The Board of Governors of the Federal Reserve System (Fed), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) (collectively, the Agencies) issued the long-awaited final Interagency Guidance On Third-Party Relationships: Risk Management (Final Guidance) on June 6, 2023. The Final Guidance replaces the disparate set of guidance and FAQs separately issued by the Agencies over the years, thereby bringing greater consistency to supervisory expectations for banks in managing risks arising from their business relationships with service providers, contract counterparties, and other third parties.

The Final Guidance will be of particular interest to fintech companies, especially those that partner with or are looking to partner with banks. The Final Guidance explicitly calls out bank-fintech partnerships as within its purview, underscoring the potential risks raised by partnerships that involve novel or complex structures, as well as arrangements where the fintech company rather than the bank serves as the main point of contact for interactions with the end user (such as certain banking-as-a-service models).

Fintech companies that currently partner with banks, or are seeking to, should pay close attention to the Final Guidance, as it is now the definitive source of guidance on supervisory expectations and also a sign of greater supervisory scrutiny on such partnerships. Small banks, which many fintech companies tend to partner with, will likely find the new guidance challenging to implement. In a rare dissenting statement, Federal Reserve Governor Bowman predicted that more resources will be needed to “ensure that small banks understand and can effectively use the guidance to inform their third-party risk management processes.” The Final Guidance notes that the Agencies plan to, but have not yet, developed these additional resources to assist community banks and other smaller banks. Consequently, fintech companies looking to partner with banks, especially small banks, should be prepared for a more rigorous and potentially drawn-out diligence process with their potential bank partner, as well as ongoing monitoring.

Overview of the Final Guidance

Banking organizations are required to operate in a safe and sound manner and in compliance with applicable regulations, whether their activities are performed internally or outsourced to a third party. Operating in a safe and sound manner requires a bank to establish risk management practices governing its activities, including risks arising from its third-party relationships. The Final Guidance provides sound risk management principles that banks can use when developing and implementing risk management practices to assess and manage risks associated with third-party relationships.

The Final Guidance is striking in its expansive scope. It broadly defines third-party relationships, encompassing any business arrangement between a banking organization and another entity, whether the arrangement is formalized by contract or otherwise established. Included in the scope of third-party relationships are:

outsourced services,

the use of independent consultants,

referral arrangements,

merchant payment processing services,

services provided by affiliates and subsidiaries, and

joint ventures.

Importantly, the Final Guidance emphasizes that a bank’s use of such third parties does not diminish or remove its responsibilities to meet those requirements and ensure compliance with applicable regulations, such as those related to consumer protection and financial crimes. In issuing the Final Guidance, the Agencies sought to promote consistency in supervisory approaches to third-party risk management by replacing each agency’s existing guidance on the topic,[1] each of which is rescinded and replaced by the Final Guidance.

Key Considerations for Fintech Companies

The Final Guidance lays out a risk management framework that outlines a series of essential steps for banking organizations that partner with fintech companies, including engaging in sufficient planning, conducting due diligence for third-party selection, negotiating contracts, monitoring on an ongoing basis, and, if necessary, effecting efficient termination. The Final Guidance also details a set of best practices for governance of third-party risk management, including oversight and accountability, independent reviews, and documentation and reporting.

Fintech companies seeking to enter into partnerships with banks should take note of the following key areas in the Final Guidance:

1. Heightened due diligence requirements

The Final Guidance calls for the scope and degree of a bank’s due diligence to align with the level of risk and complexity of the third-party relationship. Fintech companies should pay particular attention to this requirement, as the Final Guidance states that greater operational or technological complexity leads to increased risk. It is likely that a fintech company that is preparing to partner with a bank will have to undergo more thorough and rigorous due diligence with the bank. If the fintech companies will perform higher-risk activities, including critical activities, the Final Guidance calls for more comprehensive diligence.

The Final Guidance sets forth a wide range of topics that, as part of its due diligence, a banking organization should consider about a third party:

strategies and goals;

legal and regulatory compliance;

financial condition;

business experience;

the qualification and backgrounds of key personnel and other human resources considerations of a third party;

risk management;

information security;

management of information systems;

operational resilience;

incident reporting and management process;

physical security;

reliance on subcontractors;

insurance coverage; and

contractual arrangements with other parties.

2. Contract negotiation

The Final Guidance stresses the importance of contract negotiation for banks when entering into third-party arrangements. While a fintech company may initially seek to offer its own standard contract or form provisions, a bank may try to seek modifications, resulting in a more involved and drawn-out negotiation than a fintech might expect to encounter with other entities. Fintech companies should therefore expect greater attention from banks than their typical transaction counterparties in the following commercial terms, on the basis of the Final Guidance:

nature and scope of the arrangement;

performance measures or benchmarks;

responsibilities for providing, receiving, and retaining information;

the right to audit and require remediation;

responsibility for compliance with applicable laws and regulations;

cost and compensation;

ownership and license;

confidentiality and integrity;

operational resilience and business continuity;

indemnification and limits on liability;

insurance;

dispute resolutions and customer complaints;

subcontracting;

foreign-based third parties;

default and termination; and

regulatory supervision.

Moreover, the Final Guidance states that if a contract is unacceptable for a bank, the bank may consider other approaches, such as looking to bring the activity in-house or looking to other third parties. Accordingly, it will be important for fintech companies negotiating with banks to ensure that they are adequately protecting their own interests and, at the same time, address where appropriate the many areas of focus that their bank counterparty is now expected to scrutinize. For additional insights into strategic approaches to contracting for fintech companies, please see a recent article the co-authors have written separately discussing “Financial Infrastructure as a Service: Top Legal Considerations for Innovators.”

3. Ongoing monitoring

The Final Guidance also requires banks to engage in ongoing monitoring throughout the duration of a third-party relationship, commensurate with the level of risk and complexity of the relationship and the activity performed by the third party. Fintech companies should expect the following examples of typical monitoring activities from their bank partner:

review of reports regarding their performance and the effectiveness of their controls;

periodic visits and meetings with their representatives to discuss performance and operational issues; and

regular testing of the bank’s controls that manage risks from its third-party relationships, particularly when supporting higher-risk activities, including critical activities (in certain circumstances, based on risk, a bank may also perform direct testing of the third party’s own controls).

Awareness of the areas of supervisory sensitivity will be critical to a fintech company’s success in partnering with a bank to deliver banking services.

Additional Considerations

The Agencies declined to establish any “safe harbors” in the Final Guidance, even for small banks. Rather, key to the third-party risk management framework—as contemplated under the Final Guidance—is the need for banks to tailor their risk management practices commensurate to their size, complexity, risk profile, and the nature of their third-party relationships. This tailored approach acknowledges the variety among different third-party relationships and the unique challenges that arise from such relationships. However, given the breadth of the Final Guidance, this tailoring may be easier said than done, particularly for community banks.

With respect to supervisory exams of a bank’s third-party risk management, the Final Guidance noted that supervision will also be tailored based on the degree of risk and the complexity associated with the bank’s activities and its third-party relationships. While the Final Guidance focuses on bank responsibility for third-party arrangements, it also recognizes that in certain circumstances, an agency may examine the functions or operations that a third party performs on behalf of a banking organization, allowing the Agencies the flexibility needed to address the unique challenges faced by the range of banking organizations and their various types of third-party relationships. In these cases, the agency may address violations of laws and regulations through corrective measures, including enforcement actions, to address unsafe practices by the third party.

Takeaway

Small banks in particular are likely to face challenges in implementing the Final Guidance and some degree of uncertainty in meeting supervisory expectations, which may translate to more challenging contract negotiation dynamics for fintech companies and greater hesitation by banks to enter into innovative arrangements. As bank-fintech partnerships increase in their complexity and incorporate novel strategies or technologies, the Agencies will require banks to step up their risk management, which their fintech partners will need to address.

SR Letter 13–19/CA Letter 13–21, “Guidance on Managing Outsourcing Risk” (December 5, 2013, updated February 26, 2021); FIL–44–2008, “Guidance for Managing Third-Party Risk” (June 6, 2008); OCC Bulletin 2013–29, “Third-Party Relationships: Risk Management Guidance,” and OCC Bulletin 2020–10, “Third-Party Relationships: Frequently Asked Questions to Supplement OCC Bulletin 2013–29.” ↑

The furthest- and widest-reaching federal business entity law ever enacted, the Corporate Transparency Act (“CTA” or “Act”)[1] will impact an estimated 32.6 million current businesses, with its implementation going into effect on January 1, 2024. An estimated additional five million newly formed businesses will also be swept under the CTA’s purview each subsequent year.[2] However, many business owners, investors, and advisers are unaware of the CTA and its looming deadline, and when they learn of it, they are often taken aback by its scope (and even its mere existence). Now is the time to review the CTA’s requirements and get prepared before the law goes into effect at the beginning of next year.

CTA Overview

The CTA requires certain businesses (including privately held and nonprofit entities) to report direct and indirect, human, beneficial ownership, control, and service provider information to the Financial Crimes Enforcement Network (“FinCEN”) of the U.S. Department of Treasury.[3] This information will be used by federal, state, local, and tribal law enforcement authorities to streamline their investigations, bypassing the “shell game” historically posed by multiple levels of business entity ownership and affiliation.[4]

Covered Businesses

The CTA impacts “reporting companies,” which include corporations, limited liability companies, limited partnerships, business trusts, and other “similar entities”[5] that are created or registered by the filing of a document with a secretary of state or a similar Indian tribal office.[6] There is no “grandfathering” of previously formed entities: the CTA will sweep in all business entities in existence on January 1, 2024. Exempted from the CTA’s reporting regime are specified excluded entities, which generally include heavily regulated business entities or large operating companies. However, the vast majority of private businesses and many nonprofit businesses will be swept up in required compliance.

Reportable Information and Owners

The information to be reported to FinCEN (“beneficial owner information,” or “BOI”) is certain personal identifying information (“PII”), which includes (1) full legal name, (2) date of birth, (3) residential (or sometimes business) physical commercial street address, and (4) an image of an acceptable government-issued ID (e.g., a U.S. passport or state-issued driver’s license) that includes both an ID number and the person’s photograph.[7] This reported information must be kept current and accurate with FinCEN by the reporting company on an ongoing basis.

This information will need to be reported for persons who have “substantial control” over the business or who own, directly or indirectly, 25 percent or more of the equity in the business (each a beneficial owner). Every business will have at least one person to report, regardless of its ownership structure. In many instances, informed business decisions will need to be made as to who constitutes reportable beneficial owners.

For reporting companies formed on or after January 1, 2024, the same PII must also be reported for “company applicants” (i.e., incorporators and organizers), including those who directed the formation filing. This reported information is only reported as of the reporting company’s formation and is not required to be updated with FinCEN thereafter.

Mechanics and Timing of Filings

Filings will be made through an electronic interface with the online Beneficial Ownership Secure System (“BOSS”).

Businesses in existence on January 1, 2024, will have one year to file their initial report—but file an initial report they must do, even if they subsequently dissolve or otherwise alter their structure in a manner to become compliant with a CTA exemption. Businesses formed on or after January 1, 2024, will have thirty days from formation to file their initial report with FinCEN.

Any change to the status quo of a business in existence on January 1, 2024, will need to be reported as a separate amendment filing, delivered with the initial “as of January 1, 2024” report filing required to be made on or before December 31, 2024. Businesses formed on or after January 1, 2024, will have thirty days to file a correction or change to any information previously reported.

Penalties

There are steep, escalating fines ($500 per day up to $10,000 per violation) and possible jail time (up to two years) for those failing to timely and properly comply with the CTA’s requirements.[8]

It bears noting that failure to timely file a required initial report could result in up to a $10,000 fine but that subsequent events that would necessitate an amendment to such required but missing filing, had the initial report been made, would also cause penalties to accrue—meaning that a failure to file an initial report may result in aggregate fines accruing well in excess of $10,000 prior to an initial notification of violation from FinCEN to the reporting company. Also, the intent of the reporting company and its agent with regard to noncompliance will be a factor in FinCEN’s assessment of possible criminal penalties.

Bearing this in mind, the remainder of this article is an appeal to the better angels of our character—as well as a direct rebuttal of initial impulses expressed by many upon first learning of the CTA.

CTA Denial

“I am a sophisticated business owner, and I have never heard of this.”

The enactment of the CTA in 2021 came as a shock to many (to some, a much later aftershock). However, the CTA’s intent—to end the position of the United States as a haven for “shell” companies used in the commission of money laundering, terrorist financing, financial and tax fraud, and other domestic and international illicit activity and corrupt practices—was present in proposed federal legislation for decades.

The CTA marks a seismic shift in the legal landscape for businesses operating in the United States. Prior to the CTA, entity beneficial owner disclosure was solely (if at all) the purview of state or tribal law. Now it is a focus and purview of federal law enforcement agencies.

The CTA has largely flown under the radar to date, but it is now time to become educated on the actions that may be taken prior to the CTA’s January 1, 2024, implementation date, and after. The Act’s impact on and implications for businesses, particularly small businesses, are complicated and difficult to succinctly communicate, and the CTA has not received widespread mass media attention. In fact, federal lawmakers and industry groups have decried the lack of CTA public education undertaken by FinCEN to date.

Many professional advisers and business professionals have been caught off guard by this fundamental change in business entity law, now taking on a federal facet for the first time. Those that are aware have, by and large, taken a wait-and-see approach to either advising their clients and business associates or evaluating their own compliance profile. This is because much of the mechanics of compliance remains elusive. The ability for businesses to begin directly interfacing with FinCEN on filing and compliance continues to be in the future, giving those persons “in the know” little to offer as current action items—causing many to defer sounding the alarm bell until more is known from FinCEN. However, the wait must end, as there is limited and dwindling time remaining to take action before the window of opportunity closes at the end of 2023.

“I have a small business. The Corporate Transparency Act only applies to large businesses.”

The CTA’s impact on small businesses is counterintuitive to many business owners, who erroneously believe that their business is “too small” to be within FinCEN’s sights and the CTA’s purview. Quite the opposite: A business’s small size is precisely why such a business must comply with the Act! The Act is designed to cast a broad net to “catch” a small niche of nefarious actors hiding behind the “corporate veil.”

Unfortunately, the vast majority of business entities that now must comply with the CTA, including most small businesses, are unwitting and innocent bycatch in the CTA’s net. This is because they will not be able to meet the criteria to be a large operating company that is expressly excluded from CTA compliance. The CTA’s “large operating company” exception is an exception to the CTA’s reporting requirements for businesses that meet all three of the following criteria:

The business must have a commercial, physical street address in the United States.

The business must have twenty-one or more full-time employees (excluding full-time equivalent employees, part-time employees, independent contractors, and leased employees).

The business must have filed a prior year’s federal income tax return demonstrating more than $5 million in annual, U.S.-only, gross receipts or sales.

All home-based businesses, and those with only a virtual (online) presence, will not meet the physical street address part of this three-part test. In addition, by necessity, every business entity formed on or after January 1, 2024, will not initially qualify for this exclusion because such business entities will not have the prior year’s tax return necessary to establish the gross revenue part of the test. The same will be true of virtually all business entities formed between January 1, 2023, and December 31, 2023. Further, many large portfolios of business entities will likely not meet this exception because employees of the portfolio’s operations are typically consolidated into one, or a few, of the portfolio’s business entities, with the remaining business entities not having employees, thus failing the employee prong of the test. Under FinCEN’s BOI Final Rule,[9] employee head count may not be attributed across affiliated entities for purposes of meeting the employee count threshold—each business entity must stand alone in this respect.

“My industry’s lobbyists would never allow such a law to get passed.”

Lobbyists had staved off attempts to implement the CTA, and its predecessor bills, for decades. However, in December 2020, the U.S. Congress, majority-controlled by Republican lawmakers in both the House and the Senate, passed the CTA as part of the 2021 National Defense Authorization Act—which then-President Donald Trump vetoed[10] (his sole veto during his term of office). On January 1, 2021, Congress, by a two-thirds vote in both the House and Senate, overrode Trump’s veto and passed the CTA into law.

Since the CTA’s adoption, the political landscape has changed. President Joe Biden and a Democratic-controlled Senate now hold office through at least 2024. A change of party control, if any, of the presidency or the Senate will not take effect until mid-January 2025—and control of the House may then also be uncertain. By that time, all existing business entities will have been required to file their initial CTA report into the BOSS, and a full year of newly formed entities will also have been required to comply with the CTA. In short, hopes of a conservative government sea change, with an overturning of the CTA, doesn’t account for the Act’s conservative lawmaker origins or the political cycle timing between now and the Act’s January 1, 2024, implementation.

Hope for a legislative repeal or delay in the implementation of the CTA likely ended with the recent passage of the bipartisan Fiscal Responsibility Act of 2023 ( “debt ceiling bill”),[11] which lacked provisions pertaining to the CTA. In mid-June 2023, subsequent to the passage of the debt ceiling bill, the Accountability Through Confirmation Act and the Protecting Small Business Information Act were each introduced in the House Financial Services Committee by Committee Chairman Patrick McHenry (R-NC). These bills are intended to effectively delay the date that the BOI reporting requirements go into effect and to “reform” FinCEN with requirements intended to increase transparency and accountability within the agency, while protecting individuals’ privacy and businesses’ sensitive information in the BOSS reporting regime. It bears noting that Representative McHenry was also the sponsor of the debt ceiling bill. With the current gridlock in Congress, these new bills seem unlikely to move beyond the House or to become laws.

Further, the Biden administration has shown no indication of delaying the CTA’s implementation, with the U.S. Department of Treasury and FinCEN expressing publicly, and repeatedly, that implementation of the CTA by the end of 2023 is a top priority. The stated goals of the CTA—combating the use of “shell” companies in the commission of money laundering, terrorist financing, financial and tax fraud, and other domestic and international illicit activity and corrupt practices—appear to align with the administration’s agenda. In other matters, the administration has shown a proclivity to support initiatives to reign in business rather than favor it.

The CTA mandated that FinCEN promulgate regulations under the CTA prior to January 1, 2022. On December 7, 2021, FinCEN published a proposed rule related to BOI under the CTA, with a public comment period extending through February 7, 2022. In response to this notice of proposed rulemaking (NPRM), FinCEN received over 240 formal comments, with submissions coming from a broad array of individuals and organizations, including members of Congress, government officials, groups representing small-business interests, corporate transparency advocacy groups, the financial industry and trade associations representing their members, law enforcement representatives, and other interested groups and individuals. In addition to these formal responses to the NPRM, FinCEN also received, accepted, and considered many additional comments and inquiries from the public. The extensive, thorough, detailed, and pointed feedback, often in direct opposition to the proposed implementation of the Act and to specific components of the Act, was considered, weighed, and utilized by FinCEN in its adoption of the CTA BOI Final Rule, issued on September 30, 2022. FinCEN went to great length in the Final Rule to describe, with specificity, the extreme vetting on each point in the Final Rule. That Final Rule, with limited exceptions, stayed true to the CTA and the proposed rule initially proposed. FinCEN did not exercise its discretion to expand the list or scope of the enumerated reporting company exceptions (in spite of numerous pleas to do so), nor did it show any reluctance to, or anticipate delay in, implementing the CTA. Based on this process, the implementation of compliance and enforcement of the CTA’s reporting obligations will most certainly begin January 1, 2024. Hopes that a “white knight” will ride in to thwart the CTA, or that a delay or elimination of this reporting obligation implementation would occur, were vanquished last year (in 2022) and confirmed by the CTA’s omission from the bipartisan debt ceiling bill.

“That can’t be constitutional.”

A lone small business advocacy group, National Small Business United (affiliated with the National Small Business Association), has filed suit against the U.S. Department of Treasury and FinCEN contesting the constitutionality of Congress’s actions in passing the CTA into law, as well as the CTA’s implementation by FinCEN. Three other advocacy groups (Transparency International U.S., Financial Accountability & Corporate Transparency Coalition, and Main Street Alliance) jointly authored an amicus brief in support of the government’s position and the CTA. This case remains in an early stage of pleadings.[12] Pending the outcome of this case, the constitutionality of the CTA will be affirmed or better defined.

“I just won’t report.”

Statements similar to the foregoing are uttered by a shocking number of business owners with whom I speak about the CTA and its reach, application, and exposure. However, there are a number of factors uniquely associated with the CTA, its origins, and its implementation that make its enforcement and your possible noncompliance exceptionally problematic. Chief among these, at least for individuals,[13] is that their refusal will be conspicuously noted on a reporting company’s filing with FinCEN. A checkbox is included on the BOI reporting questionnaire: “(check if you are unable to obtain any required information on one or more Beneficial Owners).” Once checked, this conspicuous omission will be a red flag to FinCEN, and other law enforcement agencies, for initial or further investigation.

Further, the Internal Revenue Service (“IRS”) recently announced its taxpayer enforcement initiatives, which include plans to hire nearly 87,000 new employees and invest $80 billion over the coming years[14] to improve tax enforcement and customer service, with more than one-third of the new hires being enforcement staff. The agency also plans to hire more data scientists to complement traditional tax attorneys and revenue agents in using new data analytics technology to identify audit targets. FinCEN’s BOSS database, created under the CTA, will likely be a key component to such data analytics technology and will provide an inexpensive, efficient investigative tool and corroborating (or “red flag”) source of taxpayer information for the IRS. The IRS initiatives’ stated aims are to close the “tax gap” between taxes owed and those paid, and to rebuild the IRS’s audit capabilities and computer technology. The IRS’s stated goals also include expanding enforcement for taxpayers with complex tax filings and high-dollar noncompliance, including high-income and high-wealth individuals, complex partnerships, and large corporations.[15]

Hopes that the CTA is nothing more than another pro forma survey data collection initiative by the government are naïve and misguided. FinCEN’s BOSS database will be a critical point of diligence for investigation by federal government agencies. Your business entity’s conspicuous absence from the BOSS database, or your personal omission from a reporting company’s CTA filing, will most certainly be discovered—and will spearhead other federal investigations into you and your business practices.

“If I get caught, I’ll just pay the fine.”

The CTA provides for civil fines of $500 per day, up to $10,000, per violation of the Act. The Act also provides for a criminal penalty of up to two years’ imprisonment for CTA violations. It is important to note that the fine is per violation—not simply for violating the Act. The Act has requirements for filing report corrections and amendments based on changing circumstances, and CTA violations will likely involve multiple instances of noncompliance before FinCEN comes knocking on your door. Each reporting obligation also has a very short window (thirty calendar days) within which to make the required filing, making inadvertent violations of the CTA highly likely. Further, with only twenty days needed to reach the maximum fine of $10,000 per violation, many violations will likely come with the maximum $10,000 price tag.

These factors, in combination, could cause a simple act of not reporting to turn into the accrual of tens of thousands of dollars, or even hundreds of thousands of dollars, in fines by the time FinCEN identifies the violation and pursues collection. This will be particularly true in the first year of implementation, when 32.6 million reporting companies are projected to require reporting, with five million additional reporting companies being added each year thereafter.

Also, did I mention prison time? Noncompliance could be a costly proposition—far in excess of an initial $10,000 price tag.

“CTA responsibilities do not implicate fiduciary duties.”

Persons with “substantial control” over a reporting company under the CTA not only will be required to disclose their own PII as “beneficial owners” of the reporting company but will also, in many instances, owe fiduciary duties to the reporting company as well as to the (other) owners of the reporting company to properly comply with the CTA. Any decision by a reporting company’s management not to report under the CTA, or to partially report or to inaccurately report, will directly implicate actionable duties owed to the reporting company, its owners, and possibly third parties. Further, such actions may constitute “for cause” termination events with respect to such “substantial control” person, as the act or omission may constitute gross negligence, willful misconduct, fraud, material misrepresentation, or an illegal act with respect to the reporting company. A “substantial control” person’s evasion of the law could also implicate denial or cancellation of the reporting company’s directors and officers (D&O) insurance coverage for the event in question, and expose the individual to uncovered personal liability for the action in question. Further, grievous failure to comply with the CTA could result in imposition of a criminal sentence of up to two years in federal prison for the offending individual.

Under most states’ business statutes, the concept of fiduciary duties is prevalent and applies to the behavior of officers, managers, directors, and other governing and management parties to the business entity itself and, in some instances, to the owners of the business entity directly. Principal among the fiduciary duties is the “duty of care.” The duty of care requires that a person act with the prudence that a reasonable person in similar circumstances would use. If a person’s actions do not meet this standard of care, then the acts are considered negligent and may result in actionable damages enforceable against the individual. However, a fiduciary may discharge the duty of care by exerting appropriate diligence and informed consideration with respect to the action in question. Further, in most instances, a fiduciary may discharge its duty of care on a subject by hiring a professional adviser that the fiduciary reasonably believes has the necessary experience and expertise to advise on the subject and by relying on such advice in making the business decision. Thus, “substantial control” persons may insulate themselves against duty-of-care claims by retaining legal counsel to evaluate and advise on the reporting business decisions in question. Further, to the extent that a waiver of fiduciary duties is permitted by the applicable state and included in the applicable business entity’s charter documents, such waiver will not extend to the fiduciary duty of good faith, which could be implicated by a failure to file a CTA report.

Conclusion

The Corporate Transparency Act is a seismic shift in the beneficial owner reporting regimes in the United States, disturbing long-established norms. Beginning January 1, 2024, tens of millions of unwitting and innocent U.S. business entities, and their beneficial owners, will become bycatch in FinCEN’s dragnet designed to catch nefarious actors hiding behind the “corporate veil.” Whether you like it, hate it, or are indifferent, the CTA has been thoroughly vetted and is here to stay. Compliance is both mandatory and advisable. Just as anonymity in the business entity structure has been pierced by the CTA, so has anonymity in the Act’s compliance, with various touch points and red flags aiding in FinCEN’s ultimate enforcement regime, including FinCEN’s discovery of those choosing not to comply.

National Defense Authorization Act for Fiscal Year 2021, tit. LXIV, §§ 6401–6403. ↑

For example, limited liability partnerships, limited liability limited partnerships, decentralized autonomous organizations (“DAOs”), and other entities created through filings with a secretary of state or tribal authority. ↑

31 C.F.R. § 1010.380(g) (“Reporting violations. It shall be unlawful for any person to willfully provide, or attempt to provide, false or fraudulent beneficial ownership information, including a false or fraudulent identifying photograph or document, to FinCEN in accordance with this section.” (emphasis added)). ↑

Searches across case law databases for litigation containing the phrase Corporate Transparency Act resulted in only one case found: Trump v. Deutsche Bank AG, 943 F.3d 627, n.55 (2019). ↑

H.R. 3746, 118th Cong. (2023) became Pub. L. No. 118-5 (2023). ↑

Nat’l Small Bus. United v. Yellen, No. 5:22-cv-01448-LCB (N.D. Ala. 2022). ↑

It bears noting that the person responsible for a reporting company’s CTA filing, in some instances, may not be a “beneficial owner” of the business entity, or only one of several “beneficial owners,” and will likely make the filing (even over potential objections) to avoid personal culpability. The willingness of one person to violate the law, problematic on its face, also implicates the rights and risk profile of other persons associated with the reporting company. The other implicated individuals in the business organization may not share this risk tolerance. ↑

Note that section 251 of the debt ceiling bill, Pub. L. No. 118-5 (2023), rescinded $1,389,525,000 of IRS earmarked funding. ↑

At this point, almost every business operates some of its information technology (“IT”) assets in the cloud. Cloud‑based IT resources may be infrastructure (supplementing or replacing on‑site data centers and communications systems), platforms, or applications. Also, essential, enterprise‑level applications are now commonly licensed as subscription services maintained by third parties. Many of these third-party services also operate on IT infrastructure sourced from a cloud provider.

Moves to the cloud are multifaceted and multidisciplinary. Lawyers have an important role advising their clients about the legal rights and obligations in the tangle of licensing arrangements inherent in cloud computing. Determining the sources of those rights and obligations can, itself, be a challenge.

This project focuses on the essential steps for determining the legal rights and obligations attendant to operating in the cloud and provides practical tools to assist business lawyers. The project’s contributors are members of the Business Law Section’s Cyberspace Law Committee.

A glossary rounds out the initial work product. The glossary is intended to be an open and continuing work in progress. We welcome reader contributions.

The toolkit will also include a resource focusing on the substance of cloud licensing. The forthcoming tool describes contract terms typical for software and cloud services, highlighting, in particular, subject matter that might be prioritized for attention when opportunities for negotiation are limited.

The Lawyer’s Role: More Counselor than Drafter

A lawyer representing the purchaser/licensee in a cloud transaction will almost always be reviewing vendor contracts, not drafting or modifying purchaser/licensee forms. Opportunities for negotiation are limited by bargaining power, the cadence of business operations and IT development, and the volume of material and services that may be necessary or useful to complete the client’s IT effort. In this circumstance, lawyers add value by issue-spotting and helping the business team assess and contextualize risk reflected in the vendor’s legal terms and service descriptions.

Coordination of Relevant Stakeholders

Lawyers are also often well positioned to identify the right decision makers—or at least the appropriate subject matter domains—and facilitate work across stakeholder groups to understand and manage rights and obligations buried in the fine print of cloud contracts.[1] Establishing and managing online environments and services involve information security (a discipline not entirely the focus of IT architects, engineers, and developers), budget and finance, procurement, compliance and risk, and data management and privacy—each doing its part to support a business team’s advancement of the client organization’s objectives.

The dynamic of coordinating stakeholder input is not new, of course. But lawyers should understand whether processes and controls that the client has in place to bring relevant stakeholders together will operate effectively when technology and services are procured through cloud service providers. Cloud marketplaces make shopping easier and more accessible to more people in an organization. Enabling more people to source material in an online store speeds access to technology components and solutions. Absent proper controls, however, solutions delivered on time with the right functionality may come without adequate attention to budget, security, and other risk considerations.

The following is a rudimentary example: Assume a developer is deploying a new application in an existing cloud environment. The developer enables logging functionality consistent with the organization’s security and operations policies for logging. The logging function can be enabled for no charge, but storage fees will accrue for keeping the log files. The project budget, focused on development and deployment, includes the initial application cost and subscription fees for a term. The budget does not anticipate the incremental cost of storage as log files are retained. What does the organization do when the storage fees begin to accumulate? Turn off logging? (Not likely.) Revise its budget for the ongoing cost?

How could the lawyer have helped the client organization in this illustration? First, the lawyer would have sought out and read the applicable contract. In doing so, the lawyer would probably have found references in the documentation saying that storage is separate. Or, more generally, the lawyer could have reminded the technology team to include colleagues whose role in the design and procurement process is to calculate the cost of ongoing operations and maintenance consistent with security policies and business requirements.

A lawyer engaged early in a project or business process development can work with the organization’s IT department to build review of product documentation into the design process. With proper guidance, a nonlawyer on the project team could be tasked to review documentation for key details—technical, operational, budget, legal red flags—and facilitate communication among relevant stakeholders.

Not a full-time technology lawyer? Business and commercial lawyers with the occasional technology matter in their portfolio add value when they spot issues and raise questions for the technology and business teams to consider. “What’s going on here?” can be a useful flag and does not require the lawyer to be a technology expert. Business lawyers understand that terms drafted by the other side have a thumb on the scale favoring the drafter. (And technology licenses sometimes read like the drafter put an elephant on the scale in the drafter’s favor.) Even when there is no practical likelihood that the organization will be able to negotiate more favorable terms, “What’s going on here?” gives the organization a prompt to consider potential risks, strategies to mitigate risk, and the feasibility of taking a different approach to avoid the risk.

Contracting through a Marketplace Feature

Incorporating cloud-based procurement into an organization’s operations requires a basic understanding of how software, services, and content may be procured from cloud service providers through their “marketplace” features. Organizations need to understand each marketplace through which they source products, material, and services and take appropriate steps to bring marketplace transactions into controls for procurement, contracting, security, and other risk management. Cloud providers have developed account management tools and access controls. It is up to client organizations to take appropriate steps to configure those tools, actively monitor customer portals and notices (and respond as appropriate), and keep account structures and access controls current.

The legal terms for cloud marketplaces and the products, material, and services offered in them are long, winding, and overlapping. They are also subject to provider-instituted changes that can affect ongoing services. Navigating cloud services and the marketplace tries the patience of the most diligent and patient lawyer. Lawyers should anticipate spending some time learning to navigate the legal terms of their clients’ cloud providers. The toolkit includes one paper illustrating contract navigation for the cloud marketplace of one significant service provider.

Lawyers should also keep in mind that cloud marketplaces are not the only channel to acquire software, services, or content for cloud-based systems. Cloud-based information technology may be procured under enterprise agreements with infrastructure or platform providers. Organizations may also engage third parties to manage their information technology. Those managed service providers may build out systems, including applications and storage, in cloud environments or using cloud-based platforms. Many enterprise-wide applications are now provided as a service, for example, office applications like Microsoft 365® and relationship management systems like Salesforce. Organizations may also bring their own software and content to a cloud environment. Managing proprietary and personal information has to be a consideration in reviewing the legal terms for any cloud-based arrangement.

A comprehensive review of procuring software, services, and content for cloud-based systems is beyond the current scope of this project. To start, we aim to contribute some basics that generalist business lawyers will find useful.

The Toolkit: A Dynamic Project

We expect each of the initial tools to evolve over time with feedback from readers and future collaborators. We also recognize opportunities to expand the toolkit with pieces highlighting sector‑specific issues, for example, education, health care, financial services, and service features (such as artificial intelligence components). We welcome volunteers and contributors to the project.

To offer feedback or contact the Toolkit Project coordinators, please email the project’s virtual mailbox at [email protected].

This project does not purport to be a comprehensive study of cloud computing for lawyers. For additional background about cloud computing, refer to these other ABA publications: Cloud 3.0: Drafting and Negotiating Cloud Computing Agreements (Lisa R. Lifshitz & John A. Rothchild eds., 2019); and H. Ward Classen, The Practical Guide to Software Licensing and Cloud Computing (7th ed. 2020). ↑

Pro bono work is about more than giving back to the community or meeting a lawyer’s professional obligation to do so. For law firms, it can also make good business sense, prompting a positive domino effect for themselves, the clients they serve, and minority- and women-owned business enterprises (M/WBEs) striving for success in their communities.

Indeed, legal services are a major expense for many small businesses, including M/WBEs. Further, legal services for small businesses can span areas ranging from corporate, employment, and real estate to intellectual property, data privacy and security, and other practice areas in which owners may not even be aware they need assistance. Considering both this reality and the American Bar Association’s Model Rule 6.1 noting that “every lawyer has a professional responsibility to provide legal services to those unable to pay,” it is incumbent on law firms to assist small businesses—particularly those owned by women and minorities, who continue to face systemic challenges in securing loans and other funding and accessing critical services to launch and grow their operations. Equally important for law firms to understand is that providing pro bono services can be beneficial to their own operations, with the potential for pro bono M/WBE clients to become future billable clients. In providing pro bono corporate counseling to early-stage, scalable M/WBEs (for example, preparing for and helping them acquire seed and venture capital investments), law firms eliminate an economic barrier for such businesses. In the event these M/WBEs receive such capital financing, they would likely have the appropriate amount of funding to scale their businesses and possibly become future billable clients of the law firms that initially provided pro bono legal services to them.

Pro bono legal services for small businesses have been especially valuable in the wake of the COVID-19 pandemic, with countless startups and even established small businesses struggling to stay afloat. In 2020, our firm (Gibbons P.C.) was approached by a nonprofit, the Institute for Entrepreneurial Leadership (IFEL), to partner on one of its new initiatives, “Small Businesses Need Us” (SBNU), created to provide free legal counsel and other business services to M/WBEs impacted by the pandemic. Gibbons attorneys have since donated hundreds of hours to SBNU to clients ranging from a STEM enrichment program for students, to an event management company, to a life and business empowerment coach.

Our partnership with IFEL has been so successful that IFEL has since become a billable client of the firm. The organization devotes much of its effort to connecting small businesses with investors and other financing channels—an essential endeavor, given the World Economic Forum report that, in 2021, “Black woman start-up founders received just 0.34% percent of the total venture capital spent in the U.S.”[1] IFEL is in the process of purchasing a for-profit group of diverse women angel investors, with Gibbons as its legal counsel.

One of IFEL’s business cohorts is OneKIN, a fintech company that builds software solutions to help small businesses compete in the digital landscape. Gibbons has assisted OneKIN for the past two years through IFEL’s SBNU program. Our pro bono work for OneKIN involved restructuring its ownership and cleaning up its capitalization table, as well as negotiating the buyout of certain founders. Since we began our engagement with OneKIN, the company has been accepted into MasterCard’s Start Path Program, designed to accelerate companies and set them up for future Mastercard acquisition. Gibbons continues to provide pro bono legal services to OneKIN by (i) reviewing/drafting a MasterCard accelerator agreement; (ii) drafting an Intellectual Property Assignment Agreement between founders of the company; and (iii) reviewing a Statement of Work and Master Services Agreement for product sales overseas. OneKIN now has plans to expand its business with the launch of an AI-powered livestream shopping app and has positioned itself to become a billable client of the firm.

During the COVID pandemic, Gibbons also partnered with the African American Chamber of Commerce of New Jersey (AACCNJ) and its M/WBE members. With many small businesses, M/WBEs in particular, finding it difficult to secure Paycheck Protection Program (PPP) loans during the initial phase of the pandemic, Gibbons connected the AACCNJ with one of our longtime clients—New Jersey Community Capital, a large, regional, community development financial institution—in order for the two organizations to partner for a joint venture called the Equitable Small Business Initiative (ESBI). ESBI is well-supported by large financial institutions, enabling it to facilitate access to critical capital by New Jersey’s Black business enterprises and provide them with hands-on, customized support and pandemic relief loans. After Gibbons structured this joint venture, the AACCNJ not only became a billable client of the firm, but also asked the firm to partner on the AACCNJ Pro Bono Alliance, a joint initiative whereby Gibbons supports AACCNJ member companies, on a pro bono basis, in launching, sustaining, or advancing their businesses.

While certain types of pro bono matters have the potential to become billable matters for law firms, pro bono work can also attract other clients or individuals who look for firms with a demonstrated commitment to pro bono representation. Pro bono work can generate cost savings as well, through its inherent offering of critical training and professional development to attorneys, particularly associates. Attorneys who provide pro bono services gain a valuable, firsthand view of the tangible ways their knowledge and experience are assisting small businesses, which leads to better client service overall. Gibbons regularly holds pro bono clinics for its attorneys, with incentives for reaching a certain numbers of hours per year.

Here at Gibbons, our philosophy is “doing good while doing well.” Without a doubt, establishing and building pro bono relationships has been both rewarding and profitable. Pro bono work should be an economic incentive for all law firms, one that can lead to a win for all parties involved.

With SPAC IPOs virtually gone but SPAC mergers (aka de-SPACs) continuing at a steady pace since the beginning of the year, the questions around getting a deal done boil down to the following:

How and where can companies get financing now that the PIPE (private investment in public equity) market has dried up?

How long will it really take to get the deal closed, now that target companies are not easy to come by and every deal seems to need an extension?

How can the current litigation and regulatory risks be avoided, or at least minimized?

In this article, we’ll focus on the third question, examining how the litigation and regulatory risk for SPACs has shifted since our 2022 year-end report.

SPAC Litigation by the Numbers

Through June 15, 2023, five SPAC-related securities class actions (SCAs) have been filed so far this year. That is not a high number. With 33 total SCAs filed in 2021 and 24 in 2022, we are at a slower pace for securities class actions this year than in the previous two years.

Filed SPAC/de-SPAC Securities Class Actions.

Examining the data between January 1, 2021, and June 15, 2023, it takes, on average, 12.82 months after the merger (aka de-SPAC) for an SCA to be filed. Except for a handful of cases, most lawsuits are filed after the de-SPAC has been completed. Considering that there were 199 de-SPACs in 2021, 102 in 2022, and 35 as of June 15, 2023, the downward progression of the number of SCAs this year tied to the downward progression of de-SPACs is not surprising. But that downward progression is somewhat deceptive.

Number of Suits vs. Number of Closed de-SPACs.

Direct Cases Picking Up Steam in Delaware

What the SCA data does not show is the growing number of direct-action breach of fiduciary duty suits being brought in Delaware. These suits are a progeny of the MultiPlan case in which the Delaware Chancery Court denied the defendants’ motion to dismiss. The parties subsequently settled for $33.75 million in November 2022, and no one in the SPAC world was surprised to see plaintiffs in other cases, including at least three so far in 2023, take a similar route.

Direct cases like MultiPlan and a few news-making examples below are easier to bring because, unlike derivative cases, they do not need to go through an extra step of satisfying demand futility requirements. It is no wonder then that, spurred by several denials of the defendants’ motions to dismiss and an easier procedural hurdle, plaintiffs’ attorneys are trading their SCA strategies for direct fiduciary suits against Delaware SPACs.

Examples of Direct Breach of Fiduciary Duty Suits

Lawsuit

Suit Filed

Outcome

Amount of Settlement

MultiPlan

January 24, 2021

Defendants’ Motion to Dismiss Denied – January 3, 2022

$33.75 Million

GigAcquisitions3

January 4, 2021

Defendants’ Motion to Dismiss Denied – January 4, 2023

Unknown

GigAcquisitions2

September 23, 2021

Defendants’ Motion to Dismiss Denied – March 1, 2023

Unknown

Trident Acquisitions Corp/Lottery.com

April 3, 2023

TBD

Unknown

Lordstown Motors

December 13, 2021

Defendants’ Motion to Dismiss Withdrawn

Unknown

Source: Woodruff Sawyer

From the perspective of directors and officers (D&O) insurance coverage, claims from direct suits, while typically indemnifiable, are not covered by “Side A only” D&O coverage. Many SPAC D&O insurance programs are structured as traditional “ABC” programs that would offer coverage for claims coming out of a direct suit. However, some SPAC teams, as a cost-saving alternative at the peak of the SPAC craze in 2021, when D&O insurance prices were astronomical, chose to structure their programs as Side A only. To the extent that a SPAC purchased a Side A–only policy and the lawsuit is determined, like in MultiPlan, to be a direct one, there may be no D&O insurance response for a settlement (outside of a corporate bankruptcy).

Whose Money Is It Anyway?

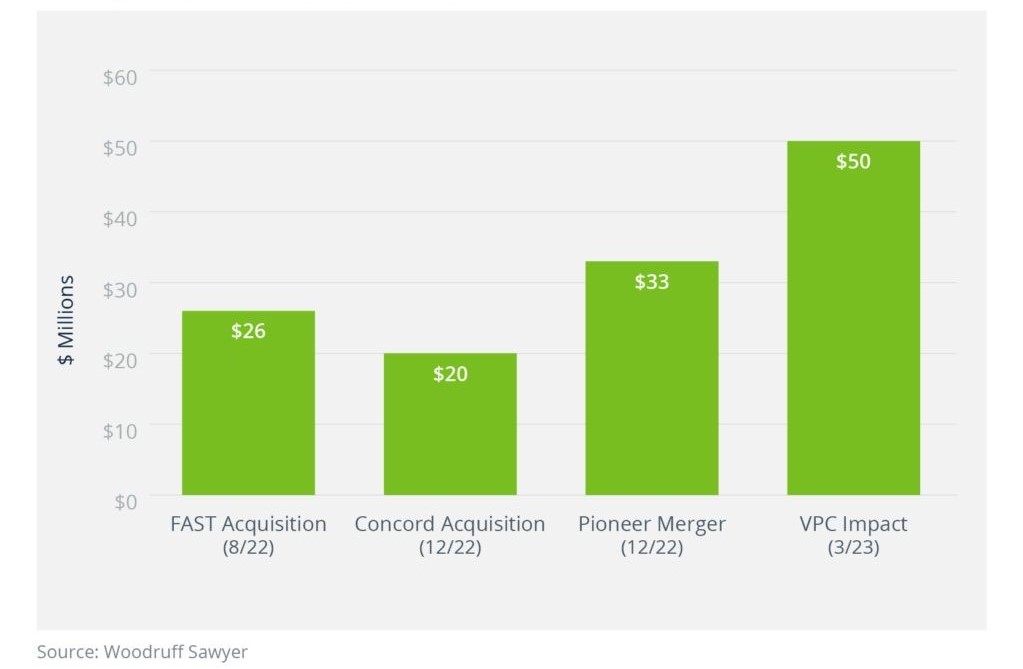

Another interesting trend continuing this year is the series of termination fee cases. In the first of these, the FAST Acquisition Corp. lawsuit from August 2022, the plaintiff investors objected to the SPAC team keeping the entire termination fee it had negotiated without sharing it with its investors. Other similar suits, with a few examples noted below, followed shortly after.

Examples of Termination Fee Suits.

The interesting element of these suits is that they would likely not have been filed had the SPAC team been able to complete a subsequent acquisition. But because the SPAC team failed to do so and had liquidated instead, the plaintiff investors naturally were not pleased to have been left out of the so-called termination spoils.

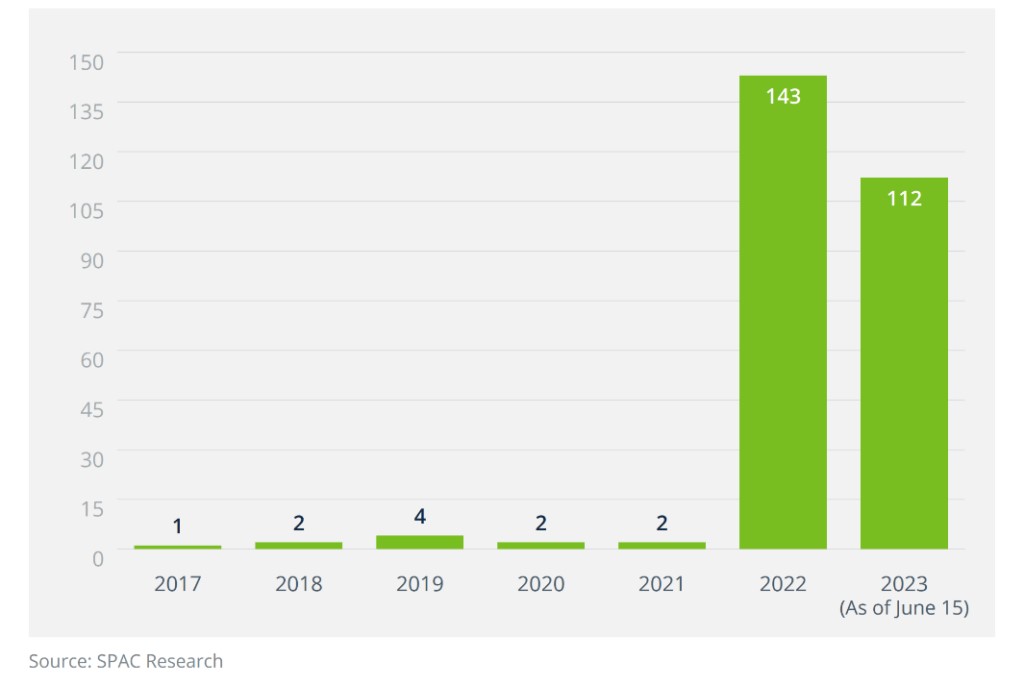

Considering the recent spike in liquidations as presented in the graph below, it is likely we will see more of these termination fee cases as more SPACs continue to liquidate—that is, unless the SPAC teams take note of this development and start approaching the apportionment of the termination fee differently.

SPAC Liquidations.

SPAC Wins

Not all SPAC-related cases came out on the side of the plaintiffs. There are several notable and interesting SPAC “wins”—decisions that went in the defendant’s favor. A few examples are:

Diamond Eagle Acquisition Corp/DraftKings: In January 2023, the United States District Court for the Southern District of New York (SDNY) granted the defendants’ motion to dismiss this SCA. The court held that the plaintiffs’ suit relied entirely on a short seller report with unknown sources, the claims in which were not adequately supported by independent research. As a result, plaintiffs failed to sufficiently allege that (1) any violations or material misstatements were made by the defendants and (2) any defendant acted with scienter as required under the law.

As a side note, about 35% of all SPAC-related securities lawsuits involve allegations from a previously published short-seller report.

Churchill Capital Acquisition Corporation IV/Lucid Motors: In January 2023, the Northern District of California granted the dismissal of the SCA on the grounds that the plaintiffs failed to plead materiality because they had no reason to know in early 2021 that the SPAC would merge with Lucid, as the parties were not engaged in merger discussions.

CarLotz: In March 2023, the SDNY dismissed the SCA assertion against CarLotz and certain directors and officers for plaintiffs’ lack of standing related to allegations of pre-merger statements. The court held that the investor plaintiffs failed to allege that they purchased shares traceable to the registration for the merger transaction.

Settlements

Let’s turn from lawsuits to settlements. There have been very few publicly disclosed settlements, so it is difficult to draw conclusions about trends. The ones that made the news are listed in the graph below.

Of particular interest are the amounts of some of those settlements that were covered by D&O insurance policies. Insurance coverage information is rarely publicly available, so it is possible, and even likely, that other settlements noted in the chart were also at least partially backed by D&O insurance payouts.

Litigation Settlements.

It’s worth remembering that outside of the actual settlement amounts, the defendants also had to pay substantial attorney fees. When deciding on the limit of a D&O policy, it’s worth factoring in the potential costs of the attorney fees, which will be due whether the lawsuit ends up being frivolous or ultimately gets dismissed.

Regulatory Enforcement Actions

Regulatory enforcement actions and investigations are, of course, the other piece of the risk puzzle. With the Securities and Exchange Commission (SEC) taking an openly hostile stance towards SPACs, many of us expected to see a barrage of SPAC-related investigations and enforcement actions. That expectation continues to be unrealized. While rumors are that the SEC is quite busy launching SPAC-related investigations, only several have been publicly reported, and we have seen only a handful of enforcements. Here are some examples that made the headlines:

Regulatory Enforcement Settlements and Fines.

Some additional details on the settlements and fines listed above are as follows:

Gordon: Administrative charges settled against CEO in January 2019 for $100,000. The SEC charged Benjamin Gordon, the former CEO of Cambridge Capital Acquisition Corporation, a SPAC, with failing to conduct appropriate due diligence to ensure that the SPAC’s shareholders voting on the merger were provided with accurate information concerning the target’s business prospects.

Momentus:Settlement total of $8.04 million in July 2021. The SEC alleged that Momentus and the founder misled Stable Road, the SPAC with which it planned to merge, about its technology and national security issues and that Stable Road had failed to perform its due diligence to identify those issues.

Nikola:Settlement total of $125 million in December 2021. The enforcement was preceded by a short seller report and an SCA and centered around misleading statements about Nikola’s products, technical advancements, and commercial prospects.

Perceptive Advisors:Settlement of $1.5 million in September 2022. This case was the SEC’s first enforcement action against an investment adviser. The SEC charged the adviser with violating the Investment Advisers Act in connection with its involvement with SPACs.

Morgenthau: Forfeiture of $5.1 million, restitution of $5.1 million, and 36 months in prison for the SPAC’s former CFO in April 2023. In January 2023, the SEC brought fraud charges against Cooper J. Morgenthau, the former CFO of African Gold Acquisition Corp., a SPAC. The charges revolved around Morgenthau orchestrating a scheme in which he stole more than $5 million from the company and from investors in two other SPACs that he incorporated.

Corvex:Settlement of $1 million in April 2023. The SEC charged investment adviser Corvex Management LP with failing to disclose conflicts of interest regarding its personnel’s ownership of sponsors of several SPACs into which Corvex advised its clients to invest. Corvex also agreed to a cease-and-desist order and a censure.

Update on the D&O Insurance Market and Rates

Market Conditions

The above data and trends have real implications on the risk and risk mitigation decisions that SPAC sponsors, their target companies, investors, and deal teams make. Higher risk of litigation or enforcement, for example, yields lower availability of D&O insurance coverage and higher premiums. Overall insurance market trends also dictate the kind of coverage and costs a team should expect.

As we noted at the end of 2022, the impossibly hard SPAC D&O market started to turn. In just a few months since the beginning of the year, we witnessed one of the fastest adjustments in the wider public company D&O market ever recorded.

Many new insurers have joined the ranks and now, with an oversupply of insurance capacity and very few IPOs, insurers are competing for public D&O new and renewal business, driving rates and retentions down for almost all companies. Mature public companies are experiencing significant rate relief, and newly public companies are seeing significant rate decreases due to higher starting premiums.

What This Market Means for SPAC D&O Insurance Rates

The pressure on carriers in the overall public D&O insurance market is good news for SPACs. We are seeing more carriers interested or willing to take a second look at SPAC tails, extensions, and new go-forward programs. Competition is driving premiums down. Self-insured retention benchmarks are also dropping. More carriers are willing to be flexible on the structuring of the coverage.

However, the likelihood of a SPAC-related company getting sued continues to be higher than that of a traditional IPO or a mature public company. Carriers are continuing to keep a very close eye on each new court decision and enforcement action. For example, a recent decision from Delaware led to many carriers being unwilling to renegotiate tail pricing on the SPAC IPO policy or imposing coverage exclusions. Many are still wary of granting long extensions or reducing premium pricing on those extensions.

Our Predictions

As we predicted at the end of 2022, SPACs have enjoyed a period of reasonable D&O insurance pricing so far in 2023, and that will likely continue into 2024. However, SPAC teams and their target companies will need to make some program restructuring decisions (with the help of their insurance brokers) to adjust for the new trends in the direct fiduciary duty cases and other court decisions as they affect D&O carriers’ obligations.

An earlier version of this article appeared in the Woodruff Sawyer SPAC Notebook.

In June 2022, the Canadian Parliament enacted amendments to the Competition Act (the Act) intended to prohibit agreements between unaffiliated employers to fix wages or terms or conditions of employment (Wage-Fixing Agreements) or not to solicit or hire each other’s employees (No-Poaching Agreements).

The amendments come into force on June 23, 2023, as subsection 45(1.1) of the criminal conspiracy provision in section 45 of the Act.

Once this occurs, any new Wage-Fixing Agreements or No-Poaching Agreements will be per se unlawful and expose the parties to those agreements to significant criminal penalties (i.e., prison sentences of up to fourteen years and/or fines with no statutory limit), as well as to potential civil liability, including by way of class actions for damages.

On January 18, 2023, the Canadian Competition Bureau (the Bureau), the law enforcement agency that administers and enforces the Act, released draft guidelines for public consultation describing its intended approach to enforcing the new criminal prohibitions (the Draft Guidelines).

On May 30, 2023, the Bureau published its final wage-fixing and no-poaching enforcement guidelines (the Final Guidelines). As detailed below, while the Final Guidelines are hardly a model of transparency or clarity, they provide the business community with some comfort with respect to the scope and application of the new prohibitions.

Final Enforcement Guidelines

The key takeaways for business lawyers and their clients from the Final Guidelines are these:

“Wage-Fixing” Is a Misnomer: The wage-fixing prohibition deals with more than just salaries and wages, also making it an offense for unaffiliated employers to enter into agreements to fix, maintain, decrease, or control “terms and conditions of employment.”

“One Way” No-Poaching Agreements Not Prohibited: The no-poaching prohibition applies only to agreements between unaffiliated employers that are reciprocal or mutual in nature.

Reasonable Clauses in Certain Categories of Business Agreements or Arrangements Should (Generally) Not Raise Concerns: The Final Guidelines confirm that the Bureau will “generally not” pursue a criminal investigation with respect to wage-fixing and no-poaching clauses that are ancillary to merger transactions, joint ventures, strategic alliances, franchise agreements, or staffing or IT service contracts, unless the wage-fixing or no-poaching clause in question is “clearly broader than necessary in terms of duration or affected employees, or where the business agreement or arrangement is a sham.” While the Final Guidelines offer some comfort, it is clear from certain statements in the Final Guidelines that the Bureau is prepared to second-guess the parties’ business judgement regarding the reasonable necessity of a given restraint and to take enforcement action to the extent that the Bureau concludes that an impugned restraint is “clearly” broader than reasonably necessary.

Ancillary Restraints Defence May be Available: Outside of the categories of business agreements and arrangements enumerated above, the so-called “ancillary restraints defence” will be available in any case where the parties to the impugned Wage-Fixing Agreement or No-Poaching Agreement (the Restraint) can show that:

the Restraint is ancillary to, or flows from, a broader or separate agreement that includes the same parties;

the Restraint is directly related to and reasonably necessary for achieving the objective of the broader or separate agreement referred to in (a) above; and

the broader or separate agreement referred to in (a) above, when considered without the Restraint, does not violate subsection 45(1.1).

New and Ongoing Agreements Captured: The new prohibitions will only apply to new agreements entered into on or after June 23, 2023, except where the parties to agreements entered into before that date engage in conduct that reaffirms or implements those older agreements. Usefully, the Final Guidelines clarify that “at least two parties must reaffirm or implement the restraint for the Bureau to establish the […] consensus or ‘meeting of the minds’” required to ground liability.

Accordingly, existing agreements need not be formally terminated in order to avoid criminal liability under the Act, but employers should be careful to avoid any conduct that could be seen as reaffirming or giving effect to agreements that precede June 23, 2023. The Final Guidelines also suggest that “employers may wish to update pre-existing company records and agreements, as they arise in the ordinary course, to ensure they accurately reflect its policies and intentions, and avoid unnecessary confusion.”

Employers should also be mindful that they can be found liable even if their “agreement” was informal, verbal only, or entirely unspoken (e.g., a “wink” or a “nod”). Moreover, the existence of an “agreement” can be established based on circumstantial evidence, with or without direct evidence of communication between or among the alleged parties to it.

We recommend that clients review all existing agreements with wage-fixing and no-poaching provisions with counsel in order to ensure that existing practices comply with the new prohibitions.

Employers Need Not Be Competitors: The new prohibitions apply to Wage-Fixing Agreements and No-Poaching Agreements between unaffiliated employers but do not apply to such agreements between affiliated employers.[1] By way of example, the Bureau states that agreements between two or more corporate entities that are controlled by the same parent company do not violate the new prohibitions.

The new prohibitions apply regardless of whether unaffiliated employers are competitors in the supply of a product (although the Bureau notes that it will prioritize its enforcement on Wage-Fixing Agreements and No-Poaching Agreements between employers that would otherwise compete in the purchase of labor).

“Employer” Broadly Defined: The definition of “employer” is broad and includes directors and officers, as well as agents or employees, such as human resources professionals. As a result, corporations may be vulnerable to liability if an offending agreement is entered into between an officer of one corporation and a director of the other, for example.

“Employee” Relationship to Be Evaluated on Case-by-Case Basis: Whether an individual is characterized as an “employee” for the purposes of the new prohibitions will be evaluated on a case-by-case basis and will depend on the laws and circumstances under which the relationship with that “employee” or “independent contractor” was entered into. Accordingly, the common law tests on whether a person is properly characterized as an employee or independent contractor may be relevant in considering whether the new prohibitions apply. The Final Guidelines include a reminder to employers that “depending on applicable legislation, their relationship with independent contractors could evolve over time. For example, if an employer treats an independent contractor as an employee, the business contract between them could transform into an employment relationship.”

Conscious Parallelism Not Prohibited: “Conscious parallelism” on its own will not be a violation of subsection 45(1.1). According to the Bureau, “conscious parallelism” occurs “when a business acts independently with awareness of the likely response of its competitors or in response to the conduct of its competitors.” However, the Bureau also cautions that parallel conduct coupled with facilitating practices (for example, sharing commercially sensitive employment information, such as employment terms) may be sufficient to prove that an illegal agreement was concluded.

Implications of the New No-Poaching and Wage-Fixing Prohibitions for Business Lawyers and Their Clients

1) No-Poaching Agreements

In section 2.2 of the Final Guidelines, the Bureau confirms that the no-poaching prohibition is limited to instances where unaffiliated employers agree not to poach “each other’s” employees. Therefore, as noted above, agreements must be reciprocal or mutual in nature in order to violate the no-poaching prohibition. “One-sided” or “one-way” agreements, where only one party agrees not to poach another’s employees, will not be an offense.

Importantly, this means that customary one-sided no-poaching/non-solicitation clauses in confidentiality and non-disclosure agreements commonly used in the diligence phase of merger transactions, joint ventures, and strategic alliances will not be subject to enforcement action by the Bureau. It bears noting, however, that the Bureau’s interpretation of the Act is not binding on the courts, and private plaintiffs (including class action plaintiffs’ lawyers) may still seek to bring damages claims with respect to one-way agreements. In this regard, the Final Guidelines note that “[t]he courts are responsible for the final interpretation of the law.”

Further, the Bureau cautions that “separate agreements between two or more employers that result in reciprocating promises not to poach each other’s employees” may trigger liability.

2) Wage-Fixing Agreements

The new prohibitions also criminalize so-called “wage-fixing.” As noted above, the prohibition makes it an offense for unaffiliated employers to enter into agreements to fix, maintain, decrease, or control not only wages and salaries but also “terms and conditions of employment.”

In its Draft Guidelines, the Bureau specified that “‘terms and conditions’ include the responsibilities, benefits and policies associated with a job. This may include job descriptions, allowances such as per diem and mileage reimbursements, non-monetary compensation, working hours, location and non-compete clauses, or other directives that may restrict an individual’s job opportunities” but then unhelpfully undercut this guidance by adding that “[t]he Bureau’s enforcement generally is limited to those ‘terms and conditions’ that could affect a person’s decision to enter into or remain in an employment contract” (emphasis added). Despite extensive criticism of the overbreadth and unhelpfulness of this guidance, no clarification was provided in the Final Guidelines.

Wages, salaries, and other terms and conditions of employment should therefore be treated as competitively sensitive information (CSI) in M&A diligence processes and in developing and implementing appropriate safeguards against the disclosure of CSI in the context of joint ventures, strategic alliances, and other commercial collaborations. Guidance should be sought in advance of providing due diligence information in order to ensure that CSI is not disclosed and that only “clean teams” gain access to CSI.

In the preface to the Final Guidelines, the Bureau states that it “may revisit these Guidelines in the future in light of experience, changing circumstances and legal developments.” As time passes and experience with the new prohibitions grows, one may hope that the Bureau will indeed revisit its enforcement approach vis-à-vis merger transactions, joint ventures, strategic alliances, franchise agreements, and staffing and IT service contracts and, consistent with the economic and procompetitive benefits generated by such business agreements and arrangements, will limit the application of the no-poaching and wage-fixing prohibitions exclusively to circumstances where the broader (or separate) agreement between the parties is a sham.

Under subsection 2(2) of the Act, affiliation is defined with reference to control. When two employers are controlled by the same parent company or individual, they are said to be affiliated. ↑

Diversity, equity, and inclusion (DE&I) is ever evolving, and the right answer on many DE&I issues is not always immediately evident. People have questions that they may or may not be afraid to ask. “Dear Alex,” a new column created by the ABA Business Law Section’s Diversity, Equity, and Inclusion Committee, is the reader’s chance to ask all about DE&I anonymously. Think of it like the old “Dear Abby” columns, but for DE&I. In each column, the Dear Alex team will answer a question related to DE&I. These questions can be interpersonal, like how to respectfully address a colleague who is transitioning from one gender to another, or even professional, like how to convince senior partners at your firm that investing in DE&I can be a competitive advantage. If you’ve ever had a DE&I question that you have been afraid or otherwise unable to ask, now is your chance to ask “Alex.” Questions can be submitted at the form linked here.

***

Dear Alex,

Another associate at my firm told me that he’s transitioning. He’s the first trans person I’ve met, and I do not want to accidentally offend him. How do I approach this?

Sincerely,

Cis and Confused

Dear Cis and Confused,

Your coworker confiding in you is indicative of the trust between you two.