A significant question pending under the recently effective Corporate Transparency Act (“CTA”) is whether a limited liability partnership (“LLP”) is a “reporting company” as defined in the CTA and the related “Reporting Regulations.” Classification as a reporting company has the effect of ab initio subjecting the firm to the beneficial ownership information reporting obligations of the CTA and the Reporting Regulations absent, on a firm-by-firm basis, an exemption from those burdens.

As detailed below, in considering the definition of a CTA reporting company with the law addressing how an LLP comes into being, it is clear that an LLP is not a reporting company.

This article begins with a review of the genesis of the LLP from the midst of the savings and loan crisis of the late 1980s and the subsequent progression of the form from bespoke supplements to state adoptions of the Uniform Partnership Act (1914) and the Uniform Partnership Act (1994), and then to the detailed provisions for LLPs set forth in the Revised Uniform Partnership Act (1997). We then turn to the CTA and the Reporting Regulations to review their respective definitions of what is a reporting company, including informal guidance from the Financial Crimes Enforcement Network (“FinCEN”) office of the Department of the Treasury as to the application of the regulatory definition. Turning then to the crux, we review why the LLP does not fall within the scope of either definition of what is a reporting company.

The Rise of the LLP

The venerable general partnership has existed for millennia;[1] aside from the sole proprietorship, likely it is the oldest organizational form. In the U.S. the common law of partnerships was reduced to statutory form in the Uniform Partnership Act (1914) (“UPA”), shortly thereafter supplemented with the Uniform Limited Partnership Act (1916), the latter providing rules applicable to those partners categorized as “limited partners.” The Uniform Partnership Act (1914) was superseded by the (Revised) Uniform Partnership Act (1994), but Texas’s adoption of the nation’s first LLP provisions in 1992 (which accompanied its initial adoption of an LLC statute) caused the Uniform Law Commissioners to revise the statute again to include LLP provisions as the Revised Uniform Partnership Act (1997) (“RUPA”). This statute has since been renamed the Uniform Partnership Act (1997) (last amended 2013) and Uniform Partnership Act (2024). While all states save Louisiana had adopted the 1914 Act, not all have to date adopted a permutation of the 1997 Act. But by the end of the twentieth century,[2] all states had engrafted LLP provisions onto whatever general partnership statute the state had.

The most commonly understood characteristic of the general partnership is the rule that each partner is vicariously personally liable for partnership obligations; in popular parlance, partners do not enjoy “limited liability” but rather bear personal exposure to the extent of their assets for the partnership’s debts and obligations.[3] While today some may look askance at this rule, because the absence of vicarious personal liability for organizational liabilities is the universal rule for other forms of organization, in fact it had important benefits. In a firm in which each owner is liable for the consequences of another’s negligence, there is incentive to oversee tasks and to require cooperative action. “Lone wolf” unilateral actions that could put the firm’s capital (including its reputational assets) and that of its partners’ at risk will not be tolerated, and there is an incentive to train employees and newer partners as a method of risk mitigation. “All for one and one for all” became a successful modus operandi. Well, it was until who the “all” was became unknown.[4] As professional firms grew to have offices distributed throughout the country with varying levels of sophistication and resultant different risk profiles, the “one” in “one for all” was reduced to this office, or my practice group, or even just me.

The fallout of the Savings and Loan Crisis of the 1980s and early 1990s demonstrated that exposing partners across the country and across practices to personal liability for claims often arising in a distant office[5] was no longer a viable structure.[6] Generically, the CPA in Lincoln, Nebraska, who performed scrupulous audit work for local farmers and farm equipment distributors found himself facing bankruptcy when his “partner” in Texas was found to have provided spotty if not actually fraudulent assurance services to a savings and loan. Public institutions including the courts asked, Where were the attorneys and accountants who (with 20/20 hindsight?) should have intervened to protect the public from the scourge of unprincipled lending? Accounting firms paid nine-figure fines[7] or were outright destroyed,[8] as were storied law firms.[9]

Okay, but if not general partnerships, then what? And here there arose the narrow gap between a rock and a hard place. On one side were the regulatory rules that limited professional firms to general partnerships (already rejected due to the personal liability rule) and in some instances professional service corporations (“PSCs”).[10] While the PSC option afforded limited liability, larger firms could not use the PSC form because of the functional size limitation imposed for S-corporation treatment.[11] Further, the conversion of an existing partnership into an entity taxed under either Subchapter C or Subchapter S resulted in phantom income because of the (for tax purposes) realization of accounts receivable.[12] Additional transactional costs would have been incurred in the real costs of drafting and negotiating a shareholder agreement, as well as the intangible costs of referring to copractitioners as “shareholders” and in some cases “directors” rather than the previously employed “partners.” What was needed was a partnership that satisfied the professional regulatory rules as to forms of practice and maintained the preferred tax classification while limiting or abolishing the venerable partnership rules as to partner liability. The LLP arose out of that tension.

The limited liability partnership (“LLP”), which in some states is labeled a “registered limited liability partnership,” is a construct in which a general partnership may via a state notice filing elect to be governed by a different rule as to the vicarious liability of the partners for the partnership’s debts and obligations.[13] In a classic general partnership, each partner is jointly and severally liable with the partnership and each other partner for the partnership’s debts and obligations.[14] The LLP is a general partnership that continued the partnership format in that it retained existing management structures and tax treatment as well as the perceived value of identifying the firm’s principals as “partners.” Crucially, because the LLP was a general partnership, it did not run afoul of then-existing rules limiting professional practices to the forms of a general partnership and in certain instances a PSC.

The importance of staying within the confines of a partnership is illustrated by the development of the laws of the Commonwealth of Kentucky governing the permitted forms of an accounting practice. Kentucky’s modern statute governing the accounting practice was adopted in 1946,[15] it providing in part for the structure of partnerships engaged in accounting.[16] Then in 1984 the defined term “firm” was added to that act, namely: “‘Firm’ means a sole proprietorship, partnership or professional service corporation or association engaged in the practice of public accountancy.”[17] The rule remained that an accounting practice could be conducted in the form of a sole proprietorship, a partnership, or a professional service corporation.[18] In 1990 additional detail was added to the rules governing the composition of partnerships and professional corporations through which accounting was practiced, but they, along with sole proprietorships, remained the only available forms.[19] Then, in 1994, coincident with the adoption of LLP amendments to Kentucky’s enactment of UPA,[20] the rules governing accountants were amended. But tellingly, while LLCs were encompassed in the permitted forms, no additional language was added to address LLPs.[21] That was not an omission but rather a recognition that no new authorization was necessary—accountants could practice as partnerships, and partnerships included the new option of electing into LLP status.[22]

What distinguished the LLP from the preexisting partnership model is that it jettisoned the no longer desired rule of joint and several vicarious liability among the partners. While there are a variety of distinctions under various state laws, if a partnership makes this notice filing and satisfies the name requirements, the partners qua partners are to one degree or another (the distinction is between so-called “partial” and “full” shield LLPs) not subject to joint and several liability for the partnership’s obligations, but rather enjoy limited liability akin to that enjoyed by shareholders in a corporation.[23] Some states require that the partnership periodically renew its LLP filing and that in the absence of that renewal it reverts to a traditional general partnership. Nearly all if not all states provide that the partnership that elects LLP status is the same entity that existed before that election was made.[24]

For purposes of this article, it is important to recognize that aside from the elimination of vicarious liability, LLPs are indistinguishable from other general partnerships in all respects: they are formed by association of two or more persons as co-owners of a business for a profit, and, most importantly in this context, they are formed by this association, not by the filing of a charter or certificate with the state. While the characteristic of vicarious liability of the partners may depend upon the filing of a registration, in the parlance of RUPA a “statement of qualification,” the absence of such a filing does not alter the fact that the partnership exists as a business organization under state law. Further, should the registration expire or be withdrawn, the partnership continues as that same partnership; there is no dissolution or other interruption of its ability to transact business as an ongoing organization.

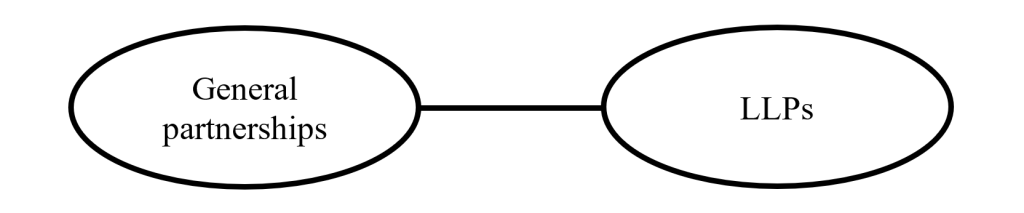

A last point on the substantive law of LLPs; the frame of reference of comparing “general partnerships” with “limited liability partnerships” is false as they are not two sets; essentially all limited liability partnerships are general partnerships.[25] The set is general partnerships, and it may be divided into the subsets of (i) general partnerships that have elected to be limited liability partnerships, and (ii) general partnerships that have not elected to be limited liability partnerships.[26] Graphically, it is not:

but rather:

General Partnerships | |

General partnerships that have not elected to be LLPs | General partnerships that have elected to be LLPs |

The CTA Reporting Company

The “gateway” to the CTA is status as a “reporting company”;[27] a reporting company is obligated to file beneficial ownership information reports (“BOIRs”) with FinCEN’s Beneficial Ownership Secure System (“BOSS”) database through its interface.[28] Conversely, an organization that is not a reporting company never enters into the range of responsibility to file BOIRs.

What is a reporting company is initially defined in the CTA, namely:

(11) Reporting Company.—The term “reporting company”—

(A) means a corporation, limited liability company, or other similar entity that is—

(i) created by the filing of a document with a secretary of state or a similar office under the law of a State or Indian Tribe[.][29]

From that source the Reporting Regulations (unfortunately) modified the definition, defining a “domestic reporting company” as:

- The term “domestic reporting company” means any entity that is:

- A corporation;

- A limited liability company; or

- Created by the filing of a document with a secretary of state or any similar office under the law of a State or Indian tribe.[30]

FinCEN/Treasury did itself no favors in modifying the definition of a reporting company in the course of drafting the Reporting Regulations, as it may be read as a reporting company is any of (i) all corporations, (ii) all limited liability companies, and (iii) any other “entity” that is “created” by a secretary of state filing.[31] FinCEN, in an FAQ, clarified that the interpretation of the Reporting Regulation’s definition of a reporting company is limited to those organizations created by a secretary of state filing and does not extend to every corporation or LLC.[32]

No state requires a secretary of state or similar filing in order for a general partnership to come into existence.[33] This rule is elemental in that partnership is a default category; when persons enter into a business relationship that satisfies the terms of what is a partnership, then a partnership comes into being,[34] unless they elect to structure their relationship in another way such as a corporation or LLC.[35] There being no secretary of state or similar filing in order to “create” a general partnership, it necessarily follows that a general partnership is not a CTA reporting company, a conclusion FinCEN/Treasury has recognized.[36]

Against this background is what is apparently only a single statement from FinCEN to the effect that an LLP is a reporting company.[37] On closer analysis that statement, to the extent it addresses LLPs, is incorrect.

LLPs Are Not Created by a Secretary of State Filing and Therefore Are Not “Reporting Companies”

No business organization is “created” by an election by a partnership to be an LLP. Rather, there was a partnership that was not an LLP, and then there is a partnership that is an LLP, and it may come to pass that there is a partnership that once was but is no longer an LLP; throughout all of those conditions there was a single partnership. That the partnership exists and then elects into LLP status is clear from the statutory language. The Revised Uniform Partnership Act (1997) provides: “[a] partnership may become a limited liability partnership pursuant to this section.”[38] The partnership exists by agreement of the partners,[39] and thereafter determines that it will be and makes the filing necessary to be an LLP. Since the partnership existed without the requirement of a state or other filing, and the already existing partnership files a document by which it elects in LLP status, it follows that a partnership is not “created” by the partnership’s filing of that election. This point was addressed in the Official Comments to RUPA § 201 in 1997 when it was observed:

Thus, just as there is no “new” partnership resulting from membership changes, the filing of a statement of qualification does not create a “new” partnership. The filing partnership continues to be the same partnership entity that existed before the filing. Similarly, the amendment or cancellation of a statement of qualification under Section 105(d) or the revocation of a statement of qualification under Section 1003(c) does not terminate the partnership and create a “new” partnership. See Section 1003(d). Accordingly, a partnership remains the same entity regardless of a filing, cancellation, or revocation of a statement of qualification.[40]

Numerous courts have applied these principles to determine that a partnership that has elected to be an LLP is the same partnership that preceded that election.[41]

This appreciation of the nature of the LLP is consistent with its roots. Recall that every organizational form is a construct, a combination of characteristics that satisfies a particular need, and as recounted above the “need” was for a structure that was and is a general partnership but with an altered rule of partner vicarious liability. If it was not a general partnership, the structure would have been outside the scope of permissible forms for the professional practices that needed (or at least wanted) the new rule.[42]

Long before the CTA and the question of its treatment of LLPs, the Permanent Editorial Board for the Uniform Commercial Code (the “PEB”) considered the question of whether the election by a partnership to become an LLP via the filing of a statement of qualification is the formation or organization of an entity, a question of importance in the context of the Uniform Commercial Code because it determines the controlling law.[43] Finding the election to be an LLP is not the organization of a new venture, the PEB wrote:

It follows that the statement of qualification filed with the State and by which a partnership becomes a limited liability partnership under the 1997 UPA is not a “public organic record” under the 2010 amendments to Article 9. The statement of qualification is not a record filed with the State to “form or organize” the partnership. It is the association of the partners that forms the partnership, not any record publicly filed with the State. Both conceptually and legally, a partnership is formed wholly apart from the filing of a statement of qualification with the State. Because a limited liability partnership is not formed or organized by the filing of a public organic record, it cannot be a “registered organization” under the 2010 amendments to Article 9.[44]

So the statutory language governing a partnership’s election of LLP status, the cases interpreting that language, the Official Comment to that provision of the Revised Uniform Partnership Act (1997), the comments of leading experts in the field, and the PEB considering the language have all agreed that an LLP is not a separate organization “created” by the election to be an LLP. Against that there is, well, really nothing except FinCEN’s unsupported assertion that LLPs are reporting companies.

It bears noting that the Department of the Treasury, in its own regulations, acknowledges that an LLP is just a type of partnership, stating: “A partnership form of registration is available for two or more individuals who are doing business as a partnership, including a limited liability partnership.”[45] At the same time other of its regulations, namely those under the customer due diligence requirements, provides that “legal entity customer” means: “a corporation, limited liability company, or other entity that is created by the filing of a public document with a Secretary of State or similar office, a general partnership, and any similar entity formed under the laws of a foreign jurisdiction that opens an account.”[46] If FinCEN is to be taken at its word, and LLPs are not general partnerships, them an LLP is not a “legal entity customer” for which a bank has customer due diligence obligations; conversely if an LLP is but a subset of general partnerships, they are included. Further, clearly FinCEN knows how to write a regulation (and how to influence the drafting of a statute such as the CTA) to include entities created by a secretary of state filing and general partnerships.

FinCEN has estimated that there may be more than 32 million firms existing on January 1, 2024, that will be classified as reporting companies required to file BOIRs into the BOSS database and interface.[47] All else being equal, those totals will not include any general partnerships that have elected to be limited liability partnerships. While some may view this treatment of LLPs as exposing a significant gap in the CTA’s coverage, that viewpoint does not alter the reach of the statutory language.

See, e.g., Robert Francis Harper, Assyrian and Babylonian Literature 263 (reciting the terms of a contract dated to 2000 BCE) (D. Appleton and Company 1901). ↑

It is somewhat disturbing to realize this was already a quarter of a century ago. ↑

See Unif. P’ship Act (1914) § 15; see also id. § 18. ↑

See also Susan Saab Fortney, Am I My Partner’s Keeper? Peer Review in Law Firms, 66 U. Colo. L. Rev. 329 (1995). ↑

See also Michael Orey, The Lessons of Kaye, Scholer: Am I My Partner’s Keeper?, Am. Law., May 1992, at 3, 81. ↑

See, e.g., Robert W. Hamilton, Registered Limited Liability Partnerships: Present at the Birth (Nearly), 66 U. Colo. L. Rev. 1065, 1069 (1995); Robert R. Keatinge et al., Limited Liability Partnerships: The Next Step in the Evolution of the Unincorporated Business Organization, 51 Bus. Law. 147 (1995). See also Joseph S. Naylor, Is the Limited Liability Partnership Now the Entity of Choice for Delaware Law Firms?, 24 Del. J. Corp. L. 145 (1999). ↑

See, e.g., Robert A. Rosenblatt, Auditor Pays $400 Million for Not Signaling S&L; Crisis, L.A. Times (Nov. 24, 1992) (discussing settlement paid by Ernst & Young). ↑

See, e.g., Nancy Rivera Brooks, Laventhol & Horwath to Seek Bankruptcy Shield, Dissolve Firm, L.A. Times (Nov. 21, 1990); see also Frederic M. Stiner, Jr., Bankruptcy of an Accounting Firm: Causes and Consequences of the Laventhol & Horwath Failure, 3 Econ. & Bus. J.: Inquiries & Persps. 1 (2010). ↑

See supra note 5, discussing $41 million fine paid by Kaye, Scholer, Fierman, Hays & Handler; Law Firm Reaches S&L Settlement, Chi. Trib. (Apr. 20, 1993) (discussing $51 million settlement paid by Jones Day); see also Susan Saab Fortney, OTS vs. the Bar: Must Attorneys Advise Directors that the Directors Owe a Duty to the Depository Fund?, 12 Ann. Rev. Banking L. 373, 375 nn.9–11 (1993); id. at 376–379; Harris Weinstein, Attorney Liability in the Savings and Loan Crisis, 1993 U. Ill. L. Rev. 53, 53 (reporting that some ninety civil cases had been brought in the preceding four years against “lawyers”); James S. Granelli, Two Firms Settle Lincoln S&L Cases, L.A. Times, Mar. 31, 1992, at A1. ↑

Recall that at this point in time LLCs had not yet exploded onto the scene, and even where available, professional regulation likely did not yet sanction the use of that form by professional firms. ↑

This statement presupposes that pass-through taxation is “necessary,” a statement more true at that time than it is today with significant narrowing of differentials between Subchapters C, K, and S, especially as to the availability of tax-favored retirement savings plans. From 1982 through 1997, the time period that includes the Savings and Loan Crisis, and the rise of the LLP, S-corporation status was limited to firms with thirty-five or fewer shareholders, greatly reducing the utility of S-corporation classified PSCs for the organization of professional firms. See Subchapter S Revision Act of 1982, Pub. L. 97–354, § 2, 96 Stat. 1669, 1669 (Oct. 19, 1982) (amending Code 1361(b)(1) to provide: “For purposes of the subchapter, the term ‘small business corporation’ means a domestic corporation which is not an ineligible corporation and which does not (A) have more than 35 shareholders . . . .”). The limit was not raised to seventy-five shareholders until 1997, and then it was raised to one hundred shareholders in 2005. See Small Business Job Protection Act of 1996, Pub. L. 104-188, § 1301, 110 Stat. 1755, 1777 (Aug. 20, 1996); American Jobs Creation Act of 2004, Pub. L. 108–357, § 232, 118 Stat. 1418, 1434 (Oct. 22, 2004). See also Richard D. Blau, Bruce N. Lemons & Thomas P. Rohman, S Corporations: Federal Taxation § 3:35 (July 2024 Update) (ebook). ↑

See 26 U.S.C. § 357(c)(1); see also Thomas Arden Roha, The Application of Section 357(c) of the Internal Revenue Code to a Section 351 Transfer of Accounts Receivable and Payable, 24 Cath. U.L. Rev. 243 (1975); Bruce G. Perrone, Incorporating a Cash Basis Business: The Problem of Section 357(c), 34 Wash. & Lee L. Rev. 329 (1977). ↑

In certain states including Colorado and Delaware a limited partnership may also make this filing, but for purposes of simplicity this discussion is in the context of a general partnership. Whether a limited partnership that elects LLP status, sometimes referred to as a limited liability limited partnership or “LLLP,” presents a different set of challenges in determining whether it is a CTA reporting company. ↑

See Unif. P’ship Act (1914) § 15; Rev. Unif. P’ship Act (1997) § 306(a); Colo. Rev. Stat. § 7-64-306(1) (“Except as otherwise provided in this section, all partners are liable jointly and severally for all partnership obligations unless otherwise agreed by the claimant or provided by law.”); Del. Code Ann. tit. 6, § 15-306(a); Ky. Rev. Stat. Ann. § 362.2-306(1). ↑

See 1946 Ky. Acts. ch. 210 (S.B. 164); see also id. at § 1 (“This Act may be cited as the ‘Public Accounting Act of 1946.’”). ↑

See id. § 5 (certified public accountants); id. § 7 (public accountants); see also id. § 8 (permits to practice public accounting to be issued to “individuals and partnerships”). ↑

See Ky. Rev. Stat. Ann. § 325.220(6) as created by 1984 Ky. Acts ch. 117 (H.B. 389). Presumably the “professional service [] association” reference is to partnership associations. ↑

See Ky. Rev. Stat. Ann. § 325.300 (repealed 1994). ↑

See Ky. Rev. Stat. Ann. § 325.300 as amended by 1990 Ky. Acts ch. 285, §1(6) (repealed 1994). ↑

See Ky. Rev. Stat. Ann. § 362.555. Kentucky would not adopt the Revised Uniform Partnership Act (1997) until 2006. ↑

See Ky. Rev. Stat. Ann. § 325.220(6) as amended by 1994 Ky. Acts 248 (HB 546) (amended 2018) (new text is underlined and deleted text struck through) (“(6) ‘Firm’ means a sole proprietorship, partnership, professional service corporation, or any other form of business organization

associationengaged solely in the practice of public accountancy that is not otherwise prohibited from operating by the laws of this Commonwealth and which complies with the provisions of this chapter.”). ↑Through 1992 the American Institute of Certified Public Accountants provided that CPAs could practice as sole proprietorships, as general partnerships, and as professional service corporations. See Keatinge et al., supra note 6 at 158. It was only in 2000 that the Kentucky Supreme Court expressly permitted attorneys to practice as PSCs and (professional) LLCs. See Ky. S. Ct. Rule 3.022 (adopted by Order 99-1, effective Feb. 1, 2000). Looking at Delaware and its rules governing attorneys and the manner in which firms could be organized, through 1995 there were particular rules for professional service corporations (Del. S. Ct. Rule 67, amended effective Jan. 1, 1995), that form having been authorized for attorneys in 1969. See id., Comment. While it does not appear there was a rule particularly addressing legal partnerships, it may well be that they were so ubiquitous it was simply understood they could operate. In 1997 Rule 67 was significantly expanded to address and expressly authorize the use of a variety of forms for the organization of law firms; beyond PSCs, all partnership, limited partnership, and LLC organized firms were recognized. See Del. S. Ct. Rule 67, amended effective May 1, 1997. For our purposes the phrase used with respect to partnerships is most telling, namely “general partnerships, including registered limited liability partnerships.” Id. Were partnerships and LLPs distinct categories, we would have expected the rule of practice of the most business law–savvy court in the country to treat them as distinct (just as PSCs are from partnerships, limited partnerships, and LLCs, etc.) from one another. Instead they are treated as members of the same class. Special thanks to Paul Altman (Richards, Layton & Finger) for his assistance in tracking down this history. ↑

See, e.g., Ky. Rev. Stat. Ann. § 362.220(2); id. § 362.555 (a partial shield statute); Rev. Unif. P’ship Act (1997) § 306(c) (full shield); Colo. Rev. Stat. § 7-64-306(3); Del. Code Ann. tit. 6, § 15-306(c); Ala. Code § 10-8A-306(c); Va. Code Ann. § 50-73.96(C). See also Christine Hurt & D. Gordon Smith, Bromberg and Ribstein on Limited Liability Partnerships, the Revised Uniform Partnership Act, and the Uniform Limited Partnership Act (2001) (2nd ed.) § 3.03; id. § 3.13[C]. While this description is sufficient for purposes of this discussion, it is worth noting that affording partners in an LLP “limited liability” required more than just altering the rule of UPA § 15. In addition, there needed to be addressed the obligation of the partners each individually to contribute to the partnership to satisfy its obligations and upon liquidation to contribute to satisfy intrapartnership settling up of accounts between partners. See Unif. P’ship Act (1914) §§ 18(a), 18(b); see also Robert R. Keatinge, The Floggings Will Continue Until Morale Improves: The Supervising Attorney and His or Her Firm, 39 S. Tex. L. Rev. 279 (1998). This was accomplished in the Revised Uniform Partnership Act (1997) by section 306(c) thereto (“A partner is not personally liable, directly or indirectly, by way of contribution or otherwise, for such an obligation solely by reason of being or so acting as a partner. This subsection applies notwithstanding anything inconsistent in the partnership agreement that existed immediately before the vote required to become a limited liability partnership under Section 1001(b).”). ↑

See, e.g., Rev. Unif. P’ship Act (1997) § 201(b) (“A limited liability partnership continues to be the same entity that existed before the filing of a statement of qualification under Section 1001.”); Del. Code Ann. tit. 6, § 15-201(b); 805 Ill. Comp. Stat. 206/201(b); Ky. Rev. Stat. Ann. § 362.1-201(2); Va. Code Ann. § 50-73.132(E) (“A partnership that has been registered as a registered limited liability partnership under this chapter is, for all purposes, the same entity that existed before it registered.”). See also Colo. Rev. Stat. § 7-64-202(1) (“A limited liability partnership is for all purposes a partnership.”). ↑

The qualification recognizes that in some states a limited partnership may elect LLP status. ↑

See also Robert Hillman, Donald Weidner & Allan Donn, The Revised Uniform Partnership Act (2023–24 ed.) at § 201, Authors’ Comment 9(b):

Limited liability partnerships are often discussed as if they were a separate form of business organization. To the contrary, a limited liability partnership is not a “new” or “separate” form of business organization. Rather, a limited liability partnership is simply a partnership that qualifies for a special limited liability shield. At bottom, a limited liability partnership is either a general partnership or a limited partnership. When it files a statement of qualification, it remains the same business organization but it gets a new liability shield. If it cancels the statement, it simply sets the shield aside. ↑

Reporting companies come in two flavors: domestic, being those organized in the U.S. including one of its territories, and “foreign,” being those organized outside the U.S. and its territories. Compare 31 C.F.R. § 1010.380(c)(1)(i) with 31 C.F.R. § 1010.380(c)(1)(ii). This discussion is focused upon LLPs organized in the U.S., so any reference to a “reporting company” should be understood to be a reference to a “domestic reporting company.” ↑

For reviews of the Corporate Transparency Act, see, e.g., (i) Allison J. Donovan & Thomas E. Rutledge, The Corporate Transparency Act Is Happening to You and Your Clients: Dealing with the Tsunami, Ky. Bar Ass’n (July 30, 2024), and (ii) Robert R. Keatinge, Anne E. Conaway, Thomas E. Rutledge & Bruce P. Ely, Keatinge and Conaway on Choice of Business Entity, ch. 21 (forthcoming Nov. 2024). ↑

See CTA, 31 U.S.C.A. § 5336(a)(11). ↑

See 31 C.F.R. § 1010.380(c)(1)(i). Note that each of “State” and “Indian tribe” are defined terms. See 31 C.F.R. § 1010.380(f)(4) (definition of “Indian tribe”); id. § 1010.380(f)(9) (definition of “State”). See also Beneficial Ownership Information: Frequently Asked Questions, FinCEN.gov (hereinafter “FinCEN FAQ”) at FAQ C.7 (Jan. 12, 2024) (discussing “reporting company” status of companies created in a variety of U.S. territories). Important for this discussion is recognition that “created” is not a defined term. ↑

See also Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. 59498 at 59589 (Sept. 30, 2022):

Description of Affected Public:

Domestic entities that are: (1) corporations; (2) limited liability companies; or (3) created by the filing of a document with a secretary of state or any similar office under the law of a state or Indian tribe, and foreign entities that are: (1) corporations, limited liability companies, or other entities; (2) formed under the law of a foreign country; and (3) registered to do business in any state or Tribal jurisdiction by the filing of a document with a secretary of state or any similar office under the laws of a state or Indian tribe.

(emphasis added). ↑

See FinCEN FAQ C.9 (Apr. 18, 2024); see also Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. at 59538 (“FinCEN . . . notes that the core consideration for the purposes of the CTA’s statutory text and the final rule is whether an ‘entity’ is ‘created’ by the filing of the document with the relevant authority.”); id. (“We emphasize again that the only relevant issue for the purposes of the CTA and the final rule is whether the filing ‘creates’ the entity.”). ↑

Intentionally not addressed herein are the laws of any of the Indian tribes or of any of the U.S. territories. ↑

See, e.g., Unif. P’ship Act (1914) § 6(1); Rev. Unif. P’ship Act (1997) § 202(a); Del. Code Ann. tit. 6, 15-202(a); Ala. Code § 10A-8A-1.01; Colo. Rev. Stat. § 7-64-202(1) (“Except as otherwise provided in subsection (2) of this section, the association of two or more persons to carry on as co-owners a business for profit forms a partnership, whether or not the persons intend to form a partnership.”); Ky. Rev. Stat. Ann. § 362.175; id. § 362.1-202(1); Va. Code Ann. § 50-73.88(A). See also In re Copeland, 291 B.R. 740 (Bankr. E.D. Tenn. 2003); Flying Phoenix Corp. v. Sinclair, 2024 WYCH 3, 2024 Wyo. Trial Order LEXIS 4 (Wyo. Ch. Apr. 25, 2024) (“A partnership is formed when ‘two or more persons’ associate ‘to carry on as co-owners a business for profit,’ ‘whether or not the persons intended to form a partnership.’ The determinative intent is not the parties’ subjective intent to be characterized (or not characterized) as partners, but their ‘intent to do things that constitute a partnership.’ This means that absent a partnership agreement, or even when the parties express their subjective intent not to form a partnership, the parties may inadvertently create a partnership through their conduct.”) (citations omitted); 1 William Meade Fletcher, Fletcher Cyclopedia of the Law of Private Corporations § 20 (“A partnership is created by mere agreement between the partners. The approval of the state is not necessary.”); 2 John Bouvier, A Law Dictionary, Partnership, 11-§4, at 294 (“Partnerships are created by mere act of the parties; and in this they differ from corporations which require the sanction of state authority, either express or implied.”) (The Lawbook Exchange 2003) (1856). ↑

See Unif. P’ship Act. (1914) § 6(2); Rev. Unif. P’ship Act (1997) § 202(b); Del. Code Ann. tit. 6, § 15-202(b); Colo. Rev. Stat. § 7-64-202(1); Ky. Rev. Stat. Ann. § 362.175; id. § 362.1-202(2); Va. Code Ann. § 50-73.88(B). ↑

See Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. at 59537:

In general, FinCEN believes that sole proprietorships, certain types of trusts, and general partnerships in many, if not most, circumstances are not created through the filing of a document with a secretary of state or similar office. In such cases, the sole proprietorship, trust, or general partnership would not be a reporting company under the final rule. ↑

See Fin. Crimes Enf’t Network, U.S. Dep’t of the Treasury, Beneficial Ownership Information Reporting Rule Fact Sheet (Sept. 29, 2022):

FinCEN expects that these definitions mean that reporting companies will include (subject to the applicability of specific exemptions) limited liability partnerships, limited liability limited partnerships, business trusts, and most limited partnerships, in addition to corporations and LLCs, because such entities are generally created by a filing with a secretary of state or similar office.

(emphasis added).

In addition, pursuant to section 6502(d) of the Anti-Money Laundering Act of 2020, the U.S. Government Accountability Office is reviewing beneficial ownership requirements for trusts, partnerships, and other legal entities, and has made specific inquiries as to LLPs. Not once, not twice, but thrice in the proposed beneficial ownership information reporting regulations FinCEN referenced LLPs, but it then did not structure a definition of a reporting company that would include LLPs within its scope. See Beneficial Ownership Information Reporting Requirements, 86 Fed. Reg. 69920 at 69938–39 (proposed Dec. 8, 2021) (“In general, FinCEN believes the proposed definition of domestic reporting company would likely include limited liability partnerships, limited liability limited partnerships, business trusts (a/k/a statutory trusts or Massachusetts trusts), and most limited partnerships, in addition to corporations and limited liability companies (LLCs), because such entities appear typically to be created by a filing with a secretary of state or similar office.”); id. at 69946–47 (“In general, FinCEN believes the phrase ‘other similar entity created by the filing of a document with a secretary of state or similar office’ in the context of the definition of ‘domestic reporting company’ would likely include limited liability partnerships, limited liability limited partnerships, business trusts (a/k/a statutory trusts or Massachusetts trusts), and most limited partnerships, because such entities appear typically to be created by a filing with a secretary of state or similar office.”); id. at 69957 (“As noted above, the counts for Q6 may include general partnerships for some jurisdictions which may not be considered reporting companies; however, because they are grouped with limited partnerships and limited liability partnerships in this survey, FinCEN is retaining this number as part of its estimate.”). ↑

See Rev. Unif. P’ship Act (1997) § 901(a) (“a partnership may elect the status of a limited liability partnership [by filing a statement of qualification with the state filing officer]”); see also Cal. Corp. Code § 16953(a) (“To become a registered limited liability partnership, a partnership, other than a limited partnership, shall file with the Secretary of State a registration, executed by one or more partners authorized to execute a registration, stating all of the following: . . . .”); Colo. Rev. Stat. § 7-64-1002(1) (“A domestic partnership governed by this article may register as a limited liability partnership . . . .”); 805 Ill. Comp. Stat. 206/1001(a) (“A partnership may become a limited liability partnership pursuant to this Section.”); Ind. Code § 23-4-1-45(a) (“To qualify as a limited liability partnership, a partnership under this chapter must file a registration with the secretary of state in a form determined by the secretary of state that satisfies the following: . . . .”); Ky. Rev. Stat. Ann. § 362.555(1) (“To become and to continue as a registered limited liability partnership, a partnership that is not a limited partnership shall file . . . .”); id. § 362.1-931(1) (“A partnership may become a limited liability partnership pursuant to this section.”); Md. Code Ann., Corps. & Ass’ns § 9A-1001(a) (“A partnership formed in accordance with an agreement governed by the laws of this State may register as a limited liability partnership by filing with the Department a certificate of limited liability partnership which sets forth: . . . .”); Mont. Code Ann. § 35-10-701(1) (“To become a limited liability partnership, a partnership shall file with the secretary of state an application for registration on a form furnished by the secretary of state that indicates an intention to register as a limited liability partnership under this section.”); Va. Code Ann. § 50-73-132(A) (“To become a registered limited liability partnership, a partnership formed under the laws of the Commonwealth shall file with the Commission a statement of registration as a registered limited liability partnership stating: . . . .”); 11 Vt. Stat. Ann. § 3291(a)(1) (“Any lawful partnership may become a limited liability partnership pursuant to this section.”). ↑

See supra notes 33 through 35 and accompanying text. ↑

See also Hillman, Weidner & Donn, supra note 26. It bears noting that as it is the same partnership both before and after an election into LLP status is made, the election to be an LLP (and likewise the election to be a partnership that is not an LLP that is made when an LLP election lapses) is not a “conversion” as contemplated by certain business organization statutes including those permitting a partnership, LLP or otherwise, to convert into, for example, LLC form. Compare, e.g., Colo. Rev. Stat. § 7-64-1002 and Del. Code Ann. tit. 6, §15-1001 (dealing with registration of general partnerships to change their status to LLPs) with Colo. Rev. Stat. § 7-90-201(a) and Del. Code Ann. tit. 6, § 15-901 (dealing with a conversion of a general partnership into another entity). Thus, FinCEN FAQ C.18 (October 3, 2024), which states, “Where a conversion does result in the creation of a new domestic reporting company, the new domestic reporting company is required to file an initial beneficial ownership information (BOI) report,” does not apply to the change of status whereby a general partnership acquires the status of LLP. ↑

See, e.g., Mudge Rose Guthrie Alexander & Ferdon v. Pickett, 11 F. Supp.2d 449, 452 n. 12 (S.D.N.Y. 1998) (commenting in footnote that the New York LLP statute “clearly enunciates that a general partnership that is registered as a RLLP is for all purposes the same entity that existed before registration and continues to be a general partnership under the laws of New York”) (citation omitted); Howard v. Klynveld Peat Marwick Goerdeler, 977 F. Supp. 654, 657 n.1 (S.D.N.Y. 1997), aff’d 173 F.3d 844 (2d Cir. 1999) (upon a partnership electing to become a limited liability partnership, “The partnership was not dissolved and continued without interruption with the same partners, principals, employees, assets, rights, obligations, liabilities and operations as maintained prior to the change. Thus, Peat Marwick LLP is in all respects the successor in interest to Peat Marwick.”); Sasaki v. McKinnon, 707 N.E.2d 9 (Ohio Ct. App. 1997) (“These two entities, E&Y and E&Y LLP are, but for the corporate change to a limited liability partnership designation, the same entities for all practicable intents and purposes.”); Maupin v. Meadow Park Manor, 125 P.3d 611 (Mont. 2005) (LLP is “same entity that existed before the registration”); Ex parte Haynes Downard Andra & Jones, LLP, 924 So. 2d 687, 699 (Ala. 2005) (an LLP “is for all purposes, except as provided in Section 10-8A-306 [not relevant to our inquiry], the same entity that existed before the registration and continues to be a partnership under the laws of this state . . . .” (citing Ala. Code § 10-8A-1001(i)); Riccardi v. Young & Young, LLP, 74 Misc. 3d 911, 915 (N.Y. Cohoes City Ct. 2022) (“An LLP is a general partnership which acquires limited liability characteristics upon registration with the secretary of state.”) (citation omitted). ↑

See, e.g., Accounting Firms Reorganize to Limit Liability, L.A. Times (Aug. 2, 1994). Of course it was not just accounting and law firms that adopted the LLP format. See, e.g., Jennifer Wong Suzuki, Limited Liability Partnerships for Firms, AIA California (“With the passage of Assembly Bill 469 (Cardoza) in 1998—one [of] the AIACC’s sponsored pieces of legislation—architects can now join accountants and lawyers in forming limited liability partnerships (LLPs).”). ↑

As recounted by the PEB in the first substantive paragraph of the report:

The location of an organization, as “location” is determined under U.C.C. § 9-307, plays an important role in determining the local law that governs perfection, the effect of perfection or nonperfection, and the priority of a security interest. See U.C.C. § 9-301(1). As a general matter, a “registered organization” is located, as determined under U.C.C. § 9-307(e), in the State under whose laws the organization is organized while an organization that is not a registered organization is considered under U.C.C. § 9-307(b)(2) to be located in the State in which the organization has its place of business.

See PEB Commentary No. 17, Limited Liability Partnerships under the Choice of Law Rules of Article 9 (June 29, 2012) (footnotes omitted). ↑

Id. ↑

See 31 C.F.R. § 363.20(c)(2). ↑

See 31 C.F.R. § 1010.230(e)(1). ↑

According to the release accompanying the Reporting Regulations, “The number of legal entities already in existence in the United States that may need to report information on themselves, their beneficial owners, and their formation or registration agents pursuant to the CTA is in the tens of millions.” See Beneficial Ownership Information Reporting Requirements, 87 Fed. Reg. at 59500 (citation omitted). The footnotes accompanying the quoted language sets forth FinCEN’s estimate “that there will be at least 32.6 million ‘reporting companies’ (entities that meet the core definition of a ‘reporting company’ and are not exempt) in existence when the proposed rule becomes effective.” Id.; see also id. at 59562. That same document goes on to state: “Summing the estimates of both domestic and foreign entities, the total number of existing entities in 2024 that may be subject to the reporting requirements is 36,581,506 and the total number of new companies annually thereafter is 5,616,382.” Id. at 59565 (citation omitted). ↑