Board responsibilities are complex and continue to grow, with directors being held accountable for the governance, oversight, and, if necessary, management of the organization. This evolution of board responsibilities is long-term and has been further intensified by the pandemic and the economic uncertainty facing organizations of all types today. The chief legal officer (“CLO”), the chief financial officer (“CFO”), and other senior officers join the chief executive officer (“CEO”) as those with the senior-most responsibilities from the management side in ensuring that proper governance, oversight, and management are occurring.

The recent, ongoing developments regarding the survival of certain banks, and perhaps even the future shape of the banking industry as a whole, stand as a testament to the fact that the CEO, CFO, and the general counsel (“GC”) and CLO must join with the board and others in focusing on operational and capital cash flows. Indeed, both the CEO and CFO were named as defendants in securities litigation arising from the failures of Silicon Valley Bank and Signature Bank. Too often, companies deemed to be healthy have not focused on cash flows, which are often the critical indicator of a company’s ability to survive. Troubled companies understand the importance of the cash flows—for some, unfortunately, when it is too late.

Case Study

Sophisticated businesses, large and otherwise, recognize the importance of tracking cash flows. One of the authors of this article served as the CFO of a diversified holding company that was the managing general partner of two sizable general partnerships. In each one, the other two general partners were major insurance companies. However, the experiences in a partnership setting are equally applicable to a corporate structure.

Each partnership met quarterly. An important component of these meetings was the CFO’s review and discussion of financial and operational results. Every one of these discussions focused on partnership cash flows—basically, the receipts and disbursements from the normal course of operations, investment income, capital expenditures, and other significant cash items. Cash was addressed comprehensively.

All of the partners agreed that this was more useful than reviewing the income statement because it avoided esoteric accounting entries, as well as footnotes that may be confusing and distracting. The cash data was much more understandable and gave a clearer picture of financial performance, a picture that was supported by money in the bank or other liquid assets.

These meetings were an exercise in highly effective governance. The general partner representatives were informed and involved, and their institution had “skin in the game.” They understood the business and recognized that the tracking of the cash flows was the most effective way to stay on top of the business. They designated to their respective internal audit staffs the responsibility for reviewing the accounting work of the managing general partner’s accounting staff and that of the partnership’s external auditor.

Cash Flow Emphasis: Can’t Be Overrated

Directors of any company, in any line of business, would do well to adopt effective techniques to improve their financial oversight. Continuous oversight and interpretation of cash flows by board and senior management are essential. Very simply, cash flows are the organization’s lifeblood.

Cash flows can be measured in an effective, timely manner; and, to repeat, cash data can be much more understandable and give a clearer financial picture than an income statement. The comparison of budgeted to actual receipts and disbursements often gives a much clearer financial picture than reported revenues and expenses and net income on a generally accepted accounting principles (“GAAP”) income statement. Discussions about the causes of cash flow variances can uncover problems and opportunities without the need for approximations or adjustments. The cash flows either did, or did not, occur within the particular time period.

Operational and capital cash flows are concrete results not easily subject to manipulation. Thus, they can serve as a safeguard against efforts to manipulate income through revisions in accruals or reclassifications of operating expenses to capital expenditures. They can also avoid misunderstanding of results that include unbudgeted, one-time charges or results that have been adjusted to exclude such charges.

Accurate cash flow information can also help to highlight possible weaknesses in controls and negative developments not readily apparent in income statement measures, as in a case where a strong, corporate emphasis on customer sales growth, combined with a relaxing of the company’s product financing and credit granting controls, may be increasing risk to an unacceptable level.

It should be noted that certain cash flow information can be very complex—for example, the statement of cash flows that is presented in GAAP. This cash flow information is viewed by some as arcane and difficult to understand. Further, it does not provide the useful insights of business unit receipts and disbursements.

Authority for Cash Flow Management and Cash Control

Who should be given the authority for budgeting the operational cash flows, tracking the actual cash flows, developing the variance reports, and providing explanations of the variances that occur? There are many options. However, an effective approach involves having the company’s operating units work with a centralized financial unit such as treasury, financial analysis, or accounting or some combination of these financial units. The board typically looks to the CFO to play a major role in structuring the team responsible for budgeting, measuring, and explaining cash flows. Both the internal auditor and the external auditor can provide input to the team and assist in ensuring accuracy.

Analytical Model

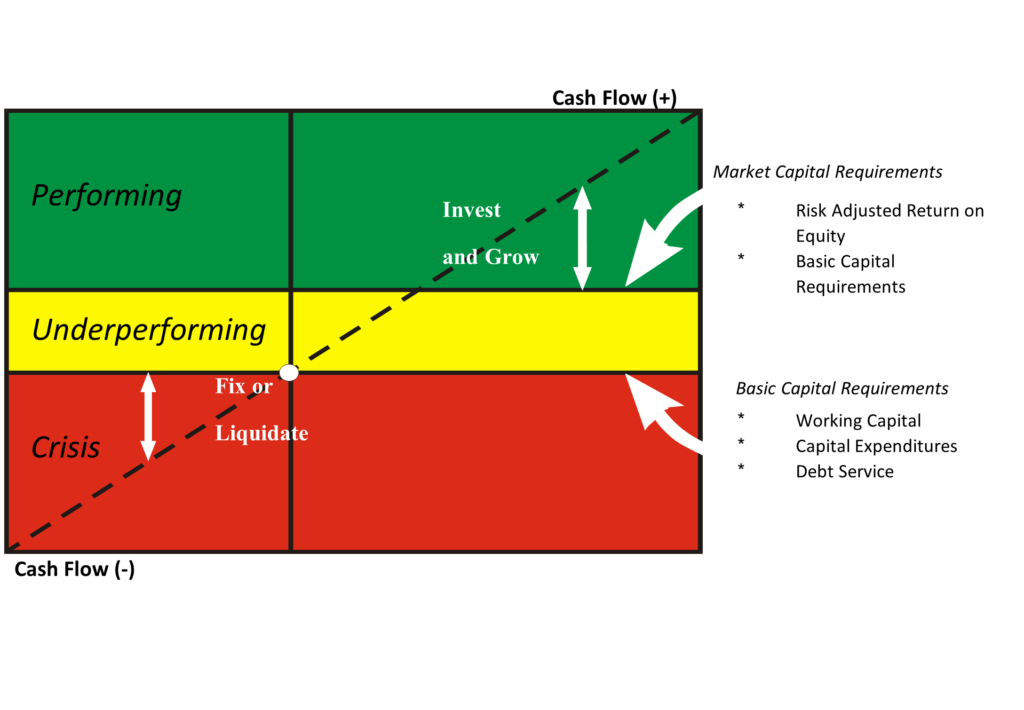

An analytical model, as shown here, aids in understanding and monitoring operational and capital cash flows. To analyze performance, such a model is developed and monitored for each business unit that generates cash flows. The model identifies basic requirements such as working capital, capital expenditures, and debt service and determines if cash flows will be adequate.

If operational cash flows do not provide enough for adequate working capital, do not fund budgeted capital expenditures, or do not cover the required debt service, the business operation is in the “crisis” zone. The options for the business operation are to “fix” or to “liquidate.”

Cash Flows: The Analytical Model.

The model also determines a risk-adjusted return on equity. When added to the basic capital requirements, this establishes the market capital requirements. As can be seen in the cash flows model, if the operational cash flows exceed the basic capital requirements but fall short of market capital requirements, the business operation is “underperforming.” While not in “crisis” mode, steps need to be taken to improve performance.

If the operational cash flows exceed the market capital requirements, the operation is in the “performing” zone. This shows an opportunity to invest and grow, pay down debt, buy back stock, or make cash distributions to equity holders.

This relatively simple presentation of cash flow data can give the board a solid understanding of whether its firm generates a positive cash flow and if its cash flow is adequate to meet present and future needs. This ability to monitor whether a firm is generating a sufficient cash flow will improve a board’s oversight and control system, in good times and bad. A board that understands the components of basic capital and market capital requirements, and how they are affected by cash flows, has considerable insight into the risks confronting the firm and can effectively address its oversight responsibilities.

Cash Control Activity

Cash control activity comprises two parts. The first involves managing the firm’s receipts and disbursements. The second involves monitoring the company-wide cash position.

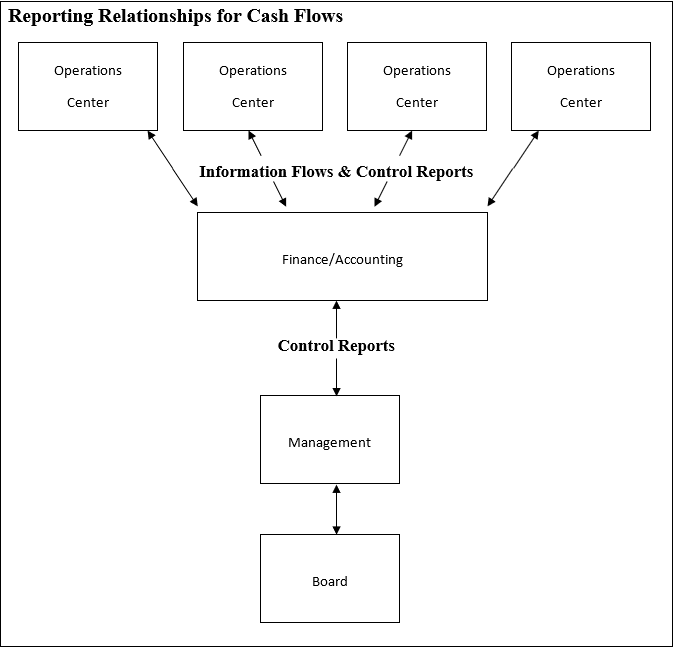

Controlling a firm’s cash inflows and outflows involves monitoring information and control reports between the firm’s operations centers and its cash management center; then, the flow of control reports from the cash management center to senior financial management. To effectively monitor cash inflows and outflows, the firm focuses on the following: the varying liquidity requirements and forecasting difficulties facing the different operations centers, development and implementation of effective reporting guidelines, and the manner and frequency with which periodic variance reports are developed and transmitted.

Liquidity Requirements and Forecasting Difficulties

Any attempt at developing an effective cash control system must start with the varying liquidity requirements and forecasting difficulties of the firm. Different sectors of a firm often have different liquidity needs and face unique problems in developing their forecasts.

Good cash forecasts are built on the correct recognition of the amounts of inflows and outflows expected to take place, and when these are expected to occur. The various areas within the firm may be able to forecast the timing for these cash flows, but they experience difficulty in estimating the amounts involved.

Electricity and gas utilities are examples of firms with this type of problem. As winter and summer approach, forecasters must predict the weather conditions in order to determine the projected revenues and expenses in the forecasting period. The timing of the revenues does not pose much of a problem for these firms because most bill a certain percentage of their customers on each day during the month.

With flows for previous forecasting periods available, it is not difficult to accurately estimate the percentage of revenues expected at a point in time. The problem is estimating the total amount of revenues for the period. Similarly, the timing of major outflows is predictable, but the problem is forecasting the amounts (like revenues) that will be affected by actual weather conditions.

Senior financial management must have consolidated cash forecasts early enough to permit them to react to the problems forecasted. This leads to the requirement that the cash management center obtain the data from the areas within the firm responsible for forecasting early enough to permit the consolidation of the data. The different areas may require varying lead times, particularly those subject to volatile revenues based on uncontrollable factors such as weather, and those with foreign exchange exposure.

Timing of the cash forecasts depends on when the various areas are able to prepare their estimates and on the time required to consolidate them and prepare the other cash-related data. Once the reporting times are set, they must be observed. This is particularly critical in the early stages of implementing a cash control system.

Each area of activity within the firm is constantly confronted with operating pressures, making it difficult for the various areas to complete their forecasts on time. However, those responsible for this activity need to know that their forecasts are being used and are important to the well-being of the entire company. Also, the cash management center needs to respond immediately when the forecasts are not received on time. Those areas that are late should be contacted as soon as the deadline has been missed, with a follow-up in writing. A further method for enforcing the guidelines is to maintain a checklist of the times at which the forecasts are received and forward the checklist to senior financial management.

Company-wide Cash Flow Reporting Structures

Similar consideration must be given to shaping the guidelines for reporting the actual cash inflows and outflows. These guidelines must be realistic and recognize the constraints that each of the areas faces.

An important point in the reporting of the inflows and outflows is the tie between cash management and cash control. The same information required for the cash management center can also be used for cash control purposes. A basic structure is set out here.

Reporting Relationships for Cash Flows.

Controlling the company-wide cash position requires the monitoring of all headquarters, division, and subsidiary bank accounts. Monitoring the headquarters-controlled cash position should be fairly straightforward because the cash management center is in constant communication with the headquarters’ accounting staff. Guidelines for maintaining the cashbook on each bank account, handling the support data, and reconciling the accounts are established in accordance with the requisites for internal control.

A means of monitoring non-headquarters-controlled accounts on a current basis must be developed. A weekly report indicating beginning and ending balances and total inflows and outflows along with monthly bank reconciliations permits timely monitoring of these accounts.

The importance of a firm’s cash flows has focused increased attention on the need for cash control systems. An effective cash control system enables the monthly, weekly, or daily monitoring of operation centers’ cash flows. This, in turn, creates an awareness of any unwarranted cash flow variances on a timely basis.

Cash Is King

Cash is “king” not only today—it has always been king.

One story that is often heard in financial circles describes the damage to a major firm whose board reviewed quarterly financial results with its sole focus on the income statement. The company’s board was told that operating income for the quarter was $490 million and was projected to increase to $525 million in the following quarter. According to this data, everything looked rosy, and no further questions were raised. However, the cash flow for the following quarter was projected to be a negative $475 million, a $1 billion difference. The firm filed for bankruptcy a few months later. Whether apocryphal or not, the point of the story is clear: ignoring cash flows can be dangerous for corporate health and bad for directors who should know better.

Understanding and monitoring cash flows is an important aid to boards in addressing their continually expanding responsibilities to oversee and direct their firms. Monitoring cash flows is an important tool in effective risk management, serves as a powerful check and balance on other forms of financial and operational reporting, and can aid in fraud detection. CFOs should coordinate the necessary financial and operational resources and take the lead in monitoring cash flows and, in doing so, create effective presentations to keep board members on top of the truest measure of a company’s finances—adequate cash flow. Also, CLOs can and should be an important check and balance regarding the existence and effectiveness of the cash flow management and control structure and their boards’ understanding and oversight of the structure.