The Barton doctrine, first articulated by the Supreme Court in 1881, requires a party to obtain leave from the appointing court (frequently a bankruptcy court) before suing a court-appointed officer in another court for actions taken in their official capacity.[1] The purpose of the doctrine is to prevent the suing party from obtaining an advantage over the other claimants while the court-appointed officer is in control of the estate.[2]

Under the doctrine, failure to seek permission from the appointing court deprives the second court of subject matter jurisdiction. Thus, any proceeding commenced without leave must be dismissed; otherwise, it would constitute a “usurpation of the powers and duties” reserved to the appointing court.[3] The Barton doctrine does not prevent suits against court‑appointed officers but rather requires that permission be granted by the appointing court before a suit can proceed elsewhere.

Though originally applied to receivers, nearly all federal circuits—except the D.C. Circuit—have held that the Barton doctrine applies in bankruptcy proceedings.[4] While a bankruptcy case is ongoing, a suit filed against a bankruptcy trustee or similar officer in another court without prior permission must be dismissed, although the same suit can be brought directly in the bankruptcy court itself.[5] There is a circuit split, however, over whether the Barton doctrine applies after a bankruptcy case has closed.

I. Barton v. Barbour

In Barton v. Barbour, the plaintiff, Ms. Barton, was a passenger who was injured in a railway accident. Barbour had previously been appointed as receiver for the railroad company and was operating the railroad for the benefit of creditors at the time of the accident.[6] Ms. Barton sued Mr. Barbour in the District of Columbia, seeking $5,000 for her injuries. He responded that he could not be sued there because the plaintiff had not obtained leave from the Virginia state court that had appointed him to serve as the receiver. The District of Columbia court agreed and dismissed the case. The plaintiff appealed to the United States Supreme Court, which affirmed, creating what is now known as the Barton doctrine.

The Supreme Court stated that “[i]t is a general rule that before suit is brought against a receiver[,] leave of the court by which he was appointed must be obtained.”[7] The Court stated that any suit against a receiver necessarily involves an attempt to obtain receivership property. In fact, the Court suggested that the main reason a person would sue a receiver is to obtain a position ahead of other creditors. The Court also reasoned that, to enforce the judgment, the plaintiff would need to levy against property already in the hands of another court—the one that had appointed the receiver. The Court stated that it could not allow this outcome, as it would undermine the power of the appointing court. The Court concluded that the court administering the receivership should act as a gatekeeper, determining whether a claim has enough merit to proceed, whether in front of it or in another venue. This prevents estate assets from being “wasted in the costs of unnecessary litigation.”[8]

The Court did note an exception to its rule, though: “[I]f one claims that the assignee has wrongfully taken possession of his property as property of the bankrupt, he is entitled to sue him in his private capacity as a wrong-doer in an action at law for its recovery.”[9] Comparing the receiver to “an assignee in bankruptcy,” the Court observed that if “by mistake or wrongfully, the receiver takes possession of property belonging to another, such person may bring suit therefor against him personally as a matter of right; for in such case the receiver would be acting ultra vires.”[10] But when the receiver is acting within the scope of his or her authority, then the matter must be handled with the blessing of the appointing court.

II. 28 U.S.C § 959

Congress enacted legislation in the wake of Barton to address the concern that operating trustees and receivers were improperly being shielded from legitimate actions while running a business. This legislation has been amended many times but is now codified at 28 U.S.C. § 959. That section provides:

(a) Trustees, receivers or managers of any property, including debtors in possession, may be sued, without leave of the court appointing them, with respect to any of their acts or transactions in carrying on business connected with such property. Such actions shall be subject to the general equity power of such court so far as the same may be necessary to the ends of justice, but this shall not deprive a litigant of his right to trial by jury.

(b) Except as provided in section 1166 of title 11, a trustee, receiver or manager appointed in any cause pending in any court of the United States, including a debtor in possession, shall manage and operate the property in his possession as such trustee, receiver or manager according to the requirements of the valid laws of the State in which such property is situated, in the same manner that the owner or possessor thereof would be bound to do if in possession thereof.

In addition to requiring that trustees, receivers, and debtors in possession comply with nonbankruptcy law, the statute prohibits a court from using its equity jurisdiction to deprive a person of a right to a jury trial.

III. The Barton Doctrine Protects Court-Appointed Fiduciaries in Bankruptcy

As noted, substantially all circuit courts of appeal have held that the Barton doctrine applies in bankruptcy. The Barton doctrine protects not just trustees but all officers appointed by the bankruptcy court when they act in their official capacity.[11] This includes receivers, attorneys for trustees, and officers acting under the trustee/receiver’s direction or serving in a functionally equivalent role.[12] The Barton doctrine has in recent years been expanded to cover trustees appointed pursuant to a plan of reorganization and other court-appointed roles.[13]

The American Bankruptcy Institute Commission to Study the Reform of Chapter 11 in 2014 proposed an amendment to the Bankruptcy Code that expressly adopts and expands the Barton doctrine. The proposed amendment would expand the scope of the Barton doctrine to the following persons in Chapter 11 reorganization cases: Chapter 11 trustees, estate neutrals/examiners, and statutory committees and their members, as well as professionals retained by each of the foregoing. According to the Commission’s Final Report, the proposed expansion reflects the Commissioners’ beliefs that it “would (i) allow any trustee, estate neutral, and statutory committee and its members to perform their fiduciary duties with confidence and focus, and (ii) eliminate unnecessary litigation concerning the application of the Barton doctrine and whether the court in which a litigant files the action has subject matter jurisdiction over the dispute.”[14]

IV. A Circuit Split Exists Regarding Whether the Barton Doctrine Remains Applicable Once a Bankruptcy Case Is Closed

The question of whether the Barton doctrine continues to apply after a bankruptcy case has closed has resulted in a 5–1 circuit split. Circuits holding that the Barton doctrine continues to apply after a case has closed reason that it is necessary to protect court-appointed officers. The bankruptcy court that approves a professional’s employment can hold them accountable, but the professional can be confident that if the bankruptcy court blesses what they have done, they do not have to worry about nettlesome litigation elsewhere. In this way, application of the Barton doctrine increases the likelihood that parties will be interested and willing to serve as estate fiduciaries. As one court noted, “the court that appointed the trustee has a strong interest in protecting him from unjustified personal liability for acts taken within the scope of his official duties.”[15]

Despite the policy merits of such an approach, the Eleventh Circuit has held that extension of the doctrine after a case is closed is unwarranted because bankruptcy courts lack in rem jurisdiction once a case is closed. Separately, the Eleventh Circuit has suggested that judicial immunity provides fairly strong protection for court-appointed officers.

A. Circuits That Support the Barton Doctrine’s Extension

Seventh Circuit: In In re Linton,[16] the Seventh Circuit held that the Barton doctrine continues to apply after a bankruptcy case is closed. In that case, a Chapter 7 trustee commenced a fraudulent transfer action against the debtor, her husband, and their sons. The trustee later dismissed the action, and the bankruptcy proceeding was closed. Eleven months later, the debtor and her husband sought leave from the bankruptcy court to file a malicious prosecution suit against the trustee in state court, arguing that the adversary proceeding was meritless. They had already filed the suit without waiting for the court’s permission, and it remained dormant pending the court’s decision. The bankruptcy court denied their motion, and the district court affirmed this decision.

The Seventh Circuit held that the Barton doctrine continued to apply notwithstanding the fact that the bankruptcy case had closed. Acknowledging that Barton was a bankruptcy case, not a receivership case, the Seventh Circuit stated:

Just like an equity receiver, a trustee in bankruptcy is working in effect for the court that appointed or approved him, administering property that has come under the court’s control by virtue of the Bankruptcy Code. If he is burdened with having to defend against suits by litigants disappointed by his actions on the court’s behalf, his work for the court will be impeded.[17]

The court stated that the trustee’s burden of defending against suits by litigants is most concerning while the bankruptcy proceeding is ongoing. “The threat of his being distracted or intimidated is then very great.”[18]

Nevertheless, the court stated, the doctrine should be continued after the bankruptcy “had been wound up.”[19] Without the doctrine, “trusteeship will become a more irksome duty,” and it will be more difficult for courts to appoint competent trustees.[20] The court continued that the expense of bankruptcy administration—already a source of considerable concern—will become even more expensive because trustees will need to pay higher malpractice premiums.[21] Moreover, the court reasoned, “requiring that leave to sue be sought enables bankruptcy judges to monitor the work of the trustees more effectively. It does this by compelling suits growing out of that work to be as it were prefiled before the bankruptcy judge that made the appointment; this helps the judge decide whether to approve this trustee in a subsequent case.”[22]

Finally, the court expressed concern for the integrity of bankruptcy jurisdiction absent extension of the doctrine:

If debtors, creditors, defendants in adversary proceedings, and other parties to a bankruptcy proceeding could sue the trustee in state court for damages arising out of the conduct of the proceeding, that court would have the practical power to turn bankruptcy losers into bankruptcy winners, and vice versa. A creditor who had gotten nothing in the bankruptcy proceeding might sue the trustee for negligence in failing to maximize the assets available to creditors, or to the particular creditor. A debtor who had failed to obtain a discharge might through a suit against the trustee obtain the funds necessary to pay the debt that had not been discharged.[23]

First Circuit: Similarly, in Muratore v. Darr,[24] the owner of a corporate debtor sued the Chapter 11 trustee in the district court, asserting claims for alleged misfeasance or malfeasance, abuse of process, negligence and violations of RICO while administering the bankruptcy estate. Specifically, the owner claimed that the trustee had failed to pay taxes, improperly sold properties, and allowed the purchase of property with illegal funds, among other allegations. The district court granted the trustee’s motion to dismiss for lack of subject matter jurisdiction based on the Barton doctrine because such suit was brought without the prior permission of the bankruptcy court. The owner appealed.

The First Circuit affirmed the district court’s dismissal, concluding that the Barton doctrine did apply and that the owner’s claims did not fall under the exception provided by 28 U.S.C. § 959(a), which allows trustees to be sued without leave for acts in carrying on business connected with the estate. The court found that the owner’s allegations pertained to the trustee’s administrative duties as a trustee rather than acts in furtherance of the debtor’s business. The court held that merely taking actions to preserve the estate—holding, collecting, liquidating or maintaining property—did not constitute “carrying on business.”[25] Rather, the statute is intended to permit redress for torts committed while operating a business.

The court specifically rejected the owner’s argument that the Barton doctrine should not apply because the bankruptcy case was closed, noting that the doctrine serves purposes beyond protecting estate assets, such as ensuring competent trustees and effective monitoring by bankruptcy judges.[26]

Ninth Circuit: In In re Crown Vantage, Inc.,[27] the Ninth Circuit held that the Barton doctrine applied notwithstanding the fact that a plan had been confirmed and therefore a bankruptcy estate no longer existed. The court required plaintiffs pursuing claims against a post-confirmation liquidating trustee to obtain leave from the bankruptcy court before filing suit in Delaware.

The court observed that if leave of the bankruptcy court were not first obtained, then the other forum lacked subject matter jurisdiction over the suit. The court noted that “[t]he Barton doctrine applies in bankruptcy, because ‘[t]he trustee in bankruptcy is a statutory successor to the equity receiver,’ and ‘[j]ust like the equity receiver, a trustee in bankruptcy is working in effect for the court that appointed or approved him, administering property that has come under the court’s control by virtue of the Bankruptcy Code.’”[28]

The court explained:

Indeed, the policies underlying the Barton doctrine apply with greater force to bankruptcy proceedings than to other proceedings involving receivers. The filing of a bankruptcy petition creates a bankruptcy estate, consisting of all of the debtor’s legal or equitable interests in property “wherever located and by whomever held.” 11 U.S.C. § 541(a). Thus, “[t]he district court in which the bankruptcy case is commenced obtains exclusive in rem jurisdiction over all of the property in the estate.” The court’s exercise of in rem bankruptcy jurisdiction “essentially creates a fiction that the property—regardless of actual location—is legally located within the jurisdictional boundaries of the district in which the court sits.” Thus, the jurisdiction of the bankruptcy court exceeds that of any other court-appointed receiver. The requirement of uniform application of bankruptcy law dictates that all legal proceedings that affect the administration of the bankruptcy estate be brought either in bankruptcy court or with leave of the bankruptcy court.[29]

The First Circuit held that the bankruptcy court’s in rem jurisdiction continues post-confirmation.[30] The court agreed “with the analysis of [its] sister circuits that ‘the doctrine serves additional purposes even after the bankruptcy case has been closed and the assets are no longer in the trustee’s hands.’”[31] If there were any objections to anything regarding the estate, the court stated, the objections should have been registered before confirmation. If a party fails to timely object, the party cannot later complain about a specific provision, even if the provision is inconsistent with the Bankruptcy Code. To raise identical issues in a second court “is an impermissible collateral attack.”[32]

Tenth Circuit: In Satterfield v. Malloy,[33] the debtor brought an action against the Chapter 7 trustee of his bankruptcy estate based on the trustee’s allegedly wrongful actions in his capacity as trustee. The debtor argued that the trustee’s actions were ultra vires, meaning beyond his legal power or authority, and thus not protected by the Barton doctrine. The debtor also contended that his action was authorized by 28 U.S.C. § 959, which allows trustees to be sued without leave of the appointing court for acts or transactions in carrying on business connected with the estate. Finally, the debtor argued that the Barton doctrine was inapplicable because his bankruptcy proceedings had concluded.

The court rejected all of these arguments. Regarding the debtor’s last argument related to applicability of the Barton doctrine after the case was closed, the Tenth Circuit stated: “Consistent with the holdings of other circuits, we reject this proposition. . . . [T]he Barton doctrine continues to serve important purposes even after a bankruptcy is complete.”[34] The court continued:

The Barton doctrine exists to ensure other courts do not intervene in the bankruptcy court’s administration of an estate without permission. A holding that [the trustee] acted ultra vires simply because he allegedly discharged his duties as trustee with improper motives would severely undermine this important judicial goal. We conclude that [the trustee’s] actions fell within the scope of his court-appointed authority as trustee because each of the alleged actions was related to his trusteeship duties. Accordingly, [the debtor] was required to obtain leave of the bankruptcy court before filing suit in the district court.[35]

Fifth Circuit: In In re Foster,[36] the Chapter 7 debtor listed three properties as assets in her bankruptcy case, but her husband claimed these properties were his separate property. The trustee initiated a case against the debtor’s husband to determine if the properties were part of the bankruptcy estate and intervened in the divorce proceedings to protect the estate’s interest. Ultimately, the bankruptcy court determined that the properties were part of the bankruptcy estate and authorized their sale by the trustee. Thereafter, the bankruptcy case was closed.

Almost ten months later, the debtor filed a motion to reopen the bankruptcy case to sue the trustee and vacate the judgment for lack of subject matter jurisdiction, which was denied. She then filed a complaint in Texas state court against the trustee, the trustee’s lawyers, and others asserting that they acted in an ultra vires manner, without obtaining permission from the bankruptcy court. The trustee moved to reopen the bankruptcy case to remove the action, dismiss the complaint, and impose sanctions. The bankruptcy court granted that motion and ultimately dismissed the complaint. The debtor appealed the bankruptcy court’s decisions, but the district court affirmed.

The Fifth Circuit held that the bankruptcy court properly applied the Barton doctrine. Acknowledging that the Barton doctrine does not apply to acts outside the scope of the trustee’s official duties, the court noted that such exception is applied narrowly and only “to the actual wrongful seizure of property by a trustee.”[37] The court found that such exception was inapplicable because all the alleged acts by the defendants occurred in their official capacity. The court affirmed dismissal of the complaint pursuant to the Barton doctrine notwithstanding the fact that the bankruptcy case had been closed when the complaint was filed. But, in doing so, it did not discuss the impact of closure of the case.

B. The Eleventh Circuit Does Not Support the Barton Doctrine’s Extension

Eleventh Circuit: In Tufts v. Hay,[38] Mr. Hay and his law firm represented a debtor in a Chapter 11 case in North Carolina. Mr. Tufts and his firm were representing the debtor in various cases in Florida when the bankruptcy case began. Hay told Tufts that there was a court order approving Tufts’s continued representation of the debtor. Relying on those representations, Tufts did extensive legal work for the debtor. There was no court authorization for Tufts to do this work, however. Because the work was done without authorization, the bankruptcy court ordered Tufts to disgorge the funds collected and held him in contempt when he failed to do so. The underlying bankruptcy case itself was ultimately dismissed by consent order. After dismissal, Tufts sued Hay in district court without first seeking leave from the bankruptcy court. The district court dismissed the suit based on the Barton doctrine. Tufts appealed.

The Eleventh Circuit held that the Barton doctrine does not extend beyond a bankruptcy case’s closure because bankruptcy courts have in rem jurisdiction over the estate. Once the assets of the estate were distributed, nothing that happened later would have any effect on the assets of the estate. Thus, there was no longer subject matter jurisdiction. The court stated:

[U]nder the “conceivable effects” test for section 1334(b), the Bankruptcy Court did not have jurisdiction to consider Tufts’s action, and Tufts counsel were not required to obtain leave from that court before filing this action in the District Court. The Barton doctrine did not therefore deprive the District Court of subject matter jurisdiction over this case. We expressly note that our holding here creates no categorical rule that the Barton doctrine can never apply once a bankruptcy case ends. We address this case only, and here these parties agreed this action could have no conceivable effect on the bankruptcy estate. On this record, the Bankruptcy Court lacked jurisdiction, and the Barton doctrine does not apply.[39]

The Eleventh Circuit revisited and clarified its view on this issue in Chua v. Ekonomou.[40] Chua ran a solo medical practice in Georgia. In 2005, a premed student moved into Chua’s home with him. Chua began prescribing medications to treat symptoms the student was displaying until, one day, Chua came home to find the student dead from an apparent drug overdose. Chua asserted that a conspiracy arose to “pin the blame” for the student’s death on him. The alleged conspiracy included a judge, a receiver appointed in a forfeiture action against him, the receiver’s attorney, and others. A jury found Chua guilty of felony murder and other offenses. Years later, Chua was released from prison, and he sued various defendants in district court, including the receiver, the receiver’s attorney, and the attorney’s law firm. The district court dismissed the claims against the receiver and related defendants for lack of subject matter jurisdiction under the Barton doctrine because Chua had not sought leave from the court that had appointed the receiver.

On appeal, the court reiterated its holding in Tufts v. Hay that “the Barton doctrine has no application when jurisdiction over a matter no longer exists in the bankruptcy court.”[41] The court explained that the policy arguments of the Seventh Circuit might be legitimate, but those concerns overlook subject matter jurisdiction. In any event, the Eleventh Circuit stated, there was no need to base the Barton doctrine on policy grounds “because court-appointed receivers enjoy judicial immunity for acts taken within the scope of their authority.”[42] The court concluded that “[r]eceivers do not need the Barton doctrine to provide an additional layer of protection for the performance of their duties” once the jurisdiction of the court that appointed the receiver comes to an end.[43] That immunity applies even if a trustee’s acts were malicious or in error. Ultimately, the Eleventh Circuit vacated the district court’s dismissal of claims against the receiver and related defendants based on the Barton doctrine and remanded with instructions to dismiss the claims against these defendants based on judicial immunity.

Conclusion

The Barton doctrine plays an important role in protecting court-appointed bankruptcy fiduciaries during the case. In that context, the doctrine has near-universal approval. While most circuits extend the doctrine past a bankruptcy case’s closure for policy reasons, the Eleventh Circuit’s jurisdictional analysis presents a strong argument that the doctrine should not be extended once the bankruptcy court no longer retains authority over a bankruptcy estate.

See, e.g., Alexander v. Hedback, 718 F.3d 762, 767 (8th Cir. 2013); Satterfield v. Malloy, 700 F.3d 1231, 1234–35 (10th Cir. 2012); McDaniel v. Blust, 668 F.3d 153, 156–57 (4th Cir. 2012); In re VistaCare Group, LLC, 678 F.3d 218, 224 (3d Cir. 2012); Lawrence v. Goldberg, 573 F.3d 1265, 1269 (11th Cir. 2009); Beck v. Fort James Corp. (In re Crown Vantage, Inc.), 421 F.3d 963, 970 (9th Cir. 2005); Muratore v. Darr, 375 F.3d 140, 147 (1st Cir. 2004); In re Linton, 136 F.3d 544, 545 (7th Cir. 1998); Lebovits v. Scheffel (In re Lehal Realty Assocs.), 101 F.3d 272, 276 (2d Cir. 1996); Allard v. Weitzman (In re DeLorean Motor Co.), 991 F.2d 1236, 1240 (6th Cir. 1993); Anderson v. United States, 520 F.2d 1027, 1029 (5th Cir. 1975). ↑

For an excellent discussion of the Barton doctrine and the cases interpreting it, see Ronald A. Spinner, Breaking Down the Gate—Changes to the Barton “Gate Keeper” Role in the Eleventh Circuit, Norton Bankr. L. Adviser, May 2022. ↑

In re Yellowstone Mt. Club, 841 F.3d 1090, 1094 (9th Cir. 2016). ↑

In re Nathurst, 207 B.R. 755, 758 (Bankr. M.D. Fla. 1997). ↑

In re Swan Transportation Co., 596 B.R. 127 (Bankr. D. Del. 2018) (Barton doctrine applied to actions against future claims trustee and is intended to protect liquidating trustees and other court appointees); Lankford v. Wagner, 853 F.3d 1119, 1122 (10th Cir. 2017) (extending Barton doctrine to trustee’s counsel where counsel acts under the direction of, or as the functional equivalent of, the trustee); In re MF Global Holdings Ltd., 562 B.R. 866, 869 (Bankr. S.D.N.Y. 2017) (enjoining action commenced by insurers against foreign provisional liquidator in Chapter 15 proceeding); In re Yellowstone Mt. Club, 841 F.3d at 1094 (applying doctrine to members of creditors’ committee); In re Circuit City Stores, Inc., 557 B.R. 443, 449 (Bankr. E.D. Va. 2016) (Barton doctrine applied to enjoin compliance with subpoena by liquidating trustee); In re East Coast Foods, Inc., 652 B.R. 910, 921 (B.A.P. 9th Cir. 2023) (Barton doctrine extended to post-confirmation Chapter 11 trustee); In re PH Dip, Inc., No. 2:23-cv-02843, 2023 WL 158879, at *1 (C.D. Cal. Jan. 11, 2023) (chief restructuring officer is entitled to quasi-judicial immunity when he is acting within the scope of his authority). ↑

Commission to Study the Reform of Chapter 11, American Bankruptcy Institute, Final Report of the ABI Commission to Study the Reform of Chapter 11, § IV(A)(5), at 44 (2014) (citation omitted). ↑

Lebovits v. Scheffel (In re Lehal Realty Assocs.), 101 F.3d 272, 276 (2d Cir. 1996). ↑

In re Linton, 136 F.3d 544, 546 (7th Cir. 1998). ↑

Retirement plans are the bedrock of financial security for millions of Americans. Historically, these systems’ complexity has insulated plan managers from accountability if they fail to meet legal obligations.

That shield is now cracking.

Courts are establishing precedents favoring plaintiffs earlier in the process, and the arrival of legal intelligence driven by artificial intelligence is making it possible to detect violations at scale. In this article, we explore how the legal community can seize this new opportunity to protect plan participants more effectively than ever before.

The Scope of ERISA Litigation Is Expanding

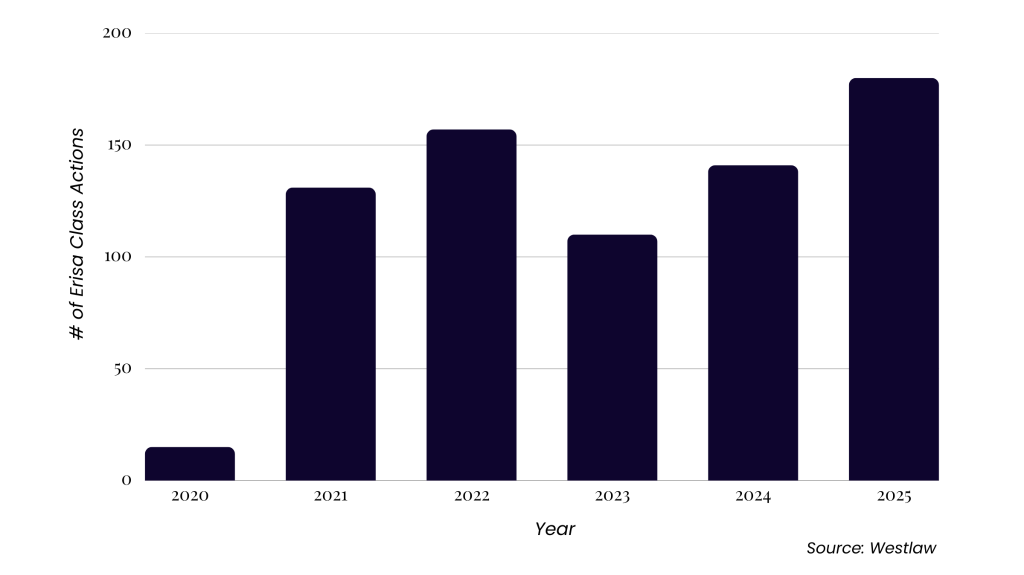

ERISA class actions are growing in volume and financial impact. The total of the top ten publicly reported ERISA settlement values reached $580.5 million in 2023 alone (an all-time high) and $413.3 million the following year, according to Duane Morris. Data analyzed from Westlaw indicates that filing counts have risen dramatically, too, from just fifteen cases in 2020 to more than 180 in 2025 (see graph below).

This growth comes as plaintiffs broaden their scrutiny of plan sponsors’ fiduciary responsibilities, moving beyond excessive fees and employee stock ownership plan (“ESOP”) violations to include an increasing number of claims involving forfeiture, pharmacy benefit manager (“PBM”) fees, and more.

The litigation has focused on two employer-sponsored retirement plan types:

Defined contribution plans: Employees have individual accounts, such as 401(k)s, and their retirement outcomes depend on contributions and investment performance.

Defined benefit plans: These traditional pension plans promise employees a fixed benefit at retirement. The employer must ensure the plan has enough assets to pay those benefits; oversight of how employers manage these plans is critical.

ERISA Class Actions 2020–2025

ERISA class actions have risen from just fifteen cases filed in 2020 to more than 180 in 2025.

Why Are ERISA Violations So Difficult to Detect?

Five structural features of retirement plans make detecting ERISA violations a challenge.

Data structures are complex and opaque. The information needed to assess plan performance is buried in Form 5500 filings, schedules, and attachments. These dense materials often lack standardized naming, contain inconsistent spellings, and require reconciliation with external data.

Investments are hidden inside complex vehicles. Many plans invest through collective trusts, pooled separate accounts, and target-date funds. Aggregated reporting can make underperformance in a fund’s underlying holdings difficult to detect.

Fee indication challenges are excessive. Fee arrangements vary by recordkeeper and investment provider, making it difficult to compare costs across plans and to determine whether fiduciaries secured reasonable pricing.

Forfeiture practices lack transparency. Determining how employer contributions are handled when an employee leaves often requires plan-by-plan reviews, as plan changes and payroll or vesting records often aren’t shown in Form 5500 filings.

Multiyear plan reconstruction is time-consuming. Addressing imprudent investment claims often requires examining performance over multiyear periods and determining whether the right comparison benchmarks were used. Without automation, this analysis is cumbersome.

Six Cases Driving New ERISA Filings

Several recent Supreme Court decisions have established precedents that have pushed ERISA litigation forward.

Reduced the reliability of ERISA statute of limitations defenses by requiring proof that plaintiffs read and understood the disclosures. This has allowed more fiduciary breach claims, particularly older ones, to proceed.

Closed the door on many defined benefit fiduciary breach lawsuits, causing plaintiff firms to shift focus to defined contribution plans, contributing to the rise in excessive fee and imprudent investment class actions.

Gave states more room to regulate PBMs, creating a pathway for more state law claims over drug pricing, reimbursement practices, and cost-containment structures within ERISA health plans. (State laws tend to be stricter on insurance plans.)

Made it easier for plaintiffs to get their ERISA cases heard, triggering a wave of excessive fee and recordkeeping fee lawsuits, many of which survived motions to dismiss based on this case.

Made it easier for ERISA lawsuits to survive early dismissal, encouraging plaintiffs to combine prohibited transaction claims with excessive fee and fiduciary breach claims. This increases plaintiffs’ ability to get their cases heard and expands the ERISA case types that proceed to discovery.

Five Trends and Signals Shaping ERISA Litigation Today

With new precedent expanding accountability across the retirement and benefits ecosystem, litigation is moving into areas that require data-driven analysis.

Excessive fee litigation and imprudent investment claims remain the core of ERISA class actions. Most new cases continue to challenge recordkeeping fees, investment expenses, and fiduciary oversight in defined contribution plans. Stable value funds, share class practices, and recordkeeping arrangements remain frequent targets. These claims will continue to anchor ERISA litigation.

Fee litigation is expanding into midsized plans. Lawsuits have long focused on large plans with billions in assets because they offered the most significant potential recoveries. That is shifting. Over 40 percent of cases in 2024 were filed against plans with assets under $1 billion, indicating an emerging area of opportunity.

Adviser and service provider liability is emerging as a new frontier. Plaintiffs are naming plan advisers, brokers, and consultants as co-fiduciaries, particularly where conflicts of interest or self-interested fee structures appear to have influenced plan decisions. Future litigation may also include business-to-business claims in which employers seek indemnification from advisers whose recommendations created fiduciary exposure.

Health and welfare plan litigation is gaining momentum. Although ERISA litigation has traditionally centered on retirement plans, new transparency rules, limited federal enforcement activity, and a history of troubling fiduciary breaches could spur more private litigation. This area, which has significantly higher total spend and less oversight, includes:

PBM pricing and rebate structures

excessive commissions and conflicts in voluntary benefit products

claims handling practices in self-funded plans

gaps in employer oversight of third-party administrators and algorithms

Regulatory developments are creating new areas of fiduciary risk. The White House’s 2025 executive order calling to expand alternative investments in 401(k) plans may encourage new claims regarding valuation, liquidity, fees, and risk disclosure. Fiduciaries that adopt these products without adequate documentation and monitoring may face higher risk of investment lawsuits.

The Opportunity: Legal Intelligence and ERISA Enforcement

Legal intelligence—the use of AI, data analysis, web intelligence, and legal expertise to identify actionable violations—is changing how plaintiff attorneys detect ERISA noncompliance. Instead of manually reviewing and reconciling fragmented plan documents, attorneys can now systematically surface patterns and anomalies that warrant closer legal analysis and select comparable funds. Peer groups can be selected that closely mirror the characteristics of the challenged funds to maximize chances of success on the merits at trial.

The comparators for each fund align closely with their corresponding fund across various dimensions, including: (1) similar equity-to-fixed-income allocations; (2) active management rather than passive or index-based strategies; (3) comparable asset sizes, ensuring scale-appropriate performance comparisons; and/or (4) similar expense ratios.

Aligning these factors between the challenged funds and the selected peer comparators ensures that the identified underperformance reflects genuine deficiencies in investment management.

Using legal intelligence, attorneys can:

Aggregate Form 5500 data and harmonize fund disclosures across disparate naming conventions and share classes.

Map investment lineups and fee evolution, accounting for plan amendments, freezes, or conversions.

Identify outliers in administrative fees and persistent investment underperformance relative to peer groups.

Detect friction between plan documents and actual reported practices.

Surface plans with data signatures that mirror past ERISA litigation triggers.

As ERISA litigation becomes more specialized and reliant on large datasets, AI-driven analysis is essential for effective case development. Legal intelligence brings hidden risk into view, supporting a more deliberate, evidence-based approach to identifying fiduciary failures and safeguarding plan participants.

A great benefit of living in today’s technological age is the opportunity to go “back to school” to take in recent lectures of prominent college professors. In the field of valuation, there is likely no more highly regarded college professor than Dr. Aswath Damodaran of New York University, whose entire Spring MBA 2025 valuation course is publicly available online.

Session 21 of Damodaran’s Spring MBA 2025 valuation class, recorded on April 16, 2025, provides instruction on the valuation of private (versus public) companies and includes several insightful observations regarding such valuations.[1] However, interested parties might find session 21 remarkable for not only what it includes but also what it excludes.

Exclusion of the (Ubiquitous) Size Premium

Notably absent from session 21 is the oft-cited and so-quantified adjustment of the size premium (“SP”),[2] which, according to popular wisdom, ought to be employed when figuring cost of equity (“COE”) estimates in virtually all private company valuations. This apparent omission, while on one hand glaring given the widespread acceptance and usage of SP by most valuation practitioners, is on the other hand understandable given both SP’s documented weaknesses[3] and Damodaran’s attendant track record of being extremely critical of it.[4] This dissonance, while certainly not the sole example of disagreement in valuation opinion and practice, is perhaps one of the more striking examples of it.

Inclusion of a Risk Element for (Suboptimal) Diversification

Just a few minutes into session 21, Damodaran lays the foundation for a lone, additional risk element when estimating COE for a “smaller” private, versus a “larger” public, company that has nothing to do with SP but, rather, everything to do with the relative level of diversification realized by the marginal investor in either company: “It’s not really a question of private versus public. It’s who the investor in the business is and whether they’re diversified. . . .”[5]

Damodaran goes on to suggest that when valuing a private company, analysts should not be including SP, nor any other such questionable risk factor, in their COE models but rather should be considering an additional risk element for the relatively poorer diversification that is likely to be realized, in some measure, by the marginal investor in that private company (versus the reduced risk from greater diversification that is readily available for the marginal investor in publicly traded stocks). This contrast between investments that carry material diversification risk and those that readily offer material diversification benefits is well-taken, given that traditional risk-and-return models incorporate as their foundation the pricing and characteristics of publicly traded stock. Indeed, as Damodaran notes on slide 136 of this Spring 2025 presentation, “[c]onventional risk and return models in finance are built on the presumption that the marginal investors in the company are diversified.”[6]

The Practical Boundaries of Diversification-Related Risk (and Return)

Damodaran’s example in session 21 of valuing a mature, yet small, single-location French restaurant (beginning around 20:00 of the lecture, or slide 134) is both entertaining and helpful in illustrating how this single incremental risk element can, as a practical matter, describe the boundaries of diversification-related risk and return. Simply put, if a private individual invests effectively all his or her wealth in the restaurant, then that market participant might assess a COE more consistent with that derived using the concept of Total Beta (i.e., the highest effective COE, suggesting the lowest potential valuation, all else equal). Conversely, if a public company considers purchasing the restaurant, then that market participant might assess a COE that is more consistent with that derived using the concept of Beta (i.e., the lowest effective COE, suggesting the highest potential valuation, all else equal). While not necessarily prescribing a method by which to figure a COE between these two bookend notions of compensable risk during his lecture, Damodaran does acknowledge the existence and importance of this middle ground, as well as market participants who may fall therein, by commenting that “everyone else is going to fall somewhere in that continuum. . . .”[7]

Stuck in the Middle

Whether market participants for private companies end up at a particular point within this continuum through negotiation, or a more detailed analysis of compensable risk, or some other reason is largely beside the main point, which is that the boundaries of this continuum may be understood to be a function of a single additional risk element related to relative diversification. Accordingly, acknowledgment of the continuum itself, and how market participants for private companies may be “stuck” somewhere in the middle of it, appears to be as fundamental to understanding private company valuations as is the exclusion of specious risk/return elements from them.

In fact, given the decades-long proliferation of college textbooks that have encouraged generations of analysts to exclude questionable, or “fudge,” risk factors from their COE calculations, one might reasonably expect that the landscape of today’s valuation texts would reflect an ever-deepening root of that basic mandate. However, as Damodaran apprises his class later in session 21: “I know there are books on how to build a cost of capital from scratch for a private business. And most of them break every rule.”[8]

Synthesis

Going “back to school” can be illuminating on certain key aspects of private company valuations. One of these key aspects relates to suboptimal diversification and, specifically, how the marginal private company investor may bear incremental risk from it relative to the marginal public company investor. Accordingly, valuation analyses of private companies that communicate and quantify such a “diversification discount,” while simultaneously eschewing specious risk/return elements, may intimate that their preparers have been “back to school.”[9]

Aswath Damodaran, Session Webcast No. 21: Recorded Session, Valuation MBA Spring 2025 (last visited Feb. 21, 2026) [hereinafter Session No. 21 Recorded Session]. Click link titled “Recorded Session” to begin the class recording. Note that Damodaran is currently on sabbatical as of the publication of this article in Spring 2026. ↑

SP may also be characterized in literature and valuation reports as the size effect, small-stock premium, or small-cap premium, among other similar terms. ↑

Numerous empirical studies conclude that SP is a market anomaly that lacks persistence in out-of-sample testing. In other words, these studies find SP to be a methodological artifact that weakens or disappears once examined outside of the original historical sample. See, for example, Ron Alquist, Ronen Israel & Tobias Moskowitz, Fact, Fiction, and the Size Effect, J. Portfolio Mgmt., Fall 2018. ↑

In 2026, the Canadian mergers and acquisitions market will reward certainty of execution over transaction speed. Domestic transactions will continue to anchor activity as foreign capital faces heightened scrutiny under Canada’s Investment Canada Act (“ICA”) and a revamped Canadian Competition Act. Government priorities spanning defense readiness, energy transition, critical minerals, and sovereign artificial intelligence infrastructure will direct capital flows. Private equity will deploy with discipline. Success will depend on structuring deals around regulatory presumptions, securing capital beyond traditional channels, and aligning with federal industrial policy.

Federal industrial policy is expected to drive sustained capital flow into defense and critical minerals over the coming decade. Domestic transactions will dominate as foreign buyers face longer approval timelines and higher rejection risk. For dealmakers, regulatory preparedness and strategic clarity will determine outcomes.

Capital diversification and the Canada-Gulf corridor

The Canada-U.S. corridor remains vital but no longer exclusive. Trade friction and rigorous ICA enforcement are prompting diversification. While the U.S. Supreme Court’s February 20, 2026, ruling struck down tariffs imposed under emergency powers, uncertainty persists as alternative statutory frameworks for tariffs remain available, creating a window of regulatory uncertainty. We expect Canadian companies to continue to pursue defensive acquisitions within the United States. Simultaneously, sovereign wealth funds from the United Arab Emirates, Qatar, and Saudi Arabia are deploying capital into critical minerals, healthcare platforms, and digital infrastructure. Capital from these allied nations is increasingly replacing investment from restricted sources, positioning Gulf funds as preferred partners for strategic infrastructure projects.

This diversification aligns with Canada’s Defence Industrial Strategy (“Strategy”), launched in February 2026, which commits CAD 180 billion in procurement by 2035 and targets 70 percent of defense acquisitions to Canadian industry across nine sovereign capability areas, including aerospace, ammunition, digital systems, sensors, and advanced manufacturing. The Strategy’s BUILD-PARTNER-BUY framework prioritizes domestic consolidation, structured partnerships with allied firms, and foreign acquisitions only under conditions requiring meaningful Canadian reinvestment. Canada’s alignment with NATO capabilities is driving acquisitions, with companies increasingly looking to European markets for procurement partnerships rather than relying exclusively on U.S. suppliers. Defense readiness acquisitions will intensify throughout 2026 as companies acquire capabilities responsive to emerging operational requirements.

The regulatory fortress: Competition and national security scrutiny

The Competition Act transformation represents a structural shift in deal risk. Mergers in concentrated markets are now presumed anti-competitive unless the parties prove otherwise. Acquirers in telecommunications, banking, grocery, retail, and related sectors must now prove their transactions will not substantially lessen competition, requiring extensive economic analysis and extending timelines. New provisions targeting misleading environmental claims impose liability on parties making unsubstantiated sustainability representations. The burden of proof rests with businesses to demonstrate environmental claims are based on adequate and proper testing. The Competition Bureau is testing its expanded enforcement powers.

The ICA is being enforced with unprecedented rigor. Mandatory pre-closing filing requirements for investments in prescribed business activities, including sensitive technologies, critical minerals, and personal data infrastructure, will introduce regulatory delays that create market risk. The expanded net benefit test effectively freezes capital from non-allied nations in strategic sectors. With foreign capital restricted, domestic buyers and allied sovereign funds face less competition for critical assets, creating pricing advantages for buyers who can move with certainty.

Private equity: Deployment pressure and exit discipline

Private equity sponsors carry record uninvested capital and face intense pressure to deploy and exit assets. In Canada, this will likely lead to disciplined add-on acquisitions and selective exits as holding periods will continue to be extended. Sponsors are crystallizing returns through secondary buyouts and take-private transactions of undervalued public companies. Sponsors dominate the mid-market, particularly in transactions valued between CAD 25 million and CAD 500 million. Growing use of continuation vehicles offers alternatives to traditional exits, enabling sponsors to hold winners longer while delivering distributions to limited partners.

As in 2025, the frequency of carve-out transactions is continuing. Portfolio rationalization is accelerating as companies look to simplify operations under geopolitical pressure and AI disruption. Corporate sellers are divesting non-core assets to refocus on strategic priorities. Private equity buyers are increasingly viewing carved-out divisions as prime deployment opportunities with embedded operational improvement potential. Although carve-out transactions often create complexity due to operational disentanglement, IT and data separation, and standalone cost structure modeling, these challenges primarily create execution risk. For sponsors with operational expertise and patient capital to manage transition services and post-separation integration, carved-out transactions offer differentiated entry points with less competitive tension than traditional auction processes.

Private credit will continue to be an active player in mid-market financing in 2026. With traditional lenders remaining risk-averse, private lenders are well positioned to finance deals between CAD 25 million and CAD 500 million, offering higher leverage multiples and greater structural flexibility. Private credit will continue to see material growth in sponsor-backed transactions. For sellers, this means buyers can move faster and with more certainty. For buyers, it means accessing leverage that traditional lenders will not underwrite.

Sector concentration: Infrastructure, defense, critical minerals, and technology

Federal nation-building priorities are driving M&A in infrastructure, energy transition assets, defense, and critical minerals. Transactions are motivated by scale, supply chain security, and long-term capital deployment. Mining M&A is expected to lead public transaction volume, driven by lithium, copper, nickel, and rare earth demand. Federal investments are supporting domestic digital capabilities and M&A activity across the AI stack—encompassing data centers, cybersecurity, and energy systems supporting advanced computing—is accelerating. Sovereign AI, referring to domestic control over AI infrastructure and capabilities essential to national security, has become a strategic priority.

Technology remains the most active sector by volume, with particular interest in software-as-a-service, data centers, and AI-enabled services. With IPO markets constrained, M&A remains the primary exit route for Canadian technology companies. Canadian and international buyers now collectively exceed U.S. buyers in technology exits, demonstrating that liquidity no longer requires exclusive reliance on U.S. capital.

Wealth management consolidation is accelerating as intergenerational wealth transfer reshapes the advisory landscape. Independent registered investment advisors are being acquired by banks and financial sponsors seeking to expand fee-generating businesses. Higher interest rates are forcing distressed transactions in certain sectors, such as real estate and other capital-intensive sectors, creating opportunities for sponsors to acquire assets at distressed valuations.

Execution discipline: Structure, diligence, and certainty

Deal structures will continue to be materially more sophisticated. Earnouts, vendor take-back financing, and milestone-based payments are expected to be standard mechanisms as buyers and sellers bridge valuation differences and share post-closing risk. Enhanced due diligence now determines transaction viability, covering cybersecurity; environmental, social, and governance (“ESG”) compliance; antitrust risk; and supply chain vulnerabilities. Certainty of execution, rather than headline price, is the decisive differentiator. In addition, representations and warranties insurance will likely continue to be widely deployed, providing risk transfer mechanisms that facilitate cleaner deal structures.

The interim period between signing and closing continues to lengthen due to regulatory scrutiny, raising the cost of capital and integration risk. Sellers now prioritize buyers who can deliver regulatory certainty and compressed timelines. Strong antitrust analysis at the letter of intent stage, pre-cleared financing, and credible ICA navigation plans provide material competitive advantages in contested processes.

The path forward

The 2026 Canadian M&A market will reward strategic clarity, regulatory preparedness, and execution discipline. Strong private capital reserves and supportive government investment could continue to create opportunities, but regulatory complexity and geopolitical uncertainty demand sophisticated navigation. In this environment, certainty outweighs speed. Success requires conducting due diligence that withstands enforcement scrutiny, accessing capital beyond traditional sources, and recognizing that certainty is the most valuable asset in an environment of strategic complexity.

This article is Part X of the Musings on Contracts series by Glenn D. West, which explores the unique contract law issues the author has been contemplating, some focused on the specifics of M&A practice, and some just random.

Introduction—The Muddy Wellies I Abandoned in the London Office

In 2009, I was shooting at the Downton Estate (a year before they started filming the “Downton Abbey” series that made Highclere Castle and its estate famous worldwide). At the end of a great day, I changed out of my shooting clothes and put my muddy Wellies in a plastic bag, which I brought back to London. I was dropped off at the London office because I needed to pick up some work stuff before heading back to my hotel to pack for my trip home to the U.S. As I thought about how I would clean those muddy Wellies and pack them with my clothes, I decided that, as much as I loved my Wellingtons, it was simply too much trouble. So, I left them at the office with instructions that anyone who wanted my muddy, but otherwise perfectly good, Wellies could have them. And a few years ago, I was told by the London partner who claimed them that they were still in use. Wellies are apparently very durable (although I am confident that the London partner has not put the same wear and tear on them that a farmer would).[1]

The Company Responsible for Creating My Wellingtons Is No More

Despite the durability of Wellington boots, the company that created them, Hunter Boots Limited, was not as resilient. Supply chain issues, inflation, and drier weather all contributed to the company’s deteriorating financial condition. But the pandemic may have been the final nail in the coffin. It seems that Wellingtons serve as both a fashion statement and a necessity in muddy conditions at outdoor events (and concertgoers tend to impulse-buy Wellies to attend such events). When the pandemic hit, and all outdoor concerts were canceled (including the famous Glastonbury Festival for both 2020 and 2021), this may have worsened Hunter Boots Limited’s financial situation. Hunter Boots Limited went into administration on June 5, 2023, and sold all its assets to pay off its £112 million of debt. In other words, the iconic, 167-year-old British company that held two Royal Warrants from Queen Elizabeth II no longer exists. However, because you can still purchase Hunter Boots–branded Wellies, you might not have realized that the company itself is no longer in business.

The Assets Sold Through the Administration

Among the assets sold through Hunter Boots Limited’s administration were the assets of its U.S. subsidiary, Hunter Boot USA LLC (“Hunter Boot USA”). Importantly, it was the assets of Hunter Boot USA that were sold by Hunter Boot USA, not the equity of Hunter Boot USA by its owner, Hunter Boots Limited, even though Hunter Boot USA did not itself file a bankruptcy petition under U.S. bankruptcy law.

Hunter Boot USA leased part of the seventeenth floor and the entire nineteenth and twentieth floors of a well-known office building in New York City at 57 West 57th Street. The purchase of Hunter Boot USA’s assets was structured as a typical asset deal, with two separate buyers collectively acquiring substantially all its assets. Neither buyer, however, assumed the 57 West 57th Street lease.

One of the buyers was Marc Fisher LLC, which purchased all of Hunter Boot USA’s footwear inventory, removable fixtures from 57 West 57th Street, and a piece of equipment. The other buyer was Authentic Brands Group LLC, which acquired Hunter Boot USA’s trademarks and domain names, along with certain non-footwear apparel and accessories. Additionally, Authentic Brands had separately acquired all of Hunter Boots Limited’s intellectual property, including the brand, directly from Hunter Boots Limited. Marc Fisher LLC reportedly now manages the operational side of the Hunter footwear category for Authentic Brands in the U.S.

The Asset Buyers Are Alleged to Have Successor Liability for the 57 West 57thStreet Lease

Within a few months after Marc Fisher LLC and Authentic Brands acquired its assets, Hunter Boot USA stopped paying rent to the landlord of 57 West 57th Street. The landlord then sued Marc Fisher LLC and Authentic Brands, as “successors” to Hunter Boot USA, for all unpaid rent through the end of the lease term. The trial court dismissed the landlord’s complaint on the simple basis that the buyers had bought assets and did not assume the tenant’s obligations under the lease. But in a recent New York case, Avamer 57 Fee LLC v. Hunter Boot USA LLC,[2] the appellate court overruled the trial court’s dismissal of the landlord’s complaint, holding that the landlord had plead sufficient facts for the case to proceed to trial based on the “mere continuation” theory of successor liability.

The General Rule—No Successor Liability for Buyers of Assets—and Its Exceptions

Buyers purchase assets from a company rather than acquiring the equity of the company, so they can leave unassumed liabilities with the selling company. However, as with most general rules, the law has long recognized several ways in which a selling company’s liabilities can be imposed on the buyer of its assets, even when the buyer has not explicitly assumed those liabilities.

The means by which a buyer of assets can become responsible for the liabilities of the selling company are generally described as being based on any one of four exceptions:

(1) the [buyer] expressly or impliedly assumes the liability of the [selling company], (2) the transaction is a de facto merger or consolidation, (3) the [buyer] is a mere continuation of the [selling company], or (4) the transaction is a fraudulent effort to avoid liabilities of the [selling company].[3]

Given the vagaries of the standards used to impose liabilities under the “mere continuation” and the “de facto merger” exceptions, particularly with respect to tort liabilities, Texas has eliminated those two exceptions by statute.[4] But most states, including New York, continue to recognize all four exceptions. And contrary to popular belief, these exceptions are not limited to imposing successor liability upon a buyer for product liability claims; they can also be used to impose ordinary contractual liabilities of the selling company on the buyer(s) who only purchased assets.

While New York recognizes all four exceptions to the general rule against successor liability for asset buyers, the court found three of them inapplicable in Avamer 57. First, there was no claim by the landlord that the asset purchase agreements included any assumption of Hunter Boot USA’s liabilities under the lease or otherwise by the buyers, which effectively ruled out the express or implied assumption theory of successor liability (exception 1). Likewise, there was no continuity of ownership between the selling company, Hunter Boot USA, and the buyers, Authentic and Fisher. As a result, the landlord apparently conceded that the de facto merger theory (exception 2) was unavailable as a basis to hold the buyers liable under the lease as Hunter Boot USA’s successors.[5] There was also no indication that the consideration paid by the buyers to Hunter Boot USA was less than the fair market value of the assets purchased, nor that the sale had been concealed, nor that there was any other indicator of fraud, so the court did not believe that the fraudulent avoidance theory of successor liability (exception 4) was available.[6] That left the mere continuation theory (exception 3) as a possible exception to the general rule that a purchaser of assets does not have successor liability.

Digging into the “Mere Continuation” Doctrine

When you understand the factors that New York courts consider in applying the mere continuation theory, you may better appreciate why the Texas Business Law Foundation, a nonprofit group formed by large Texas law firms to “help create a favorable business climate in the State of Texas,”[7] pushed for the elimination of the mere continuation theory (as well as the de facto merger theory) as exceptions to the general rule that buyers of assets do not have successor liability.

In Avamer 57, the court noted that in New York,

courts determining whether a [buying entity] is a “mere continuation” of [the selling entity] have considered [a number of factors, including] whether: (1) all or substantially all assets are transferred to the successor corporation; (2) the predecessor corporation has been effectively extinguished following the transaction; (3) the successor has assumed an identical or nearly identical name; (4) the successor has retained one or more of the same corporate officers, directors, and/or employees; and (5) the successor has continued the same business.[8]

Obviously, all of those factors are present in nearly any asset sale of an entire business. Regarding the first factor, the court noted that the landlord had plead that the buyers in fact purchased substantially all of Hunter Boot USA’s assets and even sought to lease from the landlord the same premises Hunter Boot USA had leased. Concerning the second factor, Hunter Boot USA had informed the landlord that they “would ‘imminently dissolve and wind up their affairs’ and that [they] did ‘not have sufficient funds to make any further payments, including rent.’” Regarding the third factor, the buyers had actually “purchased the Hunter Boot brand, goodwill, intellectual property, and the ability to use the Hunter Boot name” (though the main brand was purchased directly from Hunter Boots Limited). As for the fourth factor, the court noted that the buyers had apparently announced that, in connection with the purchase of Hunter Boot USA’s assets, they did not plan any leadership changes, suggesting they would retain at least some key Hunter Boot USA employees (though rehiring employees of the selling company in an acquisition of a business through an asset transaction is common). Finally, regarding the fifth factor, the court indicated that the fact that the buyers continued to use the leased premises at 57 West 57th Street for a few months after the transaction closed, while Hunter Boot USA continued paying rent and while Fisher was trying to negotiate a new lease with the landlord, constituted continued operations of Hunter Boot USA’s business at the same location by the buyers.[9] (Hmm.)

While the Avamer 57 court was only overruling the trial court’s dismissal on the pleadings, and there will now be a full fact-finding trial, it still raises a host of concerns as to the reliability of using an asset sale to avoid the liabilities of a selling entity where the mere continuation theory is an available exception. Presumably, a UK administration does not provide the same protections to a buyer as a U.S. bankruptcy proceeding with a § 363 sale might have.[10]

Concluding Thoughts

If this transaction had been governed by Texas law, the dismissal of the complaint based on the pleadings would likely have been upheld because the mere continuation and de facto merger exceptions to the general rule protecting asset buyers from successor liability have been removed. And even though Delaware apparently recognizes the mere continuation exception, it appears to be much more constrained in its application:

The mere continuation exception requires that “the purchaser of the assets to be a continuation of ‘the same legal entity,’ not just a continuation of the same business in which the seller of the assets engaged.” “The ‘primary elements’ of being the same legal entity have been said to include ‘the common identity of the officers, directors, or stockholders of the predecessor and successor corporations, and the existence of only one corporation at the completion of the transfer.’”[11]

But a recent decision by the federal district court of New Jersey suggests that New Jersey law, like New York’s, does not consider the continuity of ownership or management a necessary requirement for the invocation of the mere continuation exception.[12]

While there are certainly actions the buyers here could have taken to potentially reduce the applicability of the mere continuation theory under New York law, it is hard to see how one could fully eliminate it. However, if successor liability theories can be likened to a muddy field after a rain, you are well advised to carefully consider how to metaphorically “put on your Wellies” before traversing through it.

Avamer 57 Fee LLC v. Hunter Boot USA LLC, 241 N.Y.S.3d 181 (N.Y. App. Div. 1st Dep’t 2025). ↑

Gary Matsko, De Facto Merger: The Threat of Unexpected Successor Liability, Bus. L. Today (Mar. 14, 2018) (quoting Milliken & Co. v. Duro Textiles, LLC, 451 Mass. 547, 556, 887 N.E.2d 244, 254 (2008) (quoting Guzman v. MRM/Elgin, 409 Mass. 563, 566, 567 N.E.2d 929, 931 (1991))). ↑

Tex. Bus. Orgs. Code § 10.254(b). Indeed, “only express assumption is grounds for successor liability under Texas law.” In re 1701 Com., LLC, 511 B.R. 812, 824 (Bankr. N.D. Tex. 2014). While fraudulent transfer may invalidate the sale, it is apparently not a separate basis under Texas law for imposing successor liability on the buyer. Id. ↑

I have previously written about the de facto merger doctrine. See Glenn D. West, An Asset Purchase That Wasn’t—Beware the De Facto Merger Doctrine in Distressed M&A, Weil Glob. Priv. Equity Watch (May 4, 2020). But note that the holding of the court I discuss there has been subsequently reversed, although the discussion remains valid. See New Nello Co., LLC v. CompressAir, 168 N.E.3d 238 (Ind. 2021). ↑

There is some confusion as to how the purchase price paid by the buyers for the assets was used. Apparently, rather than Hunter Boot USA retaining the purchase price, it may have been used to repay Hunter Boots Limited’s UK secured creditors in the administration. It is not clear whether the assets of Hunter Boot USA were pledged to secure Hunter Boots Limited’s UK debt, nor how much was actually paid for the limited assets being purchased from Hunter Boot USA. The bulk of the value appears to have been in the brand itself, which was separately purchased directly from Hunter Boots Limited. The court appears to acknowledge that fair value was paid to Hunter Boot USA for its assets, but whether there was a claim that could have been filed to avoid the transfer of the consideration for Hunter Boot USA’s assets to Hunter Boots Limited’s creditors on some fraudulent transfer basis is unclear. Regardless, a fraudulent transfer does not necessarily create successor liability—it typically only creates an opportunity for the transferor’s creditor (here, the landlord) to claw back the transfer. ↑

Alan R. Bromberg, Byron F. Egan, Dan L. Nicewander & Daniel S. Trotti, The Role of the Business Law Section and the Texas Business Law Foundation in the Development of Texas Business Law, 41 Tex. J. Bus. L. 41, 63 (2005). The Texas Business Law Foundation is also responsible for legislation that severely limits the alter ego theory in contract-based cases (Tex. Bus. Orgs. Code § 21.223), the recent establishment of the Texas Business Courts, and several business-friendly revisions to Texas corporate law. ↑

Avamer 57 Fee LLC v. Hunter Boot USA LLC, 241 N.Y.S.3d 181, 185 (N.Y. App. Div. 1st Dep’t 2025). ↑

Much attention is paid by plan sponsors of tax-qualified retirement plans to their plan’s administrative practices and procedures. However, plan sponsors should also consider a few corollary administrative practices and procedures for health and welfare plans at the beginning of the year by considering the following three “new year” resolutions:

Resolution #1: Make sure health and welfare plan documentation and delegation is current, accurate, and understood.

Plan sponsors should review the documentation that describes who has authority to administer the plan and what decisions are delegated to vendors versus retained by the sponsor. Start with the plan document(s) (including any wrap plan document), insurance contracts or administrative services only (“ASO”) agreements, summary plan description(s) (“SPD”), and any administrative services agreements. Sponsors should confirm that these documents align with actual operations, especially where claims, appeals, eligibility, enrollment, and COBRA are handled by third parties.

Plan sponsors should also confirm that the documents clearly address and are consistent on key governance points, including:

who is the ERISA “plan administrator” and who is the named fiduciary (if applicable);

who has authority to interpret the plan, make discretionary decisions, and decide claims and appeals (and whether discretion is intended);

delegations to internal teams (e.g., HR/benefits, payroll) and to vendors (third-party administrator (“TPA”), carrier, pharmacy benefit manager (“PBM”), COBRA administrator), including any limits and escalation protocols;

the scope of authority to amend the plan, approve benefit changes, or approve deviations from standard terms (and who can approve exceptions); and

document hierarchy and conflict resolution (plan document vs. SPD vs. policies vs. vendor communications).

Many plan sponsors find that a formal health and welfare plan committee can provide meaningful advantages over a purely “position-based” delegation model (e.g., delegating administration entirely through one or two roles), particularly for larger employers, employers with complex benefit offerings, or employers navigating increased scrutiny around claims, vendor performance, privacy, and fiduciary governance.

A formal committee helps bring structure and consistency to decisions that can create significant legal and operational risk, such as claims appeals, plan interpretation, discretionary determinations, and vendor oversight. A formal committee can help demonstrate that fiduciary decisions are consistent and actively managed through a structured process. The formal minutes or decision records of a committee can demonstrate procedural prudence, provide clear vendor instructions, and provide better audit trails for amendments and communications if issues later arise or decisions are challenged. A delegated committee can also provide better continuity beyond any single role-holder, providing oversight over cost management and trend analysis, population health strategy, vendor rationalization, and risk management.

Once the appropriate parties or committee members are identified, they should receive both ERISA fiduciary training and confidentiality training if privy to any protected health information or individual claims data. This training should be provided upon appointment/delegation and at least once a year thereafter. Training should reinforce the “dos and don’ts” that commonly create risk in the welfare space, such as making off-script coverage promises, issuing informal eligibility overrides, deviating from claims/appeals timelines, and Health Insurance Portability and Accountability Act (“HIPAA”) and data protection obligations.

Resolution #2: Set a proactive annual calendar for welfare plan governance and vendor oversight.

Unlike retirement plans, welfare plan issues such as enrollment changes, eligibility disputes, claims escalations, leave/COBRA coordination, and vendor issues tend to arise intermittently rather than at prescheduled times throughout the year. A strong annual cadence helps the sponsor stay ahead of both compliance and operational risk before issues become urgent or inconsistent practices develop.

At the beginning of the year, sponsors should set a welfare plan governance calendar that includes, as applicable:

open enrollment planning, communications, and proofing timelines;

carrier/TPA/PBM governance meetings (quarterly is often a good baseline), including performance metrics and recurring problem categories;

claims and appeals governance touchpoints, including review of escalations, exceptions, and any “pattern” denials;

reviews of required participant notices (e.g., COBRA, HIPAA special enrollment, Children’s Health Insurance Program Reauthorization Act (“CHIPRA”), Women’s Health and Cancer Rights Act (“WHCRA”), Medicare Part D, etc.) and confirmation that vendor workflows match plan terms; and

a benefits-change and plan-amendment workstream (especially when cost-sharing, network changes, or eligibility rules shift midyear).

Meeting agendas and materials should be distributed in advance, and internal stakeholders should be reminded to review materials ahead of time so that decisions are made deliberately and consistently, not reactively in email threads.

Resolution #3: Keep detailed records of welfare plan decisions, especially exceptions, claims escalations, and vendor direction.

Welfare plan disputes often come down to documentation: what the plan says, what the sponsor communicated, what the vendor did, and why an exception was (or wasn’t) made. Plan sponsors should maintain dated, retrievable records of key decisions and instructions, including:

minutes or written summaries of governance meetings (even if informal), documenting what was reviewed, what was decided, and why;

written records of any direction to vendors—particularly where the sponsor escalates a claim, requests reprocessing, approves an accommodation, or interprets ambiguous plan language;

documentation of plan amendments and the approvals supporting them, and confirmation that the SPD and participant communications were updated accordingly; and

a controlled process for handling exceptions (eligibility overrides, late elections, premium recoupment, coverage reinstatements), including who can approve, what criteria apply, and how exceptions are documented to avoid inconsistent administration.

As a best practice, circulate decision summaries or draft minutes in advance of the next meeting and approve them as the first agenda item. Where the sponsor has authority to amend the plan or approve material vendor changes, maintain signed evidence of approval (minutes, written consents, or signature packets) and retain supporting backup materials. Over time, these governance habits can meaningfully reduce risk, improve vendor accountability, and help ensure the plan is administered in a way that is both defensible and aligned with the sponsor’s overall benefits strategy.

To prove insider trading, the government must establish that a defendant traded securities “on the basis” of material nonpublic information (“MNPI”) in violation of a duty of trust. In many insider trading investigations, those under the microscope will try to show the government that they traded for a reason other than on the basis of MNPI. The success of such a defense depends in part on the interpretation of the language “on the basis of.” Since the 1990s, there has been a circuit split, still unresolved by the U.S. Supreme Court, on how to interpret these four words. Some courts follow the “knowing possession” standard, under which the government need only prove that a defendant traded while knowingly possessing MNPI. Other courts follow the “use” standard, requiring the government to prove that the defendant traded because of the nonpublic information.

Like everything else, artificial intelligence (“AI”) may soon change the way those suspected of insider trading defend themselves. AI, which investors and analysts increasingly rely on to trade stocks and analyze data, could make it easier for an individual investor to create a defense to insider trading. Imagine that an individual gets inside information about a publicly traded company. However, before trading, that person queries AI about the stock and obtains a comprehensive bespoke analysis supporting buying the company’s stock. AI makes it possible, if not easy, for someone possessing MNPI to create a ready-made defense should the government pursue charges for insider trading—and it may be enough to create reasonable doubt.

The Rise in AI-Assisted Trading

Investors and analysts are increasingly using AI in stock trading to analyze data, generate stock picks, and automate trading decisions. And for obvious reasons: AI offers advanced algorithms that can process large volumes of real-time data in a fraction of the time it would take even a seasoned analyst to do the same. AI can also analyze complex patterns in stock prices, financial statements, economic indicators, and even news articles to make predictions with higher accuracy than traditional methods—and all without human intervention.

New trading firms like XTX Markets and Tiger Brokers purportedly use AI to execute millions of trades daily, and there are AI-driven funds like Pictet that leverage AI to try to improve returns. Beyond the professionals, AI trading tools are also becoming available to retail investors. Experts are predicting that this could create a “seismic transformation” in the entire stock market.[1]

Overview of Insider Trading Law

Insider trading is commonly understood as buying or selling securities on the basis of MNPI in breach of a duty. Importantly, there is no federal statute that explicitly bans insider trading. Rather, the law of insider trading has evolved through common-law concepts of fraud and deceit.

The “classical theory” of insider trading refers to a case of a corporate insider who owes a fiduciary duty to the company or its shareholders and breaches that duty by trading on the basis of MNPI.[2] The “misappropriation theory” expands liability by assigning fiduciary duties to certain corporate outsiders.[3]United States v. O’Hagan held that although the defendant was not a corporate insider of the acquirer, he owed a duty to his firm’s client, the source of the information, not to trade on MNPI.[4] Liability for insider trading can attach both to a person that trades on MNPI and an individual that provides a tip in breach of a duty for the personal benefit of the tipper.[5]

The Debate over “Use” Versus “Knowing Possession”