Question: What triggered your interest in family business succession planning?

Answer: Before I attended law school, I worked in several family businesses, and I enjoyed those experiences. I learned to respect the courage of entrepreneurs and owner-operators. I appreciate the contribution that family businesses make to the economy and the communities in which they operate. Also, I love my job because I can help make families happier. That’s a pretty good way to spend my work hours.

Question: In your book, you detail the planning process for business succession. What common mistakes do business owners make when it comes to succession?

Answer: The biggest mistake is not planning at all. Proper business succession planning can help a family business in many ways. It can avoid succession crises, but it also can lead to tax savings, better business practices, greater financial security for the senior generation, and opportunities for personal development for members of the next generation. A second big mistake is not planning for a change of governance mechanisms to adapt them to successor ownership. For example, when ownership passes from the founder to the founders’ children, the business’s governance structure needs to change to accommodate and define the input of multiple new owners. A third big mistake is not planning for the senior generation’s life after exit from the business. This mistake can cause senior generation managers to stay too long or to suffer lifestyle impairments in retirement.

Question: I found it interesting how retirement is linked with succession. Do they go hand in hand or does one trigger the other?

Answer: Often senior generation retirement is inextricably linked to ownership and leadership succession. First, senior generation leaders may be unwilling or unable to retire until members of the next generation are ready to take over managing the business. Often this requires a succession plan that adapts governance and management structures to optimally support the leadership skills and participation of the next generation owners. Second, senior generation leaders may be unwilling or unable to retire because they remain economically dependent on the business and its continuing success. Business succession planning can provide a secure and viable economic future for senior generation owners after they retire and transfer their ownership interests. Unless the senior owners can retire, there may be no business succession until they die. That’s a circumstance that is bad for everyone involved.

Question: The appendix material in your book is fantastic! The lawyer has a wide range of issues to confront in succession planning—in your opinion, what is the most difficult part for the practitioner?

Answer: The most difficult part of family business succession planning for the lawyer is the broad scope and diversity of issues that the lawyer must address. The purpose of the book is to help identify those issues and to suggest ways to address them. Sometimes it is important for the lawyer to get help from colleagues or the clients’ other advisors. Business valuation, tax elections or choice of entity, nonqualified retirement plans, and disability insurance are all examples of issues that may require the lawyer to collaborate with other advisors. The book will help the lawyer spot these issues, even though they may not be in the lawyer’s areas of core competency. Family business succession planning is a collaborative, long term project, and that can become confusing or messy if the lawyer doesn’t keep it organized. The appendix materials in the book provide ways to stay organized with respect to the big picture and the details.

Robert B. Dickie is the founder of The Dickie Group, which provides training in finance and accounting to most of the country’s leading law firms and to the in-house legal departments of numerous Fortune 100 companies. Peter R. Russo, retired from the Boston University Questrom School of Business in 2017, where he served for 15 years as Executive in Residence and Senior Lecturer. During that time, he served terms as the Faculty Director of both the Entrepreneurship Program and the Executive MBA Program. Bob and Pete have just published their third edition of Financial Statement Analysis and Business Valuation for the Practical Lawyer. Bob and Pete offer their insights and expertise on financial statements and business valuation.

Question: Since you wrote the first edition of your book, how has financial statements and valuation changed?

Answer: In the two decades since Bob wrote the first edition, there have been substantive changes in both how the financial statements are generated and how they are used. A series of accounting scandals, the most famous of which was the Enron case in 2001, led to an increased skepticism about reported earnings and a call for more accountability from management. The accounting profession and the Securities & Exchange Commission have responded and today management is held to a much higher level of accountability than was previously the case.

During this same period, the U.S. Generally Accepted Accounting Principles (“GAAP”) that drive the rules management must comply with in financial reporting, have been changing to be more consistent with the International Financial Reporting Standards (“IFRS”), as part of a long-term convergence project. While this process has taken longer than initially anticipated, GAAP is undeniably moving toward the time when a single set of rules will be applied globally. For example, in recent years, we have substantially revised the way that companies record revenue and account for lease obligations.

At the same time, users of financial statements have become more sophisticated. It is not uncommon to see companies measured by a more complex set of metrics than were once used.

Question: For the lawyer approaching financial statements and valuation, how much understanding does he or she need to understand of accounting issues?

Answer: The key to answering this question lies in how the lawyer provides value to his/her client. Sometimes the lawyer provides this value by answering the client’s questions, but often she can provide greater value by offering answers to the questions a client did not know to ask. Doing this does not necessarily require a deep knowledge of the accounting and reporting rules, nor does it require a great deal of finance expertise. What is needed is a basic understanding of how the numbers are generated, what information they do and don’t contain, and a sense of how the numbers are used. Of equal importance is an understanding of the motivations of management—what the client is trying to achieve with a transaction or strategic decision, and management’s biases in reporting. Armed with this level of expertise, the lawyer is able to work closely with the client to help achieve its goals.

Question:You both do an excellent job in describing valuation—when it comes to valuation and valuing a company, what are the most common mistakes made?

Answer: Perhaps the biggest misconception we see when discussing business valuation is that some people treat the question as one with a single correct answer. The value of any company is likely to vary based upon who the potential buyer is and what strategies they will be able to employ if they acquire the company. That is why we often see valuations expressed in ranges and calculations of value shown using multiple methodologies. In fact, in a business valuation, the methodologies employed often convey as much information as the numbers calculated. The process of valuing a company can help identify the drivers of value, call attention to key unknowns, and raise important questions which are worthy of attention.

Another common problem we see in business valuation is the lack of understanding of the limitations of some of the methodologies that are commonly used today. There is no “prefect formula” for calculating a business’ value and all of the methods used have their strengths and limitations. For example, if a business is being valued by comparing its performance to a group of comparable companies, it is critical to understand whether and in what ways the companies are truly comparable.

Finally, let’s keep in mind that valuing a start-up biotech company is much more difficult, and likely to yield a much wider range of possible valuations, than, for example, an apartment building in a prosperous neighborhood with a stable rent roll.

Question: This is a very daunting area of the law. How do you keep abreast of all the changes in both?

Answer: Certainly, reading about current events and trends is an essential part of staying current. But perhaps the most important skill is to stay intellectually curious. Conversations with others who find this space interesting can yield important new insights. And especially, when we see or hear of something that seems strange or unusual, seeking the story behind that phenomenon is a great way to continue to learn.

Question:Besides a business lawyer, what other types of lawyers would benefit from this book? Additionally, are there other professionals besides lawyers who would find this book useful?

Answer: Lawyers who work with estates certainly have a need to understand the concepts we discuss in this book, in that the assets that they are asked to advise their clients about are often investments in companies. This is particularly true if the assets include interests in privately owned companies, especially if they are minority interests. The knowledge might well also be useful for litigators handling securities cases, measurement of damages situations, or earn-out matters.

Other than lawyers, we think that this book can be extremely valuable to individuals who may not have business as their education emphasis, but who are making important decisions in companies. This is commonly the case in technology or life science companies, for example, where individuals with a background in science or medicine can rise to the ranks of upper management. We feel that this book can provide some very useful insights to someone like this, especially if an advanced degree in business is not a realistic option at this stage of the career.

Dear IRS, no penalties please! Taxpayers claim that penalties are not warranted for many reasons, but what actually works? One of the biggest, yet most misunderstood, is the defense that a tax position was based on reasonable cause.[1] Section 6664(c) of the IRC provides that “no penalty shall be imposed . . . with respect to any portion of an underpayment if it is shown that there was a reasonable cause for such portion and that the taxpayer acted in good faith with respect to such portion.” How the IRS evaluates this defense depends on which penalty has been assessed, so you must first know that to determine whether you are, well, reasonable. In addition, on top of reasonable cause, certain penalty defenses involve other concepts, such as an absence of willful neglect. Isn’t that proving a negative? You bet.

Who wins in a tax penalty stalemate? This one should not surprise you. The IRS does, of course. Put differently, taxpayers bear the burden of substantiating their reasonable cause. We all must exercise ordinary business care and prudence in reporting our proper tax liability, and remember that all tax returns are signed under penalties of perjury.

The IRS applies a facts-and-circumstances test on a case-by-case basis to determine whether a taxpayer meets the reasonable-cause exception. As you might expect, that can lead to inconsistent, subjective results. The stakes can be high. The reasonable-cause exception applies to accuracy-related penalties under section 6662, which are usually 20 percent of the amount at stake. It even applies to penalties for civil fraud under section 6663. How much is the civil fraud penalty? A whopping 75 percent. Thus, if your flaky tax deduction amounts to $10,000 in tax, you can add another $7,500 if the IRS says it was fraud. Fraud penalties are not asserted frequently, but it is not an exaggeration to say that penalties can be big. That makes your ability to sidestep them big, too, even if you end up having to pay all the tax and the interest.

But wait, there’s more. The reasonable-cause exception for penalty relief also applies to other penalties the IRS can impose, including penalties for: (1) failure to file a tax return and failure to pay, imposed by section 6651, (2) making an erroneous claim for refund or tax credit under section 6676; (3) failure to file Form 1099 or other information reporting returns under section 6721; and (4) the understatement of a taxpayer’s liability by a tax return preparer under section 6694.

In fact, the tax code is chock full of penalty provisions. A reasonable shortcut to all the detail is to argue that you always behaved reasonably. You also want to be able to say that you always claimed every single item listed on your tax return in good faith. However, where might you not want to bother arguing about your reasonable cause?

Well, there could be several situations. The reasonable-cause exception does not apply to an underpayment of tax that is due to transactions lacking economic substance as described in section 6662(b)(6). The same is true for penalties for a gross valuation overstatement from claiming charitable contributions deductions for property. All is not lost, though, at least not necessarily. There can be penalty relief in those two cases, but the rules are different and more complex. Fortunately, those two penalties are more the province of highly aggressive transactions that do not apply to most people or most situations.

Tax Return Reporting Is Key

According to the IRS, the most significant factor in determining whether you have reasonable cause and whether you have acted in good faith is your effort to report the proper tax liability. Doing your best to report the right amount sounds simple. Notably, though, unlike the taxpayer defense of “reasonable basis,” reasonable cause does not depend on the legal authority you have stacked up; rather, it depends on your actions. For example, suppose that you report the amount from an erroneous Form 1099, but you didn’t actually know that the Form 1099 was wrong. You think the Form 1099 has the total you were paid, but under audit it turns out that the Form 1099 reported less than you actually received. That could happen to anyone. After all, we all often rely on Form 1099 data, so reasonable cause may apply if you simply pick up a reported number and reasonably assume it is correct.

What if you were paid $300,000, but the Form 1099 said you received $300? It might be harder to say you picked up that number unintentionally and reported it, compared to an error where the inaccurate Form 1099 indicated $285,000. Still, your behavior may be reasonable, even with a big error.

How about an isolated computation or transposition error you might make on your return? That, too, may be consistent with reasonable cause and a good-faith effort. It is easy enough to transpose numbers or to make other errors. However, if you have a dozen of these on your return, it is not as likely that the IRS will understand and let you off the penalty hook.

Other factors the IRS considers include the taxpayer’s experience, knowledge, education, and reliance on the advice of a tax advisor. When considering the facts and circumstances, the taxpayer’s experience, education, and sophistication concerning the tax laws are relevant. Reliance on advice from a tax professional is obviously a point that many taxpayers use to try to avoid penalties.

However, the IRS says that your reliance must be objectively reasonable. That means you must provide your tax advisor with all of the necessary information to evaluate your tax matter. In other words, cherry picking what you tell your tax adviser to get the answer you want to hear is not reasonable. That kind of behavior would preclude you being viewed as reasonable if you are relying on a sugar-coated answer.

In addition, your tax advisor must be competent in the subject matter. If you have a complex corporate tax problem and you consult a low-income, individual income tax advisor, it might not be reasonable for you to rely on that advisor, no matter how faithfully you follow his or her advice.

The IRS tells its auditors that they should determine whether the taxpayer acted with reasonable cause and in good faith based on all the facts and circumstances on a case-by-case basis. The taxpayer must have exercised the care that a reasonably prudent person would have used under the circumstances. The meaning of “reasonable cause” can also depend on the particular penalty.

Some penalty sections also require evidence that the taxpayer acted in good faith, or that the taxpayer’s failure to comply was not due to willful neglect. Not every penalty provision has the same penalty relief standard. For instance, section 6676 of the code imposes a penalty for an excessive claim for refund or credit, but the penalty can be waived if you demonstrate reasonable cause.

Section 6662 imposes accuracy-related penalties, but to get out of them, your error must have been made with reasonable cause and in good faith. Finally, section 6651 imposes the failure to file or pay a penalty, and it provides a waiver based on reasonable cause and an absence of willful neglect. In short, if you are trying to get out of a penalty the IRS seeks to impose, it pays to look at the specific penalty in question. You want to show how your facts and your conduct meet all the required tests.

In Writing

Do you make your case orally? Usually not, although you can try that for starters in some cases. Like just about everything else with the IRS, you almost always should lay it out in writing. In fact, in many cases, the tax regulations actually require the taxpayer’s request for waiver of the penalty to be in writing and even signed under penalties of perjury.[2]

Whether the elements that constitute reasonable cause, willful neglect, or good faith are present is based on all the facts and circumstances. Reasonable cause is established when the taxpayer exercised ordinary business care and prudence. “Ordinary business care and prudence” is defined as taking that degree of care that a reasonably prudent person would exercise.

Key Factors

The taxpayer’s effort to report the proper tax liability is the most important factor in determining reasonable cause. In assessing the taxpayer’s effort, the IRS tells its agents to look at all the relevant factors, including the nature of the tax, the complexity of the issue, the competence of the tax advisor, and so on. Other factors include the taxpayer’s experience, knowledge, education, and reliance on the advice of a tax advisor.

In determining whether a taxpayer exercised ordinary business care and prudence, the IRS tells its agents to consider all the facts and circumstances, and to review all available information, such as the taxpayer’s reason, compliance history, length of time, and circumstances beyond the taxpayer’s control. You might assume that such a review would extend back one year, i.e., the tax year involved. However, the IRS tells its agents to look at the three previous tax years. They will look for your payment patterns and compliance history. A taxpayer who repeatedly is assessed the same penalty may not be exercising ordinary business care.

In contrast, if this is your first incidence of noncompliance, the IRS will consider that, along with the other reasons and circumstances you provide. The IRS is supposed to consider all the facts and circumstances, including the length of time between the occurrence of the tax problem and when you fixed it. The reason for your error should coincide with the timeframe of dates and events that relate to the penalty.

The IRS is even willing to say that some mistakes and circumstances are beyond your control. However, the IRS also asks whether you could have foreseen or anticipated the event that caused the problem in the first place.

How about relying on tax advice from the IRS? Isn’t that always reasonable? Not necessarily. This can be a surprisingly touchy subject, particularly in the case of oral advice. Oral advice usually isn’t worth the paper it’s (not) printed on. If you point to something the IRS told you in writing, however, the IRS evaluates the information and determines whether the advice was in response to a specific request and related to the facts contained in that request. The IRS also wants to know if you actually relied on its advice.

Taxes are complex, and that itself might provide you with plenty of excuses as to how you could mess up. However, some “oops” errors are a lot easier to explain than others. For example, the IRS says you generally do not have a basis for reasonable cause if the penalty relates to the late filing of a tax return or payment of a tax obligation. Arguing that you thought tax returns were due May 15, not April 15—even if a tax professional told you that—isn’t likely to save you from penalties.

Arguing that you or your accountant forgot to file also is not likely so demonstrate reasonable cause. The IRS says everyone is responsible for timely filing taxes, and for paying them, and those duties cannot be delegated. So even if you rely on accountants, bookkeepers, or attorneys, you cannot delegate responsibility to timely file tax returns and timely pay tax obligations. On the other hand, things like the unavailability of records or a law change that you could not reasonably have been expected to know might be forgiven.

In some cases, you can seek penalty relief due to a lack of knowledge of the law. Relevant factors include your education, whether you have been subject to the tax before, whether you have been penalized before, the complexity of the tax issue, and recent changes in the tax law or forms.

[1] Robert W. Wood practices law with Wood LLP and is the author of Taxation of Damage Awards and Settlement Payments and other books available at www.TaxInstitute.com. This discussion is not intended as legal advice.

On June 22, 2020, in a much anticipated decision, the Supreme Court held that the Securities and Exchange Commission (SEC or the Commission) can continue its longstanding practice of seeking disgorgement as an equitable remedy in judicial proceedings under section 21(d) of the Securities Exchange Act of 1934. In Liu, the court held that a disgorgement award that (1) does not exceed a wrongdoer’s net profits, and (2) is awarded for victims constitutes an equitable remedy within the scope of the SEC’s statutory authority.[1] In so holding, the Court made clear that legitimate business expenses must be accounted for in determining how much the SEC can seek in disgorgement. Although the Court indicated its skepticism toward the SEC’s longstanding practice of sending disgorged funds to the Treasury, it did not specifically address whether disgorged funds must be returned to victims of the misconduct being prosecuted, leaving that determination to the lower courts.[2] The Court also left unanswered whether the SEC is authorized to impose joint and several liability on violators.[3] Following Kokesh and other recent decisions, this is the Supreme Court’s latest effort to rein in the SEC’s enforcement authority. Although Liu stopped short of eliminating the power of the SEC to seek disgorgement for securities law violations, it provided companies facing SEC enforcement scrutiny with the necessary tools for challenging and circumscribing the amount sought by the Commission. This decision provides some clarity on the parameters of the SEC’s authority, but it leaves open many questions that will be resolved in future settlement negotiations and court battles.

The Court’s Holding

The Liu decision was eagerly anticipated by SEC defense counsel and regulated entities. The potential impact on SEC enforcement actions if disgorgement were eliminated as an equitable remedy would have been game-changing, but instead of providing absolute clarity in either direction, the Supreme Court stopped short. In doing so, it raised more questions that may give rise to potential future challenges. Writing for an 8-1 majority, Justice Sotomayor rejected an all-or-nothing approach to the question of whether disgorgement constitutes a permissible equitable remedy. The Court held that a disgorgement award that (1) does not exceed a wrongdoer’s net profits, and (2) is awarded for victims constitutes equitable relief the SEC is permitted to seek in enforcement actions.[4] To arrive at this holding, the Court examined whether the disgorgement sought in Liu—which required the defendants, a married couple, to disgorge the full amount they raised from defrauded investors, without any reduction for their claimed business expenses, and which imposed joint-and-several liability on the two spouses—falls into “those categories of relief that were typically available in equity.”[5] The Court examined cases in which courts imposed “profits-based remedies” while placing limitations on those remedies that ensured they did not constitute penalties beyond the scope of a court’s equitable powers.[6]

The Future of Disgorgement Post-Liu

In limiting disgorgement to a violator’s net profits, the Court provided guidance regarding how to differentiate valid expenses for future disgorgement calculations. The majority opinion draws a line between legitimate business expenses and those that are “wholly fraudulent” in furtherance of a scheme to defraud investors.[7] Although the Court left it to the lower court on remand to assess the legitimacy of the expenses in question, the Court seemed to indicate the potential legitimacy of certain expenses at issue in Liu because they “arguably have value independent of fueling a fraudulent scheme.”[8]

In what will likely set the stage for future battles both during settlement discussions and in the courtroom, the Court declined to answer whether the SEC’s longstanding practice of sending disgorgement funds to the Treasury rather than to victims or harmed investors would be permissible under its new disgorgement limitations.[9] The Court also declined to address whether imposing joint-and-several liability against violators was within the SEC’s statutory authority.[10] Both of these questions will lead to future questions and provide points of argument in upcoming SEC enforcement actions. Although not conclusive, Liu provides some indication of the Court’s skepticism toward both practices that will help entities and individuals facing SEC enforcement scrutiny going forward. In addressing the issue of improperly earned profits under equitable principles, the Court noted that “the SEC’s equitable, profits-based remedy must do more than simply benefit the public at large by virtue of depriving a wrongdoer of ill-gotten gains. To hold otherwise would render meaningless the latter part of § 78u(d)(5).”[11] The Court emphasized that no order in Liu required funds be directed to the Treasury, but that if such an order were to be entered on remand, the lower courts may evaluate whether that order would be “for the benefit of investors” and therefore within the SEC’s statutory grant of authority and in accordance with equitable principles.[12] Similarly, the Court concluded that disgorgement is inappropriate where it includes the ill-gotten gains that accrue to affiliates through a joint-and-several liability theory.[13] Instead, the Court opted to instruct the 9th Circuit to determine whether the petitioners could be found liable “for profits as partners” or whether individual liability is appropriate.[14] This latter point will also set the stage for future battles between co-defendants, individuals, and entities seeking to limit their own damages or disprove a joint venture or partnership in the underlying misconduct.

What It Means for Regulated Entities and Individuals

As SEC-regulated entities around the country await the outcomes of future legal battles, companies and individuals should expect the SEC to continue to seek disgorgement under familiar theories pre-Liu. Over the past five years, disgorgement has accounted for approximately 71 percent of the SEC’s monetary recoveries.[15] Absent a change in enforcement strategy or more stringent restrictions imposed by courts around the country—neither of which is expected—the Commission’s efforts will continue. Savvy regulated entities should nonetheless be prepared to push back on Commission overreach using the tools the Court has given them. To do so, companies and individuals subject to SEC scrutiny should take steps to anticipate how they might use the findings of the Supreme Court in Liu (and other decisions like Kokesh) to their advantage. While we await the reactions to this decision in the lower courts, the best practices for companies to consider today—before facing SEC scrutiny tomorrow—include:

understanding relationships with employees, joint venture partners, agents, and other affiliated entities that could impact future joint and several liability;

ensuring a proper understanding of the accounting issues at play in the business under review;

understanding all expenses relevant to the conduct at issue, and those expenses’ relationship to business operations outside of the allegedly improper scheme (be prepared to justify those expenses to avoid paying them in disgorgement later); and

keeping up to date on the lower court reactions to the Liu decision, and seeking advice from experienced counsel when questions arise.

[1] Liu v. Sec. & Exch. Comm’n, No. 18-1501, 2020 WL 3405845, at *2 (June 22, 2020).

[8]See id. at *12 (“[S]ome expenses from petitioners’ scheme went toward lease payments and cancer-treatment equipment. Such items arguably have value independent of fueling a fraudulent scheme.”)

A recent decision from a California trial court held that a Delaware choice-of-law/forum provision could not be enforced against a California resident because doing so would deprive him of his right to a jury trial as embodied in the California Constitution. This decision brings into question all manner of agreements, including operating agreements for LLCs organized outside of California, and the choice-of-law/forum provisions thereof.[1]

West, resident in California, entered into a series of agreements relating to Access Control Related Enterprises, LLC (ACRE), an LLC in which he was a member and its CFO and COO. One of those agreements was a Securityholders’ Agreement that contained Delaware choice-of-law and choice-of-forum (the Court of Chancery or the Federal District Court) provisions; no other provisions of the Securityholders’ Agreement are detailed in the opinion. Some two-and-a-half years after entering into the Securityholders’ Agreement and the other agreements, West was terminated by ACRE. In response, he brought suit in California and then in Delaware. The California action was stayed on the basis of the Delaware choice-of-forum provision in the Securityholders’ Agreement. An action was then filed in the Delaware federal court, but it was dismissed for lack of subject matter jurisdiction. Another action was then filed by West in the Superior Court of Delaware. In the Superior Court, the defendants moved for summary judgment, moved to transfer the action to the Chancery Court, and moved to strike West’s demand for a jury trial on the basis of a jury trial waiver in the Securityholder’s Agreement.[2] The Securityholders’ Agreement upon which the West court focuses its attention is not even mentioned in this Delaware decision. Subsequently, the motion to transfer to the Chancery Court was granted, and in so doing the demand for a jury trial was functionally denied in that the Chancery Court (being expressly a court of equity) does not conduct jury trials.

This gave rise to the motions that led to this opinion. Recall that previously the action filed in California had been stayed based upon the choice-of-forum provision in the Securityholder Agreement. His Delaware suit now moved to the Court of Chancery, West returned to the California action and asked that the stay on its proceeding be lifted on the basis that (1) in Chancery Court there is no jury, and (2) under California law, a predispute waiver of a jury trial (other than by means of an agreement to arbitrate enforceable under either the federal or California arbitration acts) is unenforceable. Needless to say, the defendants, who otherwise finally have the dispute in a forum agreed to in the Securityholder Agreement, disagreed.

Article I, section 16 of the California Constitution provides that “any waiver of the inviolate right to a jury determination must occur by the consent of the parties to the cause as provided by statute.” Under the related statute, as interpreted in Grafton Partners v. Superior Court,[3] “a jury may be waived in civil cases only as provided in subdivision (d)” of section 631 of the California Code of Civil Procedure. That provision, since redesignated subsection (f), provides:

A party waives trial by jury in any of the following ways:

(1) By failing to appear at the trial.

(2) By written consent filed with the clerk or judge.

(3) By oral consent, in open court, entered in the minutes.

(4) By failing to announce that a jury is required, at the time the cause is first set for trial, if it is set upon notice or stipulation, or within five days after notice of setting if it is set without notice or stipulation.

(5) By failing to timely pay the fee described in subdivision (b), unless another party on the same side of the case has paid that fee.

(6) By failing to deposit with the clerk or judge, at the beginning of the second and each succeeding day’s session, the sum provided in subdivision (e).

These limitations upon the capacity to waive a jury trial are exclusive; “unless the Legislature prescribes a jury waiver method, we cannot enforce it.”[4] Further, it has been held that a written consent under subsection (2) may be given only after the action is pending; “both the agreement to waive jury trial and the filing of any such agreement must occur subsequent to the commencement of the lawsuit.”[5] West would argue that the provision of the Securityholder Agreement requiring that his dispute with ACRE and the other defendants be resolved in the Delaware Chancery Court and without a jury violated his California constitutional right to a jury trial.

Certain earlier California decisions have indicated that choice of forum and choice of law that in application waived a right to a jury would not be enforced by a California court. As cited in the West decision, Handoush v. Lease Fin. Grp., LLC[6] involved an agreement containing a New York choice-of-law/forum provision and a waiver of a jury trial. New York has no policy against predispute jury waivers, and it seems questionable that a New York court would give appropriate deference to California’s policy against predispute jury waivers:

Here, enforcing the forum selection clause in favor of New York will put the issue of enforceability of the jury trial waiver contained in the same agreement before a New York court. Because New York permits predispute jury trial waivers, and California law does not, enforcing the forum selection clause has the potential to operate as a waiver of a right the Legislature and our high court have declared unwaivable.[7]

Finding the question presented to be analogous to those in Handoush, the West court determined that “refusing to lift the stay on the grounds the Securityholders’ Agreement forum selection clause is enforceable would result in a pre-dispute waiver of West’s ‘inviolate’ right to a jury trial.”[8] Further, as the action has been transferred to the Delaware Chancery Court, and as the Chancery Court does not utilize juries (except on an advisory basis), “continued enforcement of the forum selection clause in the Securityholders’ Agreement would prevent West from having a jury trial. The pre-dispute forum selection clause is effectively and impermissibly used as a pre-dispute waiver of jury trial.”[9]

On that basis the stay on the California litigation initiated by West has been lifted. How the Delaware Chancery Court will react remains to be seen.

Implications of West v. Access Control

To a certain degree, it is too soon to fully assess the implications of the West v. Access Control decision. It is a decision of a trial court that but for commentary such as this article, could be lost in the background. However, with the continual strides being made in electronic searching of court dockets, seldom can we expect anything to remain lost and therefore uncited. At minimum, even if the decision cannot be cited as anything more than persuasive authority, it addresses a common fact pattern and will be cited under the argument of avoiding conflicts among decisions.

There is as well the possibility of reversal on appeal, which is dependent upon the defendants not only bringing an appeal, but also achieving a reversal. In light of the wealth of earlier California appellate decision relied upon in the West decision, that appeal may be swimming upstream.

What the Delaware court will do is an open question. There are examples of decisions in which the Delaware courts have applied California law notwithstanding a Delaware choice-of-law provision. For example, in Ascension Ins. Holdings, LLC v. Underwood,[10] an injunction was denied to enforce a noncompete agreement entered into in California but electing to be governed by Delaware law that would be enforceable in Delaware but nonenforceable in California. However, there the Delaware court applied California law to the parties before it. That cannot be the resolution here—namely, the suit proceeding but with California’s insistence upon jury trials respected—because the matter is before the Chancery Court, and Chancery is a court of equity that does not use juries.

Setting those points aside, this decision is a wake-up call to anyone engaged in contracts with persons[11] resident in California, but the problem is not restricted to California. Rather, many state constitutions have provisions describing the right to a trial by jury as inviolate.[12] A contracting party in any state with a similar provision may argue that if in a particular forum they would not be entitled to a jury, then the choice of law/forum is unenforceable against them. At that juncture, the party seeking enforcement likely must show that the law of that state (unlike California) permits predispute jury waivers.[13] There may be other states utilizing the same rule, and it is always possible that a state determines that reversal of its prior policy allowing waiver should be changed.

Most legal opinions either exclude or heavily qualify an opinion as to the enforcement of choice-of-law/venue provisions.[14] Are those now delivering those opinions going to either do further investigation into the state constitutions and statutes to determine whether the agreement as written is enforceable, or will those opinions go by the wayside to be replaced with exclusions from the opinion?

Another significant issue is the balkanization of the law, particularly the law of business organizations. West was a member in ACRE, a Delaware-organized LLC. In becoming a member, he agreed that the controlling operating agreement, and in the absence thereof (entirely or as to a particular matter) the Delaware LLC Act, which itself incorporates Delaware’s contract law,[15] would determine his rights and obligations. The West court made the point several times that its decision was based upon the terms of the Securityholders’ Agreement; the terms of that agreement were not discussed beyond the jury waiver and choice-of-law/forum provisions, so we are left in the dark as to whether the Securityholders’ Agreement would, under Delaware law, be treated as a limited liability company (operating) agreement. Even so, the California action that may now proceed contains a count for breach of fiduciary duty,[16] and the only credible source for a duty that could have been breached is the ACRE operating agreement. According to the West decision, the Second Amended and Restated Limited Liability Company Agreement contained the same choice-of-forum provision as the Securityholders’ Agreement. Bear in mind that West was a manager of ACRE (CFO and COO), and under the Delaware LLC Act he consented to jurisdiction in Delaware for matters connected with the LLC.[17] Under this decision, West enjoys the benefits of being a member/manager of ACRE and avoids the burdens imposed upon members and managers; he asserted, and the West court agreed, that what is good for the goose is in fact not good for the gander.

Consider a Delaware LLC in which our California resident is a member (and perhaps as well a manager). The LLC has no other connection with California, and neither it nor its constituents are subject to the specific or general jurisdiction of the California courts. Although our hypothetical actor may want to avoid the jury waiver and choice-of-law/venue provisions of the controlling operating agreement, in order to gain personal jurisdiction, he or she may be required to bring suit in a foreign jurisdiction that will enforce those contractual obligations. He or she should not be heard to then object to being deprived of a right guaranteed by California law. Assume our plaintiff does not prevail, however. Will he or she have an after-the-fact ability to challenge the judgment when it is to be enforced in California? Although not listed as an affirmative defense, perhaps chutzpah should be.

West was (or so it would appear) a California resident at the time he signed the Securityholders’ and other agreements. What would be the outcome if at that time he had been a resident of another state that would enforce the jury waiver and choice-of-law/forum provisions, but then moved to California? Can he (or should he be able to) alter his contractual obligations simply by moving across a state border? If he may, how can parties to an agreement containing a jury trial waiver ever know that the obligation will be enforceable?

This decision is another cog in the jammed-up machine that is the application of the internal affairs doctrine and basic conflicts-of-law analysis between Delaware on the one hand (it being as well a proxy for some 48 other states) and California on the other hand. Another recent decision on the point, Juul Labs, Inc. v. Grove, 2020 WL 4691916 (Del. Ch. Aug. 13, 2020), will be reviewed in a forthcoming article.

[1] William West v. Access Control Related Enterprises, LLC, Superior Court of California, County of Los Angeles, Case BC642062 (July 29, 2020).

[2]See also West v. Access Control Related Enterprises, LLC, No. N17C-11-137 MMJ CCLD, 2019 WL 2385863 (Del. Super. Ct. June 5, 2019) (granting in part and denying in part a motion to dismiss).

[11] I presume, and I have not researched the point, that the California Constitutional provision on jury trials is applicable only to natural persons and not business entities.

[12]See, e.g., Ga. Const. art. I, § 1, ¶ XI(a) (“The right to trial by jury shall remain inviolate, . . . .”); Kan. Const. Bill of Rts. § 5 (“The right of trial by jury shall be inviolate.”); Mo. Const. art. I, § 22(a) (“That the right of trial by jury as heretofore enjoyed shall remain inviolate; . . . ,”); Or. Const. art. I, § 17 (“In all civil cases the right of Trial by Jury shall remain inviolate.”). In Kentucky the right to a trial by jury is not only inviolate, it is as well “sacred.” See Ky. Const. § 7.

[13]See generally, Contractual jury trial waivers in state civil cases, 42 A.L.R.5th 53. Notably, Georgia will not enforce a predispute jury waiver. See Bank South, N.A. v. Howard, 264 Ga. 339, 444 S.E.2d 799 (Ga. 1994).

[14]See, e.g. Gail Merel et al., Common Qualifications to a Remedies Opinion in U.S. Commercial Loan Transactions, 70 Bus. Law. 121, 130 (Winter, 2014/2015).

[15]See Del. LLC Act § 18-101(9) (definition of limited liability company agreement); id. § 18-1104 (incorporating law and equity).

[17]See Del. LLC Act § 18-109; see also CLP Toxicology, Inc. v. Casla Bio Holdings LLC, No. CV 2018-0783-PRW, 2020 WL 3564622 (Del. Ch. June 29, 2020).

Forever 21 is well known as a “fast-fashion” mall retailer that grew quickly from its founding in 1984 through most of the past decade, appealing primarily to a young demographic whose preferences for cutting-edge fashion would otherwise exceed their budgets. In recent years, however, the retailer has been beset by a number of controversies and, more importantly, was a latecomer to the e-commerce revolution that changed the way the world shops and, in particular, the way Forever 21’s target demographic shops. Ultimately, the woes brought on by these challenges led Forever 21 to commence chapter 11 bankruptcy proceedings early in the fall of 2019 and to close over 100 locations quickly thereafter in an attempt to restructure its remaining operations.

A few months later, a buying group consisting of Simon Properties Group, a mall landlord at nearly 100 Forever 21 stores; Brookfield Property Partners, another major Forever 21 landlord; and Authentic Brands, a brand-management company whose portfolio includes such formidable names as Judith Lieber, Hickey Freeman, and Juicy Couture, successfully bid to purchase substantially all of Forever 21’s assets for $81 million in cash and the assumption of certain liabilities through a sale conducted under the auspices of the bankruptcy court under section 363 of the Bankruptcy Code. There were no other bidders for the assets, and vendors are expected collectively to write off hundreds of millions of dollars of claims against Forever 21 that will never be repaid. The buyers, meanwhile, will chance that they can successfully rehabilitate Forever 21 around a core that includes most of the retailer’s remaining U.S. stores and, in particular, one assumes, those located within the new owner groups’ mall properties.

Analysis

Forever 21’s bankruptcy came with the usual share of victims, including hundreds of vendors owed many millions of dollars, as well as Forever 21’s mall landlords. Unlike earlier retail restructuring cycles, mall landlords are no longer able to easily replace shuttered or struggling retail dodos with surviving, fitter competitors. This is because more recent retail bankruptcies have been precipitated less by problems with the pricing, value, demand, or other qualities associated with merchandise offered for sale, but rather by the platform upon which it is sold. Even prior to the devastating nationwide lockdowns caused by the coronavirus pandemic, consumers already were increasingly eschewing physical “bricks and mortar” stores for the internet, which has required traditional retailers to reconceptualize their businesses so that their stores become complements to their online presence that usually translates into smaller and/or fewer physical locations. That has a direct, material effect on retail landlords, and mall landlords in particular, who look to the marketing and name recognition provided by marquee national retail chains to drive foot traffic to their malls. In the increasingly frequent event that any of those national retailers are faced with bankruptcy or go out of business, there may no longer be eager competitors lined up to take their place because the competition is either primarily operating from a virtual, rather than actual, premises or is itself trying to right-size its physical retail footprint and is not looking for new space of that size or scale.

Without readily available replacements, therefore, mall owners are incentivized to try to keep struggling retail chains afloat, particularly where a particular retail chain has many locations within a small number of mall owners’ portfolios. Even where a distressed retailer’s prospects are questionable or too speculative for another third-party buyer, one or more major landlords may be willing to take a leap of faith on a retailer’s post-bankruptcy business plan to avoid the cost of portfolio-wide vacancies of a name-brand retailer and the potential domino effect on other stores within the same malls.

Indeed, that appears to be exactly what happened with Forever 21. The group that included Simon and Brookfield was the only group that bid—at a price too low to permit any recovery to Forever 21’s unsecured creditors. The fact that no third party came in with a competing bid under those circumstances strongly suggests that the Simon/Brookfield bid was more defensive rather than an inherent value proposition presented by a rehabilitated Forever 21. It should also be noted that this was not the first time these landlords have bought a distressed retail chain tenant out of bankruptcy—they did essentially the same thing in the chapter 11 cases of Aeropostale, a clothing chain that targets a demographic similar to that of Forever 21.

Is the purchase of troubled mall retailers by their landlords likely to become prevalent in retail chapter 11 cases? The circumstances under which such purchases are likely to make economic sense are narrowly circumscribed, which suggests that its potential to become a trend may be limited.

First, the retailer at issue must have a Goldilocks quality about it: If its rehabilitated future looks too good, then it will either attract exit financing in an amount sufficient to fund a stand-alone plan of reorganization or, if it chooses to reorganize through a sale of its business, it will attract an array of third-party financial and strategic buyers that will bid up the business to the point where it no longer is attractive to the landlords, both because the price is too high and because the very need for the landlord bid will have been eliminated or mitigated by the going-concern purchase of the business by a third party. On the other hand, if a seller’s prospects even after an operational restructuring appear weak, then the anticipated costs of preserving it, including the likelihood of ongoing losses, quickly outweigh any benefit associated with its presence within the bidding landlords’ portfolios.

Second, in order for the cost of the landlords’ investment to offer meaningful synergies, the particular tenant footprint must have the requisite level of concentration within the mall portfolios of a small number of large landlords, all or nearly all of whom must be interested in participating in the bid.

Third, the debtor-tenant itself must be a retailer that is an attractive tenant to its mall landlord in terms of its ability to drive mall foot traffic among a desirable demographic. It is probably not a coincidence that both Forever 21 and Aeropostale market to a young, highly desirable segment of the retail market that mall owners like to see frequenting their properties. One can surmise that a retailer specializing in adult incontinence products, for example, would not draw as much interest from mall owners, regardless of how rosy its post-bankruptcy EBITDA projections.

Finally, while the long-term ramifications of the COVID-19 crisis are not yet known, for the short-to-medium term it seems likely that the pandemic will independently create deepened levels of distress and liquidity constraints for mall landlords that may preclude their employment of the Brookfield/Simon strategy, irrespective of the advantages the strategy otherwise confers.

For these reasons, among others, it seems likely that the precedent set by Forever 21 and Aeropostale has created a useful, but specialized tool in the distressed retail toolbox for successfully dealing with a narrow band of chapter 11 cases from time to time, rather than a new paradigm for resolving retail bankruptcies in the new digital economy.

As we write this article mid-summer of 2020, with a resurgence in COVID-19 cases in the South, Southwest, and Western United States, uncertainty caused by the virus abounds, including in the world of M&A transactions. Due to the unpredictability caused by the pandemic, buyers and sellers of companies have less ability to predict the earnings and future performance of the target business. As either Mark Twain or Yogi Berra supposedly said, “it is difficult to make predictions, particularly about the future.”

In this current environment, parties to M&A transactions are likely to use earnouts more frequently. For parties structuring a transaction to deal with future uncertainties caused by the pandemic, earnouts can bridge the valuation gap between buyers and sellers. The purpose of an earnout is to allocate the future risks and rewards of a target business, with both parties benefitting from a successful outcome and sharing the risk if things do not work out as hoped. Earnouts, however, are inherently difficult to design and implement because they require the parties to anticipate what might happen in the future.

Earnouts are often half-jokingly referred to as “litigation magnets.” The high stakes involved means that disputes can get particularly ugly,[1] causing the expenditure of large amounts of time and money in the ensuing litigation. An earnout that has been carefully designed and considered by the parties is worth the upfront effort if it can avoid or allow a dispute to be quickly resolved.

This article brings together the perspectives of two veteran M&A attorneys with a dispute management director at SRS Acquiom. SRS Acquiom brings a wealth of experience since it has served as the seller representative, or in another comparable capacity, in over 2,100 transactions. SRS Acquiom has seen firsthand when earnouts work as intended and when they devolve into difficult-to-resolve disputes. We will take a detailed look at the complex components of a well-structured earnout from our collective experience, and discuss some best practices for designing earnouts to minimize disputes.

Use of Earnouts Before the COVID-19 Pandemic

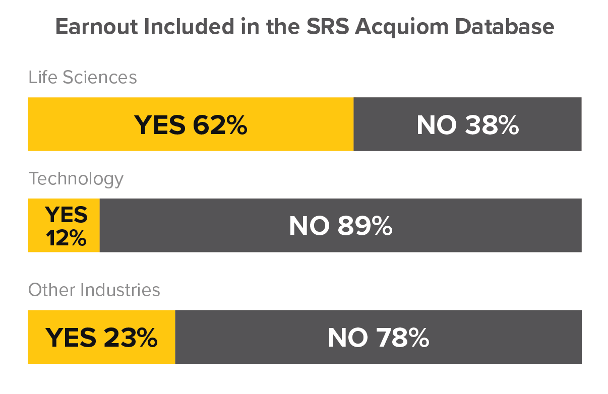

The use of earnouts often differs by industry. Using the MarketStandardTM transaction database of SRS Acquiom, which includes 1,300+ private-target acquisitions from 2015 to date, we compared the use of earnouts in life sciences, technology, and other industries over the past 18 months:

There is a long tradition of earnouts in the life-science industry focusing on regulatory and other specialized milestones that are not generally used for earnouts in technology and other industries. Although there are lessons to be learned from life-science transactions, in this article we focus primarily on using earnouts outside of the life-science industry because life-science transactions are so specialized, and their milestones are not generally used for earnouts in technology and other industries.

Outside of the life-science industry, buyers and sellers are generally more wary of using earnouts. As shown in the chart above, prior to the pandemic, earnouts were used in only a relatively small portion of the transactions[2] to bridge a valuation gap. Due to the uncertainty caused by the pandemic, we expect the use of earnouts to increase across these other industries.

Is an Earnout the Right Tool to Bridge the Valuation Gap?

For some earnout disputes, the root cause of the dispute was that the earnout structure was the wrong way to bridge the valuation gap. As a result, the buyer and seller may have had different expectations for the earnout, and their interests were not aligned after closing. Whether a specific earnout structure is the right tool to bridge the valuation gap begins with an analysis of the following questions:

Will the operations or products of the target business be merged with those of the buyer, or will the business be operated on a stand-alone basis? Earnouts measured on earnings or EBITDA make more sense when the target business will be operated on a stand-alone basis after closing. It is easier to design and track whether the earnings have been achieved during the earnout period when the business is compartmentalized. On the other hand, if the operations of the target business will be merged or otherwise integrated with those of the buyer, earnouts based on earnings become difficult to manage and track because both revenues and expenses must be determined. When the acquired business operations are merged with the buyer, an earnout based only on revenues may be more appropriate. Even then, however, if the products or services of the target company are sold as a “bundle” or otherwise combined with the products or services of the buyer, revenues specific to the sold business may be difficult to determine with objective certainty.

Will the management team of the seller continue working for the buyer, and if so, will the goals of the earnout align with the roles and authority assigned to the management team? If the seller’s management team will not be working for the buyer, or will have no real influence over the buyer’s operations and decision making after closing, the seller may not have faith that the buyer will be sufficiently focused on or motivated to achieve the earnout. The seller or its representative may find it challenging to adequately monitor earnout progress absent former management’s ongoing and direct role in managing the business. The reality is that even robust milestone reporting requirements may not tell the full story.

If the seller’s management team will continue working for the buyer, does the management team have a significant equity stake in the seller so that the management team will enjoy a meaningful amount of the earnout? In many technology companies, the founders and the management team may have been diluted over multiple funding rounds and own a relatively small equity stake in the target business. Similarly, in many private equity portfolio companies, the management team may have a small amount of equity. In these situations, the management team may not have a sufficiently large interest in the earnout to have a compelling incentive to achieve it. Instead, the seller’s management team may have business objectives and compensation incentives after closing that are different from those of the earnout.

The answers to these questions may lead to the conclusion that an earnout is the wrong approach. Too often, the parties do not pay enough attention to whether an earnout works in the particular circumstances of a specific transaction—in essence “kicking the can down the road” on valuation. If the buyer and seller have different expectations on whether and how the earnout will be achieved, the result can lead to a costly dispute.

Particularly, if an earnout is a significant portion of the consideration for a transaction, the seller must recognize the inherent risks involved with an earnout. It can be difficult and expensive to challenge an unfavorable earnout report even with seller-favorable earnout terms.

What Is the Right Metric to Use for an Earnout?

Determining the right earnout metric begins with an analysis of the methodology used by the buyer to value the target business, and whether that methodology is appropriate to measure the business during an earnout period. Three common ways to value target companies are:

multiple of prior 12 months of EBITDA, which is used for companies with earnings (this is the most common valuation methodology);

multiple of revenues, most commonly used for software and other technology companies that have been able to build significant sales but are not at the stage of having earnings; and

a “build versus buy” analysis, in which the buyer assesses the cost to duplicate the functionality of the seller’s product or technology from scratch, versus the cost to buy the seller and its entire workforce (this measure is most commonly used for early-stage software and other technology companies prior to achieving significant sales revenues).

Generally speaking, the valuation methodology used to value the business begins the discussion for the earnout metric that will be used. If a multiple of EBITDA was used to value the business, then an increase in EBITDA is a logical place to begin. The same for revenues. When a “build versus buy” methodology is used, then neither EBITDA nor revenue measures may fit the situation. In any event, the choice of the earnout metric will require a much deeper analysis of the value that the buyer is trying to create by buying the target business, and the buyer’s business plan to create this value after closing.

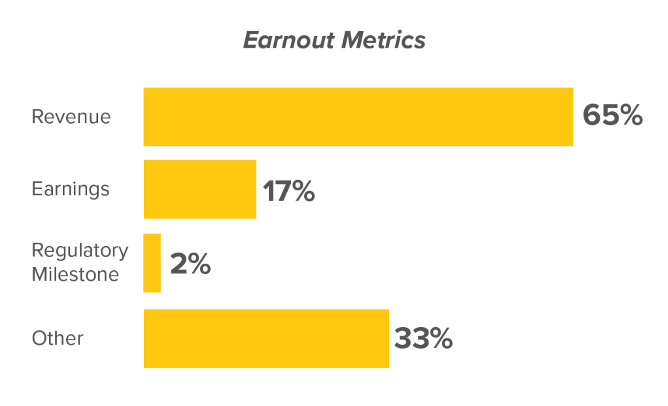

Using the SRS Acquiom MarketStandardTM transaction database, for nonlife-science transactions over the past 18 months, the most common metrics for earnouts are shown below:[3]

Before the pandemic, we were in a seller’s market with auctions of quality companies attracting numerous bidders so that sellers could obtain high prices and favorable terms. Sellers generally prefer using revenues as a metric because revenues do not include costs and expenses and are easier to measure with less ability for the buyer to skew the results. On the other hand, buyers favor using EBITDA as a metric, which includes costs and expenses, because EBITDA is generally used to gauge a company’s true operating performance and to value a business for sale. If we shift to a buyer’s market after the pandemic, we can expect more earnouts based upon EBITDA, or a combination of EBITDA and revenues, than in the past.

Nonrevenue/EBITDA metrics are common in life-science deals where the value of a target company may be based in substantial part on the future of a particular drug. For life-science deals, revenues and regulatory milestones are the most common metrics used for earnouts, or some combination, and earnings are rarely used.[4]

Outside of life-science deals, SRS Acquiom has seen some increased use of project-based or other nonrevenue/EBITDA metrics—sometimes in conjunction with these traditional approaches. The COVID-19 pandemic will likely continue to have unpredictable effects on revenue and EBITDA, so sellers and buyers should be open to other approaches for earnouts. SRS Acquiom has seen an interesting range of nonrevenue/EBITDA metrics used in conjunction with revenue and/or EBITDA, which include the following:

Project-based metrics providing for a payment if a certain discrete project is brought to completion. For software companies, this may mean bringing a certain product or product version to market. Obviously, the success parameters and resources to be dedicated to the project must be carefully defined.

Sales-based earnouts where a specific number of product units must be sold.

Earnouts tied to store openings in response to the COVID-19 crisis. This approach essentially shifts the risk to the sellers if the pandemic continues to impede retail operations.

What Are Best Practices for Defining the Metric in the Purchase Agreement?

The answer to this question can be best summed up as follows: (i) be as specific as possible, (ii) use objective measures that lend themselves to outside standards of measurement by third parties, and (iii) use illustrative examples whenever possible.

For nonrevenue/EBITDA metrics, the parties must be as specific as possible when describing the milestone, whether a milestone has been achieved, and the deadlines for achieving each milestone. Parties might use commonly used terms to describe a milestone, but fail to take into account the differing interpretations of those terms if a dispute arises years later or if unexpected scenarios arise.

For EBITDA, the definition of “EBITDA” can be complex, and it is becoming more common to define “Adjusted EBITDA”—with sometimes detailed specifications for how EBITDA is being adjusted. The analysis requires the parties to review each line item of the income statement of the target business to determine whether the specific line item will be included in the calculation of EBITDA for purposes of the earnout. The analysis also requires the parties to think about possible types of revenues or expenses that would be unfair to include in the calculation, such as gains or losses from the sale of capital assets, gains or losses caused by a change in accounting policies, and gains or losses caused by one-time events outside of the ordinary course of business. For example, if the target business has a loan under the Paycheck Protection Program, the parties will want to specify that forgiveness of the loan does not factor into the EBITDA calculation. A particularly difficult area is to determine how any shared expenses—such as insurance or other overhead—will be allocated between the target business and the rest of the buyer’s business.

It can be helpful to provide a sample EBITDA calculation as an exhibit to the purchase agreement using prior financial statements showing how EBITDA was calculated and how it will be calculated for the earnout calculation. This is commonly done for other financial metrics such as net working capital and the components of what constitutes working capital in a particular transaction. It becomes more difficult, however, if the acquired business will be integrated into a larger, possibly more sophisticated business, and the accounting will be changed to conform to the accounting practices of the buyer. In that case, it is helpful to prepare a sample template using the buyer’s accounting practices to show how EBITDA will be calculated and attach that template as an exhibit to the purchase agreement.

For a financial metric such as EBITDA, the next issue is the proper accounting principles. If the target business has audited financial statements prepared in accordance with Generally Accepted Accounting Principles (GAAP), then a typical definition of the “Accounting Policies” in a purchase agreement would be: “GAAP, applied using the same accounting principles and standards, policies, procedures and classifications used by the Company in preparing the Audited Balance Sheet.” What if there is a conflict between GAAP and the methodologies used by the Company in preparing the Audited Balance Sheet? It helps to have a controlling statement in the definition to provide which one will control if there is a conflict. This also applies if there is an accounting term specifically defined in the purchase agreement that differs from GAAP—it helps to have a controlling statement within the definition of “Accounting Policies” to provide that the defined term will control if there is a conflict with GAAP.

Conflicts also can arise when a target business is a relatively small business being acquired by a much larger company with more rigorous accounting practices. Even if the small target company has audited financial statements prepared in accordance with GAAP, there can be differing interpretations of GAAP and different policies, such as the determination of “materiality.” Accordingly, it helps if those differences in how GAAP is applied by the seller and the buyer are identified during due diligence so they can be properly dealt with in the purchase agreement definitions of the applicable accounting policies and other financial terms used for the earnout.

Another challenge is that smaller companies may not have GAAP-based financial statements, and may instead use the cash basis of accounting, the tax basis of accounting, or some hybrid. For an earnout, especially if the buyer uses GAAP, it is important to determine how the financial statements of the target business and the buyer differ, and how the earnout metrics will be determined by the buyer. In this situation, it is helpful to attach a template as an exhibit to the purchase agreement showing how EBITDA or any other metric will be calculated for purposes of the earnout.

How Else Do You Structure an Earnout to Achieve the Right Result?

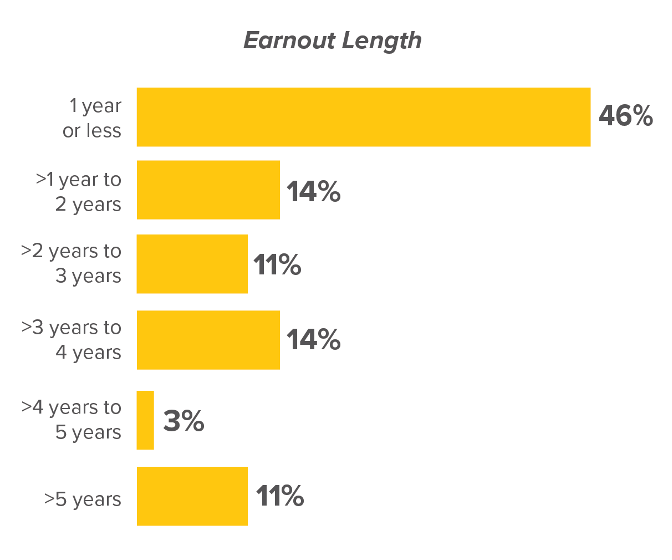

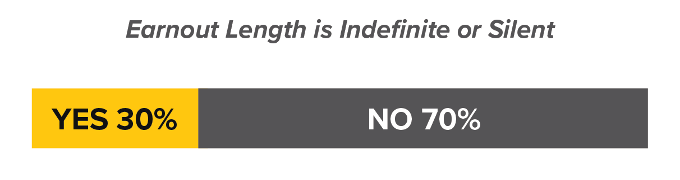

Using the SRS Acquiom MarketStandardTM transaction database, for nonlife-science transactions over the past 18 months, the earnout time periods are set forth below. Interestingly, there is a slight trend toward earnout length that is indefinite or does not expire, particularly with nonfinancial or other milestones. The lack of a deadline can remove a frequent source of dispute: whether the milestone was timely achieved, or would have been timely achieved but for some act or omission of the buyer.

Prior to the pandemic, parties generally wanted the earnout period to be as short as possible. As a result of post-pandemic uncertainty, the time period for earnouts will likely increase from the current median of 24 months to longer timeframes. Given the unpredictability of how long it will take for businesses to recover from the pandemic, most companies have no visibility into what their results will be for 2020, and even into 2021. Therefore, earnout periods may extend into 2022, 2023, and beyond to give the seller more opportunity to achieve the earnout. When the earnout period increases, this places more burden on the buyer to manage and track the earnout throughout the longer timeframe. It also increases the risks that unexpected circumstances and events will occur that affect the business and restrict the buyer’s ability to make needed changes that could potentially affect the earnout, such as merging the business with other operations of the buyer.

According to the 2020 M&A Deal Terms Study published bySRS Acquiom, in nonlife-science transactions with earnouts, the earnout potential as a percentage of the closing payment averaged 30% in 2018 and 41% in 2019, although the median was likely significantly lower, given that some outlier transactions pulled the average up. Due to the changed environment after the pandemic, the earnout potential as a percentage of the closing payment may increase from the 41% in 2019 shown in the SRS Acquiom data to 50% or higher. By doing so, buyers will shift more of the uncertainty and risk caused by the pandemic to sellers. In turn, as the size of the earnout potential increases, there is more incentive for the seller to challenge the buyer over whether the earnout has been achieved. This leads to the next structural issue of whether the earnout should be structured as “all or none” or on a sliding scale.

It is an open question whether the sliding scale may lead to more earnout disputes. When an “all or nothing” threshold applies, it is frequently clear to both seller and buyer whether the earnout metric was achieved. A disagreement becomes a formal dispute only when it will make the difference between all and nothing. If the sliding scale applies, however, the disagreement may trigger a dispute at each stage if the disagreement is material. One recent SRS Acquiom matter illustrates this dynamic. It was unclear from the earnout provision whether a specific type of customer refund should be included as revenue. The disagreement over how to interpret the provision likely would not have mattered in an “all or nothing” structure. Given that a sliding scale applied, however, the difference was sufficiently material for the parties to engage counsel and escalate to a formal dispute.

One countervailing business argument for using a sliding scale, however, is that the “all or none” structure can be demoralizing to the seller’s management team (now working for the buyer) if it becomes clear that the earnout will not be achieved, and the sliding scale would maintain the incentive. Further, use of the sliding scale could reduce the amount subject to a dispute. If a sliding scale is used, it is important to use a floor and a cap to fence in the amount of the earnout payment.

That said, when an earnout is small relative to the size of the transaction, say 10%–15% as a percentage of the closing payment, and is based on EBITDA or revenue, it is not as important whether the earnout is structured with an “all or none” threshold in which the threshold must be reached to receive any portion of the earnout. For example, if the original purchase price was justified based on a sales run rate projected by the seller that now seems questionable, the buyer may request that the earnout be paid only if the sales are actually achieved.

When the earnout potential becomes a larger portion of the total consideration, and the earnout period is longer, the parties must focus on dividing up the earnout period in shorter intervals, and providing for partial payments for each earnout period. For example, for a deal closed today, the parties could set the earnout periods as calendar years 2021 and 2022, with a portion of the earnout paid for each period based on the percentage of the earnout goal that was achieved. When a sliding scale is used, this reduces the incentive to the buyer to try to skew the results if the earnout has an “all or none” threshold and the results are close to the threshold. With the uncertainty caused by the pandemic for 2020, some parties are starting the earnout period in 2021 with the thought that earnings for 2020 will not be an accurate measure of future earnings. Further, parties using partial payments for different earnout intervals may want to allow for catch-up payments if the earnout was not achieved during the initial periods, but was caught up in the final earnout period when measured over the entire earnout period.[5]

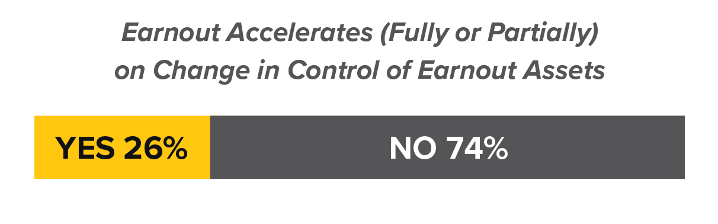

Another issue that may arise with an increase in earnouts is determining what happens to the earnout if the buyer is acquired during the earnout period. Should the earnout accelerate upon the buyer’s change of control, or continue in effect? Using the SRS Acquiom MarketStandardTM transaction database, for nonlife-science transactions over the past 18 months, the graph below shows the percentage of transactions that accelerate the earnout payment upon a change of control.[6]

The size of the buyer relative to the size of the target business is a big factor in whether the earnout should accelerate upon a change of control of the buyer. If the target business is a large portion of the buyer’s overall business, then the sellers have a strong argument that the change of control should trigger the earnout acceleration. On the other hand, if the buyer is substantially larger than the target business, the earnout is less likely to contain an acceleration upon a change of control. In either case, the purchase agreement should specify what happens to the earnout upon a change of control rather than leaving this silent.

In the right circumstances, the parties may consider including a buyout provision under which the buyer can pay a fixed sum, or use a different metric and time period to buy out and terminate the earnout. This can be especially helpful if the buyer believes there is a reasonable possibility that the buyer could be acquired during the earnout period and would not want the earnout to impede the sale of the buyer.

What Covenants Are Appropriate for Operating the Target Business after Closing with Respect to the Earnout?

Buyers and sellers will often vigorously negotiate whether there should be controls or other constraints on how the buyer operates the purchased business during the earnout period. Buyers naturally do not want any constraints; they argue that they need full discretion to run the business to deal with rapidly changing business conditions, such as what we are seeing right now with the pandemic. Sellers, however, want a fair shot at being able to earn the earnout, especially if the management team of the seller goes to work for the buyer. Many times, “soft” promises will be made to the seller for the financial support or other resources that the buyer will provide to the business after closing so that the earnout can be achieved, but those “soft” promises never make it into the purchase agreement and are generally unenforceable. The natural tension between the seller and the buyer over the buyer’s business decisions will be exacerbated if the earnout period is long.

The Standard Operating Covenants

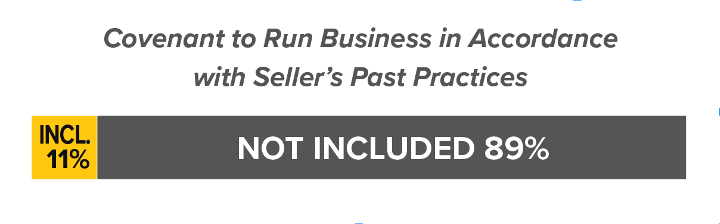

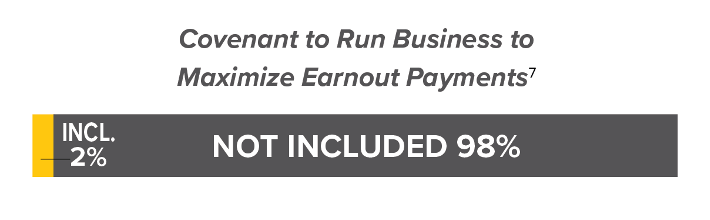

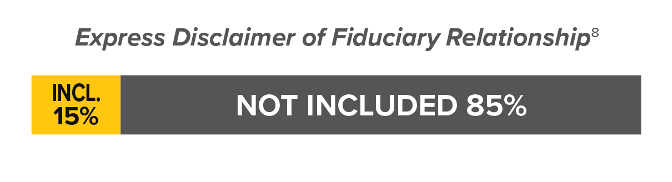

Using the SRS Acquiom MarketStandardTM transaction database, for nonlife-science transactions over the past 18 months, parties used some of the following covenants in purchase agreements in the percentages described below:

Sellers often push for a covenant that the buyer will operate the purchased business in accordance with seller’s past practices.

When sellers have a lot of leverage, they will request a covenant that the buyer will operate the business to maximize earnout payments. Although these types of covenants are sometimes agreed to by the parties to get the deal done, they must recognize the potential difficulties they are causing by using these covenants. It may not be entirely clear what the parties mean with these covenants. Many times, the buyer and seller have very different interpretations of these covenants. For the covenant to run the business in accordance with seller’s past practices, in a dispute the seller must create a factual record of how the seller operated the business prior to closing and then demonstrate that the buyer failed to do so during the earnout period.[9] If the buyer is dealing with pandemic fallout, perhaps by drastically reducing expenses due to lower customer demand, certain actions by the buyer may be prudent, but not consistent with seller’s past practices.

If the earnout period is long, buyers will be uncomfortable agreeing to any covenants that restrict their ability to run the business. Buyers will want to have a statement affirming that the buyer has full discretion to direct the management, strategy and operations of the purchased business. If buyers have negotiating leverage, they may also request a statement expressly disclaiming any fiduciary duties to the seller with respect to the earnout. This is an attempt to avoid a seller’s claim that the buyer did not abide by any implied duty of good faith with respect to the earnout. Even if the purchase agreement is silent regarding fiduciary duties, Delaware courts impose a high threshold for a seller to prevail on a claim based on an implied duty of good faith.