Disagreements between parties over the purchase price in an acquisition often can be driven by their differing views of the selling company’s future performance and cash flows. To get to “yes,” parties may bridge their valuation differences by agreeing to an earnout, meaning they set agreed-upon metrics regarding the company’s post-closing performance and measure those metrics after closing. The seller then “earns” additional payments if the post-closing performance validates its valuation position. Parties must carefully define the details of how they will measure the earnout payment. The 2019 ABA Private Target Mergers and Acquisitions Deal Points Study (which examined 151 deals valued between $30 million and $750 million from 2018 and the first quarter of 2019) found that approximately 27 percent of those deals included earnout provisions.

The well-documented problem is that the earnout bridge the parties take to close their valuation differences often leads to litigation over whether the earnout was met or why it was not met.[1] Two recent decisions from the Complex Commercial Litigation Division of the Delaware Superior Court demonstrate how careful drafting affects the resultant litigation risk.

Collab9, LLC v. En Pointe Techs. Sales, LLC

In Collab9, LLC v. En Pointe Techs. Sales, LLC,[2] a seller argued that the implied covenant of good faith and fair dealing required the purchaser to maximize an earnout provision in an asset purchase agreement (APA). The seller alleged the purchaser breached the duty of good faith and fair dealing by “maintaining financial records in a way that made it impracticable to accurately determine the correct amounts of Earn-Out payments; creating a sham entity to move revenue off [its] books; and renewing certain contracts or transferring sales persons or accounts as a means of minimizing Adjusted Gross Profit.”[3]

The APA provided, however, that the “Purchaser shall have sole discretion with regard to all matters relating to the operation of the Business. Purchaser shall have no express or implied obligation to the Seller, . . . to seek to maximize the Earn Out payment . . . .”[4]

The purchaser moved to dismiss, pointing to the “sole discretion” provision it bargained for as defeating any implied covenant claim. The court agreed and dismissed the claim. Such “comprehensive and explicit” terms “demonstrate that the parties contemplated that a dispute might arise concerning the operation of the business post-closing, specifically whether the purchaser was acting in a manner that maximized the Earn Out.”[5] The terms that “granted broad rights to the purchaser to operate the business as it sees fit” meant the implied covenant could not give the seller rights it had “failed to secure for themselves at the bargaining table.”[6]

Merrit Quarum v. Mitchell International, Inc.

In Merrit Quarum v. Mitchell International, Inc.,[7] specific contractual language imposing post-closing obligations on the purchaser led to a different outcome. At issue was an earnout agreement, entered into by the parties in connection with a stock purchase agreement, that contained three provisions addressing the post-closing obligations of the purchaser. First, although it had “the power to direct the management, strategy, and decisions” post-closing, the purchaser agreed it would “act in good faith and in a commercially reasonable manner to avoid taking actions that would reasonably be expected to materially reduce the” earnout.[8] Second, the purchaser agreed to “act in good faith and use commercially reasonable efforts to present and promote the [acquired company’s products] to customers that could reasonably be expected to utilize” them.[9] And third, the purchaser agreed to upgrade or build a bridge between the companies’ systems, within six months of closing, to allow the purchasers to sell the acquired products to its existing customers and to assist in calculating the earnout.[10]

In an action asserting, among other things, noncompliance with the earnout agreement, the seller asserted breach of contract, not implied covenant, claims. Unlike Collab9, the court denied the purchaser’s motion to dismiss for some of the seller’s earnout allegations, focusing on the first and third obligations in the earnout agreement.

As to the first obligation in the earnout agreement, the court viewed the provision as a negative covenant requiring the purchaser to refrain from “positive action[s]” that reasonably could be expected to reduce the earnout or impede calculating the earnout. That obligation did not extend, however, to “avoiding inaction” because extending that obligation would “place the power to manage the company in” the hands of the seller.[11] In analyzing the complaint’s specific allegations, the court found that many fell short of asserting positive action. Those allegations focused on “decisions and strategies [the purchaser] could have pursued but did not,” such as consulting with the seller on marketing.[12] The claims that survived the motion to dismiss focused on positive actions such as “routinely cancel[ing] regularly scheduled calls to prevent [the seller] from promoting and selling” the products, and improper accounting decisions concerning minimum thresholds for bills, and diverting revenue to different products to avoid paying the earnout.[13]

With respect to the third obligation in the earnout agreement, the purchaser argued the seller could not plead damages resulting from the purchaser’s decision to build an alternative bridge between the parties’ systems. Relying primarily on Delaware’s minimal pleading standard for damages—which does not require pleading “damages with precision or specificity”—the court concluded it was reasonable to infer from the agreement that a specific solution was necessary to provide services to customers and calculate the earnout amount, and failing to build that solution could constitute damages.[14]

Takeaways

These decisions reflect how Delaware courts understand the incentives underlying, and details of, earnout provisions and hold parties to their bargain. Concessions today might get the deal done, but purchasers must be aware that they may be agreeing to significant restrictions on how they run the business post-closing, and as Merrit Quarum demonstrates, concomitant litigation risk if the earnout is not met. That holds true for sellers, who have the opposite incentives, and could give away their ability to hold the purchasers accountable post-closing. Said differently, through the lens of analyzing future litigation (especially at the pleading stage), purchasers face more risk (and sellers have stronger leverage) from having to comply with specific earnout provisions that impose post-closing obligations on the purchaser. In analyzing earnout provisions that do not require specific obligations and grant the purchaser significant discretion to operate the business, implied covenant claims are an uphill climb because Delaware courts refuse to use the covenant to give parties “contractual protections that they failed to secure for themselves at the bargaining table.”[15]

The 2019 ABA Private Target Mergers and Acquisitions Deal Points Study indicates that, at least in the available data, purchasers are “winning” these negotiations when they occur. Of the subset of deals containing earnouts, only about 30 percent include a covenant to run the business consistent with past practice or to maximize the earnout.

[1] Aveta Inc. v. Bengoa, 986 A.2d 1166, 1173 (Del. Ch. 2009 (“Earn outs frequently give rise to disputes, and prudent parties contract for mechanisms to resolve those disputes efficiently and effectively.”).

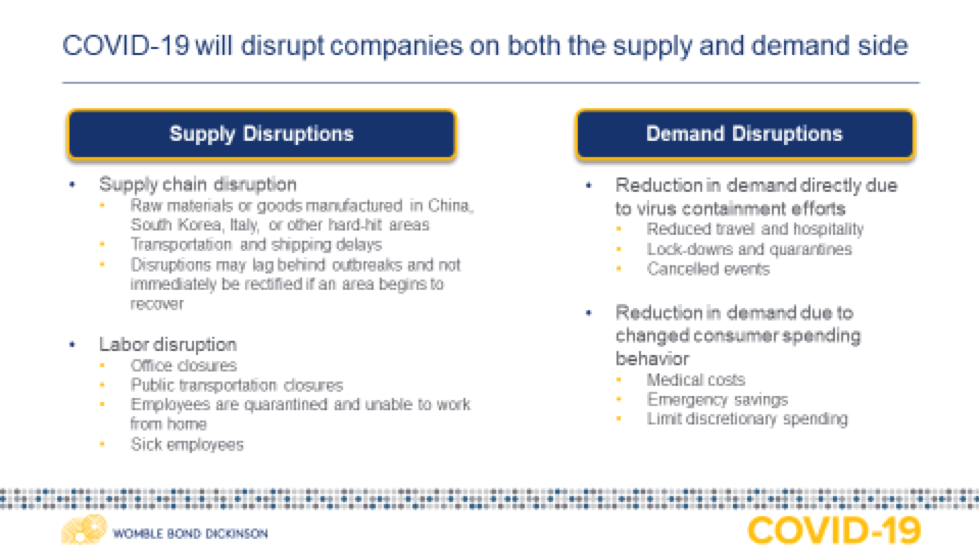

COVID-19 is having a dramatic effect on everyone’s lives. Our thoughts go out to all those who have been infected and their loved ones. While health has to be the first priority for everyone, this situation also raises significant economic and business issues. Businesses are seeing interruptions in supply, and many contracts can no longer be performed. Businesses are trying to decide whether and how to “push the pause button.” Others are unable to perform their contractual obligations and are trying to determine their legal rights. This article discusses some of the legal issues that inform the decision-making process.

II. Governmental Actions Are Restricting Business Activity

A. State of Emergency

As of March 20, 2020, there have been state of emergency declarations from the federal government in all 50 states and in all populated American territories because of the COVID-19 pandemic. Many of these emergency declarations have closed schools, limited public gatherings, and limited restaurant activities to takeout or delivery.

B. Shelter-in-Place Orders

Many states, including California, New York and Illinois, have also initiated shelter-in-place orders. Hundreds of cities and counties have also entered such orders. In the event of a shelter-in-place order or a state’s COVID-19 mitigation initiative, the distinction between “essential” and “nonessential” is crucial in assessing whether a business may have to reduce operations (to a state known as “minimum basic operations”) or close for a period of time.

There is uncertainty as to what is a “nonessential” business state-to-state, and authorities may not approach this consistently. California has referenced the Memorandum on Identification of Essential Critical Infrastructure Workers During COVID-19 Response from the US Department of Homeland Security, Cybersecurity & Infrastructure Security Agency (CISA). CISA identifies 16 sectors considered to be “essential,” and is part of the National Infrastructure Protection Plan (NIPP). This listing is advisory by CISA, but the California Order implements it as is in its listing of “essential businesses.”

However, some orders have listed different definitions of “essential business”—for example, the Alameda County order that affected San Francisco differs from the state-wide California Order. Pennsylvania and New York have each taken different paths on defining “essential business,” so there will be no “one size fits all” solution. Determining whether a particular business is required to close requires case-by-case analysis.

III. Contractual Defenses

It is basic contract law that a party that fails to perform is liable to pay damages for breach of contract. “Non-performance of a valid contract is a breach thereof … unless the person charged … shows some valid reason which may excuse the non-performance…” Cater v. Barker, 172 N.C. App. 441, 447, 617 S.E.2d 113, 117 (2005); see also Tejas Power Corp. v. Amerada Hess Corp., No. 14-98-00346-CV, 1999 WL 605550, at *2 (Tex. App.-Houston [14th Dist.], Aug. 12, 1999) (noting that while “a seller is bound to deliver the thing to the buyer… and, as a necessary consequence of this obligation, to do so at his own expense…” but also noting “extraordinary circumstances…may excuse the seller’s breach”); In re Appraisal of Metromedia Intern. Group, Inc., 971 A.2d 893, 900 (Del. Ch. 2009) (noting that a valid contract will be enforced “unless a party’s non-performance is excused.”)

Contractual defenses fall into three primary categories: (a) impossibility/impracticality; (b) frustration of purpose; and (c) force majeure.

A. Impossibility/Impracticability

The common law often recognizes a defense of impossibility. A party should not be held liable for breaching a contract that they could not perform. For example, laryngitis may make a singer’s concert performance impossible. Death and disability make personal service contracts impossible.

Some of the government orders surrounding COVID-19 may in fact render performance impossible. A contract committing to put on a theater show on March 30 is now impossible in locations where theaters have been ordered to shut down.

Some courts also recognize a defense of impracticability. Here, a party must show that performance has been made excessively burdensome by a supervening event. Generally, the supervening event must be: 1) unforeseeable (but not inconceivable); 2) not the fault of the excused party’s; 3) inconsistent with the basic assumption of the parties at the time of contract; and 4) something that a reasonable party would not have guarded against in the contract.

B. Frustration of Purpose

Some courts also recognize a separate doctrine called “frustration of purpose,” which is similar to the impracticality defense. Under this doctrine, performance is excused when a supervening event fundamentally changes the nature of a contract and makes one party’s performance worthless to the other. Unlike the other defenses, this doctrine has nothing to do with inability to perform. For example, if a contract called for cleaning a theater after a performance, the cancellation of the performance frustrated the purpose of the contract. The contract can still be performed (i.e., the cleaning personnel are available and the theater is available for cleaning), but the purpose (cleaning up after a performance) has been frustrated, making cleaning a wasted effort.

IV. Force Majeure Clauses

Unlike the preceding defenses, which arise under common law and potentially apply without regard to the language of the contract, the defense of force majeure is based on a contractual provision. Accordingly, companies should check their contracts, and those with their suppliers, for force majeure clauses. The clauses generally take two forms. The most general form excuses performance under the contract when it is due to any circumstance outside the party’s control, which presumably would include performances prevented by coronavirus. The second type of force majeure clause lists specific events that trigger the clause.

In most cases, force majeure events are contemplated to cover acts of God, extreme weather events, riot, war or invasion, government or regulatory action including strikes, terrorism, or the imposition of an embargo. It is less common to see force majeure clauses that expressly contemplate a global health emergency, pandemic, or epidemic as a force majeure event.

In addition to the force majeure event, many courts also require that the party shows an attempt to perform the contract regardless of the triggering event (here the epidemic), perhaps by finding an alternative source of supply.[1]

A. Practical Considerations

Contracting parties must be cautious in declaring a force majeure event on the basis of the recent coronavirus outbreak and ceasing performance of their obligations. Incorrectly declaring a force majeure event may result in a contracting party repudiating the contract; it may also provide the other party with a right to damages.

The China Council for the Promotion of International Trade has apparently already issued over 3,000 force majeure certificates. However, these certificates are not dispositive. Instead companies, and ultimately arbitrators and courts, will have to examine each contract and the specific circumstances to determine if a force majeure clause applies and performance under the contract is excused.

Some states in the U.S. have specific rules regarding notice of force majeure claims, including when notice must be given. Companies should check with counsel about the proper timing and format of the notice, based on the jurisdiction, choice of law provisions in the contract, and specific notice language in the contract.

Finally, companies asserting these defenses, suffering damages from breach, or generally impacted by COVID-19, should keep good records regarding the factual circumstances and damages incurred because these documents will be central to any later legal proceedings. Counsel should also consider whether litigation is “reasonably foreseeable” such that it triggers an obligation to implement a litigation hold.

V. InsuranceCoverage Issues

A. Business Interruption Insurance

Business interruption insurance can be purchased as part of a commercial property insurance policy or as a stand-alone policy or provided through a captive insurer. General business interruption insurance is intended to protect a business against profits that are lost as a result of unintended interruptions to the business or its supply chain. Typically, business interruption policies are triggered when the company suffers some sort of direct physical damage, and that physical damage leads to the interruption of its business operations.

If your policy contains a requirement of physical damage, as most do, a determination will have to be made regarding whether the COVID-19 virus is deemed to be physical damage. However, some policies do not have a requirement of physical damage if the loss arises from certain diseases. A determination will have to be made whether the virus rendered a facility totally or partially unusable or required additional costs such as testing or cleaning. COVID-19 is not a disease that has ever been mentioned in any policies.

Other policies contain contingent business interruption coverage. Rather than requiring the policyholder to suffer a direct physical loss, contingent business interruption coverage responds to some losses that impact a company’s supply chain. To the extent that a supply chain is impacted by slow-downs or stoppages in the United States, China, Europe, or within the NAFTA free trade area, a company may see more benefit from contingent business interruption coverage than from traditional business interruption coverage. However, this coverage ordinarily requires physical damages to a supplier or customer’s property by a peril covered under the company’s policy.

Another type of business interruption insurance which may have broader applicability is civil authority coverage. The coverage applies when you are unable to operate your business due to the order of local, state, or federal authorities. Several months ago, some insurers began writing limited and optional coverage for COVID-19, particularly for “civil authority” orders, where governments or health officials issue orders restricting the use of businesses or properties. If you purchased this coverage, it is likely to have certain sub-limits (which may be relatively low), but it will need to be closely reviewed. This supplemental coverage may also apply without the physical presence of COVID-19 on your premises.

B. Commercial General Liability/Professional Liability

A company’s commercial general liability (“CGL”) insurance is typically the first thought when people ask general questions about insurance. CGL coverage responds to claims that the policyholder acted in a way that caused personal injury or bodily harm to a claimant. The typical example is a slip and fall of a patron in a public building, a products liability claim, or other physical injury caused by the policyholder that resulted in injury to another.

If businesses are sued by customers or patrons for causing, spreading, or failing to take adequate steps to prevent COVID-19 transmission, the CGL policy will be the first line of defense. However, many CGL policies contain exclusions for viral and bacterial-related bodily injury. On the other hand, CGL policies for certain industries that are more susceptible to contagious disease outbreaks (including restaurants, event centers, and hotels) are more likely to be sold with optional coverage that may include bacterial and viral infection, as these industries have historically demanded optional coverage for contagious disease.

C. Workers’ Compensation

Workers’ compensation insurance is required of most employers; either explicitly by statute or implicitly by business contracts. Workers’ compensation insurance generally covers jobsite injuries, as well as occupational diseases that are peculiar to a trade, occupation, or employment. For example, the hallmark occupational diseases include asbestosis and mesothelioma for those who worked with asbestos and black lung disease for underground coal miners.

Individual state law will control whether an “ordinary disease”—i.e., one which the general public is exposed to outside of employment—will be covered by workers’ compensation. Typically, an employee who contracts an “ordinary disease” will not be covered under worker’s compensation insurance. Some states apply the “peculiar risk” approach to determine whether the risk was increased because it was related to the employment. To the extent that your employees are hospital workers, nursing home workers, or other front-line healthcare workers who may be exposed to COVID-19 on a heightened basis, your business workers’ compensation insurance may cover those employees. Law enforcement, firefighters, and other emergency responders may also have similar claims. Employees of grocery stores, or those providing childcare to medical professionals would potentially be covered, but they would be a step further down the chain. The farther your particular employees are from the “peculiar risk” of being exposed to COVID-19 in the workplace, the less likely it would fall within your workers’ compensation insurance. Employees bringing workers compensation claims for COVID-19 will also have to prove that they were exposed at the workplace, rather than as members of the general public, which could be difficult in areas where community spread is apparent.

D. Directors & Officers Liability Insurance

Directors & Officers (“D&O”) liability insurance almost always contains exclusions for bodily injury. However, as the COVID-19 pandemic begins to negatively impact financial markets, credit markets, and share prices, shareholders may bring claims that a company’s executive leadership grossly mismanaged the company. Against the background of the turmoil currently roiling the financial markets, these claims may be specious at best, but the D&O policy may respond to such claims that are based on the drop of a public company’s stock prices.

Regardless of what you see, hear, or read about insurance coverage for COVID-19, you still need to have your policy read by an attorney experienced in the area of insurance coverage. And if you believe you have a claim, you need to notify all of your insurance companies as soon as possible.

VI. CONCLUSION

Due to the broad impact, companies need to evaluate whether their contractual performance, or that of their suppliers, has been impacted by COVID-19 and the governmental response to the pandemic. If the parties cannot negotiate a mutually acceptable “pause button” postponing performance, then companies should evaluate whether there are defenses to performance which will reduce or eliminate liability for breach.

[1] See, e.g. Gulf Oil Corp. v. F.E.R.C., 706 F.2d 444, 452 (3d Cir. 1983)

This question—how COVID-19, the novel coronavirus, will impact Chapter 11 cases going forward—is still to be determined, but this author believes it may turn the Chapter 11 process into what it was originally intended to be: a reorganization.

Today, and for more than the past decade, most Chapter 11 cases (other than prepackaged plan cases) have resulted in Section 363 sales of all the assets of the debtor to the highest bidder (the term Section 363 sale means a sale pursuant to Section 363 of the Bankruptcy Code), and sometimes that 363 sale comes within months of the filing of the case. Chapter 11 sales of all assets bring more value to the creditors than foreclosure sales, and, of course, “more value to the creditors” almost always means more value for the first priority secured lender of the debtor. After the 363 sale, the Chapter 11 case is typically over for all practical purposes. What happens next is one of two things: Either (a) the Chapter 11 case is converted to a Chapter 7 case, which is a liquidation of any remaining assets by a trustee who is appointed by the U.S. Trustee; or (b) a plan is confirmed in the Chapter 11 case pursuant to which all remaining assets are transferred to a Liquidating Trust and its Liquidating Trustee who then proceeds to liquidate all of the remaining assets. Same difference almost, albeit with some technical differences and advantages to each. In either situation, the “remaining assets” are typically lawsuits which the trustee is empowered to pursue, including, for example, claims for preferential transfers to creditors, claims for fraudulent conveyances against others, claims for breach of fiduciary duty against officers and directors, and anything else, including antitrust or securities fraud claims. It usually takes years of litigation before the unsecured creditors receive anything from the process, which is typically just pennies on the dollar. It is rare that any meaningful distribution is made to the unsecured creditors.

The Chapter 11 process, described above in very general terms, has been condoned by most bankruptcy judges and attorneys involved in the process, because it is the best thing for our economy in that it preserves operating companies intact, which benefits its employees who need the jobs (and buyers typically want to continue to operate the business) and its customers who rely on its product or services. Additionally, it brings the most value to the creditors, including a continuing market for the trade creditors who supply goods or services to the debtor (and who may lose some amounts due to them by the debtor but who preserve their past and future profits). It is difficult to argue against this rationale. Of course, the attorneys who represent each of the different constituencies (the debtor, the lender, the creditors committee, and the creditors) all get paid for their time and effort too, as well they should.

This author believes COVID-19 may change the process going forward, as it may disrupt domestic economies. How will judges, secured lenders, unsecured creditors, and others evaluate a situation if the major disruption of everything becomes the new normal? Who will consider buying a bankrupt company through a Chapter 11 363 sale amid so much uncertainty? Would the value of the bankrupt entity, assuming it has some, be preserved in a “fire sale” price to a third party? Would the secured lender and the debtor even be interested in trying to find out for themselves? It may be that there is a better alternative in Chapter 11 for both a debtor and its secured and unsecured creditors, and for the judges who must face this potential new normal caused by COVID-19.

The better alternative may well be a true corporate reorganization through the more traditional Chapter 11 plan process—that is, instead of selling the debtor’s assets pursuant to a 363 sale as has been the norm for more than a decade, the debtor may want to file and seek to confirm a true Chapter 11 plan which reorganizes the debtor for the mutual benefit of all the constituencies.

The secured lender (or lenders) are usually the most controlling constituency in this process (let’s start calling the different constituencies “players”). For the secured lender, it may make more business sense for it to do two things—reduce the interest rate being charged to the debtor, and convert some portion of its debt to equity (an ownership interest) in the debtor—rather than trying to cash out its unpaid loan through a 363 sale. The rationale for the sale and “cash out” of its loan has been that it can quickly make a new loan with that cash and at least earn interest on it. That rationale may not be readily attainable in a new normal. It may make more business sense for the lender to stick with its current debtor by reducing its interest charges and even by converting some of its debt to equity under the expectation that equity will have value in the future. These are the difficult business decisions that secured lenders may face if this new state of affairs persists for months or years.

The unsecured creditors will also have to face the new normal reality and take a reduction of the amounts owed to them for past due product or services. In Chapter 11 cases, persuading unsecured creditors or forcing them to take less is much easier than it is to force the secured lender to take less. Basically, a vote of a majority in number of unsecured creditors and of two-thirds of the amounts owed to them is enough to force them to take less (or a “haircut” as it is often called). Usually that vote is not difficult to obtain, especially if an official Creditors Committee has been formed and has negotiated the deal with the debtor and recommends it to the unsecured creditors. Typically, if the secured lender has agreed to take its own haircut in some form, then it will insist that the unsecured creditors do the same for two reasons—namely, it is the fair thing overall, and a reduction of the unsecured debt increases the value of the equity interests being obtained by the secured lender. Indeed, as part of any deal with the unsecured creditors, they may be given some amount of the existing equity ownership of the debtor as a group.

Lastly, the existing equity ownership of the debtor will also have to make major concessions. First, as the last to be paid anything in terms of priority of rights, it is the fair thing to do if the secured lender and unsecured creditors will be taking haircuts of their own. Secondly, the existing equity interests may have no real value without the reorganization of the debtor, and the argument is why should the existing equity retain anything. The answer has a practical side to it of course: If management owns equity and if they continue to operate the debtor, they probably deserve some equity, however small. They may also be asked to take reductions in their compensation.

In short, all of the different players in the process will be required to take haircuts of some sort in order to save the debtor from destruction for the mutual benefit of the group. While the American way may be to look out for number 1 almost exclusively, this dire situation (if it occurs) will necessitate a balance between the different players which is mutually beneficial overall. The players will each have their own attorneys representing them, and bankruptcy attorneys will likely be familiar with the necessities of the situation. The Bankruptcy Code itself also has mechanisms built into the system to allow for each player to exert pressure on the other players to cooperate, and the bankruptcy judge sometimes is called on to intervene to help the players or their attorneys to be more reasonable in their positions. For example, the debtor can threaten a cramdown plan of reorganization on the secured lender (that is, a plan without its consent); the secured lender can threaten the unsecured creditors with a 363 sale or a liquidation whereby the unsecured creditors and the equity interests will recoup nothing at all; or the existing equity can tell them all to “go fly a kite” or worse—say here are the keys (and good luck) or threaten them with endless litigation. Everyone knows how the game can be played as required and also knows that trying to reach a consensual deal is preferable.

We live in interesting times indeed, if not somewhat scary ones even for we Americans. We all hope for the best of course, but for those of us who experienced the worst of Hurricane Katrina we have learned to try to be prepared to the extent possible.

Law firms and in-house legal departments have moved past mere recognition of the importance of diversity and inclusion (D&I) to implementing widespread programs aimed at curbing biases that can stand in the way of diversity goals.[1] Formal training programs can only go so far, however. Law firms and legal departments also need employee buy-in on the necessity of giving and receiving real-time prompts aimed at thwarting biased behavior before it takes effect.

Many organizations require their employees to participate in diversity training. Most training starts with the concept of “implicit bias”[2] and seeks to educate employees about its existence and prevalence in the workplace.

The goal of the training is to empower employees to reconsider in real time how they respond to and judge others, thereby “interrupting” their potential biased behavior from taking effect. Training sessions often demonstrate scenarios of clearly biased behavior as examples of what not to do. Sometimes participants engage in role playing to work out better responses, but formal training tends to be infrequent, in group settings, and fairly passive. When mandatory,[3] the audience may not be sufficiently attentive and invested in the desired outcome. It is imperative that law firms and in-house departments educate employees and evaluate organizational procedures for reducing bias; however, without setting the stage for fundamental change in “hallway behavior” by enlisting and educating allies in all ranks of the organization, no formal program is going to move the needle on D&I.

Identify Bias

It will take a lot of work to ensure that sufficient numbers of lawyer and nonlawyer staff internalize the necessity of a truly diverse workforce, which is the first step toward ultimate success. First, they must understand that bias exists, everyone has it, and it has an effect.[4] Next, lawyers and staff must believe that the organization cares about diversity, that a diverse workforce is fundamental to the success of the firm or department, and that their personal success depends on their participation in achieving diversity goals. We know how to teach all of this: lots of evidence-based research on effective training is widely available.[5] Firms and law departments can, with sufficient analysis and thought, hardwire systems to de-bias hiring, evaluation, and promotion to make better decisions and to provide incentives for employees to promote diversity.[6]

In 2018, the American Bar Association (ABA) and Minority Corporate Counsel Association (MCCA) published a report outlining four types of gender and racial bias in the legal profession: (1) “prove-it-again” bias, (2) “tightrope” bias, (3) “maternal wall” bias, and (4) “tug-of-war” bias.[7] The report also provides a comprehensive picture of how implicit gender and racial bias affect the legal workplace and workplace processes. In part, the study revealed that bias is pervasive in the legal workforce but, significantly, it can be interrupted.

Interrupt Bias

Assume there is employee buy-in and a recognition of bias. Joan Williams, a leading researcher in work bias, notes that although “bias trainings remain important to educate others about bias . . . the key is to arm bystanders to interrupt bias, so that the people experiencing bias don’t have to carry that burden alone.”[8] This is where allies come in.

We observe that potential allies are everywhere.[9] Many men[10] are intellectually committed to gender equity but are under-educated about their own bias and don’t know how to take action to make a difference. What is needed is a grassroots, “hallway” effort in which individual employees are trained to identify and interrupt their own personal biases and taught how to address observed bias in others in a work environment in which all employees have “given permission” to engage in bias interruption. This will set the stage for the success of revamped organizational processes aimed at hiring, retention, and promotion for a more diverse workforce.

Firms that want to use allies will be more successful if they get explicit “permission” from employees to accept guidance on their behavior. If each employee affirmatively agrees that D&I efforts are important and that it is acceptable for other employees to point out when one may be acting out of bias, resistance to corrective action is reduced. The prompt becomes the content of the discussion, and not whether one person has the right to hold another accountable.

Central to these efforts is ally training. Learning how to be an ally takes time,[11] but a commitment to shorter but frequent sessions can be an effective approach. Organizations must identify potential allies and arm them with both the “antennae” to detect possible bias and the language to draw out discussion with colleagues. This could mean intervening and taking a moment to discuss a situation.[12] An example of an intervention would be having a colleague say, “Jane did a terrible job on that assignment.” If the listener simply says, “That’s too bad,” both the speaker and the listener leave with the view that Jane is not good at her job. If, however, the listener asks, “What did she do?” and follows up with, “What did you do? Did you speak with her about it?” then the listener may find there is more to the story. Perhaps what really happened is that Jane did not meet some unspoken expectation but did in fact complete the actual assignment timely and well. Allies can learn effective ways to assess the situation and help redirect that assignment interaction and interrupt future bias.

Organizations need not rely only on D&I professionals and formal, intermittent training to change behavior; they can instead enlist an army of allies to effect quotidian change. Without allies, efforts to de-bias systems and processes have little hope of success. With them, we will have engaged the exponential power of small actions to have significant, long-term effects.

[1] Ellen McGinnis is a partner in the law firm of Haynes and Boone, LLP, the co-chair of the Fund Finance Practice Group, and serves in multiple management positions, including on the firm’s board of directors and as the chair of the Admission to Partnership Committee. Jennifer Reddien is the director of diversity and inclusion at Haynes and Boone, and frequently speaks and writes about diversity and inclusion in the legal profession.

[2] Implicit bias refers to the attitudes and stereotypes that affect our understanding, actions, and decisions in an unconscious manner. Kirwan Institute for the Study of Race and Ethnicity, The Ohio State University, State of the Science: Implicit Bias Review 2015. The terms “implicit bias” and “unconscious bias” are often used interchangeably. Although some researchers note differences between the two terms, the legal field tends to use the term “implicit bias” rather than “unconscious bias.”

[3] We endorse mandatory training but recognize that without strong efforts to persuade lawyers that it is essential to their success, they are unlikely to become advocates for taking action.

[6] Iris Bohnet, What Works: Gender Equality by Design (Harvard University Press, 2016).

[7] “Prove-it-again” bias refers to the need for women and people of color to work harder than the majority to prove themselves; they may feel that their work product must be better than the majority’s work product to receive the same recognition. “Tightrope” bias describes the narrow range of behavior expected of and deemed appropriate for women and people of color. Women often report that they feel pressure to behave in feminine ways and that they are assigned more administrative tasks than men. “Maternal wall” refers to the bias against mothers. Many women report being treated “worse” when they return to work after having children. They find they are passed over for promotions and receive low-quality work assignments. “Tug-of-war” refers to the conflict between disadvantaged groups that may result in bias from the environment. For example, in male-dominated fields, many women note feeling like they are in conflict with other women.

[12]See, e.g., Kerry Patterson, Joseph Grenny, Ron McMillan & Al Switzler, Crucial Conversations: Tools for Talking When Stakes Are High (McGraw Hill, 2002) (among other things, a “how to” on holding effective conversations about crucial issues).

I’ve spent the last 20 years as a communications consultant working with lawyers, law firms, bar associations, and law schools. It’s been a fascinating and rewarding career. Here are five things I’ve learned:

1. Identify and Understand Your Audience.

Lawyers communicate as if we are always talking with other lawyers. In law school, we train to do it, yet a big part of the job is communicating with lay people. Therein lies a fundamental mistake. The meaning of all communication—written or oral—is in the mind of the audience, not the speaker. You understand the meaning of your words, but the message may be garbled in the mind of the recipient.

Even professionals who are familiar with legalese may have different expectations and understanding than legal professionals. Understand who is receiving this communication, then go one step further: Tell your audience what it needs to know, rather than what you wish to say. This requires a bit of effort. Don’t make assumptions about what your audience knows. Identify what you know they know. Learn the vocabulary of their industry if you can, then craft your communications so your words (and you) meet the needs of your actual nonlawyer audience. You may discover that little needs to change, but those changes are the key to effective and efficient communication.

One place where lawyers forget this rule is in our bios. We tend to focus on what other lawyers want to know about us (I went to Blah Blah Law School), and forget to tell our clients what they want to know (I have 20 years of experience with your field.) Strike a balance.

2. Omit Needless Words

Strunk and White were right. Lincoln was right. Writing is easy. Editing is hard. (When I first wrote that sentence, it read, “It’s editing that is hard.”) Paring down your language almost always improves it and avoids burying your core message.

I’d never suggest that you write with no color or flair. Don’t dumb it down, but favor clarity and oppose verbosity and repetition. Watch the number of times you say “I” and “we.” Make your point with the maximum impact per word. Polish your communications until they shine.

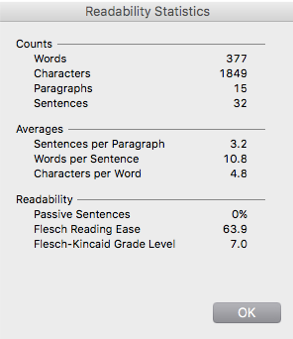

One tool that may help you is the Flesch Test. This is an application that tells you the reading level of your writing. It’s built into Word (under Tools) and there are more sophisticated versions online.

A good Flesch score is 65, and a reading level of 7th to 10th grade is perfect.

The New York Times generally has a 10th-grade Flesch level. This article has a 7th-grade reading level.

3. Start at the Beginning and End at the End

This is the organizational counterpart to brevity, but it also embodies Rule #1.

When considering your audience, a focus on organization means that you might start with a brief explanation, a bit of background, or a recap. Make it easy for your audience to jump in and understand your message, follow your explanation or argument, and arrive at the proper conclusion with you. Don’t send them scrambling for another document or googling a legal theory.

An outline may help, or outline what you’ve already written to confirm an orderly flow of ideas. Cut-and-paste commands are the best tools ever devised for writing organization—I started writing in the days of literal cutting and pasting, and my writing is better now than it was then.

Do you need to take a side trip? Consider a footnote, a literal sidebar, or an aside in a speech. There are lots of ways to give an audience a bit of extra information. Just don’t wander off and forget where you were headed.

4. Identify and Stick to a Style

When I began as a legal writer, I adopted a formal and stilted style. I was young and wanted to appear experienced and professional. There are still times when that style is appropriate, as when writing demand letters. Over time, however, I discovered that my writing had more impact when it was more conversational. I’m often introducing an audience to new ideas and want it to seem more like a discussion than a lecture. E-mail has also had a dramatic impact on legal writing, so highly structured, formal language may alienate a lay audience.

Once you identify your style for a particular communication, stick to it. Don’t wander off midway.

5. Update Your Communications Regularly

Lawyers are great at forms. One of the most common mistakes lawyers make is to create documents, bios, ads, or website text and then leave it for years without updating. I got an e-mail the other day from a lawyer with some bottom boilerplate that wasn’t consistent with current law. Does that give me confidence in that lawyer? Probably not. Refreshing your communications not only makes them more timely and accurate, it also blows the linguistic dust off. Create a schedule and regularly update your website, e-mail template, and biography. It’s like a little facelift.

All five rules boil down to one: Have empathy for your audience, and your communications will hit their mark.

In a ground-breaking decision, the Ontario Securities Commission (OSC) overturned the decision of the acting director of the Investment Funds and Structured Products Branch of the OSC (IFSP) to refuse to issue a receipt for the establishment of the Bitcoin Fund (the Fund), which is a proposed investment fund based on the cryptocurrency bitcoin.

3iQ Corp. is the investment fund manager and had been working on the Fund for three years with the goal of allowing retail investors the benefits of investing in bitcoin through a regulated, listed fund. Following multiple discussions with the IFSP, the acting director of the IFSP refused to issue a receipt for the Fund’s prospectus. In declining to issue a receipt, the director questioned the suitability of cryptocurrency as an investment, citing the lack of regulation for cryptocurrencies and the various associated risks.

Original Refusal

By way of background, the proposed Fund is a nonredeemable investment fund (NRIF) established as a trust. The objectives of the Fund are to provide investors with exposure to bitcoin and the opportunity for long-term capital appreciation.

On February 15, 2019, the acting director for the IFSP refused to issue a receipt for the Fund’s prospectus because it was not in the public interest to do so (see Securities Act, RSO 1990, ch. S.5, § 61(1)) and the Fund’s prospectus did not comply in a substantial respect with a requirement of the Securities Act (see § 61(2)(a)(i)).

In arriving at this decision, the acting director put forward the Fund’s shortfalls:

The lack of the Fund’s ability to accurately value its assets due to the “fragmented and unregulated environment in which bitcoin generally trades”;

The risk associated with safeguarding the Fund’s assets and the ability of the subcustodian to provide Customary SOC Reports;

The risk of the Fund not being able to file audited annual financial statements in accordance with National Instrument (NI) 81-106;

The operational risks associated with the lack of established regulation in the bitcoin market; and

Bitcoin being an illiquid asset, and the Fund not complying in a substantial respect with the restriction NI 81-102 against the holding of illiquid assets.

OSC Panel Decision

In establishing and structuring the Fund, 3iQ engaged industry participants and the regulators. 3iQ requested to be heard before a panel of the OSC in which it submitted that a regulated Fund is a necessity given the recent collapses of various other platforms globally whereby individuals invest in crypto-assets without regulatory oversight.

Upon review, the OSC panel found that the Fund was structurally different in nature than certain Exchange Traded Funds (ETFs) related to cryptocurrencies that have been rejected by the U.S. Securities and Exchange Commission. This was due to the Fund placing restrictions by monthly reporting and only allowing redemptions annually by using the NRIF structure, which would significantly reduce the impact of market manipulation by daily trading. The Fund would also be using MVIBTC (as defined below) as the index and would only be purchasing bitcoin from dealers that hold a license or are otherwise regulated. All of these considerations distinguished the Fund from an ETF, which requires constant trading and is more vulnerable to market manipulation.

In arriving at its decision, the OSC panel also looked at the reasoning of the acting director as well as arguments put forth by staff:

Illiquidity. Staff argued that bitcoin is illiquid because it is not currently traded on market facilities comparable to the Toronto Stock Exchange, and there is no central source for trading data concerning bitcoin. The OSC panel found that there is sufficient evidence of real volume and real trading in bitcoin on registered exchanges in large dollar size. Furthermore, the regulation does not define the term “market facility” that is found in the definition of “illiquid asset,” and the term should not be narrowly construed to imply some form of established and mature trading facility or network.

Valuation and Market Manipulation. The OSC panel stated that under NI 81-106, the Fund would be required to calculate its net asset value using the fair value of its assets and liabilities. 3iQ proposed to value the Fund’s bitcoin by reference to an index called the MVIS CryptoCompare Institutional Bitcoin Index (MVIBTC), which is regulated by the German Federal Financial Supervisory Authority. MVIBTC uses transaction data from 22 trading platforms to calculate the value of bitcoin and complies with the European Union benchmark regulations and the International Organization of Securities Commissions regulations. As such, the OSC panel was not satisfied by the staff’s argument that valuation would not be possible. The OSC panel further noted that the issue with market manipulation having an impact would also be minimal because the fund (i) will only invest in bitcoin; (ii) would pursue a buy and hold strategy; and (iii) only buy and sell bitcoin on regulated exchanges.

Safeguarding of the Fund’s Assets. The Fund would use Cidel Trust Company, which is regulated by the federal Office of the Superintendent of Financial Institutions, as a custodian and use Gemini Trust Company, LLC as a subcustodian, which is regulated by New York State, as a qualified custodian under NI 81-102. Staff made two arguments: (1) risk of loss; and (2) lack of insurance. The OSC panel commented that bitcoin can be lost or stolen like any valuable commodity, but staff did not provide sufficient evidence that Gemini, a regulated crypto-asset custodian, has suffered losses of customer assets.

Auditability of the Fund’s Financial Statements. Staff submitted that it would be against the public interest to issue a receipt due to concerns over the Fund’s ability to file audited annual financial statements. In making this argument, staff pointed to the lack of Gemini’s SOC 2 type 2 report and the fact that Gemini may deny the auditor for the Fund access to test the operating effectiveness of Gemini’s controls. However, the OSC panel relied on the Fund’s submission that a qualified auditor can conduct the audit even without the report and still comply with generally accepted auditing standards.

In reaching its decision, the OSC panel commented that denying the Fund a receipt would not promote fair and efficient capital markets and confidence because it would leave investors with no choice but to invest without the protections of a public fund. The OSC panel also found that there was no issue of unfair, improper, or fraudulent practices as far as the structure of the Fund was concerned or the operation of it.

In the end, the OSC panel decided that staff had not demonstrated that bitcoin is an illiquid asset and that the Fund will not be compliant with NI 81-102, or that it was not in the public interest to issue a receipt for the Fund’s prospectus. Accordingly, the panel ordered that the acting director’s decision be set aside, and directed the acting director to issue a receipt for the Fund’s prospectus.

Conclusion

Although the OSC’s findings in this decision are not an endorsement of investment funds based on a cryptocurrency model, they do provide guidelines for the regulation of these funds in Canada. This is an important step in that it will support innovative investment opportunities while also protect investors who will be able to invest in funds with regulatory oversight.

Highly regulated industries like the financial services industry have faced ever increasing regulatory compliance obligations. Technology, such as artificial intelligence (AI), that can be utilized to innovate the manner in which these organizations operate can lead to additional challenges for regulatory compliance, and the regulatory environment can drastically impact innovation in these sectors.

Regulatory compliance is a critical consideration for both start-ups and established organizations seeking to drive innovation in the financial services industry. Developing solutions and business strategies with compliance in mind will reduce the risk of potential fines and penalties and allow for the development of a viable solution.

To assist organizations in meeting these ever-growing compliance obligations, RegTech solutions are being developed that can be utilized to provide transparent, faster, and more efficient methods of reporting and ensuring compliance. This article will focus on the potential benefits of RegTech solutions for highly regulated industries, particularly the financial services industry.

What Is RegTech?

RegTech is a general term for new and innovative technologies designed to enable businesses to more easily meet their regulatory compliance obligations. Some of the benefits of the application of RegTech include: (1) the ability to efficiently navigate complex regulatory burdens and process enormous amounts of dense data, and (2) the reduction of risk flowing from human errors that could result in severe administrative fines.

RegTech has flourished due to a developing body of complex national and international regulations that often require the monitoring, evaluating, and reporting of vast amounts of information.

The Legal Landscape

Industries such as insurance, food and drug, oil and gas, mining, securities, telecommunications, energy, fisheries and forestry, and financial services (among many others) operate within a highly regulated environment that can be complex to navigate. Governments establish regulations with the intention of protecting the public from potential risk. This is particularly evident in the financial services industry where we have seen an increase in regulations impacting this industry in reaction to the 2008 financial crisis. However, overregulation can stifle innovation and create barriers to entry for emerging companies, such as FinTech organizations, due to the crippling expense required to comply with these regulations.

The adoption of disruptive technologies like AI in the financial services industry has led to the need for governments to develop new regulations to address the impact of these technologies.

Jurisdictions have diverged on how to address changes in the industry, including those driven by technology. This divergence creates significant obstacles for cross-border products and services or organizations that look to enter new markets. For example, organizations have differing compliance obligations with respect to data protection laws in Canada versus the European Union. Therefore, organizations must ensure that their compliance programs meet the relevant requirements of each jurisdiction in which they operate. RegTech solutions can be utilized to assist in the development of jurisdictional compliance frameworks.

Although some financial services companies have pre-emptively invested in technology to help keep up with the bourgeoning field of regulations, many don’t have the time or extra resources to focus on technology that would help them address the new regulatory burdens, so they have instead turned to using manual processes to address the frequency and volume of the new reporting requirements. This approach can be onerous and causes valuable human resources to be expended unnecessarily. Manual processing is also typically less accurate than RegTech processing.

RegTech Applications

Although there are numerous opportunities for RegTech to assist with compliance, five of the most promising applications of RegTech include the following:

Compliance. RegTech that can be used to review all relevant regulations and report on the potential impact of such regulations to the user, including jurisdictional data privacy laws.

Risk Management. RegTech solutions that conduct scenario analysis and risk monitoring on internal business operations through the use of big data analytics to identify and evaluate these risks.

Identity Management and Control. RegTech that has been developed in response to Anti-Money Laundering (AML) and the Know Your Customer (KYC) obligations regarding client identity authentication. The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) has also established various other obligations requiring regulated entities to conduct analysis and provide seamless reporting. RegTech can be used to efficiently conduct customer onboarding and monitoring activities and will allow for greater transparency.

Regulatory Reporting. RegTech that is utilized to assist in the generation and distribution of reports and information required by regulators. RegTech solutions can assist in data sharing between regulated entities and regulators and enable faster processing of vast amounts of data required to prepare these reports.

Transaction Monitoring. RegTech that monitors financial transactions for suspicious activity quickly and with a high degree of accuracy by leveraging the benefits of distributed ledger through blockchain technology and cryptocurrency. This type of RegTech also aids with much of the required FINTRAC compliance obligations.

The operational benefits gained from RegTech will depend on the specific solution. RegTech that creates reports through automation of the processes required to generate these reports (e.g., data collection, aggregation, and report generation) could lead to a significant reduction in expenses and time required to prepare these reports. In addition, if this information is available in real time, organizations can react to any issues sooner than if the reports were to be generated at a later stage.

Barriers to RegTech Adoption

Despite the promise, certain RegTech solutions are in their infancy; thus, issues related to its adoption still exist. One such issue is pricing. For certain applications, it is unclear what the true cost savings are or what value is generated by the RegTech solution. Therefore, developers may have difficulty in communicating the value of the solution or selecting the appropriate pricing model (e.g., a fee per record generated versus a monthly subscription fee). In addition, the cost of developing a tool to meet the ever-changing regulatory landscape may mean that developers will have difficulty in recouping the ongoing maintenance fees associated with building and maintaining the RegTech solution.

Another concern is the potential for large-scale errors caused by minor issues with RegTech solutions, especially a solution that is one-size-fits-all and used widely in the marketplace. For example, if a RegTech solution fails to address a change in reporting requirements, this could lead to its customers failing to meet their regulatory requirements. If this same problem is replicated multiple times in the same customer, or widespread across multiple customers, then the losses could be significant. RegTech providers and customers must consider these risks when negotiating the terms of the agreement and ensure that these risks are addressed through the apportionment of liability between the parties, indemnities, and requirements for insurance.

Due to the potential sensitivity of the data collected and processed, it is critical to ensure the adequate protection of the data. The potential risk of a data breach can be significant for both the customer and RegTech provider. Customers should therefore conduct the appropriate due diligence on both the solution and provider to ensure that this risk is mitigated. RegTech providers should also ensure that they have the appropriate cybersecurity policies and procedures in place to protect themselves from both financial and reputational risk.

Conclusion

RegTech offers many benefits to organizations operating in regulated industries. Although we have addressed some barriers to adoption, the opportunities offered by adoption of innovative technologies that can assist in meeting an organization’s regulatory requirements are significant.

The manner in which RegTech is supported and integrated into the current regulatory structure will play an important role in navigating both the developmental and implementation stages.

Developers of RegTech solutions should look to engage regulators directly and take advantage of regulatory sandboxes to assist in ensuring compliance. With cautious and thoughtful integration into the current regulatory environment, RegTech shows major promise in reshaping the way that companies interact with the growing body of regulatory oversight.

Lawyers have different professional development obligations at each stage of their career.[1] Despite that evolutionary arc, there is one constant: the best lawyers are engaged in life-long learning. Many firms have formalized the elements of the traditional training that young lawyers historically, and often organically, received from partners and other more senior lawyers within the firm. Whether by such internal training methods or going outside the firm to hear from special consultants such as law professors or industry experts, or to participate in bar and trade associations, firms develop their lawyers in a variety of ways. In addition, seasoned lawyers equally benefit from helping to train other lawyers, whether inside or outside their firm.

One of the more prevalent law firm initiatives related to professional development for younger lawyers has been assigning mentors and encouraging participation in organizations like the American Bar Association to seek outside mentoring within its ranks. Research from the Center for Talent Innovation (CTI), a well-known think tank with a research focus in this area, shows that the vast majority of women (85 percent) and multicultural professionals (81 percent) need “navigational help” inside organizations.[2] Most law firms have some sort of internal mentoring program, and many local and state bar associations also have long-standing programs, several of which are at least in part able to trace their origins to an attempt to develop or retain women and lawyers of color.[3] Despite the availability and proliferation of mentorship programs, mentorship alone has been ineffective in helping to maximize the talent hired by law firms, and the investment in young lawyers, especially women and lawyers of color, continues to dissipate.[4]

Mentorship

The big push for mentorship programs is not only among law firms, but also within trade and professional associations, including bar and affinity associations, and in programs that have been created to assist in creating pipelines for potential law students. Mentorship can be defined as either one-on-one relationships between an experienced lawyer and another lawyer, law student, or potential law student, or it can be executed in a group setting. Individuals meet in person, via emails, or on calls, and the meetings can be on a regular schedule or on an ad hoc basis. Group mentorship programs can be especially helpful and can take the form of skills training in networking, relationship development, interviewing, professionalism, evaluations, and how to take advantage of opportunities to develop an industry or practice expertise.

Mentorship programs, especially in trade organizations, bar associations, and with young students, have been especially effective. Especially in communities of color and of women, a lawyer taking the time to visit or work with potential future lawyers is extremely impactful. When one of those lawyers or even a group of lawyers are lawyers of color or are women, it is especially important because their mere presence demonstrates to female students or students of color that they themselves can be a lawyer or a judge. These anecdotal remarks are backed up by teachers and students who confirm the effect on them and their classmates of these mentoring programs.[5] Similar success can be seen in the efforts by bar associations and trade groups to mentor young professionals. Both of these types of success stories have one thing in common: external mentoring programs. By comparison, internal programs have had poor to mixed results.

Shortcomings in Mentoring Programs

Despite the success of mentorship for students of all ages, the problem with mentorship programs within law firms has often been the execution of the mentor’s duties. Oftentimes the mentor will report on progress to firm administration, and mentors are not always advocating for their mentees. Indeed, some mentorship programs are seen with suspicion by associates, either as part of the firm’s apathetic bureaucracy, or part of the firm’s self-interested management.[6] A new concept has developed out of this discord and mistrust in the value of a sponsor, as opposed to a mentor, in the context of advancement within an organization and the role mentorship can play in that context.[7][8] On the contrary, mentors play a continuing and important role in professional development and, for example, help map out the unwritten rules and practices in an organization and pave the way for a sponsor.[9]

Sponsorship as the Cure to Failed or Faltering Mentorship Programs

Sponsorship has become especially popular in law firms. Many law firms have been criticized for not retaining lawyers of color and women. In the post-mortem analysis of “why,” it was found that key advantages related to professional development have not historically been provided to lawyers of color or women. For example, partners have provided the best assignments and, thus, one of the best professional development opportunities, to those they have chosen to informally mentor, which oftentimes were lawyers of the same peer groups, race, or gender as the partner. Institutionalized mentorship programs that work in tandem with a dedicated commitment to sponsorship by firm management could be the cure to the fatigue that many firm mentorship programs are currently experiencing.

Maryann Baumgarten, the head of Tech Diversity Business Partners at Facebook, has written a wonderful comparison of the key elements of being a mentor as opposed to a sponsor that illustrates where sponsorship can both add to the efficacy of existing mentorship programs, as well as become the next step in the evolution of such programs.[10] A mentor is anyone with experience who can support a mentee on how to build skills, professional demeanor, and self confidence in the workplace, whereas a sponsor is a senior member of management invested in the protégé’s success. Mentoring tends to be more general, whereas sponsorship is tailored to the protégé and involves using the influence and the networks of the sponsor to provide access to key assignments, people, and responsibility. Mentors help a mentee develop a career vision; sponsors drive that vision. Mentors will give suggestions on how to create a network; sponsors will open up their network to the protégé. Mentors will provide advice on visibility by encouraging the mentee to seek out key projects and people; sponsors will use their own platforms and mediums to provide direct exposure to the protégé.

Sponsorship Is the Gift That Keeps on Giving

Many firms will ask, “What is in it for me?” Sponsorship is an active and engaged relationship; the protégé has just as many responsibilities and commitments to the relationship as the sponsor. The protégé must perform well, demonstrate loyalty to the firm and sponsor, and actively look to enhance the team brand.[11] CTI has researched the issue of job satisfaction for sponsors and finds that a sponsor with protégés has far greater job satisfaction (11 percent) than those who have not worked to develop new talent.[12] In terms of retention objectives, sponsors of color have reported 30 percent more job and career satisfaction than those who do not have the same following of protégés.[13] In many ways, you can see this in the legal profession directly and poignantly in the legions of law clerks that have worked with our judiciary. It is a well-known and chronicled aspect of clerking that there is a bond between the judges and their clerks that survives deep into their respective careers.[14] Even closer to the bottom line, an important update to CTI’s research published in 2019 reported that 66 percent of sponsors were confident with their ability to deliver on difficult projects with their teams, and only 53 percent of nonsponsors had the same confidence.[15]

“My crown is in my heart, not on my head; Not decked with diamonds and Indian stones, Nor to be seen. My crown is called content: A crown it is that seldom kings enjoy.”[16]

The weakness of a sponsorship program is that it requires leadership from the sponsor. The most important aspect of that leadership is to advocate for the promotion of the protégé. CTI’s latest research shows that of the one in four employees that identify themselves as sponsors, only 27 percent are advocating for their protégés, and to the point of this article, 71 percent of the sponsors have protégés who are the same race or gender as they are.[17] Probably just as applicable as the quote above from Henry VI could be the quote from Romeo and Juliet: “What’s in a name? That which we call a rose by any other name would smell as sweet.”[18] Leadership has often been defined as the art of motivating a group of people to act toward achieving a common goal. Kevin Kruse in a 2013 Forbes article dismisses the notion that leadership is defined by seniority or hierarchy, titles, extroverted charisma, or being part of management.[19] He takes a mild shot at Peter Drucker, who has been quoted as saying, “The only definition of a leader is someone who has followers,” dismissing it as “too simple.”[20] He then castigates and rejects the definitions of leadership put forth by no less than Warren Bennis (leadership is translating vision into reality), Bill Gates (leaders will be those who empower others), and John Maxwell (leadership is influence—nothing more, nothing less).[21] Instead, Kruse’s definition of leadership is “a process of social influence, which maximizes the efforts of others, towards the achievement of a goal.”[22] He emphasizes that leadership comes from social influence, not authority; requires others; does not rely on charisma or another personal trait (as leaders can come in all varieties); and focuses on a goal—and is not influence for the sake of influence—and does so by making the most of others’ talents.[23] Kruse’s definition punctuates and sums up one of the most effective executions of professional development programs: the marriage of mentoring and sponsorship, which managers in law and business should take to heart based on their collective experience in making the most of the talented professionals that they hire, train, and hope to retain.

[1] Director and practice chair, Elliott Greenleaf, P.C. Thank you to Courtney Snyder, business development director for Elliott Greenleaf, P.C.’s Delaware office, and Sarah Denis, Esq., for their assistance in the editing of this article.

[3] The National Legal Mentoring Consortium lists a wide range of programs, including law firm, law school, ethics-based, local bar, and state-based. National Legal Mentoring Consortium, Mentoring Programs – Law Firms (Feb. 20, 2020). Organizations like the American Bar Association have extensive mentorship programs among the wealth of available professional development opportunities, including the Business Law Section Fellows Program and Business Law Section Diversity Clerkship Program.

[4] Endemic issues with lack of retention of women and minorities are not exclusive to the legal profession and have been the subject of many studies and articles about management in this area. See Joan C. Williams & Marina Multhaup, For Women and Minorities to Get Ahead, Managers Must Assign Work Fairly, Harvard Bus. Rev. (last accessed Feb. 25, 2020). An excellent overview of why diversity is important to the bottom line of law firms is Sheryl L. Axelrod’s Banking on Diversity: Diversity and Inclusion as Profit Drivers—The Business Case for Diversity, americanbar.org (last accessed Feb. 25, 2020).

[5] The Leadership Council on Legal Diversity, which consists of more than 320 corporate chief legal officers and law firm managing partners, runs a leadership development program known as the LCLD Fellows, which debuted in 2011. The program works by identifying high-potential attorneys from diverse backgrounds with the objective of the Fellows becoming leadership within their organizations. The author was fortunate enough to serve on the fellows Alumni Council as the community outreach co-chair. He has first-hand knowledge of the profound impact of mentorship programs on communities of color and on women, especially in a group session with young students who are first-generation citizens, potential first-generation college students, and potential first-generation law students.

[7]See, e.g., Hewitt, S.A., Forget a Mentor, Find a Sponsor: The New Way to Fast-Track Your Career, Harvard Bus. Rev. Press, Sept. 2013.

[8] Sylvia Ann Hewitt, CEO of the Center for Talent and Innovation, a think tank based in New York, also chairs the Task Force for Talent Innovation, which is comprised of 75 global companies that focus on maximizing talent in corporations.

[14]See,e.g., Andrew Cohen, Real Mentorship: Do Judges and Law Clerks Still Do This (last accessed Feb. 25, 2020) (“Even lawyers and law students who have heard about Judge Hand probably don’t know that in addition to his stewardship of the 2nd Circuit for decades he also sort of invented the modern-day practice of federal judicial clerkships, which are nearly 100 years later still the gold standard in legal apprenticeship. . . . Most of [Judge] Hand’s clerks, fresh out of law school, were startled to find this experienced jurist; a near mythic figure, a household word to every law school graduate, the master judge of his generation, asking for help and insisting on candid criticism and continuous oral participation in the decision process. Was it really conceivable, they would wonder, that [Judge] Hand was seriously interested in their views when they were just months away from the classroom? . . . As the clerks got to know [Judge] Hand better, most realized that he was entirely serious about his constant prodding to elicit critical analysis, and that this unique way of working with his clerks was part and parcel of his distinctiveness as a judge.”); see also NALP, Clerkship Study Alumni Law Clerk Survey (last accessed Feb. 25, 2020) (“As expected, the relationships in their own judge’s chambers—their judge (87%), the other law clerks (71%) and the administrative staff (67%)—proved to be the most significantly enhanced. In addition, they developed relationships with other chambers, most reporting that their relationships with other judges, law clerks, and court personnel were also moderately or significantly enhanced.”); Chambers Associate, Clerkships, chambers-associate.com (last accessed Feb. 25, 2020) (“Clerks also build up a valuable network among members of the Bar, other clerks and judges. This comes in handy when practicing in the same state or district as the judge.”); Laura B. Bartell, A Splendid Relationship – Judge and Law Clerk, 52 La. L. Rev. 6 (July 1992) (last accessed Feb. 25, 2020) (“The partnership between a federal judge and the judge’s clerk can be a splendid and mutually rewarding relationship.”); Grace Renshaw, The Best Legal Job You’ll Ever Have, 40 Vanderbilt Law. 2 (last accessed Feb 25, 2020) (“She also gained two permanent advantages from her year as a clerk: a lifetime mentor and membership in a close-knit “family” of other former clerks. ‘Judge Collier is an amazing mentor to his law clerks,’ Johnson said. ‘He spent a lot of time talking with us and really seemed to enjoy the teaching aspect. He’s very patient and has a great understanding of the role that a clerkship plays in cultivating a young attorney’s career.’”).

[15] Center for Talent Innovation, Sponsor Dividend (last accessed Feb. 25, 2020). This survey was conducted by NORC at the University of Chicago under the auspices of the Center for Talent Innovation (CTI), a nonprofit research organization. NORC was responsible for the data collection, whereas the CTI conducted the analysis.

[16] William Shakespeare, Henry the VI, Pt. III, Act III, Scene I.

[20]Id. To be fair, Kruse states in full that: “Drucker is of course a brilliant thinker of modern business but his definition of leader is too simple.”

On February 13, 2020, the Canadian Competition Bureau struck another blow against so-called “drip-pricing” ticket selling tactics when it slammed the deceptive online advertising, marketing, and selling practices of StubHub Canada Ltd. and StubHub Inc. (collectively “StubHub”) for failing to display the real price of the entertainment and sporting events tickets they sold upfront, instead augmenting prices through the addition of quasi-hidden mandatory fees.

The companies ultimately agreed to pay a $1.3 million administrative monetary penalty to the Canadian Commissioner of Competition as part of a Consent Agreement (“Agreement”) following the Bureau’s investigation and the determination by the Commissioner of Competition/Competition Tribunal that the companies had made representations to the public that were false and misleading in a material respect and that they had engaged in conduct reviewable under the Competition Act(Canada).