At the Virtual Section Annual Meeting in September 2021, Jeannie Frey, chair of the Business Law Section, awarded Wilson Chu, immediate past chair of the Section’s Mergers & Acquisitions (M&A) Committee, the prestigious “Section’s Chair Award,” which honors members who have made exceptional contributions to the Section and the legal profession.

In her presentation remarks, Frey identified Chu’s leadership skills and his ability to remain “cool and unflappable” under any situation as key components in selecting him for this award. His stewardship as chair of the M&A Committee, noted Frey, demonstrated his commitment to the Section, its members, and the practice of law.

“Wilson brought enthusiasm and creativity to his role as chair of the Mergers & Acquisitions Committee,” said Joel I. Greenberg, partner at Arnold & Porter and a former chair of the M&A Committee. “He was constantly looking for ways to promote the Committee and bring increased value to its members, despite having the bad fortune of serving nearly half of his term during a worldwide pandemic.”

According to Frey, Chu’s accomplishments were impressive—and numerous. He paved the way for M&A to host a major conference; oversaw another Deal Points Study; produced more video content for the M&A Market Check Series; and continued to strengthen the Section’s largest substantive committee.

“Wilson has been a major contributor to the success of the M&A Committee for many years,” said Scott T. Whittaker, partner at Stone Pigman Walther Wittman L.L.C. “It was fortuitous for the M&A Committee that the pandemic coincided with Wilson’s tenure as Chair, because the Committee was able to thrive, despite the lack of in-person meetings, in large part due to his creativity and enthusiasm.”

Whittaker, who also served as chair of the M&A Committee, believes that the key to the long-term success of the Committee is the continuing contributions of its long-term members, combined with a culture that welcomes new members. “Wilson has continued to build on that tradition, which has not only kept the Committee in the forefront of thought leadership in the field of M&A, yet allows for many of our newer Committee members to enhance their personal profiles through Committee involvement.”

M&A Energized and Thriving

Leigh Walton, partner at Bass, Berry & Sims, characterized Chu as one of the most energetic chairs of the M&A Committee since its founding. Chu was also the force behind the debut of new programs, such as M&A Market Check Series in collaboration with Hotshot, and Walton predicts that this new member offering will have a profound impact on the Committee and the Section in years to come. “His emphasis on new, younger and diverse members will serve us well,” said Walton. “I cannot imagine we could have chosen a more capable leader for the last three years.”

If innovation and leadership are hallmarks of Wilson Chu’s tenure as chair, his uncanny ability to “make things happen” must also be added as an underlining theme for all his years in serving the Section. Chu was one of the founding members of the Market Trends Subcommittee that led to the creation of the Deal Points Study—one of the crown jewels of content at the ABA.

Michael O’Bryan, who succeeded Chu as chair of the M&A Committee in September, credits him with a long history of bringing energy and ideas to the M&A Committee and to the M&A profession. “It will be a challenge keeping up with Wilson,” he noted. “Wilson brought our Committee through a difficult transition and got us to a great place.”

Chu’s work has not only been confined to M&A. He also has a liaison role to the Section’s Sponsor Board; and he has helped the Section in identifying the value of Section/Committee membership and increasing the profile of events. In fact, at the Section’s Spring meeting in April 2021, Chu was able to finesse an interview with entrepreneur Mark Cuban that centered on issues relevant to our members.

Section Involvement Leads to Engagement

“As a former chair of the M&A Committee (back when it was called the Committee on Negotiated Acquisitions), I appreciate how much time and effort Wilson’s role has taken up,” said Richard Climan, partner at Hogan Lovells. “His creative thinking and seemingly boundless energy have made him a standout in this role, and his ability to navigate the stresses of the COVID pandemic has made his tenure as chair particularly memorable. He is widely admired and respected among active Committee members.”

As he accepted the award, Chu remarked that he was often asked why he would devote his limited free time to Section and Committee activities and projects. “The answer is simple,” said Chu. “It gives me the opportunity to meet people and to learn from them.”

The Section and its members, especially young lawyers, have indeed learned from Wilson, and will continue to benefit from his skills as a dealmaker.

“Wilson is steadfastly loyal to the idea of making things better than he finds them,” said Chauncey M. Lane, partner at ReedSmith LLP in Dallas. “This is the impact he has had as leader within the Business Law Section and the Mergers and Acquisitions Committee.”

In this unanimous en Banc opinion, the Delaware Supreme Court overturned its oft-criticized decision in Gentile v. Rosette, 906 A.2d 91 (Del. 2006) (“Gentile”). Gentile held that a stockholder who allegedly suffers dilution as a result of a controlling stockholder increasing its holdings had standing to pursue a direct claim because a corporate dilution/overpayment claim was “dual-natured” (i.e., direct and derivative). Gentile, however, stood in tension with the Court’s earlier decision in Tooley v. Donaldson, Lufkin & Jenrette, Inc., 845 A.2d 1031 (Del. 2004) (“Tooley”), in which the Court articulated a two-part test for determining whether a stockholder’s claim is direct or derivative. The Brookfield Court put to rest the Gentile dual-natured exception in favor of Tooley and thereby made clear that stockholder plaintiffs will now need to contend with the demand requirement under Court of Chancery Rule 23.1 in controller dilution cases.

This case arose from a June 2018 private placement in which Brookfield Asset Management, Inc. (“Brookfield”) acquired $650 million shares of TerraForm Power, Inc. (“TerraForm” or the “Company”) increasing Brookfield’s interest in TerraForm from 51% to 65.3% (the “Private Placement”). Stockholder plaintiffs sued, alleging that TerraForm issued stock for insufficient value in the Private Placement, diluting the minority stockholders’ economic and voting interests. Plaintiffs asserted their claims both directly and derivatively, but in July 2020, Brookfield affiliates acquired all outstanding stock of the Company not already owned by Brookfield, and plaintiffs lost standing to pursue the derivative claims.

Defendants moved to dismiss the plaintiffs’ remaining direct claims, arguing they are exclusively derivative under Tooley.In October 2020, the Court of Chancery found that plaintiffs’ overpayment claims were derivative under Tooley and were also direct under Gentile’s dilution claim exception to Tooley. Defendants moved for interlocutory appeal of that decision, which application was granted in light of earlier criticism from the Delaware Supreme Court questioning the continued validity of Gentile.

In this decision, the Delaware Supreme Court identified doctrinal, practical, and policy reasons for overturning Gentile. The Court acknowledged three ways in which Gentile was in tension with Tooley.

First, the Court found tension in Gentile’s conclusion that economic and voting dilution was an injury to stockholders independent of the corporation. The Court stated that the basis for plaintiffs’ claims was that the Private Placement allegedly harmed the Company by issuing shares to Brookfield for an unfairly low price, resulting in the plaintiffs suffering harm through the reduction in economic and voting power in proportion to their shareholdings, and the harm was therefore indirect.

Second, the Court found that Gentile’s explicit reliance on In re Tri-Star Pictures, Inc. Litig., 643 A.2d 319 (Del. 1993) (“Tri-Star”) created tension with Tooley because Tri-Star relied on opinions applying the “special injury” test that Tooley expressly rejected. Gentile stated that it was applying both Tooley and Tri-Star, which the Court found inconsistent with Tooley’s clear rejection of the “special injury” test.

Third, the Court noted that Gentile’s reliance on the presence of a controlling stockholder conflicted with the Tooley test, which solely focuses on who suffered harm and who would recover rather than the nature of the wrongdoer.

The Court then identified practical concerns with Gentile. First, the carve-out for dual-natured claims in Gentile was unnecessary because there are other avenues through which stockholders may assert fiduciary duty claims in change-of-control transactions or challenge the fairness of a merger. Second, because both the corporation and stockholders could recover for harm under Gentile, there was a risk of double recovery.

Next, the Court explained why stare decisis did not prevent overturning Gentile. The opinion held that fifteen years grappling with Gentile was sufficient to determine that the difficulties that it created were unworkable and that Gentile was a substantial departure from Tooley. The Court also found that the Supreme Court’s statements casting doubt on the continued viability of Gentile in El Paso Pipeline GP Co. v. Brinckerhoff, 152 A.3d 1248, 1256 (Del. 2016), meant that parties could anticipate that Gentile’s status was in jeopardy.

While Gentile was limited to dilution claims, the decision to overturn it is a continued endorsement of the simplified direct versus derivative analysis established by Tooley. This decision provides more certainty for litigants and the courts regarding the applicable pleading standards to assert a dilution claim (i.e., it must meet the Rule 23.1 pleading standard for derivative claims) and the standing of stockholders to bring a dilution claim (i.e., they must be continuous owners of the nominal defendant corporation’s stock).

In this en Banc opinion, the Delaware Supreme Court unanimously eschewed the long-standing test for determining demand futility set forth in Aronson v. Lewis, 473 A.2d 805 (Del. 1984) (“Aronson”) in favor of a “universal” three-part test that incorporates principles from both Aronson and Rales v. Blasband, 634 A.2d 927 (Del. 1993) (“Rales”). The universal demand futility test adopted in this decision focuses primarily on whether directors are disinterested and independent with respect to the litigation demand rather than the decisions or actions being challenged in the litigation. The Court also held that claims exculpated by a corporation’s Section 102(b)(7) charter provision do not expose a director to a “substantial likelihood of liability” for purposes of the demand futility analysis.

Prior to Zuckerberg, the Delaware Supreme Court had established two tests—in Aronson and Rales—to determine whether directors can exercise independent and disinterested judgment regarding a pre-suit demand. Aronson applied when the directors who made the challenged decision also constituted a majority of the directors who would consider a pre-suit litigation demand and focused on the substance of the challenged transaction. The Rales test applied when no specific board decision was challenged (e.g., failure of oversight claims) or when a majority of the directors on the board that would be considering the litigation demand did not participate in the challenged decision. The Rales test focused on the independence of the decision regarding a litigation demand rather than the underlying business decision being challenged.

Zuckerberg involved a proposed reclassification of the shares of Facebook, Inc. (“Facebook”) that would have allowed Mark Zuckerberg to donate a majority of his Facebook stock to charity while still maintaining control of the company (the “Reclassification”). The Reclassification was challenged by Facebook stockholders and, shortly before trial, Facebook withdrew the Reclassification, rendering the lawsuit moot. Facebook spent more than $20 million defending the litigation and paid plaintiffs’ counsel more than $68 million in attorneys’ fees under the corporate benefit doctrine in a class action settlement.

After the Reclassification litigation concluded, another Facebook stockholder filed a derivative complaint seeking compensation for the money Facebook spent in connection with the prior action. The stockholder plaintiff argued that demand was futile, and defendants moved to dismiss the complaint under Court of Chancery Rule 23.1 for failure to make demand on Facebook’s board of directors or adequately plead demand futility. Although the Court of Chancery acknowledged—and the parties agreed—that the Aronson test applied because a majority of the board members who would have considered a demand also made the challenged decision to pursue the Reclassification, Vice Chancellor Laster determined that Aronson’s“analytical framework [was] not up to the task,” and instead chose to apply the Rales test while also “draw[ing] upon Aronson-like principles.” In applying this hybrid test, the Court of Chancery concluded that a majority of the Facebook board was capable of considering a demand and dismissed the claim under Rule 23.1.

In Zuckerberg, the Delaware Supreme Court endorsed the demand futility analysis applied by the Court of Chancery as the “universal test” for assessing demand futility. Therefore, it is no longer necessary to determine whether the Aronson test or the Rales test governs the demand futility inquiry. Under the refined test, courts will focus on the following three questions, applied on a director-by-director basis:

whether the director received a material personal benefit from the alleged misconduct that is the subject of the litigation demand;

whether the director faces a substantial likelihood of liability on any of the claims that would be the subject of the litigation demand; and

whether the director lacks independence from someone who received a material personal benefit from the alleged misconduct that would be the subject of the litigation demand or who would face a substantial likelihood of liability on any of the claims that are the subject of the litigation demand.

If the answer to any of these questions is “yes” for at least half of the members of a demand board, then demand is excused as futile.

In affirming the Court of Chancery’s decision and adopting this approach to demand futility, the Court explained, “The purpose of the demand-futility analysis is to assess whether the board should be deprived of its decision-making authority because there is reason to doubt that the directors would be able to bring their impartial business judgment to bear on a litigation demand.” The Court’s opinion thus provides more clarity for determining demand futility, by blending the previous tests from Aronson and Rales and appropriately “refocus[ing] the inquiry on the decision regarding the litigation demand, rather than the decision being challenged,” while remaining consistent with Aronson, Rales, and their progeny. The refined test is especially helpful in situations where Aronson would have proved difficult to apply, such as when there has been turnover on a corporation’s board or director abstention.

Companies are subject to various types of regulatory and statutory compliance requirements, whether they are publicly traded, privately held, or even nonprofits. The requirements may vary by industry and location, the latter referring to both the company’s state of incorporation and where it does business. Publicly traded companies have a further overlay of Securities and Exchange Commission (SEC) and stock exchange regulation. This article provides a broad overview of how board members should address these compliance requirements as part of their oversight duties to forestall future issues, and how preparation is key when an issue does arise.

The fiduciary duties of board members include far more than just oversight of compliance, and so it is important to note at the outset that compliance is not the same as governance. However, a central duty of corporate board members is the oversight of the company’s compliance with all laws and regulations to which the company is subject. This includes staying aware of any new regulations that may arise, as well as changes in existing regulations, particularly as both the regulatory landscape and a company’s activities are constantly changing.

For example, as companies expand vertically, whether upstream into activities like production and raw material sourcing or downstream into activities like distribution and retail sales, the company may become subject to regulatory schemes that are new and unfamiliar to the company and its board. A company’s merger and acquisition activity may introduce new businesses and/or business jurisdictions, which may also be new and unfamiliar. Even the regulatory frameworks with which the company may be experienced are likely changing constantly, whether in small ways or large, and of course how those regulations are applied and interpreted by tribunals affects the requirements for compliance. The board’s oversight of compliance should therefore be a regular part of the board’s agenda, and optimally a board committee such as audit—or a risk committee, if there is one—should be assigned to monitor compliance closely, including watching out for new areas of compliance and changes in preexisting ones.

Inevitably, breakdowns in a company’s compliance policies and procedures may occur. Noncompliance can cause severe disruptions in a company’s business activities, and it can create material costs in terms of investigations—both internal and by regulatory agencies and/or law enforcement—and penalties. These failures can also seriously damage a company’s reputation and brand, impacting relationships with customers and vendors, and they can depress employee morale and hinder a company’s ability to attract new employees. And of course, noncompliance can potentially result in liability for individual directors.

Board members should also be aware that whistleblowers have become a regular part of the governance landscape, and their revelations are typically related to some area of alleged noncompliance. Many companies have programs that ostensibly are designed to encourage whistleblowers to report actual or suspected noncompliance, and to provide boards with direct visibility into such reports. However, there are significant variations in the effectiveness of whistleblower programs, as well as in the quality of the board responses. Ideally, on a “clear day,” boards should regularly review their company’s whistleblower program, looking for opportunities to strengthen and improve it, and of course to prepare extensively and in advance for their own response if/when the need arises.

When evidence of noncompliance arises—whether through an effective compliance program, whistleblower report, management discovery, or regulatory or law enforcement action—boards must decide whether to launch an internal investigation. If a regulatory agency or law enforcement is not already involved, the board must determine with the assistance of counsel whether the company is required to report the noncompliance, and then cooperate fully with any ensuing investigation. There may also be a requirement—or at least an opportunity—to communicate with stakeholders, such as customers, vendors, employees and/or local communities.

It’s usually better to “play offense rather than defense” with regard to publicity after noncompliance is discovered, which gives the company the opportunity to affect the narrative. Again, a board that is prepared in advance for a range of possible needs can be more effective in overseeing management’s response. For example, preparations could include lining up potential outside advisors, determining how company communications will be handled, and assigning a board committee to oversee the responses by management, both internal and external, as well as help coordinate any board action that may be needed. For example, in addition to the possibility of an internal investigation and notification of appropriate authorities as noted above, there may be personnel issues uncovered by the issue, weaknesses in systems and controls, or other management actions called for that should receive board oversight.

Such a board committee may need to be a new one—a “special committee”—composed exclusively of independent and “disinterested” directors, both to provide the necessary board resources to focus on the problem, as well as to insulate the board’s response from any parties that may have been involved, whether by act of omission or commission. Rather than scrambling to add independent directors when the need arises, it’s better to have enough independent directors in place at all times in order to form a special committee, should the need ever arise. Suffice it to say, “The games are won in practice!”

The quickness and thoroughness of the company’s response can favorably influence the severity of whatever regulatory or law enforcement penalties may ultimately be applied, as well as help reduce any damage to the company’s reputation and relationships. However, the potentially beneficial effect provided by the company’s response may vary widely with the type of noncompliance problem, e.g., antitrust, Foreign Corrupt Practices Act, health and safety, etc. Again, boards are well-advised to prepare for all of the above potential needs well in advance. In addition to the potential preparatory actions mentioned above, preparation may include, among other things, refreshing bylaws and strengthening and reinforcing the reporting processes, e.g., through compliance or internal audit.

Board oversight of compliance has undoubtedly been affected by the pandemic. Sources of information have been disrupted with employees not being on-site, and the lack of in-person communication may have had a subtle but nonetheless important effect on decreasing the flow of information. The lack of in-person board meetings, as well as the distraction of exigent issues raised by the pandemic, may contribute to a decrease in attention to overseeing compliance. Remaining compliant requires deliberate allocation of attention and resources, both of which may have been strained during the COVID-19 pandemic.

Boards must take account of this, or risk falling victim to compliance failure. Valuable knowledge can be gained from the cautionary tales of compliance failures of companies that have been made all too public, becoming object lessons for boards in general. In many cases, class actions and other litigation have followed, with courts reviewing the actions and inactions of boards and providing guideposts for the future through their decisions. The Caremark line of case decisions[1] has provided some guidance for boards, the overarching message of which is that boards must be diligent in their oversight of compliance, and properly document in board minutes and elsewhere that they have done so. For example, in the Marchand case,[2] involving a dairy producer and an outbreak of listeria from its products, the Court found that compliance with food safety regulations was central to the company’s business, and therefore should have received greater board oversight.

Regardless of whether a company ultimately prevails in such litigation, much of the damage may have already been done to the company’s reputation, brand and relationships—possibly its most valuable assets but which appear nowhere on its balance sheet. The value of advance preparation cannot be overestimated, since the company’s speed of response may be crucial in limiting the damage from a noncompliance issue. While not a noncompliance example, the historical “gold standard” for crisis response was that of Johnson & Johnson, when, in 1982, bottles of Tylenol were discovered to have been tampered with, leading to several deaths. The company famously took broad action, including the removal of millions of bottles from store shelves. What is less remembered is that response took several days, possibly because the company was unprepared to ever have to take such action. Contrast this with the episode on United Airlines in 2017 when a passenger was forcibly dragged off the plane, with videos circulating via the Internet within seconds. The damage to a company that can follow a crisis can occur within minutes, and companies—and the boards that oversee them—must be prepared in advance.

Oversight of compliance is an important board duty, and it should be high on the list for attorneys advising boards on their governance.

[1] See, e.g., In re Caremark Int’l Inc. Derivative Litig., 698 A.2d 959 (Del. Ch. 1996).

[2]Marchand v. Barnhill, 2019 WL 2509617 (Del., 2019).

This article is the third in a series on intersections between business law and the rule of law and their importance for business lawyers, created by the American Bar Association Business Law Section’s Rule of Law Working Group. Read more articles in the series.

Introduction

Press reports have referred to Facebook’s Oversight Board using a range of descriptors from the cynical to the ridiculous. Oversight Board has been referred to as “an elaborate structure for a supposedly independent body to review…content decisions”[1] and “a group of [Zuckerberg’s] own making.”[2] It has also been called an “independent body,”[3] an “independent panel,”[4] and a “quasi-independent oversight board.”[5] Some reports have gone so far as calling it Facebook’s “Supreme Court,”[6] “a quasi-judicial organization,”[7] or even an “international human rights tribunal.”[8] These descriptions are neither fitting nor accurate. In stark contrast, Oversight Board uses more narrow terminology to describe itself, using little more than its own highly suggestive name and sharply defined contractual terms.[9] Most recently, placing board members on par with journalists, academics, and other members of civil society, the board characterized its work as a mere “part” of a “collective effort” to steer Facebook towards greater transparency.[10] In the face of conflicting characterizations and persistent controversy surrounding Facebook’s business activities, how do lawyers, particularly business lawyers, understand and evaluate Oversight Board’s novel construction, that claims to incorporate principles of the rule of law and international human rights into the core of its activities?

The Structures of Oversight Board

As one of the world’s largest and most prominent social media platforms,[11] Facebook[12] has responded to increasing demand for the regulation of social media companies in a novel manner, by creating a separate private business entity to advise a narrow band of its content decisions. Facebook first announced such a possibility in November 2018 in a note posted to the platform by its CEO Mark Zuckerberg. There, Zuckerberg envisaged an entity that would prevent concentration of decision-making within Facebook as a business, enhance accountability and oversight of Facebook’s content decisions, and assure that content decisions were being made in the best interests of Facebook as a community, rather than merely for commercial purposes.[13]

Zuckerberg’s announcement was made on the heels of the Cambridge Analytica data scandal that broke in the Spring of 2018 when a whistleblower reported that Facebook had allowed a company that sold psychological profiles of voters to political campaigns to harvest detailed personal information from up to 87 million Facebook profiles.[14] This scandal was in addition to growing concern about the polarizing effects of Facebook’s algorithms on society[15] and Facebook’s algorithm-driven censorship practices.[16]

Many credit Sir Nick Clegg, former British Deputy Prime Minister and Facebook’s current Vice-President of Global Affairs and Communications, for forcing action on the business risk confronting Facebook as a result of its mounting scandals.[17] While transitioning to his current role with Facebook, in Fall of 2018, Clegg described Zuckerberg as being “under no illusions about the reputational squall” of the company he leads.[18] To address this “reputational squall,” Clegg conditioned his joining Facebook on the aggressive insistence that Facebook, as “a company with more than 2 billion users,” start acting like a “global power…and go out and engage with the messiness of the real world.”[19]

Subsequently, in October 2019, Facebook settled the $130 million Oversight Board Trust as its sole Settlor. Through its Trustees, the Trust then created a private entity named Oversight Board LLC,[20] a name both suggestive and misleading since Oversight Board is not a board, per se. Oversight Board is a Delaware limited liability company that holds the Oversight Board Trust as its sole member.[21] Acting through Oversight Board LLC, the Trust funds the hiring, remuneration, and maintenance of a panel of experts, also termed “Oversight Board,” and referred to herein as the “board.”

Currently made up of 20 expert members from a range of countries and backgrounds,[22] Oversight Board’s board was created to:

protect free expression by making principled, independent decisions about important pieces of content and by issuing policy advisory opinions on Facebook’s content policies.[23]

Facebook maintains a heavy hand in the selection of board members. For example, Facebook retained the right to select the board’s first four board members, all of whom automatically became (and currently remain) the first Co-Chairs of Oversight Board.[24]

Rule of Law and Oversight Board

As Kimberly Lowe pointed out in the first article in this series, “The Business Lawyer and the Rule of Law,”[25] the American Bar Association has broken down the broad concept of the rule of law into a helpful “set of principles, or ideals, for ensuring an orderly and just society” where:

no one is above the law, everyone is treated equally under the law, everyone is held accountable to the same laws, there are clear and fair processes for enforcing laws, there is an independent judiciary, and human rights are guaranteed for all.[26]

Oversight Board’s Charter quite legibly references these and other principles of the rule of law when discussing the role of its board. For example, inspired by principles of due process and equal treatment, Oversight Board’s Charter “specifies the board’s authority, scope and procedures, including how Facebook and the people registered to use its services…can access the board.”[27] Additionally, the Charter requires the board to operate transparently, including by ensuring that board decisions are “explained clearly to the public, while respecting user privacy and confidentiality” and provide “an accessible opportunity for people to request [the board’s] review and be heard.”[28] Moreover, in the style of courts and international tribunals, the Charter sets out the expectation that past decisions will establish precedent for future boards.[29]

Along these lines, the board produces written opinions that explain the reasoning behind board decisions. These opinions are freely available, in different languages, on the Oversight Board website. Moreover, opinions are structured for ease of access and include case summaries followed by detailed and structured explanations of board decisions. Mirroring the format of opinions published by courts and tribunals, opinions are divided into standardized sections to enable quick reference to key aspects of each decision.

Perhaps the most striking rule of law feature of these opinions is the inclusion of a section, in each opinion, containing a highly stylized discussion on Facebook’s human rights obligations. [30] It should be noted that from a legal standpoint, the board’s discussion of human rights is grounded in Facebook’s official Corporate Human Rights Policy.[31] This policy voluntarily incorporates the United Nations Guiding Principles on Business and Human Rights,[32] the International Bill of Human Rights, and numerous international human rights treaties.[33] Enforcing compliance with Facebook’s Corporate Human Rights Policy, board decisions include, for example, application of Article 19 of the International Convention on Civil and Political Rights on “Freedom of Expression” to Facebook’s private content decisions.[34]

Notably, in its Charter and published opinions, Oversight Board expressly rejects American-style rights adjudication in favor of European/international approaches. This bias is made legible in two ways. First, according to Oversight Board’s Charter, past opinions do not bind future boards; they retain merely persuasive value.[35] Second, the Charter adopts a balancing approach to the adjudication of human rights, an approach favored by European and international forums.[36] To elaborate, it is generally held that the American common law system tends, as a norm, to treat rights as a sort of property—either individuals have them or they do not. To determine whether an individual is in possession of a right, in addition to reliance on constitutions, statutes, and regulations, a common-law judge turns to precedent (a court decision considered authoritative for deciding subsequent cases involving identical or similar facts).

By contrast and as a general matter, European and international forums treat rights like platonic objects that exist independently of the humans that claim them. This approach permits an adjudicator to weigh and balance individual rights against a larger collection of competing and complimentary rights, with an emphasis on preserving the integrity of the broader system of rights, writ large. Thus, in European and international forums, where past decisions generally have persuasive (as opposed to binding) value, judges look to past decisions for broad guidance on general principles without being obligated to align past decisions with future outcomes. In the American system, for example, parties may press judges, on appeal, to explain and account for differences in the balancing or weighing of rights between different cases. In contrast, European judges (and judges presiding over international forums that have adopted a similar style) enjoy a reasonable degree of play in the joints when it comes to describing the interplay between rights.

Cementing its preference for European and international approaches to human rights adjudication, Oversight Board’s Charter explicitly sets up the task of its boards as one of balancing the fundamental human right to free expression against “authenticity, safety, privacy, and dignity.”[37] In a similar nod to European approaches, board decisions are produced with the support of an independent research institute headquartered at the University of Gothenburg. With support from a team of over 50 social scientists on six continents, as well as more than 3,200 country experts from around the world, the institute provides expertise to the board on socio-political and cultural context of board decisions.

This preference in favor of European approaches to human rights adjudication is especially noteworthy when considering Facebook’s long struggle for credibility, as a business, with European authorities, including its difficulties with German and European regulators[38] as well as its difficulties with Norwegian Press.[39] Similarly, a preference for a more international approach is also better appreciated when considering the fact that over 80% of Facebook’s users (and around 95% of the world’s population) are located outside the United States and Canada.[40]

Facebook’s Gains from Engaging with the Rule of Law

In 2018, in the face of seemingly endless scandal and controversy, the very act of Zuckerberg’s publicly imagining[41] and Facebook’s publicly designing and establishing Oversight Board altered, for a time and quite instantly, the public conversation around Facebook.[42] The creation of Oversight Board allowed Facebook to distance itself from the Cambridge Analytica scandal. Further, Oversight Board had given Facebook a basis to speak somewhat credibly on principles of the rule of law and on international human rights, both languages that enjoy considerable legitimacy at the international level, particularly in European and Indian courts (two forums controlling important markets for Facebook). Moreover, through Oversight Board, Facebook has added to “team Facebook” 20 established and respected international scholars, all of whom are charged to critique Facebook with the sole aim of protecting the integrity of Facebook’s most vital business asset, its global community of users.

In providing a transparent government-free procedure for ostensibly independent review of a small selection of its content decisions, Facebook has also deployed the language of human rights to the satisfaction of conservative American sensibilities.[43] For example, Casey Mattox, senior fellow at the Charles Koch Institute, argues that a self-regulatory body such as Oversight Board protects Facebook from politicians “trying to impose their own partisan will on the platforms.”[44] Moreover, Oversight Board currently counts John Samples, Vice-President of Libertarian think tank the CATO Institute, as a board member. Samples sits on the board alongside board members who are well-known progressive stalwarts.[45]

In addition to (and perhaps because of) Oversight Board’s bewildering constellation of voices from across the political spectrum, at a more pragmatic level, passing the proverbial buck on content decisions to Oversight Board has allowed Facebook to alter the nature of the scrutiny it receives, since with respect to any action taken by Oversight Board, criticism of Facebook’s conduct becomes, equally, an indictment of Oversight Board’s diverse, eminent, and expert panel.

The Limitations of Facebook’s Engagement with the Rule of Law

Oversight Board’s detailed attention to the rule of law and international human rights notwithstanding, Oversight Board’s structure enables Facebook to avoid serious questions about its ethical responsibilities to its users and the general public. As critics have pointed out, one challenge is that through Oversight Board, Facebook has subjected only a narrow sliver of its content decisions to the discipline of the rule of law. In its first year of operation, the board culled through more than 500,000 requests from users to examine Facebook’s content moderation decisions, taking on 20 cases and issuing 15 decisions. This means that, in essence, Oversight Board’s board has overturned Facebook’s disputed content decisions 11 out of 500,000 times,[46] based on extended consideration of only 0.004% of appeal requests. Notably, the board has not been transparent about how it determines which decisions to review.

Moreover, Oversight Board’s narrow focus on user-generated content has allowed Facebook to avoid much harder conversations about long-standing problems with Facebook’s back-end operations. For example, by design, Oversight Board is not able to comment on the algorithms that Facebook uses to organize and display user content or the balance that Facebook sets between user engagement and community safety. In other words, Facebook seems to have left its most fundamental speech-related business decisions completely beyond the reach of Oversight Board, leaving those paid experts sheltered in a limited liability shell with only its most downstream, politicized, and public-facing controversies on disputed user-generated content.

Reinforcing Facebook’s dominance over Oversight Board, Facebook has already proved reluctant to cooperate with Oversight Board, even within the narrow field of Oversight Board’s authorized activities. For example, Facebook refused to answer several key questions from a board that it personally curated less than one year ago. In reviewing Facebook’s ban of former US President Donald Trump from the Facebook platform, the board

sought clarification from Facebook about the extent to which the platform’s design decisions, including algorithms, policies, procedures and technical features, amplified Mr. Trump’s posts after the election and whether Facebook had conducted any internal analysis of whether such design decisions may have contributed to the events of January 6.

The board reported that Facebook declined to answer these questions, making “it difficult for the [b]oard to assess whether less severe measures, taken earlier, may have been sufficient to protect the rights of others.”[47] Facebook’s narrow construction of Oversight Board, its continued refusal to acknowledge its obligations to cooperate with the board’s fact-finding, and Facebook’s deliberate refusal to operate transparently with respect to its back-end operations raise significant questions about the sincerity of Facebook’s commitment to truly independent oversight based on principles of the rule of law.

The Facebook Files and the Limitations of Oversight Board

The benefit to Facebook in limiting Oversight Board’s scope and power have come to light through a recent document leak. In September 2021, for the first time since the creation of Oversight Board, Facebook became the subject of significant public controversy once again. This time, a whistleblower and former Facebook employee, Frances Haugen, leaked thousands of internal Facebook documents that revealed a considerable range of Facebook’s most predatory practices (the “Leak”). These predatory practices include Facebook’s practice of exempting high-profile users from its ordinary community standards;[48] Facebook’s concealment of research on Instagram’s uniquely harmful effects on teenage girls;[49] and Facebook’s willingness to prioritize user engagement at the cost of user health and personal well-being.[50]

Less than two weeks after news of this Leak, the board’s current Co-Chairs—Catalina Botero-Marino, Jamal Greene, Michael McConnell, and Helle Thorning-Schmidt—authored a narrowly formulated response, posted to the Oversight Board website.[51] The response focused solely on the content-moderation aspects of the Leak, characterizing these as “new information…on Facebook’s ‘cross-check’ system, which the company uses to review content.”[52] Framing the Leak as evidence of the need for greater transparency at Facebook, the board additionally listed examples of policy recommendations it had made to Facebook in the interests of increased transparency. For example, the board had warned, in its decision concerning Trump’s Facebook accounts, that a lack of clear public information on Facebook’s policies regarding its high-profile users could contribute to perceptions that Facebook is unduly influenced by political and commercial considerations.[53] The board pointed out that it had also warned Facebook about the danger of removing user content with little explanation, also pointing out that it had recommended in three of its first five decisions that Facebook tell users the specific rule that triggered removal of their content.[54]

While the board’s response was prompt and detailed, it was so narrowly formulated that it stood disconnected from the very same events it sought to address. First, the board is limited to speaking about Facebook’s user-generated content and content policy. As such, the board addressed the issues of content moderation raised by the Leak with laser focus, while avoiding even so much as a mention of any related issues that provided context, such as concerns about Facebook’s harmful use of algorithms. Second, and more concerningly, the board’s response subtly reframed the narrative around Facebook. For example, what credible news outlets refer to as Facebook’s problematic and deliberate deference to high-profile users, the board describes as the product of “perceptions” of undue influence created by policies in need of review.[55] As an additional example, what Haugen, an independent whistleblower, describes as a company that has made a practice of magnifying and profiting from the worst in human nature,[56] the board instead characterizes as a company that would benefit from being more transparent about its activities and from taking the advice of the board seriously.[57] Notably, Oversight Board offers no basis, textual or otherwise, for these characterizations of Facebook’s motivations and circumstances. Third, the board makes no direct reference to the Leak (referring to it as a “disclosure”), and makes no commitment to review the more than 1,000 documents that were placed on the public record in the public interest. The board merely commits to seeking further information from Facebook and addressing Facebook’s continued failures to be forthright in its dealings with Oversight Board.

Ultimately, the board’s response to the Leak reflects deliberate limitations placed on the scope of Oversight Board’s work and purpose. These limitations, in turn, stem from Facebook’s long-standing assumptions about how social media companies should be regulated. Before the appointment of a single board member, Facebook had already taken a clear position on what aspects of its social media platform should be subject to external regulation: harmful user-generated content, online activity that threatens the integrity of elections, privacy, and data portability.[58] Simultaneously, Facebook has also worked to shield its algorithms and other aspects of its back-end operations from public scrutiny and regulatory zeal.[59] Oversight Board was structured accordingly, as a $130 million project focused tightly on expert-led self-regulation of a narrow line of Facebook’s content moderation decisions. This tight structure leaves very little room to a board of experts to independently consider what effective oversight might look like.

No Court for Facebook

While even lawyers have been willing to claim that Oversight Board is comparable “to an international human rights tribunal or quasi-judicial monitoring institution,”[60] as a private activity funded and established by a single corporation, Oversight Board cannot fairly be described as (or even as similar to) a court or tribunal, simply because it publishes ordered opinions that reference the principles of rule of law and international human rights. The entity deals with a very narrow slice of appeals to Facebook’s content decisions, operating through a framework narrowly tailored by Facebook to address an even narrower pre-determined set of concerns. Even in its processing of such appeals, the board has struggled to gain information and cooperation from Facebook, an entity that has (as the creator of Oversight Board and the settlor of the Oversight Board Trust) far more power and control over the broader context of the board’s decision-making process than any “party” to a dispute should be granted.

As illustrated by the board’s recent response to Facebook’s latest controversy, the narrow ambit of Oversight Board’s work prevents it from engaging with Facebook on fair and equitable terms. The board relies on Facebook for its corporate fact finding and implementation of its policy decisions. By contrast, given the narrow scope of the board’s work, Facebook relies on the board for very little that the board is not obligated to provide. There is a power inequality between the board and Facebook that could not have existed if Facebook had truly granted Oversight Board anything remotely comparable to the authority of a court or tribunal. Oversight Board’s narrowly tailored scope seems to suggest that board members are simply playing out a role designed for them by Facebook. Even if board members fulfill this role with independence and integrity (as one can only assume that they do), their personal independence and integrity is not sufficient to deem the entire structure truly independent.

In the final analysis, there is little value in thinking of Oversight Board as a court, tribunal, or even an independent body. It is something far more interesting. It is an experiment at the cutting edge of technology and the rule of law—one that Facebook has carefully crafted to replicate a precise model of regulation of social media that the company seeks to advance.

Compare Oversight Board to another experiment in social media regulation. Twitter Chief Executive Jack Dorsey has also been experimenting for solutions for self-regulation of social media platforms. Unlike Facebook, Twitter seeks to give users more “algorithmic choice” to decide what they see. To pursue this strategy, Dorsey set up an employee-funded project called “BlueSky.” Invoking a different set of principles than those relied upon by Oversight Board, BlueSky emphasizes users “governing” themselves rather than being governed by companies (e.g., Facebook or Oversight Board). Using federalism[61] as a point of reference, BlueSky invokes the term “fediverse” to describe a de-centralized network that “hands control back to the user, who can choose the app that best suits their needs and still have the freedom to interact with users on different apps.”[62]

Facebook and Twitter could not be more different as social media platforms. Facebook has approximately 2.8 billion users located across the world, with the bulk of its users located outside of the United States and Canada.[63] Twitter has a few hundred million users, most of whom are highly educated, high-income Americans.[64] Regulation that supports one company is likely to destroy the other. For example, Twitter’s fediverse would allow people to interact with Facebook users without having to join the Facebook platform, a change comparable to how e-mail platforms like Hotmail “freed” users from reliance on email attached to paid platforms like America Online. In contrast, the thought of an unelected 20-member interdisciplinary board reigning over content decisions that impact 2.8 billion people, without any oversight of the back-end decisions organizing that content, would probably have Twitter’s highly active and highly informed customer base up in arms. As such, the threat of regulation presents considerable stakes for all companies involved.

As things stand, the situation remains unpredictable. As Oversight Board continues to engage with Facebook and the public, it could build weight for Facebook that might create a more balanced power dynamic between the two entities in the future. The board’s work thus far presents a display of the long-term potential that Oversight Board might offer Facebook in this regard. First, the board can do what Facebook cannot: it can openly acknowledge and publicly address Facebook’s scandals. Second, in so doing, by consistently addressing issues along the single axis of content moderation, the board can take control of the narrative building around Facebook scandals. For example, in its response to the recent Leak, the board characterized Facebook’s failures as stemming from a lack of transparency, rather than from what the Press had labeled deliberate predatory behavior. Third, the board has shown itself well-positioned and adequately incentivized to work with (rather than against) Facebook to address these problems, as the public perception of the board’s effectiveness depends upon its ability to provoke genuine change in Facebook’s corporate practices. On the basis of these strengths, Facebook might eventually find genuine value in cooperation with its advisory entity and support it to build capacity that more closely resembles that of a true court or tribunal. Alternatively, Facebook might find itself satisfied or frustrated with the experiment and move on to greener pastures.

Fundamentally, Oversight Board is not one thing or the other, certainly not yet. At present, it is a vessel, an experiment with various kinds of potential, potential that is itself yet unknown. What it becomes will depend greatly on how it is received, how it is understood, and how it is explained—and this depends, most centrally, on the work of business lawyers.

[34] International Covenant on Civil and Political Rights Art. 19, Dec. 16, 1966, 999 U.N.T.S. 171 (1978).

[35] Oversight Board Charter, Art. 2, § 2 (“For each decision, any prior board decisions will have precedential value and should be viewed as highly persuasive when the facts, applicable policies, or other factors are substantially similar.”).

[36]See, e.g, Michel Rosenfeld, Constitutional adjudication in Europe and the United States: paradoxes and contrasts, 2 I-CON 633 (2004) (citing Louis Favoreu, Constitutional Review in Europe, in Constitutionalism and Rights: The Influence of the United States Constitution Abroad 38 (Louis Henkin & Albert J. Rosenthal, eds., 1989)).

[47] Case decision 2021-001-FB-FBR, Oversight Board, May 5, 2021, https://oversightboard.com/decision/FB-691QAMHJ/. The board asked Facebook 46 questions. Facebook declined to answer seven entirely, and two partially.

[53] Case decision 2021-001-FB-FBR, Oversight Board, May 5, 2021, https://oversightboard.com/decision/FB-691QAMHJ/. The board asked Facebook 46 questions. Facebook declined to answer seven entirely, and two partially.

The governance bells are tolling for corporate, non-corporate, not-for-profit, governmental and other organizations. Investor and stakeholder demand, regulatory actions, and growing litigation risks are all increasing the focus on management and director responsibilities for effective governance. There is therefore the need to stress test governance structures and examine the viability of the existing checks and balances, to review the increased focus on board governance and oversight responsibilities, and to explore opportunities to create governance structures with a harder edge, while continuing to recognize governance’s often pivotal role in litigation. While exemplary corporate governance practices will never eliminate all occasions for suits, a sound governance structure will enhance the ability to successfully defend those suits to an early resolution through a motion to dismiss or for summary judgment.

The article introduces the importance of effective corporate governance, key points to consider in assessing governance, and resources—including many written by the expert co-authors—for gaining further understanding of these issues.

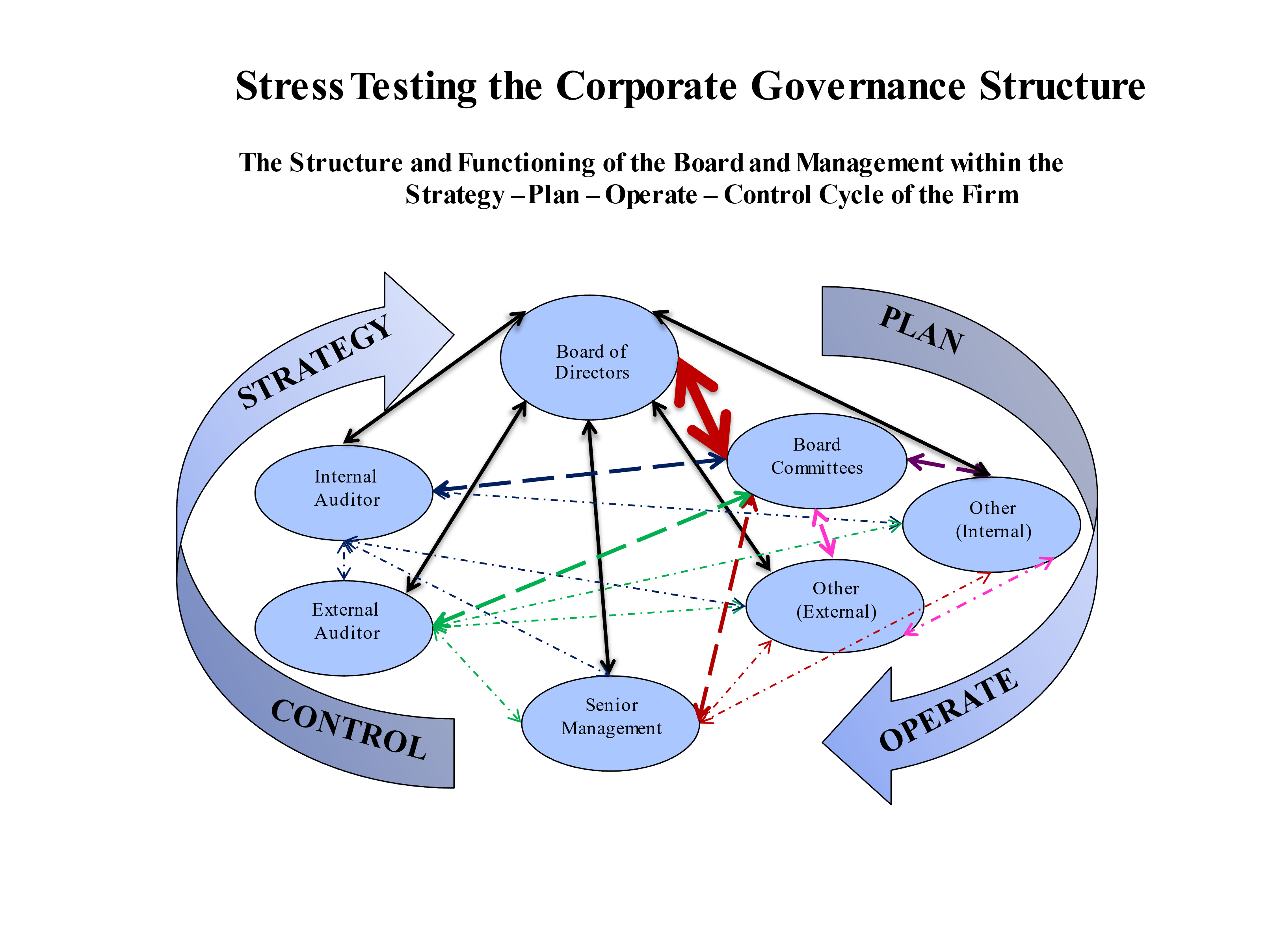

I. Stress Testing Governance Structures: An Introduction

Plan-Operate-Control Cycle

The diagram below sets out the basic governance structure of an organization. Stress testing determines the effectiveness of the governance structure in addressing the needs of the particular firm at that point in time. Stress testing examines how, and how well, an organization’s management and board are directing current operations and are prepared to react to specific risks and challenges, whether those challenges come from business competition, economic events and conditions, regulatory inquiries, changing shareowner expectations, litigation, or other causes.

This is not a middle market situation. The need for effective stress testing is exemplified by the recent breakdowns in the governance structures of Wells Fargo, Volkswagen, Credit Suisse, and Boeing, among others, with this focus on the governance structure going back to the well-known Walt Disney Shareholder Derivative Litigation involving the hiring and the subsequent termination of Michael Ovitz. In Disney, at that time referred to as “the corporate governance case of the century,” the Court made the board’s governance and oversight responsibilities clear, and examined the manner in which Disney management and its board addressed those responsibilities. The Disney litigation was eye-opening to many in the corporate sector because it was previously presumed that the business judgment rule defense would bring a quick end to the litigation. The Delaware Supreme Court did not quite see it that way and remanded the case to the lower court where the derivative suit would be tried on the merits. Ultimately, the Disney directors prevailed, but only after incurring significant legal defense expense. Our February 2019 Business Law Today article “Board Oversight and Governance: From Tone at the Top to Substantive Checks and Balances” examines the difficulties being experienced by the Wells Fargo board in addressing its responsibilities. We have authored four articles on our work in Disney, the first of which was “An Insider Revisits the ‘Disney Case’” (Directors Monthly, August 2008).

“Tone at the Top” vs. Checks and Balances

The long-revered concept of “tone at the top” as the guiding hand of an organization’s governance structure—where tone at the top took the form of a CEO/Chair essentially governing and managing the organization and the board being relegated to oversight—is still valued but now less emphasized. Today, there is broad-based recognition of the need for the appropriate “Checks and Balances” positioned in an environment characterized by transparency. The 2002 CPA Journal article “From Tone at the Top to Checks and Balances” authored by members of the Grace & Co. Board of Advisors, and the 2004 Wall Street Journal op-ed where Paul Volcker and Arthur Levitt Jr. point to the breakdown in checks and balances as the fundamental cause of major corporate collapses, both contributed to this evolving view of governance.

II. Board Governance: The Fed and Wells Fargo; Credit Suisse, Boeing and Volkswagen

One needs only to examine the 2018 Order to Cease and Desist between the Board of Governors of the Federal Reserve and the Board of Wells Fargo, and recent developments concerning Credit Suisse, Boeing and Volkswagen to gain a perspective on the current state of board, board committee and senior management “business” duties to govern, manage and oversee. Indeed, the troubles of Wells Fargo continue, with Senator Elizabeth Warren sending a letter on September 13, 2021, to Federal Reserve Chairman Jerome H. Powell urging a revocation of the bank’s operating license and forcing a break-up splitting the banking operations from Wells Fargo’s other financial and investment services.

Our 2019 article “Board Oversight and Governance: From Tone at the Top to Substantive Checks and Balances,” and the writings of former Delaware Supreme Court Chief Justice Norman Veasey and former Delaware Court of Chancery Chancellor William Chandler further contribute to that perspective that the board of directors will actually direct and monitor the management of the company, recognizing that Delaware law is clear that the business and affairs of a corporation are managed by or under the direction of its board of directors.

Chief Justice Veasey, in his May 2005 University of Pennsylvania Law Review article, stated “the board of directors will actually direct and monitor the management of the company, including strategic business and fundamental structural changes.” Chancellor Chandler, in his opinion in the Disney Shareholder Derivative Litigation, stated, “Delaware law is clear that the business and affairs of a corporation are managed by or under the direction of its Board of Directors.” The Federal Reserve website describes a board’s responsibility to create and enforce prudent policies and practices with the following statement: “Directors are placed in a position of trust by the bank’s shareholders, and both statutes and common law place responsibility for the affairs of a bank firmly and squarely on the board of directors. The board of directors of a bank should delegate the day-to-day routine of conducting the bank’s business to its officers and employees, but the board cannot delegate its responsibility for the consequences of unsound or imprudent policies and practices.”

A recent Delaware case involving Boeing is illustrative of a board’s oversight responsibilities. See In re The Boeing Company Derivative Litigation, 2021 WL 4059934 (Del. Ch. Sept. 7, 2021). This decision from the Delaware Chancery Court arose from the Boeing board’s conduct after two crashes of its 737 Max aircraft and serves as a cautionary tale for directors with regard to the importance of board and executive board committee level oversight and monitoring of “mission critical” product safety risks. Aircraft safety to a company such as Boeing would certainly be a mission critical area.

III. Governance with a Harder Edge

Governance with a harder edge merits consideration. By harder edge, we mean identifying opportunities to ensure board members are informed, involved and have skin in the game; and that the directors understand their responsibilities, are accountable to the organization—not the CEO, and bring an attitude of service and not entitlement to the position. The July 2020 BLT article “Why a Company Should Consider Using an Executive Committee of its Board of Directors” and January 2018 BLT article “Corporate Governance and Information Gaps: Importance of Internal Reporting for Board Oversight” examine the need to put in place governance structures with a harder edge, structures that ensure the voice of the General Counsel is heard. This improved governance positively impacts a firm’s operations; preparations for institutional investor visitations, activist inquiries, and plaintiff firm filings (often supported by litigation funding entities); and the availability and cost of liability insurance.

The current state of the D&O insurance marketplace is what is commonly called a “hard insurance market.” That means premiums for policies are at a relatively high level compared with earlier “soft market” years, and policy terms and conditions may be more restrictive. Also, and perhaps most important, insurance underwriters may look more critically at a risk’s corporate governance in order to select only the more desirable risks for acceptance. Because D&O insurance is frequently the sole or primary funding source in the settlement of securities class action or shareholder derivative litigation, the board and executive management must remain attuned to D&O insurer concerns.

The harder governance edge that exists in certain general partnerships merits examination, and contrasts with corporate governance. In these general partnerships, representatives of the general partners are informed—they understand the business of the partnership; they are involved in the operation of the partnership, and they have skin in the game. They understand their responsibilities, they are accountable back to the general partner they represent and not to the managing general partner, and they bring an attitude of service.

Last fall, the Pro Bono Services Subcommittee of the ABA’s Business Law Section’s Business Bankruptcy Committee presented a program entitled “Helping Those Who Have Borne the Battle: Working with Veterans, Servicemembers, and Their Families on Financial Issues” at the virtual Insolvency 2020 Conference. The program panelists[1] identified tips and several key issues arising in the representation of veterans, servicemembers, and their families, and explained significant changes made to the Bankruptcy Code in 2019.

The Importance of Identifying Clients Who Have a History of Military Service

It is critical for attorneys undertaking pro bono representation to identify clients who have served in the military or who may have family members who have served, because military service could qualify the client for special financial resources and increased legal protections. For example, servicemembers may be eligible for VA disability compensation or VA veterans’ pension, which may be protected income in bankruptcy. In addition, clients with military service could also require special considerations before filing for bankruptcy.

Identifying those who have a history of military service can be difficult, however, because the term “veteran” has different meanings across various state and federal programs and laws, as well as among individuals, and could lead some who have served not to identify themselves as a “veteran”. Instead, the experts recommend that attorneys ask prospective clients, “Have you ever served in the military?” Framing the question in this way can help the attorney identify whether the client might be eligible for service-related benefits and protections, even though the client might not satisfy a particular definition of the term “veteran.” Because service-related benefits and protections might also be available to, for example, certain family members, loved ones, and household members, it can also be helpful to frame the question even more broadly.

Specific Legal Protections and Benefits

Attorneys should generally be aware of the specific military service-related legal protections and benefits available in their jurisdiction. Some common protections and benefits are:

Servicemembers Civil Relief Act (SCRA)

Chapter 53, Title 38: Special Provisions Relating to [Veterans’] Benefits

VA Health Care

VA Disability Compensation

VA Veterans Pension

Soldiers’ Homes

Forever GI Bill

Vocational Rehabilitation

Pre-Bankruptcy Considerations

Attorneys should also keep pre-bankruptcy considerations in mind prior to and throughout representation, including:

Benefit overpayment disputes, waivers, and payment plans

Currently not collectible (hardship) status with taxing authorities

Military discharge status (and whether it can be upgraded or corrected)

Unusual issues:

Impact of debts and bankruptcy on a servicemember’s Security Clearance

Impact of bankruptcy upon future use of VA Home Loan Guaranty benefits

Possible nondischargeability in bankruptcy of fraud-related VA benefits overpayment

Recent Legislation: HAVEN Act

Attorneys should keep apprised of new developments in the Bankruptcy Code, such as the Honoring American Veterans in Extreme Need Act (the “HAVEN Act”),[3] that can help current and former servicemembers, among others, filing for bankruptcy.

In 2018, the American Bankruptcy Institute (“ABI”) created the Task Force on Veterans and Service Members Affairs. The Task Force sought to eliminate some of the underlying financial factors that contribute to suicide rates among those who have served. The Task Force targeted specific portions of the Bankruptcy Code that put servicemember and veteran disability benefits at risk.

The Task Force’s efforts culminated the HAVEN Act, a piece of bankruptcy reform legislation that amended 11 U.S.C. § 101(10A)—the definition for “current monthly income”—to exclude disability payments received from the U.S. Department of Defense and the U.S. Department of Veterans Affairs from the current monthly income calculation.[4] As a result, it is substantially easier for current and former servicemembers (among others, including family members who receive qualifying benefits) to keep those benefits while retaining eligibility for relief under the Bankruptcy Code.

Serving Those Who Have Served

More work to support servicemembers and their families is needed. You can find volunteer opportunities and more information at these sites:

[1] Judge Elizabeth S. Stong, U.S. Bankruptcy Court for the Eastern District of New York, Co-Chair of the Pro Bono Subcommittee of the ABA Business Law Section’s Business Bankruptcy Committee; Judge Mary Grace Diehl U.S. Bankruptcy Court for the Northern District of Georgia; (Army Lieutenant Colonel) Kristina M. Stanger, partner at Nyemaster Goode, P.C. law firm (Des Moines, Iowa); and Jessica H. Youngberg, Law Clerk, U.S. Bankruptcy Court for the District of Massachusetts.

[3] Pub. L. No. 116-52 (codified at 11 U.S.C. § 101(10A)(B)(ii)(IV)).

[4] The statute reads in relevant part, “…any monthly compensation, pension, pay annuity, or allowance paid under title 10, 37, or 38 in connection with a disability, combat-related injury or disability, or death of a member of the uniformed services…” The payment source and basis are key (Title 10 – Armed Forces; Title 37 – Pay and Allowances of the Uniformed Services; Title 38 – Veterans’ Benefits).

An important part of scaling for start-ups and emerging companies requires strategic use of investment tools. Stock options and warrants, while similar, are distinct forms of equity structures that are often confused. This article is part of our series discussing these strategies in turn and exploring key considerations that start-ups and emerging companies should be considering when issuing either. For further information about stock options, see our article “Stocked up: How start-ups and emerging companies can effectively utilize options to attract and retain talent.”

There has been a significant uptick in the number of start-ups and emerging companies using warrants to close the gap on various transactions. When offered in conjunction with effective negotiation, warrants can incentivize third parties to enter transactions or to agree to more favorable deal terms.

A warrant is an agreement between a company (the “Issuer”) and the holder of the warrant (the “Warrantholder”). Warrants entitle the Warrantholder to purchase shares at a specified price within a predetermined period.

What are Warrants?

Warrants are certificates or other instruments issued by a company as evidence of conversion privileges, options, or rights to acquire shares of the company at a specific price until a fixed expiration date. Since warrants do not typically entitle the Warrantholder to dividends or voting rights, warrants are valuable solely for their profit-earning potential.

Companies commonly use warrants as an inducement to attract investors or leverage favorable deal terms. For example, warrants are frequently used as “sweeteners” to incentivize investors to invest or to incentivize a lender to loan funds at a more favorable interest rate, whether bank financing or venture debt. Companies may also use warrants when entering into strategic relationships or transactions to encourage the other party to enter into the transaction or buy into the company’s long-term success.

Although warrants are similar in structure and serve a similar function to options, the critical difference is that options are typically issued to internal stakeholders, such as employees, directors, consultants and other service providers, and not to external third parties. Further, as options are typically issued under an option plan, the issuance of these options would need to conform to the terms of that plan. On the other hand, warrants are typically offered to external third parties as described above.

The issuance of a warrant is usually evidenced by way of a document called a warrant certificate. A warrant certificate sets out the essential terms of the warrant, including:

the exercise price, the number of underlying shares into which the warrants are exercisable and the term of the warrant;

procedures and conditions for exercising the warrant; and

adjustment provisions intended to protect the value of the warrant.

Key Considerations when Issuing Warrants

Types of Shares

Before issuing warrants, start-ups and emerging companies must first determine the type of underlying security the Warrantholder will have the right to acquire. In most instances, warrants are issued for common shares. However, in some instances, the Warrantholder may be entitled to preferred shares. When issued to investors as a “sweetener,” the underlying security will typically match the shares purchased by the investor. For example, outside investors, such as venture capital funds, will commonly only invest if the company is issuing preferred shares that have specific rights, privileges and preferences compared to the common shares.

Number of Shares

The number of shares underlying the warrant may be fixed or expressed as a formula. A formulaic approach to calculating the number of shares the Warrantholder may acquire can be a valuable tool to incentivize a third party, such as where the Warrantholder is a strategic sales channel partner. Therefore, the warrant could be structured so that the sales channel partner would have the right to purchase additional shares if the sales channel partner meets specific sales targets. In addition, a formulaic approach may also incentivize a lender to loan additional funds under an existing credit facility. The number of shares the lender may acquire may increase if the start-up or emerging company borrows additional funds. However, when using a formulaic approach or fixed percentage warrants, start-ups and emerging companies must carefully consider the dilutive effects of any mechanisms that allow for an increase in the number of shares a Warrantholder may acquire.

Alternatively, a company may issue warrants to an investor that will allow the investor to purchase a fixed percentage of shares equal to a fixed percentage of the outstanding equity securities at the time of exercise. Fixed percentage warrant generally does not require price-protection anti-dilution provisions (discussed below). As the number of shares the Warrantholder can purchase is calculated at the time of exercise, fixed percentage warrants can disproportionately impact other shareholders of the company, including its founders, if the company issues additional shares prior to exercise by the Warrantholder of the fixed percentage warrant. Any start-ups and emerging companies that are considering issuing fixed percentage warrants should determine whether there will be any inadvertent consequences of doing so and should consider if fixed percentage warrants should expire prior to a specific event, such as the company’s next round of financing.

Exercise Price

The exercise price (the “Strike Price”) of a warrant is the price of each share underlying the warrant. The Strike Price of a warrant can vary dramatically depending on the context in which the warrant will be issued. In certain circumstances, companies will set the Strike Price at or above the fair market value of the underlying securities. In other circumstances, the Strike Price will be set at a nominal value, which are typically called “penny warrants.” The Strike Price could also be calculated based on a predetermined formula or based on the future valuation of the start-up or emerging company.

Anti-dilution

The warrant may be subject to anti-dilution provisions, which are intended to protect the Warrantholder’s right to receive the value that was negotiated at the time of issuance of the warrant. Certain corporate actions taken by the Issuer during the term of the warrant may have a dilutive effect on the value of the underlying securities, such as consolidation of the company’s outstanding shares or distribution to shareholders of additional shares by way of dividend. A down round may also trigger price-protective anti-dilution provisions—this occurs where the company issues shares at a lower price per share than had been sold in a prior round. For price-protective anti-dilution provisions, the formula used to determine the manner in which the warrants will be adjusted is often a negotiation point.

Start-ups and emerging companies must carefully consider how a down-round will impact the warrant terms. Anti-dilution provisions may adjust the Strike Price and/or the number of underlying shares that are exercisable. The adjustment should be proportionate and reflective of the triggering event and place the Warrantholder in substantially the same position but for the triggering event. Both the Warrantholder and the emerging company must carefully consider how any anti-dilution provisions are drafted. This includes ensuring that there are appropriate carve-outs for predetermined events—such as equity issued as compensation—that do not inadvertently trigger the anti-dilution provisions.

Term

Warrants are exercisable up until a specific time, often referred to as the expiration date or maturity date. The term will depend on many factors, including the nature of the deal. Generally, a longer term increases the value of the warrant because there is a greater likelihood of the company’s success over time and, therefore, a more significant payout as the shares appreciate.

The term may be subject to adjustment provisions if certain fundamental changes are undertaken by the Issuer during the term of the warrant. For example, triggering events for term adjustment provisions may include an amalgamation, merger or disposition of the Issuer’s assets. In the case of these events, the term of the warrant may accelerate so that each outstanding warrant will, after the completion of such an event, be exercisable for the kind and amount of shares that the Warrantholder would have otherwise been entitled to receive immediately prior to the effective date of the event.

When determining the term of the warrant, start-ups and emerging companies must do so in the context of their growth strategy. As discussed above, the type of warrant and its terms may also need to be considered when establishing the expiration date of any warrant.

Exercise of Warrants

Most warrants will be freely exercisable in whole or in part by paying the cash exercise price. Some warrants also allow for what is called a “cashless exercise.” Cashless exercise entitles the Warrantholder to apply the exercise price against the aggregate value of shares it will receive. This is achieved by decreasing the number of shares the Warrantholder will receive by an amount equal to the exercise price that the Warrantholder would have been required to pay for exercising its warrants.

Conclusion

If used correctly, warrants can be a useful tool to incentivize investors and secure critical relationships with customers, buyers, sellers, and partnerships. However, start-ups and emerging companies must carefully consider the warrant terms to ensure they effectively support their long-term growth.

In mid-June, as we all started thinking that the pandemic was winding down, I stepped into my role as president of the International Women’s Forum (IWF) of Chicago. IWF is an international network of women leaders from across sectors that includes CEOs, entrepreneurs, artists, academics, film stars, and even prime ministers and presidents. It is a group of women who work to advance women’s leadership and equality worldwide.

I was humbled to be stepping into this role and excited to lead through a year of recovery and celebration over our collective defeat of COVID-19. I looked forward to bringing lessons of leadership and agility from my law firm and the legal profession more broadly to my new position. Instead, I am monitoring changing regulations and commiserating with women across the globe as COVID numbers rise.