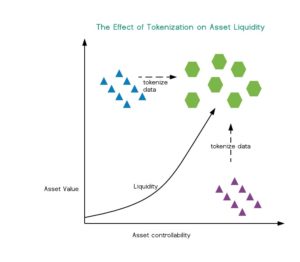

Blockchains reduce the need for “trust” in legal transactions. From a legal perspective, trust has some specific meanings with respect to custody, control, and transactional risk. It can be accurately defined as “reliance on assurance of others to reduce transactional risk.” Blockchains radically shift the economics of providing transactional assurances.

For example, blockchains reduce the cost and complexity of obtaining assurances of asset ownership and control. Blockchain offers a cheaper and more reliable mechanism of creating, storing, and proving evidence.

Commercial and financial legal processes currently rely on numerous systems to reduce overall transactional risk and give people enough confidence to transact. A critical legal inquiry regarding any kind of property is, who owned title, when, and what is the transactional history? In asset transactions, property registries provide custodial and financial histories. To risk buying an item or making a loan secured by property, a buyer or creditor must be able to verify that the person purporting to own the property really does have title, and that there are no other enforceable inconsistent claims.

For high-value, complex transactions, this means obtaining assurances of (1) proof of authoritative title to an asset (title is clean and untampered), and (2) proof that the proof of title is reliable (the source of assurance (1) is clean and untampered). Underpinning it all is property law. Rules of property law apply whether the object in question is a house, a retail installment contract, or a digital token. Critical to property law is the concept of title, or ownership of property.

Legal systems have developed multiple property registries and custodial systems to manage information and give buyers, lenders, and invested parties the ability to verify whether a specific deal represents an enforceable obligation. Financial market infrastructure spends tremendous sums to maintain structures that provide assurances of things like chain of custody and title.

Registries. Creditors and other interested parties file notices with deeds registries, secretaries of state, departments of motor vehicles, and places a creditor checks for notice of an adverse interest. Common examples are land registries and, in the United States, the U.C.C.-1 filing registry within a state. The registry record is deemed authoritative for legal enforcement of contracts, and insurers, lenders, buyers, and sellers rely on it equally to track rights and obligations. The records produced by central property registries supply chain of title and custody details.

Registries like these developed out of need: without a reliable system for registering, or “perfecting,” one’s interest in property, market confidence in buying, selling, and lending is disincentivized. Functional registries make functional markets.

Custody and Control of Intangibles. Second-and-third order monetization of a value stream often involves intangible property. For example, financial products leverage contract rights and obligations to create additional assets and revenue streams like securities and derivatives. In pre-internet commerce, custody and control of intangible assets were proved by “possession”; a lender holding a note as a security pledge against a loan might actually take possession of the note. It is impractical to run valuable paper instruments from holder to holder in real time, so the notes were placed with a trusted third party who acted as intermediary, for example, holding the notes in custodial trust, matching and settling promises to pay. The market assigned possessory rights to custodial agents who held assets “in trust” and maintained their chain of title so deals were free to flow without paper slowing them down.

Electronic Contracts. With the advent of electronic contracts, the law evolved a new method of perfecting a security interest in digital originals of notes and chattel paper. The key, when vaulting an electronic contract, is to prevent multiple copies that might result in adverse claims, or “double spends” of the same obligation. Sounds familiar!

Electronic contracting laws like Uniform Electronic Transactions Act (UETA) established standards for vaulting and proving custody and control of digital assets. The UETA drafters, however, noted that their recommendations were based on late-20th-century technological capabilities to establish “control.” UETA’s custodial “control” requirements substitute for possession to perfect electronic contracts in the absence of a unique digital “token” to represent a contract. The drafters looked to the market to develop better systems of digital asset control.

Where Blockchain Comes In

A better property registry. Blockchain gives us a decentralized, tamper-evident record of what happened and when with respect to data stored in specific tokens. This tamper-evident ledger means less reliance on central authorities to prove the integrity of assets. A blockchain-based property registry proves its own transactional history.

Assets that prove their own chain of custody. Blockchain-based data objects can represent any number of property types extrinsic to the blockchain, as well as assets that are native to digital technology, e.g., tokens. A blockchain-native asset represented by a token is inherently and immutably tied to its transaction history. This means assets stored in a blockchain can prove their own titles, chains of custody, and transactional records.

Blockchains can get chain of custody right. Without structures that prove chain of custody, the lack of reliable proof structures has a chilling effect on legitimate commerce. Blockchain offers a low-cost way to scale legal infrastructure and build commercial rails on the bedrock of rule of law.

Poorly controlled legal proof structures are also a problem with existing custodial systems. For example, after the 2008 recession, we learned of multiple frauds in the system of keeping chain of custody of loan records. Many assets were so poorly tracked that when it came time to enforce legal rights, creditors were left holding assets with chains of custody any lawyer could challenge to defeat the creditor’s claim. Blockchain storage of contract assets solves this problem, ab initio.

Blockchain proof of title, custody, and transaction history reduces the need to rely on external assurances. This opens economic potential wherever there was previously a lack of reliable legal infrastructure. Along the way, blockchain will shed light upon, and drive the transition to, more efficient methods of proof in digital infrastructure.

On October 17, 2018, the Cannabis Act came into force in Canada, establishing a comprehensive legislative scheme governing the licensing, production, distribution, and sale of cannabis and related products for recreational use. Canada’s nascent recreational cannabis industry has faced its share of growing pains, but there is reason for optimism moving forward. Statistics Canada estimates that the illicit market for cannabis was worth approximately CDN$5 – $6 billion (US$3.79 – $4.55 billion) in 2015, while a 2018 Deloitte report suggests that the total Canadian cannabis market could generate up to CDN$7.17 billion (US$5.44 billion) in sales in 2019. If the sales figures forecast by the Deloitte report are achieved, that would put the cannabis market on the same footing as both the Canadian wine industry and the Canadian spirits industry.

Excitement surrounding legalization has led to a flurry of capital markets activity in Canada, resulting in billion dollar market capitalizations for several Canadian cannabis companies traded on the Toronto Stock Exchange (“TSX”), as well as the one Canadian cannabis company that currently trades solely on the NASDAQ.

Investor optimism is not fueled exclusively by the market potential that exists within Canada’s borders; rather, international opportunities represent a significant growth target. A 2018 report published by CIBC suggests that the global cannabis market could reach approximately CDN$25 – $30 billion (US$18.96 – $22.75 billion) in 2020. The U.S. could play a significant role in the global cannabis economy, as a study conducted by the Brightfield Group estimates that Canada and the U.S. will account for more than 86% of global cannabis sales in 2021.

Although cannabis is currently legal for recreational use in ten U.S. states and for medical use in 33 states and the District of Columbia, cannabis remains a Schedule 1 narcotic under the U.S. federal Controlled Substances Act. This classification has prevented Canadian cannabis companies from entering the U.S. market. Although cannabis may be exported from Canada for medical or scientific purposes under the Cannabis Act, an export permit may be refused if such exportation would contravene the laws of the country of import, or if such exportation would not comply with the permit for importation issued by a competent authority of the country of import.

Notwithstanding these obstacles, enthusiasm regarding the U.S. market was on full display when Tilray Inc.’s shares jumped 28.95% on the same day it was reported that the Canadian cannabis producer had received approval from the U.S. Drug Enforcement Agency to export cannabis to California for a clinical trial.

What does this mean for U.S. cannabis companies?

U.S. stock exchanges are regulated by federal legislation and, as a result, you will not find any pure play U.S. cannabis companies listed on the major American stock exchanges. Similarly, the TSX and its affiliated TSX Venture have taken the position that companies with operations or investments in the U.S. cannabis industry will be in violation of the listing requirements of their exchanges and thus subject to de-listing.

However, Canada’s more junior exchange, the Canadian Securities Exchange (the “CSE”), has welcomed Canadian and U.S. cannabis companies alike, listing 116 companies that operate in the cannabis industry, as of the date of this writing. Rather than prohibiting issuers with ties to the U.S. cannabis industry, the CSE has taken a disclosure-based approach, requiring its issuers to disclose the extent of its activities in the U.S. and the risk that its activities present from a U.S. legal standpoint.

Investor response to CSElisted cannabis companies has been extremely positive, with investors showing a particular appetite for companies offering exposure to the U.S. cannabis market. While historically being considered a “third-tier” Canadian stock exchange, the CSE is gaining notoriety, attracting industry-leading U.S. cannabis companies that have been denied access to more traditional exchanges.

For example, inMay 2018, MedMen Enterprises Inc., a leading cannabis retailer in the U.S., began trading on the CSE at an implied value in excess of US$1.6 billion and on November 16, 2018, filed to raise CDN$75 million (US$56.88 million) via bought deal. In October 2018, Curaleaf Holdings Inc., a vertically integrated cannabis cultivator and retailer, closed a private placement on the CSE which raised approximately US$400 million, implying a valuation close to US$4 billion. The most recent debut on the CSE was that of Acreage Holdings, a multi-state cannabis producer that boasts former House Speaker John Boehner and former Canadian Prime Minister Brian Mulroney as board members. Acreage Holdings began trading on the CSE on November 15, 2018, shortly after raising US$314 million in a private placement, implying an enterprise value of approximately US$2.1 billion.

How are U.S. cannabis companies becoming listed?

The most popular approach to listing on the CSE by far is the reverse takeover, or “RTO”. RTOs involve the entity acquiring a publicly-listed shell or dormant company to pursue listing. RTOs are typically completed by way of a statutory amalgamation or arrangement and may require approval of each company’s shareholders, depending on the structure of the transaction and constating documents of the companies.

Compared to an IPO, RTOs are generally less time consuming and expensive and do not necessarily need to be accompanied by a concurrent equity financing—although MedMen, CuraLeaf and Acreage Holdings each completed private placements connected to their respective RTOs.

Another primary driver of expediency in RTOs is that they do not require regulatory review by securities regulators, and rather only require approval of the stock exchange. While a document with prospectus-level disclosure is still a requirement, eliminating the review of the securities regulators is one less obstacle to face in an RTO process.

Looking forward

There has been growing support to amend federal cannabis laws in the U.S. On June 7, 2018, Senators Cory Gardner and Elizabeth Warren introduced the Strengthening the Tenth Amendment Through Entrusting States (STATES) Act in Congress, which would amend the Controlled Substances Act to make it impossible to prosecute individuals and corporations who are in compliance with U.S. state laws on cannabis. A companion bill was introduced on the same day in the House of Representatives by Representatitives Earl Blumenauer and David Joyce.

The STATES Act would not remove cannabis as a Schedule 1 narcotic, meaning that cannabis would remain federally illegal. However, the STATES Act provides that compliant transactions would not be considered trafficking and would therefore not result in the proceedings accompanying an unlawful transaction. With this distinction in mind, it remains unclear what impact the STATES Act, if passed, may have on the willingness of U.S. stock exchanges and federally regulated banks to participate in the U.S. cannabis industry.

While much uncertainty remains with respect to the long-term outlook of the U.S. cannabis market, there appears to be a significant appetite among investors to participate in this burgeoning industry. As of right now, the most attractive way for U.S. cannabis companies to capitalize on this enthusiasm and to access capital markets is to look north of the border, where the CSE awaits with open arms.

While hanging around the water cooler the other day, I took an informal survey of a few colleagues. “How many of you are finding the task of addressing private information in compliance with increasingly complex laws, regulations, and corporate mandates to be hugely fun?” Unsurprisingly, the feedback was unanimous; everyone was loving it. They couldn’t get enough. They clamored for greater records management responsibilities and litigation response obligations. They also mentioned that there is no better end to a long workday than an involved information-security training, provided that their lunchtime could be interrupted for dental work with no anesthesia.

As it turns out, employees in the real world don’t really like doing anything beyond their real jobs, and certainly don’t want to have anything to do with the perceived tedium of classifying their files according to a growing set of company rules. For the vast majority of people, information management is about as fun as a root canal. And yet, effectively managing information has always been essential and is more and more a differentiator for organizations. This capability impacts a company’s reputation, risk profile, and innovation initiatives.

What can companies do? They can’t outsource their obligations—even if a third party is brought in to do some of the legwork, ultimately the obligation to comply lies with the company. Neither can they ignore the issue because there are increasingly more laws that prescribe how companies and their employees must manage information from its creation to its proper destruction. Similarly, there are far more consequences in failing to get it right. It’s an unenviable position for companies; they need their employees protecting the company’s information assets, but most employees are disinterested at best, viewing themselves to be full up with “real” work that trumps a concerted focus on these efforts.

Generally, there are two kinds of employees: the ones who are motivated by carrots, and the ones who must be inspired by sticks. There are some employees who will follow rules because they are told to and because being proactive is good for the company. However, if there is no compelling reason for employees to do something, they often fall into the latter category of needing a consequence, a penalty, or a loss of some benefit or privilege before they will dream of doing a task at work outside of their perceived job scope.

That brings us to a confluence of realities: more downside, more attacks on the IT systems, more laws dictating what is required and penalizing companies when they fail to comply, and more employees behaving badly, uninspired to lift a finger to help your company better manage information.

Here are seven keys to fix such a problem.

1. Set the Tone at the Top. The CEO in some respects is the soul of the company in that he or she sets the big-picture objectives for the organization. This is commonly communicated through a mission statement, vision, and code of ethics. These concepts and values are then seen as calls to action by others in the organization and rapidly become operationalized. When the CEO or other executives message the importance of a company initiative or action, the employees (everyone below them) are more likely to listen and follow their lead. For example, if the CEO decides that being a “greener” company is important, then initiatives that advance that idea will get more attention and funding. Employees will more likely do what it takes to make the company greener. Thus, one thing that will be essential to making information activities come to life in the company is for the executive team and others in management to support the information project or program and message its importance to all employees. Another way they can show support is by funding such activities and publicly recognizing successful efforts.

2. Make It Part of the Job. One of the best ways to get folks to take on protecting private information is to make it a part of their job responsibilities. For many businesses, at most they develop policy and expect that employees will read, understand, and follow the directives. That is usually the last time the policy is addressed until something bad happens. Then everyone wants to know what went wrong. What commonly goes wrong is that employees have a black and white view of their roles and responsibilities. They disregard policies as irrelevant to their jobs if adequate context isn’t provided.

The company can “legitimize” the activity by making it a part of the employees’ job responsibilities in writing and by making it clear that failure to do as required will, for example, impact performance incentives. When compliance with a policy is tied to compensation, it tends to get employees engaged. That would be more of the stick approach.

In terms of the carrot, why not have high-potential employees nominated by senior leadership to serve as information stewards? Formalize the role, make it a coveted position, and recognize and reward them for participating. You will find that you have inspired these employees to be your eyes and ears in the business. This causes a chain reaction whereby those around them start caring more as well.

3. Train the Employees. A policy itself, no matter how comprehensive and clear, is only as good as the training and change-management that accompanies it. Parking a myriad of policies on a website and thinking employees will search to find and master them is wholly unrealistic. Not only that, but having policies that no one follows is a liability. “Isn’t it true that your company has a privacy policy, you didn’t know about the policy, and in fact were never trained on the policy . . .” You get the idea.

Providing a written policy or other directive tells employees what is expected; training them on it helps ensure they understand what they must do in greater specificity. In other words, policy is not enough. Training and perhaps even testing on the mastery of the training is far more effective.

Remember, however, that employees can’t take in endless training sessions on one topic after another. Be mindful to not put too much in front of them at once and spread it out to maximize the training’s effectiveness. In other words, limit how much training employees receive, given the law of diminishing returns.

Training should be an important tool in your arsenal when it comes to ensuring that employees are able to digest and apply vital policy concepts. It is a stepping-stone to behavioral change. One point of consideration is to consolidate trainings where possible. Companies often have a “code of ethics” or “code of conduct” that provides high-level principles regarding the company’s position on such matters as privacy requirements, books and records management, cyber-security fundamentals, and beyond. Publishing such a code for public/external consumption bolsters a company’s reputation for being trustworthy and of sound integrity. Is it possible to consolidate your trainings on various governance topics into one large “code of ethics” training that can be taken in modular format? This then strengthens and unifies the company’s position on various interdependent information-management directives while streamlining the training experience for employees.

4. Gamify. In the last few years, gamification of training has helped create better-trained employees and kept employees engaged with longer-term retention of the topic. Gamification is a process where an employee is engaged at a deeper level to make the training like a game. This means launching awareness campaigns that involve features like points, levels, and awards. The goals of gamification are to create a sense of intrinsic motivation, achievement, and mastery. The more employees interact with the training material or policy in a game context, the more likely they are to understand the material and be able to act upon it. Bottom line is that it works.

5. Auditing/Monitoring. The only real way to know whether employees are doing what is required of them is by looking. In the workplace, that is typically done by watching their actions in real time (monitoring) or looking at what they have done after the fact (auditing). Auditing and monitoring programs help ensure that employees are getting it right. These programs also allow the company to help employees better perform tasks and fix training or implementation issues across the company as they become known.

In highly regulated industries, auditing and monitoring are part of the normal course of business. In fact, internal audit and quality assurance teams can be excellent partners in building an audit readiness program and in conducting the audits themselves.

6. Whack with Love or Not, but Be Consistent. When employees get something wrong, there may be a need to reprimand them. Thus, when policies provide that noncompliance may result in disciplinary action, the company must follow through. Failure to discipline may result in claims that such policy or disciplinary action is applied in a discriminatory fashion. Remind and follow up with employees to ensure they are getting it right, and when they don’t, act swiftly, fairly, and consistently to address the failure. Remember, word travels fast, and others will take note, which tends to change behavior in a positive way.

7. Repeat. Training, behavioral change, and the business transformation that follows are not one-time projects or instantaneous outcomes. Begin the process of training on key topics from the very beginning of an employee’s tenure at your company during orientation. For topics that are essential for employees to master, such as information security, training should be routinized and part of an established schedule. Not only that, policy principles and core concepts should be patiently and persistently reiterated via meetings with communities of practice, company newsletters, annual refresher trainings, and embedded within spotlights on governance initiatives when there has been a “big win.” Making employees care about managing information well means making these conversations part of your company’s culture.

Conclusion

Information has become the lifeblood of organizations. Oftentimes, it’s pumping life without rhyme, reason, control, or direction, and that has to change. Unless leadership institutionalizes the management of information, the employees will likely do as little as possible or nothing at all. With value, volume, growth in legal requirements, and consequences all intensifying around information management, however, companies must have their work forces engaged. The seven keys may not build love, but they will build a reasonable, repeatable, and defensible process “hook” for litigators to hang their hats on when failure occurs, and it always does.

2018 Report and Model Contract Clauses from the Working Group to Draft Human Rights Protections in International Supply Contracts, ABA Business Law Section*

David V. Snyder (chair) and Susan A. Maslow (vice chair)**

I. INTRODUCTION

In cooperation with other groups in the ABA Business Law Section and the wider American Bar Association, the ABA Business Law Section formed the Working Group to Draft Human Rights Protections in International Supply Contracts (“Working Group”). This is part of a larger effort to achieve widespread implementation of the ABA Model Business and Supplier Principles on Labor Trafficking and Child Labor[1] as well as other human rights protections.

We cannot stand by when children are trafficked and traded or when workers die in factory collapses and fires. The hope is that following the steps outlined in the ABA Model Principles will help eradicate labor trafficking and child labor from supply chains, making a difference to real people—their health, safety, and freedom—and, in some cases, saving lives.

In addition, companies need to comply with an increasing number of human-rights-related laws and regulations. The clauses below are designed to be compatible with a company’s policies with respect to any human-rights-related subject, including anti-trafficking, worker safety, conflict minerals, antidiscrimination, and sustainability. In this sense, the clauses are agnostic as to subject. The substance and content of those policies is beyond the scope of this Working Group; they were the subject of earlier ABA work[2] and have also been the subject of similar projects at the United Nations, the Organisation for Economic Co-operation and Development (“OECD”), and elsewhere. The foundational idea behind the present work is to move the commitments that companies require, whatever they may be, from corporate policy statements to the actual contract documents where those policies may have greater impact.

At the same time, the clauses below seek to minimize the risks inherent in the adoption of any corporate policy. Claims have been made against companies based on those companies’ undertakings as buyers in the supply chain. In other words, there is risk for such companies, often unrecognized and inadequately addressed in current supply contracts. The disclaimers included below address these issues, although no risk can be eliminated entirely.

II. PROTECTION THAT IS LEGALLY EFFECTIVE AND OPERATIONALLY LIKELY

Adoption of policies at the corporate level, while a good start, is not always enough: principles need to be put into practice. One way to do so is to integrate the policies into supply contracts, purchase orders, and similar documents that are part of the operational as well as the legal life of buyers and suppliers. The contracts and related documents are what govern, and often guide, the behavior of the parties. Enlightened contractual terms have great potential to make a difference when combined with effective remedies for their violation and a willingness to enforce them.

III. READY-MADE LANGUAGE FOR TRICKY ISSUES: CLAUSESTO MANAGE RISK AND MINIMIZE EXPOSURE FOR COMPANIES WHILE PROTECTING WORKERSAND COMPLYING WITH REGULATIONS

The mission of the Working Group is to make available well considered clauses that protect workers and that are sensitive to the legal and business risks that companies face. The drafting is challenging. Sales law and contract law are keyed to production of conforming goods, like well-stitched soccer balls. The background law does not deal easily with the problem of soccer balls that are perfectly stitched but that were sewn by child slaves. Further, companies reasonably wish to minimize the litigation risk and liability exposure while remaining compliant with generally applicable laws, particular regulations (like the Federal Acquisition Regulation), and moral imperatives. The clauses suggested below aim to address these sometimes conflicting goals, and they recognize that there are inevitably risks, which can be mitigated and perhaps minimized but not eliminated. The proposed clauses include annotations to explain the choices made and their benefits and risks. For those who want in-depth treatment, an upcom-ing symposium will be published later this year in the American University Law Review.[3]

Companies may wish to adopt these clauses for a number of reasons:

Compliance with U.S. anti-trafficking statutes;[4]

Compliance with other U.S. laws, such as regulations or prohibitions of imports made with child labor or forced labor;[5]

Compliance with U.S. state laws, like the California law on supply chain transparency;[6]

Compliance with the Federal Acquisition Regulation (“FAR”);[7]

Compliance with foreign law,[8] such as the national transpositions of the EU non-financial reporting directive;[9] and

Mitigation of potential liability under state statutory and common law theories such as undertaking liability,[10] third-party beneficiaries,[11] and deceptive advertising.[12]

Whatever moral and legal commitments companies want to require can be accommodated in what this Working Group entitles Schedule P,[13] which the model clauses incorporate, but the actual content of Schedule P is beyond the scope of this Working Group.

CLAUSES TO BE INSERTED INTO SUPPLY CONTRACTS, PURCHASE ORDERS, OR SIMILAR DOCUMENTS FOR THE SALE OF GOODS

The following clauses are designed for supply contracts. They assume that assurances with respect to compliance with certain human-rights-related policies is desired or required by the buyer and that such policies will appear in an appendix to the agreement, Schedule P, just as the buyer’s specifications for goods themselves are likely to appear in an appendix. The clauses below are intended to make those policies legally binding and to provide enforceable remedies for their violation while also managing the risk that may come with such policies.

The ABA Model Principles and Policies[14] are an example of what might appear in Schedule P; many companies may wish to adopt or adapt them. Some companies may prefer or need something broader (see infra note 18 regarding certain laws that apply to some buyers), and other companies may need something broader still (e.g., to comply with the FAR, other human rights and health and safety standards, or moral obligations). Other possibilities include the OECD Guidelines and the UN Guiding Principles (the Ruggie Principles). Many companies will already have supplier codes of conduct or similar documents that they can use as the content of Schedule P, or Schedule P may simply require obtaining and maintaining certification from a designated third party. The content of Schedule P will likely vary significantly by industry and is beyond the scope of this Working Group.

The text proposed assumes that buyers are located in the United States and that the applicable law is the Uniform Commercial Code (the “U.C.C.”) or the United Nations Convention on Contracts for the International Sale of Goods (the “CISG,” a treaty to which the United States is a party). Buyers and suppliers in other jurisdictions may also find these clauses a useful starting point.

Note on negotiation stance. The proposed text is buyer-friendly, sometimes extremely so, and it could be perceived by some suppliers as unduly aggressive. The drafters have crafted the text this way because some buyers may have the leverage to use the proposed text, and in any case, these clauses are aimed primarily at companies in the role of buyer. The text as proposed gives an indication of what a company would want as buyer, and each company can decide if particular provisions need to be adjusted or eliminated based on its negotiating position and its stance in other transactions (given that most companies are sometimes in the position of buyer and sometimes in the position of seller).

1. Representations, Warranties, and Covenants on Abusive Labor Practices. Supplier represents and warrants to Buyer, on the date of this Agreement and throughout the contractual relationship between Supplier and the Buyer, that:

1.1 Compliance. Supplier and its subcontractors and [to Supplier’s [best] knowledge][15] the [shareholders/partners, officers, directors, employees, and] agents of Supplier and all intermediaries, subcontractors, consultants and any other person providing staffing for Goods[16] or services required by this Agreement [on behalf of Supplier][17](collectively, the “Representatives”) are in compliance with Schedule P.[18] Each shipment and delivery of Goods shall constitute a representation by Supplier and Representatives of compliance with Schedule P; such shipment or delivery shall be deemed to have the same effect as an express representation. [Supplier’s delivery documents shall include Supplier’s certification of such compliance.][19]

1.2 Schedule P Compliance Through the Supply Chain. Supplier and its Representatives shall make the performance of all of its Representatives subject to the terms and conditions in Schedule P and Supplier shall ensure that Supplier, its Representatives, and all of its and their respective Representatives acting[20] in connection with this Agreement do so throughout the contractual relationship only on the basis of legally binding and enforceable written contracts that impose on and secure from the Representatives terms [in compliance with] [equivalent to those imposed by] [at least as protective as those imposed by] Schedule P. To restate for clarity, each Supplier and each Representative shall require each of its Representatives’ compliance so that such obligations are required at each step of the supply chain. Notwithstanding anything contained herein to the contrary, Supplier shall be responsible for the strict observance and performance by Supplier and its Representatives of the terms and conditions in Schedule P and shall be directly liable to Buyer for any violation by Supplier or its Representatives of Schedule P.

1.3 Supplier’s Policies. Supplier shall establish and maintain throughout the term of this Agreement its own policies and procedures to ensure compliance with Schedule P (“Supplier’s Policies”), which shall include a reporting mechanism for Representatives to report potential and actual violations of Supplier’s Policies and/or Schedule P.[21] Within ___ days of (a) Supplier having reason to believe there is any potential or actual violation of Supplier’s Policies and/or Schedule P, or (b) receipt of any oral or written notice of any potential or actual violation of Supplier’s Policies and/or Schedule P, Supplier shall provide a detailed summary of (i) the factual circumstances surrounding such violation, (ii) the specific provisions of the Supplier’s Policies and/or Schedule P that are alleged to have been violated, and (iii) the investigation and remediation that has been conducted or that is planned. [22]

1.4 Provision of Information. Upon request, Supplier shall deliver to Buyer such information and materials as Buyer reasonably requires with respect to the subject matter of Schedule P.

2. Rejection of Goods and [Cancellation] [Avoidance] of Agreement.

2.1 Strict Compliance. It is a material term of this Agreement that Supplier and Representatives shall strictly comply with Schedule P.

2.2 Rejection. Buyer shall have the right to reject any Goods produced by or associated with Supplier or Representative that Buyer has reason to believe has violated Schedule P, regardless of whether the rejected Goods were themselves produced in violation of Schedule P, and regardless of whether such Goods were produced under this or other contracts. [23]

2.3 [Cancellation.] [Avoidance.] Noncompliance with Schedule P [substantially impairs the value of the Goods and this Agreement to Buyer][24] [is a fundamental breach of the entire Agreement][25] and Buyer may immediately [cancel] [avoid] [26]this entire Agreement with immediate effect and without penalty and/or may exercise its right to indemnification and all other remedies.[27] Buyer shall have no liability to Supplier for such [cancellation] [avoidance].

2.4 Timely Notice. Notwithstanding any provision of this Agreement or applicable law (including without limitation [the Inspection Period in Section ___ of this Agreement and] [Articles 38 to 40 of the CISG] [and U.C.C. §§ 2-607 and 2-608]),[28] Buyer’s rejection of any Goods[29] as a result of noncompliance with Schedule P shall be deemed timely if Buyer gives notice to Supplier within a reasonable time after Buyer’s discovery of same.

2.5 No Right to Cure. Supplier hereby acknowledges that it shall have no right to cure by substitution and tender of Goods created and/or delivered without violation of Schedule P if Buyer elects to refuse such tender, in Buyer’s sole discretion. [30]

3.1 Notice of Buyer’s Discovery. Buyer may revoke its acceptance, in whole or in part, upon notice sent [in accordance with Section ___] to Supplier of Buyer’s discovery of Supplier’s noncompliance with Schedule P, which the parties have agreed in Section 2 above is a nonconformity that substantially impairs the value of the Goods and this Agreement to Buyer.

3.2 Same Rights and Duties as Rejection. Upon revocation of acceptance, Buyer shall have the same rights and duties as if it had rejected the Goods before acceptance.

3.3 Timeliness. Notwithstanding any provision of this Agreement or applicable law (including without limitation [the Inspection Period in Section ___ of this Agreement and (U.C.C. § 2-608)], Buyer’s revocation of acceptance of any Goods as a result of noncompliance with Schedule P shall be deemed timely if Buyer gives notice to Supplier within a reasonable time after Buyer’s discovery of same.

4. Nonvariation of Matters Related to Schedule P.

4.1 Course of Performance, Established Practices, and Customs. Course of performance and course of dealing (including, without limitation, any failure by Buyer to effectively exercise any audit rights)[32] shall not be construed as a waiver and shall not be a factor in Buyer’s right to reject Goods, [cancel] [avoid][33] this Agreement, or exercise any other remedy. Supplier acknowledges that with respect to the matters in Schedule P, any reliance by Supplier on course of performance, course of dealing, or similar conduct would be unreasonable. Supplier acknowledges the fundamental importance to Buyer of the matters in Schedule P and understands that no usage or practice established between the parties should be understood otherwise, and any apparent conduct or statement to the contrary should not be relied upon.[34] The parties agree that no usage of trade, industry custom, or similar usage shall apply to this Agreement to the extent such custom or usage would lessen the protections provided or the obligations imposed by Schedule P. No person except [Title/Officer] has authority on behalf of Buyer to vary Schedule P or any provisions relating to it, and any such variation must be in a signed writing or an authenticated electronic communication.

4.2 No Waiver of Remedy. Buyer’s acceptance of any Goods in whole or in part will not be deemed a waiver of any right or remedy[35] nor will it otherwise limit Supplier’s obligations, including, without limitation, those obligations with respect to warranty and indemnification.

5. Remedies.

5.1 Notice of Breach. If Buyer has reason to believe, at any time, that Supplier or a Representative is not in compliance with Schedule P, Buyer shall notify Supplier [in accordance with Section ____]. [Buyer’s notice requesting remediation as well as Buyer’s notices of breach or rejection [or revocation][36] may be given orally or in writing.] A notice to remediate noncompliance with Schedule P also constitutes notice of breach of this Agreement. [37]

5.2 Investigation and Suspension of Payment. Buyer has the right to suspend all payments to Supplier, whether due under this Agreement or other agreements, if Buyer deems, in its sole discretion, that investigation of possible noncompliance with Schedule P is advisable. Such suspension of payments will continue during investigation. Supplier shall fully cooperate with investigation by Buyer or Buyer’s agents. Without limitation, such cooperation shall include, at Buyer’s request, working with governmental authorities to enable Buyer or its agents to enter the country, to be issued appropriate visas, and to investigate fully.[38]

5.3 Exercise of Remedies. Remedies shall be cumulative. Remedies shall not be exclusive of, and shall be without prejudice to, any other remedies provided at law or in equity. Buyer’s exercise of remedies and the timing thereof shall not be construed in any circumstance as constituting a waiver of its rights under this Agreement. In addition to the right to [cancel] [avoid] this Agreement, in whole or in part, and any other remedies available to Buyer, in the event that Supplier or a Representative fails to comply with Schedule P, Buyer may:

deem itself insecure and demand adequate assurance from Supplier of due performance in conformance with Schedule P;

obtain an injunction with respect to Supplier’s noncompliance with Schedule P, and the parties agree that noncompliance with Schedule P causes Buyer great and irreparable harm for which Buyer has no adequate remedy at law and that the public interest would be served by injunctive and other equitable relief;

require Supplier to remove an employee or employees and/or other Representatives;

require Supplier to terminate a subcontract;

suspend payments, whether under this Agreement or other agreements, until Buyer determines, in Buyer’s sole discretion, that Supplier has taken appropriate remedial action;

decline to exercise available options under this Agreement; and

5.4 Damages. [Supplier acknowledges that it may be difficult for Buyer to fix actual damages or injury to its business, prospects and reputation with respect to Goods produced in violation of Schedule P or associated with a company that has violated Schedule P, and the parties have therefore agreed to liquidated damages in an amount calculated as follows:________________.] [In the event Supplier or Representative fails to comply with Schedule P, Buyer shall be entitled to all general and consequential damages [together with the liquidated damages set forth above],[40] including but not limited to losses arising from:

procurement of replacement Goods;

non-delivery of Goods;

diminished sales of Goods arising not only from the Goods to have been sold under this Agreement, but to include other diminished sales caused by noncompliance with Schedule P; and

5.5 Return, Destruction or Donation[43]of Goods; Nonacceptance of Goods.

Buyer may, in its sole discretion, store the rejected Goods for Supplier’s ac-count, reship them back to Supplier or, if permitted under applicable law, destroy or donate the Goods, all at Supplier’s sole cost and expense.

Buyer is under no duty to resell any Goods produced by or associated with a Supplier or Representative who Buyer has reasonable grounds to believe has not complied with Schedule P, whether or not such noncompliance was involved in the production of the Goods. In an effort to reduce its possible damages and not as a penalty, Buyer is entitled to discard, destroy or donate to a charitable entity any such Goods. Notwithstanding anything contained herein to the contrary or instructions otherwise provided by Supplier, destruction or donation of Goods rejected [or as to which acceptance was revoked],[44] and any conduct by Buyer required by law that would otherwise constitute acceptance, shall not be deemed acceptance and will not trigger a duty to pay for such Goods.[45]

5.6 Indemnification. Supplier shall indemnify, defend and hold harmless Buyer and its officers, directors, employees, agents, affiliates, successors and assigns (collectively, “Indemnified Party”) against any and all losses, damages, liabilities, deficiencies, claims, actions, judgments, settlements, interest, penalties, fines, costs or expenses of whatever kind, including, without limitation, the cost of storage, return, or destruction of Goods, the difference in cost between Buyer’s purchase of Supplier’s Goods and replacement Goods, reasonable attorneys’ fees, audit fees, and the costs of enforcing any right under this Agreement or applicable law, in each case, that arise out of the violation of Schedule P by Supplier or any of its Representatives. This Section shall apply, without limitation, regardless of whether claimants are contractual counterparties, investors, or any other person, entity, or governmental unit whatsoever.

Buyer does not assume a duty to monitor Supplier or its Representatives, including, without limitation, for compliance with laws or standards regarding working conditions, pay, hours, discrimination, forced labor, child labor, or the like;[46]

Buyer does not assume a duty to monitor or inspect the safety of any workplace of Supplier or its Representatives nor to monitor any labor practices of Supplier or its Representatives;[47]

Buyer does not have the authority and disclaims any obligation to control (i) the manner and method of work done by Supplier or its Representatives, (ii) implementation of safety measures by Supplier or its Representatives, or (iii) employment or engagement of employees and contractors or subcontractors by Supplier or its Representatives;[48]

There are no third-party beneficiaries to this Agreement; and

Buyer assumes no duty to disclose the results of any audit, questionnaire, or information gained pursuant to this Agreement other than as required by applicable law.[49]

* This report is the product of the Working Group, as explained in the text, and reflects the rough (and sometimes debated) consensus of the Working Group. While produced under the auspices of the Uniform Commercial Code Committee of the American Bar Association Business Law Section, the report has not been approved or endorsed by the Committee, the Section, or the Association as of the time of publication. Accordingly, the report should not be construed to be the action of either the American Bar Association or the Business Law Section. Nothing contained herein, including the clauses to be considered for adoption, is intended, nor should it be considered, as the rendering of legal advice for specific cases or particular situations, and readers are responsible for obtaining such advice from their own legal counsel. This report and the clauses and other materials herein are intended for edu-cational and informational purposes only. The lawyer who advises on the use of these clauses must take responsibility for the legal advice offered.

**David Snyder as chair and Susan Maslow as vice chair served as principal drafters of the report. David Snyder is Professor of Law and Director of the Business Law Program at American University Washington College of Law in Washington, D.C., and would like to acknowledge grant funding from the law school as well as travel funding from the American Bar Association. He would also like to thank Michael T. Francel, Chiara Vitiello, and Katherine Borchert for excellent research assistance. Susan Maslow is a partner at Antheil Maslow & MacMinn, LLP in Bucks County, Pennsylvania.

[1] There are both ABA Model Business and Supplier Principles on Labor Trafficking and Child Labor (“ABA Model Principles”) and ABA Model Business and Supplier Policies on Labor Trafficking and Child Labor (“Model Policies”) (emphasis added). The ABA Model Principles are the high level articulation of the detailed material in the Model Policies. The ABA Model Principles also form Part II of the Model Policies. Only the ABA Model Principles were adopted by the ABA House of Delegates, so only the ABA Model Principles represent the official position of the American Bar Association. For a detailed discussion, see E. Christopher Johnson, Jr., Business Lawyers Are in a Unique Position to Help Their Clients Identify Supply-Chain Risks Involving Labor Trafficking and Child Labor, 70 BUS. LAW. 1083 (2015). See also the Model Principles Task Force website.

[2] See supranote 1.

[3] 68 AM. U. L. REV. (forthcoming 2019).

[4] See, e.g., Trafficking Victims Protection Act of 2000, 22 U.S.C. §§ 7101–7114 (2018); see also 18 U.S.C. §§ 1589–1592 (2018) (criminal sanctions for forced labor, trafficking, and peonage); Trafficking Victims Protection Reauthorization Act of 2013 (TVPRA) (Title XII of the Violence Against Women Reauthorization Act of 2013, Pub. L. No. 113-4, 127 Stat. 54 (2013)).

[5] See, e.g., Trade Facilitation and Trade Enforcement Act of 2015 (TFTEA), Pub. L. No. 114-125, 130 Stat. 122 (2016).

[6] CAL. CIV. CODE ANN. § 1714.43 (West 2018).

[7] Federal Acquisition Regulation, 48 C.F.R. §§ 52.222–50 to 52.223-7 (2018).

[8] See, e.g., UK Modern Slavery Act 2015, c. 30 (Eng.); France’s Corporate Duty of Vigilance Law, Loi no 2017-399 du 27 mars 2017 relative au devoir de vigilance des sociétés mères et des entreprises donneuses d’ordre, Journal officiel de la République française.

[9] See Directive 2014/95/EU, of the European Parliament and of the Council of 22 October 2014 Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Groups, 2014 O.J. (L 330) 1.

[10] See Rahaman v. J.C. Penney Corp., No. N15C-07-174MMJ, 2016 WL 2616375, at *9 (Del. Super. Ct. May 4, 2016).

[11] See Doe I v. Wal-Mart Stores, 572 F.3d 677, 681–82 (9th Cir. 2009).

[12] See, e.g., Nat’l Consumers League v. Wal-Mart, Inc., No. 2016 CA 007731 B, 2016 WL 4080541, at *7 (D.C. Super. Ct. July 22, 2016) (order denying defendant’s motion to dismiss); the chocolate cases, such as Hodsdon v. Mars, Inc., 162 F. Supp. 3d 1016 (N.D. Cal. 2016), aff’d, 891 F.3d 857 (9th Cir. 2018); McCoy v. Nestle USA, Inc., 173 F. Supp. 3d 954 (N.D. Cal. 2016), aff’d, No. 16-15794, 2018 WL 3358227 (9th Cir. July 10, 2018); Dana v. Hershey Co., 180 F. Supp. 3d 652 (N.D. Cal. 2016), aff’d, No. 16-15789, 2018 WL 3358223 (9th Cir. July 10, 2018) and the fishermen cases, such as Sud v. Costco Wholesale Corp., No. 15-cv-03783-JSW, 2016 WL 192569, at *1 (N.D. Cal. Jan. 15, 2016). Other cases are pending and some have recently been filed. For more comprehensive consideration of recent and pending litigation in this area, see generally Ramona L. Lampley, Mitigating Risk, Eradicating Slavery: The Business Case for Eradicating Slave Labor in the Supply Chain to Reduce Domestic Liability, 68 AM. U. L. REV. (forthcoming 2019).

[13] The letter “P” was chosen to designate the schedule because it stands for “Principles” or “Policies” such as the ABA Model Principles and Policies.

[14] See supranote 1.

[15] An unqualified representation supports Buyer’s goals to allocate the risk of undiscovered issues to Supplier and contractually encourage Supplier to gather accurate information about its subcontractors. The parties may negotiate the knowledge qualifier and the degree of knowledge required as it relates to additional levels of subcontractors and any other third party and whether “best” knowledge should be defined to include the imposition of certain periodic inquiry obligations on Supplier. It can also reinforce the Buyer’s right to revoke acceptance under U.C.C. section 2-608.

[16] “Goods” is assumed to be defined earlier in the Agreement (and not defined in Schedule P). See also infra note 29 (on the definition of “Nonconforming Goods”).

[17] Supplier may attempt to negotiate the use of the phrase “on behalf of Supplier” here, but such a phrase might allow Supplier to argue that the breaching Representative did so without Supplier’s knowledge or authority, which defeats the purpose of a strict representation and covenant.

[18] The content of Schedule P is beyond the scope of this document, but note that some suggest the best practice is to avoid reference to specific laws in favor of a general reference because legislative initiatives in some countries are broader than in others. In the event that the drafter nevertheless wishes to require that Supplier specifically represent compliance with anti-trafficking and similar legislation, consider avoiding the term “applicable,” which will limit required adherence by companies that do not meet the size or revenue requirements of certain legislation. Prominent guidance can be found, for example, in the sources listed at supra note 4, as well as the U.N. Guiding Principles on Business and Human Rights (often called the Ruggie Principles); see John Ruggie (Special Representative of the Secretary-General), Guiding Principles on Business and Human Rights: Implementing the United Nations “Protect, Respect and Remedy” Framework, U.N. Doc. A/HRC/17/31, annex (Mar. 21, 2011), https://www.ohchr.org/Documents/Issues/Business/A-HRC-17-31_AEV.pdf. Note again however, that specific guidance with respect to law that might be desired by Buyer or Supplier to be included in Schedule P is beyond the scope of this document, and this note does not attempt to be exhaustive (omitting, for example, certain anti-trafficking legislation as well as conflict mineral issues and the EU rules on non-financial and diversity information).

[19] The bracketed sentence may support Buyer’s continuing reliance upon Supplier’s monitoring and compliance. The actual express representation would arguably make reliance more reasonable, and such reliance may delay Buyer’s discovery and could help explain periodic rather than constant or continual audits by Buyer. See also infra section 2.4. Delivery documents could include commercial invoices, packing lists, beneficiary’s certificates, or an additional document delivered with the goods or tendered through banking channels to obtain payment for the goods. See infra note 38. If the bracketed language is included, the second clause of the preceding sentence should be deleted.

[20] Supplier may again attempt to negotiate the use of the phrase “acting on the behalf of Supplier” here. Buyer, if possible, will want to avoid such language. See supra note 17.

[21] As part of Buyer’s due diligence in choosing its Supplier, it should request copies of all anti-trafficking policies, as well as similar policies, and should determine, for example, how and when training is conducted and to whom it is given, how Supplier’s policies are monitored, and how compliance is checked and certified. If Supplier does not have its own policies against forced and child labor, including worker health and safety, for example, or if Buyer prefers, Supplier can be required to adopt Buyer’s policies.

[22] All of the covenants set forth above are prospective. Counsel to Buyer may consider requiring Supplier to state that it has no history of using forced labor or underage workers, subjecting workers to hazardous conditions or other similar conduct, and has never been the subject of investigations or proceedings relating to such conduct. In some industries and for some companies, such historical assurances cannot be made or expected, even though the companies are currently compliant and may have been compliant for a number of years.

[23] See U.C.C. §§ 2-601, 2-602 (2011).

[24] Because installment contracts under Article 2 of the U.C.C. do not enjoy the “perfect tender” rule applicable to a single-delivery contract, such installment contracts should include the phrase within the first bracket. The additional phrase within the first bracket “and this Agreement” should be included if Buyer wishes not only to reject goods based on noncompliance with Schedule P but also wishes to terminate the installment contract in its entirety in light of, for example, Buyer’s internal policy, the possible damage to Buyer’s reputation, or justifiable fear of a repeated breach by Supplier.

[25] The phrase within the second bracket is applicable for agreements to which the CISG applies, whether for a single delivery or an installment contract, under article 49.

[26] “Cancellation” occurs when a “party puts an end to the contract for breach by the other” under U.C.C. section 2-106(4). “Avoidance” is the appropriate term under CISG article 49.

[27] This section expressly provides for cancellation as a remedy in the event of Supplier’s failure to comply with a human rights policy adopted as part of a supply contract. Ultimately, without a contract clause expressly permitting cancellation for human rights policy breaches, Buyer may have a difficult time assembling compelling evidence that the value of the goods was fatally and “substantially impaired” due to the violation of the policy. The value of a particular good supplied in violation of a human rights policy might not necessarily change in the marketplace due to the troubled and tainted background of manufacture.

[28] Articles 38 to 40 of the CISG require that Buyer examine the goods or cause them to be examined within as short a period as is practicable. Buyer loses the right to rely on a lack of conformity of the goods if it does not give Supplier notice within a reasonable time after Buyer discovers or ought to have discovered a defect and, at the latest, within two years of the date of delivery (or other contractual period) unless Supplier knew or could not have been unaware of the defect. Because U.C.C. section 2-607(3)(a) provides a similar argument that Buyer’s failure to notify Supplier of a breach within a reasonable time bars any remedy, it is suggested that the contractual text be included to limit disputes about what constitutes a reasonable time. If the U.C.C. is referenced in the text, the applicable state version should be cited.

[29] “Nonconforming Goods” and “Inspection Period” are assumed to be defined earlier in the Agreement (and not defined in Schedule P). The definitional portion of the Agreement must include as “Nonconforming Goods” any goods received by Buyer that Buyer has reasonable grounds to believe (i) include any materials in fabrication, assembly, packaging, or shipment, directly or indirectly, that do not comply with Schedule P; or (ii) originate from or are associated with a Supplier or Representative that [may have] [is reputed to have] [has] violated human rights protections similar to Schedule P.

[30] This clause negates Supplier’s right to cure under U.C.C. section 2-508 and CISG articles 37 and 48. In cases of mere technical or recordkeeping violations, Buyer may elect to accept the tender of a cure. In other cases, Buyer may not want to do business with a Supplier that violates Schedule P. Under the provision as drafted, Buyer retains discretion here. Many parties, however, may prefer to provide a right to cure; experience suggests that many violations may consist of recordkeeping problems or other clerical shortcomings. Even in cases of substantive violations of health and safety standards, for example, the parties may prefer to institute a program to alleviate the problems (e.g., by providing for appropriate working conditions) rather than to end the Agreement and throw the employees out of work. For these reasons, a “notice and cure” clause may be preferable to the elimination of any cure right for Supplier. In such a situation, this section should add, “Except as provided in Section ___,” at the beginning. Another section can then provide for Buyer to give notice of default to Supplier. That default notice would trigger a cure period, either set by this Agreement or by the notice (as the parties prefer), and if cure is not effected within that period, then Supplier would be in breach, which would then trigger the remedies provided in the Agreement. In this way, a Supplier who does not comply with Schedule P is in default but is given a chance to fix the problem. A Supplier who implements a successful fix thus avoids breach, and Buyer will have no right to a remedy (but perhaps no need for one either). A notice-and-cure mechanism may make the Agreement more palatable to Supplier, although Buyer may prefer the stronger rights provided in the text as drafted, or Buyer may need them under the FAR. See 48 C.F.R. § 22.1703(c) (2018) (requiring contractor certification (within threshold limits) that it will “monitor, detect, and terminate the contract with a subcontractor or agent engaging in prohibited activities” (emphasis added)). The text as drafted avoids the problem of disputes about whether a cure is successful. Further, nothing in the text as drafted prevents Buyer from forbearing to exercise its remedies and giving Supplier a period to cure if Buyer thinks a cure would be appropriate. The provision on Notice of Breach appears in section 5.1. Any forbearance should include an appropriate notice of reservation of rights.

[31] The clauses on revocation of acceptance are designed primarily for use in contracts governed by the U.C.C. and are drafted with U.C.C. section 2-608 in mind. They should be omitted in contracts governed by the CISG. For this reason, section 3 is bracketed.

[32] What audit rights Buyer has, if any, are beyond the scope of this document and should be set forth in Schedule P.

[33] “Cancel” for agreements under the U.C.C., “avoid” for the CISG. See supra note 26.

[34] The first phrase uses the terminology of U.C.C. section 1-303 and the second phrase uses the terminology of CISG article 9(1).

[35] U.C.C. § 2-601 (2011).

[36] Again, revocation language should be used in U.C.C. but not CISG contracts.

[37] This section addresses notice requirements under Article 2 of the U.C.C. For instance, section 2-607(3)(a) requires notice of a breach within a reasonable time after constructive discovery of the breach. A buyer who fails to give such notice will find its claims barred, with many courts holding that pre-suit notice is required.

[38] Some supply contracts will call for payment by letter of credit, which will complicate the right to suspend payment. When a documentary credit is involved, the supply contract and letter of credit should require presentation of a certificate of compliance with Schedule P. Ideally the certificate would be issued by a third party that has audited the Supplier or Representatives, but a beneficiary’s certificate may also be helpful if a third-party certificate is impractical. Under U.S. law, a false beneficiary’s certificate could allow an injunction against payment on grounds of “material fraud by the beneficiary on the issuer or applicant.” See U.C.C. § 5-109(b) (2011). Purposeful falsity of the certificate might perhaps be helpful even if suit must be in London or in a jurisdiction following English law, which requires fraud on the documents. The leading case from the House of Lords is United City Merchants (Invs.) Ltd. v. Royal Bank of Canada, [1983] A.C. 168, 183 (referring to “documents that contain, expressly or by implication, material representations of fact that to his knowledge are untrue”); see also Inflatable Toy Co. Pty Ltd v. State Bank of New South Wales Ltd, [1994] 34 NSWLR 243 (applying Australian law). If the violation of Schedule P constitutes an illegal act, the illegality theory may also be useful in a suit governed by English law. In any case, the certificate should be required to be dated within a reasonably short time of the draw. Many banks probably will not object to the requirement of an additional certificate as certificates (e.g., by SGS) are commonplace in such transactions, and environmental certificates are similar to (and in some cases may be the same as) a certificate of compliance with Schedule P. While some banks may resist the requirement of such a certificate because of fear of injunction actions and the concomitant extension of the credit risk if the injunction is ultimately denied, most banks seem unlikely to be concerned by the requirement of one more certificate, and any additional credit risk from an injunction may be mitigated by a bond or other credit support as contemplated by U.C.C. section 5-109(b)(2) and comment 7, or by the civil procedure laws or rules of certain jurisdictions or by collateralization or bonding provisions in the reimbursement agreement. Still, despite all of these efforts, suspension of payment may be impossible in cross-border documentary credit transactions because frequently a foreign bank will have honored before the injunction can issue. Once one bank honors in good faith, the commitments along the chain all become firm and cannot be enjoined. See U.C.C. § 5-109 (2011).

[39] This section reflects the remedies provided in the FAR § 52.222.50 relative to combating trafficking in persons. Additionally, the clause adds an insecurity provision under U.C.C. section 2-609. The clause also clarifies that injunctive relief may be necessary. In addition, while Buyer may want to work with a Supplier toward full compliance, Buyer should be prepared to face waiver arguments. The timing of the exercise of remedies is sensitive and the exercise of remedies and any requests for damages may themselves have impacts on human rights. Therefore, this provision expressly recognizes that such careful consideration of the exercise of remedies by Buyer does not constitute a waiver of any rights. Further, with respect to removal of employees (section 5.3.c.), see infra note 48. Note also that the remedies provisions here (including sections 5.2 and 5.3.e. on suspension of payments) do not mention setoff, see 11 U.S.C. §§ 506(a)(1), 553 (2018) (setoff is a secured claim in bankruptcy), recoupment, clawback, or similar remedies; if those remedies are not already provided in the main agreement, counsel may wish to consider making such rights explicit in this clause.

[40] While Buyer in some industries may prefer to adopt a liquidated damages clause, U.C.C. section 2-718 generally prohibits penalties, including providing that “unreasonably large liquidated damages [are] void as a penalty.” The ultimate enforceability of these provisions will turn on whether the exercise of the remedy in the contractual clause was reasonable. Particular care should be exercised if Buyer includes the bracketed language that allows liquidated damages in addition to other damages.

[41] If no liquidated damages are included above for harm to reputation.

[42] Section 5.4 addresses monetary remedies, including consequential and special damages, recoverable in the event of a breach by Supplier. While measures such as diminished sales and harm to reputation are specifically included, Buyer may face challenges with respect to proving damages. This is common in claims for breach of contract, but Buyer may have special challenges with respect to the impact on its brand that results from violations of human rights policies. It is not clear that suppliers will agree to the inclusion of Buyer’s lost profits, real or imagined, as damages. Nor is it clear, however, that Supplier will have strong views on damages; Supplier may be judgment proof—for lack of assets or for procedural reasons—and damages may not be a realistic remedy in any case. The suggested text is presented as a starting place for discussions with respect to damages. An agreed liquidation amount may be an acceptable compromise.

[43] Donation of goods manufactured or otherwise delivered with the use of forced labor may not be permitted by the U.S. Customs and Border Protection, Cargo Security, Carriers and Restricted Merchandise Branch, Office of Trade. Buyer’s only option as an importer may be to return or export the goods. Other countries may have similar restrictions on the possession and ownership of merchandise mined, produced, or manufactured in any part with the use of a prohibited class of labor and such laws, which are beyond the scope of this document, must be examined before donations are made.

[44] See supra note 31.

[45] This section is drafted to address concerns that might be raised with respect to the U.C.C. section 1-305 mandate to place the aggrieved party in the position of its expectation, without award of consequential or penal damages unless specifically allowed, particularly with respect to minimizing damages. See also U.C.C. § 2-715 (2011) (consequential damages cannot be recovered if they could have been prevented). With an understanding that mitigation applies and may be non-waivable, particularly with respect to claims of consequential damages, an attempt by Buyer to avoid mitigation might be seen as a lack of good faith. Nevertheless, reselling the goods that are produced in violation of a human rights policy may be understood as increasing Buyer’s damages, rather than reducing them. Accordingly, Buyer should be entitled to discard, destroy, or donate to a charity any goods produced in violation of a human rights policy as an attempt toward mitigation, rather than against it.

[46] This disclaimer conflicts with the requirements of the FAR, 48 C.F.R. §§ 52.222–56, 22.1703(c) (2018) (requiring contractor certification (within threshold limits) that it will “monitor, detect, and terminate the contract with a subcontractor or agent engaging in prohibited activities”).

[47] Again, note the conflict with the FAR. See 48 C.F.R. §§ 52.222–56, 22.1703(c) (2018).

[48] Note supra section 5.3.c. This disclaimer is included to help negate claims of undertaking liability or liability under the peculiar risk doctrine. See Rahaman v. J.C. Penney Corp., No. N15C-07-174MMJ, 2016 WL 2616375, at *9 (Del. Super. Ct. May 4, 2016). This disclaimer could conflict with the section noted above, however, and counsel should consider whether it is better to have the power to require that its suppliers fire employees or other representatives or whether the disclaimer as to this factor (which relates to whether a supplier is an independent contractor) is more important. See also supra section 5.3.b.

[49] This provision emphasizes that Buyer is assuming no contractual duties to disclose although Buyer may have duties to disclose under other standards (legal or non-legal). For example, Buyer must determine if it provided false or misleading information to Customs and Border Protection and other officials in the event that goods are initially accepted and removed from the dock but are later determined to be tainted by forced labor. If the original information is false, a duty to amend may arise. See, e.g., 18 U.S.C. § 541 (2018); 19 C.F.R. § 12.42(b) (2018). As another example, under the FAR, contractors and subcontractors must disclose to the government contracting officer and agency inspector general “information sufficient to identify the nature and extent of an offense and the individuals responsible for the conduct.” 48 C.F.R. § 22.1703(d).

On September 28, 2018, California became the first US state to specifically regulate the security of connected devices (otherwise known as ”Internet of Things” or “IoT devices”).

The new laws aim at increasing the security of IoT devices, whose global use is growing rapidly. Statista has estimated that in 2018 there are over 23 billion IoT devices currently in use, and this number is expected to grow to over 26 billion in 2019 (Gartner has estimated 20 billion such devices will be online by 2020). Unfortunately many IoT devices remain dangerously unprotected from cybercriminals and vulnerable to malware as they enter the market with no passwords, default passwords (think ”123”, ”admin” or even worse, ”password”) or otherwise hard-coded passwords that cannot be modified or updated.

These concerns are not merely speculative. By way of ‘real life’ example, beginning September 2016, massive distributed denial of service (DDoS) attacks took down various US Internet infrastructure companies/DNS providers, leaving much of the Internet inaccessible on the east coast of the United States and incapacitating popular websites (including AirBnB, Amazon, Github, HBO, Netflix, Paypal, Reddit, the New York Times and Twitter, just to name a few). Originally created by three teenaged hackers, the Mirai malware responsible for the attack was specifically designed to target and infect susceptible IoT devices such as security cameras, home routers, air-quality monitors, digital video recorders and routers using a table of more than 60 common factory default usernames and passwords. These devices were turned into a network of remotely controlled bots that were used to launch the DDoS attacks which later spread globally, impacting such diverse organizations as OVH (a large European provider), Lonestar Cell (a Liberian Telecom Operator) and Deutsche Telekom. At its peak, Mirai infected over 600,000 vulnerable IoT devices.

These two new substantially similar IoT laws (California Senate Bill 327, chapter 886 and Assembly Bill No. 1906, “Security of Connected Devices” (2018 Cal. Legis. Serv. Ch. (S.B. 327)(to be codified at Cal. Civ. Code § 1798.91.04(a)) (collectively, the “IoT Laws”) require manufacturers of connected devices to equip the device with a ”reasonable” security feature or features that meet all of the following criteria: (i) appropriate to the nature of the device; (ii) appropriate to the information it may collect, contain, or transmit; and (iii) designed to protect the device and any information contained therein from unauthorized access, destruction, use, modification or disclosure. The IoT Laws broadly define a ‘connected device’ to mean any devices or other physical object that is capable of connecting to the Internet (directly or indirectly), and that is assigned an Internet Protocol address or Bluetooth address, meaning that consumer, industrial, and other IoT devices are covered.

Additionally, if the connected device is equipped with a means for authentication outside of a local area network, either of the following requirements must be met before it shall be deemed to possess a “reasonable security feature”: (i) it must have a preprogrammed password unique to each device manufactured; or (ii) the device must contain a security feature that requires a user to generate a new means of authentication before access is granted for the first time.

The IoT Laws broadly capture “manufacturers” to include the producers of the devices themselves and those who manufacture on behalf of such organizations, connected devices that are sold or offered for sale in California. However, manufacturers are not responsible for any unaffiliated third-party software or applications that a user chooses to add to the device. Contracts with organizations or persons involving the mere purchase of connected devices or purchasing and branding a connected device are excluded.

Manufacturers are obliged to allow users to have full control and/or access over connected devices, including the ability to modify the software or firmware running on the device at the user’s discretion. Additionally, no obligations or duties are imposed upon electronic stores, gateways, marketplaces or other means of purchasing software or applications to review or enforce compliance with these statutes.

The IoT Laws contain various exclusions and limitations. For example, they do not apply to manufacturers of connected devices that are already subject to security requirements under US federal law, regulations or the guidance of federal agencies (presumably FDA-regulated medical devices, for example). They do not prevent law enforcement agencies from continuing to obtain connected device information from a manufacturer as authorized by law or pursuant to a court of competent jurisdiction. They also do not apply to the activities of covered entities, providers of health care, business associates, health care service plans, contractors, employers, or other persons subject to the U.S. federal Health Insurance Portability and Accountability Act of 1996 (better known as HIPAA) or California’s Confidentiality of Medical Information Act.

Significantly, the IoT Laws do not provide individuals with a private right of action against non-compliant manufacturers. Only the Attorney General, a city attorney, a county counsel, or a district attorney has the authority to enforce these requirements.

The IoT Laws are scheduled to come into force on January 1, 2020.

The enactment of the IoT Laws was clearly motivated by the desire to improve the security of smart devices and mitigate security vulnerabilities that leave such devices open to cyber-attacks such as Mirai malware. By not mandating what security features are ”reasonable,” the legislation is effectively leaving it up to the manufacturer to determine whether its security features meet the three-prong test described above. Guidance from agencies such as the National Institutes for Standards and Technology (NIST) and other industry self-regulatory guidelines can help determine what will be reasonable under the circumstances (in fact NIST is currently seeking comments on its draft guidance document which includes recommendations for addressing security and privacy risks associated with IoT devices—see Draft NISTIR 8228, “Considerations for Managing Internet of Things (IoT) Cybersecurity and Privacy Risks”.)(“NIST Guidance”).