On December 8, 2020, the U.S. Supreme Court heard oral arguments in Facebook, Inc. v. Duguid, a case that should establish a nationwide standard for the “autodialer” definition adopted by the Telephone Consumer Protection Act (TCPA). The Court must resolve a split among federal appellate courts regarding that definition. While predicting the outcome of Supreme Court decisions based on oral argument is a risky venture, the likelihood of a decision in Facebook’s favor, with a narrower “autodialer” interpretation, seems greater than a decision supporting Duguid.

The U.S. Court of Appeals for the Ninth Circuit, the appellate court that issued the most recent opinion in Duguid, adopted an expansive view of the autodialer definition. According to this view, equipment can be regulated as an autodialer if it is capable of automatically dialing telephone numbers from a stored list, even in the absence of random or sequential telephone number generation. At least two other federal appellate courts have adopted this interpretation.

Three, and arguably four, federal appellate courts have adopted a narrow view of the autodialer definition, limiting it to equipment with the capacity to store or produce telephone numbers to be called, using a random or sequential number generator.

All federal appellate courts that have addressed this issue seem to agree that the TCPA’s autodialer definition is frustratingly imprecise. As a result, these courts, as well as the attorneys representing Facebook, Duguid, and the United States at oral argument, have had to channel their advocacy for one interpretation or another between a rock of grammatical rules and a hard place of congressional intent from 1991. The grammatical puzzle is whether the definition’s reference to random or sequential number generation applies to both the capacity to store telephone numbers and the capacity to produce them (the narrow interpretation, favoring defendants), or whether it applies only to the latter (the broad interpretation, favoring plaintiffs). At oral argument, both sides claimed to have grammar on their side.

The challenge regarding congressional intent from 30 years ago is to determine how to apply the TCPA to technology that no one in Congress at the time was contemplating, such as smartphones. Several justices signaled their sense that the TCPA had exhausted its useful life as a regulator of the everyday technology around telephone calls. At the same time, no justice offered a strong defense of the TCPA’s consumer privacy purpose.

The justices were clearly concerned about the prospect that the Ninth Circuit’s expansive autodialer interpretation could result in TCPA lawsuits arising from people’s routine smartphone use. Under the expansive approach, equipment can be regulated as an autodialer if it has the capacity to store numbers and dial them automatically. Justice Alito noted that this sounded like call-forwarding technology, while Justice Barrett made the more modern observation that iPhones come equipped with the ability to autoreply to calls when someone is driving or does not want to be disturbed.

Interestingly, Duguid was represented at oral argument by Bryan Garner, the co-author with Antonin Scalia of Reading Law: The Interpretation of Legal Texts, a popular book regarding statutory interpretation. This could be seen as an attempt to win over the Court’s bloc of justices who purport to be guided by a statute’s text above other considerations. Garner did his best to defend the expansive interpretation as the most sensible reading of the text, but he did not appear to have won over a majority of the Court. He had an even harder time convincing the Court that ordinary smartphone use would not attract TCPA lawsuits under the expansive view.

As noted at the outset of this article, we should all be cautious about guessing the outcome of Supreme Court decisions based on oral argument. Having said that, this article’s prediction is a majority opinion in Facebook’s favor, making the case that it is time to retire the TCPA and replace it with modernized standards regulating the way we communicate by phone today.

The COVID-19 pandemic has been a global shock to businesses everywhere. Uncertainty about its path, duration and magnitude has wreaked havoc on many of our commercial clients. The associated government-mandated shutdown orders have drastically impacted businesses’ ability to make timely rental payments.

The Bankruptcy Code does not generally allow debtors to unilaterally abate or modify the terms of their property leases. However, Congress may enact legislation amending the Bankruptcy Code in order to provide bankruptcy courts additional tools to offer rent relief to debtor-tenants. Congress enacted the Consolidated Appropriations Act, 2021 (“CAA”), an approximately $2.3 trillion omnibus appropriations bill, which was signed into law on December 27, 2020. The CAA not only funds the federal government, but also provides additional COVID-19 relief for businesses and individuals. Significantly, the CAA includes nine amendments to the Bankruptcy Code, three of which directly impact commercial debtor-tenants.

This article aims to educate business law practitioners on how their commercial clients can get much needed rent relief based on case law and/or these newly enacted amendments. First, we explore how courts have provided rent relief to commercial debtors based on:

a force majeure clause in a tenant’s lease,

temporary suspension of a bankruptcy case, or

equitable rent relief.

Next, we review how the CAA amends Bankruptcy Code sections 365(d)(3), 365(d)(4), and 547 to extend the deadlines to perform rental obligations, assume or reject a lease, and preclude preference claims with respect to certain payments of rental arrearages. The amendments to section 365(d)(3), allowing courts to extend the time for performance under a commercial lease, are limited to subchapter V small business debtors. The other two amendments apply to all debtors. All three amendments have a two-year sunset.

A. Courts Considering Rent Relief Based on Lease Terms and Bankruptcy Code

The Bankruptcy Code generally requires a debtor in bankruptcy to pay its rental obligations during the bankruptcy case. Notwithstanding this requirement, at least one court has relied upon a force majeure clause in a lease to offer rent abatement during bankruptcy. The Bankruptcy Court for the Northern District of Illinois in Hitz Restaurant Group found that the Illinois governor’s executive order limiting restaurant capacity triggered the lease’s force majeure clause.[1] The landlord had sought to enforce the obligation of the debtor to pay post-petition rent under section 365(d)(3) of the Bankruptcy Code. The debtor argued its obligation to pay post-petition rent was excused by the lease’s force majeure clause. The court agreed with the debtor in part, allowing a 75% rent abatement in proportion to the percentage of floor space restricted by the ban on dining at the restaurant. It is worth noting that while the specific lease at issue contained language offering potential for relief, other leases may not. The lease in Hitz Restaurant Group included “governmental action” and “orders of government” provisions in the force majeure clause. Moreover, other leases may explicitly exclude rent obligations from the scope of obligations excused by force majeure events. What do your clients’ leases say? Can you amend the lease to include favorable language?

Other courts have looked to the Bankruptcy Code to grant rent relief for debtor-tenants. Section 365(d)(3) of the bankruptcy code requires timely payment of post-petition rent, but allows courts to extend the time for performance, for cause, up to 60 days following the petition date.[2] Yet some bankruptcy courts have used Bankruptcy Code sections 105 and 305 to defer payment of post-petition rent beyond the first 60 days of the case.[3] In Modell’s Sporting Goods, the Bankruptcy Court for the District of New Jersey granted the debtors’ request to temporarily suspend the bankruptcy case, and defer rent payment, pursuant to sections 105(a) and 305(a).[4] The bankruptcy case commenced on March 11, 2020, and two days later, the COVID-19 pandemic was declared a national emergency.[5] The debtors subsequently requested an “Operational Suspension” of the bankruptcy case, including rent deferment, due to COVID-19-related disruptions to the planned liquidation sales of the debtors’ stores. The court found that it was in the best interest of the debtors and creditors to grant the requested relief. The court extended the suspension twice—it ultimately lasted until June 15, 2020—due to the continued impact of stay-at-home orders on the ability to conduct going-out-of-business sales. To what extent do the current COVID-19-related governmental orders impact the progression of your clients’ Chapter 11 cases?

Similarly, in Pier 1 Imports, the Bankruptcy Court for the Eastern District of Virginia granted the debtors’ request for a “breathing spell” to allow some debtor-tenants to defer rental payments pursuant to the court’s equitable power under section 105(a).[6] The court “recognize[d] the extraordinary nature of the relief,” but found that the court’s “broad equitable powers” allowed such relief, notwithstanding section 365(d)(3) requiring timely performance of rental obligations and the limits on bankruptcy courts’ equitable powers.[7] The court explained that “[d]eferring rental payments during an unprecedented financial crisis in order to provide a post-Petition Date ‘breathing spell’ for the Debtors is not inconsistent with similar relief the bankruptcy process otherwise provides for pre-Petition Date obligations.”

Notably, the Bankruptcy Court for the Southern District of Texas rejected similar arguments for rent relief. In CEC Entertainment, the court denied the debtors’ motion to abate or reduce their rent obligations, notwithstanding the impact of COVID-19 in curtailing the debtors’ ability to operate key aspects of its business (operating a nationwide chain of Chuck E. Cheese venues).[8] The court found nothing in the Bankruptcy Code nor in state law or the lease’s force majeure clauses permitting rent abatement. The CEC Entertainment court disagreed with Pier 1 Imports, explaining that it could not override section 365(d)(3)’s unambiguous requirement of timely performance of obligations under commercial leases. The court cited to Law v. Siegel, a United States Supreme Court opinion explaining that a bankruptcy court’s equitable powers under section 105(a) are limited by the express provisions of the bankruptcy code, and section 365(d)(3) “expressly prohibits delays beyond 60 days after the order for relief.”

B. The CAA Amends the Bankruptcy Code to Offer Rent Relief to Commercial Debtors

Some courts have found creative avenues in the Bankruptcy Code or force majeure clauses to offer rent relief to commercial debtor-tenants struggling as a result of the COVID-19 pandemic. Sometimes, however, creative lawyering will not work, as reflected by the recent CEC Entertainment decision finding that section 365(d)(3) limits bankruptcy courts’ flexibility in crafting rent relief beyond the first 60 days of a case. The recent enactment of the CAA, however, has expanded bankruptcy courts’ discretion to grant relief regarding commercial leases.

First, the CAA amends section 365(d)(3) to allow courts to extend the time for performance of lease obligations beyond the normal extension period, but only in a subchapter V case. Generally, a debtor operating in bankruptcy must timely perform all obligations under an unexpired lease of nonresidential real property.[9] Section 365(d)(3) allows a court to extend, for cause, the time for performance—but not beyond 60 days after the petition date. The CAA, however, extends the potential relief period by an additional 60 days—for a potential total of 120 days— only for certain small business debtors filing under subchapter V of Chapter 11.[10] Where a subchapter V debtor is experiencing or has experienced a material financial hardship due, directly or indirectly, to the COVID-19 pandemic, a court may extend the time for performance of commercial lease obligations for 60 days after the petition date. “What’s new” here is that the CAA allows courts to extend the relief period by an additional 60 days for subchapter V debtors if such a debtor continues to experience material financial hardship due, directly or indirectly, to the COVID-19 pandemic. Further, if an extension is granted for an obligation, the obligation is treated as an administrative expense that has priority for payment in bankruptcy.

Second, the CAA amends section 365(d)(4) to extend the initial deadline for any debtor-tenant—not just those filing under subchapter V—to assume or reject an unexpired lease of nonresidential real property by an additional 90 days to a total of 210 days after the petition date.[11] Section 365(d)(4)(B)(i) already allows the court to extend the deadline to assume or reject a lease, for cause, by an additional 90 days. Therefore, a debtor could potentially have as many as 300 days to decide whether to assume or reject an unexpired commercial lease without the consent of the landlord. Yet, the court may grant further extension upon written consent of the landlord. The CAA includes a two-year sunset after enactment, upon which the above amendments will be struck from the Bankruptcy Code on December 27, 2022. However, the amendments apply to all debtors who file under subchapter V of Chapter 11 prior to the sunset.

Additionally, the CAA aims to incentivize a distressed company’s landlords and vendors to offer flexible payment terms by amending the preference provisions of section 547 to provide that any “covered payment of rental arrearages” cannot be avoided as preferences.[12] “Covered payments” are defined as payments made pursuant to arrangements entered into between any debtor-tenant and their landlord on or after March 13, 2020 to defer or postpone payments owed under a lease; such arrangement may also include the debtor’s obligation to pay penalties or fees. This amendment also includes a two-year sunset, after which it will be struck on December 27, 2022. However, the amendment to section 547 applies in any bankruptcy case commenced prior to the sunset.

Commercial tenants that take advantage of the relief offered under the Bankruptcy Code should be aware that if they decide to assume a lease, they must cure all back rent. Section 365(b) generally requires that a debtor-tenant cure, or provide adequate assurance of prompt cure, of any default under the lease.

C. Conclusion

Recent decisions inform us how courts have been grappling with the Bankruptcy Code’s inflexibility with respect to leases of non-residential real property. The Consolidated Appropriations Act, 2021 offers a measure of relief to debtors experiencing COVID-19-related financial woes by enacting amendments to Bankruptcy Code provisions relating to the treatment of lease . Significantly, the CAA will likely give pause to bankruptcy courts who would otherwise emulate the Modell’s Sporting Goods and Pier 1 Imports courts’ use of sections 105(a) and 305(a) to defer commercial rent obligations beyond the first sixty days of bankruptcy—in contravention of 365(d)(3). By providing for specific and limited rent-deferment relief to commercial debtor-tenants affected by the COVID-19 pandemic, and by limiting the extended relief to subchapter V small business debtors, the CAA expresses Congress’s intent that 365(d)(3)’s requirements for timely fulfillment of rent obligations should otherwise be strictly complied with.

[1]In re Hitz Rest. Grp., 616 B.R. 374 (Bankr. N.D. Ill. 2020).

[3] 11 U.S.C. § 105(a) (allowing the court to “issue any order, process, or judgment that is necessary or appropriate to carry out the provisions of this title”), § 305(a)(1) (allowing a court to “suspend all proceedings in a case” if “the interests of creditors and the debtor would be better served by such…suspension”).

[7]See Law v. Siegel, 571 U.S. 415, 421 (2014) (section 105(a) “does not allow the bankruptcy court to override explicit mandates of other sections of the Bankruptcy Code”).

[10] Under the Small Business Reorganization Act (SBRA) of 2019, Pub. L. No. 11654, 133 Stat. 1079, small business debtors may elect to file under subchapter V of Chapter 11 of the bankruptcy code if their debt does not exceed $2,725,625. The debt limit was increased to $7,500,000 by the Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020, Pub. L. No. 116-136, 134 Stat. 281 (effective March 27, 2020 for a period of one year).

We have been discussing the need for businesses to make public commitments to support equality, diversity, and inclusion (EDI).[1] These three related concepts are essential to a productive and happy workforce and a fair and just society for everyone. Equality comes from equal access to opportunities, free of discrimination. However, the full range of opportunities will only be available when there is respect for diversity and a willingness to include everyone in decisions regarding their lives. A related concept is social justice, which has been described as fair and just relations between an individual and society at large, as measured by the distribution of wealth opportunities for personal activity and social privileges.

Commitments are fine and necessary, but companies must do more by taking steps to embed EDI into their operations, decision making, and organizational culture and by making those values and norms part of the company’s DNA and the guiding principles for its employment policies and other business relationships. Changing the organizational culture is a difficult and challenging process that requires patience and attention to all phases of a worker’s journey through the company and the company’s relationships with customers, suppliers, and the members of the communities in which the company operates. Some of the steps that need to be taken were suggested by the International Labour Organization, which provided guidance on developing a corporate nondiscrimination and equality policy[2]:

Make a strong commitment from the top by signaling that senior management assumes responsibility for equal employment issues and is committed to diversity, thus sending a strong message to other managers, supervisors, and workers.

Conduct an assessment to determine if discrimination is taking place within the organization.

Set up an organizational policy establishing clear procedures on nondiscrimination and equal opportunities and communicating the policy both internally and externally.

Provide training at all levels of the organization, in particular for those involved in recruitment and selection, as well as supervisors and managers, to help raise awareness and encourage people to take action against discrimination.

Support ongoing sensitization campaigns to combat stereotypes.

Set measurable goals and specific time frames to achieve objectives.

Monitor and quantify progress to identify exactly what improvements have been made.

Modify work organization and distribution of tasks as necessary to avoid negative effects on the treatment and advancement of particular groups of workers, including measures to allow workers to balance work and family responsibilities.

Ensure equal opportunity for skills development, including scheduling to allow maximum participation;

Address complaints, handle appeals, and provide recourse to employees in cases where discrimination is identified;

Encourage efforts in the community to build a climate of equal access to opportunities (e.g., adult education programs and the support of health and childcare services).

Set up bipartite bodies involving workers’ freely chosen representatives in order to determine priority areas and strategies, to counter bias in the workplace, and to ensure that all workers are committed to the organizational goals regarding diversity and nondiscrimination.

Iyer and Kirschenbaum noted that the EDI efforts of companies are often carried out separately from the business units that are primarily responsible for market expansion, the quality of customer service, or human resources. They encouraged companies to implement organizational structures and expectations of accountability that embedded EDI into operations, such as forming a permanent EDI working group or team with relevant experience and expertise drawn from throughout the company (e.g., engineers, data scientists, researchers, designers). They also suggested that companies focus exclusively on advancing inclusion and rooting out bias in key activities such as product design, marketing, and customer service. Similarly, hourly employees, women, and people of color need to be given a voice in the creation, implementation, and assessment of all employment-related processes. The working group created to develop the company’s commitments to action regarding racial equality and justice should also be involved in organizational change initiatives.[3]

Ideas about the composition of the EDI working group and the manner in which it carries out its responsibilities can be gleaned from Lee’s suggestions regarding the formation of a staff-led taskforce, working, or committee on EDI.[4] Lee’s first suggestion related to the composition of the group and the need to ensure that it includes a diverse team of employees so that discussions and actions will take into account the wide range of viewpoints throughout the workplace. Certainly, passion for EDI is an important qualification for serving within the group, and anyone who can bring that kind of energy to the issues should be considered. At the same time, an effort must be made to identify underrepresented groups and not only bring them on to the team but also consider why employees might be reluctant to participate. In addition to ensuring that the composition of the group is racially and ethnically diverse, there should be representation from all levels in the organizational hierarchy and from each of the key business groups or departments.

Another suggestion Lee offered was to establish clear goals, roles, and relationships in order to define the group’s scope of work and the way it operates internally and relates to those leaders with the authority to implement the group’s recommended actions. In general, members of the working group will still be expected to fulfill their regular day-to-day responsibilities, and so they will have only limited time to invest in the group’s activities. As such, consensus should be reached on which EDI issues are most pressing for the company. This process should begin with sharing stories and experiences with the members of the group, but the group should also go outside its own boundaries and seek input from other employees. Once the issues have been identified, the group needs to consider its internal and external capacities to do the work necessary to make an impact on each issue (e.g., are there members of the group with specific experience and skills that can be leveraged to develop effective solutions for an issue?) and make decisions about which issues the group can most influence.

Lee’s suggestions were focused on what would initially be a largely volunteer effort organized and supported by the company that depended on employees willing to commit time to the working group, in addition to their other duties to the company. In contrast, Iyer and Kirschenbaum called for companies to form a permanent, full-time EDI working group or team. This would mean that members would be pulled off their previous assignments and be required to spend all of their time working on EDI issues with experienced colleagues from other divisions of the company.[5] The decision depends on a variety of factors, notably the size of the company and the ability of the company to reallocate resources to a full-time group. It might be best to start with a voluntary group, properly staffed and operating with the explicit and public support of the company’s leaders, and then determine how best to integrate the EDI working group into the company’s permanent organizational structure. While having a full-time team working on EDI issues is useful, care must be taken to ensure that the team continues to work well with the relevant departments and business units and that steps are taken to embed EDI directly into those groups.

Racial equality in the workplace cannot be achieved unless and until everyone in the organization appreciates and respects the diverse experiences of their colleagues and understands that diversity and inclusion will lead to a stronger organizational culture, a vibrant working environment. and an engine for innovative products and services that will support a sustainable enterprise. Racial discrimination in the workplace is an extremely sensitive issue that sometimes requires painful personal introspection and difficult conversations. Nonetheless, business leaders need to understand that racism can and will damage their companies in a number of ways. Certainly, racial discrimination will expose the company to potential legal liabilities, but even more corrosive is the role racism can play in dividing the workforce and undermining morale, teamwork, and productivity. In addition, in a world in which news spreads quickly over social media, incidents of racial discrimination can instantly and permanently tarnish a company’s reputation and brand, causing it to lose customers and making it more difficult for the company to recruit, engage, and retain diverse talent.

Racial equity training involves tackling sensitive issues such as internalized racial stereotypes and “unconscious bias,” which may affect decisions made within organizations as well as employees’ communication with one another in the workplace. Training sessions should be set up in ways that promote open and safe discussions about racism. Research indicates that companies that are willing and able to facilitate dialogue succeed in building stronger bonds and greater understanding. It should be expected that white employees who are challenged on their race-related beliefs during the training sessions will act defensively, often expressing emotions such as fear, anger, and guilt. They may also have concerns about how proposed diversity and inclusivity actions might undermine their historical “white privilege” and the opportunities and access to resources they have been accustomed to. Concerns from all sides need to be aired, but debating should be avoided, and all employees, regardless of race, need to clearly understand what is at stake and what their lives in the workplace will be like once changes have been implemented. It is at this point that all employees need to be educated and reassured about the benefits to everyone in the company from setting aside inequitable practices.

Racial equity training alone will not guarantee success, but it is an essential tool for establishing and continuing dialogue. Certain elements of the training need to be mandatory in order to demonstrate that the company has taken steps to ensure that all employees are aware of both their duties under the law and the company’s own internal policies and codes of conduct. Participation in training may also be required by business partners who are generally anxious to avert reputational damage from any association with companies that fail to promote a diverse and inclusive workplace free from racial discrimination. According to the Society for Human Resource Management (SHRM), companies should offer additional training and opportunities for dialogue beyond the mandatory sessions. In addition, SHRM recommends not making attendance compulsory since people who do not want to be there will often undermine the value of the meetings by displaying hostile or defensive actions. The training sessions should be led by experienced facilitators and should begin with an explanation of the ground rules for discussions so that everyone feels comfortable sharing their experiences and opinions. SHRM encourages companies to make learning interactive and experiential, avoiding long lectures from someone in the front of the room at a podium and ensuring that everyone walks out of the room armed with practical steps that they can immediately begin using to overcome unconscious bias.[6]

[1] Alan S. Gutterman is a business counselor and prolific author of practical guidance and tools for legal and financial professionals, managers, entrepreneurs, and investors on topics including sustainable entrepreneurship, leadership and management, business law and transactions, international law, and business and technology management. He is the co-editor and contributing author of several books published by the ABA Business Law Section, including The Lawyer’s Corporate Social Responsibility Deskbook, Emerging Companies Guide (3rd Edition) and Business and Human Rights: A Practitioner’s Guide for Legal Professionals. Alan is also currently a partner of GCA Law Partners LLP in Mountain View, California (www.gcalaw.com). More information about Alan and his work is available at his personal website at www.alangutterman.com. This article is adapted from the chapter on Racial Equality and Non-Discrimination, which was recently released on his website: https://alangutterman.com/wp-content/uploads/2020/07/EDI-_C1-Racial-Equality-and-Non-Discrimination.pdf.

Robert Dickie and Peter Russo’s book, Financial Statement Analysis and Business Valuation for the Practical Lawyer, Third Edition, guides lawyers through key principles of corporate finance and accounting with direction on how to analyze the income statement, balance sheet, and cash flow statements. The guide helps lawyers gain a working knowledge of financial concepts, terminology, and documents and an understanding of basic and advanced techniques of valuing companies.

This is the first in a series of articles intended to provide a working knowledge of financial statements, terms, and concepts, especially as that knowledge is useful in the practice of law. For business lawyers, the language of business is finance, and it pays to be equipped to understand the business dimension as well as the law.

There are three main financial statements—namely, the balance sheet, the income statement, and the cash flow statement. This article will discuss the balance sheet, also known as the statement of financial position. The balance sheet is a “snapshot” of a company’s position at a particular point in time. The report takes a simple approach: at any given moment, what you own (assets) less what you owe (liabilities) is what you are “worth” (shareholders’ equity). It’s important to note that “worth” for financial reporting purposes is very different from the market value of the company. Here, we simply mean worth from a reporting perspective.

Assets are economic resources available for use in the future. Liabilities are obligations to outsiders, and equity is the claim of the owners after the obligations. Expressed as an equation,

More simply, A – L = E. This equation can also be expressed as A = L + E; this is commonly referred to as the balance sheet equation. The balance sheet presents assets on one side, equal to liabilities and equity on the other. Another way to think about the balance sheet is that assets are what the company owns—the resources they have available to use in the future to run the company; liabilities and equity are where the money comes from to buy those resources.

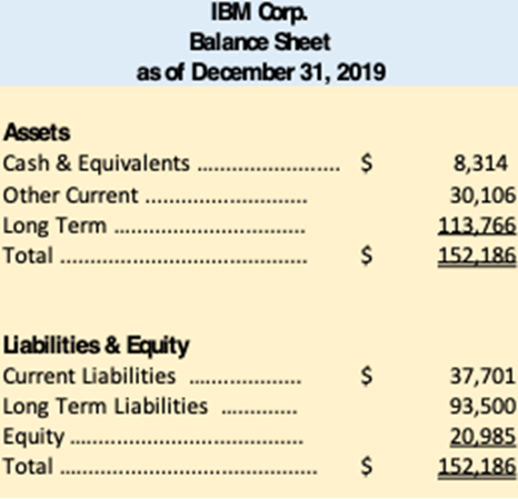

Here is a summary version of IBM’s most recent year-end balance sheet.

Note the time stamp, “as of December 31, 2019.” As of the close of business on December 31, 2019, IBM froze its books to count up where it was. Also note that these numbers are presented in millions of dollars; the cash balance of $8,314 means $8.3 billion of cash.

Assets

Assets are the tangible and intangible resources owned by the company. Almost all asset values are based on the cost to acquire these assets, not the current value of the assets. This is obviously an important distinction and is why we can’t use the reported asset amounts to determine the value of a company. For example, if IBM purchased land 50 years ago for $1 million, it’s still on their balance sheet for that amount, even though today it may be worth exponentially more.

In addition to cash, IBM had other current and long-term assets, amounting to just over $150 billion in resources owned by the company at that point in time. On the bottom half of the balance sheet are the sources for the capital used to acquire and use those resources. A distinction is made between short-term (current) and long-term assets and liabilities; current assets are expected to become cash within the next 12 months, whereas current liabilities are expected to be satisfied within the same 12 months.

The most common short-term assets are cash (and cash equivalents), accounts receivable, and inventory. Typically, the most significant of the long-term assets are “property, plant and equipment” (also referred to as “fixed” assets), goodwill, and intangible assets. There may also be deferred tax assets if the company has paid a tax to the IRS but not yet reflected the expense under the accounting rules.

If a company has goodwill or intangible assets, it is most likely because it has made an acquisition, and the purchase price exceeded the fair market value of the acquired company’s “net assets” (defined as assets – liabilities). With a few exceptions, internally produced intellectual property does not appear on the balance sheet as an asset. Instead, the costs to create the intellectual property are included as expenses on the income statement.

This can be important. For example, a company’s balance sheet may report more liabilities than assets; however, it likely owns economic assets that are not reflected on its balance sheet. Coca Cola’s most valuable asset, for example, is its formula, but that is not on Coke’s balance sheet because the costs to develop it were long since expensed, and GAAP makes no attempt to reflect the fair value of assets.

Sidebar 1: Deferred Taxes

There can be differences between when a company reports taxes for accounting purposes and when it pays them to the IRS. For instance, current tax rules allow a company to depreciate an asset more rapidly on their tax return than they do on their financial statements. This means depreciation expense this year will be higher on the tax return, and taxable income will be less than accounting income, lowering the taxes due this year. This is a temporary difference in taxable income and accounting income; total depreciation expense is the same over the life of the asset, but is allocated differently over the years. This creates a deferred tax liability because expenses have been taken earlier for the tax computation and eventually will have to be paid. Conversely, if the company accrues a workmen’s compensation expense but has not yet made the payment and thus cannot yet deduct the sum on its tax return, then the expense on its income statement will be higher than the deduction on its tax return, and its tax liability will be greater than the tax paid to the IRS. This results in a deferred tax asset for accounting purposes.

It is most important to understand that GAAP accounting rules rely upon significant judgment by management in valuing assets. For example, there are two different methods to value accounts receivable, four different methods to value inventory, and six different methods to value fixed assets. Management is allowed to decide which methods it uses (note that management must consistently apply the method it chooses and can’t change methods year to year). In addition, these methods require estimates of such things as the collectability of receivables, the potential obsolescence of inventory, and the useful life of fixed assets. These are just examples of the inherent judgment involved in all assets, with the exception of cash.

When a company is struggling financially, it is most important to understand what the numbers mean and the context of how the numbers are determined. First, remember that the reported amount of the assets do not purport to be the current market values. Second, management may be so biased as to use the allowable judgment to overstate the value of an asset in order to meet a loan covenant, or understate expenses to improve profit.

In an economic crisis liquidity, the ready access to the cash needed to fund operations becomes a particularly important indicator of a company’s ability to survive. Is the company’s cash position deteriorating, and if so how quickly? Does it have additional sources of cash available? Are the assets really worth as much as the amount reflected on the balance sheet? In considering whether assets are shown at the lower of cost or market value, has management considered current market conditions? (See Sidebar 2.) Might the market value of its assets, less its liabilities, actually exceed the going concern value of the company? If so, should the company consider liquidating its assets and distributing the proceeds to its creditors and shareholders?

When performing due diligence, each asset should be looked at and probed. Have any values been impaired? Are all receivables collectible in the current economic environment? Is inventory all usable, or is obsolescence a concern? Even in the case of buildings, the market values may have declined if there are vacancies or the tenants can’t pay the rent.

Sidebar 2: The Value of an Asset Can Change with Context

During the second quarter of 2020, Delta Airlines recorded an “impairment” charge of almost $2.2 billion. U.S. GAAP requires that the reported dollar amount of an asset cannot exceed its estimated future value to the company. Delta reduced the value attributable to certain aircraft. According to the notes to its financial statements, this write-down reflected the company’s current plans for these aircraft in light of the impact of the COVID-19 pandemic. It’s important to note that this write-down did not imply that these aircraft were in any way damaged or obsolete. The lower value on their balance sheet simply reflects the current situation; they have less utility to the company under current conditions, and their liquidation value is probably impaired at this time as well. What management is doing here is exactly what GAAP requires.

At the same time, management says that it has evaluated the reported value of its goodwill and intangibles and has concluded that those values have not been impaired, meaning that they are worth at least what they are being carried at on the balance sheet. Note that management summarizes the impact of the pandemic on the financial condition and operations of the company in a single note to the financials. Any user of the financial statements would be well advised to read it carefully.

In a crisis, a key first step is to consider the company’s strategy and plans to survive the crisis and then examine the assets from the standpoint of their likely value under that scenario. At the risk of overstating it, the reported value of the assets on the balance sheet, both individually and collectively, should not be mistaken for their market values or their liquidation values in a time of crisis.

Liabilities

Liabilities are obligations of the business. This includes obligations to employees, customers, vendors, and lenders. These are separated into short-term (those due within one year) and long-term liabilities. Liabilities are generally of two types: (1) noninterest-bearing liabilities, and (2) debt, which bears interest and has a due date. The usual short-term liabilities are accounts payable (monies owed to vendors) and accrued liabilities (estimated liabilities). It also includes any principal amounts on debt due in the next 12 months. If a company is in the enviable position of receiving cash from its customers before earning the revenue (like subscriptions paid in advance), the unearned or deferred revenue will be shown as a current liability. The most common long-term liabilities are long-term debt, deferred tax liabilities, lease obligations, and pension liabilities.

One issue that arises for all companies is “contingent” liabilities. These are liabilities that may inure to the company based on some underlying future event. For example, if a company is sued by a customer for a product liability claim, the company will be obligated only if they lose the lawsuit. In this case, the liability is not included on the balance sheet unless it is highly probable that the company will lose the lawsuit and the judgement can be reasonably estimated. Up to that point it may be required to disclose the potential liability in the footnotes, unless it is highly unlikely to lose the suit. The determination of the likelihood of winning or losing is made by management based on information from legal counsel.

Solvency refers to the comparison of a company’s assets with its liabilities. Insolvency means that the accounting value of the liabilities exceeds the accounting value of the assets (because A = L+ E, if liabilities exceed assets, the equity is actually negative). The term “insolvency” can also refer to a company unable to meet its obligations as they come due, though that may also be referred to as “cash flow insolvency” or a “liquidity problem.” This may have significant consequences, such as possible violation of financial or other contractual covenants. Under the corporate laws of many states, if there is balance sheet insolvency, payment of dividends or share repurchases can result in personal liability to directors.

Especially in times of stress, we are concerned about a company’s liquidity—its ability to meet its financial obligations as they come due. The most common measure of liquidity is current assets (those expected to generate cash within the next 12 months) divided by current liabilities (those that will consume cash during that same period). This is called the “current ratio.” However, recognizing that inventory is likely to be of little use in meeting short-term liabilities if revenues are down, a more rigorous measure counts current assets minus inventory in the numerator. That is called the “quick ratio.”

Hopefully, before a company faces either insolvency or liquidity problems, financial covenants provide lenders with an early warning that the situation may be deteriorating and may need attention. Legal counsel should advise their clients to be proactive in communicating concerns about performance against their covenants and to help them negotiate covenants that both take into account expected performance and allow flexibility where warranted.

Equity

Equity represents the claims of the owners on the company. Equity comes in two forms, money invested by the owners (contributed capital) and company-generated profits that are left in the company (retained earnings) and can be used to purchase additional assets, pay dividends, or reacquire shares. As of December 31, 2019, IBM had assets of $152.2 billion and owed $131.2 billion; the balance of the assets ($21.0 billion) was funded by the owners. (Note that, of course, Assets = Liabilities + Equity).

Contributed capital is typically reported in two elements: “common stock” (reported at par value—the “minimum value of the shares”) and “additional paid in capital” (the amounts received over par value). Also commonly included in equity is “treasury stock.” This amount, a negative number, represents the company’s shares that were repurchased from the equity markets. This is a common way to manage the financing of the company.

It is important to note that there are only three sources of capital available to any company for the purchase of assets. The company can: (1) borrow the money (liabilities), (2) sell equity positions to the owners (contributed capital), or (3) earn money on its own from running its business at a profit and leaving these funds in the company (retained earnings). Every company combines these three sources to fund the purchase of its assets and decides how much will come from each of the three sources.

This mix of liabilities and equity is called the “capital structure” of the company. Deciding on an appropriate capital structure is a key part of any company’s strategy. Debt is less expensive than equity and does not dilute the ownership of the shareholders. However, adding debt increases the company’s financial risk—the risk that it will not be able to meet its financial obligations when due. Over the last few decades, the availability of low-cost debt has motivated many companies to add a greater proportion of debt (leverage). The long-term success of this strategy depends upon the company’s ability to meet its debt obligations. It will be important to watch these companies carefully during this economic crisis. Is that increased level of debt affordable under the current scenario?

A company borrows money and sells equity to buy assets. These assets are employed to produce something of value for a market: products and/or services. The company sells the products and/or services produced by the assets to its customers, generating revenue and hopefully profits. The income statement reports on these activities, revenue, and expenses. Our next article looks at the reporting context for the income statement, what the numbers mean, and how to read the results.

In the beginning, law firm marketing departments had fewer employees than the mail room. Fast-forward thirty years: today, the rule of thumb is one marketing professional for every 20 to 25 attorneys, so a firm of 500 attorneys would have a marketing department with 20 to 25 professionals. Many firms also outsource specialized services such as digital marketing and database management.

If you are in a smaller firm or practicing solo, why do you care how large marketing departments are in large firms? You care, because you, too, need to be visible to your prospects and colleagues and engaged with your clients. We can look to the marketing professionals in larger firms to glean important ideas that are relevant to and appropriate for all practicing attorneys.

First, some definitions. Within the legal profession, marketing refers to activities that build brand awareness, including content management activities online and in print. These include brochures, newsletters, websites, videos, podcasts, other digital initiatives, database management, public relations, advertising, events, sponsorships, and so on.

Activities related to finding, wooing, winning and servicing clients come under the rubric of “business development.” This includes research on specific clients, their industries and markets, relationship building and tracking, and proposal and presentation preparation. It also includes training and coaching for attorneys, assistance with marketing and business development strategy, and business development plans for individuals, practice groups, and the firm itself.

Modern marketing departments are thinking strategically about ways to relate their personnel and services to defined client clusters. To this end, according to Calibrate Legal’s survey of North American law firm marketing departments, in larger firms there is an increased demand for:

Strategic business development initiatives

Digital marketing

Lead generation and pursuits

Data analysis and content marketing.

There is less demand for participation in 2021 conferences, events, sponsorships and inclusion in directories/awards. In -person events will also be de-emphasized in 2021: one-third of the responding firms plan to reduce them by 50% or more.[1]

Strategic Basics

The key word for 21st century consumers is “me,” translated in marketing-speak to “personalization.” The onslaught of available information has forced people to triage. Any material sent to prospects or clients must be germane to their interests, needs, opportunities and pitfalls or they won’t look at it.

This means you need to be very clear about the personalization of your own practice. Everything you write needs to reflect who you are—what your brand is. Your brand distills what makes you different and how that difference comes through in what you do with and for your clients. It is your promise to them that sets their expectations as to how it would be to work with you.

To relate authentically to your clients, you need to know more about them than just their contact information and current matter number. You need to really understand their work life, home life, wants, needs, dreams, problems, opportunities, and so on. You need to be able to “walk a mile in their shoes.” This translates into a niche market focus, a sub-group of possible clients who really could benefit from your advice, expertise and experience.

Rather than seeking out any kind of client who wants you, analyze what you like to do and who benefits from your practice. Analyze your current client base going back several years and outline the characteristics of your best clients–the ones you want to replicate. Then narrow your focus:

Tie all the characteristics of your ideal client together in a “client persona.” The persona combines everything you need to know about your prospects and clients. These are the people you want to meet, get to know, and, over time, incorporate into your work life as friends, colleagues, referral sources, resources, and clients.

Marketing Initiatives

Once you know what you want to sell and who you want to sell it to, you need to create opportunities to connect either directly through networking or indirectly through your marketing materials and initiatives. Some suggestions that continue to work in the COVID-19 environment:

Join organizations that your persona belongs to online or in-person. Join their professional, trade, or industry associations to learn what is important to them and how they approach the issues.

Expand your brand online. Use your website and LinkedIn of course, but also whatever other sites your clients favor. Go where they go and join their conversations.

Pick a marketing outreach tactic that is comfortable for you: newsletters, blog, videos, podcasts, white papers. Make the content timely and pertinent to your persona. Consider working with clients or colleagues on these endeavors.

If you work for a firm with a marketing department, use them. If you don’t, hire outside marketing service consultants and companies to help you, professionalize your efforts.

Maximize your online references and reviews. “An estimated 75% of people searching for a lawyer use legal review sites, and 84% of those people trust reviews as much as personal recommendations.”[2]

Regardless of your outreach tactics, when you meet someone you want to get to know, begin a series of contacts with them. Set up one-on-one meetings using zoom or the phone; send them information that refers back to your conversation, invite them to join you at an online networking event or webinar.

Remember it takes 8 to 12 personal “touches” on average to move forward from that first meeting to friendship.

Don’t forget your current clients. People are anxious, worried what will happen in 2021. Be there for them as a sounding board. Call them just to say, “How are you doing?” Listen to them and offer advice if they want it. Often clients are just happy to have a willing ear.

In the end, whether your firm is large or small or you work alone, you can adopt the mindset of those in large marketing departments. “Remember, business development is all about relationships. Relationships that are built on trust, empathy and a deep commitment to help clients succeed.”[3] People hire people they like and trust who have the experience and expertise they need to move forward. Think positively about moving forward, craft a brand that resonates with your market niche, and make yourself relevant to them. Success will follow.

[1] Calibrate Legal, Law Firm Marketing/BD Department Size Study 2020, https://calibrate-legal.com/marketing-bd-survey-2020/.

[3] Susanne Mandel, Chief Business development and Marketing Officer at Lowndes, quoted in ‘New Law Firm Strategies for Growth Amid the COVID-19 Pandemic and After,” Strategies+ blog, Legal Marketing Association, September 4, 2020.

Events that have taken place in the United States and Canada over the past few months have highlighted the systemic racism that Black/African American communities continue to confront and battle in both society in general and professional settings, including the legal profession. Racism and biases have created barriers to the Black/African American community in all aspects of society, including within our respective business and legal communities.

The ABA National Lawyer Population Survey 10-Year Trend in Lawyer Demographics (the Demographics Survey) evidences that in 2009 Caucasians made up 88 percent of the profession, a figure that only went down to 85 percent by 2019. Further, the Demographics Survey indicates that between 2009 and 2019 there has been only a 5.2 percent change in the male to female ratio within the profession (men in 2019 accounting for 64 percent of the profession and women for only 36 percent).

Ethical Obligation to Provide Access to the Profession

The results of the Demographics Survey show that the profession has a long way to go in becoming accessible to a diverse membership. The profession generally, and each law firm individually, has an ethical obligation to take measures to improve access to justice, including accessibility to membership for all, especially those who have traditionally encountered barriers to entry and advancement in the profession. Meeting this obligation requires greater commitment to eliminating discrimination and racism in any form, and this needs to become a greater focus for us all.

We, as a profession, can and should do better and do more.

General Initiatives Undertaken by Law Firms to Encourage Inclusion

In response to the underrepresentation of diverse attorneys in the profession, many law firms have increased their focus on initiatives meant to ensure they are able to attract diverse talent and retain that talent through meaningful engagement and advancement to senior leadership positions. Examples of these initiatives may include some of the following:

hosting sessions on cultural sensitivity and unconscious bias training;

providing financial support for diverse attorneys to become members of, and attend conferences held by, cultural or LGBTQ2+ bar associations or organizations;

educating through organized cultural programming such as diversity e-memos;

enrolling in organizations that assist with policy development and review to ensure that firm policies do not exclude or disproportionately burden any cultures, races, or sexual orientations/gender identities;

developing and implementing procedures for responding to client diversity reporting requests to ensure that legal teams are staffed by diverse attorneys at all levels (including senior/originating lawyers) and addressing the associated confidentiality/disclosure issues; and

developing and implementing affinity group policies and encouraging/causing the initiation of meaningful affinity groups.

Affinity Groups

Affinity groups play a central role in increasing diversity within law firms. They allow their membership to actively engage in communicating and gathering around a central unifying purpose and background to support one another and create a voice for their members. Through this approach, they can promote confidence, career growth, leadership potential, and success. They can also provide effective business and professional development opportunities through engagement with clients who share the personal characteristics of their membership.

To create a successful affinity group program, it is important to implement a policy that makes clear the parameters for establishing affinity groups. It is advisable that the proposed founder(s) commit to (1) serving a certain term of leadership (i.e., two years), (2) establishing the goals of the particular affinity group and its early planned initiatives, (3) acting as a mentor or champion of the membership, (4) completing sensitivity training to be able to assist membership in handling difficulties encountered, such as harassment or discrimination, and (5) regularly reporting to the firm’s diversity committee.

Given that affinity groups are an initiative of inclusion, consider making them open/welcoming of all firm members rather than just lawyers.

Examples of affinity groups may include: Asian, Black/African American, Latino/Latina, Jewish, LGBTQ2+, persons with disabilities (and their caregivers), mental wellness workers, and parents of young families.

Successful affinity groups may undertake initiatives such as the following:

volunteering/partnering with community and youth outreach programs;

hosting events during dates or periods of cultural significance (e.g., Black History Month, Pride);

engaging in affiliations with law school student affinity groups to create mentorship opportunities and assist with recruiting;

hosting/mentoring high school students from inner-city schools for exposure of youth with shared personal characteristics to law firm life (including programming addressing interactions with police and employers, relationship building with successful people who share their personal characteristics, and tours of financial districts and courthouses);

circulating firm-branded calendars that list all of the holidays/dates of note for the culture/religion associated with affinity groups;

hosting lunches and learns with speakers/panels discussing specific issues applicable to the culture or personal characteristics of the membership for CLE credit;

organizing teams to run in the annual Pride runs/walks/charity team events;

organizing initiatives to recognize and support antibullying campaigns (such as the International Day of Pink, which provides an opportunity to celebrate diversity and raise awareness to stop homophobia, transphobia, transmisogyny, and all forms of bullying);

hosting “Let’s Walk” events to build community and promote health and exercise;

hosting speakers or activities with the aim of reducing stigma and providing mental wellness education and coping strategies;

providing firm members with mental health first aid training to provide ongoing support to colleagues who may encounter mental wellness difficulties, and the like;

lobbying to enhance firm benefits, including mental wellness apps for all firm members; and

creating spaces/forums (i.e., parents of young families) for those sharing challenges, experiences, and resources with one another.

The National Venture Capital Association (NVCA) model stock purchase agreement form (Model Form) was recently updated in August 2020. After reviewing the updates to the intellectual property related sections of the Model Form, certain language and concepts regarding allocation of intellectual property risk could be revised to better reflect the NVCA goals of providing fair terms between the investor and the company and promoting consistency among financing terms. [i]

Any model forms project will cause reasonable and sophisticated practitioners to disagree as to whether certain proposed language is fair and would push companies and venture capitalists to reduce transaction costs by bringing the parties toward a middle ground that adequately protects and benefits both sides. So, there are inherent limitations in any attempt to craft language that can be used in all scenarios. The nature of a venture capital investment transaction is such that the intellectual property representations cannot be as complete as in a merger and acquisition transaction. Further, black ink on a document is valuable real estate in a venture stage stock purchase agreement, often with pressure from both parties to limit the length of the agreement.

However, even with all of the above understandings, these proposed revisions will for each modified representation, address at least one and often multiple of the following:

limit a representation to something that a company can more reasonably make given their position as a young, emerging growth company;

expand the scope of what a company should be reasonably responsible for given updates in technology and how companies interact with customers or engage in marketing;

trade some valuable ink space currently used to address an often fixable (and thus less material) infringement risk for a more relevant infringement representation;

use language that is more technically accurate and consistent with usage in the intellectual property litigation arena; and

clean up a few minor drafting nits.

Ideally, this article should be read with a copy of the Model Form handy as some suggestions and comments below apply based upon specific word choices in the Model Form. All quoted language comes directly from the Model Form, with liberal quotations from the specific language of the applicable representation being discussed as a result of some arguments being dictated by, at times, the editing or exclusion of a small number of words. However, space constraints prevent quoting large portions of the Model Form and it is always helpful to read these suggested revisions within the context of the entire Section 2.8 of the Model Form. The term “Company” below has the same meaning as “Company” as used in the Model Form.

2. Encumbrances on Company Intellectual Property

The current draft of the Model Form in Section 2.8(c) applies to “Company Intellectual Property” which is defined in a manner that effectively includes both intellectual property that is owned by Company and intellectual property that is licensed by Company. So all of the representations in Section 2.8(c) must be analyzed as to whether it is reasonable for Company to make representations about intellectual property Company doesn’t own.

It is not reasonable for Company to represent that there are no options, licenses, agreements, claims, encumbrances or share ownership interests (“Encumbrances”) for the licensed intellectual property. Company is not in a realistic position to know about Encumbrances on licensed intellectual property, such as any other licenses that may have been granted in the same intellectual property or any liens that a third party may have granted in their intellectual property. Moreover, the existence of Encumbrances does not necessarily indicate anything negative about Company’s use of licensed intellectual property.

3. Licenses Entered into by Company

The Section 2.8(c) representation asks Company to make a representation that they have not entered into any licenses for intellectual property. That is unrealistic given the prevalence of software and technology within almost every business. Of course, Company may certainly disclose the existence of such licenses as an “exception,” but given that almost every entity conducting business of any type licenses at least some software, the representation would better reflect reality by asking Company to schedule out material third party licenses and represent that Company is not in breach of such third party licenses.

Recommended Revisions to Model Form: “2.8(c) Other than with respect to commercially available software products under standard end-user object code license agreements, there are no outstanding options, licenses, agreements, claims, encumbrances or shared ownership interests of any kind relating to the Company Intellectual Property that is owned in any manner by the company, nor is the Company bound by or a party to any options, licenses or agreements of any kind with respect to the patents, trademarks, service marks, trade names, copyrights, trade secrets, licenses, information, proprietary rights and processes of any other Person. [Section 2.8(c) of the Disclosure Schedule lists all material licenses obtained by Company in intellectual property]. Company is not in material breach of any licenses in intellectual property.”

4. Definition of Intellectual Property

The Model Form defines the term “Company Intellectual Property” to include most of the traditional categories of intellectual property with an option to include mask works. The definition does not include an option to include rights of publicity, which is probably just as—if not more—important than an option to include mask works, since mask works are only applicable to semiconductors. Rights of publicity considerations are relevant for content that includes any images, names or likenesses of anyone. In addition to the obvious category of companies in the social media space, many companies display personnel images on their website or products in addition to their marketing materials. There is not universal agreement as to whether rights of publicity are intellectual property rights, so the catch-all language in the definition of “Company Intellectual Property” referencing “similar or other intellectual property rights” does not provide certainty as to whether the representations for intellectual property would also cover rights of publicity. There is a similar uncertainty as to whether the language in Sections 2.8(a) and 2.8(b) of the Model Form that reference violation of “proprietary rights” and “intellectual property rights” by Company would cover any violations by Company of an individual’s right of publicity. It is therefore important to consider whether Company is in a space where violations of rights of publicity may occur.

Recommended Revisions to Model Form: “(c) “Company Intellectual Property” means all patents, patent applications, registered and unregistered trademarks, trademark applications, registered and unregistered service marks, service mark applications, tradenames, copyrights, trade secrets, domain names, [mask works,] information and proprietary rights and processes, rights of publicity, similar or other intellectual property rights, subject matter of any of the foregoing, tangible embodiments of any of the foregoing, licenses in, to and under any of the foregoing, and in any and all such cases [that are owned or used by] [as are necessary to] the Company in the conduct of the Company’s business as now conducted and as presently proposed to be conducted.”

5. Problems with Open Source

The purpose of the open source representation in Section 2.8(g) is to elicit disclosures of use of open source software used “…in connection with any of its products or services that are generally available or in development” that would require Company to undertake certain obligations that may diminish the value of proprietary Company Intellectual Property. The legal effects of using open source software is one of the most asked about diligence items for investors in technology companies or any company that has proprietary software; it is not surprising that there is an entire section of the Model Form devoted to this topic. Whether or not use of open source software is problematic for Company is very fact specific, so the related representation should be drafted in a manner that would encourage the Company to disclose any potentially problematic situations related to open source software so that investors can perform follow up diligence. The Model Form open source representation is too narrow in scope and seems to assume that Company may only be making harmful decisions about open source software in factual scenarios.

For example, the footnote states that many of the potentially “onerous” effects of using open source software only occur if there is a distribution of open source software within a product that was actually “released” to the public. While it is true that there must be a “distribution” of GPL licensed software[ii] in order for certain terms of the GPL 2.0 or GPL 3.0 license to apply, neither GPL 2.0 nor GPL 3.0 require that such distribution be made within a product. It is not uncommon for software developers to “contribute” modifications of open source software for use by other developers even if such modifications are not used within a product commercialized by such developer’s employer. So a distribution of open source software that is made as part of a contribution by Company employees to an open source project may have negative effects on the Company while not requiring any sort of breach of the Model Form open source representation.

The same footnote also states that the open source representation is intended to require disclosures for certain use of open source software related to any products that the “Company has released…” However, the actual language of the open source representation arguably only applies to any use of open source software in connection with any products that “…are generally available” [emphasis added] which would seem to not include any Company products that were formerly released and are no longer “generally” available. Once open source software is distributed to anyone by Company, whether or not such distribution is ongoing or occurred only in the past (even if just sporadically), the potentially negative effects to the Company of such distribution remain even though such past distributions arguably do not lead to any breach of the open source representation.

To address the potential holes and ambiguities of the existing Model Form open source representation, the suggested revisions take away the qualifier that the use of open source software was done in conjunction only with any currently available product or service and simply reference any actions that would cause any Company Intellectual Property (besides the Open Source Software itself in some situations) to be subject to certain obligations. Whether past actions unrelated to currently available products diminish the value of Company owned intellectual property will always be a very fact-based analysis and having an overly narrow open source representation would eliminate certain disclosures that should be subject to further analysis by investor’s counsel.

Recommended Revisions to Model Form: “(g) The Company has not embedded, used or distributed any open source, copyleft or community source code (including but not limited to any libraries or code, software, technologies or other materials that are licensed or distributed under any General Public License, Lesser General Public License or similar license arrangement or other distribution model described by the Open Source Initiative at www.opensource.org, collectively “Open Source Software”) in connection with any of its products or services that are generally available or in development in any manner that would materially restrict the ability of the Company to protect intellectual propertyowned in any manner by the Companyproprietary interestsin any such product or service or in any manner that requires, or purports to require (i) any Company IPIntellectual Property[iii] (other than the Open Source Software itself) be disclosed or distributed in source code form or be licensed for the purpose of making derivative works; (ii) any restriction on the consideration to be charged for the distribution of any Company IPIntellectual Property; (iii) the creation of any obligation for the Company with respect to Company IPIntellectual Property owned by the Company, or the grant to any third party of any rights or immunities under Company IPIntellectual Property owned by the Company; or (iv) any other limitation, restriction or condition on the right of the Company with respect to its use or distribution of any Company IPIntellectual Property (other than the Open Source Software itself).”

6. Software Licenses

Section 2.8(d) devotes a whole section to having Company represent that it “possesses” valid licenses for all software on computers and “software-enabled electronic devices” owned or leased by the company. Rather than devote a whole section to licenses of only one type of intellectual property (software) and even then, only software used on certain machines, investor’s counsel should consider substituting Section 2.8(d) with a more targeted and applicable representation regarding the type of intellectual property that is material to Company’s business.

While every company will use software, the risk that use of unlicensed copies of widely commercially available software such as Adobe Acrobat Reader or Microsoft Windows will cause irreparable harm to Company is relatively low outside of certain narrow and specific circumstances. Further, with the increased use of cloud computing services, it is likely that at least some of the material software used by Company will not be installed on Company owned or leased hardware but instead will be installed on hardware operated by the cloud service operator. Finally, the representation merely requires that Company have a “valid license” to “use” the software. The term “use” is considered imprecise in the context of software licensing since Company may need to do a broad range of activities with licensed software such as modifying, distributing and reproducing such software. The right to “use” software generally is not considered to cover modifying or distributing such software. If Company needed to distribute certain software as part of its business, the Model Form representation arguably does not address this concept.

While almost all investment targets use software, whether such software use justifies an entire subsection of Section 2.8 should be carefully considered given that other language may already partially cover the concepts. Since a drafting option under the Model Form for Section 2.8(a) and the definition of “Company Intellectual Property” creates a “sufficiency” representation that the Company has or can obtain all “necessary” rights in intellectual property for the conduct of the Company’s business, the additional language in Section 2.8(d) may not add much value if Company’s business is not materially affected by the status of their software licenses. Further, Company’s material inbound intellectual property licenses may not be in software but may be in patents (such as a biotech spinoff from a university), trademarks (such as a franchisee or merchandising partner), or non-software copyrights (such as an online publication). For any of these, substituting a more focused representation would be more valuable.

If a software use representation is still needed, it would be better to substitute the Model Form software representation with something not limited to certain hardware in order to definitely capture software that may be used in cloud services and that specifies that Company has adequately broad license rights in such software.

Recommended Revisions to Model Form: “(d) The Company has obtained and possesses valid licenses tousefor all of the software programs that are used, modified or distributed by the Company in the conduct of its business and such licenses allow Company to exercise all rights exercised by the Company in such software programs when conducting its business present on the computers and other software-enabled electronic devices that it owns or leases or that it has otherwise provided to its employees for their use in connection with the Company’s business.”

Include the following explanatory footnote: This Section 2.8(d) is less critical if there is language in Section 2.8(a) that the company has obtained all rights in Company Intellectual Property necessary to conduct its business. If such language to cover the concept of Company having “sufficient” intellectual property already exists, consider substituting a different representation to cover an intellectual property risk that is not addressed in any manner by the existing Model Form language.

7. Infringement

Section 2.8(b) and Section 2.8(a) both deal with Company infringement of intellectual property, but the language in these sections is inconsistent. The language in Section 2.8(b) should be made more consistent with the language in Section 2.8(a) that addresses whether Company has received any notices alleging that Company (or its conduct of the business) has violated various intellectual property rights. Using the same language in both Section 2.8(a) and 2.8(b) as recommended below would bring the language in Section 2.8(b) more in line with the more accurate view that infringement occurs as a result of actions taken with regard to intellectual property and not by the intellectual property itself. The key difference is that Section 2.8(a) references violations of intellectual property rights by Company or resulting from conduct of the business while Section 2.8(b) references violation of intellectual property rights by Company’s products or services.

Recommended Revisions to Model Form: “(b) [To the Company’s knowledge,] no product or service marketed or sold (or proposed to be marketed or sold) by the Company’s conduct of its business (or proposed conduct of its business) does not or will not violatesor will violate any license or infringesor willinfringe any intellectual property rights of any other party.”

8. Conclusion

The Model Form intellectual property representations could be edited to be more accurate or applicable in almost all venture capital transactions. Some of the above revisions should be applied regardless of the nature of the investment target, while others are best used depending upon the investment target. This exercise was a reminder that the intellectual property representations should be reviewed and possibly revised (even after taking into account those proposed revisions above that apply in all situations) only after taking into account the nature of the investment target. There is a common reluctance to engage in tinkering too much with the Model Form intellectual property representations in a venture deal, but if the goal of the representations is to both elicit necessary disclosures for diligence purposes and to help guide the investment target in the diligence process, then the intellectual property representations should be tailored to address certain specific topics that are not in the current Model Form.

[i] A considerably shorter article addressing some of these topics by the author appeared in the Fall 2020 edition of the ABA Venture Capital and Private Equity group newsletter “Preferred Returns.” Space constraints in such publication prevented a more detailed analysis and inclusion of suggested revisions that appear in this article.