Delivering on the promises of the rule of law has been and will continue to be a great challenge during the COVID-19 pandemic and in its aftermath. As the world struggles to adapt to the evolving immediate consequences of this public health crisis, lawyers should be mindful of long-term consequences when providing legal advice and representation. This requires reflection on previous crises, a willingness to learn from the current pandemic, and use of acquired knowledge to navigate and prepare for comparable disruptions in the future. Business lawyers in particular should gain an understanding of how the pandemic affects their clients, the courts in which claims are brought by and against their clients, and the impact it has on lawyers in general.

Impact on Middle Market and Small Businesses

The rapidly evolving COVID-19 pandemic disrupted the economy at a global level. Small businesses took the hardest hit. As businesses reopen to the public, social distancing restrictions and demand shifts are expected to shutter many more small businesses. Virtually every business is forced to confront a host of hard questions about how to survive and conduct business in the midst of the pandemic.

In response, the government, at different levels, implemented various relief programs, such as the Paycheck Protection Program (“PPP”), to address some of the hardships created by this unprecedented pandemic. The PPP did not accomplish its stated goal for many small businesses due to its complexity and accompanying uncertainty around the forgiveness process. Small businesses may not have the financial resources to learn and keep up with the quick-changing rules of the PPP program. As the pandemic continues to evolve, businesses face new business and legal challenges. Merely creating new relief programs for small businesses is not enough. Business owners need to understand what the programs offer and how to navigate and access such programs. Pro bono legal aid services remain a key solution to this ongoing problem.

Impact on Courts

Additionally, the pandemic poses significant challenges—and opportunities—for increasing access to justice. The federal and state judiciary systems have been forced to operate in unprecedented ways to maintain essential services. In many jurisdictions, physical access to the courts has been curtailed or suspended completely, making it difficult for individuals to seek legal assistance. Courts now routinely use telephonic and videoconferencing services to move dockets forward and will continue to adjust and implement new procedures and technology as the crisis evolves. There is still uncertainty, however, about whether such measures can (1) effectively substitute for in person proceedings long-term or (2) increase or decrease access to justice.

Impact on Lawyers and Law Firms

Cases and deals are being delayed, causing law firms to make tough decisions. In hopes of withstanding the devastation brought by the pandemic, law firms have made pay cuts and layoffs, shortened summer programs, and delayed start dates for incoming associates. Despite the added stress these decisions cause, lawyers have been forced to step up and develop creative solutions for clients’ demands during these unprecedented times. Most of these solutions rely on innovative technology to meet the requirements of clients and their businesses. However, this creativity does not come without risk. Lawyers must be certain to maintain their ethical obligations, including maintaining confidentiality, professionalism, and competence. These obligations are increasingly difficult to meet given the new challenges that stay-at-home orders bring. Parents may be distracted by the responsibility to teach and care for their children, while roommates may struggle to maintain client confidentiality in their close living quarters. These new stressors add to the already demanding requirements of the legal profession, where mental illness is seen in large numbers. Lawyers should be mindful of these consequences and take steps to ensure both their physical and mental health.

Lessons from the Pandemic

There are lessons we can learn that are not new but do require more attention during times such as this pandemic.

It is necessary to make plans and decisions, but when events are rapidly evolving, it is helpful to think of plans as working hypotheses rather than as final decisions.

There is added value in flexible policies and procedures.

It is important to be aware of and take steps to mitigate cognitive bias.

Quantification is a double-edged sword, to be used carefully.

Clear and prompt communication makes a difference.

As you make changes, it is helpful to identify what intangible benefits you might be losing and how important they are (or are not) and decide whether you want to try to mitigate the loss.

Pro bono legal representation is a way to make a meaningful difference in someone’s life.

Conclusion

Maintaining an understanding of our clients, courts, and ourselves will help foster innovative ideas and practical solutions to clients’ evolving demands. It is important to be flexible and open to change, particularly during the COVID-19 pandemic when the world and its laws are changing every day. Although we have limited access to each other due to social distancing requirements, we must be cognizant of the new norm and ensure that we are doing our part to increase access to justice during this global health crisis.

“Do not get lost in a sea of despair. Be hopeful, be optimistic. Our struggle is not the struggle of a day, a week, a month, or a year, it is the struggle of a lifetime. Never, ever be afraid to make some noise and get in good trouble, necessary trouble.”

-John Robert Lewis

On September 23, 2020, an esteemed panel discussed how the COVID-19 pandemic is exposing and exacerbating existing social and economic inequalities affecting racial and ethnic minority groups in America, including higher infection and death rates, decreased access to adequate healthcare, increased educational achievement gaps, and higher rates of job losses. This panel included Chris Brummer, Professor and Faculty Director of the Institute of International Economics Law at Georgetown Law; Dave Clunie, Executive Director at Black Economic Alliance; Patrice Ficklin, Fair Lending Director at the U.S. Consumer Financial Protection Bureau; Jenn Jones, Chief of Membership & Policy at the National Consumer Reinvestment Coalition; Robin Nunn, Partner at Morgan, Lewis & Bockius LLP; Anthony Sharett, EVP, Chief Legal and Compliance Officer, and Corporate Secretary at Meta Financial Group and MetaBank; and Odette Williamson, Director of the National Consumer Law Center’s Racial Justice & Equal Economic Opportunity Initiative. ABA Business Law Section members can watch the panel for free CLE credit here.

The confluence of the current global health emergency, the economic crisis, and the Black Lives Matter protests has underscored the major inequalities that persist today. The demonstrably unjust treatment of Black and brown communities has shown Americans that insufficient progress has been made since the civil rights movement. The recent passing of two civil rights icons—Congressman John Lewis and Rev. C.T. Vivian—has caused many of us to reflect on the magnitude of their accomplishments and how much more there is to be done.

This country’s well-documented history of exclusionary policies has infected every sphere of our lives, legitimizing racism and creating structural barriers to equity. For instance, residential redlining, which was promoted by the Federal Housing Administration’s official policies, has led to persistent residential segregation. The implications of segregation are devastating and self-reinforcing: less access to good jobs, greater concentration of poverty and crime, underfunded public schools, lower levels of homeownership, poor housing quality, and increased risk of illness or death.

The ramifications of institutionalized racism and segregation returned to the headlines as COVID-19 has taken a disproportionate toll on minorities. As of the date of this article’s composition, there have been 6,343,62 confirmed cases of COVID-19 with 190,262 deaths in the United States.[1] According to the U.S. Centers for Disease Control and Prevention, there is increasing evidence that minority groups are disproportionately affected by the pandemic. While the fatality rate among white Americans rose only 9%, the fatality rate among Asian Americans, Black Americans, and Hispanics rose 30%, and the fatality rate of Native Americans rose more than 20%.[2] Financially, the pandemic’s toll may prove insurmountable for many minority families and communities. The ever-expanding wealth gap will impact Black families most as they have significantly less wealth to help protect them from the devastating effects of an economic crisis, let alone the ability to pass assets down to future generations. Due to the compounding effects of society’s treatment of our Black communities, “the median wealth for Black families in 2016 was an astonishing $3,557—about 2% of the median wealth owned by white families, which owned nearly $147,000 in the same year.”[3]

The stubborn persistence of these inequities requires renewed efforts and commitment. Our panel will discuss the role of existing legislation and what more can be done. The current legal landscape includes the Civil Rights Act, which sought to end segregation in public places, banned employment discrimination on the basis of race, color, religion, sex or national origin,[4] and became the archetype legislation for subsequent anti-discrimination laws that now permeate the financial landscape; the Fair Housing Act, which prohibits discrimination in the sale, rental, and financing of dwellings because of race, color, religion, sex, familial status, national origin, and disability;[5] the Equal Credit Opportunity Act, which prohibits credit discrimination on the basis of race, color, religion, national origin, sex, marital status, age, or for receiving public assistance;[6] and the Community Reinvestment Act, which requires federal financial supervisory agencies to encourage financial institutions to help meet the credit needs of the communities in which they do business, including low- and moderate-income neighborhoods.[7]

Also at play is the United States Department of Housing and Urban Development’s (“HUD”) new rule addressing disparate impact. In August 2019, HUD published a Proposed Rule seeking to amend the agency’s interpretation of the Fair Housing Act’s disparate impact standard. While HUD stated that the new rule was intended to better reflect the Supreme Court’s 2015 ruling in Texas Department of Housing and Community Affairs v. Inclusive Communities Project, Inc.,[8] many business executives, civil rights groups, and legal practitioners believe that the proposed rule is a step backwards, making it more difficult for plaintiffs to prove unintentional discrimination. Despite this opposition, HUD finalized the new disparate impact rule on September 4, 2020.[9]

The disparities are abundantly clear, and now is time to recommit to social justice and do more.

This article is the result of the authors’ independent research and does not necessarily represent the views of the Consumer Financial Protection Bureau, the Federal Reserve Board of Governors, the United States, or Simmonds & Narita LLP

[1]WHO Coronavirus Disease (COVID-19) Dashboard, World Health Org., https://covid19.who.int/region/amro/country/us (last visited Sept. 11, 2020).

[2]As U.S. Deaths Mount, Virus Takes Outsize Toll on Minorities, Associated Press, https://www.modernhealthcare.com/safety-quality/us-deaths-mount-virus-takes-outsize-toll-minorities (last visited Aug. 27, 2020) (compared with an average over the last five years).

[3] Alissa Kline, How Banks Aim to Close Racial Wealth Gap: More Minorities in Leadership, Am. Banker, Jul. 12, 2020, https://www.americanbanker.com/news/how-banks-aim-to-close-racial-wealth-gap-more-minorities-in-leadership.

Interested in this article? Consider attending these upcoming events at the ABA Business Law Section Virtual Section Annual Meeting, Monday, Sept. 21–Friday, Sept 25 (Information and Registration HERE.)

·Legal Analytics Program: Measuring Outside Counsel by the Numbers, Thursday, September 24, 9:00AM–10:30AM

·Legal Analytics Committee Meeting, Friday, September 25, 9:00AM–11:00AM CST

Did you know that you can make money investing in other people’s lawsuits?

Over the last decade, alternative litigation finance (ALF)[1]—the “funding of litigation activities by entities other than the parties themselves”—has taken off in the United States, with capital pouring in from “income-starved” investors seeking strong returns largely uncorrelated to public markets.

Despite ALF’s growth and institutionalization, for some, the space remains controversial. Detractors like the U.S. Chamber Institute for Legal Reform argue that it “increases the probability that meritless claims will be brought.” Supporters counter that investors have zero incentive to finance spurious cases and, to the contrary, can provide an important market-sorting function by allocating funds to resource-constrained parties’ meritorious claims while eschewing unviable matters.

In a sense, ALF hits on a core tension underlying our legal system. From a normative perspective, litigation is a system to right wrongs and promote fairness. Yet, descriptively, it is also a vast industry characterized by complex incentives and well-resourced “repeat players,” creating a dynamic that can exacerbate structural inequities.

For lawyers, ALF presents unique challenges implicating both professional responsibilities as well as practical commercial considerations. To help provide guidance, on August 4, 2020, the ABA’s House of Delegates adopted the American Bar Association Best Practices for Third-Party Litigation Funding (Best Practices). The report “surveys the types of alternative litigation funding and proposes best practices to be consulted and factors to be considered by attorneys seeking to explore or utilize litigation funding in dynamic regulatory, judicial, and arbitral environments.”

What Is Alternative Litigation Finance?

The Best Practices report notes that “[a] single narrow definition . . . cannot encompass the range of funding activities that may arise” with respect to ALF, but at its core it “is a form of distributing risk.” In that regard, ALF is not unlike contingent-fee arrangements, which for many plaintiffs represents the primary alternative for pursuing claims.

In 1897, Oliver Wendell Holmes wrote that “[w]hen we study law we are not studying a mystery but a well-known profession. . . . The object of our study, then, is prediction.” In finance terms, this implies that litigation, and thus ALF, is not a matter of Knightian uncertainty (suggesting unquantifiable outcomes) but is fundamentally subject to risk (a set of unknown, but ultimately calculable, outcomes).

Indeed, commercial clients typically come to lawyers with questions best answered in the form of a number: How much can we win (or lose)? What are the odds? How long will it take?

Legal analytics provides the tools for answering such questions, whereas litigation finance offers a vehicle for transferring the now-quantified legal risk to the parties best suited to bear it. Unsurprisingly, the Artificial Lawyer has observed at least four partnerships between legal prediction startups and litigation funders.

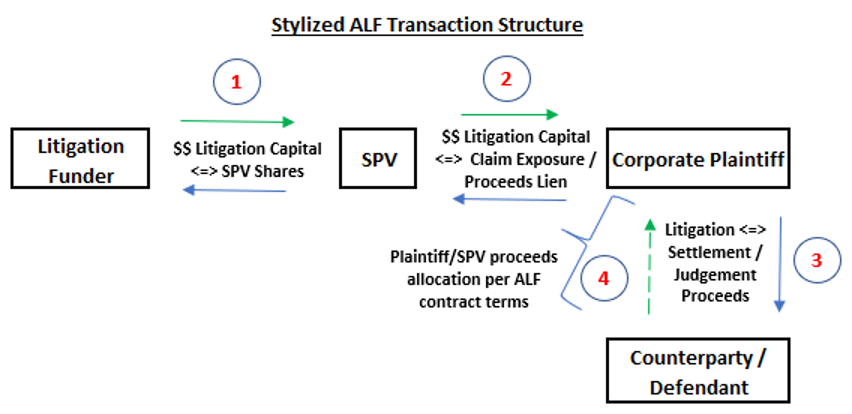

ALF transaction structures are complex and vary widely, though the core approach is transferring financial exposure to legal risk while minimizing basis and ensuring strict adherence to the rules of professional responsibility in respect of case control and otherwise.

The diagram below presents a simplified example of an ALF deal structure:

The transaction above basically works as follows: (1) a newly created special purpose vehicle (SPV) sells shares to an ALF firm; (2) the SPV uses the capital to purchase exposure to a company’s legal claims (effectively taking them off the cedant’s balance sheet) in exchange for a security interest in the proceeds; (3) using capital from the SPV, the company pursues the litigation; and (4) if successful, the company and ALF firm share in any eventual recovery.

Computationally, though at a highly simplified level, one could think of the expected value of a litigation claim as:

E [Vclaim] ~ = [(p*A) – C] / (1+r)T

where “p” is the probability of an award or settlement, “A” is the amount, “C” is the cost of litigation, “T” is the expected duration, and “r” is the applicable discount rate.

ALF Market

The Best Practices report provides a broad survey of the ALF market, finding that in recent years “[t]he frequency of funding, the diversity of types of funding, and the number of funders have increased,” along with the capital dedicated to the space. Further, “[p]erhaps most importantly, the forms of dispute financing have expanded significantly, raising challenging questions about how ‘third-party funder’ or ‘third-party funding’ should be defined,” as an International Council for Commercial Arbitration report noted.

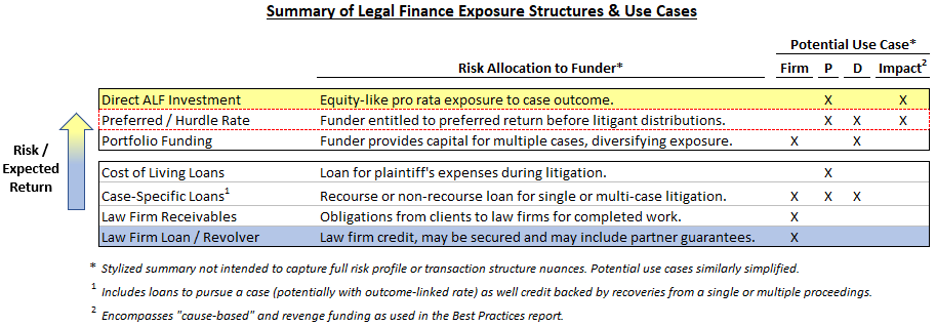

The diagram below summarizes the different ALF types discussed in the Best Practices report through a taxonomy based on the structure of the litigation funder’s financial exposure to the underlying legal risk:

Broadly, the funding types can be grouped between those offering direct exposure to case outcomes and litigation-related credit, where the funder does not necessarily share in the upside, but may have some floor on their exposure through recourse, collateral, or guarantees, such as with respect to law firm loans.

Importantly, first category of outcomes-tied ALF represents the vast majority of the market. At the same time, based on conversations with market participants, the “preferred or hurdle rate” structure, denoted by the red-dotted box, is the most common return structure in the market today.

The key distinction in the above framework is not the use of funds, which are innately litigation related, but the nature of the capital provider’s exposure to the underlying legal asset and potential corresponding implications in respect of case control and the parties’ broader incentives.

ALF Returns and Performance

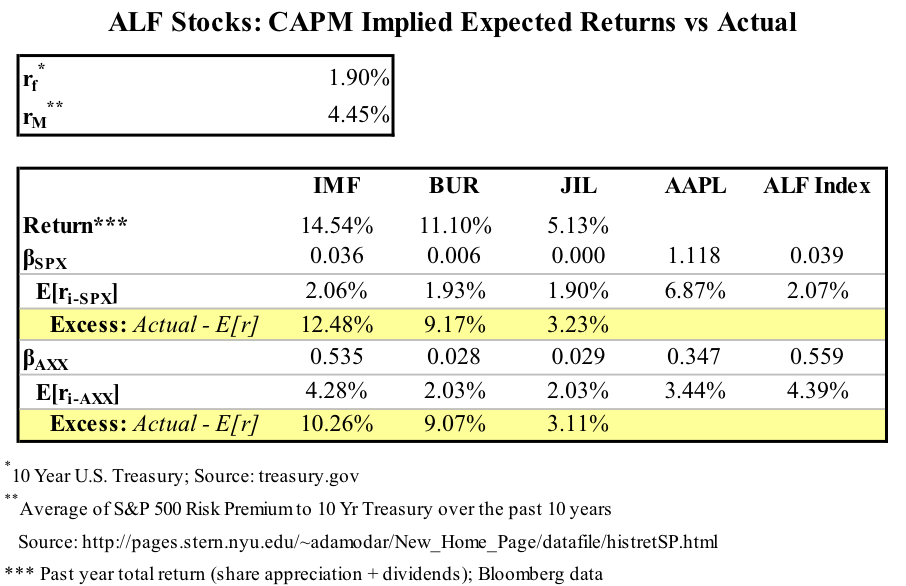

Based on performance figures, it is not difficult to see why ALF is “booming,” as Businessweek put it. Many ALF funds have reported net internal rates of return exceeding 30 percent, whereas some players, like IMF Bentham (rebranded as Omni Bridgeway), have delivered closer to 60 percent, according to a Bloomberg report. Furthermore, ALF is commonly understood to be largely uncorrelated to broader public markets, making it even more attractive from a portfolio construction perspective.

Unfortunately, due to ALF transactions being both private and generally highly illiquid, it is next to impossible to perfectly capture this dynamic empirically. With that caveat, the table below presents one—admittedly, imperfect—approach based on market prices through 2016 for publicly-listed ALF vehicles: Burford, IMF Bentham (Omni Bridgeway) and Juridica. As shown below, the Beta, or level of market exposure against the S&P 500—typically around 1 for most companies and 1.118 for Apple as shown below—is near 0 for the ALF funds.

Consequently, all three ALF firms displayed significant excess returns relative to predictions based on the CAPM model.

Report Recommendations

In part due to ALF’s complexity, the Best Practices report does “not take a position on a number of litigation funding issues” and generally eschews a prescriptive posture. Rather, the report seeks to provide certain broad-based principles “common to all types of funding.” These principles emphasize thorough documentation of the funding arrangement, as well as adherence to the Model Rules of Professional Responsibility—namely, ensuring “that the client remains in control of the case.”

Some of its key takeaways are as follows:

Any litigation funding arrangement should be in writing.

The litigation funding arrangement should assure that the client remains in control of the case.

The written document should address what happens to the funding arrangement if, down the road, the client and the funder disagree on litigation strategy or goals.

Given that the propriety and the discoverability of litigation funding arrangements are unsettled questions in many jurisdictions (and may differ across contexts within those jurisdictions), (emphasis added).

Discoverability of ALF arrangements has presented a particular point of contention and uncertainty in that “[c]ourts currently are of differing views on whether the fact of third-party funding and the details need to be disclosed to the other side or are proper issues for discovery.” Thus, the report “identifies these issues but does not take a position on whether such disclosure should occur,” although it warns attorneys of the possibility and advises that they plan accordingly.

[1] ALF is also commonly referred to as “legal funding,” “third-party litigation finance,” and certain other terms. For relative simplicity and consistency with the Best Practices report, this article uses the ALF acronym.

Since June 5, 2019, the date on which the Securities and Exchange Commission (the SEC) published its interpretation regarding the standard of conduct for investment advisers under the Advisers Act[1] the world has changed dramatically. On February 3, 2020, Larry Fink, the Founder, Chairman, and CEO of BlackRock Inc., published his open letter to CEOs asserting that climate change “has become a defining factor in companies’ long-term prospects”.[2] The World Health Organization declared COVID-19 as a pandemic on March 11, 2020. The Black Lives Matter movement has gained increased prominence following the death of George Floyd in Minneapolis on May 25, 2020.

The managers of many investment funds have made representations or covenants with respect to the incorporation of environmental, social and governance principles in their investment decisions. Prior to the COVID-19 pandemic, in the context of ESG, the investment community was focused on climate change, as evidenced in part by Larry Fink’s letter.[3] However, since the start of the current pandemic, that focus has shifted, at least temporarily.[4] The “S” in “ESG” appears to have gained more prominence than the “E” or the “G”.[5]

Registered advisers are fiduciaries under U.S. federal law and owe a duty of care and a duty of loyalty to their clients.[6] The SEC has stated that this fiduciary duty requires an adviser “to adopt the principal’s goals, objectives, or ends”[7] and that an adviser’s duty “follows the contours of the relationship between the adviser and its client, and the adviser and its client may shape that relationship by agreement, provided that there is full and fair disclosure and informed consent.”[8]

Investment fund managers may wish to take the following actions to address ESG in the time of COVID-19:

Review Scope of Existing Commitments. As investment fund managers monitor and evaluate their portfolios, they should review any side letters and the governing documents of the funds that they manage, including the limited partnership agreement and the private placement memorandum, to ensure that fund managers understand the scope and extent of their commitments and representations made to investors with respect to ESG.

Evaluate Effectiveness of Existing ESG Policies and Procedures. Investment fund managers that have made commitments with respect to ESG should evaluate the manner in which ESG principles are incorporated into investment decisions, the ongoing management of portfolio companies, and the management of the fund manager’s own business (such as the manner in which key employees are recruited and promoted, and the compensation of employees for sick days).

Adopt an ESG Policy. Investment fund managers that have not yet adopted an ESG policy may wish to consider doing so as a way of identifying and managing risks not addressed through their existing processes, thereby improving the fund’s ability to weather (and potentially thrive in) the COVID-19 storm. While conventional wisdom has pitted ESG considerations against healthy economic returns, the current pandemic has demonstrated that the two are not mutually exclusive. Funds that have already identified and addressed ESG risks, for example, may find that their portfolio companies are more resilient than those of their peers.[9]

Adjust the Investment Strategy. Managers of funds without the benefit of an investment strategy broad enough to include new types of attractive investment opportunities should consider amending the fund’s investment strategy (which would generally require investor consent) or forming a sidecar fund (which may also require investor consent, depending on the terms of the existing fund) for the purpose of pursuing those types of opportunities.

Fund managers that wish to pursue this approach should engage with investors early in the process to identify and address any concerns that investors may have with respect to style drift or potential conflicts of interest. Investors may want to know, for example, how conflicts will be managed if two different funds that are managed by the same manager could potentially invest in different parts of the capital stack of the same company.

Any fund manager that wishes to form a sidecar fund should be prepared to answer fresh new questions from investors about how the manager will address ESG risks: the investment strategy of the sidecar fund could raise materially different ESG considerations—and result in a materially different risk profile—than that of the existing fund.

These actions will not necessarily ensure the success of an investment fund or result in top-quartile returns. There are sure to be investment funds that are unable to rebound from their losses or that are ultimately unable to produce the returns expected by their investors as a result of the current pandemic. However, at a time when health, safety, and stability are of paramount concern to many institutional investors, among others, an investment fund manager that chooses to disregard its own ESG commitments, or disregard ESG considerations more generally, does so at its own peril.

[5] See, for example, “Investor Statement on Coronavirus Response”, a statement released by over 300 institutional investors which urges the business community to consider providing paid leave, prioritizing health and safety and maintaining employment, among other things: “the prospect of widespread unemployment will exacerbate the crisis and grave risks to basic social stability and the financial markets”.

[6]Interpretation, supra note 1 at 6-7, citing Amendments to Form ADV, Investment Advisers Act Release No. 3060 (July 28, 2010) and Proxy Voting By Investment Advisors, Investment Advisers Act Release No. 2106 (Jan. 31, 2003).

Almost three years ago, the ABA Business Law Section launched businesslawtoday.org, the Section’s premier digital platform for timely content on business law topics. The launch culminated a two-year project, in which I was part of a task force assigned to “reimagine” the Section’s longstanding print magazine, led by indefatigable former Section chair Chris Rockers. Our project ultimately resulted in a complete overhaul of how the Section sources, distributes, features, and promotes articles and other content from across the Section’s committees, and thanks to the leadership of Chris and the hard work of the other members of the task force, we were able to launch an entirely new BLT website in the late fall of 2017. This is my look back at that project and my tenure as BLT Editor-in-Chief, along with some highlights of how BLT may develop further after I hand the job over to new Editor-in-Chief Lisa Stark this September.

Reimagining… Content Distribution and Organization

Part of the goal in shifting to a web-based format was to bring more content to members more frequently and in new formats. Based on market research and member surveys, we decided to focus on providing shorter articles and topical month-in-brief-pieces that could be edited and posted to the site quickly. And we wanted to do this with a fresh look and feel in an easily navigable format, with plenty of links to related relevant content but without too much clutter. With the help of outside designers and strategy consultants hired for the “Reimagine BLT” project, we tried to focus on members’ user experience to make sure readers would easily find what they were looking for and would have plenty of reasons to frequently revisit the site.

When the site launched in November 2017, these were the key elements of the new BLT:

8 Practice Areas and 36 Topics.

Rather than organizing the site around the Section’s 52 substantive committees and relying on each of them to fill an allocated slot with content, we created 8 larger “Practice Areas.” These serve as general silos in which to gather written articles and other content that has some loose connection or logical relationship but not a uniform source. Each Practice Area is organized into 2 or more Topics, with a total of 36 topics across the website. With this content hierarchy, written pieces from many individual members and multiple committees might end up organized in the same section of the site, increasing the diversity of contributors and perspectives and offering an organizational scheme that is intuitive regardless of a reader’s familiarity with the Section’s committee structure.

Heightened Author Recognition.

We wanted to make sure the site would highlight its authors and their contributions in a way that would encourage members to continue to write for BLT and that would invite new authors to contribute. At the end of each article, the site features an author photo and the author’s bio (of whatever desired length) with links to his or her other articles and related content.

Month-in-Briefs—Short, Timely, Targeted.

Along with short, non-law-review-format articles on all of BLT’s topics, the site launched with its new “Month-in-Brief” pieces. These are very short and timely alerts about recent cases and legislation in each of the Practice Areas, and they are designed to make sure members always find something timely and useful on the site in each of the areas of law they follow.

In Front of the Paywall.

Another important decision made at launch: the website is accessible to all. You don’t have to log in as a Section member in order to access nearly all its content, apart from a handful of reprinted articles from the Section’s academic journal, The Business Lawyer. The purpose was to promote Section content to business law practitioners and others beyond our membership. And with nearly half of web traffic to the site coming from organic search (Google and other search engines) over the last year, it is very likely many new readers are seeing the written work of Business Law Section members through BLT.

In Living Color.

Not only did the site launch with a new logo, it added color, images, and design elements to BLT. We wanted to make sure the site was modern, fresh, and lively, and we think the images and design elements of the site add to a lively and engaging experience.

Reimagining… Content Elements

Right away we understood something our consultants warned us about: a good and useful website can’t be static—it will always need corrections, additions, and enhancements. BLT leadership has never been without a long and always-changing wish list of additional elements for the site, although we have realized some of our further goals for augmenting user experience and layering in more types of content. These include:

Video

In 2018 we began posting interviews of Section authors, speakers, and members recorded from a BLT stage area within the Section lounge at each BLS Spring and Annual meeting. These video interviews picked up where we left off with the old “Member Spotlight” series, composed of written interviews included periodically in the old BLT magazine. We expanded them to include “Author Spotlight” and “Program Spotlight” interviews, highlighting the work of the Section’s prolific authors and program chairs and speakers. Expect more of these interviews and new types of interviews in the months to come.

Business of Law

In 2019 we added a new top-level menu to the site, our new “Business of Law” practice area, with underlying topics Pro Bono, Diversity & Inclusion in the Profession, Professional Development, and Law Practice Management. Since the beginning, many Section members had asked for a place on BLT to post content in these areas, and we were happy to add a place for content that many Section committees and members have written about, and cared deeply about, for a long time.

Podcasts

Earlier in 2020 the Business Law Section launched its “To the Extent That…” podcast series, and we quickly made a place on BLT where all Section podcasts can be accessed. Look for more additions in the months to come.

Reimagining… Content Promotion and Marketing

We have also expanded the ways in which BLT can be used as a resource for coordinating, promoting, and advertising the Section’s content and the many webinars and events the Section produces. The home page features promotion of upcoming webinars, which are free for Section members, and the site also now features advertisements for Section books.

Moving into the 2020–2021 bar year, our readers can expect to discover more features and more opportunities to engage with the Business Law Section through BLT. We will offer more video content on the site, more access to podcasts and other audio content through the site, and more ways for our committees, sponsors, and advertisers to connect with our members.

…Even more than we imagined!

By this year’s Virtual Section Annual Meeting, Businesslawtoday.org will have reached important milestones: In the 2019–2020 bar year, we will have distributed more content than ever through BLT: around 175 articles, 350 month-in-briefs, and 20 video interviews went live on BLT.

With the high volume we have been able to maintain the high quality… but only because of the incredible efforts of our full time dedicated staff and our stellar lineup of incredible volunteers. Huge thanks, kudos, and much appreciation go out to the Business Section’s Content Guru (because he is o-so-much-more than a mere “content guy”) Rick Paszkiet, aka keeper-of-the-slush-pile, aka breakfaster-in-chief. Rick juggles dozens of book projects and brings record-setting numbers of them to the finish line, while keeping his eye on incoming article proposals and managing a deep pile of unsolicited and solicited submissions, from which pieces are periodically selected, tamed, edited, and posted to the site. Meanwhile, double kudos and millions of thanks to fulltime Section BLT editor par excellence, Sarah Claypoole, who has managed the editorial process across the site from day one in a way that looks seamless to the outside and keeps all the glitches, author mishaps, and editorial challenges at bay. And meanwhile, Sarah has developed an uncanny ability to understand and stay on top of the Section’s content creation process across a multitude of committees and personalities, for which she is a tremendous asset to BLT and the Section.

Thank you very much to our Executive and Managing editors who have continued to source our regular month-in-brief pieces… and for the many times you have simply written them yourselves, and to our regular contributors and Contributing Editors. Your work to source, write, edit and simply turn over month-in-brief pieces along with a slew of stellar articles are what makes this site actually work.

As I complete my term as Editor-in-Chief of Business Law Today, I couldn’t be more confident about the coming transition. As of the Business Law Section’s Virtual Section Annual Meeting this September, my vice-editor-in-chief, Lisa Stark, takes over the Editor-in-Chief role. Lisa is an experienced M&A, corporate, and securities lawyer partner with K&L Gates in Wilmington DE, and she is a co-chair of the Jurisprudence Subcommittee of the Private Equity & Venture Capital Committee of the Business Section. Lisa has been a steadfast and indefatigable vice chair and has personally contributed much private equity, partnerships and M&A content to BLT. Thank you, Lisa, for your tremendous contributions to date, and congrats and good luck as you steer things forward.

The mail is slowing down. Packages and letters that used to arrive in days are in some cases taking weeks. Data suggests that since the beginning of July, on-time rates for delivery of first-class mail has slipped by 10–30 percent depending on the area and region. Although much of the focus of the media’s coverage concerning these delays has centered around the upcoming 2020 election and questions surrounding funding for the United States Postal Service (USPS), such delays can create serious issues concerning parties’ commercial agreements. Despite the fact that unquestionably more and more transactions are completed through the exchange of scanned and emailed documents, mailing requirements in contractual agreements are still common and remain a part of how business gets done. Many attorneys may not have thought about the “mailbox rule” since their contracts class in law school, so it is worth reexamining during this period of postal uncertainty.

The Mailbox Rule

The mailbox rule is a common-law concept of contract law that governs the time at which an offer is considered accepted. Section 63 of the Restatement (Second) of Contracts provides that “[u]nless the offer provides otherwise, . . . an acceptance made in a manner and by a medium invited by an offer is operative and completes the manifestation of mutual assent as soon as put out of the offeree’s possession, without regard to whether it ever reaches the offeror . . . .” In other words, an offer is accepted the moment it is placed in the mail. The rule notably excludes option contracts by stipulating “an acceptance under an option contract is not operative until received by the offeror.” Further, although an offer may be revoked at any time prior to acceptance, revocation is typically effective only at the time of receipt, whereas an acceptance is effective upon dispatch.[1]

Issues That May Arise

The Buchbinder Tunick & Co. v. Manhattan Nat’l Life Ins. Co. matter out of New York provides an interesting example of the legal and factual issues that can be at play concerning mailings. The case involved whether an 80-year-old insured in failing health, after falling behind on his insurance payments, timely mailed premium payments to extend his life insurance despite the insurance carrier’s notice of cancelation.

On August 28, Manhattan National Life Insurance Company sent Mr. Buchbinder a letter that it would go on to claim was a reminder that unless he sent payment by August 31, his life insurance policy would be canceled. However, the court rejected the claim that the letter was a reminder based on ambiguous language in the letter that could have been read to extend Mr. Buchbinder’s time to pay for 31 days based off the standard mailing time between New York and Ohio. The court reasoned that because the expected mailing time of the August 28th letter was five days, the letter could not have been intended as a reminder because it would not have been received by the insured until after expiration of his time to make the payment. Accordingly, the court determined the letter was in fact an offer to provide the insured additional time to keep his insurance by making a payment within the next 31 days.

However, after the offer letter, the insurance company’s system autogenerated an additional letter on September 17 canceling the insureds policy for nonpayment. Although the court found that the September 17 letter qualified as a revocation of the prior August 28 offer, on September 24 the insured mailed his premium check, thus accepting the August 28 offer under the mailbox rule. Without a clear answer in the record, the case was remanded to the trial court to answer the factual question of whether the insured received the insurance company’s September 17 revocation, which unlike acceptance of an offer, became effective only upon receipt.

Accordingly, whether the carrier was able to cancel coverage would turn on whether the carrier could prove when it mailed the revocation and, more importantly, when it was received by the insured. Although what ultimately occurred to Mr. Buchbinder’s policy does not appear available in the public record, it is easy to see the uphill battle the insurer would have if this played out in today’s climate. With reports suggesting that as much as 30 percent of first-class mail is delayed, a party may be able to present a compelling case against presuming standard delivery times and that delivery was made by a certain date.

Although things have probably not yet reached a point where courts will bring into question the longstanding doctrine of presumption of regularity, which requires a court to presume a letter or notice that is mailed is received by the addressee, such presumption may become open to attack if conditions worsen. In Republic of Sudan v. Harrison[2], the U.S. Supreme Court found that mail must be sent to a foreign minister’s office in his home country, not the embassy on U.S. soil, to be effective. The Court relied on section 66 of the Restatement (Second) of Contracts, which lays out the standards to ensure that acceptance is actually made upon dispatch. Outside of the “properly addressed” requirement relied on by the Court, section 66 offers insight into “other precautions” that may be relevant in light of recent concerns with the management of USPS:

The other precautions to be taken depend on what is ordinarily observed to insure safe transmission of similar messages. In cases of acceptance by mail, the postal regulations are ordinarily controlling on such matters as the necessity for prepayment of postage. In unusual circumstances, however, as when the mails are stopped by war, reasonable diligence may require more than compliance with postal regulations. Unless the offeror manifests a contrary intention, an acceptance is not effective on dispatch if the offeree knows or has reason to know that it will not reach the offeror.

Accordingly, if the trend of issues with the USPS continues or worsens, arguments may become available that current issues amount to “unusual circumstances” where mailing alone is inadequate.

What To Do?

Although the first answer that comes to mind is to not use the USPS, it is important for businesses to check the specific language in any contract to determine whether a specific method of delivery is required. This is particularly true in the case of insurance agreements, leases, and mortgage contracts, which often contain antiquated boilerplate language. These provisions must be strictly complied with because courts still regularly hold that delivery and notice provisions must be followed in accordance with the specific terms of the agreement.[3]

With that said, there are still some simple steps parties can take to protect themselves:

Review your agreements and ensure you understand any method of transmission requirements.

Where the agreement provides for methods beyond the USPS, use those methods.

Document your mailings: if you are mailing a document that must be sent by first-class mail, additionally send an email providing a copy of the document and memorializing that it was mailed that day.

Avoid sending offers and revocations that are not effective until receipt by mail and instead use means of instant communication where available.

Ensure new agreements do not limit the means of notice to the USPS and modify existing agreements to allow for alternative means.

Expect delays in receiving mailed materials and do not take adverse action until a reasonable time has passed.

Until the issues with the USPS are resolved, attorneys and businesses should take extra precautions to ensure they are protected.

[1]See e.g., Buchbinder Tunick & Co. v. Manhattan Nat’l Life Ins. Co., 219 A.D.2d 463, 466 (1st Dep’t 1995).

[2] Republic of Sudan v. Harrison, 139 S. Ct. 1048, 1057 (2019)

[3]See e.g., JPMorgan Chase Bank, Nat’l Ass’n v. Nellis, 122 N.Y.S.3d 673 (2d Dep’t 2020) (“The plaintiff similarly failed to establish, prima facie, that it mailed a notice of default to the defendant by first-class mail as required by the terms of the mortgage as a condition precedent to acceleration of the loan.”).

The Small Business Reorganization Act of 2019 (SBRA),[1] effective February 19, 2020, has created timely opportunities for individuals to confirm a Chapter 11 plan. Prior to the enactment of this legislation, individuals who did not qualify for Chapter 13, generally because their debts exceeded statutory limits, were forced to use the business reorganization provisions in Chapter 11. These provisions subjected individuals to the cramdown requirements of the absolute priority rule and made it difficult for individual debtors to confirm a Chapter 11 plan of reorganization. Thankfully, however, mere months before the COVID-19 pandemic, Congress passed the SBRA and eliminated the absolute priority rule for qualifying small businesses, which can include individuals.

The absolute priority rule was derived under Chapter X of the Chandler Act, which was the predecessor to the Bankruptcy Code enacted in 1978.[2] Under the Bankruptcy Code, the absolute priority rule generally applies when a class of unsecured creditors did not vote in favor of the plan treatment (cramdown) and required the debtor to pay in full the allowed unsecured claims of the rejecting class if any junior interests, such as equity holders, were retaining their interest.[3] In the case of an individual, the Supreme Court held in Norwest Bank Worthington v. Ahlers[4] that the individual debtor should be regarded as an equity class, junior to unsecured creditors. This made it extremely difficult for an individual to confirm a Chapter 11 plan unless the creditors consented or the creditors were receiving full payment. Alternatively, the debtor could perhaps propose a new value plan to get around the absolute priority rule and retain their interest in their property, but such plans were difficult because the Supreme Court required significant new value and monies’ worth up front, and a promise to provide future labor was not enough to qualify as new value.[5]

Congress confirmed that the absolute priority rule applied to individual debtors through the passage of the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA).[6] This legislation appeared to make significant changes for individuals in Chapter 11 cases by acknowledging that individuals were subject to the absolute priority rule, but it did provide an exception: “in a case in which the debtor is an individual, the debtor may retain property included in the estate under section 1115 . . . .” Section 1115, in turn, added to property of the estate in an individual Chapter 11 case income the debtor earned post-petition, thus making the individual Chapter 11 case similar to a Chapter 13 case. The big advantage was that there is no debt limit in Chapter 11; thus, the individual could confirm a plan by satisfying the requirements of section 1129(a)(15). This provision permitted a plan to be approved when the debtor paid his or her “projected disposable income” to be accumulated over a 60-month period.

Although insolvency professionals welcomed the new provisions under section 1129(a)(15), the confirmation requirements were still subject to the remaining confirmation requirements under section 1129(a), thus requiring the acceptance of creditors (contrary to Chapter 13), and when that acceptance was not forthcoming, the individual debtor was still subject to the absolute priority rule when a class of unsecured creditors objected to the plan. This would not have been a major obstacle, however, if the exception to the absolute priority rule that was added by BAPCPA had been interpreted broadly. Unfortunately for individual debtors, the failure of Congress to make it clear in any legislative history when BAPCPA was enacted that Congress intended the exception to be interpreted broadly (thus eliminating the absolute priority rule as it applied to individuals) created concerns among the circuit courts that the exception should be interpreted narrowly to only except the debtor’s post-petition income that was added by section 1115.[7] Consequently, in a normal Chapter 11, individual debtors are unable to confirm a plan that allows them to retain their nonexempt property over the objection of unsecured creditors unless such objecting unsecured creditors are paid in full. Alternatively, individual debtors can retain their nonexempt property if they convince the court that they are able to provide “new value” that will circumvent the requirements of the absolute priority rule. Given that the requirements of the new value are rather stringent, this is rarely achieved.

Congress appears to have come to the rescue of individual debtors through the passage of the SBRA. This statute created a new Subchapter V within Chapter 11 that is available to electing small-business debtors who have secured and unsecured debts less than $2,725,625.00. Given that there is no exclusion for individuals, these provisions will apply to individuals, provided that their debts are primarily business debts, they otherwise fit within the debt limits, and they are “engaged in commercial or business activities.”[8] In response to the COVID-19 pandemic, Congress increased the debt limit for Subchapter V cases to $7,500,000.00 for one year, ending March 27, 2021.[9]

Although there are many aspects of the new Subchapter V that are beneficial to an individual debtor, the most significant is the elimination of the absolute priority rule. The new Subchapter V does not include a limitation on equity retaining ownership if a class of allowed unsecured claims votes against the plan. A debtor may confirm a plan over the objection of an unsecured creditor class so long as (1) all “projected disposable income” of the debtor to be received in a three-year period, or such longer period as the court may approve but not to exceed five years, will be applied to the plan, or (2) the value of the property to be distributed under the plan in the three- to five-year period is not less than the “projected disposable income” of the debtor.[10]

Other advantages of Subchapter V to an individual are as follows:

Plan exclusivity. Only the debtor may file a plan in Subchapter V.[11] Thus, there is no exclusivity period that expires after 120 days like a normal Chapter 11 case,[12] or 180 days in the case of a traditional small business.[13]

Reduced administrative expenses. There are no U.S. trustees fees in a Subchapter V case,[14] thus reducing the administrative expenses to the debtor. Further, unless the bankruptcy court orders otherwise, a committee of creditors may not be appointed in a Subchapter V case and the individual debtor will not have to pay the expenses of such committee.[15]

Easier retention of counsel. In a typical Chapter 11, the court will not approve retention of the debtor’s counsel if they are owed any amounts for prebankruptcy services.[16] Subchapter V has a special rule and allows retention of counsel or other professionals so long as the debtor’s prepetition fees do not exceed $10,000.[17] Thus, attorneys who provide services to an individual will still be able to represent the individual in the bankruptcy case even though there are some fees owed when the Subchapter V case is filed.

Modification of certain mortgages on principal residences. The restrictions on modification of a mortgage on the debtor’s residence were modified by Subchapter V to enable the debtor to modify such claims when the proceeds of the relevant mortgage were “used primarily in connection with the small business of the debtor.”[18] Although most mortgages are typically purchase money security interests and would still be prohibited from modification, this unique provision in Subchapter V will allow mortgage modification if the individual debtor had used a majority of the value in the debtor’s home to finance business operations.[19]

Limited post-confirmation plan modifications. Only the debtor may modify a plan after confirmation in Subchapter V.[20] This is a distinct advantage because section 1127(e) permits the trustee, U.S. trustee, or holders of an allowed unsecured claim to seek a modification to increase the amount of payments or extend or reduce the time for payments in a normal individual Chapter 11 case. Limiting plan modification to only the debtor excludes these parties from the threat of increasing plan payments when the debtor’s operations turn out to be more favorable than projected when the plan was confirmed. On the other hand, if the debtor’s projections were too generous, the debtor has the power to seek modification in order to reduce plan payments in a Subchapter V case. This modification right expires upon “substantial consummation”[21] when the plan is a consensual plan approved pursuant to section 1191(a), but can be accomplished at any time after confirmation when the plan is approved over the objection of a class of unsecured creditors pursuant to section 1191(b).

Paying administrative expenses over term of plan. Subchapter V permits the debtor to pay administrative expenses over the life of the plan, provided the plan was approved pursuant to the cramdown provisions of section 1191(b). A plan that is a consensual plan approved under section 1191(a) must provide for the payment of administrative expenses on the effective date of the plan in the same manner as a typical Chapter 11 plan under section 1129(a)(9)(A).[22]

Possibility of early discharge. Subchapter V allows an individual to obtain a discharge on the effective date of the plan, provided the plan was a consensual plan approved under section 1191(a).[23] In a cramdown plan approved under section 1191(b), the debtor’s discharge does not occur until the completion of the plan payments.[24] This latter requirement is similar to the discharge granted under section 1141(d)(5) in a non-Subchapter V Chapter 11 case, subject, however, to the exceptions to dischargeability of certain debts under section 523, which continue to apply to the individual debtor in Subchapter V.[25]

No limitation on cramdown of car loans. Subchapter V does not incorporate the requirements of section 1325(a) (hanging paragraph) that requires a Chapter 13 debtor to pay the full amount of a personal motor vehicle loan incurred within 910 days prior to the bankruptcy filing instead of the value of that collateral that normally is required for a secured claim under section 506(b). This means that the individual in a Subchapter V case will be able to force the vehicle lender to accept payments equal to the value of the vehicle even though the value is less than the full amount of the vehicle loan.

Greater protection of the automatic stay. Subchapter V does not invoke the exceptions to the automatic stay under section 362(n) that applies to a “small business case” that is filed within two years after the confirmation or dismissal of a prior small business case.[26] Thus, an individual in a Subchapter V case may file a second case within two years of the prior case and stay the actions of creditors that were pursuing the debtor.

Although there are many advantages to the Subchapter V for individual debtors, there are certain disadvantages that an individual must consider before heading down this path.

Limitations on eligibility. As previously discussed, there are debt limits for individuals seeking to take advantage of Subchapter V, and not less than 50 percent of the debts at issue must have arisen from the commercial or business activities of the debtor.[27] Furthermore, the debtor must be “engaged in commercial or business activities.” At least one court has ruled that an individual debtor met this requirement because he was “addressing residual business debt” arising from his defunct, closely held companies.[28]

Appointment of Subchapter V trustee. Each Subchapter V case requires the appointment of a trustee.[29] This does not require that the debtor turn over operations to the trustee because the trustee’s duties are similar to a trustee under Chapter 12. The Subchapter V trustee is tasked primarily with assisting the debtor in proposing and confirming a plan as well as making distributions under the plan. The debtor is responsible for the Subchapter V trustee’s fees. When the debtor has proposed a consensual plan, the trustee may be removed upon the substantial consummation of the plan, which generally occurs on or about the effective date of the plan when payments have been initiated to creditors.[30] In a nonconsensual plan, the trustee is responsible for making plan distributions to creditors until the plan is complete. At that time, the trustee will file a final accounting and a final report.

Plan deadlines and other mandatory procedures. A Subchapter V debtor has only 90 days to file a plan. This is a tighter deadline than a typical Chapter 11. Additionally, the court will hold a status conference within 60 days after the order of relief, and two weeks prior to that status conference the debtor must file a notice with the court explaining the debtor’s progress in confirming a consensual plan and providing such other information as the court may require.[31] This cuts in half the timing requirement for filing a plan in a small business case as provided under section 1121(e). A debtor may obtain an extension of the plan filing deadline, but the grounds for such an extension are limited under the statute to circumstances beyond the debtor’s control.[32]

Remedies upon plan default. Section 1191(c) requires the plan to provide appropriate remedies to protect the holders of claims in interest in the event that planned payments are not made. The normal requirements under Chapter 11 are merely that the plan is feasible pursuant to section 1129(a)(11), which does not require remedies to protect creditors. The only way to avoid this requirement is to convince the court with certainty that the debtor will be able to make all payments under the plan. Meeting such a standard is unlikely unless the plan already proposes a liquidation and more certain distributions to creditors. Any payment plan based on projected disposable income is not likely to have that certainty. The advantage provided to creditors by this provision is that when a plan includes a remedy, the creditor will have good grounds to force the debtor to pursue those remedies in lieu of dismissal of the Chapter 11 case or subsequent new filing of a Chapter 11 case (Chapter 22). It is also likely that courts will not view further reorganization as an adequate remedy, but rather may force a liquidation to protect the interests of creditors.

Despite these burdens on debtors, it is clear the advantages to eligible individuals under Subchapter V, particularly the elimination of the absolute priority rule, will make it substantially easier for individuals to confirm Chapter 11 plans. The plan will not depend on approval of an impaired class, and the debtor may retain assets without paying unsecured claims in full. These benefits, in tandem with the higher debt limits under the CARES Act through March 2021, will likely increase the number of individuals eligible for and taking advantage of the new Subchapter V. No doubt the current economic decline caused by the COVID-19 pandemic will result in a surge of debtors in need of bankruptcy protection. Thus, Subchapter V could not have been enacted at a more opportune time.

[4] 485 U.S. 197, 108 S. Ct. 963 (1988) (case involving an individual farmer).

[5]SeeNorwest, 485 U.S. at 202–06, 108 S. Ct. at 966–68 (rejecting argument that the “sweat equity” of the farmer after confirmation of the plan was sufficient new value for the farmer to retain his interest in farm).

[16]See id. § 327(a) (authorizing retention of professional persons “that do not hold or represent an interest adverse to the estate, and that are disinterested persons”); id. § 101(14) (defining “disinterested person” as a person that “is not a creditor”).

[19] The recent case of In re Ventura, 2020 WL 1867898 (Bankr. E.D.N.Y. Apr. 10, 2020), identified certain factors to consider before allowing modification of a mortgage on a principal residence in Subchapter V.

As organizations begin to reintroduce people back into workplaces and schools during the COVID-19 pandemic, they face a unique set of privacy issues that arise from the use of screening processes and technologies. Organizations must design and implement new procedures to protect the health and safety of workers, students, and staff, but these procedures, the technology deployed to implement them, and the data that is collected in support of them can run afoul of the legal protections set forth in privacy and security laws, not to mention labor and employment laws. The laws that impact each organization will also vary depending on whether the organization is a government or a private entity and in which jurisdiction(s) the organization operates.

Generally, bringing people back to work and school involves implementing some combination of the following strategies: (1) written rules and procedures to be followed, (2) prescreening to determine who can return to work or school, (3) symptom tracking and health screening on an ongoing basis, and (4) contact tracing and quarantining if exposure to COVID-19 is suspected. Each of these strategies creates a series of issues that must be addressed.

Although written procedures must be consistent with changing public health guidelines, they still might not be enforceable. For example, many public schools have created written procedures for athletes who are returning to their sports at the high-school and college levels.[1] Although these procedures are designed to protect and ensure safety for athletes, they often cross the boundary between encouraging athletes to follow the rules and asserting that athletes have assumed the risks of participating—constituting a waiver—with questionable enforceability.[2]

Closely related to privacy concerns is the fact that prescreening of employees to determine whether they can return to work may violate employment laws. The EEOC has already asserted that the use of COVID-19 antibody tests as a vehicle for prescreening employees to determine whether they can return to work violates the Americans with Disabilities Act’s “job related and consistent with business necessity” standard for medical examinations or inquiries for current employees because CDC guidelines provide that antibody test results “should not be used to make decisions about returning persons to the workplace.”[3]

Symptom tracking and health screening raise a number of privacy issues, from what questions can be asked for screening, to how the data that is collected should be treated. The EEOC guidance for covered employers specifies that employers may ask employees whether they are exhibiting symptoms associated with COVID-19, consistent with current CDC-specified symptoms and guidelines, or those of other public health authorities and reputable medical sources. Employers may also take the body temperature of employees during the pandemic consistent with recommendations of the CDC and state and local health authorities. All information collected must be treated as an employee medical record, with the associated implications for protecting the privacy of that data and limits on maintaining and sharing such information. It is important to note that employers are allowed to share medical information with public health agencies.

The use of contact tracing for determining whether a person has been exposed to COVID-19, or has exposed others, raises a plethora of new issues. Contact tracing can be performed manually, but is often implemented through mobile applications that communicate with each other. The Google/Apple partnership, for example, has developed a common application programming interface (API) that will be available on all mobile phones that run either the Android or iOS operating systems.[5] This API allows public health agencies and medical organizations to develop contact tracing applications. The underlying technology enables phones to contact each other when they are in proximity and share anonymous information that can later be used to develop contact lists if a person is diagnosed with COVID-19.[6] This technology is subject to a number of privacy and security concerns, including device tracking to identify and locate users,[7] sharing of personally identifiable[8] and confidential health information, and use of that data for other purposes by either the technology companies or public health organizations. These applications must also be deployed carefully by employers to prevent labor law issues associated with surveillance outside of work hours.[9] Existing privacy laws are still in effect for the data collected as part of contact tracing, and some states are weighing in to create new privacy laws to specifically address contact tracing.[10]

Finally, the collection of data also creates record retention issues. Organizations may be tasked with keeping certain records to establish compliance with privacy mandates or to otherwise address broader regulatory concerns, particularly for human resources records. Add to that the fact that some data, even if it does not rise to the level of a record, may need to be retained for statistical or other metrics measurements. These data retention issues must be carefully balanced against strict privacy regulations at the national and international levels. To that end, litigation discovery concerns could also rear their ugly heads. This is where processes and systems for record retention and disposition are most critical.

On the whole, organizations face a difficult set of privacy issues arising from the use of screening processes and technologies to reintroduce workers and students to workplaces and schools during the COVID-19 pandemic. The landscape of legal privacy issues is going to continue to change as CDC guidance changes over time and as more governments pass new legislation to specifically address COVID-19-related challenges.

* Joan Wrabetz is a J.D. candidate, 2021, at Santa Clara University. John Isaza, Esq. is Vice President of Information Governance Solutions at Access Corp in Boston. Mr. Isaza can be reached at [email protected].

Ward Classen is a member of the legal department of Discovery Education, Inc. He has over 35 years’ experience negotiating complex information technology agreements and has practiced with many of the world’s leading technology companies, including Computer Sciences Corporation (now DXC Technology Corporation), Accenture, and InterDigital, Inc. Ward is the author of A Practical Guide to Software Licensing and Cloud Computing. The seventh edition will publish in October 2020.

Question: What triggered your interest in software licensing?

Answer: As a young lawyer I attended an ABA Annual Meeting and had the good fortune to participate in the Business Law Section’s Software Licensing Subcommittee meeting where I met Ray Nimmer, Holly Towle and Don Cohn. They encouraged me to pursue my interest in software licensing and were always willing to answer my questions. Over the years we continued to cross-paths as a client, opposing counsel or opposing expert witness.

Question: Software licensing seems complicated. For the lawyer, what knowledge do you need to acquire before you even start approaching all the legal implications of the topic.

Answer: It is important to have a strong understanding of how the underlying technology will be used by the client to ensure the client obtains the rights it needs. Once an attorney understands how the client will use the underlying technology, he/she can apply the principals of commercial contracting and software law.

Question: What are some of the common pitfalls companies make when it comes to software licensing?

Answer: Many companies fail to fully understand and anticipate their technology needs, as their current and future needs will evolve over time, often preventing the company from obtaining the rights they need to meet their business objectives. For example, prudent companies should carefully consider who will access and use the software application and how such use and access may change in the future.

Question: The appendix material in your book is fantastic—and so comprehensive. Where do you think software licensing is headed? What are the challenges?

Answer: Software use and licensing continues to evolve with changes in the market, requiring an attorney to remain abreast of changes in how technology is utilized and licensed. While on-premises licenses were once the norm, an increasing number of users now access and use an application through cloud computing. Recently, COVID-19 has changed how users access and use applications, as many employees are using corporate licensed applications on their personal computers, where previously they accessed and used the application only on their employer’s hardware.

Question: What triggered your interest in family business succession planning?

Answer: Before I attended law school, I worked in several family businesses, and I enjoyed those experiences. I learned to respect the courage of entrepreneurs and owner-operators. I appreciate the contribution that family businesses make to the economy and the communities in which they operate. Also, I love my job because I can help make families happier. That’s a pretty good way to spend my work hours.

Question: In your book, you detail the planning process for business succession. What common mistakes do business owners make when it comes to succession?

Answer: The biggest mistake is not planning at all. Proper business succession planning can help a family business in many ways. It can avoid succession crises, but it also can lead to tax savings, better business practices, greater financial security for the senior generation, and opportunities for personal development for members of the next generation. A second big mistake is not planning for a change of governance mechanisms to adapt them to successor ownership. For example, when ownership passes from the founder to the founders’ children, the business’s governance structure needs to change to accommodate and define the input of multiple new owners. A third big mistake is not planning for the senior generation’s life after exit from the business. This mistake can cause senior generation managers to stay too long or to suffer lifestyle impairments in retirement.

Question: I found it interesting how retirement is linked with succession. Do they go hand in hand or does one trigger the other?

Answer: Often senior generation retirement is inextricably linked to ownership and leadership succession. First, senior generation leaders may be unwilling or unable to retire until members of the next generation are ready to take over managing the business. Often this requires a succession plan that adapts governance and management structures to optimally support the leadership skills and participation of the next generation owners. Second, senior generation leaders may be unwilling or unable to retire because they remain economically dependent on the business and its continuing success. Business succession planning can provide a secure and viable economic future for senior generation owners after they retire and transfer their ownership interests. Unless the senior owners can retire, there may be no business succession until they die. That’s a circumstance that is bad for everyone involved.

Question: The appendix material in your book is fantastic! The lawyer has a wide range of issues to confront in succession planning—in your opinion, what is the most difficult part for the practitioner?

Answer: The most difficult part of family business succession planning for the lawyer is the broad scope and diversity of issues that the lawyer must address. The purpose of the book is to help identify those issues and to suggest ways to address them. Sometimes it is important for the lawyer to get help from colleagues or the clients’ other advisors. Business valuation, tax elections or choice of entity, nonqualified retirement plans, and disability insurance are all examples of issues that may require the lawyer to collaborate with other advisors. The book will help the lawyer spot these issues, even though they may not be in the lawyer’s areas of core competency. Family business succession planning is a collaborative, long term project, and that can become confusing or messy if the lawyer doesn’t keep it organized. The appendix materials in the book provide ways to stay organized with respect to the big picture and the details.

Connect with a global network of over 30,000 business law professionals