Overview of a Compensation Committee’s Basic Responsibilities

The listing requirements of both NASDAQ and the New York Stock Exchange mandate that a committee of independent, nonemployee directors must have principal responsibility for the compensation of CEOs and other executive officers. Accordingly, as part of their basic responsibilities, compensation committee members regularly will be engaged in assessing the performance and determining the pay levels of executive officers, the design of the compensation programs applicable to them, and the contractual arrangements governing their employment. The compensation committee members typically also are responsible for formulating share ownership guidelines, compensation clawback policies, insider-trading and anti-hedging policies, and approving compensation-related proxy disclosure.

The compensation committee also is tasked with assessing the link between compensation and enterprise risk management. In that regard, since 2009 the SEC in Item 402(s) of Regulation S-K under the Securities Act of 1933 (as amended) has required a company to disclose whether “risks arising from the registrant’s compensation policies and practices for its employees are reasonably likely to have a material adverse effect on the registrant” and, if so, to disclose the compensation policies and practices as they relate to risk management. As a practical matter, this has led companies to engage in a careful risk assessment of their compensation programs, not limited to those applicable to executive officers. Given the ultimate oversight duties of a board of directors, and the specialized knowledge possessed or developed by members of the board’s compensation committee, it is unsurprising that compensation committees are frequently given the principal responsibility of overseeing the process of ensuring that compensation design throughout the organizations does not encourage inappropriate risk-taking.

The Link Between Compensation and Risk

Following the corporate scandals of the early 2000s (e.g., Enron, WorldCom, and Global Crossing), corporate-governance experts, academics, the media, elected officials, regulators, and the general public began to focus on the possible role that executive compensation played in incentivizing inappropriate behavior. In particular, many argued that the excessive risk-taking that led to such scandals was fueled by an inordinate management focus on short-term stock price gains that was tied to the overuse of stock options. The basic insight of these critics was that stock options had at least two major drawbacks. First, the flexibility as to timing of exercise allows executives to benefit from short-term stock price increases that do not necessarily reflect the creation of long-term shareholder value. Second, stock options provide an asymmetrical incentive, with the holders benefiting from stock gains but not losing any investment through stock price losses. As a consequence, all things being equal, executives with substantial stock-option holdings are more likely to favor high risk/reward investments or other corporate actions that could generate significant stock increases in the short-term (that could be captured by option exercises by those executives), but might have significant long-tail risk.

Critics recognized that there were substantial accounting and tax incentives for corporations to use stock options, and their concerns led to a revisiting of the accounting treatment of stock options and ultimately to the adoption of FAS 123R (now redesignated as ASC 718), which requires the expensing of the grant date value of stock options determined by using Black Scholes or other option valuation methodology. This led to a reduction in the use of stock options and an increased utilization of restricted stock and restricted stock units coupled with shareholding requirements—the thought being that these instruments would better align executive incentives with those of the corporation and its shareholders over the longer term, and dis-incentivize executives from excessive risk-taking.

At most public companies, compensation committees became responsible for ensuring that the design and mix of executive officer compensation elements did not create incentives for unacceptable risk-taking, and approved the annual disclosure under Item 402(s) of Regulation S-K of the Securities Act of 1933 (as amended) regarding whether the “risks arising from the registrant’s compensation policies and practices for its employees are reasonably likely to have a material adverse effect on the registrant.”

Expanding the Committee’s Role

Until recently, most compensation committees focused their compensation risk assessment exclusively on the remuneration of executive officers and, in regulated financial institutions, “significant risk-takers” (i.e., the individuals who are in the position to make significant bets of company capital). The exceptions tend to be in certain industries—in addition to financial services, the pharmaceuticals and medical-device industries are the sectors in which public companies currently are somewhat more likely to involve the independent directors in overseeing broader employee incentives. Unfortunately, most companies in which compensation committees currently are engaged in overseeing the risk assessment of rank-and-file employee compensation arrangements do not provide sufficiently detailed disclosures to describe differences in approach in any depth.

More recent events, particularly the sales practices controversy at Wells Fargo, have illustrated for corporations more generally that the conduct of relatively low-level employees can have a huge reputational impact on companies, and that the role compensation may play in incentivizing inappropriate conduct cannot be overlooked. Trusting management to police incentive arrangements of rank-and-file employees without director-level oversight seems somewhat naïve in 2017.

As a result, we can expect more and more compensation committees to undertake additional oversight responsibility over compensation arrangements applicable to employees below the executive officer level. Although this is unlikely to involve retaining day-to-day decision making about rank-and-file incentives, one can expect that companies will establish structures whereby management will be required to report regularly to compensation committees about the design of such incentives and safeguards protecting against their potential for promoting inappropriate conduct. Companies also may be more likely to highlight such oversight in their public disclosures. It should be instructive to observe the different models of risk director oversight of rank-and-file incentives—and perhaps consensus best practices—that will be developed in the coming years.

“Garbage in, garbage out” is a phrase data scientists often use. One can apply it in many contexts, but it arises from the idea that the quality of the output of a computer will only be as good as the quality of its programming. In that simple phrase, there is a central truth often overlooked in discussions surrounding artificial intelligence (AI) and machine learning (ML): no matter how skilled your coders, or how great your algorithms, the quality of the results, signals, insights, and “learnings” these technologies provide will only be as good as the data fed to them.

AI and ML are nebulous terms often used interchangeably; however, they are not the same. AI was famously described by Marvin Minsky in Steps Toward Artificial Intelligence as the ability of machines to behave and learn like humans. ML, a subset of AI, has been best described recently by Amanda Levendowski in How Copyright Law Can Fix Artificial Intelligence’s Implicit Bias Problem as the application of mathematics and computer science to create a machine’s ability to improve automatically through experience. Just like humans use massive data sets (our memories) to become more efficient and make better decisions over time, AI and ML systems rely on data to do the same.

Therefore, data is at the core of developing new AI and ML systems. Accessing and securing the most and best data is where the attorneys come in. Companies and organizations developing AI technologies want access to the best data possible with the least restrictions possible. At the same time, companies and organizations want to retain exclusive access to datasets that are (or could be) market differentiators. There are tensions between these interests, and data-licensing attorneys will increasingly be at the center of navigating them, including during negotiations with third parties and regulators and in the creation and management of data retention and usage policies.

There are terabytes of free harvestable data available online. Wikipedia, for example, is a common source of no-cost “general knowledge” data for AI and ML technologies. Many other datasets are freely available to AI and ML developers with open-access or attribution-only licenses. Attorneys must analyze each one of these licenses in the context of the use cases their clients are pursuing (or may pursue later). Conducting such an analysis requires careful planning and interviews with clients so that the attorney can accurately understand the use case for the data accessed to ensure it is consistent with the licenses granted by the licensor of the data set.

The owners and licensors of free data often lack the resources to actively curate or inspect the data to ensure quality and accuracy. Therefore, many free data sets contain errors, bias, and misinformation that can negatively affect the AI and ML systems using it. This quality-control problem has created a large market for curated data sets that sit behind paywalls, restricted licenses, and regulatory hurdles. Data-licensing attorneys are increasingly asked by clients to negotiate and draft license rights to highly protected and expensive data sets. This raises the stakes of the license analysis and negotiations. Given that exactly how AI and ML systems use data to “learn” can be opaque, a simple contractual miscalculation or limitation on use rights in a data-licensing agreement can have catastrophic results on development if the developers cannot use the data in the way that is most effective for the AI or ML system they’ve designed. Therefore, it is a good practice for data-licensing attorneys to get involved and provide advice and counsel during the development process so that that the development team can understand the legal ramifications of its design choices, and so that the attorney can work in parallel to pave the way toward accessing the best data assets available. Being embedded will also help attorneys counsel clients on regulatory compliance, privacy, and security related to the onboarding and processing of such data in real time.

AI and ML systems have a tremendous appetite for data. Failure to use the best and most accurate data can have both negative business consequences (loss of revenue and failure to remain competitive) and harmful societal implications (biased, unethical, or disparate outcomes). Some of the biggest obstacles to fueling AI and ML with the best data are not technological, but legal in nature. Thus, collaboration among lawyers, product developers, regulators, and data scientists is critical to ensuring that, as AI and ML technologies continue to develop and mature, they have access to the best data available and simultaneously protect the privacy of data subjects and the security and integrity of the data and the technologies that use it.

At one time, the New Business Rule generally prevented an injured party from obtaining a damages award for lost profits due to the opposing party if the injured party was a newly established business (R. Dunn, Recovery of Damages for Lost Profits, 3d ed.,1987). Absent a history of past profits, future profits seemed too “uncertain and speculative,” particularly in the progress-oriented atmosphere of the late 1800s when rules defining damages first developed (Hickman v. Coshocton Real Estate Co., 58 Ohio App. 38 (Ohio ct. App. 1936)). In addition to their desire to limit excessive damages, courts often distrusted jurors with the discretion necessary to evaluate the reasonableness of future profit estimates (B. Bollas, New Business Rule and the Denial of Lost Profits, 48 Ohio State L.J. (1987)).

Changing attitudes towards jurors, a consensus focused on the inherent injustice to new businesses, and recognition of the economically nonoptimal allocation of resources that the New Business Rule encouraged may have all played a role in the shift in the interpretation of the rule away from a finding of law to a finding of fact, as pointed out by Bollas in the Ohio State Law Journal, and by Everett Gee Warner and Mark Adam Nelson in “Recovering Lost Profits,” 39 Mercer L. Rev. (1988). In most cases, says Michael L. Roberts in his article, “Recovery for the New or Unestablished Business” (The Alabama Law. (Mar. 1987)), the emphasis focuses on the fact that profits were lost, not on an absolute measure of those profits. As a result, calculation of lost profits need no longer conform to “absolute certainty” requirements; the “reasonable certainty” standard as applied to existing businesses with a history of profits has been applied to new enterprises as well (Michael G. Stewart, The Evolution of the New Business Rule, 17 Cumberland L. Rev. (1986)). However, as evidenced in Schonfel v. Hilliard, 62F. Supp. 2d 1062 (S.D.N.Y 1999) and Tipton v. Mill Creek Gravel, Inc., 373 F.3d 913 (2004) courts still give lost-profits claims heightened scrutiny when the party has no financial history. Clearly, when a business can show a history of profitability, both in the long-term and recent past, this profitability can often be reasonably projected into the future (with all other variables held constant). Additionally, if the contractual agreement between two parties makes mention of expected profits, quantification of those profits lost in the event of a breach proceeds without difficulty.

When faced with quantifying lost profits for new businesses with little or no history of earnings prior to the breach, quantification of lost profits becomes more of a challenge. Fortunately, the widespread application of the “reasonable certainty” standard allows several methods of quantifying damages without the requirement of complete and absolute certainty as to amount. The specific approach taken depends upon the operational effect the breach has upon the new business. An enterprise that fails because of the breach necessitates slightly different analysis than does one which continues operations at a reduced or at a level capacity. Regardless of the approach taken, however, an overriding concern focuses on the individuality of the case.

1. Business Enterprise Continues

If the business enterprise survives the breach, post-breach income figures, either for the injured party or for another who continues the enterprise at the same location, may be used to approximate profits lost due to the breach.

Post-Breach Profits, Injured Party

In some cases, the harmed business may be able to resume business along the same growth curve as existed prior to the breach. Although no permanent harm has occurred, the business has experienced a shortfall in income from the time of breach until production returns to normal. Profits will always lag as a result of the breach.

Notice that this method does not rely upon profitability at the time of breach. Rather, it focuses on the timing of profits. In limited circumstances, it may be possible to utilize post-breach income numbers as a proxy for expected income during the shortfall period. Additionally, use of this method depends heavily upon the continuation of existing market and production factors after the breach.

McDermott v. Middle East Carpet Co. Associated, 811 F.2d 1422, (11th cir.1987) (MECCA) applied this concept in determining a damage award for lost profits. Plaintiffs McDermott and his corporation Criterion Mills served as co-consultants to the royal family of Kuwait during construction of a carpet factory in the Middle East. As a result of McDermott’s inability to perform his contractual duties, production of the facility fell behind schedule. Additionally, McDermott ordered raw materials that were incompatible with production equipment installed earlier. In combination, these factors caused an eight-month delay in the production of carpets. MECCA suffered diminishing losses for 1979, 1980, and 1981 before a fire destroyed the factory in 1982. A new carpet plant completed in late 1982 was profitable.

Expert testimony utilizing a hypothetical economic model incorporating market variables established that a “delay in commencing production will cause a corresponding delay in reaching full profitability.” Significantly, profits were awarded based on MECCA’s profit and loss statement for 1983, more than four years subsequent to the breach and with a reconstructed facility. Post-fire income figures were sufficient because the relevant variables remained constant. The new facility produced the same kind of carpet, used similar machinery, and operated within the same market as the destroyed facility. The pattern of diminishing losses just prior to the fire, consistent with the expert’s economic model, suggested that MECCA would have soon reached profitability.

Expert testimony convincingly quantified lost profits because the economic model supported the substitution of the new facility’s performance for that of the old. Additionally, the model properly accounted for variables such as changes in management, labor, capital, and raw materials. Finally, the existence of a “stable and monopolistic” Egyptian market and protection from foreign competition simplified the analysis by eliminating many variables associated with a free-market system.

Post-Breach Profits, Successor Business

It is possible that the injured party may vacate the premises of former activity, only to be replaced by another company in the same business. In this case, assuming that market variables have remained constant, an extrapolation can be calculated based on comparing the replacement business entity with the original. Care should be taken here to ensure that the replacement business is actually comparable to the original. Calculating lost profits in these circumstances approaches quantification using benchmarking techniques.

2. Business Enterprise Ceases

Using post-breach income figures makes sense when a business merely experiences a temporary shortfall in production of income or is continued by a different entity. However, in the event that the new business is unable to recover from the breach, it will have neither a significant history nor a future of recorded profits. Although this complicates matters, lost profits may still be quantified with reasonable certainty.

In all cases, the most important step involves the identification of critical success factors. Critical success factors, as the name implies, are those elements that are absolutely necessary for a particular business to succeed. Although most businesses share a common core of essential skills and attributes that promote economic viability, the mix of these skills can vary widely among individual businesses. Elements that are important for the success of a service-oriented business may differ substantially from that of a capital-intensive business. For example, the critical success factors for a health spa may include location, marketing strength, employee reputation, management expertise, and start-up capital. On the other hand, the critical success factors for a computer manufacturer may be sufficient capital, patented technology, distribution channels, supplier relationships, and advantageous labor relationships.

Short-Term, Prebreach Operations

Prior to the breach, the new business may have experienced some level of short-term operations. Even if the business operated for less than one year, sufficient information may exist to extrapolate lost profits as a result of the breach. So long as some information is available, it can serve as the starting point for a comparison to industry statistics. Key industry statistics to examine, among others, include financial ratios such as profit margins, debt-to-equity ratios, and receivable and inventory turnover. Other vital information includes trends in sales, cost of sales, general and administrative expenses, customer profiles, and potential regulatory impacts. Furthermore, a thorough analysis of contracts such as sales contracts, lease agreements, and employee contracts can provide a valuable source of information regarding projected future revenue and expenses.

It is not even necessary in all cases to demonstrate the existence of profits during that abbreviated period (Brookridge Party Center v. Fisher Foods, Inc.,12 Ohio App. 3d 130 (1983)). For example, most new businesses experience an initial period of diminishing losses followed by a gradual progression to profitability as the business moves up the learning curve. Losses in the initial stages of the business’ life cycle are to be expected, particularly if they remain in line with industry averages. If the business possesses the critical success factors specific to its particular enterprise, it can be reasonably expected to perform at least as well as the industry average, implying that it would “turn the corner” at some point in the future (along the industry average growth curve).

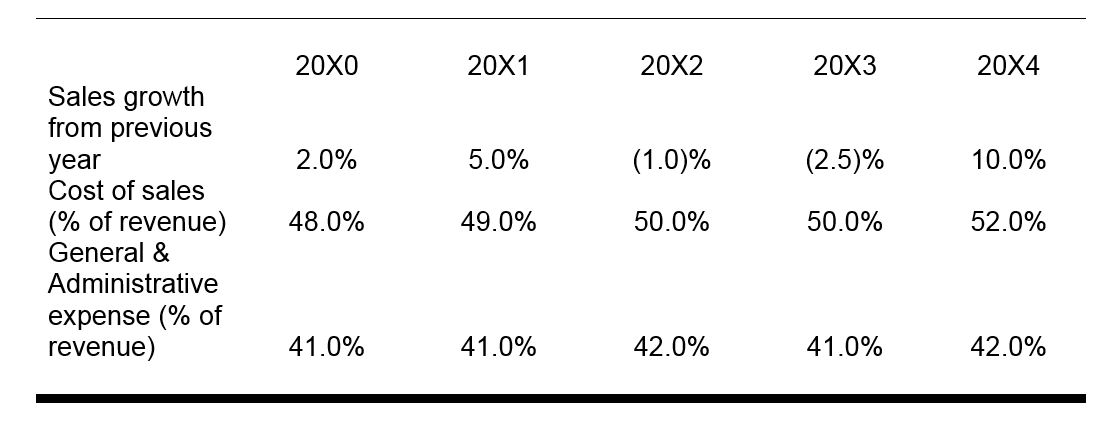

Example

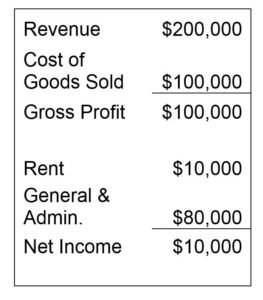

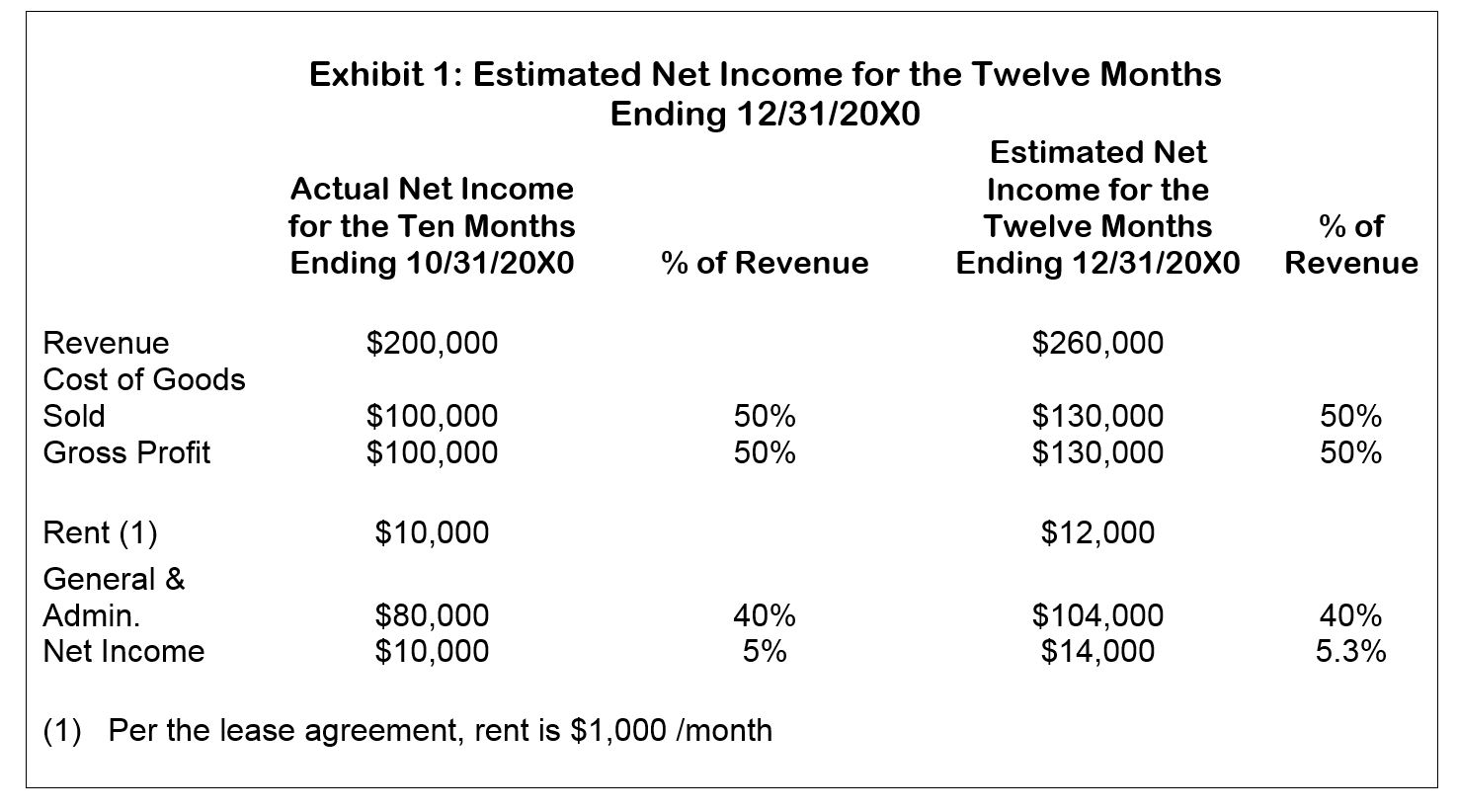

Assume a retail business commences operations on January 1, 20X0 and ceases business on October 31, 20X0 due to a contract breach. Furthermore, assume it is now January 20X5 and the case is going to trial. Actual net income for the ten months ending 10/31/20X0 is as follows:

Step 1

The first step involves projecting financial results achieved in the first 10 months over a 12-month period. Where possible, contracts or agreements should be used to determine future activity.

For example, let us assume that rent expense is fixed at $1,000 per month as stipulated by the lease agreement. Therefore, we would expect rent expense of $12,000 for the 12-month period ending 12/31/20X0 ($10,000 plus $2,000 rent for November and December). Where contracts and agreements cannot be used to project financial results, other techniques must be employed. Assume that an interview of similar retailers at the same location reveals that January to November sales are relatively constant, with December averaging twice that of any other single month. Multiplying actual financial results for the 10-month period ending 10/31/20X0 by a multiple of 13/10 provides a reasonable estimate of results for the year ended 12/31/20X0 (see Exhibit 1).

Step 2

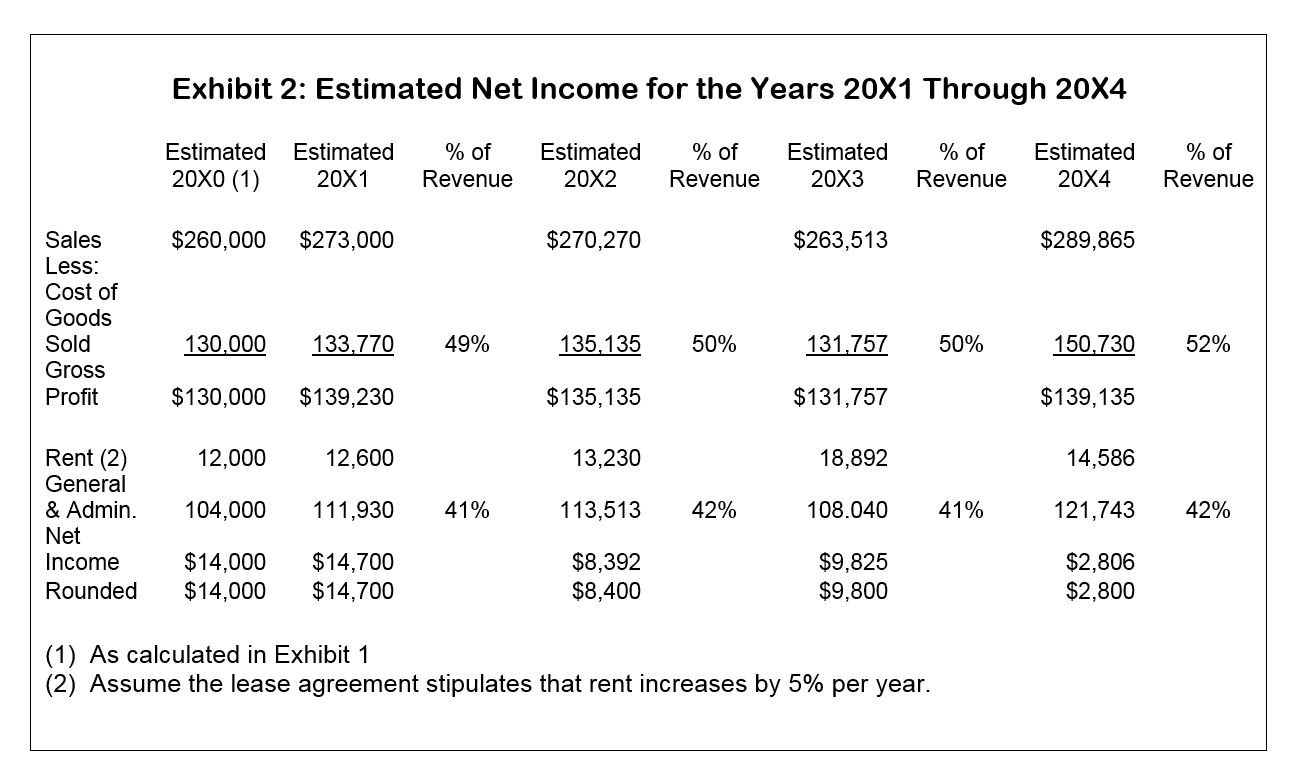

The next step involves accumulating industry data (statistics and financial ratios) for companies operating in the same industry as the injured company. This information can be accumulated by conducting database searches. For example, the SIC (standard industry code supplied by the IRS) for the injured company can be used to search databases such as Dunn & Bradstreet, NEXIS, and the SEC for financial data specific to that industry. Let us assume that the following information regarding financial results was uncovered thorough a database search for our example (see below).

These ratios can then be applied to the injured company to estimate financial results in the years 20X1 to 20X4 (see Exhibit 2).

Note that the estimated financial results in 20X0 do not exactly match industry ratios in that same year. One would expect a start-up company to operate with less efficiency than industry averages (which include companies with significant experience). However, given that actual financial results in the first 10 months ending 10/31/20X0 approximate industry ratios in 20X0, actual results for that 10-month period are used to project earnings in future years.

Losses suffered during initial operations do not necessarily preclude projection of profits in future years. For example, if the injured company in the example below suffered an actual loss in the first 10 months of 20X0, one could argue that industry ratios should be applied to actual revenue in 20X0 to estimate net income or net loss in 20X0. After all, as a start-up company, the injured company can expect losses in its initial period of growth. By utilizing industry ratios, we nullify the “start-up effect” by assuming performance of an established company.

Bear in mind that industry averages are meant merely as guidelines; they should not be taken verbatim. Industry average statistics and specific company statistics commonly differ, particularly when the specific company is a brand-new enterprise.

This means merely that industry statistics and ratios should be used as a starting point, with adjustments made to approximate the specific circumstances of the injured company. For example, if you know that the injured company utilizes a greater proportion of debt financing than the industry average, estimated interest expense should be increased accordingly. Additionally, if the injured company is more labor intensive than that of the industry average, salary expense should be adjusted accordingly.

Benchmarking

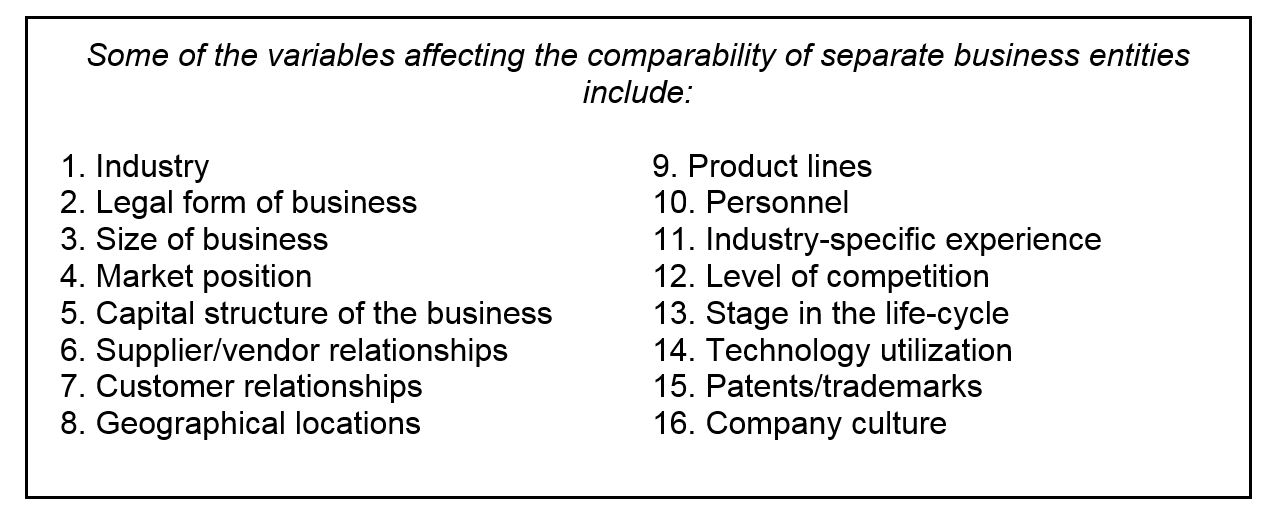

Another effective method often utilized to quantify lost profits when a business ceases operations is benchmarking (see Lehrman v. Gulf Oil Corp.,464 F.2d 26 (5th Cir. 1969). As the term suggests, benchmarking calculates likely anticipated earnings based on a relative comparison of the defunct business to a similar company in the same industry. Theoretically, a company that is comparable in size, location, management, product lines, and market position could experience the same approximate earnings stream. Earnings for a similar company can be used as a proxy for earnings of the defunct business provided that relevant factors are identified and determined roughly equivalent.

Although benchmarking makes intuitive sense, it can be difficult to implement. In practice, no two companies are equivalent, even in general terms. Differences in just one of the variables in the following box can make a tremendous difference in performance between two otherwise similar firms. For example, two publishing companies in the same city with similarly sized staffs may have vastly different earnings potential simply because they market their services to different clients.

Another potential difficulty with using benchmarking as a means for estimating lost earnings lies in the availability of information. Because of regulatory requirements, publicly traded companies must make selected financial and accounting information available to stakeholders and potential investors. Thus, benchmarking can usually be used on a general level for publicly traded companies. However, comparison of privately held and nonregulated companies becomes more difficult simply because information cannot be readily obtained.

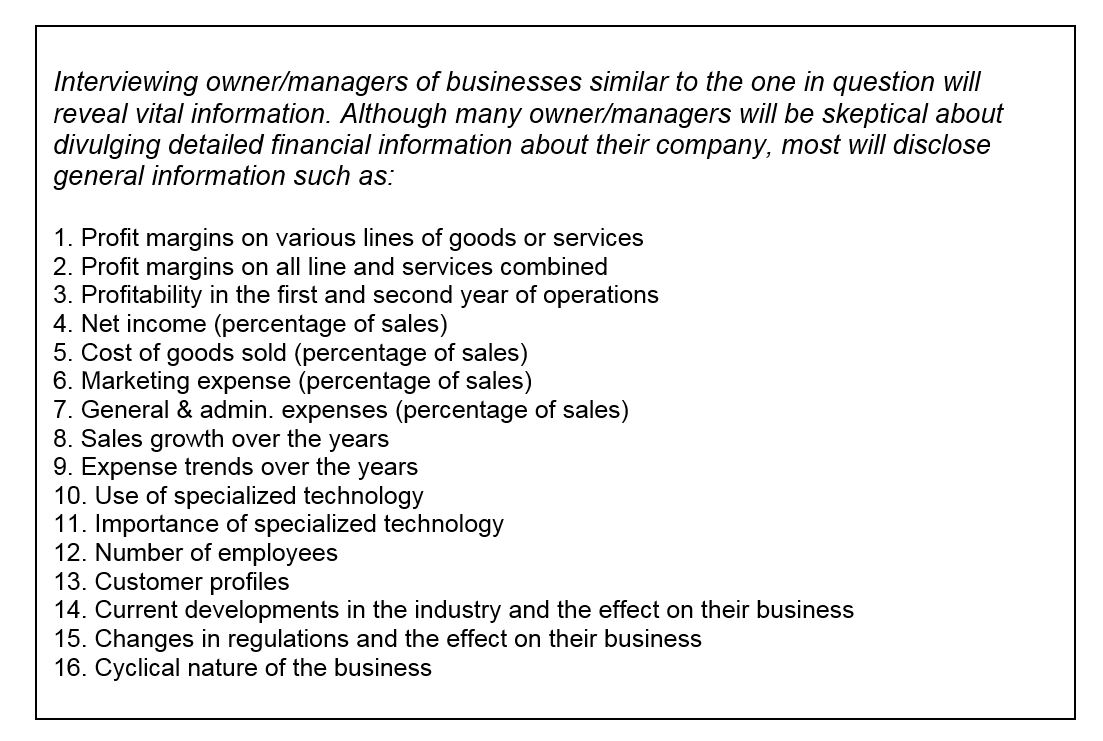

An effective method of overcoming the limitations in the availability of detailed information for privately held or nonregulated companies is through the use of interviews.

The key to using benchmarking as a means of quantifying lost profits is the realization that it can provide a general estimate of profits when little else is available. If a sufficiently similar business enterprise can be identified, benchmarking can be a powerful tool for demonstrating likely lost profits. Because of the assumptions made, however, benchmarking must be used carefully, with particular attention given to assumptions made about what constitutes a “mirror” company. As with other methods, critical success factors should be identified, both for the defunct business and potential “mirror” businesses. Furthermore, differences in facts between the injured company and the benchmarked company should be taken into consideration, and adjustments to financial results should be made accordingly.

Past Experiences, Injured Party

If the injured party has prior experience with a similar business, financial and operational information from that business may translate roughly into projections for the new, injured business. As is the case with benchmarking, the previous business should be examined carefully to ensure that it compares sufficiently to the new business. If the prior business passes the test of comparability, using past experience has the added benefit of intuitively including hard-to-quantify variables such as industry-specific experience (presumably the same with the same business owner/manager).

Conclusion

In determining lost profits for start-up companies with little or no prior earnings history, several methods can be utilized to arrive at an estimate backed by reasonable certainty. Crucial in selecting the method of projecting or applying those profits is the recognition of the individual characteristics of the business in question in relation to the industry and market as a whole. Numbers alone are not enough; qualitative as well as quantitative factors must be taken into account. In the final analysis, assumptions made and calculations performed must make sense from a general business perspective and must be supportable. Through an understanding of the strengths and weaknesses of common techniques for determining lost profits, an appropriate mix of approaches can be utilized to produce reasonably certain, supportable results.

The following is an adaptation of remarks by Simon M. Lorne, vice chairman and chief legal officer of Millennium Management LLC and business law advisor to the Professional Responsibility Committee, at its meeting at the Business Law Section’s 2017 Annual Meeting in Chicago.

In my years of practice, I’ve been privileged to occupy a number of different positions, from law firm partner, to the Securities Exchange Commission’s general counsel, to my current role as chief legal officer of a major hedge fund advisor. In all of those roles, I’ve been actively involved with this committee, and particularly with the question of how appropriately to balance the lawyer’s duty of client confidentiality with the ability to perceive, and perhaps to prevent, a course of client conduct that may subsequently be characterized by enforcement authorities—the SEC, the Commodity Futures Trading Commission, the Department of Justice, etc.—as client improprieties. Perhaps obviously, I choose my words carefully. When those authorities do challenge a course of conduct, they are likely to identify it as “fraud,” but it was likely not identified as such by the lawyer at the time, and to so characterize it is to bias the analysis of the lawyer’s obligation. Those questions were surfaced in a number of high-profile SEC cases from the 1970s to the early 1990s. The principal cases from that era are probably SEC v. National Student Marketing Corp., Fed. Sec. L. Rep. (CCH) ¶93,581 (DDC 1972); SEC v. Nat’l Student Marketing Corp., 402 F. Supp. 641 (DDC 1975); SEC v. Nat’l Student Marketing Corp., Fed. Sec. L. Rep. (CCH) ¶96,027 (DDC 1977); In re Carter, Sec. Exch. Act Rel. No. 17,597 (Feb. 28, 1981); and In re Kern, Sec. Exch. Act Rel. No. 29,356 (June 21, 1991).

These issues received focused attention from the securities bar in 2003 when the SEC adopted the Attorney Conduct Rules, Part 205 of Title 17 of the Code of Federal Regulations (the Rules). With that promulgation, law firms throughout the country (and in some foreign climes) adopted policies, established committees, saw to the education of younger attorneys, and in other ways prepared for the potential onslaught of SEC actions charging lawyers with a failure to act properly—generally defined in the rules as escalating attention to the chief legal officer and, if necessary, the board of directors whenever a lawyer “appearing and practicing” before the SEC became aware of “credible evidence” of a violation of the securities laws or breach of fiduciary obligations. Under the SEC’s interpretation of the Rules (although this remains a hotly contested point), the Rules further operated to pre-empt any contrary state law to permit such a lawyer to report a matter directly to the SEC if a matter were not handled appropriately (apparently, as determined by the lawyer’s own judgment) by the highest authority within the corporation.

Then a funny thing happened. Silence.

In what is now 14 years since the adoption of the Rules, the actual number of attorney conduct cases brought by the SEC, including both litigated cases and settled cases, has been . . . zero. There was one Department of Labor case in which the Rules were relevant to the purported wrongful discharge of a lawyer-employee, but that’s been it. See Jordan v. Sprint Nextel Corp., Dep’t. of Labor Admin. Review Bd. Case No. 06-105, ALJ Case No. 2006-SOX-041 (Sept. 30, 2009).

However, the Rules remain in place, and with inactivity on the SEC’s enforcement side (not that any lawyers I know are complaining about that inactivity), I feel comfortable in suggesting that many of the law firm policies and procedures initiated in response to the initial adoption of the Rules have fallen into disuse. It is almost certain that there are a number of lawyers today who have been practicing for as many as 10 years or more who have never even heard of the Rules, and that number only grows as we look at more recent law school graduates.

The enforcement environment will inevitably change, and I would not take much comfort in the notion that the current administration will be softer on enforcement. Historically (although, as the SEC requires us to say in another context, past performance may certainly be no indication of future results), SEC enforcement has often been tougher in Republican administrations, just as regulatory enhancements have been more relaxed. Be that as it may, there will in the future be a corporate fraud—we hope not on the scale of Enron or WorldCom—and there will be lawyers who will have been on the scene, who will have been “appearing and practicing” before the SEC, and who will have become aware of “credible evidence” of the fraud. They will find themselves on the wrong side of an SEC complaint, or perhaps worse, and they will wish that their law firm had been more diligent in impressing upon them the requirements of the Rules.

A court’s primary goal in the interpretation of a commercial contract is to discern the parties’ intentions. In Canada, courts use a range of tools to achieve this end. They look to the ordinary meaning of the words chosen by the parties in their agreement. They also consider which interpretation of the contract will give it business efficacy or which will make the most commercial sense.

A recent debate has emerged in Canadian contract law about whether and how courts should consider the parties’ conduct in determining their contractual intentions. In a leading case, Sattva Capital Corp. v. Creston Moly Corp., [2014] SCC 53, per Rothstein J., the Supreme Court of Canada made it clear that when interpreting a commercial agreement, courts should consider evidence of what it calls the “factual matrix” to determine the contract’s meaning.

The factual matrix “consists only of objective evidence of the background facts at the time of the execution of the contract—that is, knowledge that was or reasonably ought to have been within the knowledge of both parties at or before the date of contracting” (emphasis added).

Evidence of the factual matrix may very well include evidence of the parties’ negotiations and correspondence at the time they executed the agreement. In this way, Sattva aligns Canadian contract law with its American counterpart. See, for example, Droplets Inc. v. E*Trade Financial Corp., 939 F. Supp. 2d 336 (Apr. 4, 2013).

Sattva left one key issue unresolved, however: can a court consider evidence of the parties’ conduct after they enter into a commercial agreement as an aid to its interpretation?

Canadian courts have now answered this question in the affirmative, with one significant qualifier. Evidence of the parties’ post-contract conduct is admissible as an aid to contract interpretation, but only in cases of contractual ambiguity. In the absence of ambiguity, the evidence is inadmissible. Even where the court finds that evidence of the parties’ “subsequent conduct” is admissible, it must then decide whether to accord the evidence any weight. Shewchuk v. Blackmount Capital Inc., [2016] ONCA 912, per Strathy C.J.O., at ¶ 56.

This approach represents a departure from the rigid position in the United Kingdom, where post-agreement conduct has long been deemed inadmissible. See id. at ¶ 43 (citing James Miller & Partners Ltd. v. Whitworth Street Estate (Manchester Ltd.), [1970] A.C. 583 (H.L.), per Lord Reid, at 603; F.L. Shuler A.G. v. Wickman Machine Tool Sales Ltd., [1974] A.C. 235 (H.L.), per Lord Wilberforce, at 261. U.K. courts have expressed concern that if post-agreement evidence is used as a tool for contractual interpretation, the meaning of the commercial contract will change over time. This could undermine the principle of contractual certainty. As one U.K. court put it, “one might have the result that a contract meant one thing the day it was signed, but by reasons of subsequent events meant something different a month or a year later.” James Miller & Partners, supra, at 603.

In rejecting the U.K. position, Canadian courts are not blind to the inherent dangers of using the parties’ subsequent conduct to interpret a contract. In Shewchuk, which opened the door to the admissibility of evidence of the parties’ subsequent conduct, the court identified the perils of such evidence as:

allowing the meaning of the contract to fluctuate over time, as recognized by the U.K. courts;

ambiguity in that a party not enforcing strict legal rights under a contract does not necessarily mean that the party never enjoyed those rights; and

the commercial parties beginning to conduct themselves in a way that favors their interpretation of the contract; by admitting evidence of post-agreement conduct, the courts would be rewarding this type of self-serving behavior.

Despite these concerns, the Shewhuck court recognized that “evidence of subsequent conduct may be useful in resolving ambiguities”—that is, the parties’ behavior after the execution of the contract could support an inference regarding their original intentions at the time of contract formation. The court likened the evidence of post-contract conduct to a criminal’s behavior after the commission of an offence:

However, the lesson learned in Canada from the British position is that the parties’ subsequent conduct is relevant only to inferentially establishing their intentions at the time they executed their contract. Like evidence of post-offence conduct in criminal matters, it is a kind of circumstantial evidence that “invokes a retrospectant chain of reasoning”; the trier of fact is invited to infer the parties’ prior intentions from their later conduct. . . .

Once admitted, however, the evidence is still subject to the court’s scrutiny. The court must decide whether to give it any weight. In deciding the evidence’s reliability, the court will consider whether the conduct is that of both parties, is intentional, is consistent over time, and belongs to individuals, rather than agents of corporations. The court will also give the evidence more weight if it is unequivocal “in the sense of being consistent with only one of the two alternative interpretations of the contract.” Moreover, the closer in time to the execution of the contract, the more likely the evidence will be considered reliable.

The reasoning in Shewchuk remains to be tested. As a recent decision of the Ontario Court of Appeal, it is not yet clear whether Shewchuk has injected of level of contractual uncertainty in the Canadian legal landscape.

Despite all the safeguards in place to ensure that evidence of post-agreement conduct is properly admitted and weighed by the courts, commercial parties may be tempted to engage in self-serving behavior after the execution of the contract, knowing that there is a possibility such behavior could support their preferred interpretation of a contractual ambiguity.

Canadian courts must be on their guard and approach any evidence of the parties’ post-contract dealings with caution. They must bear in mind that post-agreement conduct is generally unreliable and often undermines the parties’ original contractual intentions.

Of all the ways that a merger can go wrong, it is hard to think of a worse scenario than the deal falling apart and the parties being subject to a criminal investigation. Lawyers are constantly tracking and negotiating terms in an effort to close the deal. And in this push to finalize the transaction and meet the expectations of clients and various regulatory agencies, practitioners can be faced with potential ramifications far more serious to the business than they ever would have expected (or, at least, had hoped not to expect).

At its surface, antitrust can neatly be divided into civil and criminal matters. Civil matters involve merger review, civil non‑merger conduct review, and civil litigation. Criminal matters generally consist of investigating violations of price-fixing, bid rigging, and market allocation. Two U.S. agencies, the Federal Trade Commission (FTC) and the U.S. Department of Justice Antitrust Division (Antitrust Division), are responsible for enforcing federal antitrust laws. While the FTC is solely civil, the Antitrust Division is separated into civil and criminal enforcement sections. The Antitrust Division’s offices responsible for criminal enforcement are located in Washington, D.C., San Francisco, Chicago, and New York. Although these criminal offices have assigned territories, they are not bound by geography, as investigations often take place across the country and around the globe. The six civil sections of the Antitrust Division are all located in Washington and are divided by subject matter expertise.

But that separation of criminal and civil enforcement sections at the Antitrust Division does not create walls or silos. The different criminal offices often work together on large investigations and trials. Similarly, the size of many civil investigations requires pulling resources from the various civil sections, as well as from the Antitrust Division’s Appellate, International, and Competition Policy and Advocacy sections. But the collaboration does not end there. Coordination between the civil and criminal sections is the norm. Section managers meet regularly to discuss matters and often consult on an informal basis. Cross‑pollination occurs at the trial attorney level as attorneys are detailed to other sections for specific matters or periods of time. And understanding this collaboration between the civil and criminal sections is vital to attorneys and their clients subject to the merger review process. A recent case not only shows how in sync the Antitrust Division’s criminal and civil sections are, but also highlights the implications of that collaboration.

In December 2014, two packaged seafood companies announced their proposed merger. As is customary to the review process, the parties submitted documents to one of the Antitrust Division’s civil sections. What followed was anything but routine. However, based on the level of collaboration within the Antitrust Division, it should not have been unexpected.

From document review to charges for price-fixing

The Antitrust Division’s civil attorneys reviewed the documents submitted by the parties and uncovered information that raised concerns of price‑fixing. When the parties walked away from the deal on December 3, 2015, then-Assistant Attorney General Bill Baer’s statement in the press release made a veiled reference to their problematic documents. He said, “Our investigation convinced us—and the parties knew or should have known from the get-go—that the market is not functioning competitively today, and further consolidation would only make things worse.”

The parties’ abandonment of the deal did not end the Antitrust Division’s investigation. Instead, the civil attorneys conducting the merger review shared their findings with their criminal counterparts. A criminal section proceeded to open a price‑fixing investigation based on the shared materials. That investigation has borne fruit and is ongoing. To date, three individuals and one company have been charged for participation in a price‑fixing conspiracy. Criminal antitrust violations, such as price-fixing, have serious implications. Not only are the criminal penalties substantial, but companies can be subject to civil suits with treble damages (15 U.S.C. § 15.).

For individuals, the maximum penalties are 10 years in prison and a $1 million fine. For corporations, the maximum fine is $100 million. Fines for both individuals and corporations can exceed the statutory maximum amount by up to twice the gain derived or twice the loss by victims. See, e.g., Price Fixing, Bid Rigging and Market Allocation: An Antitrust Primer, Department of Justice Antitrust Division, available at https://www.justice.gov/atr/priceifxing-bid-rigging-and-market-al location-schemes (discussing the Sherman Act).

While it is not public what specific information was contained in the documents that raised the attention of the reviewing attorneys, or exactly how the process happened, the Antitrust Division did state that the criminal investigation was triggered by “information and party materials produced in the ordinary course of business.” Until more information is revealed, several questions remain, including whether similar criminal investigations based on documents submitted for merger review could be waiting to surface.

The packaged seafood matter is not the first criminal case to stem from a civil investigation and likely will not be the last. The hand‑in‑hand coordination between the civil and criminal sections of the Antitrust Division will continue. Companies need to be increasingly aware of the risks that ordinary course documents present, not just in impacting merger approval but also in criminal implications. Merger review does not exist in a vacuum. Once documents fall into the Antitrust Division’s (or FTC’s) hands, parties can expect that they will be closely reviewed with an eye toward both civil and criminal actions. Documents always tell a story—and attorneys need to be sure that the story told is one to support a proposed deal and not a criminal investigation.

Similarly, the FTC and Antitrust Division share a close working relationship. We will continue to explore and monitor the collaboration between those two agencies as well as with state attorneys general. We also plan to address the collaboration among competition agencies around the world. Stay tuned.

Craig Lee and Creighton Macy are antitrust partners in Baker McKenzie’s Washington, D.C., office. Prior to joining the firm, Craig served as assistant chief of Washington Criminal 1 and Creighton served as chief of staff and senior counsel at the Antitrust Division. All discussions of DOJ matters in this article are based on public information.

In his latest book, The Undoing Project, author Michael Lewis introduces us to the fathers of behavioral economics, Amos Tversky and Daniel Kahneman. Its first chapter describes how Houston Rockets General Manager Daryl Morey used behavioral economics to rebuild the team beginning in 2007. The key, Daryl Morey noticed, was that his recruiters and coaching staff invariably fell prey to specific errors in their decision making when selecting players. For example, recruiters who found a candidate they liked tended to overvalue information reinforcing their decision and ignore information suggesting that the player should not, in fact, be drafted. Eliminate these errors in judgment, replacing “judgment calls” with hard data, and they could pay less for better players. This was the same approach the Oakland A’s used to achieve success during their famous 2002 baseball season and the subject of Michael Lewis’ prior book, Moneyball.

What is behavioral economics, and how does it relate to the work we do as business lawyers? In short, behavioral economics is the science of how people make decisions. By understanding the techniques people use to make their decisions, including those that cause us to occasionally make bad decisions, we can accomplish two things. First, we can help other people make better decisions (or perhaps, instead, make the decisions we want them to make). Second, we can better understand our own decision making processes and, with a more concrete understanding, improve them.Understanding decision making can improve our performance in a large number of arenas, but certainly assists in performing such tasks as negotiating deals, structuring contracts, or building compliance systems.

Behavioral economics builds on the traditional economics concept of normative decision theory, which describes the rules by which a fully rational individual makes choices. Normative decision theory makes two basic assumptions. First, that the person making choices has complete information. In other words, the person knows all the information relevant to making the choice. Second, normative decision theory assumes that the person is rational—that is, capable of making choices that are logical and consistent based on that person’s desires. For example, if a person prefers coffee to tea, and also prefers hot chocolate to coffee, then a rational person will ask for a hot chocolate when offered a choice between that and tea (this is called the principal of transitivity). When you know the logical rules by which rational persons make decisions, the argument goes, you can build mathematical and logic models of their behavior, use those models to predict results, and also develop responsive strategies. These rules of logical choice, called utility theory, were described by mathematician John von Neumann and economist Oskar Morganstern in their 1944 work, Theory of Games and Economic Behavior, and form the basis for modern game theory.

The problem with utility theory is its limited application in real-world situations. People don’t have complete information when they make decisions, and as Tversky and Kahneman proved, people do not follow the rules of rational decision making when making choices. Instead, decision making employs a variety of cognitive short cuts, called heuristics. Behavioral scientists, through empirical studies, have identified dozens of these heuristics. They bear names such as “planning fallacy,” “anchoring,” “confirmation bias,” and “loss aversion,” but they essentially describe the rules by which human minds tend to make decisions in place of the strict logical constructs that utility theory describes. In short, behavioral economics provides a useful tool for predicting and understanding decisions where standard economics tends to fail. For example, anchoring refers to a tendency to determine subjective values based on recent exposures to something similar, although unrelated. When asked to guess the percentage of African countries in the UN, people consistently pick a higher number when exposed to the number 65 than when exposed to the number 10 just prior to guessing.The planning fallacy refers to the consistent tendency to underestimate the length of time a task will take, even when a person has extensive experience performing that task. Kahneman and Tversky’s work is significant—Kahneman was awarded the Nobel Prize in Economics for his work in the area.

Understanding these rules can play a significant role in negotiations. For example, an attorney who understands how anchoring works can employ the concept to set expectations both for his client and the opposite party that are reasonable and conducive to obtaining a negotiated solution. In addition, the attorney can be more aware of situations where anchoring might be affecting her own decision making, resulting in a potentially poor negotiation outcome. This article explores some of the more significant heuristics and how they affect negotiations.

Planning Fallacy

In Thinking, Fast and Slow, Daniel Kahneman describes the process of planning a book for a psychology course. When he polled the group of authors about how long they thought the project would take, they estimated about two years. Kahneman then asked the most experienced member of the group how long similar projects had taken in the past. After a little thought, the expert replied, “I cannot think of any group that finished in less than seven years,” and he said that about 40 percent of the projects had failed to reach completion altogether! Still, even though none of the authors were prepared to make a seven-year investment in a project with only a 60-percent chance of success, they went ahead designing the book. They finished it eight years later, and it was never used.

Closely related to the optimism heuristic, the “planning fallacy” refers to the tendency for people to consistently underestimate both the time and costs for completing projects. Although the most obvious examples come from large public works projects, any lawyer can think of the times that a lawsuit, negotiation, or business deal took longer than expected and cost more than estimated. Empirical studies show that the planning fallacy reflects an underlying psychological tendency to ignore historical evidence when estimating the time and expense for a project. In one study, students were asked to estimate the length of time needed to complete and submit their honors thesis. The average estimated time was 34 days. The average actual time was 55 days. Follow-up studies showed that formalized planning and thinking about the results of prior projects had little effect on the planning error. Studies show not only that the planning fallacy is pervasive across different activities, but that even experienced professionals fall prey to planning errors on a consistent basis.

In a negotiation, the planning fallacy can play a significant role in how each side evaluates its positions. In a litigation situation, both sides will likely underestimate not only the amount of time needed to reach a conclusion, but also the cost of the litigation process. This will make them less likely to settle, based on a mistaken belief about the costs of reaching a non-negotiated resolution. In short, parties elect to take on unanticipated risks based on their unrealistic belief in the potential results. They fail to settle when they should because of the planning fallacy.

In a deal situation, the planning fallacy has a different, but equally unfortunate, effect. Parties will underestimate the time needed to work through the negotiations or even the amount of time needed to negotiate and draft the details of the relevant documents. The unpredicted delay creates frustration as tasks a client or her counsel thought would take a couple of days or maybe a week to complete remain unfinished weeks later. In some cases, this frustration, resulting from the original unrealistic expectations, can cause a deal to blow up.

Daniel Kahneman suggests that the best way of avoiding the planning fallacy is to use a technique called “reference class forecasting.” Essentially, reference class forecasting entails a four-step process. First, identify a set of similar activities. When trying to predict how much a lawsuit might cost in legal fees, for example, identify a group of similar lawsuits. This group of similar, prior lawsuits is your reference class. Second, collect data on the reference class. How long did those lawsuits last from beginning to end? How much were the total legal fees? This data provides the baseline for evaluating your own situation. So, if your firm has handled 10 similar types of lawsuits in the past, and the average legal fees incurred were $100,000, then $100,000 is your baseline. Third, evaluate the effect of concrete differences between your particular case and the reference class cases. For example, if your firm’s hourly rates have increased year over year, you will want to adjust the baseline estimate upward to reflect the increases in hourly rates. If some of the prior cases required more witnesses than your case will, you might adjust your estimate downward.

Finally, the fourth, and possibly hardest, step is to actually use the estimate and ignore your inevitable desire to use your original “prediction” about the cost in place of the hard data. By using a data-driven, objective approach to forecasting, you can reduce the planning fallacy effect and make better decisions in negotiations.

Anchoring

Amos Tversky and Daniel Kahneman ran an experiment where college students spun a number wheel rigged to stop only on the numbers 10 and 65. After each student spun the wheel, he or she had to guess the percentage of African nations in the United Nations. Oddly, the number on which the number wheel landed had a profound effect on the guess. Students whose spin resulting in a 10 guessed, on average, that 25 percent of African nations were in the UN, whereas the students whose spin resulted in a 65 had an average guess of 45 percent. Kahneman and Tversky called this mental heuristic—the tendency for a recently experienced number to affect decision making—“anchoring.” Kahneman describes anchoring as “one of the most reliable and robust results of experimental psychology.”

Most lawyers are familiar with the concept, although they might tend to think about it in basic terms. Lawyers learn to begin negotiations with either a high number or a low number to set expectations about the final result. Anchoring does work in this context, but anchoring effects also operate in subtle ways that are harder to identify and more effective than one might think. First, the number used as an anchor does not have to be related to the number being anchored. In the African nations experiment, the number on the wheel was unrelated to the question of how many African nations are in the UN, but greatly influenced the students’ decision making. In another common experiment, subjects are asked to write down the last few digits of their Social Security number and then guess the number of marbles in a jar. Subjects with higher Social Security numbers invariably guess higher. Anchoring effects are hard to shake and operate even where the subject has independent information on which to make a reasoned decision. In one experiment, real estate agents were told the listing price of a property and then were asked to appraise it. Even when they had complete information about the property, their appraisals remained anchored to the listing price (including when the listing price was clearly implausible).

According to Kahneman, two different mechanisms cause anchoring: one that operates when we consciously think about the decision, and one that operates when we do not. When we are making conscious decisions about values (what Kahneman refers to as System 2 thinking), we tend to find an initial anchor for the value and adjust from that value. We also tend to under-adjust. As a result, the starting point supplied has a very real effect on the final result. In a negotiation, making the first offer—or even opening negotiations with a discussion that includes appropriately scaled numbers—can help set that anchor point and thus affect the final negotiation results.

Anchoring also affects unconscious decision making (what Kahneman refers to as System 1) through something called the “priming” effect. In this context, the anchoring number can create mental associations that inform the final decision making. Although the mechanism is different, the final effect remains similar.

In negotiations, taking advantage of the anchoring effect means acting quickly, perhaps by making an early offer designed to anchor the final results, or perhaps by opening negotiations with a discussion designed to expose the other party to higher or lower numbers generally. Anchoring doesn’t necessarily have to target the final result. You might seek to anchor the inputs to the other party’s decision making processes, such as their view of your client’s cost of capital, litigation costs, or other factors. Also consider the setting for negotiations. Conducting a meeting in a cheap coffee shop might create mental associations that help you negotiate a lower price, whereas meeting in an expensive restaurant might have the opposite effect. In any negotiation, anchoring efforts should occur early in the process, before the other party has an opportunity to anchor based on its own decision making processes or other experiences.

Confirmation Bias

In Predictably Irrational, psychologist Daniel Ariely describes an experiment where he asked MIT students to taste-test two types of beer. One is a regular beer, and the other is the same beer, but with some balsamic vinegar added. They called this “MIT Beer.” Predictably, when forewarned that MIT Beer contained vinegar, the students preferred the regular beer. When they were not forewarned about the secret ingredient, however, the students typically preferred MIT Beer. This and similar experiments demonstrated that peoples’ prior perception of something strongly affects their interpretation of future experiences. This heuristic is commonly referred to as “confirmation bias”—the idea that we tend to interpret new facts and experiences in ways that reinforce our pre-existing beliefs. When we expect a beer to taste odd because we are told in advance that it contains vinegar, we are more likely to dislike the flavor when we actually drink the beer.

Confirmation bias affects how people process new information and leads to serious errors in judgment. For example, a lawyer who believes strongly in his client’s case might discount the effect of negative testimony at a deposition, focusing on the parts of the deposition that support his client’s position. As a result, he will fail to properly evaluate his case, concluding that the deposition testimony helped his case more than it hurt. A CEO trying to close an M&A transaction that she championed to her board of directors, with an eye on the big payoff from a successful merger, might ignore information about the buyer’s poor history of successfully integrating prior acquisition targets. Confirmation bias can affect how we and our clients process all kinds of information, including factual information, legal research results, case evaluation, and even the desirability of doing a deal in the first place.

This tendency to focus on facts that confirm pre-existing beliefs, while discounting facts that counter those beliefs, contributes to a related heuristic called “optimism bias.” Optimism bias is the demonstrated tendency for people to overestimate their chances of success in a particular endeavor. For example, one study found that 68 percent of entrepreneurs believe that their company is more likely to succeed than other similar companies; by definition, only 50 percent are more likely to succeed. Another study found that optimistic CEOs are 65 percent more likely to complete mergers and more likely to overpay, leading to a post-merger failure.

In negotiations, confirmation bias and optimism bias can lead to suboptimal decision making on both sides and interfere with parties reaching a deal. A seller might enter a negotiation discussing facts it thinks strongly support its decision and will help sway the buyer’s pricing, failing to realize the buyer discounts those facts. Particularly in a dispute, optimism bias can give each side an unrealistic viewpoint of its chance of success, leading to negotiation deadlocks. These heuristics are most likely to affect decision making where parties enter into negotiations already holding well-defined beliefs.

Understanding these cognitive effects helps us control the extent to which we might make misjudgments based on the information we receive during a negotiation. Confirmation bias can be countered by approaching, from the start of a matter, issues from an objective viewpoint. We can also counter bias by seeking input and feedback from objective third parties during the process and listening to what they have to say. A conscious effort can be made to identify negative information and carefully analyze the effect that information should have on our decisions. Careful, systematic approaches to evaluating information provide a way to counter confirmation bias in our own decision making.

Other parties in negotiations are also subject to confirmation bias. We can recognize that where the other side in a negotiation is starting with a different set of beliefs or a different starting viewpoint, they will evaluate the information shared during the negotiation in a different light. An effort to consider their point of view and evaluate how they are receiving and interpreting information will provide greater insight into their decision-making processes and make negotiations more productive.

Finally, like anchoring, these biases are best countered by opening negotiations and discussions early in the dispute-resolution process, before parties have an opportunity to develop strongly held beliefs about facts and positions.

Loss Aversion

Traditional economic theory posits that a dollar gained is equivalent to a dollar lost. Thus, people who have an item (a mug, for example) should be willing to sell that mug, on average, for the same price that a similar group of people would be willing to pay for a mug; however, that is not the case. In a famous experiment, people who had a mug wanted, on average, twice as much for the mug than people without a mug were willing to pay. This effect, called the “endowment effect,” has been demonstrated experimentally over and over again.People who have an item inherently give that item a higher value than those thinking about acquiring it. The endowment effect goes hand in hand with a concept Daniel Kahneman referred to as “loss aversion”—the simple idea that people fear losses more than they desire gains, and so the value of a thing, whether money or some other object, depends on the person’s point of view. A person viewing themselves as losing something places more value on the thing than someone who views the transaction as receiving the thing. As Kahneman put it, “losses loom larger than gains.”

Understanding how loss aversion might affect each party’s perception of value in a negotiation helps to understand the incentives behind each party’s positions. Understanding these incentives can help you to set up the negotiation to benefit your client or simply better align the party’s economic incentives to increase the chance of reaching a successful result. For example, imagine that you are negotiating whether your client’s business partner is due a performance bonus under a contract. If your client’s starting position is that the bonus was not earned, your client will view paying the bonus as a loss. On the other hand, where the bonus has been paid or escrowed already, and your client later discovered that its business partner was arguably not entitled to the bonus, your client might view any return of the bonus money as a gain. In the first situation, your client is less likely to want to pay any part of the bonus, potentially making settlement more difficult. On the other hand, when your client still has the funds, the other party might view any funds received as a gain and be more willing to settle. Here, loss aversion suggests making sure your client holds the funds pending negotiations; the combination of your client being less willing to pay, and the other party being more willing to settle, should result in a better settlement for your client.

Loss aversion also explains a benefit of escrows. Both sides should view funds placed in an escrow pending resolution of a dispute as held by a third party. For each side, it can only receive a gain from a resolution, not a loss. This will increase the willingness to settle and help bring together the parties negotiating positions. Loss aversion suggests using escrow arrangements even when both parties are financially capable of covering any payments that might need to be made.

The lawyer who can frame the negotiation’s effect on the other party as a gain should do better than when the effect is viewed as a loss. This might be done through prenegotiation litigation, such as by attaching a bank account or real estate. When this occurs, the other party gains from the settlement, rather than loses, and because the dollars gained are valued less than dollars lost, the other party should be willing to “pay” more for a settlement. Alternatively, a lawyer might frame the details of the deal so as to make an element appear as a gain instead of a loss. For example, in a shipping contract, a lawyer might start with a higher base price that includes insurance and offer a discount if the customer maintains its own insurance, rather than start with a lower base price and then try to get the customer to pay extra for the shipper to cover insurance. Loss aversion suggests that the customer will view the discount as a gain, and the payment of extra fees as a loss, and be more willing to forgo the discount than pay the extra fees.

Conclusion

This article describes just four of many biases and heuristics identified by behavioral economists through empirical research.The planning fallacy, anchoring, the confirmation bias, and loss aversion strike familiar chords among experienced attorneys. But, behavioral economics provides more than vague concepts about behavior. Its research provides deeper insights into exactly how and when these mechanisms operate, and also provides tools for mathematically modelling behavior in negotiations and litigation. Lawyers who become familiar with this new social science will undoubtedly gain an edge over their competition.

Additional Resources

Behavioral economics generally:

Lewis, Michael. The Undoing Project (W. W. Norton & Company, 2016) (as much a story about Daniel Kahneman and Amos Tversky as a book about behavioral economics, but an easy introduction to the subject).

Thaler, Richard & Sunstein, Cass. Nudge (Yale University Press, 2008).

Kahneman,Daniel. Thinking, Fast and Slow(Farrar, Straus and Giroux, 2011).

Planning fallacy:

Kahneman, Daniel and Amos Tversky. 1979. “Intuitive Prediction: Biases and Corrective Procedures.” TIMS Studies in Management Science, 12, 313–27.

Buehler, Roger, Dale Griffin, and Michael Ross. 1994. “Exploring the Planning Fallacy: Why People Underestimate their Task Completion Times.” 67 Journal of Personality and Social Psychology 366–81.

Anchoring:

Mussweiler, Thomas, Fritz Strack and Tim Pfeiffer. 2000. “Overcoming the Inevitable Anchoring Effect: Considering the Opposite Compensates for Selective Accessibility.” Personality and Social Psychology Bulletin 26: 1142–50.

Northcraft, Gregory B., and Margaret A. Neale. 1987. “Experts, Amateurs, and Real Estate: An Anchoring-and-Adjustment Perspective on Property Pricing Decision.” Organizational Behavior and Human Decision Processes 39: 84–97.

Tversky, Amos, and Daniel Kahneman. 1974. “Judgment under Uncertainty: Heuristics and Biases.” Science 185: 1124–30.

Confirmation bias:

Baker, Malcolm, Richard S. Ruback, and Jeffrey Wurgler. 2007. Behavioral Corporate Finance: A Survey, Vol. 1 of Handbook of Finance Series, Chap. 4.

Malmendier, Ulrike, and Geoffrey Tate. 2008. “Who Makes Acquisitions? CEO Overconfidence and the Market’s Reaction.” The Journal of Finance 89(1): 20–43.

Loss aversion:

Kahneman, Daniel, and Amos Tversky, 1976. “Prospect Theory: An Analysis of Decision Under Risk.” Econometrica 47: 263–91

Kahneman, Daniel,Knetsch, Jack L.; Thaler, Richard H. (1990). “Experimental Tests of the Endowment Effect and the Coase Theorem.” Journal of Political Economy. 98 (6): 1325–48.

Hossain, Tanjim, List, John A. (2012). “The Behavioralist Visits the Factory: Increasing Productivity Using Simple Framing Manipulations.” Management Science. 58 (12): 2151–67.

So long as marijuana remains illegal at the federal level, many financial institutions (FIs) will remain wary of the industry, no matter how many states legalize marijuana. However, there may be changes on the horizon for dispensaries and other marijuana-related businesses (MRBs) seeking access to banking services. According to a recent report from the Financial Crimes Enforcement Network (FinCEN), 368 banks and credit unions are providing services to MRBs. For MRBs, this is undoubtedly a positive, if still nascent, development. For this growth to continue, FIs and MRBs must work together to ensure that financial services are provided to, and used by, the marijuana industry in a responsible, safe, and sound manner.

The Regulatory Framework for Banking MRBs

Although marijuana remains illegal under the federal Controlled Substances Act (CSA), 29 states and the District of Columbia have authorized the use and sale of medical marijuana, and eight states and the District of Columbia have legalized its recreational use. In response to these developments, the Department of Justice’s Deputy Attorney General James M. Cole issued a memorandum in August 2013 advising U.S. attorneys on marijuana enforcement under the CSA, and then issued a second memorandum in February 2014 addressing application of federal law to FIs that deal with MRBs (collectively, the Cole Memos).

The Cole Memos direct DOJ attorneys and law enforcement to focus their resources on persons or organizations whose conduct interferes with any one or more of eight enforcement priorities, such as preventing the distribution of marijuana to minors. On the regulatory side, FinCEN has issued guidance (FinCEN Guidance) clarifying how FIs can provide services to MRBs consistent with their anti-money-laundering (AML) obligations under the Bank Secrecy Act (BSA). The FinCEN Guidance establishes unique suspicious-activity reporting (SAR) procedures for MRB-related accounts, including the filing of limited, priority, and termination SARs, depending on specific circumstances.

How Banks and Merchants Can Work Together to Improve MRB Banking

Together, the Cole Memos and FinCEN Guidance provide the framework for banking the marijuana industry. This framework is high level, however, and leaves most day-to-day compliance issues unaddressed. Given the regulatory challenges in banking MRBs, it is critical for banks and their MRB customers to develop a common understanding of these challenges and best practices for banking high-risk merchants.

From a bank’s perspective, the starting point for banking MRBs is ensuring that the bank has a BSA program that satisfies all of the regulatory basics. From there, the bank must enhance and tailor its program for dealing with MRB customers. FinCEN has directed banks to perform comprehensive due diligence on applicants, and then to monitor MRB customers closely once accounts are opened. Given these expectations, a bank may be better served by committing to providing services to the industry (and developing formal MRB-specific components within its AML program) than by accepting MRB customers on an ad hoc basis.

For MRBs, understanding the framework for banking marijuana and the pressures banks face when serving the marijuana industry is critical to developing and maintaining a successful banking relationship. There are a number of steps that can help put an MRB in the best possible position to work with a bank. Although obtaining all necessary state licenses to operate an MRB is a given, an MRB should also appoint a compliance officer and implement policies and procedures for compliance with applicable laws and requirements, including areas impacted by the Cole Memos.

When applying for a bank account, an MRB must provide accurate and truthful information in all applications and other materials submitted to a bank—providing false information to a bank is a potential federal offense. Once an account is opened, the MRB must use the account responsibly and in compliance with applicable laws and regulations. Similarly, MRBs should be prepared to provide any documentation or information the bank requests as part of its initial or ongoing due diligence.

Although banks are likely to continue to take a cautious approach to MRBs for the foreseeable future, MRBs and banks would both benefit from working together to ensure that banking services are provided in a safe, sound, and responsible manner. Doing so can help protect the banking system and ensure that responsible MRBs are able to obtain banking services.

On March 22, 2017, the U.S. Supreme Court addressed and decided whether features incorporated into the design of a useful article are eligible for protection under federal copyright law. In a 6-2 decision, and in an opinion written by Justice Thomas, the court held in Star Athletica, LLC v. Varsity Brands, Inc.that such features are protectable under federal copyright law only if: (i) they can be perceived as a two- or three-dimensional work of art separate from the useful article, and (ii) they would qualify as protectable pictorial, graphic, or sculptural work separately from the useful article into which they are incorporated. In the case, which concerned graphic design features of cheerleading uniforms, the court held that the conjunctive test announced in its decision had been met and that the designs at issue were protectable.

The underlying litigation arose from a copyright infringement complaint filed against Star Athletica for the marketing and sale of cheerleading uniforms that were claimed to be substantially similar to those designed, marketed, and sold by Varsity Brands. The principal basis and support for the complaint was 17 U.S.C. § 101, which protects “pictorial, graphic, or sculptural features” in the “design of a useful article” if they can be identified separately and can exist independently of the “utilitarian aspects of the article.”

Varsity had obtained “more than 200 U.S. copyright registrations for two-dimensional designs appearing on the surface of their uniforms and other garments,” which included shapes, lines, curves, angles, and “chevrons.” After summarizing the travel of the case in the lower courts and recounting the statutory definitions under the Copyright Act of 1976 (the Copyright Act) for “works of authorship” and “useful article,” the court defined the central question as “whether the arrangements of lines, chevrons, and colorful shapes appearing on the surface of respondents’ cheerleading uniforms are eligible for copyright protection as separable features of the design of those cheerleading uniforms.”