In my frequent exposures to different federal judicial proceedings as a law student judicial intern in the U.S. District Court for the Southern District of New York, I have witnessed several high-profile proceedings garner heightened interest from the public and the press. During these proceedings, I sit in the courtroom gallery alongside anyone else fortunate enough to get a seat in the room. In most courtrooms, that includes around twenty members of the public and court staff, as well as twenty to thirty members of the press. All of us are barked at by court marshals and given a multitude of instructions for how to properly exist in the courtroom. Instructions including “no hats,” “no phones,” “no food,” and “no chewing gum” remind me of being a child in church. While the hearing is underway, I watch a sketch artist work quickly and tirelessly to complete as much of her sketch as possible in such a short time, capturing as many details as she can, all to have some record of what happened so it can be shared with the rest of the world. The day after the hearing ends, I see her sketches plastered all over newspapers’ websites to give a brief snapshot of what has occurred inside the courtroom.

All of these theatrics, rules, and limitations make the courtroom experience feel like Manhattan’s most secret club that prioritizes exclusivity above all. The implication of these procedures is that in courtrooms, things happen that we want to keep out of the public eye and hide away from any firsthand observers. However, I argue that a judicial system that theoretically values transparency and accountability should not function outside public observation and instead, should put resources toward creating a more accessible, public-facing court system.

A simple but impactful way that federal courts can make hearings and trials more accessible is to allow limited video camera recording in court proceedings. With the feed from court-installed cameras, courts could livestream all hearings, and news outlets could disseminate footage they deem to be of public importance after the hearings conclude. The footage could then be archived, allowing anyone to view the full recording for any reason. Removing unnecessary barriers to access in this way would build more public trust between the courts and members of the public, educate the public about what goes on in courtrooms outside of what they see on television or the internet, and give litigants greater assurance that there are people watching who are not a part of the system, providing a greater sense of accountability.

From the court’s perspective, increased accessibility would allow the public to bear witness to what occurs inside the courtroom, fostering a sense of trust from the public since the proceedings would no longer seem secretive. Although the nature of what occurs in courtrooms is potentially sensitive in nature, there is already an understanding among judges and court staff that anyone is capable of sitting in on nearly any hearing. Therefore, a video recording would hardly be any greater intrusion on the proceedings than is already possible. Further, because viewership would be less exclusive, high-profile proceedings would invite less of a circus of individuals hoping to watch the proceeding in real time, since they would be able to livestream it from anywhere. This would alleviate some of the strain on court marshals who need to control crowds for these proceedings.

From the public’s perspective, this access would offer educational, civically engaging content that is important to hear and observe. Students could watch from classrooms to gain an understanding of courtroom procedure, how lawyers work, and the day-to-day functions of the justice system. Friends and families of the parties could observe from afar and keep up with case progress. Lawyers could observe how specific judges run their courtrooms to prepare for future arguments in front of those judges. When elected officials or government entities are parties to a proceeding, members of the electorate could observe how those officials conduct themselves and what kinds of issues are at stake. If those officials are acting in a way that is unethical or unprofessional during the proceedings, people who vote for them should have the opportunity to observe that conduct.

Finally, from the parties’ perspective, this level of access would add a layer of accountability from the public to ensure that the parties’ day in court is respected. This concern is especially significant for criminal defendants who face systemic challenges to fair treatment throughout the legal process. Although hopefully it is not common, abuses of power do occur inside the courtroom. If court staff, judges, and law enforcement personnel are aware that the public and the press can observe their actions even if observers are not physically present, potential abuses of power may be prevented.

Although court proceedings are technically open to the public, there still remains a great feeling of secrecy and exclusivity. This perception is harmful to the public opinion of the judicial system, makes education and understanding of court proceedings more difficult, and can make litigants, especially criminal defendants, feel isolated and powerless. Increasing access to court proceedings would help mitigate these harmful effects, and I believe procedures to further that goal should be implemented in federal courtrooms in the future. In the meantime, I plan to inform and remind the people around me, both those who are interested in the legal field and those who are not, that they can attend court proceedings whenever they want, as long as there is room.

This article is Part VII of the Musings on Contracts series by Glenn D. West, which explores the unique contract law issues the author has been contemplating, some focused on the specifics of M&A practice, and some just random.

The adjective material is ubiquitous in business acquisition agreements. Designed to ensure that whatever is being represented or covenanted will not be deemed breached unless the impact of any inaccuracy or failure to perform is actually significant (which is itself a word that fails to convey a clear-cut standard), the word material is fraught with an uncertain meaning as applied to a particular set of circumstances.

One of my faithful readers recently asked me whether I had ever written anything about the use of the term material as a qualifier in a purchase agreement. The answer was, “Of course I have.”[1] But perhaps a reminder is necessary. Conveniently, Vice Chancellor Laster, in a recent Delaware Court of Chancery decision, In re Dura Medic Holdings, Inc. Consolidated Litigation,[2]had occasion to reiterate Delaware’s approach to determining the meaning of the word material when it is used as an adjective qualifying a covenant or representation.

It is tempting to view the word material standing alone (or as used in the phrase “in all material respects”) as having a similar meaning to the term material when used in the phrase “material adverse effect.” But legally the two have nothing to do with one another. Caselaw has declared that material when used in the phrase “material adverse effect” requires not only a truly significant (in the sense of really, really bad) negative impact, but also a negative impact that is “durationally significant.”[3] The word material standing alone or as used in the phrase “in all material respects,” however, has a different meaning. In Dura Medic Holdings, Vice Chancellor Laster reminds us:

When used to qualify a representation, the adjective “material” “seeks to exclude small, de minimis, and nitpicky issues that should not derail an acquisition.” For the breach of a representation to be material, there need only be a “substantial likelihood that the . . . fact [of breach] would have been viewed by the reasonable investor as having significantly altered the ‘total mix’ of information.” That interpretation “strives to limit [a contract term with a materiality qualifier] to issues that are significant in the context of the parties’ contract, even if the breaches are not severe enough to excuse a counterparty’s performance under a common law analysis.”[4]

In other words, a “materiality” qualifier imposes a much lower standard for measuring the significance of a breach than does the term “material adverse effect.” And it specifically serves to lessen the high bar that the common law imposes for permitting a counterparty to treat the other party’s breach as significant enough to excuse that counterparty’s own performance.

But it is far from clear how material, on the one hand, simply means more than de minimis, but on the other, means important enough to have “significantly altered the ‘total mix’ of information” upon which a counterparty relied in entering into the purchase and sale agreement. One could well wonder when a breach would not be deemed “material” as a practical matter.[5] Indeed, according to Ken Adams, one of the foremost authorities on syntactic ambiguity and contract drafting clarity generally, the word “material is not only vague but also ambiguous.”[6]

This is particularly true given the fact that the “significantly altered the ‘total mix’ of information” standard for determining materiality appears to have been borrowed from the U.S. Supreme Court decision of TSC Industries, Inc. v. Northway, Inc.[7]TSC Industries involved the determination of what was material in the context of securities fraud, specifically allegations that a proxy statement “was materially misleading.”[8] In that context, the Court held:

The general standard of materiality that we think best comports with the policies of Rule 14a-9 is as follows: an omitted fact is material if there is a substantial likelihood that a reasonable shareholder would consider it important in deciding how to vote. This standard is fully consistent with Mills’ general description of materiality as a requirement that “the defect have a significant propensity to affect the voting process.” It does not require proof of a substantial likelihood that disclosure of the omitted fact would have caused the reasonable investor to change his vote. What the standard does contemplate is a showing of a substantial likelihood that, under all the circumstances, the omitted fact would have assumed actual significance in the deliberations of the reasonable shareholder. Put another way, there must be a substantial likelihood that the disclosure of the omitted fact would have been viewed by the reasonable investor as having significantly altered the “total mix” of information made available.[9]

So—important enough to have been significant in the “deliberations” being made by the recipient of the information, but not important enough to have actually affected the decision that was made. Huh?

Adams has suggested that the “significantly altered the ‘total mix’ of information” standard is just another way of saying nontrivial, with the other understanding of material (the common-law definition) being equated to his term dealbreaker—i.e., significant enough to have actually made the counterparty not want to do the deal at all.[10] After all, the whole point of a materiality threshold is to lessen the “dealbreaker” requirement that the common law imposes for a counterparty’s contract breach to excuse the other party’s performance.[11]But that stark dichotomy between material meaning simply “nontrivial” and its common-law meaning of an actual “dealbreaker” is not what most transactional lawyers are seeking to convey with the word material. Instead, it’s something a little more than the merely “nontrivial” meaning and a lot less than the “dealbreaker” meaning.

Another faithful reader of my contract musings pointed out that “[i]n the securities fraud context, courts in [the Second] Circuit have ‘typically’ used five percent as ‘the numerical threshold . . . for quantitative materiality.’”[12] Setting aside that materiality in the securities law context also requires a qualitative analysis,[13] courts have applied the quantitative five percent rule alone in cases not involving securities fraud. Indeed, in Stone Key Partners LLC v. Monster Worldwide, Inc.,[14]the court applied that rule to determine, in a dispute over whether a financial adviser was entitled to a fee, that a sale of less than four percent of a company’s “total assets” did not constitute a “sale of a material portion of the assets or operations of the Company and its subsidiaries taken as a whole.”[15]

Five percent seems intuitively to be well past nontrivial, but well below dealbreaker status. And recall that Vice Chancellor Laster, in Akorn, Inc. v. Fresenius Kabi, AG, used a decline of more than 20 percent of the target’s equity value as sufficient to declare a material adverse effect, for purposes of a bring down condition.[16] And the material required for a material adverse effect seems closer aligned to Adams’s dealbreaker concept.[17] But is 1 percent still trivial and 2 percent nontrivial? Who knows.

So, to repeat what I have in fact said before on this subject:

If a matter will matter it may be best to recast a material liability, a material contract or a material litigation as a liability, contract or litigation involving (or that potentially could involve) [an impact of] more than a specified dollar amount [or specified percentage of equity value, net income, or assets] (below which dollar [or percentage] threshold any such liability, contract or litigation would be considered insignificant [or immaterial]). But, . . . [s]ometimes the vague, if not ambiguous, “material” is all you can get and is perhaps good enough (but at least know that the term is fraught with uncertainty).[18]

Adams, supra note 6, at 92–93 (“Because the TSC Industries standard treats a fact as material if it would have been worth paying attention to, whether or not it would have caused a reasonable investor to change their vote, it’s reasonable to equate that standard with nontrivial.”). ↑

Akorn, Inc. v. Fresenius Kabi AG, 2018 WL 4719347, at *74–76 (Del. Ch. Oct. 1, 2018), aff’d, 198 A.3d 724 (Del. 2018). ↑

See Adams, supra note 6, at 95 (“Given what’s required to establish material breach under common law, it’s reasonable to equate that standard with dealbreaker. The same goes for the IBP standard because it requires ‘a strong showing’ to invoke a MAE exception.”). ↑

Last year, the U.S. Supreme Court struck down the use of nonconsensual third-party releases in Chapter 11 reorganization plans as not authorized under the Bankruptcy Code.[1] While the Harrington v. Purdue Pharma decision involved mass tort liability, the broader curtailment of third-party releases in all contexts should cause directors and officers to reevaluate their personal liability exposure when companies enter the zone of insolvency.

Prior to Purdue, Chapter 11 plans routinely featured broad third-party releases in favor of the debtor’s directors and officers, insulating those individuals from any and all claims associated with the conduct of the business prior to and during the bankruptcy proceeding. The new Purdue prohibition on nonconsensual third-party releases underscores the need for robust risk-management strategies, including comprehensive directors’ and officers’ (“D&O”) liability insurance coverage, to effectively protect boards and executives from personal exposure.

This article explores common claims against directors and officers, including claims likely to arise in the event of corporate insolvency, and addresses best practices for mitigating liability risk in insolvency situations, particularly key D&O policy provisions.

Common Claims Arising from Insolvency

Companies and the people who run them are always subject to new and emerging risks. When a company approaches insolvency or seeks formal court protection from creditors, the actions of the directors and officers before and during such period become subject to even closer scrutiny by the company’s stakeholders. Claims can come from shareholders, lenders, court-appointed trustees or receivers, and individual creditors or creditor committees, to name just a few. It is common for such stakeholders to investigate the conduct of the company’s directors and officers—and to attempt to have the company incur the cost of such investigation—and to pursue a variety of claims if warranted by the results of the investigation. Such claims can take many forms.

Securities Claims

Securities claims against directors and officers can arise from alleged violations of federal or state laws that regulate the issuing, trading, and handling of securities. These claims typically involve allegations of fraud related to the sale of securities, insider trading based on nonpublic information, or failure to comply with disclosure requirements.

Modern D&O policies contain a broad range of protections for both the company (under so-called “Side C” or entity, coverage) and individuals (“Side B” or “Side A,” depending on whether the company indemnifies them) in the event of alleged securities violations. This is particularly crucial during insolvency or bankruptcy, as the company’s ability to indemnify may be impaired due to financial constraints or prohibited by bankruptcy law.

Fiduciary Duty Claims

Directors and officers can also face exposure from derivative suits for alleged self-dealing, corporate waste, failure to act in good faith, or failure to protect the interests of creditors or other stakeholders. These types of claims involve allegations that directors and officers breached their fiduciary duties to the company or its stakeholders in a way that financially harmed the company or diminished the value of its assets.

If directors or officers are accused of mismanagement leading to insolvency, Side A coverage could provide protection for individual directors and officers, even if the company cannot indemnify them due to its bankruptcy status. Additionally, fiduciary liability insurance, sometimes included within D&O policies, may protect directors and officers from claims related to the mismanagement of employee benefit plans, such as pension plans.

The above examples are merely illustrative and do not tell the full picture of potential claims, which also include things like mismanagement that deepens insolvency, fraudulent trading and transfers, and a host of other alleged fiduciary, tort, and statutory violations implicating conduct by individuals.

D&O Risk-Mitigation Tips

While the goal of protecting individual directors and officers is straightforward, securing adequate executive protection in a post-Purdue world can be complex. Below are several risk-mitigation considerations that can be implicated before, during, and after bankruptcy proceedings.

Evaluating Policy Exclusions

D&O policies contain several exclusions that could be implicated in insolvency situations.

The most problematic for companies facing insolvency are bankruptcy or insolvency exclusions, which may be added to policies when a company faces financial distress and can bar directors and officers from accessing D&O coverage during bankruptcy. While rare, these exclusions can significantly limit or eliminate coverage. If the exclusion cannot be avoided, insureds should attempt to limit its scope during the underwriting process.

Another exclusion implicated in bankruptcy is the “insured versus insured” exclusion, which bars coverage for claims brought by or on behalf of one insured against another insured. Issues can arise in bankruptcy when a trustee or creditor committee asserts claims against a director or officer on behalf of the debtor. Without appropriate carveouts to this exclusion, claims may be denied because these claimants are acting on behalf of the debtor company—an insured—against directors or officers, who are also insureds. Negotiating appropriate exceptions to this broad exclusion can protect coverage in the event of bankruptcy.

Insolvency-related claims against directors and officers may also implicate so-called conduct exclusions for deliberate criminal, fraudulent, or dishonest acts. Allegations of reckless or intentional conduct, even if baseless, can pose significant obstacles to advancing legal fees if the exclusion does not have appropriate “final adjudication” language, which can preserve coverage until the offending conduct is established by a final, nonappealable adjudication. As with most D&O policy provisions, exclusionary language is not one-size-fits-all and varies materially among insurers, forms, and endorsements, so policyholders must pay close attention to variations in wording that can have an outsize impact on coverage.

Understanding Runoff Coverage

The time to think about D&O insurance is before potential insolvency proceedings. One important aspect to vet in advance of bankruptcy is the availability and scope of a potential extended reporting period that may be available to the company to report claims in the event coverage is terminated during bankruptcy.

Preserving the ability to report claims—via what is often referred to as “tail” or “runoff” coverage—ensures that directors and officers are protected against claims if the company undergoes a change in ownership or management control during bankruptcy. Without runoff coverage, directors and officers would no longer have access to D&O insurance to defend against claims for actions taken during their tenure. This is important because claims might take time to surface as the bankruptcy process unfolds, or stakeholders may file claims even after the company’s operations end.

Securing Dedicated Side A Coverage

Traditional D&O policies include coverage for both the company and its directors and officers, usually subject to the same set of limits. That means that claims against the company may deplete or extinguish limits that otherwise would be available to protect directors and officers.

In most circumstances when the company is solvent, that structure is not problematic because even if the D&O insurance limits are extinguished, directors and officers can still count on the company to advance their legal fees and indemnify them in connection with claims arising from the decisions made on behalf of the company. In insolvency situations, however, that backstop of advancement and indemnity from the company is gone because the company is not able to pay, leaving D&O insurance as the sole protection for directors and officers facing personal exposure.

For that reason, policies should include dedicated Side A coverage, which sets aside separate limits available solely to protect individual directors and officers when an insolvent company is unable or unwilling to do so. Additional Side A limits are often available as part of the traditional “Side ABC” policy but can also be purchased via a stand-alone Side A–only policy, which can provide additional benefits like broader coverage and fewer exclusions. Finally, bankruptcy courts have held that Side A policy proceeds are not the property of the debtor’s estate.[2] Therefore, the ability of directors and officers to access Side A policy proceeds is not constrained by the automatic stay, providing additional benefits to individuals who need to access that coverage quickly and efficiently to avoid being personally exposed.[3]

Relying on Subcommittees and Outside Examiners

The formation of subcommittees chaired by independent directors or the hiring of outside examiners to evaluate potential claims is an effective strategy for proactively identifying and addressing directors’ and officers’ exposure. These pre-bankruptcy investigations can include a review of existing insurance policy provisions, decisions of directors and officers leading up to insolvency, and analysis of potential claim exposure.

By assessing the potential existence of claims at an early stage, companies can take steps to implement mitigation measures as necessary to minimize exposure to those claims. And the involvement of an outside examiner or independent board member can enhance the credibility of the investigation given their independent and unbiased position. In the event of subsequent litigation, this proactive approach can lay the groundwork for a successful defense through the documentation of key facts concerning D&O actions leading up to bankruptcy.

Implementing Consensual Release Agreements/Plans and Litigation Trusts

The above-described proactive liability-management strategies are best practices to mitigate D&O liability, but in the event of a bankruptcy, additional measures may be required to address potential D&O claims, which may require companies to navigate the issues in Purdue. For example, consensual third-party releases and litigation trusts are tools available for addressing personal liability in bankruptcy court.

Consensual Third-Party Releases: RSAs and Opt-In/Opt-Out Releases

A restructuring support agreement (“RSA”) is a prepetition agreement that a company reaches with its key stakeholders regarding restructuring terms. In exchange for stipulated economic treatment, RSAs can require the stakeholders to agree to third-party releases as part of a bankruptcy plan. These releases differ from those prohibited by Purdue because they are consensual. As a result, the utility of an RSA release turns largely on the company’s organization and the type of liability that directors and officers face.

For certain companies with a few key constituents with potential claims, an RSA that includes a third-party release provision is an effective liability-management strategy. For other companies with many third parties with potential claims, negotiating consensual releases may be untenable. And regardless of a company’s structure, RSA releases are not usually a realistic strategy for addressing mass tort liability, such as in Purdue, due to the massive number of claimants. In those instances, companies may try to obtain consensual releases through plan voting.

Since Purdue came down, litigation has ensued regarding whether “opt-in” and “opt-out” releases in bankruptcy plans constitute consent as part of the plan voting process. Opt-in releases require the releasing party to affirmatively consent to the release. Opt-out releases assume consent to the release unless the releasing party affirmatively opts out. Some courts have held that opt-out releases are acceptable in limited circumstances, depending on the specific facts and circumstances of the case.[4] The Bankruptcy Court for the Southern District of Texas has gone further, approving a plan containing an opt-out release because opt-out consent has long been standard practice in the district.[5] However, the U.S. trustee appealed the confirmation order in In re Container Store Group, Inc., setting the stage for the next potential Supreme Court bankruptcy release battle.

Litigation Trusts

Where consensual releases do not fully address D&O liability, litigation trusts are an additional option. Litigation trusts are created as part of a bankruptcy plan and channel claims of the estate (i.e., derivative claims of shareholders) into the hands of a litigation trustee to pursue on behalf of the estate. While this tactic does not release directors and officers from personal liability, it does make litigation and settlement negotiations efficient given that the trustee has the sole authority to pursue the channeled claims.

Conclusion

As the contours of Purdue continue to unfold, companies should proactively monitor developments in the law to avoid surprise coverage denials, large exposures, and similar issues that arise when a company enters the zone of insolvency. Engaging experienced professionals, such as insurance brokers and outside bankruptcy and coverage counsel, can help establish robust risk-mitigation measures and insulate directors and officers from personal liability.

Harrington v. Purdue Pharma L.P., 603 U.S. 204 (2024). ↑

See, e.g., In re Downey Fin. Corp., 428 B.R. 595 (Bankr. D. Del. 2010); In re Petters Co., 419 B.R. 369 (Bankr. D. Minn. 2009); In re MILA, Inc., 423 B.R. 537 (B.A.P. 9th Cir. 2010). ↑

This article provides a high-level overview of approaches to ESG disclosures in the United States, European Union, and United Kingdom, noting the implications of these differences for investors and global businesses. Beyond shedding more light on the general ESG regulatory landscape under these regimes, the article explores the emerging ESG regulatory frameworks and policy drivers for ESG on both sides of the Atlantic and delves further into the implications of these differences to investors and multinational corporations, and why companies should care about these regulatory requirements and differences.

What Is ESG and ESG Disclosure?

ESG, which stands for “environmental, social, and governance,” refers to metrics often used by analysts to evaluate and vet the non-financial sustainability impact and social consciousness of companies. These metrics can impact a company’s risk profile and public perception—and, ultimately, the bottom line.

“ESG disclosures” are specific metrics used by organizations to report on their ESG performance and initiatives. ESG disclosures are generally broken into three categories:

Environmental: focuses on climate risks, emissions, energy efficiency, use of natural resources, pollution, and biodiversity

Social: focuses on human capital; labor regulations; diversity, equity, and inclusion (“ DEI”); safety; human rights; and community engagement

Governance: focuses on board diversity, corruption and bribery, corporate ethics and compliance, compensation policies, and risk tolerance

The terms ESG disclosure, sustainability report, and corporate social responsibility report are often used interchangeably.

Overview of the ESG Disclosure Regimes in the US

Federal Government

ESG disclosure in the United States (“US”) remains largely voluntary, except for the state of California’s requirements, discussed below. Governmental agencies and shareholder activists, however, continue to advocate for mandatory ESG disclosure. On March 6, 2024, the US Securities and Exchange Commission (“SEC”) adopted climate-related disclosure rules, two years after publishing the proposed rules.[1] Shortly thereafter, on April 4, 2024, the SEC stayed its climate disclosure rules following a flurry of lawsuits by many stakeholders challenging both the rules and the SEC’s authority to issue the rules.[2] A total of forty-three states (twenty-five against and eighteen advocating for the SEC rules as intervenors), as well as interest groups and trade associations, have since filed their petitions for review across different appellate courts, which are now consolidated in a multidistrict litigation in the U.S. Court of Appeals for the Eighth Circuit, dubbed Iowa v. Securities & Exchange Commission.[3] Many opponents to the SEC’s ESG disclosure rules argue that following the Loper Bright decision[4] by the US Supreme Court, which overturned the long-standing Chevron deference doctrine,[5] the SEC lacks authority under federal securities laws to require corporate reporting of greenhouse gas emissions and other climate disclosures. This case remains in litigation and the rules are stayed. In any event, many experts believe that the Trump administration will abandon the rules.[6]

State of California

In 2023, the state of California enacted Senate Bill 253 (“SB 253”) (“Climate Corporate Data Accountability Act”) and Senate Bill 261 (“SB 261”) (“Greenhouse Gases: Climate‐Related Financial Risk”) as part of the Climate Accountability Package. These laws are applicable to both public and private US companies “doing business” in California.[7]

Senate Bill 219 (“SB 219”) was proposed and signed into law on September 27, 2024, amending the Climate Accountability Package by granting the California Air Resources Board (“CARB”) time and discretion to adopt implementing regulations and clarify answers to key implementation questions. While SB 219 extended CARB’s implementation date from January 1, 2025, to July 1, 2025, it does not offer an extension of the date of first reportable data under SB 253 for Scope 1 and Scope 2 emissions, which remains January 1, 2025.[8] This means that US entities required to report under SB 253 may still have to collect Scopes 1 and 2 data for the first half of 2025 and include this in their first report to CARB, due by January 1, 2026.

On December 5, 2024, CARB issued an enforcement notice indicating its intent to exercise “discretion” in enforcing SB 253 during the first 2026 reporting cycle to allow companies additional time to implement data collection necessary to comply with the reporting requirements.

Shortly thereafter, on December 16, 2024, CARB issued a feedback solicitation inviting public comments on the implementation of SB 253 and SB 261, due by February 14, 2025.

Overview of the ESG Disclosure Regimes in the EU and the UK

Prior to 2023, only a relatively small number of large companies (referred to as public-interest entities)[9] within the European Union (“EU”) were required to disclose ESG information under the Non-Financial Reporting Directive (“NFRD”), which came into force in December 2014. Work to substantially expand the scope of the NFRD started in 2017 on the heels of the 2016 COP21 Paris Agreement.[10] In January 2023, the Corporate Sustainability Reporting Directive (“CSRD”) came into force.[11] However, please note our commentary below in relation to changes being proposed to the CSRD.

The CSRD is a mandatory ESG disclosure framework that modernizes and strengthens ESG reporting, requiring companies to report on environmental and social impacts, risks, and opportunities. EU member states were required to transpose the CSRD into domestic legislation by July 6, 2024; however, some countries have not yet done so (e.g., Germany, the Netherlands, and Spain).

The CSRD is broad and reaches a much wider group of companies compared to the NFRD, including some listed small and medium-sized enterprises (“SMEs”); certain non-EU issuers; and non-EU parent companies that generate over EUR 150 million in the EU and have at least one large subsidiary, public interest SME (see definition of public-interest entities in note 9), or branch in the EU. It requires businesses to report and disclose information on their societal and environmental impact and external sustainability factors affecting their operations.

A key feature of the CSRD is the double materiality assessment (“DMA”). The materiality of risks is reportable on two fronts: (1) how sustainability issues may affect the company and (2) how the company may impact people and the environment. The concept of DMA is yet to be established, with no proven or approved methodologies. This is causing some confusion in the marketplace and has been a source of criticism.

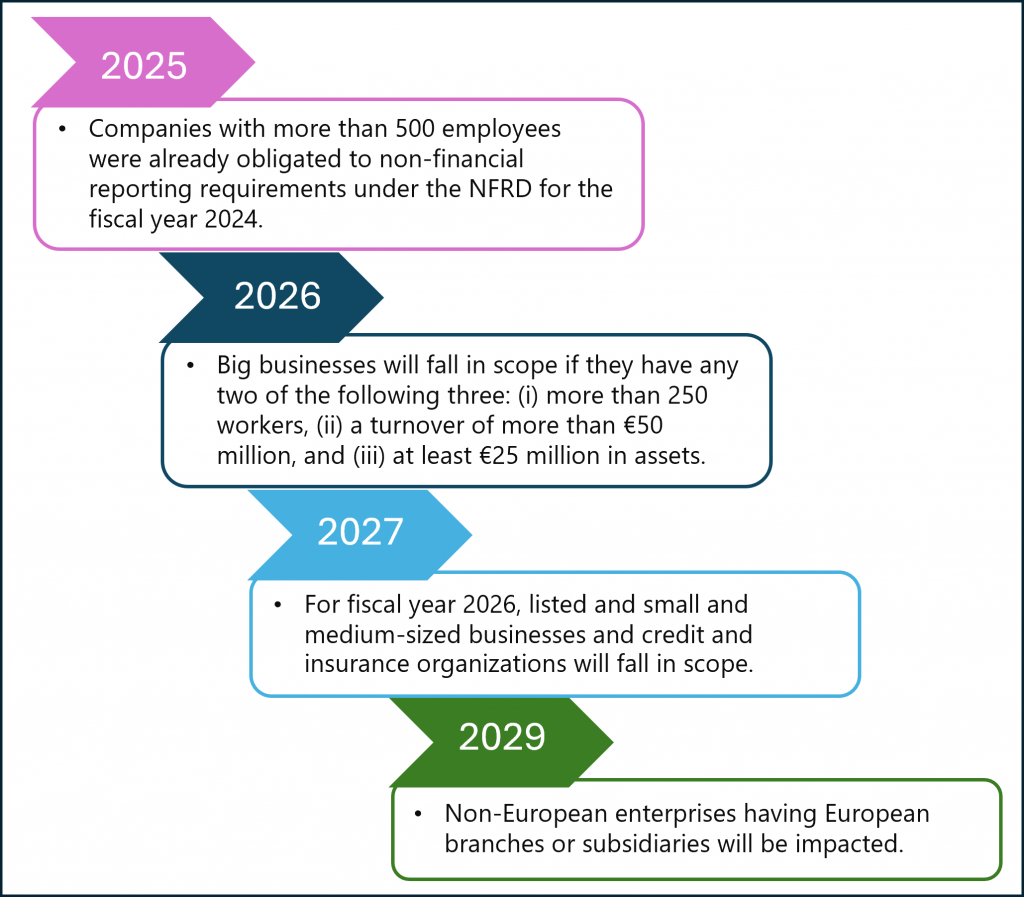

Implementation of the CSRD is a phased-in approach, with a rolling timeline (see figure 1). Companies already reporting under NFRD and large issuers with more than 500 employees are required to submit their ESG disclosures under CSRD in 2025, covering FY 2024. Other “large” EU companies or corporate groups (which includes those with two of the following three: (a) EUR 50 million+ in net turnover, (b) EUR 25 million+ in assets, and (c) 250+ employees) are required to submit initial ESG disclosures in 2026, covering FY 2025. Finally, all non-EU ultimate parent companies with “large” EU subsidiaries or operative branches are required to submit their initial ESG disclosures in 2029, covering FY 2028.

Figure 1. Timeline of Implementation of the CSRD.

Upstream of reporting, certain companies (including non-EU businesses) will be required to comply with the EU Corporate Sustainability Due Diligence Directive (“CSDDD”). This regulatory framework provides a process for mapping and conducting an in-depth assessment of a company’s operations and its chain of activities in order to (i) identify and prioritize actual and potential impacts based on the severity and likelihood of occurrence, (ii) prevent potential adverse impacts through an action plan with “reasonable and clearly defined” timelines, and (iii) end any actual adverse impacts by minimizing the impact with corrective action plans.[12] The CSDDD has regulatory enforcement requirements and civil liability for violations.

It is important to note that on February 26, 2025, the European Commission published an “Omnibus package” (“Omnibus”)[13] that seeks to simplify and streamline the requirements under the CSRD, the CSDDD, and the EU Taxonomy Regulation.

Some of the key proposed changes to CSRD include introducing a two-year delay to the reporting requirements applicable to “large” EU companies (from FY 2025 to FY 2027, with the first reports due in 2028 rather than 2026) and amending the thresholds applicable to in-scope EU companies (the reporting requirements would only apply to entities with more than one thousand employees either at the individual or group level and with either (a) EUR 50 million or more in net turnover or (b) EUR 25 million or more in assets). The Omnibus also proposes changes to the thresholds applicable to non-EU ultimate parent companies with “large” EU subsidiaries or operative branches.

The Omnibus also includes changes to the CSDDD, which affect scope and timeline of reporting, as well as potential removal of the requirement for EU member states to introduce civil liability for violations.

It is still unclear whether the changes proposed by the Omnibus will be adopted and what the timing of that would be, although the European Commission has invited EU institutions to treat this matter as a priority in light of the upcoming compliance deadlines under the CSRD.

In the United Kingdom (“UK”), there are also mandatory ESG reporting requirements that apply to certain in-scope companies. Since 2019, listed companies and large companies have been required to disclose energy use and carbon emissions under the Energy and Carbon Report Regulations 2018[14] (“Streamlined Energy and Carbon Reporting” (“SECR”)). Listed companies are required to make disclosures aligned with the Task Force on Climate-Related Financial Disclosures framework. For accounting periods starting from April 2022, the Companies Act 2006 has required UK high-turnover companies with more than 500 employees, as well as traded insurance and banking companies, to produce a non-financial and sustainability information statement as part of their strategic report.

Looking ahead, the UK government is considering whether to introduce new sustainability disclosure requirements (“SDR”) on companies under a new reporting regime based on the standards issued by the International Sustainability Standards Board (“ISSB”), as well as a requirement for certain entities to publish climate transition plans. As these new regimes are still being developed, UK and non-UK entities will need to consider the extent to which any changes will affect their reporting obligations. Alongside the new disclosure requirements, the UK is also developing its own UK Taxonomy Framework for determining which activities can be considered “environmentally sustainable.”

Table 1, below, compares the main reporting frameworks in the EU and the UK.

Table 1. Main Reporting Frameworks in the EU and UK

Streamlined Energy and Carbon Reporting (“SECR”) regulations

Corporate Sustainability Due Diligence Disclosure Directive (“CSDDD”)

Sustainability Disclosure Requirements (“SDR”) and standards aligned with the International Sustainability Standards Board (“ISSB”) (to be confirmed)

Comparing the Disclosure Regimes in the US and the EU/UK

While the topics addressed by ESG regulations vary across regimes, they all include a focus on greenhouse gas emissions and other climate-related matters. It is important to recognize that reporting beyond climate topics—such as biodiversity, pollution, and certain workforce metrics—is also typically required. The reporting frameworks require a description of how risks are identified and managed, as well as corporate board oversight of identified risks. The identification of the applicable risks is fundamental and is an area where it is particularly essential to create a cross-functional approach.[16]

The most significant differentiators between the US and EU/UK disclosure approaches are the “scope and scale” of disclosures and the definition of materiality.

First, with respect to scope and scale, the CSRD covers a broad range of topics and applies to a wide group of entities, including large companies, non-EU parents of large EU subsidiaries, and certain listed SMEs operating in the EU (although this may be subject to change if the Omnibus is adopted). On the other hand, the SEC’s disclosure rules focus specifically on climate-related information, particularly climate-related risks and Scope 1 and 2 emissions, and are applicable to both registered US domestic issuers and foreign issuers. Note, however, that California’s ESG reporting requirements also include Scope 3 emissions disclosure.

Second, the meaning of materiality in each regime is critical since it determines reportability. An incorrect interpretation or an invalid assessment of materiality could be very expensive and detrimental, triggering hefty fines and sanctions. The CSRD applies a double materiality approach, which requires companies to report on how sustainability issues affect their business and how their business impacts society and the environment. The SEC rules focus solely on financial materiality, requiring companies to disclose information that is material to investors. California’s laws require extensive emissions reporting irrespective of materiality.[17]

Conclusion: The Transatlantic Divide and Why Global Companies Should Care

While ESG disclosures in the EU are mandatory, reporting in the US remains voluntary, with the exception of California’s requirements. As such, compliance with evolving ESG disclosure requirements will become more complex for global public companies. In particular, private equity funds and traditional energy players that have an increased interest in energy transition to meet stakeholder demands and regulatory changes will continue to wrestle with varying ESG reporting requirements. These critical interests are coupled with the challenges of addressing escalating climate change risks and supplying the world’s insatiable energy demand. The combination of these factors in a fast-paced business arena presents a ripe environment for ESG-related claims.[18] With more disclosure requirements and a lack of standardization across global jurisdictions, it is likely that there will be more missteps. Noncompliance with the reporting requirements in the applicable jurisdiction(s) may be fatal to potential ventures, investment opportunities, and the public perception of involved parties.

Companies, advisers, funds, and counsel should carefully curate their reviews, vetting, and setting of ESG targets to ensure alignment with required ESG and sustainability reportable information across regimes, while at the same time ensuring alignment with other investment materials, offering documents, and annual reports. In addition, disclosures should be vetted by external experts and legal counsel to ensure consistent, reliable, and accurate reporting.

See Press Release, U.S. Sec. & Exch. Comm’n, SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors (Mar. 6, 2024). The SEC disclosure rules—aimed at reducing greenwashing, increasing transparency for investors, and standardizing and harmonizing reporting metrics across all industries—were intended to be effective beginning with the year ending December 31, 2025, and would require disclosure by public companies to include governance issues, risk management strategies, and financial implications of climate-related risks. ↑

See U.S. Sec. & Exch. Comm’n Order Issuing Stay, In re Enhancement and Standardization of Climate-Related Disclosures for Investors, File No. S7-10-22 (Apr. 4, 2024). The SEC disclosure rules were stayed in April 2024 following challenges by several states, investors, interest groups, and trade associations. ↑

Loper Bright Enters. v. Raimondo, 144 S. Ct. 2244 (2024) (providing that courts should use their own judgment when interpreting ambiguity in laws and not rely on agency interpretations). ↑

Chevron U.S.A., Inc. v. Nat. Res. Def. Council, 467 U.S. 837 (1984) (providing that courts were to give deference to agencies where there was ambiguity in the law, as long as the interpretation was reasonable). This case has since been overturned. ↑

See S. 253, 2023 Leg., Reg. Sess. § 1(l) (Cal. 2023); S. 261, 2023 Leg., Reg. Sess. § 1(j) (Cal. 2023). Signed into law in 2023, SB 253 and SB 261 establish greenhouse gas emissions and climate-related financial risk reporting requirements for corporations that meet certain criteria. SB 253 (greenhouse gas emissions disclosure) tasks the California Air Resources Board (“CARB”) with promulgating regulations requiring US-based entities with $1 billion or more in annual revenue to report their greenhouse gas Scope 1 and Scope 2 emissions for 2025 by January 1, 2026, and Scope 3 emissions starting in 2027 for emissions for 2026. SB 261 (climate-related risks reporting) applies to companies with total annual revenues over $500 million and mandates disclosure of climate-related financial risks and measures for risk reduction. ↑

See S. 219, 2024 Leg., Reg. Sess. § 1(c) (Cal. 2024). SB 219 gives CARB six additional months to finalize its rules under SB 253, pushing the CARB implementation deadline to July 1, 2025. Additionally, SB 219 eliminates the filing fee requirement for corporations reporting their greenhouse gas emissions, gives CARB the option (but not the requirement) to contract with an outside organization to develop a program by which the required disclosures would be made public, and authorize any corporate disclosures to be consolidated at the parent company level. ↑

These are defined as EU entities with transferable securities admitted to trading on an EU-regulated market, certain credit institutions, insurance undertakings, or other entities designated as such by EU member states. ↑

The Paris Agreement is a legally binding international treaty on climate change. It was adopted by 196 parties at the UN Climate Change Conference (COP21) in Paris on December 12, 2015, and entered into force on November 4, 2016. ↑

By the end of 2025, more than half of the largest 30 U.S. accounting firms will have either sold an ownership stake or part of their business to private-equity investors, up from zero in 2020, said Allan Koltin, chief executive at advisory firm Koltin Consulting Group.

—Mark Maurer, “Private Equity’s Ties to Companies’ Auditors Have Never Been Closer. That Worries Some Regulators.”[1]

Persistent market volatility, high inflation levels, and lack of investor confidence have challenged, among other things, mergers and acquisitions processes and the debt capital markets over the past few years. Private equity sponsors have responded in part by seeking to penetrate new sectors for platform acquisitions. Professional services firms have become one such target, driven by large profit margins, sustained growth, and strong cash flows. This article focuses on accounting firms, a subset of professional service providers and a popular target of sponsored investment via leveraged buyout (or “LBO”). As competition to acquire quality assets and accordingly, provide related financing, remains fierce, this article will discuss material considerations for lenders in connection with the financing of audit and accountancy businesses.

A Rising Trend

According to S&P Global, November 2024 “saw a surge” in private equity– and venture capital–backed transactions in the accounting and audit sector.[2] In fact, in the period from October 1 through November 30, 2024, seven deals were done in the sector, compared to six deals for the entire fourth quarter of 2023.[3] By way of further example, according to the Financial Times, in 2024 alone, Hellman & Friedman agreed to purchase a controlling portion of the equity interests in Baker Tilly; New Mountain Capital purchased the U.S. operations of Grant Thornton; Investcorp and PSP Investments purchased PKF O’Connor Davies; and a Centerbridge Partners–led consortium of investors purchased a majority of equity in Carr, Riggs & Ingram.[4]

Attractive Targets

Accounting firms are attractive targets for private equity investment for several reasons. The “fragmented”[5] character of the professional accounting industry presents consolidation opportunities as well as the potential to scale business, a hallmark of private equity’s investment thesis. Furthermore, private equity sponsors may be able to strategically acquire and roll up current and future targets, often centralizing shared services and functions, thereby lowering costs and maximizing profits, which, in turn, ultimately maximizes limited partner returns. Accounting firms’ business is also fairly reliable and stable, usually with predictable income streams and the potential to expand into advisory services to augment profits.[6] Some industry observers predict private equity investment in the accounting sector may allow firms to deploy capital into new areas like enhanced technology and artificial intelligence, each of which theoretically might, consequently, promote consistency, efficiency, and lower costs.[7]

Top Three Considerations for Lenders and Their Counsel

In light of popularity of accounting and audit firm acquisitions, we offer the following top three considerations for lenders considering financing the same: (1) structuring, (2) auditor independence and regulatory considerations, and (3) management services agreements (“MSAs”) and/or administrative services agreements (“ASAs”).

1. Structuring

The alternative practice structure is ideal for businesses looking for external investment. Firms governed by alternative practice structure regimes are typically split between the advisory arm (“AdvisoryCo”) and the accounting business (“AttestCo”). Under a credit facility, AdvisoryCo is usually the borrower and AttestCo is a non-guarantor restricted subsidiary. It is therefore crucial for lenders and their counsel to appreciate how transactions between AdvisoryCo and AttestCo are governed and what rights and restrictions apply to targets’ partners and/or employees.

Importantly, accounting firm employment and partnership agreements often contain non-compete, non-solicitation, mandatory retirement, and other similar restrictions on partners and employees. As alternative practice structures may vary from firm to firm, a thorough review of relevant partnership and employment agreements, operating agreements, and other governing documents should be undertaken—most crucially, the MSA and/or the ASA (discussed below).

2. Auditor Independence

Accounting firms are typically subject to the U.S. Securities and Exchange Commission’s (“SEC”) and Public Company Accounting Oversight Board’s auditor independence rules and other similar regulations. Due to the broad reach and scope of such rules, financing arrangements may impair independence. Company and sponsor’s counsel should conduct a thorough independence analysis and confirm no issues; lenders’ counsel should expressly inquire about this during legal diligence. Lenders should push for credit agreement representations and warranties to the effect that the financing transaction does not violate the SEC’s Rule 2-01 under Regulation S-X or other applicable laws, as it may be detrimental to the underlying financing to have AdvisoryCo deemed an “associated entity” of AttestCo.

3. MSAs/ASAs

Alternative practice structures and the two entity silos are governed via MSAs or ASAs. The MSA or ASA, as applicable, spells out the agreements between AdvisoryCo and AttestCo. For example, such agreements will provide that AttestCo provides only accounting services and that AdvisoryCo provides—importantly, for a fee—administrative and “back-office” services to AttestCo (think personnel management, information technology and other tech services, billing and accounts, and so on).

It is imperative that lenders and their counsel obtain, review, and understand the relevant MSA or ASA. Key focus areas of such review include the following:

Fee for services: What is the scope of the fee and related services? When is such fee paid?

Termination fee: To which party is it payable? Are there any exclusions to payment of such fee?

Because MSAs/ASAs are key strategic assets of AdvisoryCo borrowers, credit agreement provisions should be tailored accordingly. For example, lenders should consider appropriate representations and warranties as to the effectiveness of MSAs/ASAs, fulsome events of default for termination of MSAs/ASAs, and a covenant restricting modifications of MSAs/ASAs adverse to the interests of the lenders. Lenders may also wish to consider restrictions on transferring MSAs/ASAs outside the ring-fenced loan party group and include reporting requirements.

Conclusion

As accounting firm LBO financings become increasingly commonplace, the body of relevant credit documentation that may serve as precedent for future transactions is growing. Sponsors, wishing to preserve their forms and ensure consistency across their portfolio companies, may resist bespoke constructs. Yet, lenders must be wary of cookie-cutter approaches and not lose sight of the fact that accounting firms (and other professional services firms) are no ordinary targets. Credit documentation must be diligently negotiated and be grounded in a firm understanding of the often-complex corporate and partnership structures and complex web of regulations to which each unique accounting firm is subject.

Mark Maurer, Private Equity’s Ties to Companies’ Auditors Have Never Been Closer. That Worries Some Regulators, Wall St. J. (Oct. 30, 2024). ↑

Shortly following his inauguration in January, President Donald J. Trump signed a flurry of executive orders implementing a wide array of administration policies. One of the executive orders, entitled “Ending Illegal Discrimination and Restoring Merit-Based Opportunity” (“DEI EO”), is designed to ban both public- and private-sector programs encouraging diversity, equity, and inclusion (“DEI”). Another, entitled “Ending Radical and Wasteful Government DEI Programs and Preferencing” (“EJ EO”), terminates environmental justice programs within the executive branch and targets federal contractors and grant recipients that advance DEI and environmental justice by instructing each federal agency to “terminate, to the maximum extent allowed by law, all . . . ‘equity-related’ grants or contracts.”

Shortly following her confirmation by the U.S. Senate, on February 5, Attorney General Pam Bondi issued a pair of memoranda to U.S. Department of Justice (“DOJ”) personnel, directing the Department to eliminate internal practices related to DEI and environmental justice and directing various elements of the DOJ to “investigate, eliminate, and penalize” private companies and universities (including nonprofits) that have “illegal” DEI programs. She instructed DOJ officials to enforce federal civil rights laws to abandon what she called “illegal discrimination and preferences,” outlining strategies such as launching criminal and civil investigations. These directives were issued to implement the president’s earlier executive orders.

While the concepts of these executive orders and DOJ enforcement memoranda were not surprising, given widespread criticism of DEI and other programs considered “woke” by the political right, the text of the directives surprised many with their explicit mentions of private sector and nonprofit organizations, many of which have long-established programs dedicated to DEI efforts. Some others are organized with DEI as a central tenet or purpose. The new directives have raised many concerns among nonprofit executives about the legality of both legacy and emerging DEI efforts and the status of their organizations’ funding secured through federal grants, cooperative agreements, contracts, and loans.

At a minimum, these directives signal the administration’s intent to pressure private-sector organizations regarding their DEI practices. A more expansive view of them foreshadows an aggressive effort to challenge DEI programs through lawsuits and regulations targeting organizations perceived as ideological and political enemies of the current administration and its policies.

Of immediate concern to many nonprofit recipients of federal grants, cooperative agreements, and contracts are the requirements in the DEI EO for such recipients to affirmatively certify that their organization (i) “does not operate any programs promoting DEI that violate any applicable Federal anti-discrimination laws” and (ii) is in compliance with all federal anti-discrimination laws that are “material to the government’s payment decisions for purposes of” establishing federal False Claims Act liability.

Executive orders carry the force of law. They are legally binding and can be enforced, both within the executive branch and against other entities. Executive orders traditionally carry out existing powers of the president and implement existing law, rather than creating new law, and often dictate how the executive branch will operate by directing departments and agencies to carry out certain initiatives. Given the executive branch’s vast bureaucracy and spending, executive orders have traditionally been a powerful policymaking tool for presidents to test or implement new economic and social policy. Executive orders are subject to judicial review by federal courts and can be revoked by the sitting president (including successors).

DEI Executive Order

The January 21 DEI EO’s stated purpose is to end “pernicious discrimination.” It directs federal departments and agencies to terminate “all discriminatory and illegal” DEI programs and practices and declares that DEI programs and practices are illegal” and “dangerous.” Both the executive orders and the DOJ directives contain cursory citations to the federal Civil Rights Act of 1964 and the U.S. Supreme Court’s 2023 decision in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College as supporting the conclusion that DEI programs, broadly speaking, are illegal.

Notably, the DEI EO and the DOJ directives also took aim at DEI efforts in the private sector, attempting to extend the order’s reach beyond the typical province of executive orders of federal agencies and federal award recipients. The DEI EO directed agency heads to “take all appropriate action” to “advance in the private sector the policy of individual initiative, excellence, and hard work.” The order directs federal agencies to submit recommendations for enforcement of civil rights laws, including by identifying “discriminatory DEI practitioners” and by recommending investigations and potential litigation related to DEI programs of “publicly traded corporations, large non-profit corporations or associations, foundations with assets of 500 million dollars or more, State and local bar and medical associations, and institutions of higher education with endowments over 1 billion dollars.” The explicit reference to nonprofit organizations and associations has generated concern among nonprofit and association executives, and a rush to evaluate whether any DEI practices could be considered “discriminatory.” One of the DOJ directives similarly directed DOJ’s Civil Rights Division to recommend enforcement actions and “other appropriate measures to encourage the private sector to end illegal discrimination and preferences.” Among the recommendations the attorney general requested are “proposals for criminal investigations and for up to nine potential civil compliance investigations.”

Environmental Justice Executive Order

Like the DEI EO, the EJ EO directs federal agencies to terminate federally funded DEI programs and initiatives—including through nonprofits that receive federal grants or contracts—and extends the culling to include agency efforts to promote environmental justice. The intent of the EJ EO seems to be to claw back parts of the Biden administration’s environmental regulations, as well as portions of the federal Infrastructure Investment and Jobs Act and the Inflation Reduction Act that provided funding for environmental justice programs.

Although there is some clear overlap in the subject matter of the EJ EO and the DEI EO, the EJ EO goes further than the DEI EO by targeting federal contractors and grant recipients. It directs agencies to provide the White House Office of Management and Budget (“OMB”) with a list of federal contractors who have provided DEI training to federal agencies, as well as federal grantees who received federal funding “to provide or advance DEI, DEIA, or ‘environmental justice’” programs. Although the EJ EO does not direct that litigation or enforcement actions be taken against these grantees or contractors, the intent of the executive order seems clear: to achieve compliance with its goals by the mere threat of including these organizations on an administration list of supposed transgressors.

Also of note is that on January 27, OMB took the extreme step of “pausing” all federal grants, cooperative agreements, and loans, putting mission-driven nonprofits in critical areas—including public health, environmental protection, immigration, international development, and others—at risk of losing funding that they rely on to carry out their missions. While the administration reversed its “pause” shortly after its issuance, and multiple federal courts have since enjoined the action, the executive orders remain in full force and effect.

Related Litigation

On February 21, a federal judge in Maryland issued a nationwide preliminary injunction against portions of the DEI EO and EJ EO, ruling that portions of the orders were likely to violate the First Amendment’s Free Speech Clause because those portions constituted impermissible content and viewpoint discrimination. The injunction also found that portions of the executive orders were likely to violate the Fifth Amendment because they are unconstitutionally vague.

The trend in private litigation against private-sector DEI programs, which increased in the wake of Students for Fair Admissions, has continued following the president’s executive orders. As a recent example, on March 5, a nonprofit group called Do No Harm, a watchdog group that describes itself as mobilized around “protecting healthcare from the disastrous consequences of identity politics,” filed a complaint in federal district court against the nonprofit 501(c)(3) American Chemical Society (“ACS”), seeking to enjoin ACS from operating the ACS Scholars Program, a scholarship program for students from historically underrepresented groups in the chemical sciences. Only Black, Hispanic, and Indigenous American applicants are eligible for the scholarships. Do No Harm alleged that the program violated Section 1981 of the Civil Rights Act of 1866, which prohibits discrimination on the basis of race in making and enforcing contracts. The suit also alleges violations of Title VI of the Civil Rights Act of 1964, which prohibits discrimination on the basis of race, color, and national origin in programs that receive federal financial assistance. To that end, the suit claims that ACS’s federal tax exemption under Section 501(c)(3) (due to the ability to receive tax-deductible charitable contributions) is a form of federal financial assistance that brings ACS’s scholarship program within the scope of Title VI. Note that the antidiscrimination reach of Title VI is not limited only to race and contracts and is in fact far broader.

Practical Considerations

Unfortunately, the DEI EO and the EJ EO do little to elaborate on what they view as “discriminatory” and “illegal.” Additionally, the EJ EO and DOJ directives somewhat obscure the consequences of being on an administration “list” of organizations providing DEI training or programming for the federal government, although the clear implication is the loss of federal funds. While both executive orders and the DOJ directives make oblique references to statutes and court decisions, they do not examine them in depth, nor do they indicate which elements of a DEI program would make it discriminatory or illegal, adding to the lack of clarity regarding the legal risk and the anxiety of nonprofit leaders. Recent administrative actions have been so broad as to imply that innocuous textual references to diverse groups are evidence of illegal activity prohibited by the executive orders. For instance, according to recent reporting, staff at the National Science Foundation (“NSF”) have reviewed thousands of active science research projects using a list of flagged keywords (such as “women,” “diversity,” “minority,” “institutional,” “historically,” and “socioeconomic,” among dozens of others), to determine if the projects include activities that violate the new executive orders. Scientists who receive NSF funding were already put on notice to cease any activities that do not comply with the executive orders. In this context, nonprofit executives who have concerns about the legality of DEI programs should consult experienced legal counsel to further examine their legal risk and discuss potential mitigation strategies.

Aside from concerns related to federal funding, many nonprofits are concerned that their federal tax-exempt status may be at risk due to DEI-related activities. Although there has not been any evidence of DOJ or the Internal Revenue Service (“IRS”) challenging nonprofit organizations’ federal tax exemptions on this basis, such concerns have been raised by claims made in private litigation framing 501(c)(3) tax-exempt status as a form of federal financial assistance, thus bringing such organizations under the ambit of Title VI of the federal Civil Rights Act of 1964, which has a much broader reach—with even more alarming adverse consequences—for these entities. Beyond this argument, it is not inconceivable that a “weaponized” IRS or DOJ could seek to revoke the tax-exempt status of any tax-exempt organization that it believes is primarily engaged in activities—such as “illegal DEI”— that it believes are contrary to public policy. There is some precedent in case law for such arguments. If the IRS and/or DOJ were to go down this path, the potential adverse implications for some tax-exempt organizations are sweeping.

Even in this time of uncertainty, there are several steps nonprofit executives can take to understand their legal risk related to DEI initiatives. These steps all require a degree of self-awareness of an organization’s values and culture, as well as a careful examination of organizational finances, legal risk, and public profile.

Know your values. Some nonprofits are organized for the specific purpose of supporting certain racial, ethnic, religious, or gender groups, or other groups, in a way that may be considered “DEI” by the Trump administration. For these organizations, there may be a direct conflict between their organizational purposes and the dictates of the executive orders and DOJ directives. Don’t be too quick to abandon a central tenet of your organization without careful consideration, but examine whether certain less drastic steps can be taken to mitigate risk. For instance, many nonprofits are scrubbing their public-facing websites to remove any DEI-related references.

Examine your funding streams. Organizations that do not rely on federal awards for their operations are much more insulated from these executive orders and potential DOJ enforcement than ones that do. If your organization does receive federal funds, and it has a constellation of subsidiaries and affiliates, identify which entity or entities house the federally funded programs and the DEI or environmental justice programs that put you at risk under the executive orders, and do what you can to insulate the other entities accordingly. Also, begin examining funding alternatives, such as private foundation grants, that may allow you to fulfill your mission and meet your funding needs.

Scrutinize your DEI initiatives. Take a hard look at your DEI-related initiatives to ensure that they are consistent with current law, and consult experienced legal counsel for assistance. The federal Civil Rights Act of 1964, mentioned in the DEI EO, is only one of the laws implicated by such programs. As discussed above, also very relevant is Section 1981 of the federal Civil Rights Act of 1866, which has been used to launch legal attacks on programs from nonprofits and other entities that restrict eligibility for certain grants, scholarships, fellowships, and other opportunities to certain races, among other protected characteristics. Other laws implicated could include state public accommodations laws and state education and employment laws. Several states have passed anti-DEI laws covering employment, state grants, and education that need to be taken into account, such as the Florida law that prohibits private nonprofit and other employers from providing any DEI-related training to their Florida-based employees. See our prior article on mitigating risks of DEIA programs for a more expansive discussion of these issues.

Assess your culture. Have a good understanding of the level of support for DEI-related initiatives within your nonprofit organization and among your members, donors, grantors, and other stakeholders. Understand your organization’s risk tolerance, budget, values, public profile, and ability to withstand legal challenges and the significant costs that often accompany them (some of which may not be covered by insurance). Be able to identify any potentially controversial programs as a way to anticipate legal and regulatory challenges, and consider what interim changes can be made in order to mitigate risk and make your organization less of a target in the current climate.

Most of the administration’s directives in this area (and others) are already the subject of legal challenges in the courts—some of which have found early success—but the fate of that litigation, much of which is likely to work its way up to the U.S. Supreme Court, is uncertain. While many legal experts believe that a number of the new directives are unlawful, relying on such presumptions can carry with it a high degree of risk.

Although the new administration’s actions have instilled fear and uncertainty in many in the nonprofit community, these early actions may prove to be the catalysts that encourage nonprofits to take necessary protective actions. The Trump administration has given nonprofit organizations an early opportunity to galvanize themselves against potential adverse legal and regulatory consequences. By taking early prophylactic steps against these threats, nonprofits will be better positioned to defend themselves for the next four years while maintaining progress toward their missions.

The views expressed herein are solely those of the authors and are not necessarily those of the authors’ firm, the American Bar Association, or the Business Law Section.

On February 17, 2025,[2] the U.S. District Court for the Eastern District of Texas, before which is pending the Smith v. U.S. Department of the Treasury dispute, lifted the preliminary injunction it issued January 7, 2025, against the Reporting Rules[3] adopted pursuant to the Corporate Transparency Act (“CTA”),[4] thereby clearing the way for enforcement of the CTA and its filing obligations. With that action, the last pending judicial barrier to broad enforcement of the CTA’s reporting obligations was lifted, and its general enforcement recommenced.

That was, however, far from the final development with respect to the implementation of the CTA. Rather, over the first weekend of March, the government and a variety of public officials, including the current chief executive of the United States, issued a series of pronouncements as to the CTA’s reach and enforcement that ultimately foreshadow the intention to abdicate much of its enforcement. The same week, another federal district court became the first to find that the CTA violates the Fourth Amendment right against unreasonable search and seizure.

The Smith Preliminary Injunction and the New March 21 Filing Deadline

To recap, as previously reviewed in detail,[5] even while the nationwide preliminary injunction issued by the district court in Texas Top Cop Shop, Inc. v. McHenry (formerly Texas Top Cop Shop, Inc. v. Garland) (“TTCS”)[6] was in effect and challenges thereto were proceeding, the Smith court issued a preliminary injunction against enforcement of the CTA, with that relief being restricted to the parties to the suit before the court, and a nationwide injunction against the Reporting Rules.[7] On January 23, 2025, the Supreme Court lifted the TTCS preliminary injunction. In response to the government’s motion to stay the Smith preliminary injunction pending appeal,[8] to which the plaintiffs filed a response,[9] on February 18, 2025, the Smith court lifted its preliminary injunction as to both the CTA and the Reporting Rules.

In furtherance of the undertaking it made in its motion to stay the preliminary injunction pending appeal,[10] the Financial Crimes Enforcement Network (“FinCEN”) announced on February 18, 2025, that it was granting reporting companies until March 21, 2025, to bring current all outstanding filing obligations.[11] Further, the directive as to the new filing deadline “bridges” the companies that would have fallen into any of the gaps that otherwise existed, an example being companies whose obligation to file an initial or an updated beneficial ownership information report (“BOIR”) would have fallen on February 18 or 19, 2025.

Under the Reporting Rules,[12] reporting companies preexisting January 1, 2024, were afforded until “not later than” January 1, 2025, within which to file an initial BOIR.[13] Companies created on or after January 1, 2024, and before January 1, 2025, were afforded ninety days within which to file an initial BOIR.[14] For companies created on or after January 1, 2025, they are afforded thirty days within which to file an initial BOIR.[15] Once a BOIR has been filed, a reporting company has thirty days within which to file an update as to any change in the submitted information.[16]

Between the TTCS and Smith injunctions, except for a brief period while the TTCS injunction was stayed and until that stay was lifted, those deadlines were on hold from the December 3, 2024, granting of the TTCS preliminary injunction through the February 18, 2025, lifting of the Smith injunction. In that period, there arose filing deadlines for companies preexisting January 1, 2024; companies created on or after September 4, 2024; and updates to previously filed BOIRs.[17]

Application of the March 21, 2025, Deadline

The examples below will help to understand how—in the face of these on-again, off-again injunctions and prior reporting periods for initial and updated BOIRs for companies created at various times—the new March 21 deadline was intended to apply. We use the phrase was intended to apply instead of will apply because shortly after the FinCEN Notice dated February 18 that instituted the March 21 deadline, FinCEN published a press release rescinding that deadline (see “And Then the Seventy-Two Hours of Mayhem,” below).

Examples of application of the March 21, 2025, deadline:

ABC Inc. was created on September 4, 2024; its initial BOIR was due not later than December 3, 2024. That day, the TTCS preliminary injunction was issued, and no filing was made. That initial BOIR would have been due not later than March 21, 2025.

XYZ LLC was created on December 31, 2022; its initial BOIR was due not later than January 1, 2025. With the TTCS preliminary injunction then in effect, no filing was made, and after it was lifted, no action was taken with regard to the Smith injunction. That initial BOIR would have been due not later than March 21, 2025.

DEF LLC was created on December 31, 2024; its initial BOIR was due not later than March 31, 2025. The March 21, 2025, deadline is eighty days after its creation, and DEF would have been afforded the full ninety days of the Reporting Rules within which to file its initial BOIR.

GHI Inc. was incorporated on January 1, 2025; its initial BOIR was due before January 31, 2025. However, as of that day, the Smith injunction was in place, and no action was taken. That initial BOIR would have been due not later than March 21, 2025.

JKL Inc. was created on March 1, 2024, and filed its initial BOIR on May 1, 2024; that report identified Laura as a beneficial owner, a position she held as a senior officer of the company. On December 1, 2024, Laura resigned her position, and she ceased to have any relationship with the company; an updated BOIR was due by the end of the month. However, with the TTCS and then the Smith injunctions in place, no updated BOIR was filed. JKL would have had until March 21, 2025, to file an updated BOIR deleting any reference to Laura as a beneficial owner and otherwise updating the filed information to address, if applicable, her replacement in that role.

MNO LLC was created on January 1, 2022; while its initial BOIR was not due until January 1, 2025, it filed its initial BOIR on June 1, 2024. On November 15, 2024, a senior officer of the LLC resigned and ceased to be a beneficial owner of MNO. The company was due to file an updated BOIR not later than December 15, 2024. With the TTCS injunction in place, no filing was made. That BOIR update would have been due not later than March 21, 2025.

“True, Correct, and Complete”

It bears noting that simply filing a report that was held in abeyance during the period that the CTA and Reporting Rules were enjoined is not necessarily the entirety of a company’s obligations. A BOIR must, as of its filing, be “true, correct, and complete.”[18] Counsel and other filers who are “sitting on” filings need to confirm that the information set forth therein remains accurate as of the filing date. If inaccurate information is inadvertently filed, there is a ninety-day period within which to file a correction.[19]