Despite the existence of a global pandemic that we continue to navigate, the payments ecosystem is experiencing robust growth, amplifying certain trends such as shifting to omnichannel and contactless payments. We are seeing disruption across the payments ecosystem as new competitors enter the fray and scale up and new business models emerge. The pandemic has led to a surge in e-commerce, including transactions on “marketplaces”—online sites that match buyers and third-party sellers. Previously, it was primarily brick-and-mortar merchants who entered e-commerce through online platforms.

The development of new payment technologies, such as peer-to-peer payment technologies and contactless payment technologies, shows the payments ecosystem has evolved to provide an expanded set of point-of-sale payments options for consumers. The payments ecosystem is leveraging improvements in technology to adapt to consumer demand for speed and convenience, as well as for “touchless” aspects that make such technology desirable for consumers to use at point-of-sale during a pandemic.

The panel “Payments Link: Rails, Platforms, and Deals,” held virtually on September 22, 2021, as part of the 2021 Business Law Virtual Section Annual Meeting, shed light on the aforementioned issues by featuring a discussion on the current payments landscape and key considerations for merchants and consumers with respect to their preferred payment methods. The speakers on the panel were:

Judy Mok, Partner at Ballard Spahr (moderator)

Tracy Cheney, General Counsel of Early Warning Services

Lisa Detig, Vice President & Associate General Counsel Americas at Match Group, LLC

Ryan Richardson, Lead Global Partnerships Counsel at Stripe Inc.

Ling Ling Ang, Associate Director at NERA Economic Consulting

In this panel, Ling Ling Ang highlighted recent (at the time) antitrust developments related to the payments ecosystem, such as the termination of Visa’s proposed acquisition of Plaid following a suit filed by the U.S. Department of Justice; Square, Inc.’s acquisition of Afterpay; and the filing of Camp Grounds Coffee, LLC et al. v. Visa, Inc. et al. Interest in antitrust in financial services at the federal level is demonstrated by the U.S. Department of Justice’s newly established Financial Services, Fintech, and Banking Section, along with the July 9, 2021, Executive Order on Promoting Competition in the American Economy. Antitrust considerations in payments include the effects of vertical mergers, the role of platforms, digitization, and consumer welfare. The panel discussed how the evolution of payments ecosystems appears to call for additional critical legal and economic analysis, likely applying novel models and techniques.

There was an in-depth discussion on Zelle, a peer-to-peer payment solution provider and how it works. Tracy Cheney provided basic statistics about Zelle in terms of volume and participants. Cheney discussed how the money movement flows with Zelle, its distribution channels, and integration with settlement rails such as Visa, Mastercard, ACH, and RTP. Cheney also highlighted some payment opportunities using Zelle, including:

Person-to-Person Payments (P2P): paying a babysitter, a mom sending emergency money to a kid at college, or paying a friend back for purchasing concert tickets

Consumer-to-Business Payments (C2B): paying for general services around the house, such as landscaping or cleaning; paying rent; paying a personal trainer or groomer

Business-to-Consumer Payments (B2C): insurance companies disbursing insurance proceeds to a homeowner, an employer reimbursing employees for travel and expenses, a class action administrator disbursing a settlement pool

Cheney also discussed the Zelle Network’s governance structure.

Ryan Richardson discussed the flow of data and funds in the payment system, and Stripe’s role in the payment system. This role differs country to country: “Stripe is an acquirer in most of the European Union and the United Kingdom, Hong Kong, Singapore, and many parts of Asia, but in the United States and some other markets, [Stripe] is not a direct or a principal member of the payment system.” He also discussed other services Stripe provides to its customers, including business analytics services.

The panel also discussed the rise of other payment options, including card not present transactions and buy now, pay later (BNPL) programs (the latter of which may be offered in both online and in-store channels), which is consistent with payment methods having evolved to address pain points in the way customers shop and pay online. Judy Mok discussed how millennials make up a substantial portion of the customer base for BNPL programs because these types of programs tend to appeal to younger consumers who may be wary of credit cards. Traditional financial services players and Silicon Valley giants alike are trying to enter this line of business that fintechs have pioneered. Some recent examples include Comenity Bank’s acquisition of Bread and Apple Inc. and Goldman Sachs’s entry into the BNPL space, along with Square, Inc.’s acquisition of Afterpay.

The panel discussed how, for merchants to offer payment solutions that are attractive to consumers (whether on the acceptance or issuance side), merchants must enter into commercial agreements with payments solution providers (whether such a provider is a financial institution, a fintech partner or some other third-party provider) to provide such offerings to their customers. Lisa Detig spoke about procurement processes for and considerations of merchants in strategic payments arrangements. Considerations include information security and data privacy, the long-term nature of the partnerships, and potential evolution in the payments landscape.

Panelists shared legal contractual considerations for merchants looking to enter strategic partnership arrangements in the payments space. The panel also discussed allocation of risk in the payment world including liability for unauthorized transactions, misdirected payments, and scams.

On February 24, 2022, Lex Machina released its 2022 Law Firms Activity Report (the “Report”). The Report ranked firms across sixteen federal practice areas over the last three years, revealing which firms filed and defended the most cases in how many districts and involving what amounts of damages.

In the past, in-house attorneys have used this report as a starting point for selecting outside counsel. Law firms have historically used the report to understand how they compare to their peers and competitors in order to maximize their strategies in bids for clients. However, the report also provides valuable data-driven insights into evolving litigation trends across practice areas, districts, and time.

One of the most interesting trends highlighted in the report involves the effect of the COVID-19 pandemic on case filings in various practice areas. When the pandemic first began two years ago, Lex Machina began to track cases caused by COVID-19 (the “COVID Cases”), and it continues to do so now. The data and analytics from tracking these cases reveal that the impact of COVID-19 on litigation activity in different practice areas has continued to evolve and change as the pandemic has progressed.

For example, several of the most active law firms involved in COVID Cases filed cases under the American Disabilities Act (the “ADA”) or alleged employment claims. This pattern contrasts with litigation activity in the early stages of the pandemic, when according to Lex Machina’s previous Law Firms Activity Report, contracts and securities case filings were some of the most robust, as plaintiffs reacted to broken contracts and plummeting stock value. These trends likely reflect the fact that the later stages of the pandemic have tended to heavily impact different practice areas, such as employment and civil rights cases involving the ADA. This stands to reason, as over time, remote-work situations and morphing government mandates have given rise to a new host of legal issues. The Report indicated that employment defense firms were especially busy, filing cases involving claims related to vaccine mandates, disability discrimination, whistleblower retaliation, and lack of protective equipment, among other claims.

In addition, the case filing trends revealed that class actions and lawsuits related to singular large-scale events continued to influence the legal landscape and drive up case counts, particularly in the areas of product liability, torts, and insurance. For example, in product liability, the most active law firms representing plaintiffs and defendants were each involved in approximately 800 cases in 2020 that were related to a Bard medical device, which drove up their three-year case counts and placed them at the top of the lists of most active firms.

Some other trends revealed in the Report include the Department of Justice’s continued dominance as the most active counsel overall. In terms of the most active law firms, the Legal Analytics showed that while some law firms with high case counts had dedicated specializations, there were several national litigation firms that appeared in multiple practice areas. For example, Skadden, Arps, Slate, Meagher, & Flom topped two different lists for defense firms in the practice areas of Antitrust and Securities, while Fox Rothschild appeared in multiple lists of top firms in the Bankruptcy, Contracts, Copyright, False Claims, Trade Secret, and Trademark practice areas. Many of the most active employment firms, such as Jackson Lewis, also appeared in the lists of the most active firms with cases caused by COVID, as well as the most active firms overall.

The Report revealed several key litigation trends over the last three years, as well as highlighting the law firms and counsel that were most active in different practice areas during this time. Leveraging the data-driven insights provided by the Report can be powerful for gaining an enhanced understanding of the evolving landscape of federal litigation.

Lex Machina’s Law Firms Activity Report presented data from Lex Machina’s Legal Analytics platform. Using machine learning and technology-assisted attorney review, raw data was extracted from PACER (Public Access to Court Electronic Records), which contains documents from federal district court. The raw data was then cleaned, tagged, structured, and loaded into Lex Machina’s proprietary platform. The report was prepared by the Lex Machina Product Team using charts and graphs from the platform. The commentary was provided by Lex Machina’s legal experts.

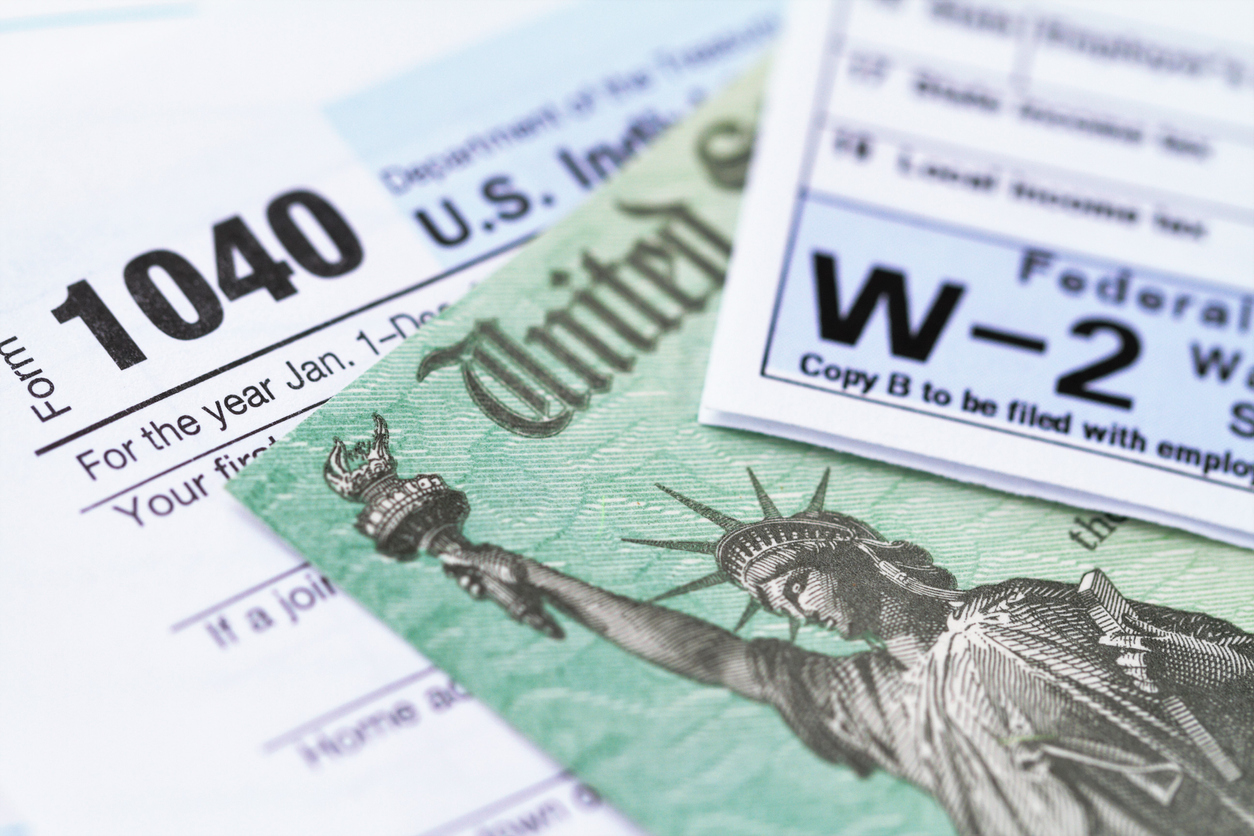

If you hope to write off your legal fees, there is some good news from the IRS. Before you rejoice, the bad news is that the complex and confusing rules governing when legal fees are deductible have not gotten any easier. There are still plenty of cases in which deducting legal fees is difficult or when the rules seem to say that you shouldn’t be deducting them at all. Even so, there is some good news, because the mechanics for deducting employment, whistleblower, and civil rights legal fees have been improved, at long last: starting with 2021 tax returns, the IRS is implementing a new Form 1040 that has a line item for attorney fees.

Deductions Were Previously Hard to Claim

The tax code was amended back in 2004 to allow legal fee deductions “above the line” in some cases, which is almost like not having the income in the first place. But the deduction has been quirky to claim ever since. Many taxpayers have trouble; so do accountants and some types of tax return preparation software. That is barely surprising. Since 2004 it has been a kind of write-in deduction, sort of like writing in a political candidate who isn’t on the ballot.

Before and after 2004, the other kind of deduction was below the line. That meant subject to all sorts of limits and thresholds (including the dreaded alternative minimum tax (AMT)). The result was usually that you lost much or even all of your deduction. And starting in 2018, that below the line deduction went away entirely (until 2026, when it is supposed to come back). Talk about confusing. So this above the line deduction was and remains terribly important, which is one reason why how to claim it is so critical.

I have seen plenty of mechanical glitches with these deductions since 2004. I have seen some plaintiffs not properly claim the deductions they deserve and some plaintiffs and their return preparers not claim them at all—sometimes purely or largely because they cannot seem to manage the mechanics. In that sense, the easier mechanics created by the recent IRS update are a big win.

Because the previous versions of Form 1040 did not have a separate line to write in “other” above-the-line deductions, above-the-line deductions involving employment, whistleblower, and civil rights cases had to be written onto the dotted leader line next to the box where the total of the above-the-line deductions was to be calculated. This reporting not infrequently created confusion with the computer systems of state taxing agencies, because their algorithms often didn’t recognize the legal fee deduction reported on the leader line, or outside of any box of the form.

State agencies, like California’s Franchise Tax Board, would regularly send notices to taxpayers who followed the IRS’s instructions asserting that the taxpayers’ tax returns must contain a calculation error: The total of the above-the-line deductions reported in the boxes of the Form 1040 as calculated by the states’ computers simply did not match the taxpayer’s self-reported total on the tax form, they said. Of course, in these cases, the supposed calculation error was simply that the taxpayer’s calculated total correctly included the legal fee deduction written onto the leader line, whereas the state’s calculation did not. Even though these state notices are relatively easy to address, it was obviously frustrating to taxpayers to default into a state income tax examination over a poorly drafted tax form.

Not only was there no proper line for legal fee deductions on the IRS forms, but you had to include a particular code next to your write-in. If your case was an employment case, the code to enter was “UDC” for unlawful discrimination claim. The instructions said:

Write “UDC” and the amount of the attorney’s fees next to line 36 of Form 1040. For example, if you paid $100,000 in attorney fees, write “UDC $100,000” next to line 36.

If your case was a whistleblower case, you put in “WBF” for whistleblower. (I’m not sure what the F stood for, though “fees” seems the most likely candidate).

But at long last, starting with 2021 tax returns, the IRS is finally making it easier with a new Form 1040 that has a line item for attorney fees. For 2021, Schedule 1 to Form 1040 now gives you two lines. Line 24 of Part II, Adjustments to Income, allows for:

(h) Attorney fees and court costs for actions involving certain unlawful discrimination claims $_________

(i) Attorney fees and court costs you paid in connection with an award from the IRS for information you provided that helped the IRS detect tax law violations $_______

Notably, there is still not a separate line item specifically for “WBF” whistleblower fees under Section 62(a)(21). Perhaps that deduction is too rarely claimed to merit its own line. Still, the new form makes life a little better for those claiming “other” above-the-line deductions that do not have their own line on the tax form. The IRS has finally included an “other adjustments” line, Line 24z, where other above-the-line deductions can be reported in an actual box on the form without having to write them onto any leader lines. Hopefully, the inclusion of this catchall line will fix the state “calculation error” notices issue created by the previous versions of the Form 1040.

When the IRS updated the Form 1040, it also updated its instructions for the Form 1040, which now make no mention of the codes (“UDC” and “WBF,” for example) that used to be necessary to identify the deduction on the old forms. That makes sense for UDC deductions under Section 62(a)(20), since they now have their own line and do not have to be identified by a code.

However, this is somewhat puzzling for the above-the-line deductions that have not been given their own lines, since taxpayers will still need to identify the type of “other” deduction claimed on the new catchall Line 24z. It will be interesting to see if tax preparers continue to use “WBF” to identify whistleblower fee deductions out of convention, even though that code is no longer required or mentioned in the form’s instructions.

Plaintiffs Paying Tax on Legal Fees

Why worry about deducting legal fees in the first place? Most plaintiffs would rather have the lawyer paid separately and avoid the need for the deduction. Unfortunately, it is not that simple. If the lawyer is entitled to 40 percent, the plaintiff generally will receive only the net recovery after the fees. Most plaintiffs therefore sensibly assume that the biggest tax they could face would be tax on their net recoveries.

However, regardless of how the checks are cut, the plaintiff must usually contend with 100 percent of the proceeds under Commissioner v.Banks, 543 U.S. 426 (2005). As a result of that seminal case, plaintiffs in contingent fee cases must generally recognize gross income equal to 100 percent of their recoveries, even if the lawyer is paid directly, and even if the plaintiff receives only a net settlement after fees. This harsh tax rule usually means plaintiffs must figure out a way to deduct their 40 percent (or other) fee.

Fortunately, in 2004 shortly before Banks was decided, Congress enacted an above-the-line deduction for employment claims, civil rights claims, and some whistleblower claims. Plaintiffs in employment and civil rights cases can use this deduction for contingent fees, generally ensuring that they are taxed on their net recoveries, not their gross. Even so, many taxpayers and return preparers have had trouble with the mechanics of claiming it, as discussed above. There are also technical limits because a plaintiff’s deduction for fees in employment, civil rights, and qualifying whistleblower cases cannot exceed the income the plaintiff received from the litigation in the same tax year.

If all the legal fees are paid in the same tax year as the recovery (such as in a typical contingent fee case), that limit causes no problem. But this is a problem if the plaintiff has been paying legal fees hourly over several years. In that event, there is no income to offset, so you cannot deduct the fees above the line. Paying back the prior fees and having the lawyer charge them again in the year of the settlement is sometimes suggested to bring the fee payment into the same tax year as the recovery. It is unclear if that kind of circular flow of funds would adequately address the issue, although perhaps it might give a potential return position.

Who Can Claim the Above-the-Line Legal Fee Deduction?

The big question, of course, is what types of cases qualify for the above-the-line deduction? The answer is that only employment, civil rights, and some types of whistleblower claims qualify for it. Some people fear that employment cases based on contract disputes without discrimination might somehow not qualify. Perhaps that fear was fueled by the “UDC” notion that might seem to suggest that only unlawful discrimination claims (as opposed to all employment claims) qualify. However, there is a catchall provision, section 62(e)(18), that seems to cover the waterfront and make the long list of claims unnecessary. In the tax code itself, any claim about employment is actually defined as an unlawful discrimination claim.

Unlawful Discrimination

The above-the-line deduction applies to attorney fees paid because of claims of “unlawful discrimination.” The definition of such claims refers to claims for unlawful discrimination brought under these federal statutes:

the Civil Rights Act of 1991;

the Congressional Accountability Act of 1995;

the National Labor Relations Act;

the Fair Labor Standards Act of 1938;

the Age Discrimination in Employment Act of 1967;

the Rehabilitation Act of 1973;

the Employee Retirement Income Security Act of 1974;

the Education Amendments of 1972;

the Employee Polygraph Protection Act of 1988;

the Worker Adjustment and Retraining Notification Act;

the Family and Medical Leave Act of 1993;

chapter 43 of Title 38 (concerning employment rights of uniformed service personnel);

Section 1981, Section 1983, and Section 1985;

the Civil Rights Act of 1964;

the Fair Housing Act; and

the Americans with Disabilities Act of 1990.

It also refers to claims permitted under any provision of federal law (popularly known as whistleblower protection provisions) prohibiting discharge, discrimination, retaliation, or reprisal, and under any provision of federal, state, local, or common law providing for the enforcement of civil rights or regulating any aspect of the employment relationship.

Catchall Employment Claims

Arguably the most important piece in all this is the section 62(e)(18) catchall provision, which makes a deduction available for claims alleged under:

Any provision of federal, state, or local law, or common law claims permitted under federal, state, or local law —

i. providing for the enforcement of civil rights, or

ii. regulating any aspect of the employment relationship, including claims for wages, compensation, or benefits, or prohibiting the discharge of an employee, the discrimination against an employee, or any other form of retaliation or reprisal against an employee for asserting rights or taking other actions permitted by law.

This language is very broad. Some people may argue that an employment contract between a company and an executive doesn’t involve alleged discrimination and might not be covered. However, it seems hard to argue that an employment contract dispute does not amount to an employment matter within the meaning of this broad catchall statement. Many people claim these deductions and have been doing so since 2004. Yet so far, there is little guidance on this issue.

In LTR 200550004, however, the IRS ruled that attorney fees and costs rendered to obtain federal pension benefits fell within the catchall category. The case concerned a taxpayer who, after his retirement, discovered that he was being shortchanged on his pension. The IRS found unlawful discrimination. Interestingly, the IRS ruled that the case fell within the catchall category for unlawful discrimination even though the action was brought under ERISA (one of the enumerated types of unlawful discrimination).

Because only actions brought under section 510 of ERISA are expressly allowed under section 62(e), the catchall provision was needed to cover the taxpayer’s case. This ruling suggests an expansive reading of the catchall category, and so does the plain language of the statute.

Whistleblower Recoveries

The “unlawful discrimination” deduction also creates an above-the-line deduction for whistleblowers who were fired from their employment or retaliated against at work. But what about whistleblowers who expended legal fees to obtain a qui tam award but were not fired? Separately from the unlawful discrimination deduction, section 62 allows these qui tam plaintiffs to deduct their attorney fees above the line.

Several features about fees in non-employment whistleblower cases are noteworthy. Originally, the law for non-employment whistleblowers covered only federal False Claims Act cases. In 2006 the above-the-line attorney fees deduction was expanded to include attorney fees paid by tax whistleblowers in cases brought under section 7623 (regarding detection of underpayments of tax, fraud, etc.). In 2018 it was extended to SEC and Commodities Futures Trading Commission whistleblowers. Regarding False Claims Act recoveries, commencing with the 2018 tax year, the above-the-line deduction for attorney fees was extended to cover state whistleblower statutes as well.

Civil Rights Claims

The catchall language in section 62(e)(18) also provides for the deduction of legal fees to enforce civil rights. This unlawful discrimination deduction is arguably even more important than the deduction for fees concerning employment cases. What exactly are civil rights, anyway? You might think of civil rights cases as only those brought under 42 U.S.C. section 1983.

However, the above-the-line deduction extends to any claim for the enforcement of civil rights under federal, state, local, or common law. Section 62 of the Internal Revenue Code does not define “civil rights” for purposes of the above-the-line deduction, nor does the legislative history or committee reports. Some definitions are broad indeed, including:

. . . a privilege accorded to an individual, as well as a right due from one individual to another, the trespassing upon which is a civil injury for which redress may be sought in a civil action. . . . Thus, a civil right is a legally enforceable claim of one person against another. See Volume 15, American Jurisprudence, 2d at Page 281, quoted in In re Colegrove, 9 B.R. at 339 (emphasis added).

Moreover, in an admittedly different context (charitable organizations), the IRS itself has generally preferred a broad definition of civil rights. In one general counsel memorandum, the IRS stated: “We believe that the scope of the term ‘human and civil rights secured by law’ should be construed quite broadly.” Could invasion of privacy cases, defamation, debt collection, and other such cases be called civil rights cases? Possibly.

What about credit reporting cases? Don’t those laws arguably implicate civil rights as well? Might wrongful death, wrongful birth, or wrongful life cases also be viewed in this way? Of course, if all damages in any of these cases are compensatory damages for personal physical injuries, then the section 104 exclusion should protect them, making attorney fees deductions irrelevant.

However, what about punitive damages? In that context, plaintiffs may once again be on the hunt for an avenue to deduct their legal fees. Reconsidering civil rights broadly might be one way to consider fees in the new environment. In any event, the scope of the civil rights category for potential legal fee deductions seems broad.

Conclusion

The IRS gets big points for fixing what has been a tough deduction to claim since 2004. Personally, I’m still not used to the Schedule 1 idea for Form 1040, which may have been part of the effort to make tax returns more akin to postcards. Of course, we know how that turned out. But those issues aside, the IRS change for 2021 returns with the express line item for above-the-line attorney fees is a huge win.

Schedule 1 devotes two lines to these deductions: Line 24 of Part II, Adjustments to Income, for “(h) Attorney fees and court costs for actions involving certain unlawful discrimination claims” and “(i) Attorney fees and court costs you paid in connection with an award from the IRS for information you provided that helped the IRS detect tax law violations.” Don’t overlook them.

In recent months, two courts expressed disapproval of the use of non-consensual third-party releases in plans of reorganization: (i) the Southern District of New York, in In re Purdue Pharma, L.P., and (ii) Eastern District of Virginia, in Patterson v. Mahwah Bergen Retail Group, Inc. These decisions represent a significant shift towards curtailment of the use of non-consensual third-party releases in plans of reorganization. Non-consensual third-party releases arise in Chapter 11 plans and are an uncommon tool in bankruptcy proceedings. Instead of voluntary releases—which are the typical, and preferred, tool in Chapter 11 plans—a non-consensual third-party release is generally sought when the claim(s) against the third party must be released because the third party has a substantial and essential economic contribution that makes such release vital to the plan.

The Southern District of New York’s Decision in In re Purdue Pharma L.P.

On December 16, 2021, Judge McMahon of the Southern District of New York reversed the Bankruptcy Court’s confirmation of the Debtors’ plan of reorganization because of the non-consensual third-party release provisions in the plan.[1] In her decision, Judge McMahon analyzed whether Section 105(a), 1123(a)(5), 1123(b)(6), or 1129 of the Bankruptcy Code authorizes the Bankruptcy Court’s approval of non-consensual third-party releases. Judge McMahon concluded that none of those statutory sections confer authority on the Bankruptcy Court to grant non-consensual third-party releases.

After concluding that the Bankruptcy Code does not expressly authorize the approval of the third-party releases at issue, Judge McMahon considered the Debtors’ argument that the Bankruptcy Court could approve the non-consensual third-party releases because of the lack of any statutory prohibition prohibiting them. Judge McMahon rejected the Debtors’ argument, finding that Congress’s silence on the issue does not mean that the Bankruptcy Court has authority to approve non-consensual third-party releases. In contrast, as Judge McMahon noted, Congress has expressly authorized such releases, assuming certain conditions are met, in asbestos-related cases.[2]

The Eastern District of Virginia’s Decision in Patterson v. Mahwah Bergen Retail Group, Inc.

Following on the heels of the Judge McMahon’s decision in In re Purdue Pharma, Judge Novak of the Eastern District of Virginia similarly disapproved of the use of non-consensual third-party releases in a plan of reorganization in his January 13, 2022 decision.[3] In the underlying bankruptcy case, the Bankruptcy Court approved broad non-debtor releases of—among other claims—securities-fraud claims against the Debtors’ insiders as part of the Bankruptcy Court’s confirmation of the Debtors’ plan of reorganization. Finding the third-party release provisions void and unenforceable, Judge Novak labeled the breadth of the release provisions as “shocking” and cautioned that third-party releases are a “device that lends itself to abuse.”

In reaching his decision, Judge Novak expressed significant concern with the due process implications of non-consensual third-party releases, explaining that the “third-party releases strike at the heart of these fundamental rights.” As the third-party releases would release the claims of—at a minimum—hundreds of third parties without their consent, Judge Novak held that the third-party releases “offended the most fundamental precepts of due process.”

In addition, Judge Novak held that the Bankruptcy Court lacked jurisdiction to approve the broad, third-party releases at issue. Analyzing whether the Bankruptcy Court has constitutional authority to release the claims of third parties under the Supreme Court’s decision in Stern v. Marshall,[4] Judge Novak found that the Bankruptcy Court:

failed to identify whether it had jurisdiction over the released claims; and

lacked jurisdiction over many of the released claims because such claims included claims between non-debtors that have little to no connection to the bankruptcy estate or the administration of the bankruptcy case.

Conclusions & Takeaways

The In re Purdue Pharma and Mahwah Bergen Retail Group decisions add to the growing uncertainty regarding the use of third-party non-consensual releases in a plan of reorganization. Even prior to the In re Purdue Pharma and Mahwah Bergen Retail Group decisions, courts had been split on the issue of third-party non-consensual releases. Judge McMahon’s and Judge Novak’s decisions add to the increasing body of case law that either disfavors or expressly prohibits the use of broad, non-consensual third-party releases.[5] In the wake of these decisions and until the uncertainty regarding the use of third-party of releases is resolved, debtors will have to proceed cautiously before seeking approval of broad, non-consensual third-party release provisions in a plan of reorganization.

Judge McMahon’s decision can be found at In re Purdue Pharma, L.P., 7:21-cv-08566-CM (S.D.N.Y. Dec. 16, 2021). ↑

See, e.g., In re Pac. Lumber Co., 584 F.3d 229 (5th Cir. 2009); In re Lowenschuss, 67 F.3d 1394 (9th Cir. 1995); In re W. Real Estate Fund, Inc., 922 F.2d 592 (10th Cir. 1990). ↑

This article is related to a Showcase CLE program at the ABA Business Law Section’s 2022 Hybrid Spring Meeting. To learn more about this topic, view the program as on-demand CLE, free for Section members.

Traditionally, corporations’ main risk factors were related to business and business environment, and the primary criterion for evaluating corporate action was maximizing shareholder welfare and return. Recently, a new set of risk criteria outside the traditional focus on financial performance is gaining prominence: environmental, social and governance (ESG) risk management. ESG risks are more than just reputational—they can include costly litigation, hefty fines, seizures at U.S. ports, debarment, bank insecurity, and plunging stock value. Bottom line: ESG risks can stop or seriously delay company operations.

On March 31, a panel discussion at the American Bar Association Business Law Section Hybrid Spring Meeting will consider the evolution of ESG concerns and reporting, from philanthropic and discretionary corporate social responsibility (CSR) acts to required disclosure and regulatory focus as an inherent part of valuation. The breadth of shareholder proposals related to ESG and the importance of board governance and oversight will be discussed, along with the need for robust internal ESG governance processes for assessing materiality. The panelists will examine ESG risks through the eyes of not only major company or financial institution general counsel or senior in-house and outside counsel, but also of a diverse group of professionals in this area from several perspectives, including the founder and president of a leading human rights litigation advocacy group. These perspectives include:

Regulatory activity regarding climate risk within the financial services sector, including expectations of the Office of the Comptroller of the Currency and the Federal Reserve Board. In addressing climate risk, financial institutions must analyze physical risk (e.g., the risk associated with the direct impact of climate change on institutions’ physical assets and the physical assets of their borrowers); transition risk (e.g., the risk associated with increased market demand for lower carbon–producing products and services); acute risks (e.g., the risks associated with a specific short-term climate event, such as a natural disaster); and chronic risks (e.g., the risks associated with the increase in frequency of natural disasters over time). The panelists will provide an overview of recent developments and discuss the practical implications for financial institutions and their customers.

Litigation risks for companies as well as board members and officers, whether from regulatory agencies, private plaintiffs, or public interest organizations. Discussion also will include the status of strategic litigation in the human rights arena; other mechanisms underway that can disrupt labor trafficking, such as the Trade Facilitation and Trade Enforcement Act and the Federal Acquisition Regulation; trends in the litigation arena; and the status of extraterritorial application in human rights cases.

Risks springing from the draft E.U. Directive requiring human rights due diligence and remediation of adverse impact issues in supply chain management, and specific contract assurances addressing such human rights initiatives, including the concept of shared responsibility. Recently, shared responsibility was addressed in a unique buyer code of conduct found in Version 2.0 of the Model Contract Clauses to Protect Human Rights in International Supply Chains (the MCCs), which incorporate the UN Guiding Principles on Business and Human Rights (UNGPs) and the Organisation for Economic Co-operation and Development (OECD) guidelines and are drawn from the ABA Model Principles on Labor Trafficking and Child Labor. Published in the Winter 2021–2022 issue of The Business Lawyer, the MCCs integrate human rights due diligence into every stage of the supply chain contract, allow enforcement by every buyer and supplier in the chain (eliminating conventional privity of contract), and prioritize remediation of human rights harms over conventional contract remedies.

Other newly manifest risks that have surfaced in recent years.

The program will emphasize how companies, banks, investors, and advisors take legal risks all the time, but often fail to integrate these risks effectively in an environment that is changing continuously. Those who ignore these and other ESG risks do so at their peril and miss the chance to create long-term value as advocated by BlackRock CEO Larry Fink in his last few annual CEO letters. As the demand for data and transparency with respect to ESG factors increases, the need to break down silos and be sure legal oversight is truly integrated with an organization’s compliance and operations is the only way to create an effective overall enterprise risk strategy. We will also discuss essential, practical tools for measuring, monitoring, and proactively managing a variety of ESG risks and provide ample materials for future reference.

There can be no question that the role of legal counsel is expanding into a proactive role in an organization’s broader enterprise governance, risk management, and compliance (GRC) strategy. The ever-increasing ESG initiatives impacting many aspects of business are evidenced, in part, by the number of ESG-related CLEs at the upcoming Business Law Section Hybrid Spring Meeting. The objective of all these ESG-related CLE programs, listed below, is to be sure business lawyers have the tools to assist clients in coordinated efforts to act with integrity in fulfilling legislative, regulatory, contractual, and even self-imposed obligations.

ESG in the Board Room: Counseling Directors on ESG, April 1, 4:00–5:00 p.m. ET, from the Federal Regulation of Securities, Corporate Social Responsibility Law, Corporate Governance, International Business Law and International Coordinating Committees

Work is nearing completion on proposed amendments to the Uniform Commercial Code (“UCC”) to address a limited set of transactions largely involving emerging technologies, such as virtual (non-fiat) currencies, distributed ledger technologies, and, to a limited extent, artificial intelligence. The principal amendments address so-called digital assets. The rules covering transfers of covered digital assets, including security interests in those assets, are carefully coordinated so that the transactions generate predictable and consistent results.

Background

Since 2019, a Committee appointed by the American Law Institute and the Uniform Law Commission, the sponsoring organizations of the UCC, has been considering and formulating amendments to the UCC to address emerging technological developments. The Committee has included and worked with both lawyers experienced in UCC matters and lawyers whose practices concentrate on digital assets. The work of the Committee has benefitted enormously from the contributions of American Bar Association advisors and more than 300 observers from academia, trade groups, government agencies, law firms, private technology companies, and foreign participants from multinational law reform organizations or who are active in technology-related law reform efforts in their respective countries.

The Committee presented its initial draft of the amendments to the Uniform Law Commission at the Commission’s annual meeting in July of 2021. The ALI Members Consultative Group (“MCG”) met and discussed the draft in October 2021. A revised draft was considered and approved by the American Law Institute Council in January of 2022. The MCG will meet again and consider the latest draft late in April. The Council of the American Law Institute approved the amendments at the Council’s meeting in January 2022. The Committee hopes to obtain approval of the members of the American Law Institute at the Institute’s Annual Meeting in May of 2022, and of the Uniform Law Commission at the Commission’s Annual Meeting in July of 2022. The amendments would then be offered for enactment by the states.

The following is a high-level summary of the current draft of the proposed amendments as they relate to certain digital assets.

Executive Summary

The proposed amendments respond to market concerns about the lack of definitive commercial law rules for transactions involving digital assets, especially relating to:

negotiability for virtual (non-fiat) currencies,

certain electronic payment rights,

secured lending against virtual (non-fiat) currencies, and

security interests in electronic (fiat) money, such as central bank digital currencies.

The proposed amendments address only state commercial law rules. They do not address the federal or state regulation or taxation of digital assets, regulation of money transmitters, or anti-money laundering laws. The amendments look to law outside of the UCC to answer many questions concerning digital assets.

The proposed amendments concern a class of digital assets—defined as “controllable electronic records” (“CERs”)—which would include certain virtual (non-fiat) currencies, non-fungible tokens, and digital assets in which specified payment rights are embedded. The amendments provide for a CER to be in effect negotiable, i.e., capable of being transferred in such a way as to cut off competing property claims (including security interests) to the CER (a “take-free” rule).

The proposed amendments also provide for a security interest in a CER to be perfected by “control” (or by filing a financing statement) and for a security interest perfected by “control” to have priority over a security interest in the CER perfected only by the filing of a financing statement (or another method other than “control”). There are also proposed amendments to address security interests in electronic money.

Definition of “Controllable Electronic Record”

A “controllable electronic record” is a record in electronic form that is susceptible to “control.” For a person to have “control” of a CER, the person must have:

the power to enjoy “substantially all the benefit” of the CER,

the exclusive power to prevent others from enjoying “substantially all the benefit” of the CER, and

the exclusive power to transfer control of the CER.

Moreover, the person must be able readily to identify itself to a third party as the person having these powers. Identification can be made by a cryptographic key or account number. The exclusivity requirement is satisfied even if there is a sharing of these powers through a “multi-sig” or similar arrangement or if changes occur automatically as part of the protocol built into the system in which the CER is recorded.

The amendments include the following language:

A virtual (non-fiat) currency would be an example of a CER. If a person owns an electronic “wallet” that contains a virtual currency, the person would have control of the virtual currency if (a) the person may benefit from the use of the virtual currency as a medium of exchange by spending the virtual currency or exchanging the virtual currency for another virtual currency, (b) the person has the exclusive power to prevent others from doing so, and (c) the person has the exclusive power to transfer control of the virtual currency to another person.

If an electronic record is not susceptible to control, it is outside the scope of the proposed amendments. In addition, the definition of a CER excludes certain digital assets that might otherwise be considered to fall within the definition of that term. These assets are excluded because commercial law rules already exist and generally work well for these assets. They include electronic chattel paper, electronic documents, investment property, transferable records under the federal E-SIGN law or the Uniform Electronic Transactions Act (“UETA”), deposit accounts, and, to some extent, electronic money (discussed below).

Nothing in the proposed amendments, for example, disturbs transacting parties’ current practices of using transferable records under E-SIGN. Nor do the proposed amendments affect transacting parties’ ability, in effect, to “opt-in” to Article 8 of the UCC by arranging for a digital asset to be held with a securities intermediary as a financial asset credited to a securities account. Electronic money is treated separately under the proposed amendments, as described below.

Rights of a Transferee of a Controllable Electronic Record

Proposed Article 12 governs certain transfers of CERs. If a CER is purchased (which consists of a voluntary transaction, including obtaining a security interest in the CER), the purchaser acquires all rights in the CER that the transferor had. In addition, if the purchaser is a “qualifying purchaser,” the purchaser benefits from the “take-free” rule, i.e., the purchaser acquires the CER free from competing property claims to the CER. A “qualifying purchaser” is a purchaser who obtains control of a CER for value, in good faith, and without notice of a property claim to the CER. As with negotiable instruments and investment property, the filing of a financing statement in and of itself is not notice of a property claim to the CER.

This is summarized in the amendments as follows:

Consider again the example of a person in control of a virtual (non-fiat) currency. If the person transfers control to another person, the transferee obtains whatever rights in the virtual currency that the transferor had. If the transferee is a “qualifying purchaser” of the virtual currency, the transferee also benefits from the “take-free” rule.

Tethering and Certain Payment Rights

With one important exception described in the following paragraph, what rights are embodied in the CER, and whether the “take-free” rule applies to those other rights (in addition to the CER itself) upon a transfer of the CER, are all determined by law outside of the proposed amendments. For example, the proposed amendments do not affect copyright law as it relates to someone in control of a non-fungible token “tethered” to intellectual property. Other law would determine the effect of that “tethering.” Similarly, if a CER purported to evidence an interest in real estate, whether the “take-free” rule applies to the interest in the real estate upon a transfer of control of the CER would be determined under other law, presumably the applicable real estate law.

There is one important exception: An “account” or “payment intangible,” as those terms are already defined in Article 9 of the UCC, embodied in a CER is a “controllable account” or “controllable payment intangible” if the account debtor (the person obligated on the account or payment intangible) has agreed to pay the person in control of the CER. If control of a CER with an embedded controllable account or controllable payment intangible is transferred, the controllable account or controllable payment intangible travels with the CER, and the transferee may benefit from the same “take-free” rule that applies to the CER. The effect is to create what is functionally an electronic instrument even though the payment rights would continue to be classified as a “controllable account” or “controllable payment intangible.” If the terms of the CER provide that the account debtor will not assert claims or defenses against the transferee of the CER (as and to the extent permitted by UCC § 9-403 and subject to consumer laws), then the effect is to create the substantial equivalent of an electronic negotiable instrument. These provisions respond to market concerns in the trade finance area that commercial law rules are currently insufficient for electronic promissory notes and electronic bills of exchange.

Consider a buyer of goods who delivers to the buyer’s seller a promissory note in payment for the goods. If the promissory note is in a writing, it might, if certain conditions are met, qualify as a negotiable instrument under Article 3 of the UCC, and potentially a holder of the promissory note could be a holder in due course of the negotiable instrument. But, if the promissory note is in electronic form and even if those conditions are met, Article 3 does not apply because the promissory note is not in a writing. Absent the promissory note qualifying as a “transferable record” under UETA, the rights of a transferee of the promissory note would be governed under normal contract rules and some rules under UCC Article 9. Under the proposed amendments, though, the promissory note (in electronic form) could be a CER, If the promissory note were a CER, the “take-free” rule would apply to a qualifying purchaser of the promissory note. If the buyer also agreed not to assert claims or defenses against a transferee of the promissory note, the electronic promissory note would, subject to applicable consumer laws, have negotiability characteristics similar to those of a negotiable instrument under Article 3.

Secured Lending

The provisions applicable to purchasers of CERs are carefully coordinated with corresponding changes to lending secured by security interests in CERs under Article 9 and are designed to preserve the availability of existing transaction patterns. Under the proposed amendments, there would be no need to change collateral descriptions in security agreements or collateral indications on financing statements. A CER is a “general intangible,” a controllable account is an “account,” and a controllable payment intangible is a “payment intangible,” as those terms are already defined in Article 9 of the UCC. The normal rules for attachment would continue to apply, and a security interest in a CER, a controllable account, or a controllable payment intangible could still be perfected by the filing of a financing statement.

However, under the proposed amendments, a security interest in a CER, a controllable account, or a controllable payment intangible could also be perfected by the secured party obtaining “control” of the CER. A security interest in a CER, a controllable account, or a controllable payment intangible perfected by “control” would have priority over a security interest in the CER, controllable account, or controllable payment intangible perfected only by filing (or by another method other than control). Control would be defined as described above.

Another example may be helpful. SP-1 lends to Debtor, obtains a security interest in Debtor’s accounts, payment intangibles, and other general intangibles, and perfects the security interest by the filing of a financing statement. SP-2 later lends to Debtor, obtains a security interest in a CER in which is embodied what is functionally an electronic promissory note payable to the person in control is embodied, and files a financing statement to perfect its security interest. SP-1’s security interest has priority under the first to file or perfect priority rule of Article 9. If SP-2 obtains control of the CER, SP-2’s security interest in the electronic promissory note is senior to SP-1’s security interest in the electronic promissory note.

Account Debtor Discharge

Similar to current UCC Article 9 provisions for accounts and payment intangibles generally, an account debtor (the obligor on an account or payment intangible) receives a discharge by paying the person formerly in control until the account debtor receives a notification signed in writing or electronically by the debtor or its secured party that the secured party has a security interest in the controllable account or controllable payment intangible and a payment instruction (often referred to a “deflection notification”) to pay the secured party as the person now in control. Following receipt of the deflection notification, the account debtor may obtain a discharge only by paying the secured party and may not obtain a discharge by paying the debtor.

Also, similar to current UCC Article 9, the debtor may ask for reasonable proof that the secured party is the person in control before paying the secured party. However, unlike under current Article 9, for a controllable account or controllable payment intangible the method of providing that reasonable proof must have been agreed to by the account debtor, presumably as part of the CER when it was created. Absent an agreed method of providing reasonable proof, the deflection notification is not effective, and the account debtor may obtain a discharge by continuing to pay the debtor.

As a practical matter, few account debtors question a deflection notification or ask for reasonable proof. However, if an account debtor does ask for reasonable proof, the relevant parties have the flexibility to develop for market acceptance methods for providing the reasonable proof.

Electronic Money

The current definition of “money” in the UCC is sufficient to include a virtual (fiat) currency authorized or adopted by a government, whether token-based or deposit account-based. The definition of “money” would be revised to exclude a medium of exchange in an electronic record (such as Bitcoin) that existed and operated as a medium of exchange before it was authorized or adopted as a medium of exchange by a government. However, a medium of exchange in an electronic record so excluded might still qualify as a CER.

Under current UCC Article 9, a security interest in money can perfected only by possession. However, electronic money is not susceptible to possession. The proposed amendments provide that, if electronic money is credited to a deposit account (even one at a central bank), the normal deposit account perfection rules apply. Electronic money also would exclude money that cannot be subject to “control,” similar to control for a CER. If the electronic money is not credited to a deposit account, a security interest may be perfected by “control”. UCC § 9-332 would be amended generally to provide for a transferee of money, whether tangible or electronic, to take free of a security interest in the money. Otherwise, any “take-free” rule would be determined by the law governing the electronic money.

Choice of Law

The proposed amendments include substantially identical choice-of-law rules for the take-free rules for transferees of CERs and the perfection by control and priority of a security interest in a CER, controllable account, or controllable payment intangible perfected by control. Having the same rules promotes consistent results and predictability.

The amendments generally follow the choice-of-law approach taken in UCC Articles 8 and 9 for financial assets credited to a securities account at a securities intermediary. The application of take-free rules in connection with transfers of CERs and the perfection, effect of perfection or non-perfection, and priority of a security interest in a CER perfected by control would be determined by the law where the CER is deemed to be “located” – i.e., the CER’s jurisdiction. For a CER that expressly provides its jurisdiction, perfection, other than by the filing of a financing statement, and priority are governed by the law of that jurisdiction. Otherwise the CER’s jurisdiction would be the jurisdiction whose law governs the system in which the CER is recorded. If no express provision is made in the CER or the system, the CER would be located in Washington, D.C. If Washington D.C. has not enacted the amendments, the substantive law rules of the Official Text of the amendments would apply. However, in the case of perfection of a security interest by the filing of a financing statement, the normal debtor location rules would apply.

Transition Rules

Transition rules are being developed. These rules will be designed to protect the expectations to parties to pre-amendments effective date transactions and to provide for sufficient time for parties to plan transactions post-amendments effective date.

The transition rules will likely not contain a uniform amendments effective date. for the amendments because some states appear ready to enact the amendments as early as possible. However, a uniform adjustment date is being considered. The adjustment date would give transacting parties a grace period to preserve priorities established on the effective date if the amendments would otherwise affect those priorities.

Other Proposed Amendments

The proposed amendments also contain some provisions relating to chattel paper, “bundled” transactions (involving as a single transaction for the sale or lease of goods, the licensing of software or information, and the provision of services), negotiable instruments, payment systems, letters of credit, documents of title, the meaning of “conspicuous,” and some miscellaneous amendments to the UCC. The amendments unrelated to CERs and electronic money are beyond the scope of this summary.

This article is adapted from a Showcase CLE program titled “Social Justice Intersecting with Sports: Is It Right?” that took place at the ABA Business Law Section’s Hybrid Spring Meeting on Friday, April 1, 2022. To learn more about this topic, view the program as on-demand CLE, free for Section members.

“I have a dream that one day this nation will rise up and live out the true meaning of its creed: “We hold these truths to be self-evident, that all men are created equal.”

“I have a dream that one day on the red hills of Georgia, the sons of former slaves and the sons of former slave owners will be able to sit down together at the table of brotherhood….”

Dr. Martin Luther King, Jr., August 28, 1963

What is social justice? What is its relationship to sports? How do they intersect with the law? Starting with the first question, the term is defined by the John Lewis Institute for Social Justice as: “Social justice is a communal effort dedicated to creating and sustaining a fair and equal society in which each person and all groups are valued and affirmed. It encompasses efforts to end systemic violence and racism and all systems that devalue the dignity and humanity of any person.” While the focus here is on race, social justice can be applied more broadly to include, among other things, gender, ethnicity, religion and sexual orientation.

This article will describe how social justice and sports overlap. But a valid question remains—how does all of this relate to the law? First, social justice inherently relates to fundamental rights of athletes—including the constitutional rights to free speech and to vote. Perhaps the most recent, bold expression of social justice issues in sports litigation is Brian Flores’s lawsuit alleging rampant discrimination in National Football League (NFL) hiring, but many other legal issues come into play. For example, Major League Baseball (MLB) abruptly relocating its All-Star Game in 2021 in response to controversial Georgia legislation making voting more difficult impacted a web of contractual relationships among parties supporting that event. Potentially the most transformative change ever in college athletics is the advent of athletes’ ability to monetize their name, image, and likeness (NIL). This was enabled by a seminal case before the US Supreme Court in 2021 involving antitrust law, NCAA v. Alston. What’s the connection with social justice there? The perception of many and particularly people of color has been the multi-billion-dollar business of major college athletics is a plantation-like model. The belief was the system is leveraged on the backs of unpaid labor, largely that of Black students, who generate funding for less lucrative sports with mostly White participants. And, as reflected in the O’Bannon v. NCAA case, NILs constitute intellectual property.

Over the past half century, the US Supreme Court on other occasions has spoken on subjects relating to or impacting issues of social justice including its decisions in Tinkerv. Des Moines Inde. Cmty. Sch. Dist. (First Amendment does not prevent schools from student speech restrictions) and Floodv. Kuhn (rejecting a player challenge to the MLB reserve clause, which prevented freedom of movement). Further, many social justice issues can be interwoven with collective bargaining agreements (CBAs), league/team rules and other labor-related legal issues that arise in the sports world.

The intersection of social justice with sports has been prominent in the U.S. for over a century. As the two began to overlap, it took time but eventually legal challenges emerged. The MLB “color barrier” was first imposed in 1887. At the 1936 Olympic Games in Berlin, capital of Hitler’s Nazi Germany, several Jewish US athletes opted out in protest. Meanwhile, Black athlete Jesse Owens decided to defy Hitler’s vision of an Aryan nation by competing—quite successfully. After World War II, systematic US racism remained. Yet in 1947, finally a Black baseball player, Jackie Robinson, was promoted to MLB. Robinson’s courage and resilience are the subject of books and films but often overlooked is his civil rights commitment, including his organizing of marches with Dr. King. After all, even after his groundbreaking career was over Black people in many parts of this country continued to be denied basic rights under the Constitution including the right to vote.

In the 1960s, active Black athletes began to speak and engage in acts of protest. Muhammad Ali took center stage, and at the peak of his career became a conscientious objector after being drafted. Ultimately the US Supreme Court overturned Ali’s conviction for draft evasion, but he lost his title and economic livelihood for years. Other courageous Black athletes supported him, including Bill Russell, Lew Alcindor (now Kareem Abdul-Jabbar) and Jim Brown. More events spotlighting social justice in sports arose later in the decade. On the international stage, Americans Tommie Smith and John Carlo protested during the Olympics medal ceremony in 1968 in Mexico City, despite the consequences they would face from the International Olympic Committee (IOC). And yet another prominent professional athlete would bring a challenge all the way to the highest court in the land: MLB player Curt Flood challenged MLB on antitrust grounds, likening the reserve clause in baseball contracts to “being a slave 100 years ago.” Ali and then Flood were legal trailblazers—challenging the US Government and an entire sport in court.

Many overlook the periodic social justice consciousness-raising that took place in sports in the succeeding decades, perhaps partly because it was overshadowed by these earlier athletes but also because the economics of sports changed radically. Players gained free agency gradually, and their earning power grew tremendously. Owners also grew wealthier through valuable revenue sources, including richer broadcast deals. Issues regarding compensation centered around CBAs, lockouts and strikes, with both sides represented by high-priced lawyers, and labor law disputes overshadowed cries for equity and fairness. This is not to ignore the Syracuse 8, the Battle of the Sexes and Title IX, Georgetown coach John Thompson, Arthur Ashe, NBA courtside protests and Proposition 48—much of which went no farther than protests and powerful symbolism but some spilled into courts of law.

However, in the past decade, athletes’ contribution to consciousness-raising regarding race reached a pinnacle. Catalysts were the unjustifiable killings of Black people, first teenager Trayvon Martin and then (among others) Michael Brown, Eric Garner and Freddie Gray, in first instance by a neighbor who avoided conviction and the others by police using unnecessary force. These events put out into the open very legitimate questions about the US legal system and race. Player protests took various forms, including LeBron James and teammates donning hoodies in honor of Martin, NFL players making “don’t shoot” on-field poses, boycotts by collegiate football players and WNBA players wearing “Black Lives Matter” t-shirts. Activism by athletes was spotlighting concerns about law enforcement, prosecutors and courts not giving people of color equal justice.

A pivotal moment was the 2016 NFL season, when Colin Kaepernick began kneeling during the national anthem in protest over US oppression of Black people. Teammates and others followed his lead by kneeling or staying inside the locker room during the anthem. These calls for social justice were well publicized and generated controversy, partly stoked by the former President. Conventional notions of league and team “rules” and collectively bargained employer-employee relationships were suddenly questioned. Kaepernick would soon be unable to find a job in the NFL and filed a grievance against all 32 teams (a procedure required under the NFL’s CBA). He alleged that the teams colluded to keep him out of the league in retaliation for his activism in raising awareness of social justice issues. The matter was settled confidentially in 2019. The result after a tumultuous period appeared to be greater acceptance and awareness of racial issues, and even an agreement between players and the NFL for funding certain initiatives.

Attention to social justice in sports reached a crescendo in 2020 with the tragic murder of George Floyd. Black Lives Matter became an important, historic movement as thousands of protests took place across the US and more White people joined in. There was unprecedented player action across all sports, and partly by leagues and teams themselves. Some action had legal implications, but all stemmed from seemingly systemic issues with unequal treatment in our legal system. The Milwaukee Bucks players elected not to play a game in protest, and the League rescheduled games. In soccer (with its own historical racial issues) domestically and overseas players engaged in acts of solidarity. Even MLB, with its checkered racial history, moved its All-Star Game from Atlanta in light of Georgia’s controversial voting legislation; the untangling of a maze of event-related contracts and avoiding or minimizing the legal consequences followed. Most recently, former NFL coach Brian Flores commenced a class action challenge against the league and three teams alleging racial discrimination. Such a legal challenge by a young Black coach was unimaginable only a few years ago.

Sports and social justice are intersecting more than ever. Will that continue? Yes. The real question is how impactful it will be in causing change and what role the law will play. Is the Flores action a sign the legal issues underlying social justice more frequently will come to the fore in courts of law? We’ll see.

This article is related to a Showcase CLE program at the ABA Business Law Section’s 2022 Hybrid Spring Meeting. To learn more about this topic, view the program as on-demand CLE, free for Section members.

Although the rules of professional conduct differ in each state, all states in the United States have enacted some form of the Model Rules of Professional Conduct adopted by the American Bar Association. Such rules apply not only to lawyers in private practice but also to in-house lawyers. Further, the application of such rules to how lawyers in private practice interact with each other at a law firm also applies to in-house lawyers, as such rules generally define “law firm” (or “firm”) to include “the legal department of a corporation or other organization.” See, for example, Rule 1.0(c) of the ABA’s Model Rules of Professional Conduct (“Model Rules”). Also see Comment [3] to Model Rule 1.0: “With respect to the law department of an organization, including the government, there is ordinarily no question that the members of the department constitute a firm within the meaning of the Rules of Professional Conduct.”

While it is clear that the Model Rules and the rules of professional conduct in most states apply to in-house attorneys, how those rules actually apply is not always clear. Attorneys are generally familiar with the application of the ethical rules to their practices when they work in private practice. In fact, many of the rules contemplate the attorney as an outside legal adviser with multiple clients, and not an employee of a single client. Some of the rules are obvious in their application to in-house attorneys (such as the duty of confidentiality contained in Model Rule 1.6). Certain other rules don’t really apply to the in-house attorney as a practical matter (such as the obligation to maintain trust accounts pursuant to Model Rule 1.15, and the limitations on advertising and solicitation contained in Model Rules 7.1, 7.2, and 7.3).

But some of the rules may have a different or surprising application to many in-house attorneys, due in part to the nature of the employer-employee relationship where the employer is the client (and perhaps the only client) of the in-house attorney, and also due to the mixed role of some in-house attorneys who serve as both a lawyer for the organization and also as a businessperson or principal of the organization. Such rules include the following:

Model Rule 1.7, which precludes an attorney from representing two or more clients if the representation of one client is directly adverse to another client, or if there is a substantial risk that the representation of a client will be materially limited by the attorney’s responsibilities to another client (unless the attorney secures the informed consent, confirmed in writing, from each affected client). Such a conflict situation might arise when the attorney is representing both its employer organization or business entity and one of its officers, directors, or shareholders. Conflicts of interest may also exist among entities within the corporate family and among affiliated entities.

Model Rule 1.9, which precludes an attorney from working on a matter on behalf of a client if that client’s interests are materially adverse to the interests of a former client of the attorney and the attorney represented that former client in the same or a substantially related matter (unless the attorney secures the informed consent, confirmed in writing, of the former client). Such a conflict situation might arise when an in-house attorney finds themselves across the table from a former client (from when the in-house attorney worked at a law firm) or a former employer (if the in-house attorney worked in-house at another company).

Model Rule 1.10, which provides that the conflict of interest of one attorney in a law firm (defined in the Model Rules to include a legal department) is imputed to all other attorneys in the firm, such that none of them may represent a client when any one of them practicing alone would be prohibited from doing so. This is particularly troublesome in a legal department, where the conflict of one in-house attorney may be imputed to all of the other in-house attorneys in the legal department, thereby precluding the in-house team from working on a particular matter on behalf of their employer client.

Model Rule 1.13, which makes clear that an attorney employed or retained by an organization represents the organization acting through its duly authorized constituents (e.g., officers, directors, etc.), although such rule also permits the attorney to represent any such constituent in addition to the organization. However, if the organization’s consent to such a dual representation is required by Model Rule 1.7, the consent must be provided by an appropriate official of the organization other than the individual constituent who is also being represented.

In addition, although the attorney-client privilege generally applies to communications between clients and their attorneys, where an in-house attorney is acting in their capacity as a businessperson or principal of the organization (and not as an attorney), such communications may not be privileged. This same risk may apply to outside attorneys as well if they are also interacting with their entity clients in a non-legal capacity, such as by serving as a member of the entity’s board of directors.

As a result, it is important for both in-house and outside counsel to consider and address the following requirements:

properly identifying who is, and who is not, the client with respect to an entity client;

dealing with conflict of interest in an entity client context, especially with the respect to dealing with entity constituents, the inadvertent creation of attorney-client relationships, possible joint representations, and affiliated entities and joint ventures (Model Rules 1.7, 1.9, 1.10, and 1.13);

addressing Model Rule 1.6 confidentiality, the attorney-client privilege, and the work product doctrine in the entity client context; and

gaining a better understanding of the application of other Model Rules to the attorney (in-house or outside counsel) representing an entity, including Rule 1.8 (business transactions and other relations with a client); Rule 5.5 (the unauthorized practice of law and multi-jurisdictional practice, in the cross-border context); and Rule 1.13(b) and (c) (reporting up and out when representing an entity client).

The increased use of digitalized healthcare technologies amid the global pandemic continues to pique the interest of many institutional healthcare organizations and professionals, emphasizing its utility as an influential healthcare delivery segment; however, telehealth’s accelerated growth and fast-tracked implementation raise many concerns, including physicians’ licensure compliance and fraudulent behavior by healthcare providers.[1] Although the pandemic’s exit is not yet foreseeable, governments are now better equipped to manage its repercussions without imposing another set of stringent lockdowns, which begs the question: what is the future of this potentially robust healthcare sector? Many proponents, such as the American Medical Association (“AMA”), have advocated for Congress to facilitate a smooth transition so patients can continue to address their healthcare needs via telehealth processes.[2]

Prior to the global pandemic, state and federal regulations partially inhibited patients’ and physicians’ ability to convene by utilizing digitalized healthcare systems. Regulations dictated that physicians adhere to state licensure requirements when providing patient care. Moreover, Section 1834(m) of the Social Security Act restricts the usage of telehealth services unless such care is provided at an approved site—a provision that has traditionally been used in rural communities.[3] The Public Health Emergency (“PHE”) declaration partially suspended these strict regulatory requirements. Further, the passage of the CARES Act authorized the Centers of Medicare and Medicaid Services (“CMS”) to waive geographic barriers for the duration of the PHE.[4] As a result, many patients are able to receive medical services from the comfort of their residences instead of strictly at an approved site.[5] As CMS waived many of these geographic barriers in March of 2020, Medicare, Medicaid, private insurance companies, and state governments enabled reimbursements for telehealth services at the same rate as physical visits.[6] Additionally, during the peak of the pandemic, 41 states temporarily suspended licensure requirements, authorizing out-of-state physicians to administer services across state lines by utilizing telehealth infrastructure.

On January 14, 2022, the U.S. Department of Health & Human Services (“HHS”) extended the PHE until April 16, 2022.[7] Coinciding with the continuance of the PHE declaration is the issuance of Section 1135 Waivers of the Social Security Act. Section 1135 grants the HHS the authority to modify or suspend federal requirements for the duration of a PHE. Among the significant modifications issued by the HHS and CMS are state-specific Medicaid waivers, which allow providers to administer care by utilizing telehealth across state lines.[8] Moreover, Medicare telehealth coverage and federal oversight reporting requirements continue to be modified to ensure healthcare accessibility during the PHE.[9] These waivers and similar modifications will cease when the PHE expires; thus, uncertainty looms regarding the future of telehealth and its accessibility. Absent Congressional action, the flexibilities of Medicare reimbursements and temporary suspension of geographic restrictions will cease at the expiration of the PHE.

Some federal developments are under consideration to ensure that access to these services is not inhibited after the PHE expires. For example, legislation has been introduced in the Senate, including the Creating Opportunities Now for Necessary and Effective Care Technologies for Health Act of 2021 (“CONNECT Act”). This act would permanently remove the geographic restrictions under Medicare, allowing patients to access mental telehealth services from their residence rather than an approved location; additionally, the CONNECT Act would also remove the geographic restrictions for rural health clinics and federally qualified health centers.[10] Similarly, H.R. 2903 (a companion bill to the CONNECT Act) amends the Social Security Act to expand access and reimbursement of telehealth services.[11] Although a step in the right direction, these bills have experienced little momentum in their respective houses. As the new PHE declaration will soon expire, and as COVID immunity builds, maybe lawmakers will prioritize this bipartisan and bicameral legislation.

With respect to physicians’ licensure requirements, uniformity is nearly impossible to ensure. As referenced prior, licensing requirements are state-specific. Therefore, state legislatures must determine if they wish to continue, or make permanent, flexible licensure procedures. State legislatures are seeking to make their temporary waiver exemptions permanent, granting out-of-state practitioners the ability to deliver telehealth services across state lines if they comply with local state practices and requirements. Specifically, many states have entered interstate compacts, which allow certain providers to practice across state lines if they remain in good standing with their home jurisdiction.