Commercial disputes are a fact of life in every industry. From counterparties that fail to honor contracts, to companies that use deceitful tactics, to individuals who misappropriate proprietary information for their own benefit, running a business regularly requires consultation with an attorney and frequently involves the business in litigation. Historically, businesses faced with a legal conflict had just three options: fight a lawsuit by hiring counsel on expensive retainer, instead find a lawyer who offers “no win, no fee” contingency billing, or abandon the case (by either paying a settlement or giving up on a claim). More recently, third-party litigation funding has given attorneys and their clients a powerful alternative to these traditional solutions.

The costs of hiring a lawyer, discovery procedures, arranging depositions, and retaining experts can snowball quickly—especially in cases that span several years. Wrongdoers know this. They therefore can, and often do, weaponize any financial superiority in court, much to the detriment of plaintiffs who cannot, or prefer not, to pay full litigation costs upfront. It is no surprise, then, that corporate legal departments are frequently perceived by management as cost centers necessary to put out legal fires—not as the strategic revenue sources they can become.

With litigation finance, however, businesses can lift the financial burden of litigation, reduce financial risk, build a stronger case, and achieve fairer legal outcomes in court.

What, exactly, is litigation finance?

Litigation finance is the practice of a third party providing capital to a plaintiff, such as a business or individual. This third party, known as a litigation funder, is a specialty finance firm that is otherwise unrelated to the lawsuit in question. The litigation funder invests in the action and, in return for this investment, is promised a portion of any monetary recovery. Typically, this is structured either a multiple of the original investment, or a percentage of the gross recovery.

Commercial litigation finance is almost always a non-recourse arrangement wherein the only collateral for the investment is a single case or portfolio of cases. If the case does not resolve favorably, the recipient of the funds owes the litigation funder nothing. If the claim is successful, the litigation funder will usually receive first dollar in until it is repaid, while the remainder of the proceeds will be divided between the claimant and the attorneys as agreed between them.

How can businesses use litigation finance?

Litigation finance investments are highly customizable, rendering them suitable for a wide variety of needs. Bespoke agreements are common, especially as the size of the investment increases and the relationship between funder and company deepens. In that vein, businesses can use funding to pay for case-related legal expenses, including attorney fees, expert witness fees, depositions, court reporter fees, arbitration filing fees, discovery, appeals, and more.

In addition, as litigation progresses, companies can also use the funds received to cover business operating expenses when existing sources of working capital are insufficient. This option can be critical for companies that have been actively harmed by the actions of the defendant(s) and would otherwise find it challenging to continue doing business while the lawsuit is pending if not for additional sources of capital.

Thus, litigation finance can support both the pursuit of meritorious litigation and ensure the financial survival of thinly capitalized commercial claimants.

How can litigation finance help manage corporate balance sheets?

Under Generally Accepted Accounting Principles, litigation costs are reflected as expenses. Carrying and reporting such expenses can negatively impact a company’s financials and quarterly performance. This is especially true for public companies that are valued on earnings or cash flow or require certain financial criteria to be met to comply with credit obligations.

For companies in that position, litigation costs paid from company funds must be recorded as expenses when incurred, thereby diminishing reportable earnings. Moreover, even if litigation results in a favorable outcome (whether via judgment or settlement), such outcomes sometimes take months or years to enforce and actually pay out, leaving a temporary gap in a company’s cash flow despite obtaining a ruling in their favor. Worse yet, recoveries from successful legal matters may not offset the adverse impact of lawsuit-related costs because such recoveries are generally treated as below-the-line items that do not increase earnings. General counsel and in-house legal departments can shift both the risk and financial burden of litigation to third-party funding specialists in exchange for a portion of any recoveries.

For instance, litigation finance companies can make funds available in a segregated account so that law firms bill against those funds, rather than through the business, keeping the ongoing expenses off the company’s balance sheets until resolution of the matter. In this way, businesses do not have to carry and report expenses on an ongoing basis but will only have to do so at the end of the dispute. Further, once the matter resolves, the company incurs the liability of having to repay the investment but can then simultaneously report the funds received from resolution of the matter. This simultaneous reporting creates a more accurate accounting of the events because the payment to the litigation finance company (which subsumes the expenses) appears on the claimant-business’s financial statements at the same time as any recovery realized from the underlying litigation.

Ultimately, securing third-party funding for operating expenses can transform otherwise illiquid liquid claims into a valuable source of capital.

What types of cases do litigation funders invest in?

Litigation finance companies invest in a wide range of cases that varies based on their particular risk profile, expertise, and available capital. Whether a company’s dispute revolves around trade secrets, contracts, shareholders, IP, or some other matter, litigation finance can support virtually any claim type.

In October, LexShares published “The Litigation Funding Barometer,” an analysis of the types of cases that are often best suited for non-recourse financing. The data presented in the Barometer report was based on data produced by the firm’s proprietary Diamond Mine software, which in 2021 scored more than 30,000 state and federal cases based on several different factors. Among other conclusions, the report found that a higher percentage of strong funding opportunities existed among federal cases than state cases. Federal trade secrets, antitrust, and contract disputes also presented some of the strongest funding opportunities across jurisdictions. While this data represents the investment potential of various case types, we feel it is nevertheless a valuable gauge of how the funding industry generally views the U.S. litigation landscape.

Notably, litigation finance companies are also not limited to investing in contingency cases. Financing can be made available to hourly representation, usually requiring deferral of a portion of the hourly attorney’s rate and ongoing billing against segregated amounts.

What are some attributes of reputable litigation finance companies?

Evidently, the idea of receiving funding—at some times substantial amounts of funding—from a third party can raise some concerns. Attorneys seeking out and recommending litigation finance to their clients should watch for the following things:

First, a reputable litigation finance company will implement a demanding due diligence process. While this is frustrating while already dealing with the litigation process, a robust underwriting process signals a serious partner. The old adage holds true: if something is too good to be true, it probably is.

Second, a litigation finance company should never attempt to control or direct the litigation. There are a number of reasons for this, including rules of ethics pertaining to an attorney’s duty of loyalty. If a litigation finance company attempts to insert itself into the actual litigation, this is a sign that another funder may be a better choice.

Reputable litigation finance companies are an excellent resource for savvy businesspeople and their legal advisors. Careful vetting and selection of that tool is of paramount importance.

In-house legal departments leveraging a powerful new tool for accessing justice.

Maya Steinitz, a legal scholar and University of Iowa College of Law professor, refers to litigation finance as “likely the most important development in civil justice of our time.” As founders and executives grow more familiar with commercial litigation finance as a useful financial resource, the potential appeal of offsetting litigation risk and optimizing corporate balance sheets for legal action stands to become more mainstream. For CEOs and founders weighing the prospect of litigation, the ultimate question is no longer why they should be using litigation finance. The real question is: why not?

Knobbe Martens 2040 Main St., 14th Floor Irvine, CA 92614 [email protected]

Contributors

Julia Hanson

Knobbe Martens 2040 Main St., 14th Floor Irvine, CA 92614 [email protected]

Alistair McIntyre

Knobbe Martens 2040 Main St., 14th Floor Irvine, CA 92614 [email protected]

Nyja Prior

Knobbe Martens 2040 Main St., 14th Floor Irvine, CA 92614 [email protected]

Clint Saylor

Knobbe Martens 2040 Main St., 14th Floor Irvine, CA 92614 [email protected]

Michelle Ziperstein

Knobbe Martens 2040 Main St., 14th Floor Irvine, CA 92614 [email protected]

§ I. Patent Cases

I.a. Supreme Court decisions

Minerva Surgical, Inc. v. Hologic, Inc., 141 S. Ct. 2298 (2021)

Facts: This case concerns the conditions for applying assignor estoppel where a party who assigns its patent rights later asserts an invalidity defense to that patent.

In the late 1990s, Csaba Truckai invented a device for treating abnormal uterine bleeding using a moisture-permeable applicator head and assigned the patent application to his company Novacept. Hologic later acquired Novacept. Truckai also founded Minerva Surgical, and obtained a patent directed to an improved device to treat abnormal uterine bleeding using a moisture-impermeable applicator head. Meanwhile, Hologic filed for another patent in the same patent family as the Novacept application, and obtained a broad patent claim to applicator heads, without regard to whether they are moisture permeable.

Hologic sued Minerva for patent infringement of this newly obtained claim. In response, Minerva argued that Hologic’s patent was invalid because the new, broad claim to applicator heads did not correspond to the invention’s written description, which addressed applicator heads that were water permeable. Hologic then invoked the doctrine of assignor estoppel, arguing that Truckai and Minerva could not challenge patent validity. The District Court granted summary judgment to Hologic, holding that assignor estoppel barred Minerva’s invalidity defense, and the Court of Appeals for the Federal Circuit affirmed in relevant part. The Supreme Court granted certiorari.

Held: The doctrine of assignor estoppel is upheld, but the judgment was vacated and remanded. Assignor estoppel applies only when the assignor’s assertions of invalidity contradicts explicit or implicit representations the assignor made in assigning the patent.

Reasoning: The doctrine of assignor estoppel, which limits an inventor’s ability to assign a patent to another for value and later contend in litigation that the patent is invalid, is based on equitable principles. Assignor estoppel reflects a demand for consistency and fair dealing with others. A person should not be able to sell his or her patent rights—making an implicit representation that the patent at issue is valid—and later raise an invalidity defense, disavowing that implied warranty. But when an assignor has made neither explicit nor implicit representations in conflict with an invalidity defense, then there is no unfairness in the assertion of invalidity and no ground for applying assignor estoppel.

The Court noted three situations where this may occur: 1) when an employee assigns patent rights to his or her employer in any future inventions he or she may develop during his or her employment; 2) when a later legal development renders the warranty given at the time of assignment irrelevant; and 3) when the assignees of a patent application make a post-assignment change that materially broadens the patent claims. In the last situation, relevant here, the assignor could not have warranted the validity of the broader claims. The Court noted that as long as there is no inconsistency in the assignor’s positions, then there is no basis for estoppel, and he or she can challenge the new claims in litigation. As a result, the Court vacated the decision and remanded the case to the Federal Circuit to determine whether Hologic’s new patent claim was materially broader than the claims originally assigned by Truckai.

The Court further noted that beyond promoting fairness, patent assignor estoppel furthers some policy goals, because assignors—with their knowledge of the relevant technology—are especially likely to be infringers. By preventing assignors from raising an invalidity defense in a later infringement suit, the doctrine gives assignees confidence in the value of what they have purchased. The Court further noted that even when an assignor is barred from asserting in an infringement suit that the patent is invalid, the assignor can still argue about how to construe the patent’s claims.

Justice Alito filed a dissenting opinion, stating that the question in this case cannot be decided without deciding whether Westinghouse Elec. & Mfg. Co. v. Formica Insulation Co., 266 U.S. 342 (1924)—which approved the use of assignor estoppel in the U.S.—should be overruled. Justice Barrett also filed a dissenting opinion, in which Justices Thomas and Gorsuch joined. The dissent noted that this case turned on whether the Patent Act of 1952 incorporated the doctrine of assignor estoppel and concluded that it did not.

I.b. Federal Circuit Decisions

Bot M8 LLC v. Sony Corp. of Amer., 4 F.4th 1342 (Fed. Cir. 2021)

Facts: This case concerns the pleading requirements for patent infringement.

Bot M8 owns five patents directed to video game machines. Bot M8 sued Sony for patent infringement based on Sony’s PlayStation 4 (“PS4”) console and accompanying game software. Following a transfer to the Northern District of California, a case management conference resulted in the district court sua sponte directing Bot 8 to file an amended complaint detailing “every element of every claim that [Bot M8] say[s] is infringed and/or explain why it can’t be done.” Bot M8 filed its 223-page first amended complaint. Sony moved to dismiss for failure to state a claim of infringement. The district court granted Sony’s motion as to four of the five patents.

The court then denied Bot M8’s second motion for leave to amend, reasoning that Bot M8 failed to raise concerns about the legality of reverse engineering Sony’s software at the time it was first ordered to file an amended complaint. For the same reasons, the court also denied Bot M8’s motion for reconsideration.

Applying Alice, the district court also found one claim of the last remaining patent to be patent ineligible. Alice Corp. v. CLS Bank International, 573 U.S. 208, 217-18 (2014).

Bot M8 and Sony then entered a joint stipulation dismissing the remaining claims without prejudice, and with Bot M8 reserving its right to appeal. On appeal, the Federal Circuit affirmed in part and reversed in part.

Held: Patent owners do not need to prove their entire case at the pleading stage, but they cannot rely solely on conclusory statements of infringement.

Reasoning: The Federal Circuit affirmed (1) dismissal of the infringement allegations as to two patents for being conclusory; (2) denial of leave to file a second amended complaint as to four patents; and (3) summary judgment in favor of Sony on one patent in view of the claims being directed to patent ineligible subject matter. The Court reversed and remanded as to the remaining two patents because the infringement claims were found to plausibly state a claim at the early pleading stages.

The panel acknowledged the district court’s authority to request an amended complaint, but disagreed with its requirement that Bot M8 explain “every element of every claim” because a plaintiff “need not prove its case at the pleading stage.” The panel explained that any district court approach that employs a “blanket element-by-element” requirement for patent infringement cases exceeds the scope of the Supreme Court’s pleading standard set forth in Ashcroft v. Iqbal, 556 U.S. 662, 678 (2009) and Bell v. Twombly, 550 U.S. 544, 570 (2007). Instead, plaintiffs must only articulate a “plausible claim for relief.”

However, the panel stated that merely reciting claim elements and concluding that an allegedly infringing product has each element will not be enough to meet this pleading standard, as there must be some factual allegations suggesting a plausible claim. Under this reasoning, allegations of infringement for two patents were deemed conclusory and lacking in factual allegations. Similarly, the panel found no error in the district court’s application of Alice, and affirmed summary judgment in favor of Sony. But the panel determined that the district court erred by dismissing the other two patents for failure to state a claim of infringement by demanding highly specific allegations too early in the proceedings. The panel found that Bot M8 alleged specific instances of infringement sufficient to meet the plausibility requirements for Bot M8’s claim.

The Federal Circuit also found no abuse of discretion in the district court’s denial of Bot M8’s request for leave to file a second amended complaint. While the court acknowledged that requiring reverse engineering of the accused device may not have been necessary, Bot M8 waived any objection to this requirement by volunteering to complete the task without suggesting that compliance would be difficult in terms of labor or obtaining legal permissions.

Yu v. Apple Inc., 1 F.4th 1040 (Fed. Cir. 2021)

Facts: This case concerns whether claims directed to a device that implements an abstract idea are patent ineligible under 35 U.S.C. § 101.

Yu owns U.S. Patent No. 6,611,289 (“the ‘289 patent”) titled “Digital Cameras Using Multiple Sensors with Multiple Lenses.” Yu sued Apple Inc. and Samsung Electronics Co., Ltd. (“Defendants”) for infringement of claims 1, 2, and 4. Claim 1 is representative and recites:

1. An improved digital camera comprising:

a first and a second image sensor closely positioned with respect to a common plane, said second image sensor sensitive to a full region of visible color spectrum;

two lenses, each being mounted in front of one of said two image sensors;

said first image sensor producing a first image and said second image sensor producing a second image;

an analog-to-digital converting circuitry coupled to said first and said second image sensor and digitizing said first and said second intensity images to produce correspondingly a first digital image and a second digital image;

an image memory, coupled to said analog-to-digital converting circuitry, for storing said first digital image and said second digital image; and

a digital image processor, coupled to said image memory and receiving said first digital image and said second digital image, producing a resultant digital image from said first digital image enhanced with said second digital image.

Defendants filed a Rule 12(b)(6) motion to dismiss. The district court found that the asserted claims were directed to “the abstract idea of taking two pictures and using those pictures to enhance each other in some way,” decided that each asserted claim was patent ineligible under § 101, and granted the motion to dismiss. Yu appealed to the Federal Circuit.

Held: Affirmed. The claims are directed to an abstract idea and lack an inventive concept sufficient to transform the abstract idea into a patent-eligible invention.

Reasoning: The Court applied 9th Circuit law, which reviews a district court’s grant of a Rule 12(b)(6) motion de novo. It also applied its own law and reviewed the district court’s determination of patent ineligibility under § 101 de novo.

The Court used the Mayo/Alice two-step framework to analyze whether a patent claim is eligible under § 101. The first step analyzes whether “a patent claim is directed to an unpatentable law of nature, natural phenomenon, or abstract idea.” Alice Corp. v. CLS Bank Int’l, 573 U.S. 208, 217 (2014). If it is, then the court determines “whether the claim nonetheless includes an ‘inventive concept’ sufficient to ‘transform the nature of the claim’ into a patent-eligible application.” Id. (quoting Mayo Collaborative Servs. v. Prometheus Labs., Inc., 566 U.S. 66, 72 (2012)).

At step one, the Court found that “claim 1 is directed to the abstract idea of taking two pictures (which may be at different exposures) and using one picture to enhance the other in some way.” Reading the claim language in view of the specification, the Court noted that claim 1 results in “producing a resultant digital image from said first digital image enhanced with said second digital image,” and that “Yu does not dispute that . . . the idea and practice of using multiple pictures to enhance each other has been known by photographers for over a century.”

The Court further found that “[o]nly conventional camera components are recited to effectuate the resulting ‘enhanced’ image” and that “it is undisputed that these components were well-known and conventional.” It therefore concluded that “[w]hat is claimed is simply a generic environment in which to carry out the abstract idea.”

Yu asserted that claim 1 is “directed to a ‘patent-eligible improvement in digital camera functionality’ by ‘providing a specific solution’ to problems such as ‘low resolution caused by low pixel counts’ and ‘inability to show vivid colors caused by limited pixel depth.’” The Court, however, found that “claim 1’s solution to these problems is the abstract idea itself—to take one image and ‘enhance’ it with another.”

Yu also argued that parts of the specification provide support that the patentable advance in the claims is “the particular configuration of lenses and image sensors.” The Court, though, found that “[e]ven a specification full of technical details about a physical invention may nonetheless conclude with claims that claim nothing more than the broad law or abstract idea underlying the claims.” ChargePoint, Inc. v. Sema-Connect, Inc. 920 F.3d 759, 769 (Fed. Cir. 2019). For instance, the specification refers to a “four-lens, four-image-sensor configuration” as an advance over the prior art, where “three of the sensors are color-specific while the fourth is a black-and-white sensor.” Claim 1, however, is limited only to a “two-lens, two-image-sensor configuration in which none of the image sensors must be color.” The Court found “the mismatch between the specification . . . and the breadth of claim 1 underscores that the focus of the claimed advance is the abstract idea and not the particular configuration discussed in the specification that allegedly departs from the prior art.”

At step two, the Court found that there was no inventive concept sufficient to transform the claimed abstract idea into a patent-eligible invention. The Court reasoned that claim 1 failed under step two because it is “recited at a high level of generality and merely invokes well-understood, routine, conventional components to apply the abstract idea.” Yu asserted that the prosecution history shows that the claim was allowed over multiple prior art references. The Court, however, found that “even if claim 1 recites novel subject matter, that fact is insufficient by itself to confer [patent] eligibility” and went on to explain that “[t]he claimed [two-lens, two-image-sensor] configuration does not add sufficient substance to the underlying abstract idea of enhancement—the generic hardware limitations of claim 1 merely serve as ‘a conduit for the abstract idea.’” In re TLI Commc’ns LLC Pat. Litig., 823 F.3d 607, 612 (Fed. Cir. 2016).

Additionally, the Federal Circuit found that the district court’s recognition of a “century-old practice” at the pleadings stage was appropriate, that the 12(b)(6) motion could properly be determined without hearing expert testimony, and that it was not error for the district court to consider only the intrinsic record (the patent itself) to conclude that it was patent ineligible.

The Federal Circuit therefore affirmed the district court’s decision that the claims of Yu’s patent are ineligible under § 101 and affirmed the order granting the 12(b)(6) motion.

Judge Newman dissented and argued that the majority was “further enlarge[ing] . . . and further obfuscat[ing] the statute.” She argued that the claimed “camera is a mechanical and electronic device of defined structure and mechanism; it is not an ‘abstract idea.’ Observation of the claims makes clear that they are for a specific digital camera . . . . not for the general idea of enhancing camera images.” Such a device “easily fits the standard subject matter eligibility criteria.” While the patent specification describes the superior image definition capabilities of the claimed camera, “[a] statement of purpose or advantage does not convert a device into an abstract idea.”

Trimble Inc. v. PerDiemCo LLC, 997 F.3d 1147 (Fed. Cir. 2021)

Facts: This case concerns whether a patentee is subject to specific personal jurisdiction in the federal district where an alleged infringer is headquartered, when the alleged infringer files a declaratory judgment action in that district after the parties have engaged in licensing negotiations.

PerDiemCo LLC (“PerDiemCo”) is a Texas LLC. It owns eleven patents all related to electronic logging devices and/or geofencing designed to help employers track commercial vehicles and drivers. PerDiemCo’s sole owner, officer, and employee lives and works in Washington, D.C. PerDiemCo rents office space in Marshall, TX, but its sole owner, officer, and employee has never visited the space and it has no employees there.

Trimble Inc. (“Trimble”) and its wholly owned subsidiary Innovative Software Engineering, LLC (“ISE”) make and sell GPS navigation products and services, which include electronic logging and geofencing devices and services. Trimble is a Delaware Corporation with its headquarters in the Northern District of California. ISE is an Iowa LLC with its headquarters and principal place of business in Iowa.

PerDiemCo sent a letter to ISE in Iowa alleging that ISE was infringing PerDiemCo’s patents. This letter was forwarded to Trimble’s Chief IP Counsel in Colorado. Between October and December 2018, the parties engaged in licensing negotiations, and PerDiemCo threatened to sue Trimble and ISE for patent infringement in the Eastern District of Texas. During these negotiations, PerDiemCo communicated with Trimble at least twenty-two times via letter, email, or telephone.

In January 2019, Trimble and ISE filed a complaint in the Northern District of California, where Trimble is headquartered. They sought a declaratory judgement that they did not infringe any of the patents PerDiemCo asserted.

PerDiemCo moved to dismiss for lack of personal jurisdiction under Red Wing Shoe Co. v. Hockerson-Halberstadt, Inc., 148 F.3d 1355 (Fed. Cir. 1998), which states that “[a] patentee should not subject itself to personal jurisdiction in a forum solely by informing a party who happens to be located there of suspected infringement” because “[g]rounding personal jurisdiction on such contacts alone would not comport with principles of fairness,” id. at 1361.

The district court found that while PerDiemCo had established sufficient minimum contacts with California through its negotiations with Trimble, it would be constitutionally unreasonable to exercise personal jurisdiction over PerDiemCo in view of Red Wing. It therefore dismissed Trimble and ISE’s complaint. Trimble and ISE appealed to the Federal Circuit.

Held: Reversed and remanded. The exercise of personal jurisdiction over PerDiemCo in the Northern District of California is not unreasonable and satisfies due process.

Reasoning: The Court applied Federal Circuit law “because the jurisdictional issue is intimately involved with the substance of the patent laws.” Autogenomics, Inc. v. Oxford Gene Tech. Ltd., 566 F.3d 1012, 1016 (Fed. Cir. 2009). Therefore, because the parties did not dispute the jurisdictional facts, the Court reviewed the question of personal jurisdiction de novo.

The exercise of personal jurisdiction over an out-of-state defendant involves an evaluation as to whether the forum state’s long-arm statute permits service of process and whether the assertion of personal jurisdiction violates due process. California allows service of process to the limits of the Due Process Clauses, and therefore the “two inquiries fold into one”—whether personal jurisdiction over PerDiemCo was consistent with due process.

A Court may exercise personal jurisdiction over a defendant when the defendant has had sufficient minimum contacts with the forum state and when the exercise of personal jurisdiction “does not offend traditional notions of fair play and substantial justice.” Int’l Shoe Co. v. Washington, 326 310, 316-17 (1945).

Minimum contacts are typically established when the defendant intentionally reaches out to the forum state and purposefully avails itself of doing business there. The plaintiff’s claims must arise out of or relate to those contacts. To satisfy fair play and substantial justice, the Court considers the burden on the defendant, the forum state’s interest in adjudicating the dispute, the plaintiff’s interest in convenient and effective relief, the interstate judicial system’s interest in obtaining an efficient resolution, and the shared interest of the states in furthering fundamental substantive social policies.

The Court noted that Supreme Court cases following Red Wing make clear that special patent policies and considerations cannot impact the personal jurisdiction analysis.

The Supreme Court has held that communications sent into a state may give rise to specific personal jurisdiction and that a defendant that repeatedly communicates with the forum state “clearly has fair warning that [its] activity may subject [it] to the jurisdiction of a foreign sovereign.” Quill Corp. v. North Dakota, 504 U.S. 298, 308 (1992). The Federal Circuit has interpreted this to mean that “negotiation efforts, although accomplished through telephone and mail . . . can still be considered as activities purposefully directed at residents of [the forum].” Inamed Corp. v. Kuzmak, 249 F.3d 1356, 1362 (Fed. Cir. 2001) (discussing Quill). The Court noted that it previously held that Red Wing did not create a rule that “patent enforcement letters can never provide the basis for jurisdiction in a declaratory judgement action.” Jack Henry & Associates, Inc. v. Plano Encryption Technologies LLC, 910 F.3d 1199, 1206 (Fed. Cir. 2018).

Other circuits have found that communications from outside a forum state can lead to specific personal jurisdiction in the forum. See, e.g., Yahoo! Inc. v. La Ligue Contre le Racisme et l’Antisemitisme, 433 F.3d 1199, 1208 (9th Cir. 2006) (en banc) (cease-and-desist letter can be basis for personal jurisdiction); Oriental Trading Co. v. Firetti, 236 F.3d 938, 943 (8th Cir. 2001) (directing communications into state gives rise to personal jurisdiction).

Other activities have also led to minimum contacts relevant to declaratory judgment patent cases, such as hiring an attorney or patent agent in the forum state, Elecs. for Imaging, Inc. v. Coyle, 340 F.3d 1344, 1351 (Fed. Cir. 2003); physically entering the state to demonstrate the technology, id., or to discuss infringement allegations with the plaintiff, Xilinx, Inc. v. Papst Licensing GmbH & Co. KG, 848 F.3d 1346, 1357 (Fed. Cir. 2017); the presence of an exclusive licensee in the state, Breckenridge Pharm., Inc. v. Metabolite Labs., Inc., 444 F.3d 1356, 1366-67 (Fed. Cir. 2006); and “extra-judicial patent enforcement” targeting businesses in the state, Campbell Pet Co. v. Miale, 542 F.3d 879, 886 (Fed. Cir. 2008).

Further, the Court evaluated the Supreme Court’s recent decision in Ford Motor Co. v. Mont. Eighth Jud. Dist. Ct., which found that the “link” or “connection” between the defendant’s contact with the state and the plaintiff’s suit requires only that the complaint “arise out of or relate to the defendant’s contacts with the forum.” 141 S.Ct. 1017, 1026 (2021). The Federal Circuit interpreted this to mean that nonexclusive patent licenses in a forum state can support personal jurisdiction over the licensor.

Here, the Court found that PerDiemCo’s contacts with California were extensive, including twenty-two communications with Trimble in California over three months. This is “far beyond solely informing a party who happens to be located in California of suspected infringement.” Therefore, PerDiemCo had sufficient minimum contacts to justify personal jurisdiction in California.

Further, the Court found that the factors of fair play and substantial justice each lean in favor of personal jurisdiction being reasonable. The Federal Circuit reversed the district court’s order finding a lack of personal jurisdiction and remanded for further proceedings.

Hyatt v. Hirshfeld, 998 F.3d 1347 (Fed. Cir. 2021)

Facts: Hyatt bulk filed 381 patent applications in 1995. These applications claimed priority to applications filed in the ‘70s and ‘80s, through Hyatt’s practice of submarine patenting, which allowed an applicant to extend the term of a patent by claiming priority to an earlier filed, and subsequently abandoned, application in the patent family.

Within the bulk filing, the 381 applications ranged from 289 to 576 pages of text and 40-60 pages of figures, much longer than a typical patent application. While Hyatt initially agreed with the USPTO to focus his claims on distinct subject matter, he instead filed amendments over the next several years to increase the number of pending claims to about 300 per application, or 115,000 total. Of these claims, 45,000 were independent claims. Some amendments resulted in entirely new claims. In others, Hyatt reintroduced claims that had previously been lost in interference proceedings.

The USPTO began to examine Hyatt’s filings, but due to the sheer volume and the subsequent amendments, examination was slow. Because each filing claimed priority to several earlier filings, it was difficult for examiners to determine priority dates to identify prior art. The size of the patents also made it difficult to determine whether the applications complied with 35 U.S.C. § 112 written description requirements. Further, examination of Hyatt’s patents was stayed from 2003 to 2012 due to pending litigation. Examination restarted in 2013. The USPTO created an art unit dedicated to examining Hyatt’s filings. It was estimated that to complete examination, it would take a single examiner over 500 years.

The USPTO ultimately rejected the applications. Hyatt appealed to the Board of Patent Appeals and Interferences, which placed only a small subset of his claims in condition for allowance.

Hyatt filed a district court action under 35 U.S.C. § 145 against the USPTO to obtain four patents from his bulk filing, totaling 1592 claims. The PTO asserted an affirmative defense of prosecution laches. The district court held that the USPTO did not meet its burden of proving prosecution laches and that the claims were not invalid. Specifically, the court found that the USPTO had not provided Hyatt with adequate warning of a laches rejection, had not shown prejudice, had not issued laches rejections for the four applications at issue, and had not met its burden of proving “unreasonable and unexplained delay” by a preponderance of the evidence. The USPTO appealed the decision.

Held: Prosecution laches is an affirmative defense available to the USPTO in a 35 U.S.C. § 145 proceeding. The USPTO may assert prosecution laches even if it did not previously issue rejections based on laches. The USPTO met its burden to shift the burden of proof to Hyatt. Delay by the USPTO does not excuse delay by the applicant.

Reasoning: Prosecution laches “render[s] a patent unenforceable when it has issued only after an unreasonable and unexplained delay in prosecution that constitutes and egregious misuse of the statutory patent system under a totality of the circumstances.”

The Court first addressed whether the USPTO may assert prosecution laches in a § 145 proceeding. The Court reasoned that the USPTO can reject applications based on prosecution laches, and 35 U.S.C. § 282 evidences congressional intent to allow the USPTO to assert affirmative defenses, such as prosecution laches, in any patent validity action. Thus, the Court held that prosecution laches was available.

Second, the Court addressed whether the USPTO can raise the issue of prosecution laches in a §145 proceeding even if it had not raised it previously. Because § 145 proceedings permitted the plaintiff to introduce new evidence and arguments, fairness dictated that the USPTO must also be able to assert new meritorious defenses, such as prosecution laches.

Third, the Court considered which facts the district court should have considered when determining whether the delay in prosecution was “unreasonable.” Though the “totality of the circumstances” must be considered, the Court held that the consideration should place more weight on delays caused by the applicant than delays caused by the USPTO.

Fourth, the Court held that the USPTO had presented enough evidence to shift the burden of proof to Hyatt. It found that Hyatt’s actions “all but guaranteed indefinite prosecution delay,” and that, even though he had not literally violated regulations or statutes, he had “clear[ly] abuse[d] the patent system.” Further, the Court found that the USPTO had proven prejudice. In a proceeding between an accused infringer and a patentee, a prosecution of delay of over six years raises a presumption of prejudice. Here, the Court reasoned that Hyatt’s admission that there was a delay of seven years between the claimed priority date and the filing date of the patents at issue triggered this presumption. Alternatively, the Court reasoned that Hyatt’s “clear abuse” of the examination system was also sufficient to raise the presumption.

The Court remanded the case so that Hyatt could present his own evidence against prosecution laches.

Facts: Mylan petitioned for inter partes review (IPR) to challenge the validity of a Janssen patent. Janssen argued that the IPR would be inefficient, since two pending court cases involving that patent would likely reach a final judgment on validity prior to the IPR. One of those cases was also between Janssen and Mylan. The Patent Trial and Appeal Board (Board) agreed with Janssen and denied institution of the IPR. Mylan filed a direct appeal and a request for mandamus to the Federal Circuit.

Held: The Federal Circuit has no jurisdiction to consider a direct appeal of a decision to deny IPR institution. The Federal Circuit does, however, have jurisdiction over a mandamus request to review a failure to institute an IPR.

Reasoning: The Court found that it had no jurisdiction to consider Mylan’s direct appeal. It reasoned that federal courts can only hear “cases and controversies” within the meaning of Article III of the Constitution. Further, lower federal courts may only hear causes of action identified by statute. The Court held that no statute grants jurisdiction over direct appeals for denial of IPR institution. 28 U.S.C. § 1295(a) merely enables federal courts to review final written decisions of an IPR, but 35 U.S.C. § 314(d) prevents appeal of denial of IPR institution.

The Court held that it had jurisdiction to review Mylan’s petition for mandamus. 28 U.S.C. § 1651(a) authorizes federal courts to issue “necessary and appropriate” writs in aid of their jurisdiction. Because 28 U.S.C. § 1295(a)(4) grants federal courts “exclusive jurisdiction” over Board decisions if that decision is appealable (e.g. in the case of a final judgement in an IPR), the Court reasoned that a denial of IPR institution effectively prevents the Federal Circuit from reviewing a final decision, thereby diminishing its jurisdiction. The Court concluded that, to protect its prospective jurisdiction, it must be able to conduct review when presented with a mandamus request.

The Court held that Mylan’s mandamus request failed on the merits, however. Mandamus is reserved for “extraordinary” circumstances, but the Court found that Mylan could not show that it was being denied a legal right and that it had no other method of obtaining relief. The Court reasoned that Mylan, through its ongoing litigation against Janssen, could easily try the validity of Janssen’s patent even after the Board denied IPR institution. Thus, the Federal Circuit rejected Mylan’s mandamus request.

§ II. Copyright Cases

II.a. Supreme Court decisions

Google LLC v. Oracle America, Inc., 141 S. Ct. 1183 (2021)

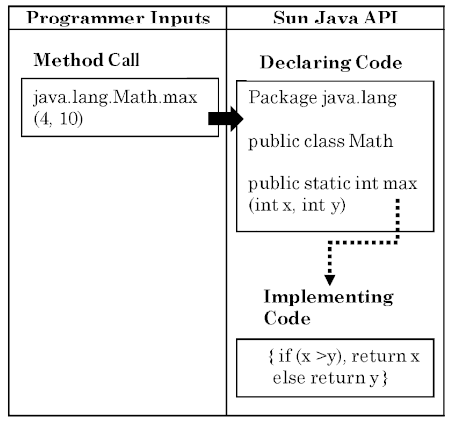

Facts: This case concerns whether copying the “declaring code” of an Application Programming Interface (“API”) is fair use, and thus avoids copyright infringement, when the copying party has written and implemented its own “implementing code.”

In 2005, Google purchased Android, Inc. to develop a software platform for mobile devices. The Android software platform used Java, a programming language many software programmers were already using. Java is a programing language developed by Oracle’s predecessor Sun Microsystems and Oracle owns the copyright in the software platform Java SE.

Google originally planned to license the Java platform from Oracle for Android, but after negotiations broke down, Google decided to build its own software platform for Android. Google developed the Android platform specifically with mobile devices in mind. The Android platform includes millions of lines of code written by Google engineers. However, the Android platform also includes about 11,500 lines of code copied from the Application Programming Interface (“API”) of the Java SE platform.

An API is a tool for programmers to access prewritten code aimed at performing functions rather than writing the raw code that provides that functionality. The Court broke down the portions of an API at issue into three parts: a “method call,” the “declaring code,” and the “implementing code.” A “method call” is a line of code a programmer will use to ask the program to perform a task. The “implementing code” is the set of instructions that will instruct the processor how to perform that task. The “declaring code” performs the needed link to between the “method call” and the “implementing code” so the desired functionality occurs. As such, while both are essential to the operation of the API, “the implementing code” requires a much greater amount of code than the “declaring code” does.

The 11,500 lines of code that Google copied were of the Java SE API’s “declaring code” so that programmers coding for Android could use the same “method calls” they were accustomed to while coding in the Java programing language.

In 2010, Oracle brought action against Google in the Northern District of California for copyright infringement. The district court ruled at trial that the API’s “declaring code” was not protected under copyright law. On appeal, the Federal Circuit reversed, stating that the “declaring code” was also entitled to copyright and remanded to the district court on the issue of fair use. The Supreme Court, at that time, denied certiorari on the Federal Circuit’s copyrightability determination.

The district court found fair use and the case was once again appealed to the Federal Circuit. The Federal Circuit again reversed, finding that “there is nothing fair about taking a copyrighted work verbatim and using it for the same purpose and function as the original in a competing platform” and remanded on the issue of damages. 141 S. Ct. 1183, 1195 (2021) (internal quotations omitted). The Supreme Court granted certiorari to review the Federal Circuit’s determinations on both the copyrightability and fair use issues.

Held: The Court did not rule on whether the API was entitled to copyright protection and instead reviewed only whether Google’s use of part of that API constituted fair use. The Court ultimately concluded that Google’s use of that portion of the API was fair use and thus did not constitute copyright infringement.

Reasoning: The Court analyzed Google’s use under the four factors of 17 U.S.C. § 107 but noted that “applying copyright law to computer programs is like assembling a jigsaw puzzle whose pieces do not quite fit.” Id. at 1998 (internal quotations omitted). The Court gave specific attention to the following factors of the “fair use” defense to copyright infringement:

Nature of the Copyrighted Work: While Congress has declared computer programs as subject to copyright, “declaring code” differs from other kinds of copyrightable computer code. First, “declaring code” is “inextricably bound” to the general system and the organizing tasks that the Court determined are not copyrightable. Second, “declaring code” is similarly bound to the “method calls” and the “implementing code” that either were not contested or were not the subject of any evidence of copying. Additionally, “declaring code” derives its value from the programmers using it who do not hold the copyright. Therefore, the Court identified that this factor “points in the direction of fair use.” Id. at 1202.

Purpose and Character of the Use: The Court said the analysis of this factor must go further than determining if the copying itself was transformative and should include the purpose and character of the use as dictated by § 107. Here the Court focused on Google’s expanding use toward new products. This “reimplementing” use furthered the development of computer programs. Id. at 1203. Since the purpose and character was transformative, even if the code was copied verbatim, this factor weighed in favor of fair use.

The Amount and Substantiality of the Portion Used: The Court suggested that the better way to view this factor in this context is to view that amount of “declaring code” copied (around 11,500 lines of code) against the much larger amount of “implementing code” (millions of lines of code) that Google wrote. The “declaring code” is inseparably bound to those “task-implementing lines.” Id. at 1205. The Court also disagreed with the Federal Circuit that Google could have only copied the 170 lines of code fundamental to writing in Java, stating that determination construed Google’s “legitimate objectives too narrowly.” Id. Therefore, this objective weighted in favor of fair use.

Market Effects: Google has made significant money from Android in the mobile computing market, a market that Oracle’s predecessor had attempted to enter. However, the Court pointed to Oracle’s predecessor’s failure to compete in that market, the sources of its lost revenue, and the risk of public harm as helping this factor weigh towards fair use. To the Court, Google’s revenue was not supplanting Oracle. Rather, it came because of third party programmer’s investments of time in learning the Java language and Google’s own efforts to developing a platform geared towards high functionality mobile devices.

Therefore, the Supreme Court found Google’s copying of portions of Java SE’s API constituted fair use.

II.b. Circuit Court decisions

Unicolors, Inc. v. H&M Hennes & Mauritz, L.P., 959 F.3d 1194, 1196 (9th Cir. 2020), cert. granted in part, 141 S. Ct. 2698 (2021)

Facts: This case determines the scope of the knowledge inquiry under 17 U.S.C. §411(b), which prevents the filing of a lawsuit for copyright infringement without a valid copyright. This case also determines the meaning of the Copyright Act’s publication standard, deciding the requirements for a single-unit registration.

Unicolors Inc. (“Unicolors) filed suit against H&M Hennes & Mauritz L.P. (“H&M”) claiming that H&M infringed its copyright by selling two clothing items made from Unicolors’ copyrighted fabric design. Unicolors filed its copyright registration (‘400 Registration) as a single-unit registration of thirty-one separate designs. Unicolors registered the date of first publication as the date when it presented the designs collectively to its salespeople. At a later date following the presentation, Unicolors placed nine of the works in its showroom available for public view and purchase.

H&M argued that because Unicolors sold nine of the works in the ‘400 registration separately to customers, the works identified in the ‘400 single-unit registration were not first sold together or at the same time. To register a copyright as a “single unit” the works must have been first sold or offered for sale in some integrated manner. H&M further argued that because Unicolors knew that the works were not sold as a single unit, the intent requirement to invalidate a copyright registration under 17 U.S.C. § 411(b) was met, and the copyright registration was invalid.

The district court upheld the validity of Unicolors’ registration on two grounds. First, H&M failed to show that Unicolors intended to defraud the Copyright Office at the time of filing its application and thus its registration was valid. Second, although Unicolors may have sold the works separately, the collection of works were made available to the public at the same time and thus “published” on the same day. The jury reached a verdict in favor of Unicolors. H&M appealed and argued that the court erred in finding Unicolors’ copyright registration valid.

Held: The Ninth Circuit reversed the district court’s decision and held that a single-unit registration under 37 C.F.R. § 202.3(b)(4) requires that the work is first made available for sale to the public in a singular, bundled collection. The Ninth Circuit also held that a copyright registration can be invalidated through constructive knowledge under 17 U.S.C. § 411(b). Therefore, Unicolors’ knowledge that the works were not first published in a singular bundled collection was enough to invalidate Unicolor’s registration.

Reasoning: The Ninth Circuit applied the principles of statutory interpretation to determine the requirements for a single-unit publication under the Copyright Act. The Ninth Circuit looked to the definition of publication under the Copyright Act as “offering to distribute” the “work to the public by sale or other transfer of ownership” regardless of whether a sale occurred. Because Unicolors did make the designs available for the public’s purchase at the same time, Unicolors did not meet the single-unit registration requirement.

The Ninth Circuit interpreted the knowledge requirement under 17 U.S.C. § 411(b) as not whether Unicolors knew that the registration ran afoul of the single-unit requirement but whether Unicolors knew that certain designs in the registration were published separately to exclusive customers. The court expressly chose to not infer an intent-to-defraud requirement in the statute. This left a split between the Eleventh and Ninth Circuit.

Unicolors filed a petition and the Supreme Court granted certiorari to determine (1) whether the Ninth Circuit misapplied the publication standard when it determined that a single-unit registration requires a collection to be “offered for sale as part of a ‘bundled collection and (2) whether 17 U.S.C. § 411(b) requires a fraud standard to invalidate a copyright.

§ III. Trademark/Trade Dress Cases

Ezaki Glico Kabushiki Kaisha v. Lotte Int’l Am. Corp., 986 F.3d 250 (3d Cir. 2021), as amended (Mar. 10, 2021), cert. denied sub nom. Glico v. Lotte Int’l Am., No. 20-1817, 2021 WL 5043589 (U.S. 2021)

Facts: This case concerns the doctrine of functionality in trade dress protection of product designs.

Ezaki Glico (“Ezaki”) a Japanese confectionary company, sells a product line of thin, stick-shaped cookies. The cookies are partly coated with chocolate or a flavored cream with an uncoated portion to serve as a handle. Ezaki has two incontestable trade dress registrations for the elongated rod partially covered with chocolate, another for almonds on top of the chocolate or cream, and a utility patent for “Stick Shaped Snack and Method for Producing the Same.”

Lotte International American Corporation (“Lotte”) began selling Pepero, a similar-looking stick shaped cookie partly covered in chocolate with an uncoated portion. Ezaki filed suit for trade dress infringement in the district court. The district court granted summary judgment in favor of Lotte holding that the Ezaki’s product configurations were functional, and therefore nonprotectable trade dress.

Ezaki appealed the district court’s order for summary judgment on the grounds that its product design is not essential and therefore not functional.

Held: To be considered functional and thus ineligible for trade dress protection, product designs do not need to be essential, just useful. Because both the stick shape and the uncoated handle were useful for holding the snack, the Third Circuit held that Ezaki’s trade dress was functional and thus nonprotectable, thus affirming the district court’s holding.

Reasoning: The Third Circuit determined that the prohibition on trade dress protection for functional elements is not narrowly limited to essential product configurations. The Supreme Court’s decision in Qualitex Co. v. Jacobson Products Co., 514 U.S. 159 (1995) listed several ways in which a product feature is functional but not hold that a product feature is considered functional “only” if it is essential. Because functionality is intended to keep trade dress protection as a workaround from patent law, the test for functionality should be interpreted similarly to patent law.

In analyzing the functionality of Ezaki’s trade dress, the Third Circuit looked to the usefulness of the uncoated portion of the snack, the shape of the snack itself, and the design as a whole. The Third Circuit also pointed to Ezaki’s promotion of its snack’s utilitarian advantages.

The Third Circuit noted that the availability of alternative designs was unimportant for the functionality determination because even if there are alternatives, a product design can still be functional. The Third Circuit also determined that the district court erroneously considered Ezaki’s utility patent for the making of the snack’s stick shape. Because the features claimed in the trade dress were for the shape itself and the shape was not the “central advance” of the utility patent, the patent shed no light on whether the trade dress was functional.

The Great Recession taught an important lesson: if economic pressures prevent your organization from buying new software, then be on the lookout for an audit of your existing software licenses. Software vendors have seized upon noncompliance issues as leverage in convincing reluctant customers to buy new products.

For the past fifteen years, we have advised clients on how to manage software audits, even litigating when necessary. Over time, we’ve seen audits become consistently more sophisticated—employing well-known consulting firms, elaborate and tricky reporting mechanisms, and vendor-friendly scripts or automated review processes.

In this two-part article series, we will first delve into the steps of a software audit and tips for managing audits. Then, we will explore ways to improve your agreements to limit audits and put you in the best position possible when the auditor comes knocking.

Part One – Steps of the Software Audit and How to Manage It

By John Gary Maynard, III

What should I do upon receipt of an audit demand?

When you receive an audit demand, there are several things you should do immediately.

Ownership. First, determine who will “own” the software audit. Is it your legal department or IT? The worst thing you can do is create ambiguity about who is managing the audit. You should also consider whether outside counsel should be engaged. Outside counsel can provide key advantages, particularly with respect to preserving privilege and avoiding admissions.

Collect Relevant Documents. At its core, a software audit is a contract dispute. Identifying and collecting all governing contracts and related documents is therefore imperative. If in doubt, collect it. Of course, there may be executed contracts between the parties that govern, but note that many vendors use clickwrap agreements. It may be difficult to obtain copies of these agreements, or even to verify through the vendor’s website which version applies to your software. Don’t forget that related documents, including settlements of prior disputes, may be set forth in emails or letters rather than in formal agreements. Vendors sometimes refer to these as “close letters.” These can be crucial. Whether due to the passage of time or sloppiness on the part of the vendor, it is not uncommon for vendors to present noncompliance fees based upon usage that was previously released.

Confirm Basic Terms. Although the terms of software contracts are as varied as the types of software, you should conduct an initial review of the relevant documents to answer the following questions: (a) which legal entities of the company are subject to the audit? (b) what is the geographic scope of the audit? (c) what software products are covered by the audit? and (d) what are the relevant deadlines? On that last point, you don’t want to waive arguments by failing to respond in a timely manner.

Control Communications. Put procedures in place to control communications with, and about, the vendor. Establish a single point of contract, preferably someone with sound judgment and a good understanding of the business issues. We recommend a businessperson for this role rather than a lawyer. Once you’ve identified the single point of contact, notify the vendor and your employees. Guard against employees unwittingly making admissions regarding noncompliance. Relatedly, verify whether the vendor has any on-site personnel. If so, ensure your employees with regular interaction with the on-site vendor personnel do not talk about the audit.

What does the audit process look like?

Each vendor has its own process, but large vendors typically employ outside consultants as auditors. Shortly after issuing the audit demand, the vendor will likely introduce you to the auditor. Don’t be surprised if the vendor does not participate in the audit from that point forward.

Kickoff Meeting. Once the auditor has been identified, you will be asked to participate in a kickoff meeting. There are several issues to consider before participating in this meeting, but, at a minimum, you need to confirm confidentiality of the audit. Your software contract likely contains confidentiality obligations between you and the vendor, but you likely will need a separate agreement with the auditor.

The Rest of the Audit Process. In general, the next steps will include: (a) an explanation of the data collection process, (b) collection of the data, (c) review of the data, (d) confirmation of the data by each party, and (e) monetization of any noncompliance issues. Each step is potentially fraught with peril. Whether you use inside counsel or engage outside counsel, it is imperative that counsel be involved at this point in the process, even though counsel likely will not communicate directly with the auditor.

How do I manage the audit process?

The goal with any audit is to resolve it with the least disruption to the company’s business, and at the lowest price. Treating the audit as a business transaction, not an adversarial proceeding, is the best approach. Most vendors do not want to sue their customers. But this does not mean the audit process is not adversarial. Audits routinely identify alleged noncompliance issues, which vendors then attempt to monetize. The numbers can be extremely large—we’ve seen initial demands in excess of $100 million. Software agreements are simply too complicated for noncompliance issues not to arise. But those complicated agreements also provide opportunities for reasonable disagreement about the scope of noncompliance. It is a tricky process.

Role of Lawyers. Lawyers have important roles to play and should be involved from the very beginning. Obvious roles for lawyers include reviewing and revising confidentiality agreements with auditors, as well as drafting any final settlement agreements or close letters. But the real value of lawyers is preserving privilege issues and avoiding admissions. At the outset, one way for lawyers to do this is to help business personnel establish reasonable parameters for the scope of the audit. Providing auditors with more information than they are entitled to rarely benefits the company. The single point of contact will convey the company’s message in business terms, but that message will be guided by the terms of the relevant agreements that benefit the company.

Similarly, lawyers should help establish the parameters of the data collection process and the subsequent review of such data. This is particularly important for businesses in highly regulated markets. An audit should not unwittingly trigger regulatory breaches. Relatedly, several vendors use automated review procedures with prepopulated language that cannot be modified. These tools may appear to be an innocuous way to confirm usage information, but the prepopulated fields often contain admissions the company should not make. For example, the template might state all information is final and cannot be changed or modified. We’ve even seen some forms that have the company swear under penalty of perjury that the information is accurate and complete.

Finally, at the end of every audit, the business and its lawyers should work together to conduct a post-mortem. It is important to know if any noncompliance issues arose from inadequate internal controls. Any such issues should be addressed. Similarly, the company should consider whether technical problems or practices undermined or interfered with the audit. Finally, the company should also evaluate the vendor: was the vendor a good business partner during the audit? We once assisted a client who generated most of its revenue during a particular quarter. The vendor agreed to move the audit to prevent disruption during the company’s busiest season. It was a simple gesture by the vendor, but it generated a lot of goodwill with the company.

Are there events within the control of the company that trigger an audit?

As previously noted, economic downturns can trigger audits. But other events that are within the control of the company can also trigger audits. For example, corporate restructuring can trigger an audit, because such restructuring may make changes to the identity of the licensed user. Most software agreements not only limit use to specific entities but also prevent an assignment to other legal entities—including affiliates of the original licensee—without the prior written consent of the vendor. Rapid growth can also trigger an audit. Most licensing metrics are tethered to the size of the licensee, such as the number of processors. Rapid growth, therefore, increases the incentive of a vendor to audit a licensee. Finally, nonrenewal of an existing software license can trigger an audit.

Final consideration: Not all licensed software is the same.

Broadly speaking, there are two types of licensed software. First, there is software that facilitates the operation of a business. Here, the business does not incorporate the software into a product that it sells but simply uses the software to make daily operations easier. For example, a doctor’s office may use billing software in this way. Conversely, there is software that a company incorporates into its own product—the code that operates a vehicle’s entertainment system, for example. Not surprisingly, this second type of software is typically unique. Audits regarding business operation software rarely result in formal litigation. It is simply in neither party’s interest to formally litigate. Product-based software, however, can and often does result in litigation.

With respect to business operation software, each vendor generally has its own licensing metric. Understanding that metric can go a long way toward identifying the likely focus of noncompliance issues. One common metric is the number of “users.” This may seem like a relatively benign term, but disputes can arise over terms like “named users,” “concurrent users,” and “access.” For example, with respect to the term “access,” ambiguity in the agreement might allow the vendor to define a user as anyone with the ability to access the software as opposed to anyone who actually accesses the software. This definitional distinction could literally be the difference in millions of noncompliance fees.

With respect to product-based software licenses, it is difficult to generalize, because these are typically not off-the-shelf licenses that follow familiar patterns.

In any event, regardless of the nature of the software, the terms of the agreement will be crucial in determining noncompliance issues. In the next article, we will discuss ways to improve your agreements to avoid or limit an audit.

Historically, the legal industry has lagged behind many other professions in the diversity, equity, and inclusion space. The industry is working to change that today, as DEI-focused recruitment and retention efforts take high priority within the offices of forward-thinking law firms and in-house legal departments.

Executive management and recruiters are embracing every opportunity to build teams that not only fulfill client expectations for diversity but also benefit their own organizations. Research, including yearslong tracking by McKinsey, has repeatedly shown that companies with higher levels of diversity outperform their peers financially, as well as in other areas. When a team includes people of various genders, ages, ethnicities, cultural backgrounds, sexual orientations, etc., it is not only the right thing to do, but it also holds the potential to produce more creative, innovative, and effective results.

Achieving the diversity goals of your firm or department requires attention on two fronts: attracting a diverse group of new talent and working to support and retain attorneys already on your team. Engaging contract attorneys can support achieving both of these objectives.

How Contract Attorneys Can Help You Retain Diverse Talent

Lawyers’ perceptions of their organization’s culture are built on their experiences in a wide range of areas. Work-life balance, collaboration, equitable compensation, the opportunity to work remotely, and the quality of work they are assigned register high on the list of what matters to lawyers as they determine whether to switch jobs or stay put.

Some of these factors can be particularly important to women and people of color. A recent ABA report found, for example, that 68% of women lawyers and 68% of lawyers of color cited better work-life balance as an important factor when deciding to change jobs. Law firms and legal departments looking to retain top talent, especially in underrepresented groups, must understand these priorities, evaluate where their organizations may be falling short, and enact more supportive policies.

How can engaging contract attorneys help? Contract attorneys fill staffing gaps and lessen internal workload, promoting improved work-life balance and preventing burnout among associates. Contract staff can also reduce the burdens associated with routine tasks, such as document review and discovery, to help ensure associates can do the higher-level work that makes them feel more valued and fulfilled. Additionally, having a blended team of associates and contractors can increase team productivity, fueling higher morale and a greater sense of camaraderie.

Bringing contract attorneys into the mix demonstrates empathy for the challenges the lawyers on your team face and communicates your commitment to creating a nurturing culture where they can thrive.

How Your Alternative Legal Service Provider Can Help You Attract Diverse Talent

When you demonstrate your commitment to diversity and present your organization as welcoming to all, you are much more likely to attract diverse candidates. Again, that perception of your firm or department is created when candidates discover that your culture provides work-life balance, equitable compensation, remote work opportunities, and so on.

If you work with contract attorneys, this perception can also be augmented by your choice of alternative legal service provider (ALSP). Working with a woman- or minority-owned firm, or another ALSP that truly understands and supports your DEI goals and initiatives, can give you a leg up in recruiting diverse talent. In general, reputable ALSPs have access to a deep and diverse pool of candidates, for a number of reasons. For example, they are not limited by geography; they can recruit across a much broader expanse of talent and specialization. They can also offer, through contract work, the work-life balance that is especially important to women and attorneys of color, as well as esteemed lawyers in later stages of their careers, who are often looking to share their expertise on their own terms.

As you connect with these candidates and incorporate them into your staff, you can not only bring diversity of thought to your team today but also tee up the potential for bolstering your organization’s diversity in the long term. While contract attorneys are typically brought on for temporary assignments, you may have the option to convert those who prove to be ideal matches for your organization into permanent staff. Your ALSP can help you recruit and onboard those individuals as full-time members of your team.

Talk with your ALSP about your DEI policies and goals. Let them know what you are doing internally to provide an inclusive culture, and discuss ways they can partner with you to achieve your short- and long-term objectives. A good ALSP will have the capability to connect you with exceptional contract attorneys to energize your initiatives and strengthen your team.

Over the past year, SPACs have been through market shifts, regulatory thrashing, economic issues, novel litigation theories, and SEC enforcement actions. I touched on all of these in my previous post for the SPAC Notebook, but for this month’s edition, I turn to some of the most commonly asked but not necessarily answered questions that are top of mind for many SPAC teams right now.

These two questions keep popping up in my inbox:

How can our SPAC team handle the 1% excise tax?

Are there new avenues to get a SPAC deal done?

How to Handle the 1% Excise Tax

The Inflation Reduction Act, which was signed into law on August 16, 2022, establishes a new 1% excise tax on certain stock buybacks by domestic public companies. Many experts, including most attorneys I’ve spoken to, believe the provisions of this new law could be broad enough to possibly pull SPAC redemptions into their sphere.

Option 1: Liquidate Before Year-End

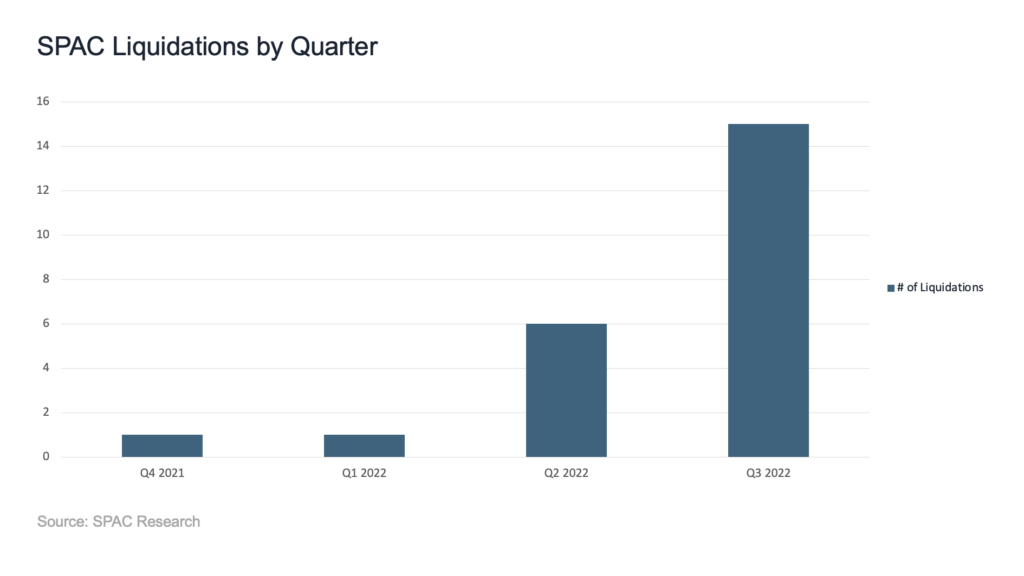

As a result of the new excise tax, most SPAC teams that do not currently have a deal in the works are rushing to liquidate before January 1, when the tax becomes effective. According to SPAC Research, as of December 2, 64 SPACs have liquidated this year, with the frequency of liquidations increasing significantly in the last two quarters. There were 18 liquidations in October.

Source: SPAC Research

Although we have not seen many post-liquidation lawsuits so far, some litigators expect that the increased number of liquidations will prompt the plaintiff’s bar to test some of those liquidation decisions and proceedings in court. Therefore, a careful look at whether an extension of D&O insurance coverage (also known as a tail) for the SPAC’s directors and officers post-liquidation is warranted.

Option 2: Extend and Cover the Tax Bill

Other SPAC teams that believe they will get a deal done before their deadline or have one on the table but are waiting to close in early 2023 may be willing to risk becoming subject to the excise tax. These teams usually are looking to extend their investment period for another three to six months.

But, of course, with such an extension landing the SPAC and any of its redemptions square into 2023, the question is who will pay for the excise tax? Will it be the SPAC sponsor or the shareholders? Will this tax come out of the trust funds, or will the sponsors need to come up with additional sponsor capital to cover what could end up being a multimillion-dollar tax bill?

Some SPACs, like the Data Knights Acquisition team, realizing that this could become a sticking point for shareholders who need to approve their extension, are coming out with promises that they will not touch the trust but will cover the tax out of sponsor capital. Other SPAC teams will likely follow this strategy as well.

Option 3: Extend but Leave the Tax Bill to Shareholders

Other SPAC teams may have a different view. Depending on how the SPAC’s documentation is written, some SPACs may take the position that the excise tax, like franchise and other taxes, will need to come out of the trust funds. This will, of course, endanger the $10-per-share shareholder investment, especially if these same SPACs decide to keep their trust funds in cash to avoid tripping the SEC’s Investment Company Act safe harbor. Will the shareholders of these SPACs go along with this idea, or will they object via a lawsuit? We have yet to find out.

New Avenues for SPAC Dealmaking

Necessity is the mother of invention, and that proverb is proving to be true in SPAC land. Aside from the creative ways SPAC teams are enticing their shareholders to approve extensions, many teams are looking for alternative avenues for getting a deal done.

Having realized that they may not have what it takes to land or close a deal but not wishing to liquidate, some SPAC teams now are considering two options: a team swap or a public company merger.

Team Swap

In a team swap, the old team enters a sharing or hand-over arrangement with a new team, in which they share some of the economics of the deal, but essentially the new team takes the reins on finding a suitable target and/or closing the transaction. The new team invariably brings deal know-how and connections to the table. As for the old team, walking away with a fraction of interest in a potential deal versus 100% of interest in no deal is often a better alternative.

As you can imagine, these swaps are difficult to accomplish. They are also challenging when it comes to insurance coverage. The old team wants to be covered in case they’re pulled into a lawsuit or an enforcement action after the swap. And the new team, of course, wants to be protected as well.

For insurance underwriters who based their terms and premium pricing on the track record of the old team, a new team with a different track record may not be palatable. If the underwriter is not willing to extend the original policy to the new team, the new team may need to go looking for new coverage, which may be unavailable or a lot more expensive than what the old team was able to obtain 18+ months ago.

The costs of this coverage will need to be folded into the swapping arrangement the two teams ultimately agree on. Having this conversation with your SPAC insurance broker before entering into any agreements is key.

Complicating the situation is coverage for the outgoing team after the swap. If the new team obtains a new policy, it is unlikely to cover the old team’s directors and officers, and the old policy is unlikely to continue after the swap. The outgoing team then will need to consider whether it needs to buy tail coverage for its original policy, another cost that it may not have anticipated. The new team may be willing to cover this cost, but again, this discussion needs to happen before completing the swap. That way, the insurance broker will be able to advise the two teams on the best course of action.

Public Company Merger

On the theory that some public companies may be more willing and able than private companies to enter into a merger with a SPAC, some SPAC teams are considering a merger with an already existing public company. An example of such a transaction is the October 31, 2022, closed merger of Coeptis Therapeutics Inc. with the SPAC Bull Horn Holdings Corp. The SPAC sponsor reportedly liked the idea because of greater transparency stemming from the publicly available performance record of the target.

For the public company, a merger with a SPAC provides a cash infusion from the SPAC’s trust account and access to the SPAC team’s expertise. For the SPAC, aside from the undeniable benefit of getting the deal done, the risk is presumably reduced for several reasons. First, there are fewer issues with public company readiness, a problem that has plagued many newly de-SPACed companies. And second, there is the greater transparency of an already publicly filed business. I’ll leave it to the bankers to opine on whether the economics of these kinds of deals will benefit the investors in the SPAC and the target company.

From the insurance perspective, interesting questions come up as far as coverage of the original SPAC and its team prior to the merger. As with other unusual SPAC-related situations, the insurance coverage and costs need to be looked into thoroughly ahead of making any major budgeting decisions.

Mergers with already public companies arguably miss the point of the SPAC vehicle, which was designed as an alternative to a traditional IPO. However, in the current hostile market, I would not be surprised to see other similar transactions in the near future.

Looking Ahead