As chair of the ABA’s Private Target Mergers & Acquisitions Deal Points Study (the Private Target Deal Points Study), I am pleased to announce that we published the latest iteration of the study to the ABA’s website in December 2017.

Congratulations! But Wait. What Exactly Is This Private Target Deal Points Study, Anyway?

The Private Target Deal Points Study is a publication of the Market Trends Subcommittee of the Business Law Section’s M&A Committee. It examines the prevalence of certain provisions in publicly available private target mergers and acquisitions transactions during a specified time period. The Private Target Deal Points Study is the preeminent study of M&A transactions, widely utilized by practitioners, investment bankers, corporate development teams, and other advisors.

The 2017 iteration of the Private Target Deal Points Study analyzes publicly available definitive acquisition agreements for transactions executed and/or completed either during calendar year 2016 or during the first half of calendar year 2017. In each case, the transaction involved a private target acquired by a public buyer, with the acquisition material enough to that public buyer for the Securities and Exchange Commission to require public disclosure of the applicable definitive acquisition agreement.

The final sample examined by the 2017 Private Target Deal Points Study is made up of 139 definitive acquisition agreements and excludes agreements for transactions in which the target was in bankruptcy, reverse mergers, divisional sales (for divisional sales, see the Carveout Study also published by the Market Trends Subcommittee in December 2017), and transactions otherwise deemed inappropriate for inclusion.

Although the deals in the 2017 Private Target Deal Points Study reflect a broad swath of industries, the technology and health-care sectors together made up nearly half of the deals. Asset deals comprised 13.7 percent of the sample, with the remainder either equity purchases or mergers.

Of the 2017 Private Target Deal Points Study sample, 21 deals signed and closed simultaneously, whereas the remaining 118 deals had a deferred closing some time after execution of the definitive purchase agreement.

The transactions analyzed in the 2017 Private Target Deal Points Study were in the “middle market,” with purchase prices ranging between $30 million and $500 million; purchase prices for most deals in the data pool were below $300 million.

The Private Target Deal Points Study Sounds Great! How Can I Get a Copy?

All members of the M&A Committee of the Business Law Section received an e-mail alert from me with a link when the study was published. If you are not currently a member of the M&A Committee but don’t want to miss future e-mail alerts, committee membership is free to Business Law Section members, and you can sign up on the M&A Committee’s homepage.

The published 2017 Private Target Deal Points Study is available for download by M&A Committee members from the Market Trends Subcommittee’s page on the ABA’s website. Also available at that link are the other studies published by the Market Trends Subcommittee, including the recently released Canadian Public Target M&A Deal Points Study (chaired by Cameron Rusaw), Carveout Transactions M&A Deal Points Study (chaired by Rita-Anne O’Neill), and Strategic Buyer/Public Target M&A Deal Points Study (chaired by Claudia Simon).

How Does the 2017 Private Target Deal Points Study Differ from the Prior Version?

The 2017 version of the Private Target Deal Points Study has a number of features that differentiate it from prior iterations.

Data in the 2017 version of the Private Target Deal Points Study is more current:

The 2017 version of the Private Target Deal Points Study includes not only 2016 transactions, but also transactions from the first half of 2017.

The 2017 version of the Private Target Deal Points Study includes deals signed during those periods, not just deals that closed during those periods.

The 2017 version of the Private Target Deal Points Study excludes divisional sales:

The Market Trends Subcommittee of the M&A Committee has also published a special study of carveout sales; thus, by excluding them from the 2017 version of the Private Target Deal Points Study, we can better compare results for given data points between the two studies.

The 2017 version of the Private Target Deal Points Study contains new data points:

There is an entire new section in the 2017 version of the Private Target Deal Points Study regarding representations and warranties insurance, along with correlations to certain data points relating to indemnification.

There are other new data points scattered throughout the 2017 Private Target Deal Points Study with “new data” flags (like the sample shown below) to make them easy to spot:

The 2017 version of the Private Target Deal Points Study provides multiyear comparisons:

We have been collecting many of the data points for over a decade now, allowing us to display data—and trend lines—over a number of years in the 2017 version of the Private Target Deal Points Study.

Please join me in extending a hearty thank you to everyone who worked so hard on this study, from leadership to advisors to issue group leaders to the working groups, all of whom are listed in the credits pages.

For more information, there will be an In the Know webinar covering the Private Target M&A Deal Points Study on March 8, 2018, from 1:00 p.m. to 2:30 p.m. (ET).

The Tax Cuts and Jobs Act (the Act) provides seven tax brackets (10 percent, 12 percent, 22 percent, 24 percent, 32 percent, 35 percent, and 37 percent) for individuals paying taxes on their ordinary income, such as wages. The Act repeals the Affordable Care Act’s individual mandate penalty. The Act did not repeal, however, the 3.8 percent net investment income tax, nor did it remove the additional payroll and Medicare taxes, resulting in a possible top marginal rate of 40.8 percent for individuals. These new individual tax rates will sunset on December 31, 2025.

Generally, fewer individuals will itemize their deductions for tax year 2018 because although the Act eliminated personal exemptions, it doubled the current standard deduction. In addition, although charitable deductions were left untouched, the mortgage interest deduction will be based on a new $750,000 limit instead of the prior $1,000,000 limit for home acquisition debt. State and local taxes for individuals can also still be itemized and deducted, but only up to $10,000. There was previously no limit on the amount of state and local taxes that could be deducted on personal income tax returns.

Taxation of Pass-through Income

The Act provides a 20-percent deduction for pass-through entities, such as partnerships, S corporations, and sole proprietorships. Business income from specified services (including health, law, accounting, consulting, athletics, financial services, brokerage services, and certain other services) is ineligible for the deduction, except for taxpayers with income below certain thresholds. Taxpayers with taxable income not exceeding $157,500 (or $315,000 in the case of a joint return) are exempt from the prohibition on specified services. As with other individual income tax provisions in the Act, the 20-percent deduction for pass-through entities will sunset on December 31, 2025.

Corporate Taxation

Corporate tax rates are reduced from a maximum rate of 35 percent to a flat rate of 21 percent under the Act. The corporate alternative minimum tax is also eliminated, unlike the individual alternative minimum tax which was retained. Although the Act has eliminated most corporate deductions and credits, it provides for the immediate write-off of the cost of business investments under bonus depreciation.

Estate and Gift Taxes

The Act increases the federal estate and gift tax unified credit basic exclusion amount to $10 million (adjusted for inflation from the same 2010 base year), effective for decedents dying and gifts made after 2017 and before 2026. The Act increases the federal GST exemption amount to $10 million (adjusted for inflation from the same 2010 base year), effective for generation-skipping transfers made after 2017 and before 2026.

Employee Tax Benefits

Generally, a deduction for compensation paid or accrued with respect to a “covered employee” of a publicly traded corporation is capped at $1 million per year. Covered employees include the CEO, CFO, and the three highest-paid employees. Pre-reform, the deduction limitation did not apply to commissions or performance-based remuneration (including stock options). The Act repeals the commission and performance-based compensation exceptions.

Section 83(i) of the Internal Revenue Code will provide new tax benefits to employees of certain startup companies. Here, a qualified employee may make an election to defer income with respect to qualified stock so that no amount is included in income for up to five years or until a specified event occurs, such as the company going public. The company must have a written plan that provides RSUs or stock options to at least 80 percent of the employees of the company. Employers must provide notice that the employee may be eligible to elect to defer income. Certain highly compensated employees are explicitly excluded.

International Taxation

Subtitle D of the Act contains the international tax provisions. Here, the Act creates a new territorial system of taxation by exempting certain foreign income of U.S. corporations from U.S. taxation.

Conclusion

Although President Trump signed the Act into law, Americans can expect further legislation to clarify and modify the new rules. Outside of budget reconciliation, any subsequent bills are going to require 60 votes to pass in the Senate, which means some Democrats will also have to be on board. In the interim, we will have to rely on further IRS guidance to fill in the gaps of this tax reform legislation.

Analysis of trends in U.S. capital markets reveals “an undeniable fact that the number of U.S. public companies has declined considerably from the peak of 20 years ago.” Ernst & Young LLP, Foreword, Looking Behind the Declining Number of Public Companies, an Analysis of Trends in US Capital Markets, May 2017 (E&Y Analysis). Listings of public companies in the United States “fell by roughly 50 percent . . . from 1996 through 2016.” Credit Suisse, The Incredible Shrinking Universe of Stocks, the Causes and Consequences of Fewer U.S. Equities, Mar. 22, 2017, at 1 (Credit Suisse Report). The reality is that more companies are choosing to stay private longer, and some public companies voluntarily “go dark” (i.e., deregister their stock from the Securities and Exchange Commission) or are acquired.

In his July 12, 2017 remarks at the Economic Club of New York, SEC Chairman Jay Clayton unequivocally stated that “the reduction in the number of U.S.-listed public companies is a serious issue for our markets and the country more generally,” and that “we need to increase the attractiveness of our public capital markets without adversely affecting the availability of capital from our private markets.”

In August 2017, the Council of Institutional Investors (CII) and the U.S. Chamber of Commerce, along with representatives of different segments of the U.S. economy, wrote letters to the Department of Treasury in connection with its upcoming report on regulations impacting the capital markets. See Council of Institutional Investors, Letter to the U.S. Department of Treasury on Capital Markets Report, (Aug. 23, 2017) (CII Letter); Joint Letter to Treasury Regarding the Decline in Public Companies (Aug. 22, 2017) (Joint Letter). (The Joint Letter was submitted by the U.S. Chamber of Commerce, as well as the Intercontinental Exchange; Nasdaq; Biotechnology Innovation Organization; Equity Dealers of America; Steven Bochner, Partner, Wilson Sonsini Goodrich & Rosati; Joseph D. Culley, Jr., Janney Montgomery Scott LLC; Kate Mitchell, Co-Founder and Partner, Scale Venture Partners; Jeffrey M. Solomon, President, Cowen Inc.; and Joel H. Trotter, Partner, Latham & Watkins.) Both the CII Letter and the Joint Letter identify the problem of shrinking public company markets but approach it differently.

CII, as the voice of institutional shareholders, including employee benefit plans, foundations, and endowments, believes that the SEC must “improve the delivery and access of the information required to be provided to investors,” but should not significantly alter “the total mix of information provided to investors.” The Joint Letter, representing views of businesses, expresses concern that “the decline in U.S. public companies inhibits economic growth, job creation, and the ability of households to create sustainable wealth” and suggests the following reforms to help reinvigorate the U.S. IPO market:

extend the “on-ramp” accommodations of the JOBS Act from five years to ten years for all emerging growth companies (EGCs), and revise the EGC definition to eliminate the premature phase-out of those accommodations;

make the JOBS Act on-ramp available for all companies seeking an IPO for five years, regardless of whether they meet the definition of an EGC;

modernize the regulatory regime for internal control reporting requirements under the Sarbanes-Oxley Act;

modernize the disclosure regime administered by the SEC, including elimination of outdated or duplicative disclosures, repeal of immaterial social and politically motivated disclosure mandates, as well as further scaled disclosure requirements for EGCs;

reform the outdated rules governing shareholder proposals under Rule 14a-8, including modernizing the thresholds for shareholder proposal resubmissions by increasing the shareholder support thresholds;

enhance regulatory oversight of the proxy advisory firm industry;

promote an equity market structure that enhances liquidity for EGCs and other small capitalization companies; and

incentivize both pre-IPO and post-IPO research of companies.

In his speech, Chairman Clayton praised the U.S. public company disclosure and trading system as “an incredibly powerful, efficient, and reliable means of making investment opportunities available to the general public,” but he also acknowledged that the SEC, lawmakers, and other regulators “have slowly but significantly expanded the scope of required disclosures beyond the core concept of materiality.”

The SEC’s Regulatory Flexibility Agenda (see 82 Fed. Reg. 163 (Aug. 24, 2017)) published for public comment, delays (arguably indefinitely) the adoption of rules that many companies view as burdensome and pushes forward rules that are designed to lead to a more balanced disclosure regime. For example, the proposed agenda places the adoption of final rules implementing the following Dodd-Frank mandates on hold, with the timetable for the SEC action identified as “to be determined”:

disclosure of hedging by employees, officers, and directors;

clawback of erroneously awarded compensation; and

pay-versus-performance disclosure.

The adoption of the following final rules, among certain other actions, is targeted for April 2018:

amendments to the definition of a “smaller reporting company” to expand the number of registrants that qualify as smaller reporting companies in order to promote capital formation and reduce compliance costs for smaller registrants; and

updates to certain disclosure requirements in Regulations S–X and S–K that may have become redundant, duplicative, overlapping, outdated, or superseded.

The adoption of these rules, albeit important, is unlikely to be a game-changer in a company’s decision whether to go public. The implementation of significant reforms that will spur public company activity may involve a lengthy SEC rulemaking process and will not happen overnight; however, it is important that the issue of declining interest in becoming a U.S. public company is recognized, discussed, and put at the forefront of the SEC agenda.

Sometimes, uncontrollable financial circumstances precipitate a company’s decision to seek the protection of the Bankruptcy Code. Other times, a bankruptcy filing results, at least in part, from poor decisions made by the company’s management. A bankruptcy trustee is duty-bound to scrutinize the decisions of management and determine whether certain errors were made that caused harm to the debtor or its creditors and, if appropriate, commence litigation against the relevant decision makers for the benefit of the bankruptcy estate and its creditors. These suits often involve allegations that directors and officers have breached their fiduciary duties.

This type of litigation is all the more likely in cases where the debtor has or had a director and officer liability policy (D&O policy) in place to cover such claims, but most D&O policies contain an “insured vs. insured” exclusion, which excludes claims made by an insured against another insured under the policy.

Although not all courts have agreed, in a majority of jurisdictions, court-appointed trustees (Chapter 7 and Chapter 11) have circumvented insured vs. insured exclusions by arguing that there is no risk of collusion when the suit is brought by an independent, court-appointed fiduciary, and that the debtor company and the debtor’s estate—on whose behalf a trustee is bringing suit—are distinct legal entities.

But what about bankruptcy fiduciaries who are not court-appointed Chapter 7 or Chapter 11 trustees? A debtor-in-possession often will include in its Chapter 11 plan of reorganization the appointment of a litigation trustee, liquidating trustee, or other fiduciary to oversee litigation and make distributions for the benefit of creditors. Just like a court-appointed trustee, these fiduciaries will see a D&O policy as a source of potential recovery.

But a recent decision of the Sixth Circuit Court of Appeals may have far-reaching ramifications for fiduciaries who are not court-appointed, and may even erode at the general success Chapter 7 and Chapter 11 trustees have had in pursuing claims against debtors’ D&O policies.

In Indian Harbor Ins. Co. v. Zucker for Liquidation Tr. of Capitol Bancorp Ltd., 860 F.3d 373 (6th Cir. 2017), the debtor, Capitol Bancorp, confirmed a liquidating plan that created a liquidating trust to pursue litigation claims on behalf of the estate. The liquidation trustee sued Capitol Bancorp’s officers, alleging that they breached their fiduciary duties to the company. Indian Harbor Insurance—the company’s D&O insurer—filed a separate action seeking a declaration that the trustee’s claims fell within the policy’s insured vs. insured exclusion. The district court found the exclusion applied, and the liquidation trustee appealed.

The Sixth Circuit began its analysis with the language of the insured vs. insured exclusions, which excluded coverage for “any claim made against an Insured Person . . . by, on behalf of, or in the name or right of, the Company or any Insured Person.” This is fairly standard language, some variant of which is found in most D&O policies. Notably, there was no mention of the existence in the policy at issue of an exclusion to the insured versus insured exclusion which relates to insolvency and/or bankruptcy proceedings

The court went on to discuss the purpose of insured vs. insured exclusions, analogized well by the Zucker majority:

Not unlike a homeowner’s insurance policy that excludes coverage for a fire that the policyholder intentionally sets, these exclusions limit the management-liability insurance to claims by outsiders, prohibiting coverage for claims by people within the insured company. A company thus cannot hope to push the costs of mismanagement onto an insurance company just by suing (and perhaps collusively settling with) past officers who made bad business decisions.

(citing Biltmore Assocs., LLC v. Twin City Fire Ins. Co., 572 F.3d 663, 670 (9th Cir. 2009)). Although one would generally consider a liquidating trustee to be similarly disinterested as a court-appointed trustee so as to dissuade any fears of collusive behavior, the Zucker majority was not so convinced. It admitted that court approval of the debtor’s plan was a procedural safeguard, but stated that that alone did not “eliminate the practical and legal difference between an assignee [the liquidating trustee who was assigned causes of action under the plan] and a court-appointed trustee that receives the right to sue on the estate’s behalf by statute.” The majority concluded that “[t]he risk of collusion is surely higher when the insured individuals—the management of the debtor in possession—can negotiate and put conditions on a trustee’s right to sue them.” In other words, the mere fact that the debtor’s former managers can propose to name the individual who will serve as trustee and condition his or her authority is enough to raise the red flag of collusion beyond an acceptable threshold.

This is troubling for two reasons. First, if anything, management typically attempts to restrict the ability of a trustee to bring causes of action against them—a negotiating tactic that, if successful, would reduce overall the types of claims the trustee could bring; it would not elevate the risk of the trustee bringing collusive claims to the insurer’s detriment. Second, even if management sought to restrict or steer the trustee’s recovery efforts, those provisions would be subject to objection by creditors and interested parties and, if unacceptable, may result in a failure to garner sufficient votes to confirm the plan. As the dissent points out, “[f]unctionally, however, there is no distinction between an assigned trustee that a bankruptcy court has determined is independent and does not pose a risk of collusion, and one that is appointed by a bankruptcy court and is by nature of that appointment independent.”

With respect to the distinct-legal-entity argument, the liquidation trustee argued that a debtor-in-possession is legally distinct from the prebankruptcy “Company” defined in the insurance policy, making the insured vs. insured exclusion inapplicable to the trustee, who is the debtor-in-possession’s assignee. In response, the Zucker majority provides another analogy:

[T]his new-entity argument surely would not work before bankruptcy. Capitol could not have dodged the exclusion by transferring a mismanagement claim to a new company—call it Capitol II—for the purpose of filing a mismanagement claim against [Capitol’s management]. No matter how legally distinct Capitol II might be, the claim would still be ‘by, on behalf of, or in the name or right of’ Capitol. The same conclusion applies to a claim filed after bankruptcy. Here too the voluntarily transferred claim would be filed “on behalf of” or “in . . . the right of” Capitol. The exclusion remains applicable by its terms.

The majority interpreted its own precedent discussing the legal distinction between a prebankruptcy debtor and a debtor-in-possession narrowly, stating that the two are “one and the same person, although ‘wearing two hats’” (quoting Cle-Ware Indus., Inc. v. Sokolsky, 493 F.2d 863, 871 (6th Cir. 1974)). The majority concluded that Capitol, as a debtor-in-possession, was the same “Company” that entered into the insurance contract; therefore, the liquidation trustee, as assignee of the debtor-in-possession, stand’s in the “Company’s” shoes and is subject to the same defenses. “Just as the exclusion would bar a suit ‘by’ or ‘on behalf of” Capitol, it bars a suit by or on behalf of the Trust” (citing Biltmore, 572 F.3d at 671).

The majority then went a step further, putting even court-appointed trustees on shaky ground. The court stated, “[i]n truth, because the exclusion also applies to claims ‘in the . . . right of’ Capitol, it’s not even clear that a court-appointed trustee or creditor’s committee could collect on the policy.” But the court stopped short of deciding that issue, and held merely that “a voluntary assignee like the Trust, which stands in Capitol’s shoes, brings a breach-of-fiduciary-duty suit ‘by, on behalf of, or in the name or right of’ the debtor in possession” and, therefore, the claim was excluded from coverage under Capitol’s D&O policy.

The Zucker holding could have a dramatic and unintended impact on bankruptcy cases, the assertion of breach of fiduciary duty claims, and the availability of coverage for those claims. As the dissent notes:

If the majority’s decision becomes settled precedent, this Court will send a clear message to creditors in chapter 11 proceedings that if claims against directors and officers are deemed to be of significant value and the plan proposes to put those claims into a trust, the creditors must not agree to a plan proposed or even agreed to by the debtor-in-possession. Instead creditors will be required to seek the appointment of a bankruptcy trustee, where appropriate, or they will have to defeat the debtor-in-possession’s plan and propose their own disclosure statement and plan.

We will have to wait and see the true effect of Zucker, but all debtors, creditors, fiduciaries, and directors and officers are now on notice that the ability to recover against or receive coverage under a D&O policy may, depending upon the terms of the policy and the exact circumstances of the case, be compromised when such claims are pursued by a fiduciary who has not been appointed pursuant to statute or court order.

Over the past decade, several legislative proposals have been made for the establishment of a national infrastructure bank by both Democrats and Republicans. Although President Trump spoke against such a bank during his campaign, more recent indications are that he is inclined to support one. An infrastructure bank will, in fact, be a means to achieve, at least in part, his campaign promise to make major improvements in needed areas of U.S. infrastructure. It will also potentially provide a bi-partisan means of making these improvements.

A number of articles have been written on the subject of creating a U.S. infrastructure bank (see, e.g., Brookings, Setting Priorities, Meeting Needs: The Case for a National Infrastructure Bank). Although this article borrows some of what was written in such articles, it is focused on providing a roadmap for the creation of a U.S. infrastructure bank. It draws both on elements from three successful models of development banks—the European Investment Bank (EIB), the International Finance Corp. (IFC), a constituent member of the World Bank Group, and Kreditanstalt fur Wiederaufbau (KFW), the German promotional bank—and on prior legislative proposals for the creation of a U.S. infrastructure bank.

A reasonable goal for the initial operation of the new bank is to provide it with $20 billion of capital so that it can, in its first few years of operation, fund $200 billion of projects and quickly grow from that base. The initial capital can readily come from an earmarked portion of the tax proceeds derived from taxing the offshore profits of U.S. multinationals, a proposal that is part of the tax bills now before Congress.

This article recommends that the infrastructure bank be operated on an independent basis as a for-profit, government-owned corporation. It should be professionally managed with a long-term perspective on the type of projects it funds. The article concludes with suggestions about how a U.S. infrastructure bank might be established, funded, and operated.

Models of Development/Infrastructure Banks

EIB. The EIB was created in 1957 under the treaty establishing the European Economic Community. It is owned by the member states of the EU. Its capital is provided by the member states, and it is funded in the international capital markets. Management states that its purpose is “lending, blending and advising”—it lends to projects principally in the EU but also in the broader world, it blends its funds with those provided by other EU institutions, and it advises on project selection and project design (Governance of EIB).

The EIB holds itself out as following best practices in decision-making, management, and internal controls. Most observers agree that the EIB is an effectively managed institution. Given that it is an “international institution” by virtue of its joint ownership by the EU member states, it is not regulated as a commercial bank. The bank has generated a surplus of funds in each year of its operations (under IFRS it reported a financial loss in 2016 largely because of marking its funding liabilities to market). It issues fully audited financial statements under IFRS principles.

The key take-away from the EIB is that strength of management is critically important. A development institution must be run on a sound basis and should not be dependent on a continuing stream of government handouts.

KFW. KFW was founded in 1948 after World War II as part of the Marshall Plan. It is 80-percent owned by the Federal Republic of Germany and 20 percent by the German states. Its capital is provided by its shareholders, but it funds its operations from the capital markets. Although not formally regulated as a commercial bank, the German bank supervisory laws are “analogously applicable” to KFW (Application of German Banking Act to KFW). It has been operated on a continuous basis in a profitable manner and issues annual audited financial statements under IFRS principles.

KFW operates in areas where no banks are active due to unfavorable risk-return ratios in the market. Specifically, it lends monies in areas identified by the state, including, among others, providing financing for infrastructure, small- and medium-sized enterprises, environmental protection, and the housing sector. It seeks to focus on areas of the German economy that will promote growth (see “Management” discussion in KFW’s 2016 Annual Report).

The key take-away from KFW is its focus on areas of market failure, its regulation under essentially the same laws applicable to commercial banks, and its ownership structure being a partnership between the federal government and the German state governments.

IFC. The IFC was created in 1956 as the private-sector arm of the World Bank Group. It is a separately incorporated member of the group and is owned and governed by the member countries of the group. Like the EIB and KFW, its shareholders have provided the equity for its operations, but it funds itself in the international capital markets. As with the other two institutions, it annually issues fully audited financial statements, but in its case under GAAP.

The IFC was founded to further economic development by encouraging the growth of productive private enterprises largely in less-developed countries. It does so by providing debt funding singly or together with other lenders to development projects. It also provides equity funding to some projects and has established several equity funds for this purpose (IFC Products and Services). It generally has operated on a profitable basis.

The key take-away form the IFC is its partnership with private enterprise. By forging public-private partnership investing in worthwhile projects, it has been able to further development in less-developed countries.

Overall, these three institutions show the importance of high-quality management, a well-defined purpose charting the institution’s operational goals, and the ability to sustain themselves by conducting their business in profitable manner. KFW is a model for cooperation between a federal government and state governments and for operating under the regulatory standards of a commercial bank. The IFC brings to the fore the importance of a development bank joining with private enterprises in significant projects. All the institutions operate in a fully transparent fashion with audited financial statements available for public scrutiny.

History of National Legislative Proposals

Legislative proposals for infrastructure banks in the United States go back to 1983 when legislation was introduced to authorize state infrastructure banks (A History of Infrastructure Bank Proposals). In subsequent years, many of these banks were created, but they never became of significant size. Not until 2007 did a proposal for a national infrastructure bank emerge. In that year, Senator Dodd (D-CT) and Senator Hagel (R-NE) introduced the Infrastructure Bank Act of 2007. This legislation was never enacted, but the idea for a national infrastructure bank was picked up by President Obama in his 2008 campaign. This idea was carried forward and became part of President Obama’s legislative preproposal to Congress in 2009 and was repeated in subsequent years. Several proposed bills were also introduced in Congress. None came to fruition.

More recently, proposals for national infrastructure banks were made in the 114th Congress (2015 and 2016) and the 115th Congress (2017 and 2018). Four of these proposals (HR 413 by Rep. Delaney (D-ND), HR 3337 by Rep. DeLauro (D-CT), S 1296 by Sen. Fischer (R-NE), and S 1289 by Sen. Warner (D-VA)) deserve a brief appraisal (summarized in How a National Infrastructure Bank Might Work). S 1589 and HR 413 received broad, bi-partisan support. None of the bills in the 114th Congress were enacted.

All the bills call for the bank to be a wholly owned government corporation. Three of them call for a board of trustees/directors to be appointed by the President, while one (S 1296) somewhat unusually calls for the directors to be appointed by the majority and minority leaders of the Senate and House. As for eligible infrastructure projects, all cover transportation, two add energy and water projects, and one adds environmental measures and telecommunications. All authorize the bank to make loans. Several expand the nature of assistance from loans to include loan guarantees, grants, and equity investments. A mix of measures is suggested for the means to capitalize and fund the new entities. Of interest, two suggest that some of the capital could come from repatriated foreign earnings, a suggestion picked up later in this article.

Infrastructure Bank Proposal

The basic features for a new, national infrastructure bank are suggested below.

Type of company. The new bank should be incorporated as an independent, government-owned corporation (GOC). Congress establishes GOCs to provided market-oriented services on a self-sustaining basis. They span a wide spectrum of businesses from the Tennessee Valley Authority to the Federal Home Loan Banks (CRS, Federal Government Corporations: An Overview). The legislative proposals previously examined unanimously suggested this form of corporation. An idea to consider is to follow the precedent set by KFW and have the corporation jointly owned by the federal government and the various states; however, given the 50 U.S. states, this might create a cumbersome ownership structure. A state advisory council may be a more effective means of involving the states in the new bank.

The new bank should not be created as a government-sponsored enterprise (GSE). Because of the bailout of Fannie Mae and Freddie Mac (both GSEs) in the financial crisis of 2008, a stigma now surrounds GSEs. It would be wise to avoid this stigma with the new bank. For the same reason, it should not be in the business of building up a massive position of off-balance sheet liabilities as Fannie and Freddie did by providing a large number of loan guarantees.

Governance. To insulate the institution from overly partisan oversight, the bank should be independent and not subject to direct supervision by an executive agency or a Congressional committee. Thus, the most effective governance structure is for the bank to have a Board of Directors seven in number, six appointed by the President and confirmed by the Senate, and the seventh from a state advisory council.

Although independently managed, the infrastructure bank should be subject to the provisions of the Government Corporate Control Act and to the Chief Financial Officers Act (as discussed in the CRS article cited above). Under the former, the infrastructure bank must prepare and submit to the President annually a business-type budget for the coming year; under the latter, it must submit to Congress an annual management report, including, among other things, financial statements and a statement of accounting and administrative controls. Although GOCs are given some options on the type of annual financial audit they must undergo, the option most appropriate to the new infrastructure bank is that of an independent external auditor from a firm well versed in auditing financial institutions.

As an additional feature, the new bank should create an advisory council consisting of members appointed by the 50 state governors. The council would create an executive committee to meet periodically with the bank’s management. In addition, the executive committee would appoint one member to the board of directors.

Scope of infrastructure projects authorized. In its 2017 Infrastructure Report Card, the American Society of Civil Engineers estimated that the infrastructure needs of the United States from 2016 through 2025 would be about $4.590 trillion, and the estimated amount of funding available to satisfy that need under current projections would be about $2.526 trillion. The resulting funding gap is approximately $2.064 trillion. The need for infrastructure spending was divided into 11 different categories, including surface transportation and water and electricity projects, among others. During the most recent presidential campaign, both candidates recognized the importance of infrastructure improvements and made promises to dramatically increase the amount of infrastructure spending.

Given the foregoing, a compelling case can be made for a large-sized national infrastructure bank. With the diversity of where spending is needed, a broad definition of the scope of infrastructure projects that can be funded by the infrastructure bank is desirable. An expansive definition for “infrastructure” suitable for the new bank can be taken from the definition found in the proposed National Infrastructure Development Act of 2007:

a road, highway, bridge, tunnel, airport, mass transportation vehicle or system, passenger or freight rail vehicle or system, intermodal transportation facility, waterway, commercial port, drinking or waste water treatment facility, solid waste disposal facility, pollution control system, hazardous waste facility, federally designated national information highway facility, school, and any ancillary facility which forms a part of any such facility or is reasonably related to such facility, whether owned, leased or operated by a public entity or a private entity or by a combination of such entities . . .

A necessary caveat to this proposed definition is that funding for any targeted project should not be readily available in existing credit markets. The national infrastructure bank should not enter markets adequately served by the private financial institutions and the credit markets in which they operate. That said, the role of the IFC in encouraging private investment by investing side by side with private investors can be adopted for many projects. The creation of public-private partnerships for many projects should be encouraged.

Operation of the bank. The new infrastructure bank should be operated on a quasi-independent basis. It should not be simply another department in the executive branch of the government. Furthermore, it should not be forced to seek funds from Congress on an annual basis. If it is established in this fashion, it can be focused on long-term projects needing funding. Given that it should be operated in an independent manner, it must be operated as a profit-making bank. This will be akin to how EIB, KFW, and IFC all operate today.

If it is to be a profitable, successful bank, it must have capable, long-term management. Like the EIB, it should seek to follow best practices in decision-making, management, and controls. In short, it should have a cadre of highly qualified professional managers.

Drawing from the fashion in which KFW is operated, appropriate banking regulations should be issued regarding the infrastructure bank. The regulations should stipulate that the key provisions of the federal banking regulations will be applied analogously to the bank. The most suitable body to be tasked with creating and implementing these regulations is the Federal Reserve Bank.

Form of funding for financed projects. The infrastructure bank should fund projects through individual loans or as the lead manager of loan syndications where it has invited other public and private institutions to join it in making a loan or a package of loans. It may also raise money by establishing debt funds designed for specific types of projects or for specific geographic areas.

It addition, the new bank may make equity investments. These investments typically would provide a base for raising added debt financing for suitable projects. As with debt funds, equity investment funds could also be established.

In every instance, the investments made by the infrastructure bank should be made with a view toward making a profit in the long-term. The new bank should not be in the business of making outright grants for projects. If it gets into the grant-making business, it will need to quickly obtain annual funding from Congress and would not be able to operate independently with a long-term horizon.

Capital for the bank. In order to have a material impact, the new infrastructure bank should be adequately capitalized at the outset. A reasonable goal is to have the bank supply funds for $100 billion of projects in its first two years of operations and to quickly build its balance sheet from that point. To give the bank a solid base of capital, it should be provided with initial Tier 1 equity capital of $20 billion. Under the capital standards set for U.S. banks following the Basel accords, this should permit the bank to grow its balance sheet in its first years of operation to over $200 billion and still have the bank well capitalized. Further growth should come from the bank’s retained earnings.

A good source of the capital for the new bank is from an earmarked portion of the tax proceeds derived from the new tax to be imposed on the overseas retained earnings of U.S. multinationals, as currently contemplated in the tax bills before Congress. In 2016, the Joint Committee on Taxation estimated that the previously untaxed foreign earnings of U.S. corporations at the end of 2015 to be approximately $2.6 trillion (Letter of Joint Committee on Taxation to Congressman Brady). The pending tax bills would tax these earnings at a rate of somewhere between 5 percent and 14 percent, depending on how the earnings were invested and on the version of the tax legislation to be considered. The Joint Committee has estimated that the tax raised by this provision would be approximately $200 billion (Joint Committee Revenue Estimate of Senate Bill). Hence, a capital base for the new bank of $20 billion would only amount to earmarking 10 percent of this tax. This may seem like a novel suggestion, but it is one that was proposed in several of the infrastructure bank legislative proposals previously examined. Although it may not be possible to have this type of provision included in the pending tax legislation, the legislation needed to create an infrastructure bank could contain such a provision, particularly given that the current proposals allow for the tax on untaxed foreign earnings to be paid over eight years.

The balance of the funds needed to grow the infrastructure bank’s portfolio of loans and investments should be raised in the form of debt from the capital markets. The bank should be able to tap these markets for the needed funds. EIB, KFW, and IFC all raise needed funds in this fashion.

Conclusion

The suggestions in this article can be summarized as follows:

Enabling environment. The infrastructure bank should be established under appropriate legislation with a clear mandate for the scope of its operation. In addition, it should be subject to banking supervision under the equivalent of established U.S. regulatory guidelines for banking institutions. These measures will ensure that the bank is appropriately incorporated with a clear focus on the nature of its business. It should prevent operational creep into areas not intended for its operations.

Well managed. The infrastructure bank should have a core of professional bankers leading it with a clear view toward making it a successful bank. Although profitability should not be its sole goal, it is a necessary condition to satisfying the next recommendation below.

Operates on a continuing and sustainable basis. The infrastructure bank should not need to rely on continuing government support for its operations. It should be able to engage in meeting long-term goals for the funding of infrastructure projects. It should not be subject to the immediacy of political pressures.

Insulated from political interference and undue pressure. One of the causes of failures of national development banks in other countries is the engagement in some form of crony capitalism. This corrupted the bank’s credit intermediation function. By making the proposed new bank independent from political interference, this fate should be avoided.

Provides funding not otherwise available in private credit markets. The infrastructure bank should not compete with private financial institutions in the credit intermediation function. Private institutions can efficiently allocate capital in areas where they can generate an adequate long-term return on their capital. The infrastructure bank should operate in areas where private institutions are not providing needed capital. These are areas of so-called market failures. This may be a murky concept to apply in practice. Nevertheless, it is an important one, and one where appropriate banking supervision should be of assistance in realizing this goal.

Close to 10 years have passed since the filing of the Chapter 11 cases of Tulsa, Oklahoma-based SemCrude L.P. However, the Third Circuit Court of Appeals recently affirmed a 2015 district court ruling that resolved a dispute between oil producers and downstream purchasers over the perfection and priority of interests in oil sold by SemCrude L.P. and its affiliates. The Third Circuit’s holding in In re SemCrude L.P., 864 F.3d 380 (3d Cir. 2017), affirmed the earlier bankruptcy and district court rulings that the downstream purchasers were “buyers for value” and took oil purchased from SemGroup free and clear of the oil producers’ liens. The decision serves as a stark warning for oil producers not to rely on automatic perfection provisions of state law, and take efforts to put subsequent purchasers on actual notice.

SemGroup filed for Chapter 11 in 2008. SemGroup and its subsidiaries provided midstream oil services, whereby SemGroup purchased oil from oil producers and resold that oil to downstream purchasers. SemGroup also traded oil futures with two of its downstream purchasers in a trading strategy that ultimately led to SemGroup’s insolvency. The downstream purchase agreements provided that in the case of default, the downstream purchasers could offset the amounts owed to SemGroup by the amount that the SemGroup owed the purchasers for the value of outstanding futures trades. At the time of SemGroup’s filing, more than one thousand oil producers were unpaid.

The offset feature of the purchase agreements resulted in full recovery to the downstream purchasers; however, the oil producers received only partial payment in the plan of reorganization. Unhappy with only a partial recovery under the plan, the oil producers brought claims against the downstream purchasers under theories of fraud, priority security interests under Texas and Kansas laws, and implied trust under the Oklahoma Production Revenue Standards Act (PRSA).

The court entirely rejected the claims of security interests. Texas and Kansas have enacted nonuniform Uniform Commercial Codes with special provisions for owners such as oil producers. In Texas, interest owners have an automatically perfected security interest in oil produced and the identifiable proceeds related thereto. In Kansas, oil producers are required to file an “affidavit of production” in order to perfect their security interests in the oil. In both jurisdictions, the oil producers’ lien is extinguished after the first purchaser sells to a buyer in the ordinary course.

The oil producers argued that, under applicable state law, they held automatically perfected security interests in all oil sold to SemCrude, and that the downstream purchasers took subject to those security interests. First, the court held that the oil producers had not perfected the security interests in accordance with the local laws of Delaware and Oklahoma (where the debtors, the first purchaser of the oil, reside). Given that Texas and Kansas had adopted Article 9 of the Uniform Commercial Code, it is the laws of the jurisdiction of the debtor’s location that “governs perfection, the effect of perfection or nonperfection, and the priority of a security interest in collateral” under U.C.C. § 9-301(1).

Second, the Third Circuit held that the downstream purchasers were “buyers for value” who acquired the oil without any actual knowledge of the oil producers’ interests, and therefore the downstream purchasers acquired the oil free and clear of any asserted security interest. In short, although Texas and Kansas state law appeared to afford oil producers automatic protection of their security interests, the validity of those security interests turned on perfection in the debtor’s locale and the actual knowledge of the purchaser.

With respect to the oil producers’ PRSA claim, the oil producers asserted that they held an implied trust that traveled “perpetually down the stream of commerce . . . [and] whoever possess the oil does so for [the oil producers’] benefit.” The Third Circuit rebuffed the oil producers, holding that “this interpretation simply fails the text of the statute” and that “whatever duties PRSA creates, they do not apply to downstream purchasers.” Similarly, the court found no hallmarks of fraud and observed that there existed no evidence that SemGroup “ever intended to avoid paying for oil” or that the downstream purchasers conspired with SemGroup.

In closing, the court observed that the oil producers “theoretically could have perfected their security interests, traced those interests in the oil that extended to their accounts receivable, and forbade SemGroup from using those accounts as margin collateral for their options trades.” Having failed to take those steps, the oil producers could not look to parties like the downstream purchasers “who took precautions against insolvency . . . [to] act as insurers to those who took none.” The effect of any other finding “would be chaos.”

Overview of a Compensation Committee’s Basic Responsibilities

The listing requirements of both NASDAQ and the New York Stock Exchange mandate that a committee of independent, nonemployee directors must have principal responsibility for the compensation of CEOs and other executive officers. Accordingly, as part of their basic responsibilities, compensation committee members regularly will be engaged in assessing the performance and determining the pay levels of executive officers, the design of the compensation programs applicable to them, and the contractual arrangements governing their employment. The compensation committee members typically also are responsible for formulating share ownership guidelines, compensation clawback policies, insider-trading and anti-hedging policies, and approving compensation-related proxy disclosure.

The compensation committee also is tasked with assessing the link between compensation and enterprise risk management. In that regard, since 2009 the SEC in Item 402(s) of Regulation S-K under the Securities Act of 1933 (as amended) has required a company to disclose whether “risks arising from the registrant’s compensation policies and practices for its employees are reasonably likely to have a material adverse effect on the registrant” and, if so, to disclose the compensation policies and practices as they relate to risk management. As a practical matter, this has led companies to engage in a careful risk assessment of their compensation programs, not limited to those applicable to executive officers. Given the ultimate oversight duties of a board of directors, and the specialized knowledge possessed or developed by members of the board’s compensation committee, it is unsurprising that compensation committees are frequently given the principal responsibility of overseeing the process of ensuring that compensation design throughout the organizations does not encourage inappropriate risk-taking.

The Link Between Compensation and Risk

Following the corporate scandals of the early 2000s (e.g., Enron, WorldCom, and Global Crossing), corporate-governance experts, academics, the media, elected officials, regulators, and the general public began to focus on the possible role that executive compensation played in incentivizing inappropriate behavior. In particular, many argued that the excessive risk-taking that led to such scandals was fueled by an inordinate management focus on short-term stock price gains that was tied to the overuse of stock options. The basic insight of these critics was that stock options had at least two major drawbacks. First, the flexibility as to timing of exercise allows executives to benefit from short-term stock price increases that do not necessarily reflect the creation of long-term shareholder value. Second, stock options provide an asymmetrical incentive, with the holders benefiting from stock gains but not losing any investment through stock price losses. As a consequence, all things being equal, executives with substantial stock-option holdings are more likely to favor high risk/reward investments or other corporate actions that could generate significant stock increases in the short-term (that could be captured by option exercises by those executives), but might have significant long-tail risk.

Critics recognized that there were substantial accounting and tax incentives for corporations to use stock options, and their concerns led to a revisiting of the accounting treatment of stock options and ultimately to the adoption of FAS 123R (now redesignated as ASC 718), which requires the expensing of the grant date value of stock options determined by using Black Scholes or other option valuation methodology. This led to a reduction in the use of stock options and an increased utilization of restricted stock and restricted stock units coupled with shareholding requirements—the thought being that these instruments would better align executive incentives with those of the corporation and its shareholders over the longer term, and dis-incentivize executives from excessive risk-taking.

At most public companies, compensation committees became responsible for ensuring that the design and mix of executive officer compensation elements did not create incentives for unacceptable risk-taking, and approved the annual disclosure under Item 402(s) of Regulation S-K of the Securities Act of 1933 (as amended) regarding whether the “risks arising from the registrant’s compensation policies and practices for its employees are reasonably likely to have a material adverse effect on the registrant.”

Expanding the Committee’s Role

Until recently, most compensation committees focused their compensation risk assessment exclusively on the remuneration of executive officers and, in regulated financial institutions, “significant risk-takers” (i.e., the individuals who are in the position to make significant bets of company capital). The exceptions tend to be in certain industries—in addition to financial services, the pharmaceuticals and medical-device industries are the sectors in which public companies currently are somewhat more likely to involve the independent directors in overseeing broader employee incentives. Unfortunately, most companies in which compensation committees currently are engaged in overseeing the risk assessment of rank-and-file employee compensation arrangements do not provide sufficiently detailed disclosures to describe differences in approach in any depth.

More recent events, particularly the sales practices controversy at Wells Fargo, have illustrated for corporations more generally that the conduct of relatively low-level employees can have a huge reputational impact on companies, and that the role compensation may play in incentivizing inappropriate conduct cannot be overlooked. Trusting management to police incentive arrangements of rank-and-file employees without director-level oversight seems somewhat naïve in 2017.

As a result, we can expect more and more compensation committees to undertake additional oversight responsibility over compensation arrangements applicable to employees below the executive officer level. Although this is unlikely to involve retaining day-to-day decision making about rank-and-file incentives, one can expect that companies will establish structures whereby management will be required to report regularly to compensation committees about the design of such incentives and safeguards protecting against their potential for promoting inappropriate conduct. Companies also may be more likely to highlight such oversight in their public disclosures. It should be instructive to observe the different models of risk director oversight of rank-and-file incentives—and perhaps consensus best practices—that will be developed in the coming years.

“Garbage in, garbage out” is a phrase data scientists often use. One can apply it in many contexts, but it arises from the idea that the quality of the output of a computer will only be as good as the quality of its programming. In that simple phrase, there is a central truth often overlooked in discussions surrounding artificial intelligence (AI) and machine learning (ML): no matter how skilled your coders, or how great your algorithms, the quality of the results, signals, insights, and “learnings” these technologies provide will only be as good as the data fed to them.

AI and ML are nebulous terms often used interchangeably; however, they are not the same. AI was famously described by Marvin Minsky in Steps Toward Artificial Intelligence as the ability of machines to behave and learn like humans. ML, a subset of AI, has been best described recently by Amanda Levendowski in How Copyright Law Can Fix Artificial Intelligence’s Implicit Bias Problem as the application of mathematics and computer science to create a machine’s ability to improve automatically through experience. Just like humans use massive data sets (our memories) to become more efficient and make better decisions over time, AI and ML systems rely on data to do the same.

Therefore, data is at the core of developing new AI and ML systems. Accessing and securing the most and best data is where the attorneys come in. Companies and organizations developing AI technologies want access to the best data possible with the least restrictions possible. At the same time, companies and organizations want to retain exclusive access to datasets that are (or could be) market differentiators. There are tensions between these interests, and data-licensing attorneys will increasingly be at the center of navigating them, including during negotiations with third parties and regulators and in the creation and management of data retention and usage policies.

There are terabytes of free harvestable data available online. Wikipedia, for example, is a common source of no-cost “general knowledge” data for AI and ML technologies. Many other datasets are freely available to AI and ML developers with open-access or attribution-only licenses. Attorneys must analyze each one of these licenses in the context of the use cases their clients are pursuing (or may pursue later). Conducting such an analysis requires careful planning and interviews with clients so that the attorney can accurately understand the use case for the data accessed to ensure it is consistent with the licenses granted by the licensor of the data set.

The owners and licensors of free data often lack the resources to actively curate or inspect the data to ensure quality and accuracy. Therefore, many free data sets contain errors, bias, and misinformation that can negatively affect the AI and ML systems using it. This quality-control problem has created a large market for curated data sets that sit behind paywalls, restricted licenses, and regulatory hurdles. Data-licensing attorneys are increasingly asked by clients to negotiate and draft license rights to highly protected and expensive data sets. This raises the stakes of the license analysis and negotiations. Given that exactly how AI and ML systems use data to “learn” can be opaque, a simple contractual miscalculation or limitation on use rights in a data-licensing agreement can have catastrophic results on development if the developers cannot use the data in the way that is most effective for the AI or ML system they’ve designed. Therefore, it is a good practice for data-licensing attorneys to get involved and provide advice and counsel during the development process so that that the development team can understand the legal ramifications of its design choices, and so that the attorney can work in parallel to pave the way toward accessing the best data assets available. Being embedded will also help attorneys counsel clients on regulatory compliance, privacy, and security related to the onboarding and processing of such data in real time.

AI and ML systems have a tremendous appetite for data. Failure to use the best and most accurate data can have both negative business consequences (loss of revenue and failure to remain competitive) and harmful societal implications (biased, unethical, or disparate outcomes). Some of the biggest obstacles to fueling AI and ML with the best data are not technological, but legal in nature. Thus, collaboration among lawyers, product developers, regulators, and data scientists is critical to ensuring that, as AI and ML technologies continue to develop and mature, they have access to the best data available and simultaneously protect the privacy of data subjects and the security and integrity of the data and the technologies that use it.

At one time, the New Business Rule generally prevented an injured party from obtaining a damages award for lost profits due to the opposing party if the injured party was a newly established business (R. Dunn, Recovery of Damages for Lost Profits, 3d ed.,1987). Absent a history of past profits, future profits seemed too “uncertain and speculative,” particularly in the progress-oriented atmosphere of the late 1800s when rules defining damages first developed (Hickman v. Coshocton Real Estate Co., 58 Ohio App. 38 (Ohio ct. App. 1936)). In addition to their desire to limit excessive damages, courts often distrusted jurors with the discretion necessary to evaluate the reasonableness of future profit estimates (B. Bollas, New Business Rule and the Denial of Lost Profits, 48 Ohio State L.J. (1987)).

Changing attitudes towards jurors, a consensus focused on the inherent injustice to new businesses, and recognition of the economically nonoptimal allocation of resources that the New Business Rule encouraged may have all played a role in the shift in the interpretation of the rule away from a finding of law to a finding of fact, as pointed out by Bollas in the Ohio State Law Journal, and by Everett Gee Warner and Mark Adam Nelson in “Recovering Lost Profits,” 39 Mercer L. Rev. (1988). In most cases, says Michael L. Roberts in his article, “Recovery for the New or Unestablished Business” (The Alabama Law. (Mar. 1987)), the emphasis focuses on the fact that profits were lost, not on an absolute measure of those profits. As a result, calculation of lost profits need no longer conform to “absolute certainty” requirements; the “reasonable certainty” standard as applied to existing businesses with a history of profits has been applied to new enterprises as well (Michael G. Stewart, The Evolution of the New Business Rule, 17 Cumberland L. Rev. (1986)). However, as evidenced in Schonfel v. Hilliard, 62F. Supp. 2d 1062 (S.D.N.Y 1999) and Tipton v. Mill Creek Gravel, Inc., 373 F.3d 913 (2004) courts still give lost-profits claims heightened scrutiny when the party has no financial history. Clearly, when a business can show a history of profitability, both in the long-term and recent past, this profitability can often be reasonably projected into the future (with all other variables held constant). Additionally, if the contractual agreement between two parties makes mention of expected profits, quantification of those profits lost in the event of a breach proceeds without difficulty.

When faced with quantifying lost profits for new businesses with little or no history of earnings prior to the breach, quantification of lost profits becomes more of a challenge. Fortunately, the widespread application of the “reasonable certainty” standard allows several methods of quantifying damages without the requirement of complete and absolute certainty as to amount. The specific approach taken depends upon the operational effect the breach has upon the new business. An enterprise that fails because of the breach necessitates slightly different analysis than does one which continues operations at a reduced or at a level capacity. Regardless of the approach taken, however, an overriding concern focuses on the individuality of the case.

1. Business Enterprise Continues

If the business enterprise survives the breach, post-breach income figures, either for the injured party or for another who continues the enterprise at the same location, may be used to approximate profits lost due to the breach.

Post-Breach Profits, Injured Party

In some cases, the harmed business may be able to resume business along the same growth curve as existed prior to the breach. Although no permanent harm has occurred, the business has experienced a shortfall in income from the time of breach until production returns to normal. Profits will always lag as a result of the breach.

Notice that this method does not rely upon profitability at the time of breach. Rather, it focuses on the timing of profits. In limited circumstances, it may be possible to utilize post-breach income numbers as a proxy for expected income during the shortfall period. Additionally, use of this method depends heavily upon the continuation of existing market and production factors after the breach.

McDermott v. Middle East Carpet Co. Associated, 811 F.2d 1422, (11th cir.1987) (MECCA) applied this concept in determining a damage award for lost profits. Plaintiffs McDermott and his corporation Criterion Mills served as co-consultants to the royal family of Kuwait during construction of a carpet factory in the Middle East. As a result of McDermott’s inability to perform his contractual duties, production of the facility fell behind schedule. Additionally, McDermott ordered raw materials that were incompatible with production equipment installed earlier. In combination, these factors caused an eight-month delay in the production of carpets. MECCA suffered diminishing losses for 1979, 1980, and 1981 before a fire destroyed the factory in 1982. A new carpet plant completed in late 1982 was profitable.

Expert testimony utilizing a hypothetical economic model incorporating market variables established that a “delay in commencing production will cause a corresponding delay in reaching full profitability.” Significantly, profits were awarded based on MECCA’s profit and loss statement for 1983, more than four years subsequent to the breach and with a reconstructed facility. Post-fire income figures were sufficient because the relevant variables remained constant. The new facility produced the same kind of carpet, used similar machinery, and operated within the same market as the destroyed facility. The pattern of diminishing losses just prior to the fire, consistent with the expert’s economic model, suggested that MECCA would have soon reached profitability.

Expert testimony convincingly quantified lost profits because the economic model supported the substitution of the new facility’s performance for that of the old. Additionally, the model properly accounted for variables such as changes in management, labor, capital, and raw materials. Finally, the existence of a “stable and monopolistic” Egyptian market and protection from foreign competition simplified the analysis by eliminating many variables associated with a free-market system.

Post-Breach Profits, Successor Business

It is possible that the injured party may vacate the premises of former activity, only to be replaced by another company in the same business. In this case, assuming that market variables have remained constant, an extrapolation can be calculated based on comparing the replacement business entity with the original. Care should be taken here to ensure that the replacement business is actually comparable to the original. Calculating lost profits in these circumstances approaches quantification using benchmarking techniques.

2. Business Enterprise Ceases

Using post-breach income figures makes sense when a business merely experiences a temporary shortfall in production of income or is continued by a different entity. However, in the event that the new business is unable to recover from the breach, it will have neither a significant history nor a future of recorded profits. Although this complicates matters, lost profits may still be quantified with reasonable certainty.

In all cases, the most important step involves the identification of critical success factors. Critical success factors, as the name implies, are those elements that are absolutely necessary for a particular business to succeed. Although most businesses share a common core of essential skills and attributes that promote economic viability, the mix of these skills can vary widely among individual businesses. Elements that are important for the success of a service-oriented business may differ substantially from that of a capital-intensive business. For example, the critical success factors for a health spa may include location, marketing strength, employee reputation, management expertise, and start-up capital. On the other hand, the critical success factors for a computer manufacturer may be sufficient capital, patented technology, distribution channels, supplier relationships, and advantageous labor relationships.

Short-Term, Prebreach Operations

Prior to the breach, the new business may have experienced some level of short-term operations. Even if the business operated for less than one year, sufficient information may exist to extrapolate lost profits as a result of the breach. So long as some information is available, it can serve as the starting point for a comparison to industry statistics. Key industry statistics to examine, among others, include financial ratios such as profit margins, debt-to-equity ratios, and receivable and inventory turnover. Other vital information includes trends in sales, cost of sales, general and administrative expenses, customer profiles, and potential regulatory impacts. Furthermore, a thorough analysis of contracts such as sales contracts, lease agreements, and employee contracts can provide a valuable source of information regarding projected future revenue and expenses.

It is not even necessary in all cases to demonstrate the existence of profits during that abbreviated period (Brookridge Party Center v. Fisher Foods, Inc.,12 Ohio App. 3d 130 (1983)). For example, most new businesses experience an initial period of diminishing losses followed by a gradual progression to profitability as the business moves up the learning curve. Losses in the initial stages of the business’ life cycle are to be expected, particularly if they remain in line with industry averages. If the business possesses the critical success factors specific to its particular enterprise, it can be reasonably expected to perform at least as well as the industry average, implying that it would “turn the corner” at some point in the future (along the industry average growth curve).

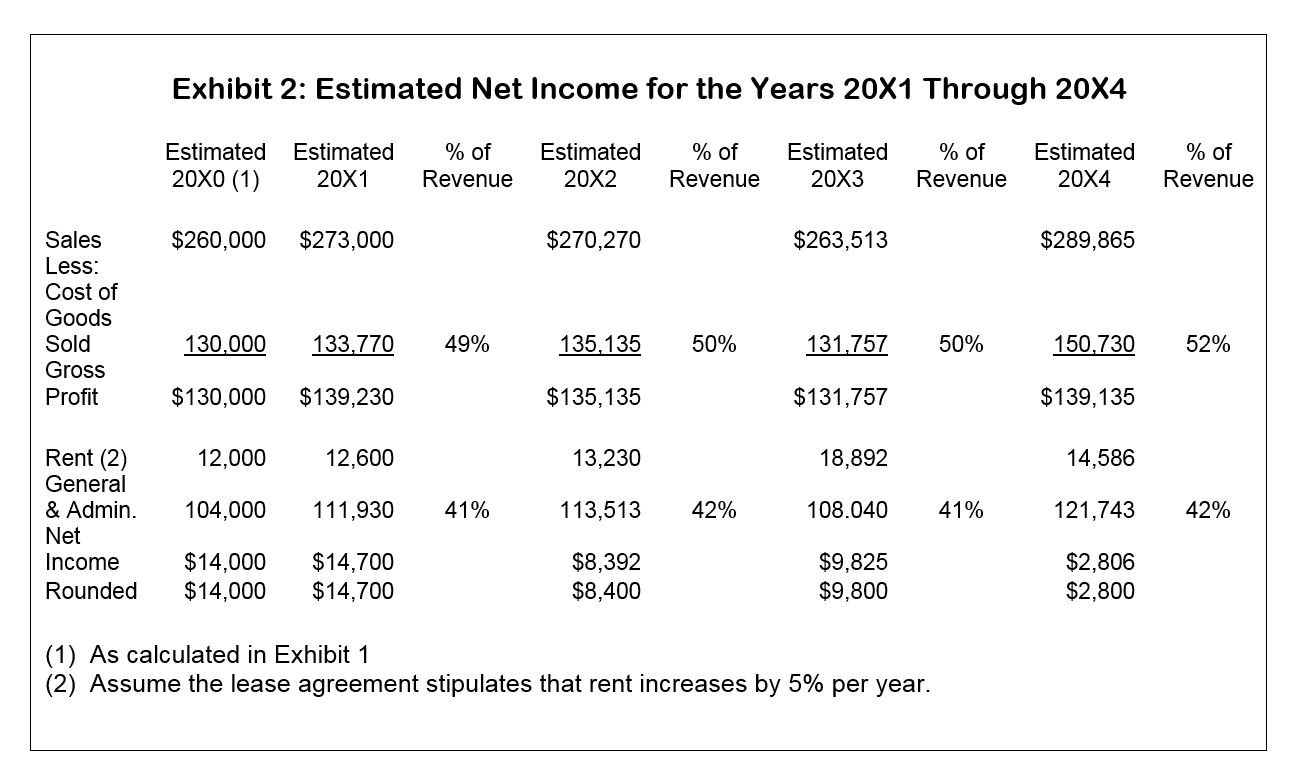

Example

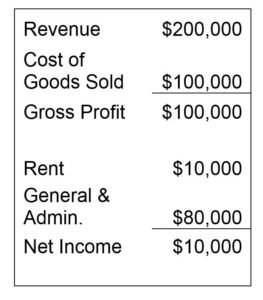

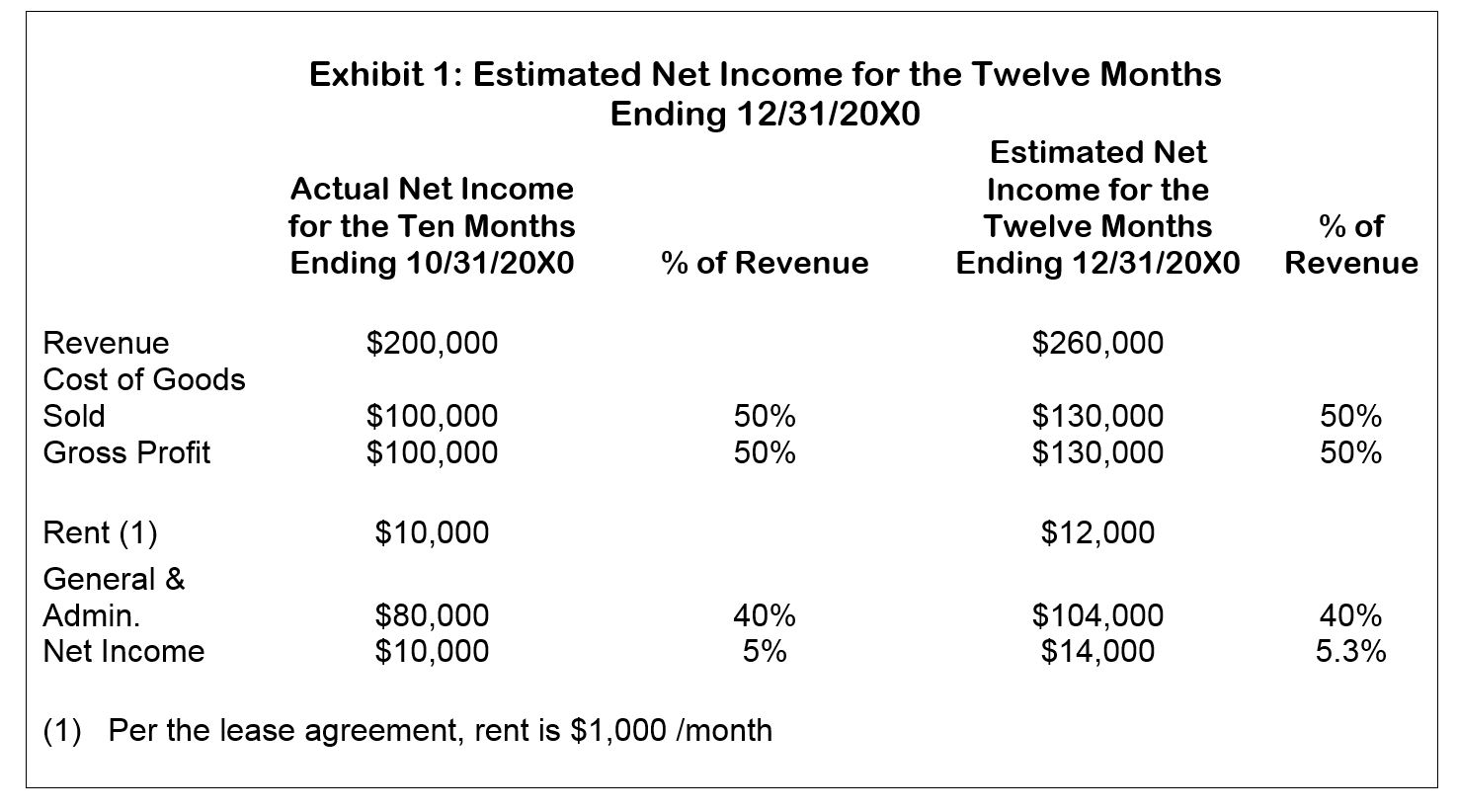

Assume a retail business commences operations on January 1, 20X0 and ceases business on October 31, 20X0 due to a contract breach. Furthermore, assume it is now January 20X5 and the case is going to trial. Actual net income for the ten months ending 10/31/20X0 is as follows:

Step 1

The first step involves projecting financial results achieved in the first 10 months over a 12-month period. Where possible, contracts or agreements should be used to determine future activity.

For example, let us assume that rent expense is fixed at $1,000 per month as stipulated by the lease agreement. Therefore, we would expect rent expense of $12,000 for the 12-month period ending 12/31/20X0 ($10,000 plus $2,000 rent for November and December). Where contracts and agreements cannot be used to project financial results, other techniques must be employed. Assume that an interview of similar retailers at the same location reveals that January to November sales are relatively constant, with December averaging twice that of any other single month. Multiplying actual financial results for the 10-month period ending 10/31/20X0 by a multiple of 13/10 provides a reasonable estimate of results for the year ended 12/31/20X0 (see Exhibit 1).

Step 2

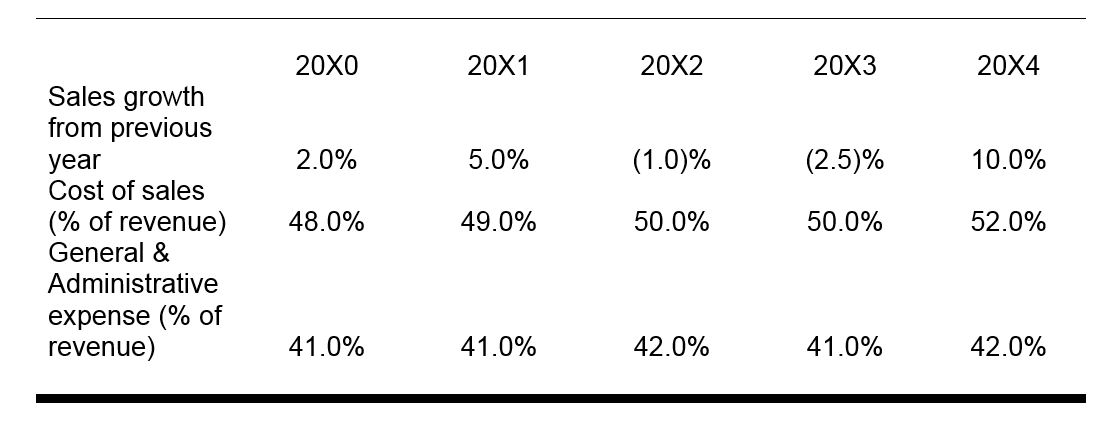

The next step involves accumulating industry data (statistics and financial ratios) for companies operating in the same industry as the injured company. This information can be accumulated by conducting database searches. For example, the SIC (standard industry code supplied by the IRS) for the injured company can be used to search databases such as Dunn & Bradstreet, NEXIS, and the SEC for financial data specific to that industry. Let us assume that the following information regarding financial results was uncovered thorough a database search for our example (see below).

These ratios can then be applied to the injured company to estimate financial results in the years 20X1 to 20X4 (see Exhibit 2).

Note that the estimated financial results in 20X0 do not exactly match industry ratios in that same year. One would expect a start-up company to operate with less efficiency than industry averages (which include companies with significant experience). However, given that actual financial results in the first 10 months ending 10/31/20X0 approximate industry ratios in 20X0, actual results for that 10-month period are used to project earnings in future years.

Losses suffered during initial operations do not necessarily preclude projection of profits in future years. For example, if the injured company in the example below suffered an actual loss in the first 10 months of 20X0, one could argue that industry ratios should be applied to actual revenue in 20X0 to estimate net income or net loss in 20X0. After all, as a start-up company, the injured company can expect losses in its initial period of growth. By utilizing industry ratios, we nullify the “start-up effect” by assuming performance of an established company.

Bear in mind that industry averages are meant merely as guidelines; they should not be taken verbatim. Industry average statistics and specific company statistics commonly differ, particularly when the specific company is a brand-new enterprise.

This means merely that industry statistics and ratios should be used as a starting point, with adjustments made to approximate the specific circumstances of the injured company. For example, if you know that the injured company utilizes a greater proportion of debt financing than the industry average, estimated interest expense should be increased accordingly. Additionally, if the injured company is more labor intensive than that of the industry average, salary expense should be adjusted accordingly.

Benchmarking

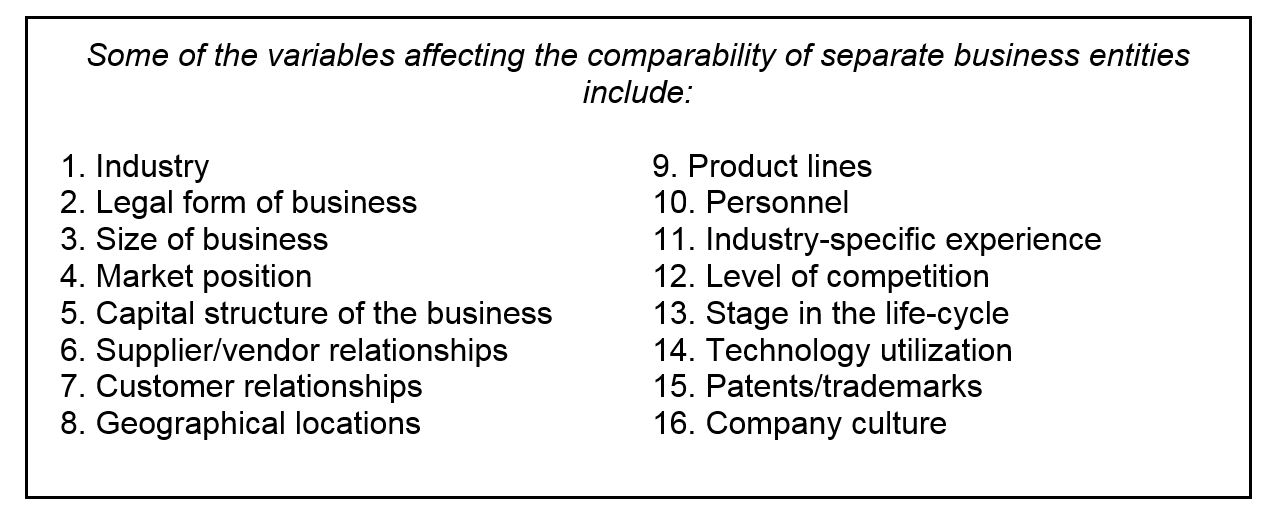

Another effective method often utilized to quantify lost profits when a business ceases operations is benchmarking (see Lehrman v. Gulf Oil Corp.,464 F.2d 26 (5th Cir. 1969). As the term suggests, benchmarking calculates likely anticipated earnings based on a relative comparison of the defunct business to a similar company in the same industry. Theoretically, a company that is comparable in size, location, management, product lines, and market position could experience the same approximate earnings stream. Earnings for a similar company can be used as a proxy for earnings of the defunct business provided that relevant factors are identified and determined roughly equivalent.

Although benchmarking makes intuitive sense, it can be difficult to implement. In practice, no two companies are equivalent, even in general terms. Differences in just one of the variables in the following box can make a tremendous difference in performance between two otherwise similar firms. For example, two publishing companies in the same city with similarly sized staffs may have vastly different earnings potential simply because they market their services to different clients.

Another potential difficulty with using benchmarking as a means for estimating lost earnings lies in the availability of information. Because of regulatory requirements, publicly traded companies must make selected financial and accounting information available to stakeholders and potential investors. Thus, benchmarking can usually be used on a general level for publicly traded companies. However, comparison of privately held and nonregulated companies becomes more difficult simply because information cannot be readily obtained.

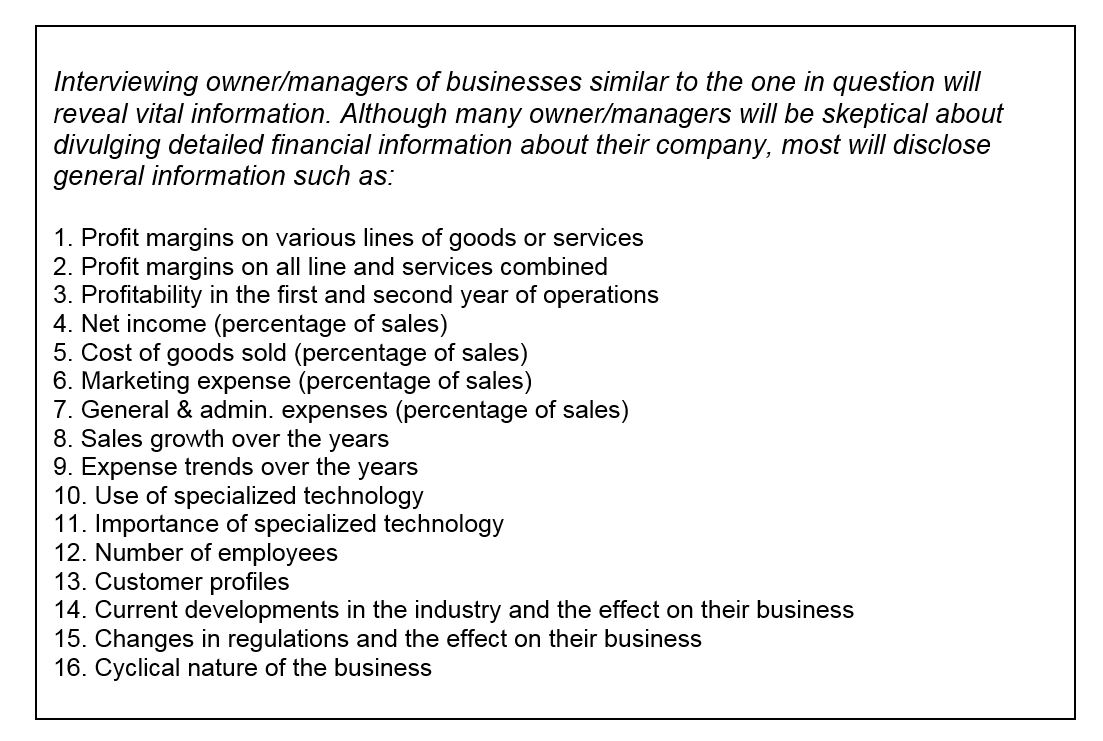

An effective method of overcoming the limitations in the availability of detailed information for privately held or nonregulated companies is through the use of interviews.