, (2) just law, (3) open government, and (4) accessible and impartial justice.”

So, what do these four principles really mean?

“Accountability” means that the government and private actors are all accountable under the law.

“Just Law” refers to the fact that laws are clear, publicized, stable, and applied evenly.

“Open Government” means that the processes for adopting, administering, adjudicating, and enforcing the laws are accessible, fair, and efficient.

“Accessible and Impartial Justice” means that justice is delivered timely by competent, ethical, and independent officials who are respected by and can identify with the communities they serve.

It is not difficult to understand that the failure of a legal system to have any of these attributes could lead to distrust in the system.

Judicial Independence

Judicial independence is an essential part of the rule of law because it ensures that the court system operates free from undue influence from powerful interests, such as the executive or legislative leaders or well-funded private interests. Independent judges can make rulings based solely on the law and facts, not political pressure or bribery.

Together, these elements create a legal environment where business can function without fear of arbitrary interference, and where economic disputes are resolved fairly and efficiently.

As retired U.S. Supreme Court Justice Anthony Kennedy said, “Judicial independence is not conferred so judges can do as they please. Judicial independence is conferred so judges can do as they must.”

Business Success Depends on the Rule of Law and Judicial Independence

Practically all economic activity depends on the rule of law because it allows people and companies to rely on the fact that they can invest, build, buy, or sell without improper interference or violating agreements or rights.

1. Legal Certainty and Predictability

Businesses depend on clear, consistent rules. The rule of law ensures that laws are applied consistently over time and that companies can plan their operations, investments, and contracts accordingly. From standardized weights and measurements of the smallest items to anticorruption regulations of the largest, law undergirds it all. Without this predictability, businesses face heightened risk and uncertainty.

In the United States, for example, companies rely on long-standing statutes and legal precedents when entering into contracts or assessing liability risks. Investors are more likely to fund ventures in jurisdictions where they can anticipate the legal consequences of their actions and have confidence in dispute resolution mechanisms.

2. Enforceable Contracts

A fundamental requirement for business is the ability to form and enforce contracts. Without the assurance that contracts will be upheld by courts, market transactions become unreliable.

Judicial systems that can swiftly and fairly enforce contracts encourage both domestic and international investment.

For instance, in the United States, the Uniform Commercial Code (“UCC”) provides a standardized legal framework for commercial transactions across state lines, further enhancing trust and reducing transactional friction.

3. Protection of Property Rights

The rule of law also ensures secure property rights, which are essential for businesses and entrepreneurs. Clear legal protections, whether they secure physical property, intellectual property, or shares in a company, incentivize investment and innovation.

An independent judiciary is crucial in resolving disputes over ownership or infringement. In the United States, the judiciary plays a vital role in protecting patent rights, trademarks, and copyrights—key drivers of the innovation economy.

Countries with weak property rights often struggle to attract capital or support entrepreneurial ventures. Investors are hesitant to commit resources where expropriation or arbitrary seizure are a threat.

4. Anti-Corruption and Fair Competition

Corruption undermines market fairness and deters honest competition. When bribes or political connections are needed to secure licenses, win contracts, or resolve disputes, efficient and fair markets collapse.

An independent judiciary can check corruption by holding officials accountable and ensuring that laws are applied impartially.

The Economic Benefits of the Rule of Law and Judicial Independence

Not only do societies with strong rule of law traditions and independent judiciaries create an atmosphere of economic freedom for their own citizens, but the stability of these systems also attracts investment from around the world.

1. Attraction of Foreign Direct Investment

One of the clearest links between the rule of law and judicial independence and economic development is foreign investment. Investors from abroad typically seek countries where their investments will be protected by a stable and impartial legal system.

In countries like the United States, the credibility of the legal system is a major draw for foreign capital. Investors know that if disputes arise, they can turn to a fair, professional court system.

Conversely, in jurisdictions where people perceive the judiciary as biased or beholden to political authorities, foreign direct investment (“FDI”) tends to be lower, even if other economic indicators appear favorable.

2. Support for Entrepreneurship and Innovation

A fair legal system is crucial for startups and entrepreneurs, who often lack the resources to navigate informal systems or secure “favors.” Independent courts offer a venue for smaller actors to defend their rights against larger competitors or government overreach.

Furthermore, robust legal protections for intellectual property, contracts, and business operations enable innovation by ensuring that innovators can profit from their ideas.

Global leadership of the United States in technology and entrepreneurship is partially attributable to its well-developed legal system that protects innovation through enforceable patents, copyrights, and antitrust laws.

3. Lower Transaction Costs

When legal institutions are effective and impartial, businesses spend less time and money on enforcement, negotiation, and risk management. This efficiency improves overall productivity and reduces the costs of doing business.

Imagine a scenario where every contract needs personal guarantees or backup arbitration because the courts are unreliable. These additional layers of cost and complexity can deter smaller firms and inflate costs for larger ones. Independent courts reduce these burdens by providing a reliable dispute resolution mechanism. (Think about how this works in your own life. How often do you read every word of any agreement you might sign—such as for a credit card or other legal paperwork? People usually breeze past them on the assumption that everything included is fairly standard legal language that is not going to result in disaster for the consumer—although that can happen.)

Global Challenges to Judicial Independence and Rule of Law

Despite their importance, both the rule of law and judicial independence are under threat in various parts of the world—including, at times, in the United States. Recent reports from the World Justice Project highlight a concerning trend: rule of law has entered its eighth straight year in decline. Such erosion threatens to destabilize economies, diminish trust in government, and undermine basic human rights. As geopolitical tensions escalate, the need to strengthen the rule of law is increasingly urgent to safeguard a just and stable future.

One important initiative that is underway to combat the decline in the rule of law and to support the resilience of an independent judiciary is the Judicial Fellowship Program hosted by the U.S. Chamber of Commerce Foundation in partnership with the Presidential Precinct. Through this fellowship program, judges and magistrates from around the world are brought to the United States for a two-week professional exchange and residential learning experience designed to strengthen the legal systems in foreign countries by building a cadre of judicial leaders from around the world.

Political Interference

The executive and legislative branches of governments may attempt to influence court decisions through appointments, funding threats, or direct intimidation. The U.S. Constitution has enshrined separation of powers among the branches of the government, and weakening that separation can undermine public trust and discourages both domestic and foreign investment.

Overloaded or Underfunded Court

Even without overt interference, courts that are underresourced or inefficient can become bottlenecks for economic development. Delayed justice or complex bureaucratic procedures increase the cost of legal recourse. Similarly, judges who fear retribution by leaders or members of the public may not be able to render justice fairly.

Corruption

In some systems, bribery or cronyism can distort judicial outcomes. When judges are beholden to wealthy or powerful patrons, it erodes public confidence in the system and deters honest businesses from entering or staying in the market. Maintaining judicial independence requires constant vigilance, robust legal and ethical safeguards, and a culture that respects institutional integrity.

Conclusion: Legal Institutions as Economic Advantages

The rule of law and judicial independence are not abstract ideals; they are practical necessities for economic development and business success. Just as roads, power grids, and digital networks support economic activity, so, too, does a trustworthy legal system. It creates an environment where contracts are honored, property is secure, innovation is rewarded, and disputes are fairly resolved.

In the United States, these legal foundations have helped create one of the world’s most successful and resilient economies where individuals are free to pursue their version of the American Dream. Globally, the same pattern holds: countries that invest in their legal institutions attract more capital, nurture more innovation, and experience more stable growth.

As businesses become increasingly global and interconnected, the need for impartial, effective legal systems becomes even more critical. Policymakers, investors, and entrepreneurs alike must recognize that the health of a nation’s judiciary is not just a matter of justice: it is a matter of economic survival and prosperity.

* * *

Note: Law Day is an annual commemoration, held on May 1, to reflect on the rule of law and its importance. The 2026 Law Day theme is “The Rule of Law and the American Dream.” It focuses attention on how the rule of law—the idea that no person is above the law—ensures the rights of the people to live their lives as freely as possible and to pursue the American Dream. This essay launches a conversation on this theme, and the American Bar Association invites people to visit lawday.org to find more resources and information about 2026 Law Day programs and activities.

This article is part of a series on the rule of law and its importance for business lawyers created by the American Bar Association Business Law Section’s Rule of Law Working Group. Read more articles in the series.

To mark the forty-year anniversary of the American Bar Association Business Law Section’s Mergers & Acquisitions Committee, Emily Marco, vice chair of the Women in M&A Subcommittee, reflects on the rise of women in M&A in the last forty years.[1]

There is a saying that by small means, great things can come to fruition. Leigh Walton (Bass, Berry & Sims; Nashville, TN), who served as the first female leader of the Mergers & Acquisitions Committee, can attest to this. When a male partner at her firm could not attend an ABA conference in 1986, she attended in his place. She then found herself discussing the need for practice-oriented guidance for M&A practitioners as part of the ABA Business Law Section. More than two decades later, Walton became the first woman vice chair and then the first woman chair of the M&A Committee.

As John Clifford noted in the article The Mergers & Acquisitions Committee—40 Years On, women have historically been underrepresented in the field of M&A, including within the M&A Committee itself. He explained that “[w]omen have participated in the M&A Committee from its beginning and have held important leadership positions, although the number of women lawyers who actively participated often has been small.”

At the close of Walton’s tenure as chair of the M&A Committee in 2012, Jen Muller (Houlihan Lokey; San Francisco, CA), became the second woman vice chair of the M&A Committee. One enduring initiative was launched shortly thereafter: the Women in M&A Task Force, which set out to evaluate female engagement in M&A. Together, Walton and Muller led the task force until Rita-Anne O’Neill (Sullivan & Cromwell; Los Angeles, CA) (who today is the current chair of the M&A Committee), succeeded Walton. Muller and O’Neill then became the founding co-chairs of the Women in M&A Subcommittee, established in 2013 to focus on increasing the level of participation and retention of women in M&A.

Through its work, the Women in M&A Subcommittee furthers women’s involvement in M&A and enhances opportunities at the top of the deal team.

Early Exposure and Engagement Act as Catalysts for Women’s Advancement in M&A

The Women in M&A Subcommittee began to conduct biennial studies in 2014 to more deeply assess the gender disparity in M&A and create a baseline on which to measure improvements going forward. The studies measure the composition of lawyers at each level within top law firms in North America, both in corporate groups and in M&A specifically. The early Women in M&A surveys identified, as expected, that across all disciplines, including M&A, the percentage of women decreases as the role becomes more senior. But what was interesting is that the participation of women was lower in M&A from the outset. This caused the Women in M&A Subcommittee to investigate the experience women have during law school and prompted the creation of the subcommittee’s Law School Initiative. This initiative brings senior women M&A practitioners to law schools to speak about their experience in M&A and encourage women to participate in the field, among other efforts. Encouragingly, the studies have shown that from 2014 to 2024, the percentage of M&A lawyers who are women increased from 27 percent to 37 percent. The involvement of women in the M&A Committee has risen in tandem.

Ultimately, as argued by legal scholar Afra Afsharipour, “[u]nderstanding, documenting, and disclosing the gender disparity in leadership in M&A beyond the board is critical for increasing accountability and for determining the solutions that may work to reduce such disparities.”[2] And for the Women in M&A Subcommittee, the “small means” that can lead to great things include providing early exposure to M&A. The knock-on effects of this early and ongoing engagement are shown to result in the participation and retention of women in M&A.

Women’s Involvement in the M&A Committee Is a Lever for Change

The evolution of women’s participation in the M&A Committee has become a powerful lever for change, both within the profession and in the broader market. As the field of M&A has historically been dominated by men, the increasing visibility and leadership of women in the ABA M&A Committee has helped to challenge entrenched biases and open new pathways for advancement.

Research consistently demonstrates that gender bias—both explicit and implicit—remains a significant barrier to women’s advancement in M&A leadership. This bias manifests in a variety of ways, from the types of assignments women receive to the opportunities for client exposure and leadership roles. For example, as described by Afsharipour, “[w]omen are often assigned support work while men are given the plum assignments that further enhance their leadership and client connections.”[3]

Empirical data further underscores these disparities. Women are more likely to be in the third, fourth, or fifth positions on deal teams (comprising 28–32% of those roles) while their representation in the top spot is just 19%, and in the second spot, 23%.[4] This pattern reflects both the persistence of gendered expectations and the structural barriers that limit women’s access to the most visible and influential positions on major transactions.

Involvement in the M&A Committee offers visible leadership opportunities that can accelerate the advancement of women practitioners. This dynamic is especially important given that, as Afsharipour notes, “much of M&A practice and advancement seems to rely on social contacts and client development norms that perpetuate the exclusion of women and people of color from leadership in practice.”[5]

Jessica Pearlman (K&L Gates; Seattle, WA), vice chair of the M&A Committee, reflected on the transformative impact of her involvement with the M&A Committee:

I’ve been coming to the M&A Committee meetings since I was a third-year associate. So, it’s been a part of my now 26+ year career since almost the very beginning. As an associate, the exposure to the thought leadership of the Committee kept me up to date on the latest in M&A practice; since then, the M&A Committee has provided me with countless opportunities to be part of that thought leadership, not only at M&A Committee meetings but also through panels at top law schools and through publications (such as my interview of Marty Lipton[6] that was published in the 75th anniversary volume of The Business Lawyer[7]). And I’m not a one-off; this is the experience of women in M&A who not only join the M&A Committee but attend the meetings. Women in M&A often do not get the same benefit of the doubt as their male counterparts that they truly know what they are doing; the opportunities provided by the M&A Committee can bridge that perception gap.

Pearlman’s sentiments are shared by other Women in M&A Subcommittee leaders and members. Visible leadership is a core focus of the subcommittee.

Women Dealmakers Are Paving the Path for the Future

As the number of women in visible leadership positions in M&A increases, it creates a virtuous cycle where, through mentorship and sponsorship, the path to leadership becomes more attainable. Current M&A Committee Chair O’Neill selected Pearlman, Charlotte May (Covington; Washington, DC) and Jenny Hochenberg (Freshfields; New York, NY) to serve as her vice chairs of the M&A Committee. Prior to assuming the chair role, Rita-Ann was vice chair of the Committee, along with Pearlman and Patricia Vella (Morris, Nichols, Arsht & Tunnell; Wilmington, DE). All of these women dealmakers are also leading landmark deals. These women M&A leaders set new standards for practice and demonstrate the value of diverse perspectives in high-stakes negotiations.

Reflecting on the progress made since co-founding of the Women in M&A Subcommittee, Muller explained, “Early in my career, it was often notable simply to be a woman in the room. Today, that reaction is far less common—the focus has shifted to the quality of advice and leadership, not who is delivering it. That progress reflects the sustained efforts of many men and women to address the underrepresentation in the field, and while it’s not complete, it has meaningfully reduced the noise and allowed women to be more effective and fully heard.” This shift continues to benefit rising M&A leaders of all genders.

Walton’s journey—from stepping in for a male colleague at an ABA conference to becoming the first woman chair of the M&A Committee—illustrates how early exposure and a willingness to seize an opportunity grew into a legacy of leadership, connection, and inspiration. Her path is a powerful reminder that by opening doors for women in M&A today, we are building a generation of future women leaders.

Emily thanks the chairs of the Women in M&A Subcommittee, Joanna Lin (Dechert; Dallas, TX) and Charlotte May (Covington; Washington, DC), for their review and helpful comments on earlier drafts of this article. ↑

Afra Afsharipour, Women and M&A, 12 U.C. Irvine L. Rev. 359, 418 (2022). ↑

When the founders of the Mergers & Acquisitions Committee first gathered four decades ago, M&A was very different. To mark the forty-year anniversary of the Business Law Section’s M&A Committee, Daniel Rosenberg, chair of the Committee’s Technology in M&A Subcommittee, surveys how technology has reshaped M&A, bringing us to the start of a new technology revolution arguably as significant as all previous ones combined.

Late 1980s

In the second half of the 1980s, M&A was largely analog. Drafting was migrating from typewriters to early word processors, enabling lawyers to produce longer, more complex agreements. Documents were assembled manually from precedents in physical binders. Communications were dominated by phone and fax. Fax machines accelerated document circulation, but document comparison involved reading documents aloud and redlining with pens and rulers. Data rooms were literally rooms with binders, disclosure exercises involved manual cross-referencing, and closings were compiled in physical binders.

1990s

Email’s widespread adoption sped up deals as drafts could be circulated more quickly. Microsoft Office became standard, and document comparison software emerged. The first generation of knowledge management took shape, with digital precedent banks and clause libraries enabling quicker assembly of tailored documents. While diligence remained largely physical, scanned documents on CD-ROMs began to appear. Mobile phones became ubiquitous, though closings still relied on wet-ink signatures and couriered signature pages.

Early 2000s

Virtual data rooms (“VDRs”) matured, allowing sellers to run auctions with multiple bidders reviewing in parallel. PDFs and scanning became routine, with documents digitized to facilitate parallel workstreams. Electronic filing emerged at registries and regulators, reducing timetables. Document management systems became core law firm infrastructure, with more sophisticated matter management and e-billing systems giving clients greater visibility on work in progress and spend. Closing checklists and signing agendas became formalized and maintained electronically. E-signatures started to appear but remained niche due to regulatory uncertainty, with closings still relying on wet-ink and courier packs.

2010s

The 2010s consolidated a shift to cloud-based collaboration, accelerated by air travel disruption from the 2010 Eyjafjallajökull ash cloud. VDRs added sophisticated Q&A modules, bulk uploads, and analytics. E-signatures moved mainstream with clearer legal frameworks, materially shortening closing timetables and enabling same-day closings across time zones.

Automation progressed from isolated scripts to repeatable workflows, with document assembly generating standard forms such as nondisclosure agreements (“NDAs”), resolutions, and ancillary agreements from user-friendly questionnaires.

Early artificial intelligence (“AI”) tools emerged, with contract-analysis platforms applying machine learning to identify key issues such as change-of-control triggers, consent requirements, and unusual terms across large document populations. While human review remained decisive, technology triaged and prioritized documents, allowing lawyers to focus on judgment calls.

Market-terms databases matured, providing aggregated data on key metrics. These enabled more evidence-based negotiation of market terms and accelerated drafting against playbooks. Security and privacy concerns intensified, with firms adopting multifactor authentication and stricter information barriers.

2020s

The pandemic accelerated remote execution. Entire sale processes—from management presentations to signings—were conducted virtually. Videoconferencing became standard for negotiations, while e-signatures and digital closing rooms became the default. Transaction management platforms emerged, integrating checklists, document repositories, and signature packets into single workspaces.

Generative AI has begun shaping drafting, issue-spotting, and knowledge retrieval, producing first-cut markups, board minutes, and diligence summaries while surfacing precedents and market language.

Due diligence has been profoundly transformed. VDRs, AI-assisted review, and collaboration spaces enable simultaneous review, with structured reporting aligned to risk categories allowing faster conversion of findings into actionable drafting. Drafting and negotiation increasingly exploit structured data and analytics, with clause-level benchmarking informing positions on key issues. Legal project management platforms have expanded, with e-signatures and digital closing rooms compressing signing timelines.

Increasing reliance on technology has introduced new risks—in particular, cybersecurity. Multifactor authentication, encryption, and intrusion detection are standard; and strong data governance and a focus on confidentiality are becoming increasingly important issues to win and retain client trust.

Technology has reshaped the M&A legal team. Legal project managers, technologists, and knowledge lawyers are now standard in larger practices. Associates and partners are expected to be fluent in VDR configuration, document automation, and analytics.

Clients expect transparency through dashboards and disciplined budgeting, but how technological efficiencies will impact billing remains a hotly discussed topic.

Looking Forward

The speed of technological change for M&A lawyers is faster than ever, with new technology improving at astonishing speed.

The model for advice-based professions such as law is changing, and, accordingly, looking ahead at the future of M&A is challenging. It is also a challenge because brave new technology is often launched to look and feel like the comfortable past—so, for example, early movies were filmed to look like stage plays, and even the ChatGPT interface bears a remarkable resemblance to a (now) old-school Google search screen. As Canadian philosopher Marshall McLuhan observed, “We look at the present through a rear-view mirror. We march backwards into the future.”

Generative AI will likely become more embedded in drafting assistants, guided review, and negotiation support, with outputs checked against curated precedent libraries. Systems will increasingly surface prior team experience from multiple sources, with AI assistance provided within core platforms such as Word and Outlook through pop-ups and in-line suggestions.

Our ABA Technology in M&A Subcommittee produces the Directory of M&A Technologies, and, while the number of point solutions in it grows, usage will likely focus on a smaller number of integrated platforms providing end-to-end deal life-cycle coverage. The winning technologies will combine integrated coverage with proprietary, curated knowledge—insight-based conclusions and nonpublic practice points that cannot be replicated.

These systems will, in part, level the playing field between larger and smaller firms. Smaller firms will leverage technology for work previously requiring large teams, while larger firms will use technology to compete on smaller deals. More legal work will migrate in-house, with clients using platforms (increasingly contract life-cycle management systems) deploying generative AI for automated draft review against playbooks.

Conclusion

The last four decades have seen huge changes in how M&A lawyers operate. We now require not just legal expertise but also technical fluency, underpinned by strong governance and a focus on confidentiality and client trust. Those who combine these elements are best placed to succeed in the exciting years ahead. Here’s to the next decade of deals, technology improvement, and the M&A Committee.

During the Great Depression many “mom and pop” local stores suffered with their neighbors. At the same time, large companies found that by creating chains of retail outlets, they could leverage suppliers to give them better prices and terms than small businesses. Congress passed the Robinson-Patman Act, 15 U.S.C. § 13 (the “Act”), an amendment to the Clayton Act, to protect these small competitors from price discrimination that gave larger competitors an unfair pricing edge. The Act became an important tool to prevent large chains from pushing small stores out of the market and was actively enforced through the late 1970s.

Enforcement dropped off after a 1977 U.S. Department of Justice report that said preventing volume discounts to large chains caused consumers to pay higher prices notwithstanding harm to small retailers. The focus on consumer prices by regulators and courts since that time has resulted in far fewer suits under the Act. In effect, by the 1990s, the Act faced a sharp drop in both government and private party lawsuits as the U.S. Supreme Court focused antitrust law enforcement sharply on current impact on consumers.

While most people associate the Sherman Act with federal antitrust law, the Robinson-Patman Act also plays an important role. The Robinson-Patman Act applies to consumers, not just retailers or others in the sales chain. It states that “[i]t shall be unlawful for any person engaged in commerce, in the course of such commerce, either directly or indirectly, to discriminate in price between different purchasers of commodities of like grade and quality, . . . and where the effect of such discrimination may be substantially to lessen competition or tend to create a monopoly in any line of commerce, or to injure, destroy, or prevent competition . . . .” The Act is limited to commodities—it does not apply to any services (e.g., medical services), or other intangibles (e.g., wireless internet service, smartphone apps or “in-app purchases,” and advertising, including online advertising). Moreover, the commodities must be of “like grade and quality,” which generally will exclude bespoke products, pieces of art, and limited releases of high-end products.

But the Act is back! In Federal Trade Commission v. Southern Glazer’s Wine and Spirits, LLC, No. 8:24-cv-02684 (C.D. Cal. filed Dec. 12, 2024), the Federal Trade Commission (“FTC”) alleged the distributor’s discriminatory pricing practices for products harmed local stores and smaller retailers around the country by giving much better discounts and terms to large chains. This case was filed in the last months of the Biden administration. According to the complaint, defendant Southern Glazer’s Wine and Spirits had set up a scale for discounts based on volume purchases, but the volume of purchases for the deepest discounts could only be met by the biggest buyers. The biggest buyers also got a second significant advantage over smaller competitors in how Southern Glazer’s computed the volume purchase thresholds. In April 2025, the federal district court denied Southern Glazer’s motion to dismiss the FTC’s amended complaint.

The Trump administration reviewed both the Southern Glazer’s lawsuit and another Robinson-Patman Act case also filed late in the Biden administration, Federal Trade Commission v. PepsiCo, Inc., No. 1:25-cv-00664-JMF (S.D.N.Y. filed Jan. 17, 2025). The Trump administration FTC agreed to continue the Southern Glazer’s case but dropped the PepsiCo lawsuit.

The PepsiCo lawsuit alleged that PepsiCo gave Walmart unfair pricing advantages and promotional payments that were not offered to smaller retailers. The three FTC commissioners at the time of the review, all Republican, voted to dismiss the lawsuit in a settlement, arguing that the evidence was weak and the case politically motivated. In situations like those alleged in the cases above, a Sherman Act Section 1 claim or Sherman Act Section 2 claim is very difficult to pursue, since the net result of a Robinson-Patman Act claim typically will disrupt, slow, or stop price cuts to consumers by big box stores, while a Sherman Act claim generally requires harm to consumers—either through an agreement or a monopoly that reduces choice or availability or price. Claims based on price cuts to consumers generally require that there is a realistic chance of driving others out of the market by driving prices lower than their costs; the same is true for state antitrust laws based on Sherman Act Section 1 and/or 2. Nonetheless, many states have a sales below costs or unfair competition statute that can be used to capture the same conduct as that addressed by the Robinson-Patman Act.

Small businesses now have an example of a Trump administration lawsuit that shows suppliers must treat them fairly when compared to their larger competitors under the Robinson-Patman Act. Small businesses now also have a new district court decision to support their claims.

But how do smaller retailers discover the terms and prices from suppliers are giving them in comparison to those given to larger competitors? The conundrum here is the Supreme Court’s decision in Bell Atlantic Corp. v. Twombly, 550 U.S. 544 (2007), which held allegations of parallel conduct do not state an antitrust claim without a plausible allegation of an agreement to act in concert. Bell Atlantic Corp. created the plausibility requirement, which can cause difficulty in a Sherman Act Section 1 pleading. Plausibility is easier to show when a monopoly has actually been created because monopolies do not come about by accident.

Moreover, the Robinson-Patman Act has a series of exceptions, such as meeting competing suppliers’ prices or terms, or services or other consideration provided by the big box store that justifies the discount. Anyone looking at a price discrimination issue under federal or state law needs to understand the true amount of the discount and what the justification for it is.

A supplier and a big box store may try to cover their agreements and terms as trade secrets with nondisclosure agreements. This requires the potential plaintiff to look for pricing by the big box store so extreme, or a new burst of advertising of products sold by the same supplier, that the most plausible explanation for the situation is an agreement to give the big box store a significant price or other financial advantage over its small competitors.

As for suppliers and big box stores, significant discounts not provided to smaller buyers should be well documented to show they fall within an exception to the Act, preferably simply meeting competition.

To mark the forty-year anniversary of the Business Law Section’s Mergers & Acquisitions Committee, Lisa Hedrick, chair of the Committee’s Market Trends Subcommittee, reflects on M&A market trend developments in the last forty years.[1]

For more than two decades, the Market Trends Subcommittee of the ABA Mergers and Acquisitions Committee has served as a central resource for practitioners seeking to understand the current “market” status and evolution of deal structures, negotiations, and transaction terms. The Subcommittee’s mission is straightforward but essential: to educate M&A professionals on the latest trends shaping the deal landscape. Through speaker presentations, mock negotiations, open discussion, deal points studies, and market check videos, the Subcommittee has consistently provided members with practical insights into navigating an environment where norms shift quickly and competitive pressures continue to rise.

To understand the changes in the M&A market over the last forty years, Houlihan Lokey, a leading investment bank, provided information from their dataset of transactions over this period. Several themes stand out from a review of their data: the dramatic expansion of global deal volume, the cyclical but upward‑sloping nature of U.S. activity, and the steady rebalancing of buyers as financial sponsors have grown from niche participants to dominant players.

The Rise and Cycles of Global M&A Activity

Global M&A activity has expanded enormously since the mid‑1980s. In 1985, worldwide announced transaction value totaled roughly $240 billion. By 2021, that figure exceeded $5.6 trillion, representing one of the most significant long‑term growth arcs in modern corporate finance. Even accounting for recessions, credit contractions, and geopolitical shocks, the overall trajectory is unmistakably upward.

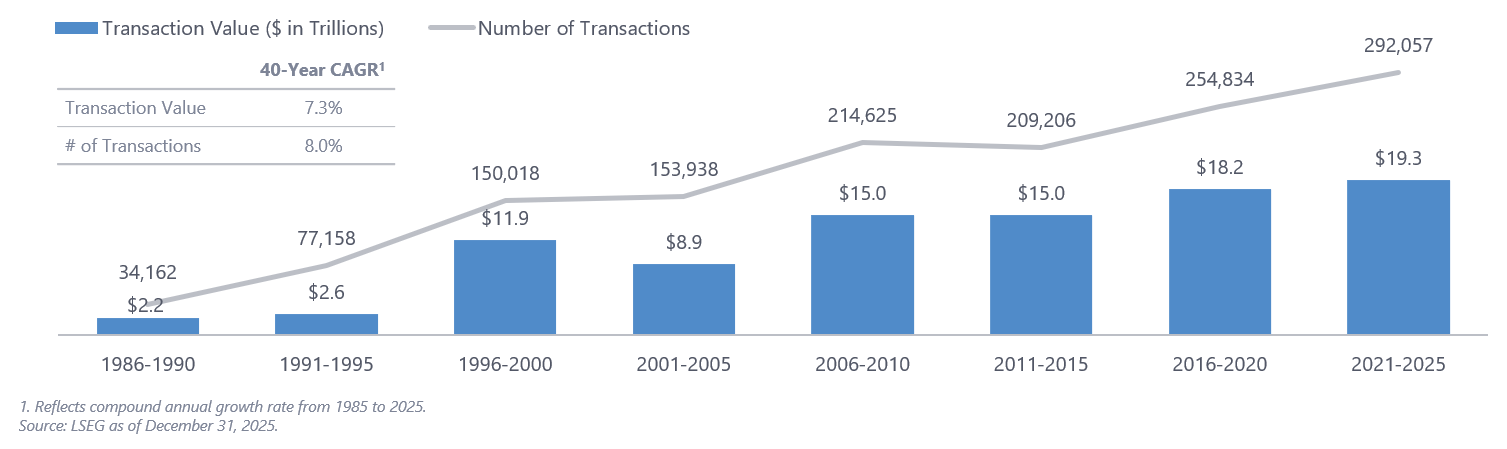

Global M&A Volume

From 1985 to 2025, global M&A transaction value and number of transactions grew by compound annual growth rates of 7.3% and 8%, a dramatic expansion. Source: LSEG as of December 31, 2025.

The data reveal several distinct cycles. The late‑1990s surge reflected the dot‑com boom and cross‑border liberalization. The mid‑2000s peak was fueled by abundant credit and the rise of large‑scale leveraged transactions. The 2008–2009 collapse remains the sharpest contraction in the dataset, followed by a decade of recovery and the unprecedented 2021 spike driven by low interest rates, pent‑up pandemic demand, and record sponsor dry powder.

Yet the most striking feature is not the peaks—it is the resilience. Even after downturns, global deal value consistently rebounds to new highs. This suggests that M&A has become a core strategic tool for corporate growth, not merely a cyclical phenomenon.

U.S. M&A: Cyclical, Concentrated, and Still the Global Anchor

The United States remains the gravitational center of global M&A. U.S. deal value has grown from roughly $200 billion in the mid‑1980s to more than $2.4 trillion in 2021. While the U.S. market mirrors global cycles, its peaks and troughs tend to be more pronounced, reflecting the outsize role of U.S. credit markets and domestic private equity.

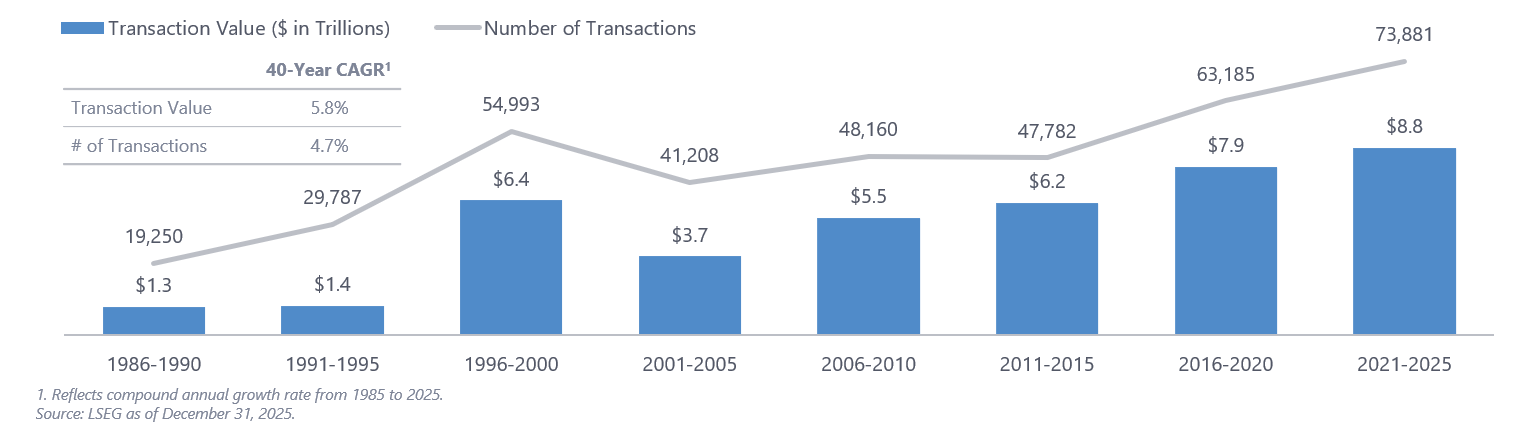

U.S. M&A Volume

From 1985 to 2025, U.S. M&A transaction value and number of transactions grew by CAGRs of 5.8% and 4.7%, similarly showing long-term growth. Source: LSEG as of December 31, 2025.

The 1990s expansion, the 2006–2007 credit‑fueled boom, the post‑global financial crisis recovery, and the 2021 surge all appear more sharply in the U.S. data. Yet the long‑term trend is consistent: dealmaking has become a central strategic lever for U.S. corporations, particularly in technology, healthcare, and consumer sectors.

Strategic Buyers Still Lead, but Sponsors Have Redefined the Market

Few developments have reshaped the market more profoundly than the rise of private equity. In the 1980s, private equity was still emerging from its leveraged-buyout‑era reputation. Today, it is a central pillar of the global M&A ecosystem.

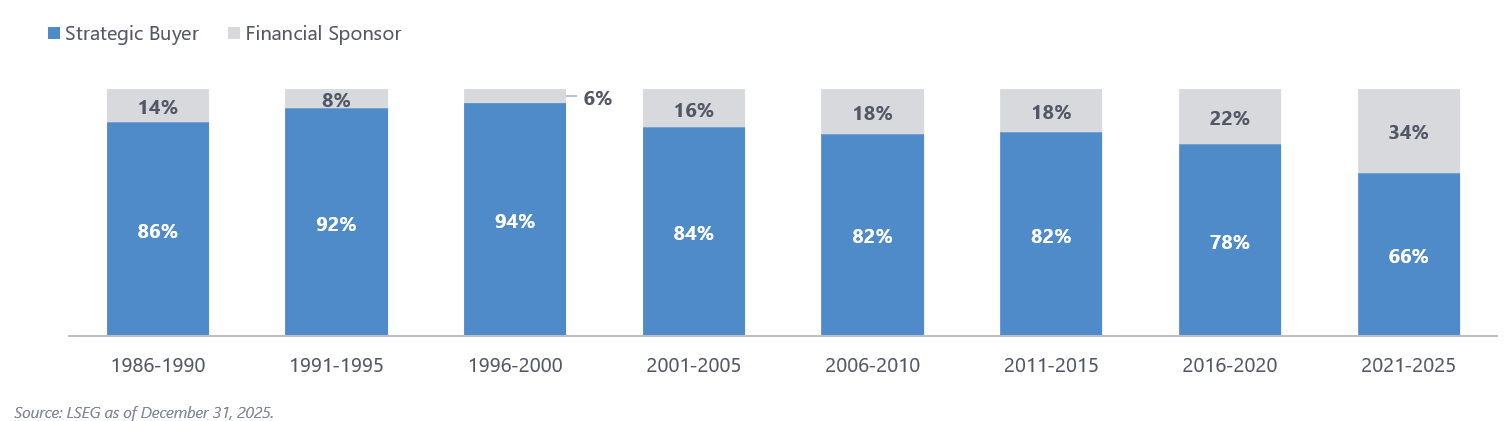

In the late 1980s, strategic buyers accounted for more than 85 percent of global transaction value. The landscape has shifted dramatically since that time. As private equity matured, institutionalized, and expanded its capital base, sponsors steadily increased their share of global M&A.

Global M&A Activity: Percent Buyer Mix by Total Transaction Value

Financial sponsors have more than doubled their share of global M&A, going from 14% of transaction value in 1986–1990 to 34% in 2021–2025. Source: LSEG as of December 31, 2025.

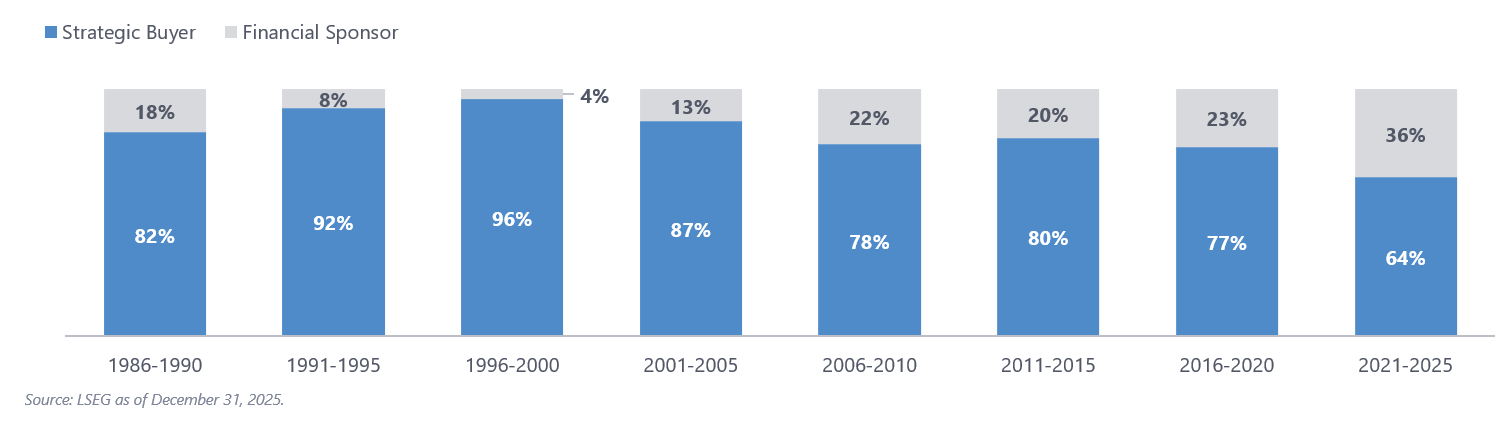

By the 2021–2025 period, strategic buyers represented roughly 66 percent of global deal value, while financial sponsors accounted for 34 percent—more than doubling their relative participation since the 1980s. The U.S. buyer mix tells a similar story to the global data. In the late 1980s, sponsors represented less than 18 percent of U.S. deal value. By 2021–2025, that share had climbed to more than 35 percent.

U.S. M&A Activity: Percent Buyer Mix by Total Transaction Value

Financial sponsors have similarly increased their share of U.S. M&A, going from 18% of transaction value in 1986–1990 to 36% in 2021–2025. Source: LSEG as of December 31, 2025.

This shift reflects several structural changes:

Massive capital formation in private equity, with global assets under management surpassing $8 trillion

Operational sophistication, enabling sponsors to compete directly with strategics for complex assets

A robust secondary market, allowing sponsors to recycle capital more efficiently

A shift in corporate behavior, with strategics increasingly disciplined on valuation and integration risk

The result is a more balanced buyer ecosystem, one in which sponsors are no longer opportunistic participants but central actors shaping valuation, auction dynamics, and deal terms.

The Data‑Driven Deal: Technology’s Transformation of M&A Practice

If one theme defines the modern era of M&A, it is the integration of technology into every stage of the deal life cycle. The last forty years have seen a shift from paper data rooms and manual diligence to a highly digitized, analytics‑driven process.

For example, virtual data rooms, introduced in the early 2000s, revolutionized diligence by enabling secure, remote document review. They shortened timelines, expanded bidder pools, and made global auctions feasible. Long gone is the day when buyers were required to travel to a conference room in a law firm’s or accountant’s office to sift through boxes of documents. Now, sellers establish a data room and are able to track which documents are reviewed and for how long by the various bidders. More recently, deal teams have the ability to use machine learning tools to analyze contracts, suggest drafting changes, and evaluate comments from opposing counsel.

Technology has not replaced judgment, but it has fundamentally changed the speed, scope, and precision of M&A execution.

The Emergence and Influence of Deal Points Studies

One of the most important developments in the M&A marketplace over the past two decades has been the rise of deal points studies. These studies have fundamentally changed how practitioners understand market norms, negotiate key provisions, and benchmark deal terms. They have brought empirical rigor to an area that historically relied on anecdote, experience, and negotiation leverage.

The ABA M&A Committee played a pioneering role in this transformation. In 2006, the Committee published its first two deal points studies: (1) the Public Target Deal Points Study, which looked at negotiated terms in public company transactions; and (2) the Private Target Deal Points Study, providing a parallel analysis for private company acquisitions.

These studies were groundbreaking. For the first time, practitioners had access to systematically collected, anonymized data showing how often certain provisions appeared, how they were drafted, and how they evolved over time. Instead of relying on “market practice” as a rhetorical device, deal lawyers could point to actual market data.

Over time, this Subcommittee expanded the studies to include studies focusing on Canadian deals, both private and public; European deals; and carveout transactions.

The ABA’s leadership also catalyzed a broader ecosystem of deal analytics. Today, a wide range of market participants produces their own studies, including investment banks, commercial banks, stockholder representative firms, and insurance providers (particularly in the representation and warranty insurance space), among others.

A Market in Constant Motion

The past forty years have been defined by cycles of innovation, disruption, and reinvention in the M&A marketplace. Increased global M&A volume, the rise of private equity, technological transformation, and the emergence of deal points studies have each left an indelible mark on the practice.

Yet the through‑line across all these developments is adaptability. M&A has always been a forward‑looking discipline that responds quickly to economic shifts, regulatory changes, and new strategic imperatives. As we look ahead to the next forty years, the forces shaping the market will undoubtedly evolve, but the central role of M&A in corporate strategy will remain.

The Market Trends Subcommittee is proud to contribute this reflection as part of the Committee’s fortieth anniversary celebration and looks forward to continuing the conversation at the Spring Meeting.

Lisa thanks Houlihan Lokey for providing analysis of London Stock Exchange Group (“LSEG”) data for this article and also thanks the vice-chairs of the Market Trends Subcommittee—Edward Deibert (Arnold & Porter, San Francisco, CA) and Tatjana Paterno (Bass, Berry & Sims PLC, Nashville, TN)—for their review and helpful comments on earlier drafts. ↑

To mark the forty-year anniversary of the Business Law Section’s Mergers & Acquisitions Committee, Nate Cartmell and Nick Mozal, cochairs of the Committee’s M&A Jurisprudence Subcommittee, reflect on developments in M&A jurisprudence over the last forty years.

Like the other sections of the M&A Committee, the state of the practice area covered by the M&A Jurisprudence Subcommittee in 1986 could only be described as nascent. M&A itself was undergoing significant change and evolution, and it was only natural that the jurisprudence arising from those transactions would change and evolve as well. The most recurring topics covered in the cases presented at our subcommittee meetings in recent years—fiduciary duties of directors in evaluating mergers and disputes between parties about their deal agreements—looked very different forty years ago, if they existed at all. Because jurisprudence sits at the intersection of so many of the other subcommittees, the following summary is necessarily generic and high-level to avoid stepping on their toes.

Fiduciary Duty Litigation of the 1980s

Transporting back to the 1980s would find one in the maelstrom of deal litigation the outcomes of which created the cornerstone of guidance practitioners have used to guide fiduciaries and companies ever since. The Delaware Court of Chancery and Delaware Supreme Court were busy writing the opinions that remain the starting points for the M&A textbooks that students study in law school.

1986 was particularly transformative. Of the many notable developments that year, two stand out. The first came from the Delaware Supreme Court handing down its Revlon, Inc. v. MacAndrews & Forbes Holdings, Inc. decision on March 13,1986, which built on the court’s Unocal Corp. v. Mesa Petroleum Co. decision from June 1985. The second was the Delaware legislature springing into action to adopt exculpation through section 102(b)(7), essentially overturning parts of the Delaware Supreme Court’s March 1985 decision in Smith v. Van Gorkom.

So much more was to come in the following years: the “barbarians” were not yet at RJR Nabisco’s gates, and in a sign that the more things change, the more they stay the same, Paramount had not yet injected itself into the merger between Time Incorporated and Warner Communications.

Committee Beginnings

The fiduciary developments in the law into the 1990s provided such usable guidance and standards that hostile takeovers became less common. M&A generally, of course, was only picking up steam. As M&A grew and became more varied, so did the jurisprudence concerning it.

By 2002, a small group of attorneys from what was then called the ABA’s “Negotiated Acquisitions Committee” came together and, in their first Annual Survey of Judicial Developments Pertaining to Mergers and Acquisitions, described the founding of this subcommittee as follows:

The Subcommittee on Recent Judicial Developments was formed at the 2002 Annual Meeting of the American Bar Association in Washington, D.C. The primary charge of the Subcommittee on Recent Judicial Developments is to summarize, on an annual basis, significant judicial decisions in the area of mergers and acquisitions (“M&A”), and to publish that summary as a service to ABA members who practice in the M&A area.[1]

The cochairs were Scott Whittaker (New Orleans, LA) and Jon Hirschoff (Stamford, CT), with contributors listed as Patrick Leddy (Cleveland, OH), Robert Ouellette (Columbus, OH), Mike Pittenger (Wilmington, DE), Tricia Vella (Wilmington, DE), and Arthur Wright (Dallas, TX).

The categories of cases summarized included interpretation of agreements, successor liability, and fiduciary duties.

Current Issues

Our recent Annual Surveys and meetings still cover these topics, though the most recurring issues have changed. For fiduciary challenges, mostly gone are the days of hostile acquirers asserting fiduciary challenges as a basis to enjoin target boards from taking a different deal. Instead, the fiduciary cases predominantly originate from non-acquirer stockholders seeking relief, which is increasingly either a pre-closing injunction related to governance disputes (such as compliance with a charter, bylaws, or other organizational document) or post-closing damages. The key decisions of the last decade—Corwin v. KKR Financial Holdings LLC, In reMFW Shareholders Litigation, C&J Energy Services, Inc. v. City of Miami General Employees’ Retirement Trust—arose in that context.

The topic of interpreting agreements is the one where we spend most of our ink in the annual survey and time in our meetings. This category involves disputes between parties, leading to court decisions, about the terms of the parties’ agreements. They tend to be private companies, and often private equity firms are the ones buying or selling. It seems there is no limit to contracting parties’ abilities to find something to fight about in the merger agreements, stock purchase agreements, asset purchase agreements, side letters (and on and on) to which they agreed. It gives us plenty to fill our agenda!

Our subcommittee deals with both pre-closing and post-closing cases. The pre-closing cases are usually “busted deal” cases. These cases involve one of the parties regretting their agreement and trying to get out before closing. Sometimes they arise in the context of one of the parties trying to force closing by seeking specific performance. Although material adverse effect (“MAE”) or material adverse change (“MAC”) clauses existed for many years, it was not until the In re IBP, Inc. Shareholder’s Litigation decision in 2001 that the Delaware courts started parsing them finely at the request of disputing parties. As is well known, this type of dispute exploded during the coronavirus pandemic and expanded to not just disputes over MAC clauses but interim operating covenants as well. We’ve been lucky to have plenty of jurisprudence to discuss in this area in recent years. And all M&A practitioners are lucky for the guidance set out in those decisions.

The post-closing contractual disputes between deal parties arise in a variety of contexts. These disputes primarily arise in private company sales. They include claims for contractual indemnification related to breaches of reps and warranties, fraud claims, and (increasingly) disputes over earnout provisions. Again, looking back forty years in this area, one would struggle to find much specific M&A jurisprudence on these topics until recently. But as deals of all types and sizes have become more common, so have these disputes. Just as the disputes keep coming and leading to decisions, they also lead to lessons. Each meeting we are lucky enough to have presenters discussing a decision that involves a fact pattern or contractual language worthy of lessons and consideration. We would be remiss not to mention Glenn West (Dallas, TX) and his contributions, both in his public writings and in his presentations and contributions in our meetings, in this area. And the same is true for the many jurists from Delaware who have graced us with their time and patience in answering questions at our meetings.

Navigating Issues

Our subcommittee is grateful for the continued opportunity to discuss the lessons from M&A disputes when they make their way to court. Though we do not always have the answer about what the next party should do in a similar situation, we hope that attendees feel better equipped at navigating those issues in their practices when they face them.

Available on Westlaw at Subcommittee on Recent Judicial Developments, Negotiated Acquisitions Committee, Annual Survey of Judicial Developments Pertaining to Mergers and Acquisitions, 58 Bus. Law. 1521 (2003). The subsequent edition in 2004 is available on the ABA website. ↑

By any measure, the Mergers & Acquisitions Committee is the most successful committee of the ABA Business Law Section.[1] The Committee boasts more than 5,000 members—from sixty-one countries on six continents—making it the largest committee in the Section and, by far, the world’s largest forum for M&A lawyers. Committee publications and programs organized and sponsored by the Committee have generated substantial revenue and recognition for the ABA and the Business Law Section over the years.

You might think that the M&A Committee has always been a robust feature of the ABA and that the ABA established the Committee early in its history because ABA leadership knew from the outset that M&A lawyers needed a forum to discuss their deals, their practices, market trends, and legal developments. But that is not the case.

Early Beginnings

The M&A Committee was formed in 1986 under the inspiration and leadership of Pat Garrett (Houston, TX), Karl Ege (Tacoma, WA), and Vince Garrity (Philadelphia, PA), who were then members of the ABA Corporate Laws Committee. They observed that no existing committee of the ABA Business Law Section dealt directly with the legal and practice-oriented issues involved in negotiated acquisition transactions. Committee lore is that they and a few other acquisition lawyers—including Byron Egan (Dallas, TX), Joel Greenberg (New York, NY), and Leigh Walton (Nashville, TN)—met in a conference room at the Dallas–Fort Worth airport in 1986 to talk about forming a new group within the Business Law Section that would focus on transaction practice and process (rather than emphasizing statutory provisions and governmental rules and regulations) and would share their experiences helping their clients get deals done. Walton’s attendance was fortuitous (and a great win for the Committee); she attended in place of a partner of her firm who had been invited but became unavailable. More than two decades later, she became the first woman vice chair and then the first woman chair of the Committee. This grassroots beginning of the M&A Committee was and continues to be one of its great strengths.

Then Committee Chair Rick Climan (lower left) with Vice Chairs (clockwise) Byron Egan, Joel Greenberg, and Leigh Walton (Honolulu, 2006). Photo credit: Tracy Bacigalupo.

The M&A Committee originally had the unfortunate name of the Ad Hoc Committee on Consensual Combinations. It was “Ad Hoc” because it wasn’t initially approved as a committee of the Business Law Section, and the founders were not allowed to call themselves an M&A committee because the larger and more powerful Securities Regulations Committee claimed domain over M&A within the Section by virtue of its work in the area of public tender offers. In 1989, the Ad Hoc Committee on Consensual Combinations became the Committee on Negotiated Acquisitions, and Garrett became its first chair. The Committee was renamed the Mergers & Acquisitions Committee in 2008, several years after it eclipsed the Federal Regulation of Securities Committee as the largest committee of the Business Law Section.

The M&A Committee initially attracted senior lawyers practicing throughout the United States who handled mergers and acquisitions. By 1988, when Nat Doliner (Tampa, FL) attended his first meeting, thirty to forty lawyers attended Committee meetings. The Committee’s primary activity was developing a “model” stock purchase agreement that reflected generally accepted acquisition practices in the United States.

Model Documents: An Early Foundation of the M&A Committee

Deal lawyers working together to develop model documents and related explanatory commentary is a cornerstone of the M&A Committee and continues to be an important aspect of the Committee’s work.

The first publication of the M&A Committee, the Model Stock Purchase Agreement with Commentary (“MSPA”), was published in 1995 under the leadership of David Bronner (Chicago, IL), Greenberg, and an editorial subcommittee that included subsequent chairs of the Committee Rick Climan (Silicon Valley, CA) and Walton. (Climan attended his first Committee meeting in St. Louis in 1989.)

The published work included the names of all members of the M&A Committee and indicated with an asterisk whether a member had attended more than one meeting. Sixty-two names had an asterisk, so you could say that in 1995, the Committee had sixty-two active members.

The detailed explanatory commentary included with the MSPA made the publication an instant hit with practitioners and educators. It provided practical guidance explaining the rationale and authority for key provisions of the model agreement. It was not about case law or regulations but rather the stock purchase agreement itself and how the agreement provisions connected with each other. The interplay of the agreement provisions was illustrated in hypothetical scenarios included with the commentary, which were developed under Climan’s leadership. Deal lawyers sharing their experiences.

The M&A Committee also published the Manual on Acquisition Review in 1995, a companion to the MSPA that provided guidance on due diligence and substantive areas of law that may be implicated by a seller’s representations and warranties in a stock purchase agreement.

As the M&A Committee completed its work on the MSPA, it determined that the next logical project would be a model asset purchase agreement. A task force was created in 1994 (cochaired by Egan and Lawrence Tafe (Boston, MA)), which culminated in the Model Asset Purchase Agreement with Commentary being published in 2001. (Egan went on to serve two terms as vice chair of the Committee.)

The early 2000s were a period of great growth for the M&A Committee. New subcommittees and task forces were established and empowered with projects. Publications proliferated, including the following:

A second edition of the Model Asset Purchase Agreement with Commentary will be published in early 2026.

CLE and Other Programming

Substantive programs became a feature of M&A Committee meetings in the mid-1990s and became more regular after the MSPA was published. The Committee pioneered the use of the “mock negotiation” as a teaching tool to illustrate the real-world give-and-take of contentious M&A negotiations. The first mock negotiation presentation took place in the late 1990s before a large audience at a meeting at Opryland in Nashville, Tennessee, featuring Climan, Greenberg, Bronner, and other Committee members. Those same presenters, joined by Ege and Walton, later staged a mock negotiation presentation that was broadcast live to a large nationwide audience from a television studio in Washington, D.C. (with presenters in full TV makeup).

Then Committee Chair Leigh Walton with (from left) future Chair Wilson Chu and former Chairs (from right) Rick Climan and Joel Greenberg (2010).

During the same period, the M&A Committee launched the National Institute on Negotiating Business Acquisitions (“National Institute”), originally chaired by Garrity and featuring senior Committee members as presenters and panelists. The National Institute was presented as a separate two-day conference because of the sizable volume of substantive content that was offered. The Committee’s first National Institute was staged in New York City, and subsequent National Institute programs have been presented in Chicago, New Orleans, Miami, Las Vegas, and other locations. The twenty-eighth annual National Institute, cochaired by former Committee Chairs Climan, Greenberg, and Scott Whittaker (New Orleans, LA), took place in November 2025. All past chairs/cochairs of the National Institute served at one time as chair of the Committee.

The National Institute has been used as a forum to provide M&A Committee members—young and more seasoned—with speaking opportunities. For the past twenty years, the centerpiece of the National Institute has been a four-hour mock negotiation panel chaired by Climan and featuring other past Committee chairs.

Today, the M&A Committee sponsors and presents regular educational programs on M&A-related topics, including continuing legal education (“CLE”) programs and other presentations at its committee, subcommittee, and task force meetings and as part of Committee-sponsored webinars. Since the 1990s, the Committee has also disseminated valuable substantive content through its official newsletter, Deal Points, which is published three times a year.

Innovation and Growth

You could say that the “modern era” of the M&A Committee began under Climan’s leadership (chair from 2002 to 2006). In addition to new task forces focused on publications, Climan established the Market Trends Subcommittee, the Subcommittee on Recent Judicial Developments (which was later renamed the Jurisprudence Subcommittee), and the Private Equity Subcommittee. Under the leadership of Whittaker, who later became chair of the Committee, and Jon Hirschoff (Stamford, CT), the Subcommittee on Recent Judicial Developments took on reporting on judicial decisions affecting M&A practice. It began publishing the “Annual Survey of Judicial Developments Pertaining to Mergers and Acquisitions” in the Business Lawyer in 2003.

Discussion at M&A Committee meetings became more substantive under Climan’s leadership, with a new focus on hearing from members of the Delaware judiciary. The strength of the Committee allowed it to foster involvement of federal and state governmental officials, especially Delaware judges. Delaware Chief Justice Myron Steele was a frequent attendee and speaker at Committee meetings during Climan’s term as chair, and Climan’s videos featuring Delaware Chancery Court Judge (and later Chief Justice) Leo Strine were particularly popular with Committee members.

Then Committee Chair Scott Whittaker (far right) with (from left) former Chairs Nat Doliner, Rick Climan, Karl Ege, Leigh Walton, and Joel Greenberg (Montreal, 2016).

Wilson Chu (Dallas, TX) developed a study on “Deal Point Trends in Private Company M&A,” which he presented at a conference of the American Conference Institute (unrelated to the ABA) in March 2001. The consummate generator of good ideas, Chu subsequently shared the presentation with the M&A Committee. (Chu attended his first Committee meeting in 1997, at the suggestion of John Leopold (Montreal, Canada). Leopold, who became a member of the Committee in 1989, was the first Canadian lawyer to join. Today, there are more than 250 Canadian lawyers on the Committee’s membership roster.) Chu recalls the warm welcome he received when he joined the Committee and being impressed with the Committee’s culture, which was focused on building community rather than Committee members building their own individual brand.

Chu’s “Deal Point Trends” report was of immediate interest to M&A Committee members. With Larry Glasgow (Dallas, TX), Chu presented the report over several years until Committee Chair Climan suggested that the study be “transitioned” to the Committee. Hence, Climan established the Market Trends Subcommittee in 2004, initially cochaired by Chu and Glasgow.

Since its first private target deal points study in 2006, the Market Trends Subcommittee has published ten U.S. private target studies (the most recent in December 2025), as well as studies reporting on deal trends in strategic buyer / public target transactions and carve-out transactions and deal trends in Canadian and European private target transactions. The first public target deal points study—chaired by Keith Flaum (Silicon Valley, CA), who went on to become a vice chair of the M&A Committee—also was published in 2006.

In 2002, Climan appointed Chu chair of the M&A Committee’s Membership Subcommittee. (“One of my best decisions as chair,” Climan says.) Chu proposed that access to the deal points studies, while free of charge, be limited solely to members of the Committee. Another great idea from Chu. His plan was implemented, and, in relatively short order, membership of the Committee grew from 800 to more than 2,000. By the summer of 2008, Committee membership exceeded 3,000. It has grown steadily since then.