Retirement plans are the bedrock of financial security for millions of Americans. Historically, these systems’ complexity has insulated plan managers from accountability if they fail to meet legal obligations.

That shield is now cracking.

Courts are establishing precedents favoring plaintiffs earlier in the process, and the arrival of legal intelligence driven by artificial intelligence is making it possible to detect violations at scale. In this article, we explore how the legal community can seize this new opportunity to protect plan participants more effectively than ever before.

The Scope of ERISA Litigation Is Expanding

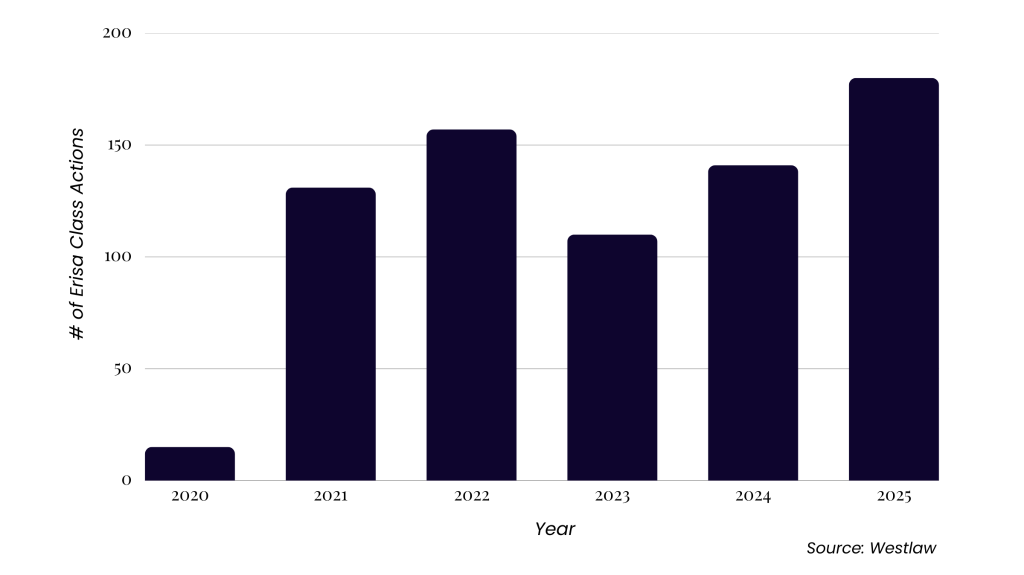

ERISA class actions are growing in volume and financial impact. The total of the top ten publicly reported ERISA settlement values reached $580.5 million in 2023 alone (an all-time high) and $413.3 million the following year, according to Duane Morris. Data analyzed from Westlaw indicates that filing counts have risen dramatically, too, from just fifteen cases in 2020 to more than 180 in 2025 (see graph below).

This growth comes as plaintiffs broaden their scrutiny of plan sponsors’ fiduciary responsibilities, moving beyond excessive fees and employee stock ownership plan (“ESOP”) violations to include an increasing number of claims involving forfeiture, pharmacy benefit manager (“PBM”) fees, and more.

The litigation has focused on two employer-sponsored retirement plan types:

- Defined contribution plans: Employees have individual accounts, such as 401(k)s, and their retirement outcomes depend on contributions and investment performance.

- Defined benefit plans: These traditional pension plans promise employees a fixed benefit at retirement. The employer must ensure the plan has enough assets to pay those benefits; oversight of how employers manage these plans is critical.

ERISA Class Actions 2020–2025

ERISA class actions have risen from just fifteen cases filed in 2020 to more than 180 in 2025.

Why Are ERISA Violations So Difficult to Detect?

Five structural features of retirement plans make detecting ERISA violations a challenge.

- Data structures are complex and opaque. The information needed to assess plan performance is buried in Form 5500 filings, schedules, and attachments. These dense materials often lack standardized naming, contain inconsistent spellings, and require reconciliation with external data.

- Investments are hidden inside complex vehicles. Many plans invest through collective trusts, pooled separate accounts, and target-date funds. Aggregated reporting can make underperformance in a fund’s underlying holdings difficult to detect.

- Fee indication challenges are excessive. Fee arrangements vary by recordkeeper and investment provider, making it difficult to compare costs across plans and to determine whether fiduciaries secured reasonable pricing.

- Forfeiture practices lack transparency. Determining how employer contributions are handled when an employee leaves often requires plan-by-plan reviews, as plan changes and payroll or vesting records often aren’t shown in Form 5500 filings.

- Multiyear plan reconstruction is time-consuming. Addressing imprudent investment claims often requires examining performance over multiyear periods and determining whether the right comparison benchmarks were used. Without automation, this analysis is cumbersome.

Six Cases Driving New ERISA Filings

Several recent Supreme Court decisions have established precedents that have pushed ERISA litigation forward.

Year | Case | Impact |

2020 | Reduced the reliability of ERISA statute of limitations defenses by requiring proof that plaintiffs read and understood the disclosures. This has allowed more fiduciary breach claims, particularly older ones, to proceed. | |

2020 | Closed the door on many defined benefit fiduciary breach lawsuits, causing plaintiff firms to shift focus to defined contribution plans, contributing to the rise in excessive fee and imprudent investment class actions. | |

2020 | Gave states more room to regulate PBMs, creating a pathway for more state law claims over drug pricing, reimbursement practices, and cost-containment structures within ERISA health plans. (State laws tend to be stricter on insurance plans.) | |

2022 | Made it easier for plaintiffs to get their ERISA cases heard, triggering a wave of excessive fee and recordkeeping fee lawsuits, many of which survived motions to dismiss based on this case. | |

2025 | Made it easier for ERISA lawsuits to survive early dismissal, encouraging plaintiffs to combine prohibited transaction claims with excessive fee and fiduciary breach claims. This increases plaintiffs’ ability to get their cases heard and expands the ERISA case types that proceed to discovery. |

Five Trends and Signals Shaping ERISA Litigation Today

With new precedent expanding accountability across the retirement and benefits ecosystem, litigation is moving into areas that require data-driven analysis.

- Excessive fee litigation and imprudent investment claims remain the core of ERISA class actions. Most new cases continue to challenge recordkeeping fees, investment expenses, and fiduciary oversight in defined contribution plans. Stable value funds, share class practices, and recordkeeping arrangements remain frequent targets. These claims will continue to anchor ERISA litigation.

- Fee litigation is expanding into midsized plans. Lawsuits have long focused on large plans with billions in assets because they offered the most significant potential recoveries. That is shifting. Over 40 percent of cases in 2024 were filed against plans with assets under $1 billion, indicating an emerging area of opportunity.

- Adviser and service provider liability is emerging as a new frontier. Plaintiffs are naming plan advisers, brokers, and consultants as co-fiduciaries, particularly where conflicts of interest or self-interested fee structures appear to have influenced plan decisions. Future litigation may also include business-to-business claims in which employers seek indemnification from advisers whose recommendations created fiduciary exposure.

- Health and welfare plan litigation is gaining momentum. Although ERISA litigation has traditionally centered on retirement plans, new transparency rules, limited federal enforcement activity, and a history of troubling fiduciary breaches could spur more private litigation. This area, which has significantly higher total spend and less oversight, includes:

- PBM pricing and rebate structures

- excessive commissions and conflicts in voluntary benefit products

- claims handling practices in self-funded plans

- gaps in employer oversight of third-party administrators and algorithms

- Regulatory developments are creating new areas of fiduciary risk. The White House’s 2025 executive order calling to expand alternative investments in 401(k) plans may encourage new claims regarding valuation, liquidity, fees, and risk disclosure. Fiduciaries that adopt these products without adequate documentation and monitoring may face higher risk of investment lawsuits.

The Opportunity: Legal Intelligence and ERISA Enforcement

Legal intelligence—the use of AI, data analysis, web intelligence, and legal expertise to identify actionable violations—is changing how plaintiff attorneys detect ERISA noncompliance. Instead of manually reviewing and reconciling fragmented plan documents, attorneys can now systematically surface patterns and anomalies that warrant closer legal analysis and select comparable funds. Peer groups can be selected that closely mirror the characteristics of the challenged funds to maximize chances of success on the merits at trial.

The comparators for each fund align closely with their corresponding fund across various dimensions, including: (1) similar equity-to-fixed-income allocations; (2) active management rather than passive or index-based strategies; (3) comparable asset sizes, ensuring scale-appropriate performance comparisons; and/or (4) similar expense ratios.

Aligning these factors between the challenged funds and the selected peer comparators ensures that the identified underperformance reflects genuine deficiencies in investment management.

Using legal intelligence, attorneys can:

- Aggregate Form 5500 data and harmonize fund disclosures across disparate naming conventions and share classes.

- Map investment lineups and fee evolution, accounting for plan amendments, freezes, or conversions.

- Identify outliers in administrative fees and persistent investment underperformance relative to peer groups.

- Detect friction between plan documents and actual reported practices.

- Surface plans with data signatures that mirror past ERISA litigation triggers.

As ERISA litigation becomes more specialized and reliant on large datasets, AI-driven analysis is essential for effective case development. Legal intelligence brings hidden risk into view, supporting a more deliberate, evidence-based approach to identifying fiduciary failures and safeguarding plan participants.