In a 64-page settlement agreement with the Department of Justice (DOJ), Skadden, Arps, Slate, Meagher & Flom has agreed to pay more than $4.6 million to the U.S. Treasury and register retroactively as a foreign agent of the Ukrainian government in a case tied to Paul Manafort. Under the Foreign Agents Registration Act (FARA), a U.S. person engaging in political activities on behalf of a foreign principal, which includes a foreign government, is required to register and make a variety of written public disclosures to the DOJ.

DOJ’s January 15 press release asserts that Skadden made false and misleading statements to DOJ’s FARA Registration Unit about the scope of the firm’s work for Ukraine, which began back in 2012. The statements were made to persuade the Registration Unit that Skadden was not required to register as a foreign agent under the statute. Skadden reportedly spent more than a year negotiating with the Registration Unit over whether it had to register as an agent of Ukraine in the matter. As such registration determinations are based on the evidence DOJ receives about whether registration as a foreign agent is required, either DOJ or the FARA Registration Unit may qualify as a “tribunal” under Model Rule 1.0(m). Lawyers are prohibited under Model Rule 3.3 from knowingly making false statements to a tribunal and, more generally under Model Rule 4.1, from knowingly making a false statement of material fact to any third party.

Questions leading to the firm’s settlement with DOJ came to light tangentially out of the Mueller probe. Suspicions apparently arose because the engagement letter provided that Skadden was going to charge the Ukrainian government 100 Ukrainian hryvnia per hour—equivalent to only $12,000. The press release reads that the law firm initially took a $4 million advance from a third party—an unnamed “business person”—before beginning work on the project. By the end of the engagement, Skadden had been paid $5.2 million by the “business person,” largely through Cyprus-based offshore firms controlled by Manafort.

According to the settlement agreement, “Registration under FARA would have required [Skadden] to disclose, among other things, accurate and complete information related to the compensation that it received for preparing the Report on behalf of the [Ukrainian government], and the identity of” the business person who paid for it. The settlement agreement also reads, “Skadden has already taken substantial steps to comply with its terms, and so long as the firm continues to comply with it, the Department will not undertake any action against the firm” related to its conduct in the matter.

Separately, however, the lead partner in the matter, a former Obama White House counsel who left Skadden last April, has reportedly been under investigation by prosecutors for his work on the matter. Another former Skadden lawyer, a Dutch national, pleaded guilty to lying repeatedly to Mueller’s team about the work done for the Ukrainian regime and was deported after serving 30 days in prison.

These facts if admitted or otherwise proved would constitute misconduct under various provisions of Model Rule 8.4 and can result in suspension or disbarment for the lawyers involved. Possible grounds include violating the Rules of Professional Conduct (R. 8.4(a)); committing a criminal act that reflects negatively on a lawyer’s honesty, trustworthiness, or fitness as a lawyer in other respects (R. 8.4(b)); engaging in conduct involving dishonesty, fraud, deceit, or misrepresentation (R. 8.4(c)); and engaging in conduct that is prejudicial to the administration of justice (R. 8.4(d)).

It is a quirk of the Bankruptcy Code that while it expressly allows oversecured creditors’ claims for post-petition contractual attorneys’ fees, it is silent as to the treatment of claims for post-petition contractual attorneys’ fees on unsecured claims. In part because the Supreme Court in Travelers Casualty & Surety Co. of America v. Pacific Gas & Electric Co., 549 U.S. 443 (2007) did not directly address the question whether unsecured creditors can recover post-petition contractual attorneys’ fees as part of their claims, courts continue to reach conflicting decisions. Very recently, in connection with a dispute arising out of the Tribune Company’s 2008 bankruptcy, Delaware District Judge Richard G. Andrews reversed the decision below and interpreted Travelers to mean that unsecured claims for post-petition contractual attorneys’ fees are not barred by Section 506(b) of the Bankruptcy Code. Wilmington Trust Co. v. Tribune Media Co. (In re Tribune Media Co., et al), Case No. 15-01116 9 (RGA), 2018 WL 6167504 (D. Del. Nov. 26, 2018).

Background

Wilmington Trust Company (the “Trustee”) was the trustee under an indenture for certain unsecured notes issued by Tribune Company (“Tribune”). The indenture required Tribune to reimburse the Trustee for the reasonable attorneys’ and other professionals’ fees and expenses incurred by the Trustee as a result of Tribune’s default. The Trustee submitted a claim in the Tribune bankruptcy that included more than $30 million for attorneys’ and other professionals’ fees and expenses incurred during the bankruptcy case (the “Fee Claim”).

After Tribune objected to the Trustee’s Fee Claim, the mediator appointed by the bankruptcy court recommended that the claim be disallowed in its entirety. The mediator concluded that because Section 506(b) of the Bankruptcy Code addresses only secured creditors’ entitlement to post-petition attorneys’ fees as part of its claim, the expressio unius est exclusio alterius principle of statutory construction applied and precluded recovery of post-petition attorneys’ fees by unsecured creditors.

The bankruptcy court adopted the mediator’s recommendation and disallowed the Trustee’s Fee Claim. In doing so, the bankruptcy court agreed with the reasoning in the mediator’s report—in particular, “the conclusion that the plain language of §502(b) and §506(b), when read together, indicate that postpetition interest, attorneys’ fees and costs are recoverable only by oversecured creditors”—and rejected the Trustee’s Travelers-based arguments with the explanation that the Travelers Court did not consider whether Section 506(b) of the Bankruptcy Code disallows unsecured claims for post-petition contractual attorneys’ fees.

The District Court’s Ruling

In a three-page memorandum opinion, Judge Andrews briskly dispensed with Tribune’s expressio unius argument and the bankruptcy court’s conclusion that because section 506(b) of the Bankruptcy Code expressly allows the claim of an oversecured creditor for post-petition attorneys’ fees, Congress must have intended to disallow such claims to unsecured creditors.

First, Judge Andrews characterized the Supreme Court’s Travelers opinion as having “reaffirmed a requirement that claims that are within the scope of Section 502 are allowed unless they are expressly disallowed in the Bankruptcy Code.” Next, while noting that there continue to be reasoned bankruptcy and district court decisions to the contrary, he observed that “[t]he courts of appeals that have considered this issue post-Travelers have unanimously rejected Appellee’s position and have allowed unsecured claims for contractual attorneys’ fees that accrued post-filing of the bankruptcy petition.” Finally, taking the cue from Travelers, he said “I cannot conclude that Section 506(b) ‘expressly’ disallows the claims at issue here. Thus, I agree with the position adopted by every court of appeals faced with the question; Section 506(b) does not limit the allowability of unsecured claims for contractual post-petition attorneys’ fees under Section 502.”

Observations

As Judge Andrews observed, there has never been a nationwide consensus on the allowability of an unsecured creditor’s claim for post-petition contractual attorneys’ fees. Because Tribune appealed Judge Andrews’ decision, the Third Circuit soon may have an opportunity to decide the issue. Whether it will take that opportunity remains to be seen, however; as of this writing, it has asked the parties to file briefs addressing whether Judge Andrews’ order, which remanded the case to the bankruptcy court for further consideration, is final or otherwise appealable. Putting aside potential jurisdictional defects, it is safe to say that a decision on the merits from another court of appeals—particularly if it joined the other courts of appeals that have considered the issue post-Travelers in allowing unsecured creditors’ claims for post-petition contractual attorneys’ fees—could strongly influence future courts’ decisions on this recurring question.

Competition law, anti-bribery and anti-corruption (ABC), and personal data protection are all essential (but not exclusive) components of a robust legal compliance program. In companies where no such program is in place, employees may nevertheless obtain a general understanding of ABC compliance via mainstream media, and of personal data protection via the numerous GDPR awareness campaigns on social media. Awareness and understanding of competition law, however, is often less robust, and this is especially true outside the United States.

This article provides thoughts, observations, and practical guidance from both the in-house and outside counsel perspectives to help ensure your company practices effective competition law compliance. We know that every company’s in-house legal and/or compliance functions differ in size, scope, and role, but we believe that many of these thoughts and observations are applicable to all.

From the In-House Perspective

Where to Begin

A targeted approach to delivering an effective competition law compliance program (as part of a wider legal compliance program) is vital to ensure that the key messages are absorbed and practiced by all colleagues, including those who have never worked with in-house lawyers. This process can be challenging, especially for the sales and legal teams, because it can reveal cultural differences between in-house lawyers and their nonlegal colleagues. Sales colleagues, for instance, may on occasion push back if they perceive in-house lawyers as blocking essential sales activities; therefore, it is crucial that a competition law program wins credibility by demonstrating added value to commercial activities. When this confidence and trust are established, they can serve to empower a mindset and organizational culture of compliant sales.

Make It Relevant

There is no better way to establish trust than to show colleagues that your role is to support their role and activities. So, treat colleagues as customers, and ensure that you understand the way they do business before advising them on competition law compliance. In practical terms, this means identifying their unique processes in the documents and training materials that you create.

Using templates and one-size-fits-all materials, without tailoring them to the particular issues and business, risks undermining the opportunity to build a relationship of trust. However, working together to create policies, processes, guidelines, and training that support the creation of legally compliant methods can produce significant results. It is also equally important to demonstrate a commitment to supporting commercial activities by being solution-orientated. For example, establishing an ethical wall between purchasing and sales that allows an important activity to take place while ensuring that restricted information flows are not compromised is a common example of a practical solution that also reduces risk.

Make It Understandable

Even lawyers don’t like legalese, so we do not recommend imposing it on your nonlegal colleagues. Instead, draft practical policies and guidelines in plain language and include examples that relate to the business at issue. Remind colleagues from time to time that competition law programs are there to protect the profits of the business by avoiding fines, investigations, and litigation. Compliance programs provide important policies and training that aim to protect the company against revenue loss and reputational damage, and to protect employees from potential personal liability. Periodically, share with business colleagues recent news items relating to other companies in the same (or similar) industry that ran afoul of competition laws. Highlight the impact on both the infringing company’s business and personnel, and consider using these examples as case studies in any future training sessions. These messages, alongside a tailored competition law compliance program, will begin to demonstrate the real added value of the program and help gain the trust of colleagues.

Make It Visible

We recommend that you create and maintain a dedicated and easy-to-locate space on the company intranet to post policies, processes, and guidelines. Promote new policies, processes, and guidelines internally. Don’t overload colleagues with too much information, but create sufficient awareness so that they know how to identify a potential competition law issue and who to contact within the compliance team for inquiries. Then, make yourself approachable and accessible for discussion of these issues with colleagues to enhance their understanding of the law, to troubleshoot, and to find a solution to their situation within the competition law compliance parameters.

All-employee meetings or other large business meetings can be used to deliver presentations that review competition law concepts or introduce new competition law initiatives. Introduce daily reminders—for instance, following a recent meeting, Kyocera Legal provided nonlegal colleagues with a competition law desk card setting out key principles in bullet points. It was a useful and fun takeaway from the meeting, and Kyocera’s nonlegal colleagues are now encouraged to keep these cards on their desks for easy reference. Their presence contributes to creating the mindset and organizational culture of competition law compliance.

We have found that different people learn in different ways, so using varied approaches—for example, formal presentations, informal discussions, and/or daily reminders—will enhance the effectiveness of your competition law compliance program. It is also important to recognize that different personnel come to your company with different knowledge of, and attitudes toward, competition law. Some personnel have worked at organizations where legal compliance and understanding were important values. Others may come from organizations where the law and the legal department were viewed as obstacles to avoid or ignore. The most effective legal compliance leaders will actively seek to identify personnel in this latter group and take steps to educate them, helping them to develop new values that are consistent with their new company’s views on compliance.

Choosing External Competition Law Advisors

The purpose of a competition law program is to support a serious message. Creating an interesting or fun initiative that aims to maximize learning and engagement is important but should not detract from the premise that the legal principles of competition law are non-negotiable. Strengthening this critical message will require expertise on competition law topics in addition to implementing operational activities. It is vital to select external competition law advisors with whom you can effortlessly communicate so that you can absorb the information they provide and, in turn, confidently explain the legal issues to the business.

Supporting as Outside Counsel

Beginning Basics and a Reaffirmed Importance

According to business leaders, competition law is one of the top-three threats to organizations (along with IT and fraud), yet it is not uncommon to see low compliance effectiveness in the competition area. The biggest barrier that we see to effective competition law compliance programs is the traditional attitude of some businesses toward compliance and the way in which compliance teams are kept at arm’s length, separate from key business decisions.

Compliance programs work largely out of sight to protect companies from risk in the form of, among other things, investigations, regulatory violations, and litigation. When they are working well, there is little need for business leaders to consider their function and, as a result, the contribution of compliance is counted in cost rather than in value. Perhaps unfairly, compliance functions are often viewed as the police rather than as partners, and as a hindrance to growth and innovation.

This misconception belies the significant responsibility shouldered by compliance teams in today’s increasingly complex and punitive regulatory environment, and fails to acknowledge the crucial role those teams play in protecting a company’s value and brand. Indeed, research shows that an effective “connected compliance” program has a positive impact on the top, as well as the bottom, line. Strong compliance is not only good practice, it is good business. For instance, an executive’s knowledge of the competition laws can be the difference between breaking the law—and potentially facing a prison sentence—and not.

Connected Compliance

Connected compliance envisages a fully integrated compliance function that is connected to the business and plays an active role in strategic thinking and growth decisions. It rejects the traditional image of a siloed compliance team, where there is no collaboration among departments and where, to employees, compliance means an annual “tick box” exercise, a multitude of complex policies, and a high degree of self-management based on an employee’s own “moral compass.” Indeed, although we observe that business managers have taken more interest in compliance—as they observe longer jail sentences for antitrust violations in the United States—an overwhelming 60 percent still believe that the compliance team takes sole responsibility for good governance.

It Is Everyone’s Responsibility for a Reason

In effective programs, clear responsibility for compliance is given to specific individuals, or “compliance contacts,” who sit within strategic business lines and are involved in determining a company’s growth plan and risk appetite. Clear, simple policies and procedures are outlined, but most importantly, responsibility for compliance is shared across every business division and every organization. This creates a culture of compliance from the top (i.e., senior-most leadership) down so that compliance becomes everyone’s concern and everyone’s responsibility.

Such compliance integration is not a new concept, but some in the business community have been slow to embrace it. Research shows that companies have made little progress in improving critical connections among different business functions or in addressing gaps in compliance accountability among employees at all levels of the business.

For example, take M&A activity, which is on the rise as companies pursue aggressive growth and innovation. M&A activity necessarily involves high risks, cultural upheaval, and regulatory scrutiny, but we observe that many compliance teams are not consistently included when planning and implementing deals. Research by Baker McKenzie shows that fewer than one in five companies involves compliance “substantively” in planning and implementing M&A deals, whereas almost half bring in compliance when selecting new business partners. More than a quarter of respondents admitted to deliberately keeping compliance out of the loop for fear of issues being uncovered and plans derailed. This has serious consequences: on average, 40 percent of organizations that acquired a new business admitted to uncovering compliance issues within that business only after the acquisition.

Not only does this approach increase a company’s risk exposure, it also negates a company’s opportunity to tackle compliance risks during the deal process and to best negotiate the terms of the deal. In short, it risks undermining the value of the investment the company has just made. Most seriously, legislation empowers authorities to hold companies accountable for failing to prevent noncompliant activity, so the “don’t ask, don’t tell” approach sometimes adopted by companies is an insufficient defense in many circumstances.

What Does It Mean?

Promoting an effective compliance program is not only in a company’s interest in the long term, but is arguably an immediate necessity as well. More than half of respondents to a survey conducted by Baker McKenzie are aware of a hidden compliance breach in their organization that is yet to surface to the regulator or the public. Two-thirds of compliance chiefs expect breaches to rise as regulation becomes more complex, and as agencies and prosecutors promote more aggressive enforcement policies. Such enforcement has been particularly apparent for competition law violations, where recent high-profile, high-penalty cases have raised the perceived risk level. Indeed, leaders view competition law as the number-one threat for business compliance, yet competition law is not a top priority in many strained compliance budgets, which often focus on developing “adequate procedures” as a compliance defense in other legal areas, such as bribery and tax evasion.

In spite of these growing risks, more than a third of companies are planning to reduce the compliance services offered to the business as a way of cutting costs. Although there are strong commercial realities—and we know that in-house legal and compliance departments face significant workloads beyond their “compliance” work—businesses must not lose their focus on compliance. Businesses should and can adapt their compliance functions to match the evolving landscape, much like any other business segment. Developing a compliance program that is agile, collaborative, and above all connected will ensure its effectiveness and protect the company’s brand and value.

Final Words

There are many aspects to developing, implementing, and maintaining a comprehensive compliance program, and this article does not endeavor to cover them all. However, we hope that our observations and practical guidance provide an overview of the importance of developing a comprehensive and dynamic compliance program.

Today’s computer hackers are helping themselves to the privileged information that has been a core covenant of the attorney-client relationship for hundreds of years. Hackers know the value of sensitive information that is exchanged and retained between a business and its law firms. According to the most recent information from the American Bar Association, 23 percent of law firms experienced a cyber attack or data breach in 2018.

There has been widespread response to breaches from the largest businesses and law firms, who were initially hit the hardest; they have been working to lock down their data and information. Small- and mid-sized companies and their law firms have also grown serious about cybersecurity. Cybersecurity has become a top priority for legal departments and their service providers.

To assess progress and continue to find ways to increase security, it is critical to take inventory across the chain of information exchange and storage, ensuring all law firms working for the company, regardless of their size and location, reach consistently high levels of compliance with cybersecurity standards. That is because every link in the chain of information is a potentially vulnerable junction for compromise.

Here are questions to ask to help you better understand the risks and opportunities for strengthening every link in your cybersecurity chain:

Are there consistencies in cybersecurity between large, mid-sized, and small law firms?

Larger law firms assessed their security measures after the now-infamous DLA Piper data breach and subsequent shutdown of the firm in 2017. Clients began to require their firms to complete extensive cybersecurity surveys to demonstrate readiness in the event of a potential hack. Clients wanted to know their exposure given their firms’ cybersecurity sophistication, or lack thereof.

Smaller firms moved into action as well, many working with consultants who assessed their processes and formulated plans to achieve a higher state of security. The partners of small and mid-sized firms have been able to enact change as they have closer management oversight of their IT systems and were likely involved in the development of the IT department and decisions on selected tech programs from the beginning. They have intimate knowledge of their current processes and practices and, in the end, these partners are ultimately responsible for the safeguarding of all client relationships and the sustainability of the firm over the long term, given their names are on the door.

All law firms should now have cybersecurity plans in place. The key indicator to understand, however, is their capacity to take action on the plan to make enhancements as soon as the environment changes. Many times, scaling cybersecurity best practices across smaller firms can happen more quickly. That is not to say that it is easy—the most effective cybersecurity assessment and enhancements should be rigorous for any firm.

Are there cybersecurity variances across law firms in different jurisdictions and geographies?

Data privacy and protection regulations are constantly changing across states and countries. If a company does business across jurisdictions and regions, it is important that its law firms stay current on changes in all of those markets and proactively advise on how they affect the overall cybersecurity of the clients’ information and their legal obligations.

The EU’s recent implementation of the General Data Protection Regulation (GDPR) is only the latest (albeit most sweeping) development in this crucial area of law. Outside the EU, however, there is little uniformity in how different countries protect data.

For example, personal information protection does not have a long history in the Chinese legal system, but it is now one of the hottest legal topics in China. Chinese legislation contains broad, confusing definitions of protection and involves stringent regulations and severe legal penalties. The Chinese government is still exploring a feasible way to implement the relevant legal requirements. This has delayed the process of issuing the rules.

In contrast, Taiwan recognized the importance of data protection and put information protections in place more than 20 years ago. The most current personal data protection law in Taiwan was enacted in 2010 and implemented in stages. The law is now fully in effect and, among other changes, removes the data user-registration requirement and expands data protection obligations to all industries in Taiwan and to all methods of processing. All business entities in Taiwan that collect, process, or use data must comply with this law, but it does not extend to non-Taiwan business entities that collect, process, or use data of Taiwan resident “protected parties” outside Taiwan.

In Singapore, the mandatory protection of personal data came into force only in 2014 and is meant to address growing concerns from individuals about how their personal data is used, maintain the trust of individuals in organizations that manage data, and strengthen Singapore’s position as a trusted business hub.

Australian privacy law has national significance and contains 13 principles, which have the force of law by virtue of the country’s Privacy Act of 1988. The federal privacy regulator is the Australian Information Commissioner.

These are just a few of the differences that exist by region. If a company does business in multiple jurisdictions, it should expect its law firms to not only intimately understand the data rules of their market, but proactively share their knowledge. An example of this is a recent guide published by a global network of legal firms.

What should the cybersecurity culture be at my law firm(s)?

The cybersecurity culture at your law firm should be proactive and integrated into everyday practice, prioritized and lead by those at the partner level. Cybersecurity should be a top focus of upper management, not relegated to IT staff or firm administration. Many major breeches have occurred because of employee or vendor error, and are not directly controlled by the IT department. Partners should play or share the role of chief compliance officer and chief information security officer to keep cybersecurity at the forefront of their practice.

With what standards should my law firm(s) comply?

Having a current information security plan, and reporting to demonstrate ongoing progress against that plan, are critical indicators of the cybersecurity strength of a law firm. All law firms should be able to report high levels of standards in these areas:

management’s demonstrative commitment to cybersecurity

ongoing risk assessments

technical safeguards

physical safeguards

employee training

third-party risk management

business continuity

breach response

frequent reviews and updates

Significant progress has been made in boosting cybersecurity in the legal industry. In 2018, the American Bar Association reported just a 1 percent increase in law firms that have experienced an attack, much improved over the 8 percent increase from 2016 to 2017. While it will never be possible to completely eliminate breeches, the hard work law firms are doing to reduce the risk is clearly making a difference.

Most public employees in California are eligible to enroll in a state or county retirement system. These retirement systems are governed by state statutes, known primarily as either the Public Employees’ Retirement Law (“PERL”) or the County Employees’ Retirement Law (“CERL”), depending on the retirement system in question.

While the legislature enacts statutes to provide benefits in retirement, the California courts have developed what is known as the “California Rule” regarding vesting of these benefits. This judicially created rule states that public employees in California have vested rights in their pension benefits, and therefore begin earning this deferred form of compensation from their very first day of employment. While they may not remain employed long enough to actually receive benefits, as long as they do remain employed, they have the right to keep earning this deferred compensation to be paid after they retire. The courts have held that these pension benefits cannot be modified unless: (1) the modification maintains the integrity of the system; (2) bears some relation to the theory of the pension system; and (3) if the modification results in some disadvantage, it is accompanied by a comparable new advantage. Practically speaking, this makes it difficult for the state legislature to revise pension statutes in order to allow reductions in benefits that had previously been promised to public employees. The result is that promises made years or decades earlier generally cannot be modified despite current exploding costs being absorbed by public employers.

On September 12, 2012, Governor Jerry Brown signed into law the Public Employees’ Pension Reform Act of 2013 (“PEPRA”) in order to address the looming crisis of increasing pension costs. PEPRA primarily changed the pension benefits that employees hired after its enactment could expect. However, PEPRA also modified some of the pension benefits for existing public employees under both the PERL and CERL. Some of these changes include the discontinuation of the right to purchase service credit not related in any way to prior employment (known as “airtime”), as well as the discontinuation of certain types of compensation in pension calculations, among others. There are currently several cases before the California Supreme Court, which will analyze whether PEPRA changes to existing employees’ pension benefits violated the California Rule.

On December 5, 2018, the California Supreme Court heard oral argument in Cal Fire Local 2881 v. CalPERS, which it chose to hear first. The state intervened in the case to defend PEPRA. In this case, public employees are challenging PEPRA’s elimination of “airtime.” The appellate court held that employees did not have a vested right to purchase airtime because there was no express language in the statute, or its legislative history, that unambiguously stated an intent by the Legislature to create a vested pension benefit. Alternatively, the appellate court held that it was permissible to eliminate “airtime” because a pension system was established to compensate for actual work and that, in fact, the option to purchase “airtime” was detrimental to the successful operation of the pension system because it does not relate to any work performed. Finally, the appellate court held that while a comparable new advantage “should” be provided, the term “shall” in prior decisions was not a mandate. If upheld, this decision would mark a serious erosion of California public employee pension vesting principles.

During oral argument before the California Supreme Court, the justices directed questions at both attorneys to address whether the opportunity to purchase airtime was a vested right. The employees argued that the opportunity to purchase airtime was a vested right upon one’s acceptance of and/or continued employment. The justices challenged this notion because any such rule may be overbroad and may apply to any employment benefit offered to an employee. Interestingly, the justices did not question either side on whether there needed to be a comparable new advantage provided to employees in exchange for the elimination of the right to purchase “airtime.”

On the other side, the state argued that the legislature never intended for this opportunity be to a vested right, neither expressly nor impliedly. The justices seemed to concede that there was no express language that created a vested right, but questioned whether the legislature could ever create an implied right to a benefit and if so, how. The state responded that there appears to be an implied right to a “substantial, reasonable pension,” but that purchasing “airtime” was not necessary to providing a substantial, reasonable pension.

While it is usually difficult to predict a court’s final ruling based on the questions the justices ask during oral argument, the court could be signaling its direction here given the questions it did not ask. Specifically, the justices did not ask about the heart of the California Rule; whether alternative benefits must be provided whenever a vested right is impaired. Given the other cases pending before the Supreme Court and the nature of the justices’ questions in Cal Fire, the court appeared to signal that it will likely issue a narrow ruling related to airtime itself, allowing major components of the California Rule to be argued in later cases. In any event, even if the Supreme Court overturns the California Rule in full and allows pension benefits to be modified more easily, there is unlikely to be an immediate impact on California public employees nor relief to public employers facing ever-increasing pension costs. Any change to public employee pension benefits must first come from the state legislature. While overturning the California Rule would, in theory, make it easier to modify pension benefits, it would still be up to the state legislature, not individual public employers enrolled in these pension plans, to first make modifications to the state statutes. Absent such statutory change, these benefits will remain largely untouchable, regardless of the court’s ultimate decision.

Partner Steven M. Berliner and Associate Danny Y. Yoo are attorneys with Liebert Cassidy Whitmore, California’s largest education and public sector labor and employment firm. Berliner is the Chair of the firm’s Retirement, Health and Disability Practice Group; he can be reached at [email protected] or 310-981-2000. Yoo represents public agency clients in all facets of labor and employment law; he can be reached at [email protected] or 310-981-2069.

Last year, I authored an article for Business Law Today discussing the ethical obligations of lawyers in connection with potential searches of confidential information on their portable electronic devices by the U.S. Customs and Border Protection (CBP) and Immigration and Customs Enforcement (ICE)—both agencies within the Department of Homeland Security (DHS).[1] This companion article briefly considers the ethical obligations in this scenario of judges—including business court judges and bankruptcy judges—under the canons of judicial conduct. Like lawyers, judges should consider whether consenting to a device search by a CBP or ICE agent is compatible with their professional responsibilities.

Rather than reiterate information about current CBP and ICE policies as background, the reader should refer to that earlier article.

Sources of Rules and Principles of Judicial Ethics

Judges of the States and U.S. Territories

The responsibilities of a state judge are set forth in the applicable code of judicial conduct (CJC) for the state in which he or she is a judicial officer;[2] guidance and interpretations on the meaning of individual provisions are periodically issued by the appropriate authorities, whether judicial advisory committees or similar bodies, or judicial conduct commissions in connection with disciplinary proceedings, which, if appealed, may also lead to interpretations by the jurisdiction’s court of last resort. In addition, interpretations of the MCJC are periodically issued by the ABA Standing Committee on Ethics and Professional Responsibility. These interpretations, although not binding on judges in any jurisdiction, can be influential for interpretation of identical or substantially identical provisions in the relevant jurisdiction’s CJC.[3]

Part-time judges are also bound by the CJC. To the extent that they are also practicing lawyers, however, they should be aware of pertinent obligations under applicable rules of professional conduct as well. (Although full-time judges are usually members of the bar, they may not practice law (MCJC Rule 3.10), so the latter set of rules are largely inapplicable to them).

Federal Judges

Federal judges are subject to statutory rules of judicial conduct and to the Code of Conduct for United States Judges.[4] Interpretive guidance is also available in the form of advisory opinions issued by the Codes of Conduct Committee of the Judicial Conference of the United States.

Pertinent Principles of Judicial Ethics

Compliance with Law. MCJC Rule 1.1 requires judges to comply with the “law”; the comparable provision in the Federal CJC is Canon 2A. The purpose of these provisions is central to judicial ethics—avoiding both the appearance of impropriety and diminishing public confidence in the judiciary. Assuming, arguendo, that border searches of personal electronic devices are authorized by existing federal statutes,[5] there can be no civil disobedience by a judge of CBP and ICE policies.

Avoiding Abuse of the Prestige of Judicial Office. MCJC Rule 1.3 prohibits judges from using or attempting to use the prestige of judicial office to gain personal advantage of deferential treatment of any kind; the comparable provision of the Federal CJC is Canon 2B.[6] Thus, a judge should avoid any conduct that might be, or be construed as, an attempt to use the cachet of judicial authority to intimidate or cajole a border official wishing to search any of the judge’s electronic devices.[7]

Nonpublic Information. Perhaps the most pertinent provision of the MCJC is Rule 3.5,[8] although its language creates some ambiguity. Like its predecessor, Canon 3(B)12, the rule prohibits intentional disclosure of use of “nonpublic information acquired in a judicial capacity for any purpose unrelated to the judge’s judicial duties.” “Nonpublic information” is a term of art specific to this rule; initially it is defined, somewhat circularly, as “information unavailable to the public,” but the definition goes on to provide a nonexclusive list of examples: “information that is sealed by statute or court order or impounded or communicated in camera, and information offered in grand jury proceedings, presentencing reports, dependency cases, or psychiatric reports.” As electronic filing becomes more ubiquitous, judges are increasingly likely to have these sorts of pleadings or documents on their portable electronic devices.

One might well ask whether a border search of an electronic device qualifies as an “intentional” disclosure of nonpublic information acquired in a judicial capacity. That is certainly an open interpretive question. Given the breadth accorded the concept of “intent” in tort law and criminal law, however, it would be dicey in a disciplinary proceeding to hang one’s hat on such an argument, especially where the expected retort would be that the judge knew or reasonably should have known that his or her electronic devices would potentially be subject to search when traveling abroad, and that such a search would unduly risk the proscribed disclosure.

Some Concluding Observations

The following are worthy considerations by any judge anticipating cross-border travel:

Consider whether it is necessary to bring with you any electronic device containing confidential or privileged information. (If you’re going on vacation, the foolproof solution is to enjoy yourself and leave the device behind!)

If you absolutely must bring one or more portable electronic devices along, make sure each one is thoroughly scrubbed of all privileged or confidential information. Note that merely deleting files may not be adequate to remove them completely. Alternatively, consider acquiring an electronic device exclusively for use during foreign travel and avoid, to the maximum extent possible, placing confidential or privileged information thereon.

Merely encrypting privileged or confidential information on a device is no guarantee of its remaining confidential. Remember that border agents may demand that you provide password or other decrypting information, and failure to do so can lead to your device being seized and detained for a period of time.

Advise the border agent of the existence of any privileged material on the device in question.

Finally, be cognizant of the location and content of all privileged and confidential information on each device you bring across the border, and be prepared when advising a federal officer of the existence of privileged or confidential information to identify for the officer specific files or categories of files, and any other information that will help the officer segregate such information.

[2] Specific references in this article will be to the ABA Model Code of Judicial Conduct (MCJC). Judges should consult the version adopted in their respective states.

[4]See Admin. Office of the U.S. Courts, Code of Conduct for United States Judges [hereinafter Federal CJC]. The Federal CJC is applicable to U.S. circuit judges, district judges, Court of International Trade judges, Court of Federal Claims judges, bankruptcy judges, and magistrate judges, and has been adopted by the U.S. Tax Court, the Court of Appeals for Veterans Claims, and the Court of Appeals for the Armed Forces.

[5] Interestingly, the MCJC defines “law” somewhat broadly to include statutes, although not broadly enough expressly to include regulations or agency policy statements. The Federal CJC contains no definition of “law.” The commentary to Canon 2A, which also does not expressly include regulations or agency policy statements, seems more inclusive: “Because it is not practicable to list all prohibited acts, the prohibition [against impropriety and the appearance of impropriety] is necessarily cast in general terms that extend to conduct by judges that is harmful although not specifically mentioned in the Code. Actual improprieties under this standard include violations of law, court rules, or other specific provisions of this Code.” (Emphasis added).

[6] Canon 2B provides in pertinent part: “A judge should [not] lend the prestige of the judicial office to advance the private interests of the judge or others . . . .”

[7]Cf.In re Muller, No. 069351, Presentment (N.J. Sup. Ct. Adv. Comm. Judl. Cond. 2011), Final Order (N.J. 2011) (reprimanding judge who made 9-1-1 call in connection with service of subpoena on her husband in unrelated matter for repeatedly identifying her judicial position when rebuking responding officers); In re Heiple, 97-CC-1 (Ill. Cts. Comm’n 1997) (censuring state chief justice for avoiding speeding tickets by producing judicial identification credential rather than driver’s license when stopped by police on several occasions and saying, “Don’t you know who I am?”).

[8] The closest analogue in the Federal CJC is found in Canon 4, which relates to extrajudicial activities. Canon 4D(5) provides, “A judge should not disclose or use nonpublic information acquired in a judicial capacity for any purpose unrelated to the judge’s official duties.” This language, in contrast to MCJC Rule 3.5, is not modified by the adjective “intentional.” It is uncertain, however, whether this language, although unambiguous, applies to general disclosures, as it is part of Canon 4D, which is headed “Financial Activities.”

In 2018, the first full year with Chairman Clayton at the helm of the Securities and Exchange Commission (“SEC”), private fund managers continued to receive significant attention from the SEC’s Office of Compliance Inspections and Examinations (“OCIE”) and Division of Enforcement, notwithstanding the SEC’s stated focus on retail investment managers. Highlights of the SEC’s activity in the private fund space and certain other regulatory developments affecting private fund managers are discussed below.

SEC Continues to Bring Significant Enforcement Actions Against Private Fund Managers

In 2018, the SEC continued to bring a significant number of enforcement actions against private fund managers, including the following:

Allocation of expenses to and fee-sharing arrangements with co-investors. In December 2018, the SEC settled charges with a PE fund manager over its failure to allocate expenses to employee funds and co-investors investing alongside the manager’s flagship funds, noting in the consent order that the flagship funds’ organizational documents failed to disclose that employee funds and co-investors would not bear their proportional share of expenses. Additionally, the manager failed to disclose arrangements it made with co-investors to share portfolio company fees, where such co-investors did not provide services to the portfolio companies and such arrangements resulted in the flagship funds paying higher management fees because fees shared with co-investors did not offset the flagship funds’ management fees. Notably, the SEC acknowledged that the manager, prior to being contacted by the SEC’s Division of Enforcement, had fully reimbursed the misallocated expenses and shared portfolio company fees dating back to 2001 (over a decade after the five-year statute of limitations on the SEC’s disgorgement remedy), yet still ended up settling with the SEC and paying a civil penalty.

Use of operations groups; in-house charges; service provider conflicts. In December 2018, the SEC settled charges with a PE fund manager whose funds made minority investments in other private fund managers. The consent order noted that the manager allocated the full cost of its “business services platform” (i.e., an operations group), which it created to provide operational consulting services to the alternative investment firms in which its funds invested, to its funds, although a percentage of the operations group employees’ time was spent performing services for the manager instead of the firms the funds invested in (e.g., capital raising and deal sourcing for the manager’s funds). In December 2018, the SEC also settled charges with a PE fund manager for charging the preparation cost of its funds’ tax returns by the manager’s in-house personnel to the funds without specific authorizing disclosure, as well as for failing to adequately track or allocate the expenses of two consulting firms between the manager and its funds (or among its funds). Further, that consent order noted that the manager failed to disclose conflicts related to the manager’s relationship with these consulting firms, resulting in expense allocation decisions that posed actual or potential conflicts of interest, including a (i) personal loan made by the manager’s principal to a consulting firm, secured by money owed by the manager and the funds, which was repaid with consulting fees paid by one of the manager’s funds; and (ii) services relationship between the manager’s principal and a consulting firm that was also providing services to the funds and, while such consulting firm was servicing the funds, the manager’s principal made a personal investment in the firm.

Preferential arrangement with group purchasing organization. In April 2018, the SEC settled charges with a PE fund manager for failing to disclose conflicts of interest related to its arrangement with a third-party group purchasing organization (“GPO”), a company that aggregates portfolio companies’ spending to obtain volume discounts from participating vendors, where the GPO compensated the manager based on a share of the fees received from vendors in connection with purchases by the funds’ portfolio companies through the GPO.

Failure to apply fee offsets. The SEC continued its focus on fee and expense practices, settling charges with a private fund manager in June 2018 over its failure to offset consulting fees received from portfolio companies against fund management fees, as required by its funds’ governing documents.

Accelerated monitoring fees. The SEC continued its focus on accelerated monitoring fees in 2018, bringing its fourth high-profile case in as many years, and continuing to target a lack of specific, pre-commitment disclosure of such fees to all fund investors. Most recently, in June 2018, the SEC settled charges with a PE fund manager despite the manager disclosing its accelerated monitoring fee practices in its funds’ semi-annual financial reports and side letters with many, but not all, investors.

Failure to disclose material information in connection with purchase of fund interests. The SEC settled charges with a PE fund manager and the manager’s principal in September 2018 in connection with the principal’s purchase of limited partner interests from fund investors based on stale year-end pricing, when the manager and its principal had received financial information indicating a materially higher valuation since year-end.

General advertising and solicitation. An unregistered private fund manager settled charges with the SEC in September 2018 in connection with, among other things, its failure to comply with Regulation D’s prohibition on general advertising and solicitation when it engaged in general solicitation of a private cryptocurrency fund offering through its website, social media accounts and traditional media outlets. In addition to paying a civil penalty, the manager was required to make a rescission offering to each investor in the fund.

Political contributions. The SEC settled charges with three investment managers in July 2018 in connection with violations of the SEC’s Political Contributions or “Pay-to-Play” Rule, reflecting the SEC’s ongoing focus on prohibited political contributions.[i] Similar to several earlier Pay-to-Play Rule cases, some of the 2018 cases involved modest contributions that were returned to the donor. Additionally, in June 2018, following a lengthy application process, the SEC granted exemptive relief to a fund manager in connection with its violation of the Pay-to-Play Rule stemming from a $2,700 contribution by an executive of the manager to an incumbent state governor running for President, permitting the manager to retain approximately $37 million in advisory fees that would have been subject to forfeiture absent such relief.[ii]

Insider trading. The SEC continued its longstanding focus on pursuing insider trading actions, including cases against private fund managers for failing to establish, maintain and enforce policies and procedures to prevent insider trading. In May 2018, the SEC settled charges with a private fund manager after two of its portfolio managers made trades based on material nonpublic information (“MNPI”) received from outside consultants where the manager failed to enforce its insider trading policies regarding the use of, and failed to monitor employees’ communications with, these consultants. Specifically, the consent order noted that the manager failed to ensure employees were following a checklist the manager had adopted for resolving insider trading concerns. In December 2018, the SEC settled charges with a manager to private funds and business development companies (“BDCs”) in connection with its failure to maintain policies and procedures to address its potential use of one of its client’s MNPI for the benefit of another client, noting in the consent order that the manager previously indicated that it seeks to leverage information flow generated by its BDC clients for its private fund clients.[iii]

“Broken windows” cases. Although the current administration has given some indication it may be shifting away from the prior SEC administration’s touted strategy of pursuing small “broken window” violations, the SEC brought a number of cases in 2018 against private fund managers related to minor and/or technical infractions, including cases involving technical violations of the SEC’s Custody Rule[iv] and the failure to file Form PF.[v]

Update on Impact of Kokesh Five-Year Statute of Limitations on Disgorgement

The Division of Enforcement’s 2018 annual report highlighted the impact of the 2017 unanimous Supreme Court decision in Kokesh v. SEC on the Division’s activity. The report estimated that Kokesh, which generally limits the SEC’s ability to obtain disgorgement more than five years after the underlying violations, resulted in the SEC foregoing approximately $900 million it would have otherwise sought since the Kokesh decision.[vi]

Modest Increase in SEC Exams; Additional Resources Allocated to Oversight of Investment Advisers

As expected, unlike the more than 40% increase in the number of investment adviser examinations in 2017, the SEC’s fiscal year ended September 30, 2018 saw a modest 11% increase in the number of such exams. Additionally, the SEC’s 2019 budget request to Congress sought 13 restored positions that would focus on examinations of investment advisers and investment companies with the stated goal of improving overall examination coverage of investment advisers, including an emphasis on the nearly 35% of advisers who have never been examined, and, similar to its 2018 budget request, more than 50% of the SEC’s 2019 budget plan is allocated to its examination and enforcement programs. We have continued to see private fund registered adviser examinations at approximately the same frequency as prior years.

Other Notable Developments

Proposed SEC Fiduciary Rule and Regulation Best Interest. In April 2018, the SEC proposed a package of rulemakings and interpretations intended, among other things, to codify and reaffirm (and, in some cases, clarify) the fiduciary duties investment advisers owe their clients under the Advisers Act. Specifically, the proposal highlights: (i) the “duty of care,” which generally requires an adviser to provide advice that is in its clients’ best interest, seek best execution of public securities transactions and to act and provide advice and monitoring over the course of a relationship with a client; and (ii) the “duty of loyalty,” which generally requires an adviser to put its clients’ interests ahead of its own, avoid unfairly favoring one client over another, make full and fair disclosure of material facts and seek to avoid, and otherwise make full and fair disclosure of, material conflicts of interest with clients.

Electronic messaging. The SEC showed a focus on advisers’ use of electronic messaging for business purposes and, in December 2018, OCIE issued a risk alert reminding advisers of their obligations when using various forms of electronic messaging (e.g., text messaging, instant messaging, personal and private email, etc.) to conduct business.[vii]

Advisory fees and expenses. The SEC remains focused on fee and expense practices and, in April 2018, OCIE issued a risk alert detailing frequent advisory fee and expense compliance issues identified in examinations of registered advisers, such as applying incorrect fees (e.g., charging carried interest to investors who were not “qualified clients” under the Advisers Act), omitting credits or rebates or applying discounts incorrectly, and misallocating certain adviser expenses to clients (e.g., regulatory filing fees, certain travel expenses, etc.).[viii]

EU and State Privacy Laws. The EU’s wide-sweeping General Data Protection Regulation (“GDPR”) became enforceable in May 2018. Notably, GDPR has extra-territorial reach, applying to all “processing” (e.g., collection, recording, use, etc.) of “personal data” (e.g., name, identification number, online identifier, etc.) relating to individuals in the EU regardless of whether processing takes place in the EU. As such, GDPR may reach U.S. private fund managers whose funds include EU-based investors even if a manager maintains no offices or operations in the EU.

Additionally, a new California privacy law enacted in 2018 (effective January 1, 2020) potentially will impact private fund managers (and their portfolio companies) doing business in California with gross revenue in excess of $25 million, including managers not located in California whose funds include California-based investors. Additional changes are likely to be made to the law before its effective date, but the new law generally would require affected managers to update their privacy practices and business processes to accommodate new consumer privacy rights. Notably, a recent amendment to the law exempts most personal information collected and used pursuant to the Gramm-Leach-Bliley Act, which is currently applicable to most private fund managers. It is also worth monitoring whether other states follow California’s lead and enact similarly expansive privacy laws.

Increase in BDC Leverage Limits. As part of the Consolidated Appropriations Act, 2018, the permitted leverage ratio of total debt to equity for BDCs was increased from one-to-one to two-to-one, a significant development for private equity and private credit managers operating or interested in operating BDCs.

Cayman AML. In 2018, the scope of Cayman Islands’ Anti-Money Laundering Regulations (“Cayman AML Regulations”) was expanded to reach private funds, including private equity, venture and real estate funds domiciled in the Cayman Islands that are not registered with the Cayman Islands Monetary Authority. A key component of the updated Cayman AML Regulations included a requirement for Cayman funds to designate, by December 31, 2018, natural persons at a managerial level to serve as: (i) Anti-Money Laundering Compliance Officer; (ii) Money Laundering Reporting Officer; and (iii) Deputy Money Laundering Reporting Officer. Cayman Islands-domiciled private funds also are required to maintain policies and procedures for risk-based due diligence on investors.

In the aftermath of the widely-publicized control breakdowns at Wells Fargo Bank, and in a number of regulatory actions occurring this past year, boards of directors of public companies and financial institutions have been directed to improve oversight and corporate governance. Reacting to demands from regulators and shareholders to improve board oversight and governance, it seems that boards are evolving from an approach of focusing primarily on “tone at the top” to one of instituting substantive checks and balances and considering broader aspects of ethics, values and corporate culture.

In making this shift, boards not only oversee checks and balances being put in place, but also may take on direct responsibilities regarding the design of the checks and balances, especially checks and balances related to the CEO and other members of senior management. Because a number of reported ethics problems and failures in corporate controls have involved the senior-most executives, the responsibility for addressing these risks falls to a company’s board.

This article addresses the integration of board oversight and governance responsibilities along with what we believe to be the evolution from a focus on “tone at the top” to a focus on “checks and balances.” We also discuss the importance of ethics and values in corporate culture within the context of board governance.

Mandating Improved Board Oversight and Governance

Responding to widespread abuses in consumer sales practices and control breakdowns that occurred at Wells Fargo Bank over a period of several years, on February 2, 2018, the U.S. Federal Reserve Board announced consent and cease and desist orders requiring improvements in the firm’s governance and risk management processes, controls and board oversight. The orders included a restriction in the company’s growth until sufficient improvements are made. The public announcements of both the Fed and Wells Fargo confirmed the need for improvement, stating, “Within 60 days the company’s board will submit a plan to further enhance the board’s effectiveness in carrying out its oversight and governance of the company.” The Fed also criticized the job performance of the bank’s board and CEO in a press release, stating that the Fed “has sent letters to each current Wells Fargo board member confirming that the firm’s board of directors during the period of compliance breakdowns did not meet supervisory expectations. Letters were also sent to former Chairman and Chief Executive Officer John Stumpf and past lead independent director Steven Sanger stating that their performance in those roles, in particular, did not meet the Federal Reserve’s expectations.”

The Fed’s regulatory action expanded what many individuals and organizations have heretofore considered as a customary and general oversight responsibility to instead comprise a significant mandated obligation to institute procedures for enhanced oversight and governance. The action also required reporting on the same. This was no small step; however, the view that a fundamental responsibility of a governing board is to govern is not new. Retired Delaware Supreme Court Chief Justice E. Norman Veasey, in his Pennsylvania Law Review article of May 2005, stated that stockholders should have the right to expect that “the board of directors will actually direct and monitor the management of the company, including strategic business and fundamental structural changes.” Further to the point that directors have management as well as oversight responsibilities, retired Delaware Chancery Court Chancellor William B. Chandler also stated in his opinion in the 2003 Disney shareowner derivative suit, “Delaware law is clear that the business and affairs of a corporation are managed by or under the direction of its Board of Directors. The business judgment rule serves to protect and promote the role of the board as the ultimate manager of the corporation.” In a discussion of internal controls and director responsibilities on the Federal Reserve website, the Fed describes a board’s responsibility to create and enforce prudent policies and practices with the following statement: “Directors are placed in a position of trust by the bank’s shareholders, and both statutes and common law place responsibility for the affairs of a bank firmly and squarely on the board of directors. The board of directors of a bank should delegate the day-to-day routine of conducting the bank’s business to its officers and employees, but the board cannot delegate its responsibility for the consequences of unsound or imprudent policies and practices.”

Boards seeking to address expectations for enhanced oversight and governance face many challenges, among them a lack of definition of what constitutes “effective governance” in organizations. Economists have long recognized that the division of labor of a firm is specific to a firm at a point in time. Similarly, there is no single standard and no single metric for what constitutes effective governance—no common best practice, no “one size fits all” approach to follow. Just as the division of labor in an organization is unique to each organization and to each point in time, effective governance is necessarily both organization-specific and time-specific. Models and practices are useful sources of information to consider in designing governance and control structures, but there is no off-the-shelf, “one best way” for any organization. What is needed in an organization will inevitably change over time, sometimes unexpectedly and rapidly in response to a crisis or other change in circumstances.

The “Principles of Corporate Governance,” issued by the Business Roundtable (BRT), an organization of the CEOs of America’s leading companies, is one document that speaks to this reality. The following is a short excerpt from the most recent update of the Principles, issued in 2016:

“In light of the evolving landscape affecting U.S. public companies, Business Roundtable has updated Principles of Corporate Governance. Although Business Roundtable believes that these principles represent current practical and effective corporate governance practices, it recognizes that wide variations exist among the businesses, relevant regulatory regimes, ownership structures and investors of U.S. public companies. No one approach to corporate governance may be right for all companies, and Business Roundtable does not prescribe or endorse any particular option, leaving that to the considered judgment of boards, management and shareholders. Accordingly, each company should look to these principles as a guide in developing the structures, practices and processes that are appropriate in light of its needs and circumstances.”

The BRT’s Principles as well as other corporate governance references underscore the importance of each company’s senior management and board of directors devoting time and attention to designing structures, policies and processes that will provide effective governance in their organization’s unique situation. It is also important to examine and evaluate governance on an ongoing basis, especially as special events and circumstances arise. Mergers, acquisitions, takeover attempts, product failures, breakdowns in controls, lapses in ethical conduct—all these and other special conditions can arise at any time.

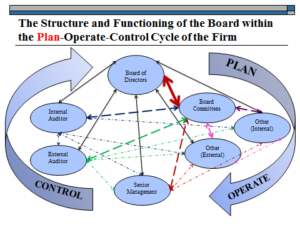

There is a very wide range of structures, functions, and players involved in considering a company’s governance and control system, as illustrated in the following diagram developed in H.S. Grace & Company’s services assisting senior management and boards of directors.

FIGURE 1

Figure 1 sets out the breadth of relationships which must be addressed by the board in formulating and activating effective corporate governance practices.[1] Once addressed, these relationships will require monitoring and updating.

Evolving from “Tone at the Top” to “Checks and Balances”

For the past several decades, corporate governance experts focused on an approach of improving the “tone at the top” out of a belief that a strong CEO setting the right tone was the best way to ensure good management practices and adequate controls throughout a company. But as failures occurred, at times involving CEOs who had ostensibly set “a right tone” in statements to employees and the general public, the limitations of such reliance became apparent. Now a distinct shift in approach is underway, focusing on a substantive set of checks and balances as essential in carrying out effective governance.

A substantive checks and balances approach addresses the roles, responsibilities, and relationships among the key elements and players in a firm’s governance, controls, and oversight system. Institutional investors, individual investors, and other market and regulatory interests increasingly demand that those involved in corporate governance recognize their responsibilities and are held accountable in addressing these responsibilities. An additional emerging expectation is that senior leaders in an organization, both board and management, recognize that a leader’s role is one of service rather than entitlement. Experience has shown that governing structures which consolidate power and authority into fewer and fewer hands, while conceptually attractive in terms of potential efficiency and effectiveness, often fail to meet conceptual ideals if individuals in power come to feel entitled to do as they please. Without effective oversight and a system of checks and balances, conditions are ripe for misconduct. In response to this reality, boards must not simply witness the implementation of the checks and balances, but also involve themselves in formulating the checks and balances and occupy active roles in the execution therein. Carrying out these active roles will necessarily lead to regular interaction with the CEO and others in senior management as well as with a company’s internal and external auditors. While tone at the top may sometimes remain only as words that do not actually affect behavior, the institution of checks and balances can exert considerable influence.

Careful inspection of what drives or underlies the effectiveness of successful organizations would indicate that over time they have put in place highly effective policies, procedures and controls. Individuals have well-defined responsibilities; the organizations make certain that individuals understand those responsibilities, and the organizations demand strict accountability. Individuals are expected to understand the organization’s mission and values and have an attitude of service. Moreover, there are well-understood consequences for falling short in discharging responsibilities, a clear measure of accountability.

Effective Governance Includes Ethics, Values, Corporate Culture

In addition to the structures, policies and processes that provide checks and balances, effective governance includes an organization’s ethics, values and corporate culture. Many problems in recent years have involved CEOs and other members of senior management. Much less often have board members been involved, but some instances of failures have occurred. Ethics problems can arise at any level; however, most corporate efforts at addressing ethical issues have seemed to involve developing broad programs for the entire organization, with limited attention being paid specifically to those at the top.

There are good business reasons to consider installing ethics programs for senior leaders—programs that are based on long-standing principles and that boards implement for themselves and senior management. In such an approach, the board would create a program and a set of expectations, then continue to monitor and periodically review the program, modifying where and when appropriate. Such programs integrate oversight and governance with ethics, values and corporate culture in a way that can enhance success of an organization.

A successful organization is attractive to prospective employees who will be the source of its intellectual capital. There is increasing recognition today that a firm’s most valuable asset is its intellectual capital. One need only look at the emergence and growth in value of innovative firms such as Google, Apple and WeWork to see evidence of the recognition accorded their intellectual capital. Although difficult to measure, intellectual capital is credited with significant portions of economic productivity increases and can play a critical role in the achievement and continuation of profitability in organizations. However, beyond the issues of profitability and monetary returns that have been traditionally sought by providers of financial capital and the owners of the physical components of production, the owners of intellectual capital —the skilled individuals who are “today’s professionals” — tend to seek to maximize their economic wellbeing via a combination of monetary and non-monetary compensation. Economic well-being is a broad concept that encompasses numerous factors affecting the overall quality of one’s life, as opposed to financial well-being, which considers only monetary compensation and the accumulation of wealth. One component of non-monetary compensation of interest to many of today’s professionals is a management culture based on ethics and values and respect, one that incorporates an attitude of responsibility, accountability, and service, as well as expertise and performance excellence.

The most effective managers of today’s intellectual capital and today’s professionals will be those who demonstrate a sense of responsibility, a willingness to be accountable, and an attitude of service. Today’s professionals tend to believe that “doing well” and “doing good” are not mutually exclusive, and that a combination of the two will result in the maximization of their individual economic well-being. Boards and management leaders who understand the difference between economic well-being and financial well-being and the complementary relationship between “doing well” and “doing good” are the most likely to be successful today. In contrast, management scenarios that are structured around entitlement or privilege are unlikely to be tolerated or sustainable. Intellectual capital is highly mobile, and individuals providing capital can exercise that mobility if management is not clear in its recognition of responsibilities, accountability, and an attitude of service.

It is interesting to note the research and insights of Robert Fogel, a Nobel laureate and one of the world’s leading economic historians. Fogel in his book, The Fourth Great Awakening: The Future of Egalitarianism in America (2000), discusses profound long-term trends in individual work habits. He points out that over the last 100 years there has been a considerable reduction in the time individuals spend in “earnwork” —that is, work associated with earning wages which in turn permits the acquisition of material possessions. He points out that what has increased is the time individuals spend in “volwork” —that is, personal time directed toward what he calls “non-material” and “spiritual” goods. Fogel found that individuals have consciously and deliberately made the decision to reduce the amount of “earnwork” and thus the material possessions they might otherwise acquire, and, instead have directed their time to family, community, religious, and other related activities. An important lesson for management that emerges from Fogel’s analysis is that as individuals seek to maximize their personal utility and personal satisfaction, not just to maximize their financial wealth, they become more cognizant of the activities from which their economic well-being springs. They see many more options and alternatives available to enable them to achieve an increased level of economic well-being. Today’s professionals look management directly in the eye. They call for management to have a comprehensive understanding of and a willingness to address responsibilities. They call upon management to be accountable, and to put in place appropriate sets of checks and balances for their own activities which will ensure accountability on the part of all the involved parties. Perhaps most importantly, they call for management to bring an attitude of service to leadership. Smart, well-trained, and mobile, today’s professionals will gravitate to working environments where management has their respect. The need for management to demonstrate an attitude of service is not surprising—one only has to recall that an attitude of service is a shared quality amongst the leaders from all walks of life who have been most widely revered and remembered.

Improving Oversight and Governance is Timely and Good Business

In furtherance of achieving and maintaining effective oversight and governance, and in the interest of earning the respect and loyalty of workers, the time is ripe for boards to focus on the ethics of management as well as the traditional focus on the ethics of the overall organization. It is both timely and good business for boards to put in place systems of substantive checks and balances that start with the CEO, senior management, and the board itself, and then proceed through the entire organization. Improving board and organizational oversight and governance can not only lower the risk of failures and problems in the organization, but can also bring sustainable operating benefits to a company and its shareholders.

In a term that seems to be touching upon the Federal Arbitration Act (the FAA) with unusual frequency, on January 15, 2019, the Supreme Court issued its second decision addressed to aspects of the FAA. In New Prime Inc. v. Oliveira, No. 17-340, the Court focused on the interpretation and application of section 1 of the FAA, which provides that the FAA does not apply “to contracts of employment or any other class of workers engaged in foreign or interstate commerce.” 9 U.S.C. § 1. The Court determined that independent-contractor truck drivers who drive interstate are covered by section 1 of the FAA and cannot be forced into arbitration by a court. Specifically, the Court addressed two issues: (1) whether it was the court or the arbitrator that must determine the applicability of section 1; and (2) whether section 1’s exemption for contracts of employment included, as a matter of law, independent contractor agreements.

Facts