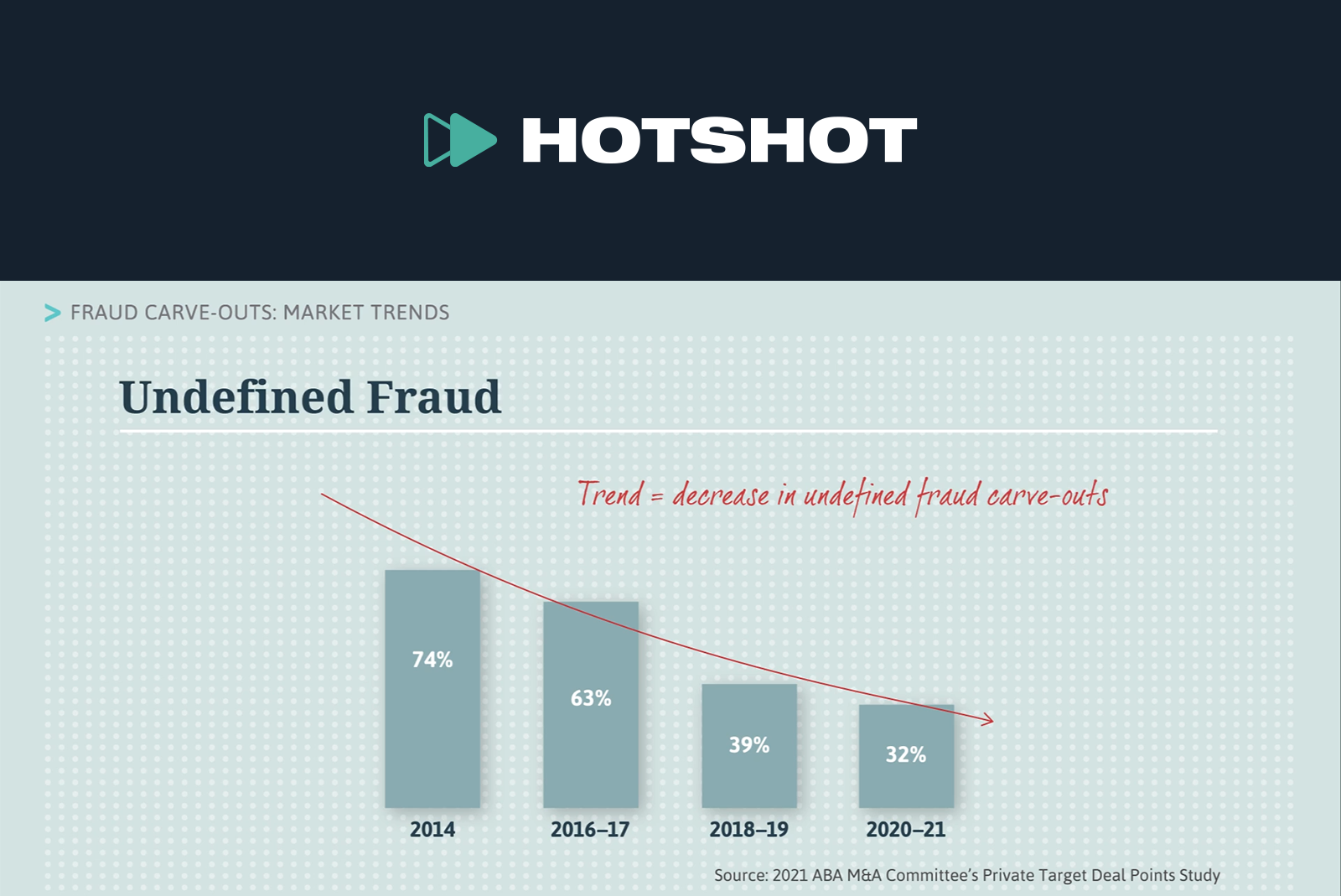

Canada’s M&A activity is poised at the crossroads of anticipation and opportunity as we step into 2024. Reflecting on both recent trends that have shaped the Canadian legal landscape and predicted ones, it’s clear that a sense of cautious optimism pervades discussions about the future.

In this article, we delve into the anticipated trends in Canada’s M&A landscape for 2024. Through a pragmatic lens, we explore key factors shaping the M&A environment, ranging from considerations like interest rates and inflation to the evolving dynamics of private credit and the increasing international interest in Canadian renewable energy.

Increased Confidence Surrounding Interest Rates and Inflation

In the evolving landscape of Canadian M&A in 2024, a critical factor influencing dealmaking will be the projected stabilization of interest rates and inflation. Some buyers may remain cautious, evaluating economic conditions, while others, stimulated by the “new normal” of higher interest rates, may boldly charge forward with M&A activity.

The Bank of Canada and the US Federal Reserve have each hinted at interest rate cuts in 2024. Though the timing is unclear, the reduced concerns about ongoing inflation and rate increases may drive market activity.

Distressed Acquisition Opportunities

The aftermath of government support during the post-COVID-19 era, coupled with the impact of high interest rates, has created a landscape ripe with distressed acquisition opportunities and restructuring potential. Limited liquidity and inflated valuations will compel organizations to evaluate strategic alternatives, leading to an expected uptick in distressed M&A activities. In 2024, well-capitalized companies are anticipated to be well poised to engage in strategic acquisition transactions at discounted prices.

Less Frenzied M&A Market

A notable shift in the M&A landscape for 2024 is the anticipation of a less frenzied market characterized by greater parity among buyers and sellers. The days of rushed transactions may give way to a more deliberate approach, with extended negotiation periods and in-depth due diligence becoming the norm. Both buyers and sellers are expected to exercise heightened caution, leading to more balanced and nuanced deal terms, including the continued prevalence of earn-out structures. This shift towards a measured M&A environment emphasizes the importance of thorough assessments and collaborative negotiations in achieving mutually beneficial outcomes.

The delicate balance between risk and reward will bring dealmakers back to the negotiating table, fostering a climate where astute decision-making becomes paramount. Within this context, we are cautiously optimistic that we will see continued deal activity in 2024, with stakeholders keenly assessing the impact of the economic factors discussed above on transaction dynamics.

Increased Availability and Use of Private Sources of Funds

In response to the evolving financial landscape, a notable trend on the horizon is the increased use of private credit to finance purchase prices. The significant increase in borrowing costs, not wholly offset by decreased valuations for targets, means that traditional banks constrained by regulatory frameworks and risk appetites may be unable or unwilling to provide the capital required for M&A transactions. Consequently, private credit has become an attractive alternative source of capital. Dealmakers are expected to increasingly turn to private credit instruments and innovative financial solutions in 2024. Borrowers are also likely to leverage their existing lending relationships, as banks and other lenders will be more willing to deploy their capital to borrowers with whom they have established a history.

Regulatory Scrutiny

A growing consensus among competition regulators and policymakers suggests that many markets have become less competitive, necessitating heightened merger enforcement. In 2024, regulatory bodies are expected to intensify their examination of foreign investment transactions and strategic combinations.

Proposed changes to the Competition Act aim to strengthen the Competition Bureau’s enforcement powers, penalties, and sanctions. These changes subject more mergers to notification and approval requirements, lowering the bar for the Bureau to challenge transactions. The result is regulatory uncertainty and increased costs. Such considerations lessen the attraction for some companies seeking to engage in Canadian business deals.

Attention on ESG and Canadian Renewable Energy

Canada’s renewable energy sector is poised to attract heightened international interest in 2024. As global initiatives focus on sustainable practices, Canadian projects present attractive investment opportunities. The confluence of Canada’s commitment to ESG, including renewable energy targets, and the international appetite for green investments positions the country as a key player in the global energy transition. For investors looking to take advantage of more readily available capital, projects involving clean energy innovation will be an attractive option, given the Canadian federal budget and provincial measures being used to entice investment. Investors and dealmakers alike are expected to explore partnerships and acquisitions within the Canadian renewable energy landscape, contributing to the sector’s growth and fostering international collaboration.

With this said, it is growing increasingly important that parties to M&A transactions carefully evaluate and structure their deals with ESG considerations top of mind, ensuring that a clear narrative, targets, and performance indicators are employed. This is especially true for larger public or multinational companies, given the rising pressure from investors and stakeholders to prioritize ESG considerations.

Conclusion

The landscape of Canadian M&A in 2024 is characterized by opportunity—to create value through creative financing, strategic acquisitions, and carefully considered deal terms and structures. As we anticipate the stabilization of interest rates and inflation, the surge in private credit, international interest in Canadian renewable energy, distressed acquisition opportunities, increased regulatory scrutiny, and a less frenzied M&A market, strategic and well-informed dealmakers and their legal representatives are poised to capitalize on the evolving M&A terrain.

The trends forecast for 2024 underscore the importance of strategic foresight, adaptability, and a nuanced understanding of the intricacies inherent in each transaction. As the legal landscape responds to economic shifts and global imperatives, dealmakers can leverage this knowledge to navigate M&A scenarios with confidence and clarity.