Your pacemaker uses machine learning algorithms to detect irregularities in your breathing and make related predictions about the function of your heart.[1] Although this allows for more precise treatment of your condition, it may take the privacy and security concerns from your smart watch, a mere wearable, and literally implant them into your heart.[2] Surgeons using smart scalpels;[3] dermatologists using AI-assisted research and data-mining tools to assist with difficult diagnoses;[4] radiologists using deep-learning algorithms to read diagnostic imagery with greater precision than human capability;[5] precision AI to detect breast cancer as well as applications in cardiology, pathology, and ophthalmology[6] are only some of the examples of the ever-increasing availability and use of wearable and implantable medical AI.[7] Each such use of medical AI offers potential benefits of greater patient well-being through earlier detection and more effective treatment of disease, but with all technology, the benefits come with trade-offs.

Some of these trade-offs come in the form of legal uncertainty. Indeed, increasing use of medical AI raises a number of legal questions. For example, who is liable if your heart is hacked and damage results?[8] Does available insurance adequately cover the risks?[9] Can patients be expected to understand enough about how a device functions to fully comprehend the scope of potential downstream risk?[10] This article offers a brief introduction to these issues and points out areas that require careful attention by legal scholars and practitioners alike.

A (Very) Brief Introduction to AI

Many misunderstand AI at least in part because of the lack of a generally agreed-upon definition.[11] When speaking in the most general terms, experts explain AI as “a set of techniques aimed at approximating some aspect of human or animal cognition using machines.”[12]Although many view AI as a broad term used to refer to a large set of information sciences, each with its own growing domain of research and application,[13] advances in computer processing speed and the growth of big data promoted increased interest in a subdiscipline of AI generally referred to as machine learning.[14] Interest in machine learning is so widespread that popular discussion of AI often uses the term “AI” to refer to one or more types of machine learning.[15] Given that machine learning is typically used to make predictions, it often makes up some element of medical AI technologies.[16] As a result, the core issues that exist at the intersection of law and AI are also applicable in the medical AI context.[17] Complicating those already complex issues (because medical AI deals in large amounts of health data), medical AI also raises novel issues at the intersection of privacy law, cybersecurity obligations, and consumer protection.

Legal Issues in Medical AI: Automated Insulin Pumps

To explore the legal issues raised by medical AI, consider a specific use case. Medical professionals increasingly use AI to help treat chronic illnesses such as type 1 diabetes. An autoimmune disease that usually strikes children at the age of 12, medical professionals treat type 1 diabetes through the use of insulin. Insulin can be administered through daily injections or through the use of an insulin pump. Insulin pumps continually infuse insulin through a small catheter placed under the skin, which is changed out every two to three days.[18] The difficulty in treating type 1 diabetes lies in the regulation of blood sugar through this insulin infusion. Almost any external factor, such as food intake, water intake, exercise, temperature, and internal factors such as cortisol output, thyroid function, and other illnesses, can cause blood glucose readings to fluctuate wildly throughout any given day.[19] This fluctuation especially hits extremes in growing children and in those patients in the midst of puberty due to the natural hormone fluctuations that occur during that time.[20] In order to better control these blood sugar fluctuations, insulin pump manufacturers like Medtronic have begun to employ algorithmic and AI technology in their latest generation of insulin pumps.[21]

Medtronic’s 670G insulin pump uses data from a corresponding Continuous Glucose Monitor (CGM) worn by the patient to consistently alter insulin infusion.[22] The data flow supplied by the CGM allows the machine learning algorithm embedded in the insulin pump to automatically give less or more insulin as the patient’s blood glucose trend rises or falls.[23] This technology represents a significant step forward in the treatment of type 1 diabetes, and many view it as the next step forward for researchers working to create an “artificial pancreas,” an external device that would regulate blood sugars autonomously, without numerous interventions from the patient.[24]

Although this new insulin-regulating technology represents a significant step forward for patients and doctors, it highlights some of the key issues in the use of medical AI more broadly. The 670G pump uses “a human in the loop” type of AI[25] which utilizes machine learning but defers to humans for essential decisions.[26] Although this type of system can limit liability for the pump creator, it can impose a higher burden on patients because patients must interact with the pump repeatedly throughout the day and night.[27] Part of the difficulty in using a human-in-the-loop machine learning algorithm for treatment of chronic medical conditions relates to the “long tail problem.”[28] Essentially, a system may never get “smart” enough to truly be autonomous in some contexts because of the large quantity of variables that cannot be anticipated.[29] Wearable technology such as the 670G closed-loop hybrid insulin pump involves a vast number of variables internal and external to the body that greatly affect blood glucose values, and that limit the level of autonomy that can be achieved in this treatment context.[30]

Another set of issues raised by medical AI is cybersecurity and data privacy.[31] In the case of insulin pumps, many users are concerned about the capturing of their data and personal medical information by both insulin pump manufacturers and hackers.[32] This is especially important due to the rise of CGMs, which connect to a patient’s phone and computer automatically.[33] Although this connection can help the patient examine their blood glucose trends, it also makes sensitive medical data available to hackers who could manipulate readings, causing significant harm to the patient.[34] As the use of CGMs continues to rise not only in type 1 diabetics, but also in type 2 diabetics, cybersecurity will only continue to be a greater concern.[35] Notably, CGMS and the 670G pump represent examples of broader industry trends in which wearable medical technology use similar product approaches, triggering similar concerns.

Conclusion

In some medical contexts, AI has already proven itself effective in helping patients and doctors.[36] For example, the technology unquestionably improves diagnosis of diseases in certain contexts because information about diagnosis from imaging can be retrieved from a set of experts and input for evaluation by the computational device.[37] However, as evidenced by the example of the 670G insulin pump, the use of medical AI for ongoing treatment of chronic conditions poses some difficulties. Those difficulties, including heightened burden for patients using products that rely on a human-in-the-loop system, cybersecurity, and data privacy, represent issues that attorneys guiding companies in this context should keep in mind for the purpose of adequately conducting risk assessments and in the interest of serving patients well. If the future of medical AI is to extend beyond medical diagnosis of narrow conditions,[38] the law and lawyers guiding clients through the law as they build products should keep these issues in mind and seek workable solutions. Ultimately, medical AI represents an area to watch in that patients need the ability to make informed decisions about the trade-offs between potentially improved medical care and risks to privacy, security, and available remedies if something goes wrong with the device.

[4] Esteva A, Kuprel B, Novoa RA, et al., Dermatologist-Level Classification of Skin Cancer with Deep Neural Networks, 542 Nature 115, 115–18 (2017).

[5] J.G. Lee, S. Jun, Y.W. Cho, H. Lee, G.B. Kim, J.B. Seo, N. Kim,Deep Learning in Medical Imaging: General Overview, 18 Korean J. Radiol. 570 (2017).

[7] Changhyun Pang, Chanseok Lee & Kahp-Yang Suh, Recent Advances in Flexible Sensors for Wearable and Implantable Devices, 130 J. App. Polym. Sci. 1429 (2013).

[11] Ryan Calo, Artificial Intelligence Policy: A Primer and Roadmap, 51 U.C. Davis L. Rev. 399, 403 (2017); Matthew U. Scherer, Regulating Artificial Intelligence Systems: Risks, Challenges, Competencies, and Strategies, 29 Hvd. J. L. & Tech. 353, 359 (2016) (“Unfortunately, there does not yet appear to be any widely accepted definition of artificial intelligence even among experts in the field, much less a useful working definition for the purposes of regulation.”).

[13] M. Tim Jones, Artificial Intelligence: A Systems Approach 5 (2007).

[14] Calo, supra note 11, at 403; see also Amanda Levendowski, How Copyright Law Can Fix Artificial Intelligence’s Implicit Bias Problem, 93 Wash. L. Rev. 579, 590 (2018) (“Most AI systems are trained using vast amounts of data and over time hone the ability to suss out patterns that can help humans identify anomalies or make predictions. Most AI needs lots of data exposure to automatically perform a task.”).

[15] Levendowski, supra note 14, at 590 (“When journalists, researchers, and even engineers say ‘AI,’ they tend to be talking about machine learning, a field that blends mathematics, statistics, and computer science to create computer programs with the ability to improve through experience automatically.”). There are several types of machine learning, the details of which are beyond the scope of this short article. For more information, see Stuart J. Russell & Peter Norvig, Artificial Intelligence: A Modern Approach 650 (2d ed. 2009).

[16] A. Michael Froomkin, Ian Kerr & Joelle Pineau, When AIs Outperform Doctors: Confronting the Challenges of a Tort-Induced Over-Reliance on Machine Learning, 61 Ariz. L. Rev. 33, 39–48 (2019).

[17]See generally Harry Surden, Artificial Intelligence and Law: An Overview, 35 Ga. St. U. L. Rev. 1305 (2019) (describing machine learning and expert systems as the two preeminent forms of AI in use today and offering an overview of the current associated legal issues).

[31] David C Klonoff, Cybersecurity for Connected Diabetes Devices, J. Diabetes Sci. & Tech. (2015); W. Nicholson Price II, Artificial Intelligence in Health Care: Applications and Legal Issues, 14 SciTech Law. 10 (2017).

In Re PLX Technology Inc. Stockholders Litigation[1] is not just another opinion out of the Delaware Court of Chancery: it is a parable that captures the zeitgeist of our modern activist epoch. The facts (as established by Vice Chancellor Travis Laster[2]) unfold like a morality play with a familiar and colorful cast of characters and caricatures—the opportunistic shareholder activist fixated on wringing out a quick profit, the exhausted board surrendering to the inevitable, the conflicted banker playing both sides, the complicit lawyers covering up bad process, and the powerful but perfunctory proxy advisors acting as kingmakers. As the actors play their parts, they illuminate the practical realities and complexities of corporate America in the age of activism. Although not groundbreaking as a matter of legal precedent, the case offers “teachable moments” for all engaged in corporate governance and M&A.

The Story

PLX was a small cap Delaware corporation that developed and sold high-tech gizmos (more precisely, specialized integrated circuits used in connectivity applications). After a shareholder activist fund pressured the company to sell itself in 2012, it entered into an agreement to be acquired by a competitor, IDT. That deal was shot down in 2013 by the FTC on antitrust grounds, causing PLX’s stock to plummet. At that point, another activist hedge fund, Potomac Capital Partners, led by one Eric Singer and the antagonist in our tale, bought five percent of the company’s shares at the depressed price (later increasing its stake to 10 percent). Singer’s investment thesis was simple: he read in the proxy statement for the doomed IDT deal that another bidder, Avago, had expressed interest in buying PLX during the “go-shop” market testing period, and so he figured that he could force a sale and make a quick profit.

Singer fired off a series of highly critical public letters against PLX’s management and board of directors and bullied his way into meetings with them, demanding that they sell the company forthwith. He threatened to sue them personally and launched a proxy fight. The influential proxy advisory firm Institutional Shareholder Services (ISS), whose support the court acknowledged is the deciding factor in many proxy contests, endorsed Singer and his slate even though his only plan for the company was a quick sale. Singer prevailed and was elected to the board along with his two other nominees. At Singer’s “request” and with ISS’s support, he was made chair of the special committee formed to explore “strategic alternatives” (often, as in this case, a euphemism for an effort to sell the company).

Soon after that, PLX’s financial advisor was told by a representative of Avago (whom that adviser was separately representing in buying another competitor, LSI) that Avago was in the “penalty box” while it was buying LSI, but once that deal was completed, it would be happy to buy PLX as well. In addition, the representative specified the price that Avago was willing to pay—$300 million, about $6.50 per share—which was less than LSI had offered but well above PLX’s then-trading price. The financial advisor shared that information with Singer, but neither told PLX’s management or the other members of its board.

A few months later, shortly after Avago had closed its purchase of LSI, Avago’s representative met with Singer and offered to acquire PLX for $6.25 per share. As chair of the strategic alternatives special committee, Singer managed the negotiation process and led the board in a few short days to agree to a price of $6.50, exactly what Avago had said it wanted to pay a few months earlier (which fact remained concealed from the rest of the board).

One “major problem” for that deal, the court found, was that PLX management’s existing business plan generated a discounted cash flow valuation far higher than the proposed $6.50 price.[3] The special committee and the financial adviser had management prepare a lower set of projections, which happened to place the $6.50 deal price squarely in the middle of the fairness range, and which the financial advisor then used as its “base case” for its fairness opinion. The board accepted the deal price pushed by Singer even though they had not received the explanation they had requested for the changed business plan. The judge found that there had been a coordinated effort after the fact, including finessing board minutes and coaching witnesses, to characterize the original business plan as an “aggressive” upside case (while the buyer, he noted, continued to treat that as their base case and the revised lower set of projections as the “downside case”).

Thus, the deal was announced and the tender offer launched. No higher bidders emerged (although the agreement did not impose any preclusive deal protections), and the transaction closed with each share being converted into $6.50 in cash. The board’s 14D-9 recommendation statement advocating acceptance of that price had not disclosed that Singer and the company’s investment bankers had been told by Avago six months earlier what it would be willing to pay (or that this fact had been concealed from the rest of the board). It also asserted that the new projections on which the board’s approval of the deal price was based had been prepared “in the ordinary course of business.”[4] The court found both the former omission and the latter assertion materially misleading.

The plaintiffs sued the directors for breach of their fiduciary duties in approving the merger and for breaching their duty of disclosure when recommending the deal, and sued Potomac, the investment banker as well as the buyer Avago for aiding and abetting the directors’ breaches. The claims against Avago and some directors were dismissed, and the remaining directors and investment bank settled, leaving only Singer’s activist fund Potomac to defend the aiding and abetting claim at trial.

The Holdings

The court first held that because of the materially misleading public disclosures in the board’s recommendation statement, the directors’ decisions were not entitled to business judgment deference under the Corwin[5] line of cases. The directors’ actions instead would be subjected to the elevated level of judicial scrutiny under the Revlon[6] standard applicable when a board decides to sell the company that obligates them to seek the transaction offering the best value reasonably available to stockholders.

The court found that the company’s directors breached those fiduciary duties to stockholders by engaging in a sale process without knowing critical information in addition to breaching their duty of disclosure. The judge noted, however, that the directors other than Singer (who were no longer defendants because they had settled or been dismissed) could not be blamed in any morally culpable sense, given that they had been misled by Singer and their own financial adviser. Moreover, the judge noted that the sale process conducted by the board in this case would have fallen within in the range of reasonableness called for by Revlon absent the divergent interests of Singer and the financial adviser, which called for skepticism. In Potomac and Singer’s case, the judge noted that although shareholders are generally aligned in seeking higher value, “activist hedge funds are impatient shareholders” who “espouse short-term investment strategies and structure their affairs to benefit economically from those strategies, thereby creating a divergent interest in pursuing short-term performance at the expense of long-term wealth.”[7] The investment adviser’s conflicts derived from their contingent-fee arrangement and their “longstanding and thick relationship with Avago,”[8] both of which were disclosed, although the earlier price tip (which is what “fatally undermined the sale process”[9]) was not. The financial advisor had also settled before the trial, but both sets of divergent interests had “color[ed] the [c]ourt’s assessment of the decisions that the directors made.”[10]

Turning then to Potomac, the court held that the activist fund, acting through its co-manager Singer, had knowingly participated in—indeed caused—the directors’ breaches of duty by withholding material information from the board and by working to engineer the sale that he had wanted from the outset. The villain had been caught with his little red hands in the cookie jar. So far so good in our parable.

However, then came an unexpected plot twist: despite finding that Singer had acted improperly and caused the board to violate its fiduciary and disclosure duties, the court declined to grant any remedy for shareholders or impose any consequences on Singer or Potomac for their wrongful behavior. This is because the court found that the plaintiffs did not prove any causally related damages. The plaintiffs had argued that the company should have remained a standalone entity and, as such, it was worth more than $6.50 per share. The judge held that they failed to prove that point, and determining that on the record the merger consideration exceeded the standalone value of the company at the time it was sold, entered judgment in favor of the wrongdoers: Singer and Potomac could keep their ill-gotten gains.

The parties cross-appealed, the plaintiffs arguing that Vice-Chancellor Laster erred in not finding damages, and Potomac seeking to overturn the fiduciary breach findings. In a three-page opinion issued on May 16, 2019, the Supreme Court of Delaware affirmed the Court of Chancery’s finding that the plaintiffs failed to prove that they suffered damages and therefore did not need to address Potomac’s cross-appeal arguments. In essence, the Supreme Court determined that it had no basis to overturn the lower court’s decision that because the plaintiffs had not proven damages, Potomac could keep its gains whether ill-gotten or not.

The Moral of the Story

There are several morals that can be drawn from this sordid little tale.

One of them is hopefully not that activist stockholders can get away with unlawful and reprehensible behavior. An activist might be forgiven for concluding that, given the same situation, they can do exactly what Singer did because if they did not succeed in getting the company sold, there would be no claim, and if they did get it sold for a premium, a judge would say “no harm, no foul.”[11]

Many commentators on the corporate side of the debate over shareholder activism celebrated the PLX decision, lauding the Chancery Court’s recognition that activist shareholders often have short-term incentives that are not aligned with those of the shareholder body at large. They were also encouraged by the court’s reiteration that directors representing investors cannot cite their obligations to those investors to dilute their fiduciary duties to the company’s shareholders at large, its finding that Singer violated his duties as a director, and its willingness to hold Potomac liable for its representative’s behavior. There is indeed much to commend in this decision that should at least have activist investors considering whether their own self-interested tactics are consistent with the duties they or their board nominees have undertaken. However, the plaintiffs’ failure to convince the court that the wrongdoers did in fact cause harm to the shareholders is unfortunate.

A large part of the Chancery Court’s reasoning in holding that PLX’s shareholders were not harmed by the sale is that it was merely being true to the recent jurisprudence established in the appraisal context, as emphasized by the Delaware Supreme Court in the Dell[12] case. If the (adequately shopped) deal price is good enough to establish the value of the sold company for appraisal purposes, the argument runs, it should be good enough in the post-closing “quasi-appraisal” context as well. There is, however, a fundamental distinction between the PLX situation and the appraisal context. In a typical appraisal case, the board of directors had determined that the time was right to sell the company, and the question at issue is whether the price obtained in the sale was fair value for the challenging shareholder’s interest. In such a case, for all the reasons enunciated in the Dell and DFC[13] line of cases, it makes perfect sense to give great gravitational weight to the negotiated board- and shareholder-approved deal price. In a case like PLX, however, where an activist forced through the sale of the company, the claim that this was not the right time to sell the company, which would have been more valuable on a standalone basis, has more legitimacy. In most cases, activists who “force a sale” do so by obtaining shareholder support using some combination of financial power, stealth accumulation, bullying or bad-mouthing tactics, and open or covert collusion with their fellow travelers (or “wolf pack”). Given that they typically do not owe fiduciary duties to the other shareholders of the target company, these tactics, however disagreeable, do not amount to a fiduciary breach. (The collusion may violate federal securities laws,[14] but that is grist for a different morality play.) In this case, however, Singer added subterfuge to the usual activist arsenal and did so at a time when he was on the company’s board, thus owing duties both to the company’s other directors and to its shareholders, which he breached. Singer and Potomac’s behavior may well have cost PLX shareholders substantial value by causing the company to be sold before the time was right.

This is not just a hypothetical possibility, although the fact pattern is not one that comes up very often. One prominent example of how activist “value creation” by forcing the sale of a company can in fact be value destructive is provided by the case of Actelion Ltd., a Swiss biotech company. In 2011, Paul Singer’s Elliott Management ran a campaign to force “underperforming” Actelion to sell itself for around $10 billion (a seemingly reasonable premium to its then-market cap of around $7 billion).[15] Fortunately, Elliott was defeated (despite ISS having supported three of his candidates). This defeat allowed Actelion to keep building long-term value and sell itself in 2017 to Johnson & Johnson for over $30 billion, more than three times the value Elliott had hoped to yield.[16] Actelion’s shareholders would have forfeited over $20 billion in value if Paul Singer had used the tactics that Eric Singer used and won his bid to sell the company in 2011. PLX may well have been worth far more on a standalone basis, but the plaintiffs were not able to make that case.

Post-closing damages claims (sometimes called “quasi-appraisal” claims) are—and should be—difficult to sustain. As some recent cases have noted,[17] the Revlon test for board conduct in selling a company was designed with pre-closing injunctive relief in mind and is better suited to that equitable remedy than to post-closing damages awards. In general, plaintiffs seeking to assert that the directors did not satisfy their Revlon duties by designing a process to seek the transaction offering the best value reasonably available, or alleging flaws in the disclosure on which the stockholders’ decision is based, should bring those claims before the closing or the shareholder vote, as the case may be. However, in a case like that of PLX where the company’s management and directors were misled and unaware of the facts that “fatally undermined the sales process,” and so could not possibly have addressed them in designing the sale process or disclosed them to shareholders, there is no way the Revlon or disclosure challenges could have been brought in advance. In such a situation, a damages award against the party that tainted the process and caused the disclosure violations may well be warranted.

The lesson that activist nominees should and hopefully will derive from the PLX decision is that when they join a board, they are undertaking strict fiduciary duties to do what is best for all of the company’s shareholders, not just the investor who nominated them. They are now on judicial notice that the Delaware courts understand that activist investors often have a special interest in a short-term profit that diverges from the interests of the shareholders at large. This, of course, also—perhaps especially—holds true for activists nominating themselves. One possible consequence of this decision is that activists may seek fewer board seats for themselves to avoid the uncomfortable position of having to look out for the best interests of someone other than themselves.

The incumbent directors of the company did not escape criticism even though the judge acknowledged that they were not morally culpable. Recognizing that they had been kept in the dark by Singer and their own financial advisers on crucial facts, he nevertheless disparaged them for deferring to Singer and allowing him to control the process, and for being “susceptible to activist pressure,”[18] noting that they “found within themselves a new willingness to support a sale at prices below the values that they had previously rejected.”[19] Alighting on an incumbent director’s testimony that the board was “engaging in the ‘art of the possible,’” the judge perceived this as being in tension with their Revlon duty to seek the best transaction reasonably available.[20]

One can readily derive lessons for corporate directors from this judicial pen-lashing: stay strong; do not give in to activist pressure or defer to activists who join the board; insist on receiving the information you need to make the decisions you are called upon to make; and be vigilant to the possibility that those advising you, whether they be outside advisers, company management, or even other directors, may have conflicting interests that taint their advice. These lessons are important, and many of these critiques may well be applicable to the PLX board; however, anyone who has been in the trenches with a board facing an activist proxy fight can also sympathize to some degree with these incumbent directors.

As much as our corporate governance system in days of yore may have facilitated passive and complacent clubby boards, our current system is stacked against the incumbents. Unless there is a sizable friendly voting bloc in the boardroom, an activist is often able to declare victory as soon as he or she emerges from the shadows. Our securities laws’ early-warning system that was intended to alert the market to impending changes in control is based on half-century-old technology and fails to pick up the range of derivatives and swap transactions used by modern activists engaging in stealth accumulations.[21] Activists are often able to accumulate stakes close to or even over 10 percent of the outstanding shares by the time they have to unveil themselves. The lead activist is often followed by a wolf pack of “me-too” investors with smaller individual stakes that can add up to a sizable supporting bloc. Sometimes these investors are tipped off by the activist about the impending campaign. After the abuses of the 1980s, people like Michael Milken and Ivan Boesky went to jail for “stock parking” violations[22] not all that different to this, but the “group” concept in our securities laws requires an actual “agreement” (even if that can be just an oral understanding).[23] Modern “alpha-wolf” activists and their wolf packs are usually careful not to lay themselves open to allegations that they had agreed to form a group, thus triggering the filing obligation (within the outdated 10-day window), and they do not have to because they can rely on conscious parallelism based on aligned incentives. Often even when there is an acknowledged “13D group” acting in concert with respect to an activist campaign, the timing of the group’s formation is fuzzy, and the SEC has not been particularly aggressive in policing groups, but has allowed the activists to decide for themselves when in the course of their dealings they have reached a sufficient degree of agreement to consider themselves a formal “group.” Adding to the power of the activist, its group members, and its wolf pack, history shows that there is a high likelihood that the proxy advisors, particularly ISS, will throw their substantial weight behind the activist, at least partially. In most companies’ cases, this assures the activist another 10 to 20 percent in support. Moreover, the proxy rules also allow shareholders considerable leeway to communicate among themselves so long as they do not actually solicit proxies.[24] The result of all this is that by the time the activist files its 13D or summons the company’s leadership for a meeting, both sides already know that the activist has a leg up of 25 or 35 percent, if not more, and the activists can often say with some credibility (although they also often exaggerate) that they have spoken with and received support from a majority of the company’s shareholders. Is it at all surprising in this system that the incumbent board will often feel irresistible pressure to accommodate the activist, even if what is being demanded is not what they themselves might feel is the best path for the company?

In recent years, it has become standard operating procedure for a company attacked by an activist to try to reach a quick settlement on suitable terms, usually involving a number of board seats for the activist’s nominees or mutually acceptable third-party candidates, depending on the parties’ relative strength. This practice of settling quickly has in fact also been criticized, including by leaders in the institutional investor community like Larry Fink, CEO of Black Rock.[25] It is a rational response to the situation facing many boards, however, not only because of the likelihood that the activist will win seats anyway (for the reasons described above), but also because the implications of a nasty proxy fight can be devastating for the company and its strategy. The core skill of economic shareholder activists (in addition to their expertise in stealth accumulations) is their ability to drive change to make something happen. Some activists (ValueAct Capital is a leading example) specialize in working behind the scenes as long as possible and taking their fight public only if they believe it necessary to achieve their goals. Others (Carl Icahn and Paul Singer are prime examples) typically come out of the gate swinging, using aggressive tactics such as poison-pen letters and a withering campaign of personal attacks (sometimes with little regard for the veracity of their assertions). Like any other bully, they know that their ability to achieve their desired outcome is proportional to their ability to inflict pain and spread fear. These tactics do not only inflict a heavy personal toll on the directors and executives targeted (something that arguably goes with the territory and may even in some cases be warranted), but they can also jeopardize the company’s ability to succeed in its chosen strategy, sometimes leaving the activist’s plan as the only viable one.

This is not the corporate governance system one would design if one were writing on a blank slate. The PLX parable therefore also offers teachable moments for those who are empowered with the ability to influence our corporate governance system: the SEC, Congress, state legislatures, and judges. They should be aware of the flaws in our system so that they can try to address them.

At the most basic and practical level, companies and boards of directors can learn from PLX that they must remain extremely vigilant against activist investors, especially at moments of vulnerability. Any event that can cause a temporary drop in stock price creates an opportunity for short-term speculators—like Potomac in this case—to buy in and try to orchestrate a quick profit. Losing an announced transaction as PLX did is an obvious situation for such a risk, but unexpected management changes, natural or man-made disasters, legal pronouncements, announcement of some acquisitions, even missing a quarter by a few pennies, could do it too. Vigilance means having contingency plans, knowing what could happen and how you would respond, knowing who your friends and enemies are likely to be, and having a trusted team on deck to deal with any crisis that may arise.

[1]In re PLX Tech. Inc. Stockholders Litig., CA No. 9880-VCL, 2018 WL 5018535 (Del. Ch. Oct. 15, 2018).

[2] The 70-plus pages of factual findings summarized briefly in this article are, as in any case, based on the record before the judge and his determinations of which witnesses were more credible.

[3]In re PLX Tech. Inc. Stockholders Litig., CA No. 9880-VCL, 2018 WL 5018535 at *2 (Del. Ch. Oct. 15, 2018).

[5]See Corwin v. KKR Fin. Holdings LLC, 125 A.3d 304 (Del. 2015). See also Singh v. Attenborough, 506 A.2d 151 (Del. 2016); In re OM Group, Inc. Stockholders Litig., 2016 Del. Ch. LEXIS 155 (Ch. Oct 12, 2016); In re Volcano Corp. Stockholders Litig., 143 A.3d 727 (Del. Ch. 2016).

[6] Revlon, Inc. v. Macandrews & Forbes Holdings, Inc., 506 A.2d 173 (Del. 1986).

[7] In re PLX Tech. Inc. Stockholders Litig., CA No. 9880-VCL, 2018 WL 5018535 at *41 (Del. Ch. Oct. 15, 2018).

Andrew Pery and Michael Simon have been commissioned by the ABA Business Law Section to write a book on Contract Analytics adoption trends. To that end, they have asked the Business Law Section membership to complete a brief survey about your views and use of Contract Analytics technology. You can access the survey by clicking here.

In his seminal work On Legal AI,Joshua Walker, a pioneer in the application of AI to the practice of law, posited the following rhetorical question relating to the benefits of applying AI to contract analysis: How do we use AI to produce “wise contracts”?

Walker’s predicate for posing this question is based on compelling empirical evidence. The legal profession is using outdated and inefficient practices in contract formation and analysis. As lawyers, we tend to be creatures of habit and, as Walker warns, “include certain vestigial clauses whose original purpose has long been absent and . . . do not necessarily reflect evolving business realities.”

In today’s interdependent and high-velocity business climate, contracts should not be viewed only as legal documents that may be used both as a sword and a shield in the event of breach or noncompliance, but rather as documents that set out a mutually enduring business relationship between the contracting parties. This ambition is far from current practices, however. In a recently published HBR article, A New Approach to Contracts, the authors, David Frydlinger, Oliver Hart, and Kate Vitasek, found that:

“[w]hen contract negotiations begin, they default to an adversarial mindset and a transactional contracting approach . . . used to try to gain the upper hand. However, these tactics not only confer a false sense of security but also foster negative behaviors that undermine the relationship and the contract itself.”

A McKinsey study likewise found that a narrowly focused transactional approach to contracting leads to considerable inefficiencies because such contracts “are lacking basic elements that could enable better vendor performance and cost savings.” Contracts are the engine of a business, with 90 percent of spending and investments governed by terms and conditions embodied in them, yet the McKinsey study found that “suboptimal contract terms and conditions combined with a lack of effective contract management can cause an erosion of value in sourcing equal to 9 percent of annual revenues. For Fortune’s 2016 Global 500 companies, this 9 percent would have equaled $2.5 trillion in value.”

Among the recommendations proposed by the McKinsey study is implementation of more rigorous contract review processes that involve cross-functional collaboration between operations and legal teams in order to achieve “greater visibility into existing contracts to enable the organization to write better contracts going forward. A semiautomated, basic screening process involves scanning contracts for keywords and phrases related to performance, value, and selected cost drivers.”

In the case of investigational contract analytics, contract language is important to surface obligations, potential liabilities, choice of law and forum, and representations and warranties in the event of material breach and penalties. Andrew Bartels, a contract life-cycle expert at the industry analyst giant Forrester, refers to this aspect of contract analytics as “who is responsible or liable when things don’t work as planned.”

According to the Institute for Supply Management, a typical Fortune 1000 company manages anywhere between 20,000 to 40,000 active contracts at any given time, at least 10 percent of which are misplaced, difficult to find, still in paper form, or on a file share somewhere, buried in an e-mail attachment, or otherwise unmanaged or forgotten. Unsurprisingly, the general counsel respondents to a Lexis 2018 study demonstrated that more than half of them—53 percent—spent “too much time on repetitive tasks.”

The pressure to adapt to the demands of high-velocity business transactions coupled with an intensely competitive global business environment is transforming how legal services are consumed and delivered. Richard Susskind, in his book Tomorrow’s Lawyers, referenced a confluence of three market drivers that impact the practice of law:

The “more for less challenge.” While legal department’s budgets are cut, the demand for increased output is increasing whereby legal departments are “facing the prospect of an increasing workload and yet diminishing legal resources.”

Liberalization of legal services delivery. Several jurisdictions now endorse Alternative Legal Service Providers (ALSPs), which could pose a significant competitive threat to traditional law firms. The ALSP market is pegged at $11 billion.

Legal expert systems. New AI systems mimic (even if they cannot replicate) human cognitive intelligence and automate tedious and labor-intensive contract review tasks traditionally performed by an army of over-worked lawyers. By way of illustration, JP Morgan developed an automated commercial credit and contracts review AI-based application that can extract 150 attributes from 12,000 commercial credit agreements and contracts in only a few seconds with a high degree of precision—the equivalent to 360,000 billable hours of legal work by its lawyers.

The level of innovation and its transformative impact on the practice of law is unprecedented. As a recent Yale Journal of Legal Technology article warned: “Technological innovation has accelerated at an exponential pace ushering in an era of unprecedented advancements in algorithms and artificial intelligence technologies . . . . [T]o survive the rise of technology in the legal field, lawyers will need to adapt to a new practice of law.”

Looping back to Joshua Walker’s question—“how do we use AI to produce wise contracts?”—the application of AI to contract formation and analysis is not a panacea. Contrary to the dystopian view that AI will replace lawyers, its likely impact will be as a compliment to good and efficient lawyering. One thing is certain, however: as Joshua Walker observes, “AI is fast. AI is cheap and you [as lawyers] are neither.”

Andrew Pery and Michael Simon have been commissioned by the ABA Business Law Section to write a book on contract analytics adoption trends. Please complete a brief survey about your views and use of contract analytics technology. The survey will take less than 20 minutes to complete. Please don’t miss your chance to tell us how you see the future of contracting.

M&A deal terms originating from Europe are increasingly found in the United States, particularly in the context of cross-border deals. Transactions featuring these deal terms are not yet common, but with the current deal environment, including the prevalence of auctions and increased sell-side private equity activity (both primary and secondary exits), some of these deal terms may eventually become commonplace in the United States. This article focuses on two emerging trends in the United States: the use of Vendor Due Diligence Reports (VDD) and the locked-box mechanism.

B. Vendor Due Diligence Reports

A VDD is typically found in a competitive auction process or a dual-track process (which involves preparing a company for an initial public offering while simultaneously pursuing a third-party sale). The VDD is not a marketing document and differs from a confidential information memorandum in that it objectively and comprehensively describes the target company’s financial and legal situation and discloses issues and risks. This is particularly useful in complex transactions because it helps accelerate the process by providing prospective buyers with more information at an earlier stage.

Of course, the VDD is not without its drawbacks. First, the exercise of producing a VDD can potentially be a source of tension between the client and its advisors, not unlike the auditors and their client in the context of audited financial statements. Second, although the VDD provides several benefits to the seller, including accelerating the bid timeline and helping foster detailed and high-quality indicative bids, one of the significant drawbacks is that it identifies issues that may result in lower bids. In this regard, VDD proponents argue that by disclosing the issues up front, the seller reduces the likelihood of a bid being lowered at a later stage of the negotiations (the rationale being that a sophisticated buyer would likely identify these issues as part of its due diligence and could then attempt to lower its initial bid). Third, the time saved during the accelerated bid timeline is simply shifted to the preparation phase, and the costs associated with a VDD can be significant. In Europe, the VDD can be provided to the prospective buyer and its lenders on a reliance basis, with the accounting or law firm preparing the VDD capping its liability vis-à-vis these third parties. VDDs are increasingly offered by accounting firms in the United States, but they are issued on a nonreliance basis. U.S. law firms generally would not provide any due diligence materials on a reliance basis, and it is unclear whether a law firm would be able to limit its liability, which is permitted in several European jurisdictions. However, European law firms and clients sometimes ask American law firms to provide a due diligence report on a reliance basis, and it may be helpful for the parties to clarify early in the process what the expectation is on this particular point. Please refer to the Report of the ABA Business Law Section Task Force on Delivery of Document Review Reports to Third Parties (67 Bus. Law. 99 (2011)) for an in-depth discussion on this particular issue.

C. Locked-Box Mechanism

The locked-box mechanism originated from the United Kingdom and has been used for years in M&A transactions across Europe, but many American sellers and buyers are still unfamiliar with it. In a nutshell, the locked-box approach removes price uncertainty associated with a post-closing working capital or other similar post-closing adjustment in that the seller and buyer negotiate a fixed price when signing the purchase agreement based on the agreed upon locked-box balance sheet. The locked-box mechanism forces the parties to focus on items such as normalized working capital before signing. Given that the economic interest passes to the buyer as at the locked-box date, the seller will often charge a per diem or (alternatively) interest on the equity value from the locked-box date until the closing to reflect the fact that the seller did not receive the proceeds from the buyer when the economic interest was passed to the buyer. Although concepts such as normalized working capital also apply to closing accounts, the parties sometimes do not focus on it as much as they should before signing and procrastinate until it is time to prepare the closing balance sheet, only to realize that they had not focused on (or agreed to) specific adjustments or normalizations. This lack of focus often results in disputes between the parties, and any claims resulting therefrom would not be covered by representations and warranties (R&W) insurance. The paradox is that the parties secure R&W insurance to avoid post-closing claims, but according to escrow claim studies, claims relating to purchase price adjustments are among the most frequent claims under a purchase agreement. As a result, one of the most “common” risk is one that is not covered by R&W insurance. Although the locked-box mechanism virtually eliminates purchase price adjustment disputes, it can introduce other issues. For one thing, the parties must agree on what constitutes permitted leakage between the locked-box date and the date of closing. An example of such permitted leakage would be arm’s-length, intra-group payments in the ordinary course. The locked box may not be appropriate in all circumstances: a carve-out transaction where assets from different divisions are sold and where there are no financial statements for the carved-out business would be problematic. Finally, agreeing on the locked-box balance sheet may prove to be more difficult in the context of a highly cyclical business, such as a toy business.

D. Conclusion

Although the deal terms described above remain uncommon in America, they are increasingly seen particularly in the context of cross-border deals with Europe. Some of these trends have already migrated to other parts of the world. Given the predictability of the locked-box mechanism and the fact that it virtually eliminates purchase price adjustment disputes, it seems to be the logical complement to R&W insurance, and it is surprising that this approach is not more common in the United States, especially in transactions involving a private equity seller.

In her chapter titled “Artificial Intelligence and the Work of Visionary Boards” from the ABA’s new book Law of Artificial Intelligence and Smart Machines, Anastassia Lauterbach reports that her research has shown that “traditional boards are not sufficiently prepared to address and fully benefit from AI.” Here are some of her findings from the chapter.

Editor, Ted Claypoole

“Before starting with any AI implementation, directors have to understand three facts:

It is becoming an increasingly obvious fact that certain mission critical business and compliance problems cannot and will not be properly solved without AI, including notably, cyber-security.

The regulatory environment around AI is in flux. Technology once again is outpacing and out-flanking the legal and regulatory frameworks, creating confusion as well as opportunity.

Companies must find talent that understands technology, but also has a keen ability to work cross-functionally. Business development and HR executives should rise to new prominence in companies that embrace emerging technologies such as AI.

. . .

There are several market-related factors boards need to understand in order to consider AI within their operational risk management frameworks and strategy oversight.

Technology leaders expect that within the next ten years AI as a stand-alone theme might disappear. It will get embedded into whatever product, service or process a company is designing and/or implementing. There are several market- and customer-related questions a board can ask to evaluate if a company should add Machine Learning components into its products and services. Some of these questions can also support decision making around AI vendors.

Cost to deploy. How much will it cost your customer not just to purchase your technology but also to change from their current solution to the new one? What is a minimum payback period in years in capital expenditures for a prospective customer, or for your company, if a vendor pitches a new Machine Learning solution?

Added-value beyond cost: What value does your Machine Learning-based software offer beyond labor substitution? Better quality, enhanced customer satisfaction, fewer errors, higher performance or throughput, something else?

Conflicting goals within potential customers: The scale at which AI or ML will eliminate or reduce human labor is likely to be significantly larger than any prior technology, resulting in potentially greater resistance. Will the human teams you are selling to lose their jobs as a result of your technology?

Regulatory/compliance issues: What are the current regulatory constraints that might complicate the adoption of your/the vendor’s offering? Besides technical challenges, humans tend to be more forgiving about mistakes made by humans as opposed to those made by AI, which might increase the liability hurdle on people overseeing automated systems.

Cybersecurity issues: The U.S. intelligence community reports that AI actually works in cybercriminals’ favor.[1] Neural networks can be trained to create spams resembling a real email and become an agent for phishing attacks. Fake audio and video files can mimic voice. CAPTCHA bypassing seems to be very easy, exposing digital sign in.[2] Most passwords can be breached with the brute force of Machine Learning. In 2017, the first publicly known example of AI for malware creation was proposed at Peking University in Beijing, when the authors created a MalGAN network.[3]

Industry readiness: Sometimes an industry is just not ready to adopt a new solution because it is highly risk-averse. This occurs primarily in industries that are focused and incentivized on time-consuming activities rather than efficiency through new business models and technologies. An example of this can be seen in traditional utilities. Artificial Intelligence is sometimes incorrectly thought of as a “plug and play” or “black box” solution, when in fact it is not.[4]

Vendors’ dynamics: Boards need to understand how top Internet brands, Machine Learning startups and traditional enterprise vendors compete. So far there are five full-stack AI companies, and all of them are among the global Fortune 10 list of the most valuable companies. These are Alphabet, Apple, Microsoft, Facebook and Amazon. I call these players “full-stack AI companies” as they control the whole technology stack—from semiconductors to devices—from their own platforms to ensure Machine Learning is utilized at every part of their organizations to build AI-powered consumer and business applications. Alphabet, Microsoft and Amazon are competing for dominance in cloud while constantly adding AI offerings. On the other hand, successful machine learning startups have deep domain expertise, and have concrete suggestions on how to solve their customers’ problems within a given legacy IT environment. Traditional enterprise vendors are jumping on the AI bandwagon, though they still have to demonstrate they can differentiate with their ML offerings.”

[1] James R. Clapper, “Statement for the Record. Worldwide Threat Assessment of the US Intelligence Community”, Senate Armed Services Committee, February 9th 2016.

[2] Suphannee Sivakorn, Jason Polakis, and Angelos D. Keromytis, “I’m not a Human: Breaking the Googe reCAPTCHA”, Columbia University, NY, 2016.

[3] “Weiwei Hu, Ying Tan, “Generating Adversarial Malware Examples for Black-Box Attacks Based on GAN”, Peking University, Beijing, 2017, arxiv.org.

[4] Daniel Fagella, “AI Adoption – What it Takes for Industries to Change, HuffPost, August 1st 2017.

For the last several years, noncompete agreements have been under attack in the United States by regulators, legislators, and the courts. For example, late last year, Massachusetts joined a number of states by enacting a law regulating noncompete agreements, including making them inapplicable to “nonexempt” employees. Courts do not favor noncompetes and will limit them or invalidate them completely. Regardless, noncompete agreements are here to stay, and businesses continue to rely on them as one way to protect customer goodwill along with confidential and proprietary information, which is why it’s important for counsel (in-house and outside) to take steps to ensure the noncompete agreements used by their clients have the best chance of surviving regulatory and judicial scrutiny. Here are some tips:

What is a noncompete agreement? A noncompete agreement is a contract entered into by an employer and an employee whereby the employee agrees that if their employment terminates (usually for any reason), then the employee will not—for some period of time and within some geographic boundary—compete directly with or go to work for a company that competes directly with the employer. Most U.S. courts will enforce noncompete agreements if they are reasonable as to geography and time and there is a legitimate business interest at stake.

Keep the group small. One controversial area is the extension of noncompete agreements to all the employees of a company, including administrative assistants and minimum wage workers. When reviewing a noncompete dispute, courts will review whether the employee has access to sensitive customer information and/or any other specialized or confidential information that could harm the employer if that employee started a competing business or went to work for a competitor. Tailor your agreement to the applicable employees and their particular circumstances.

Keep the restrictions reasonable and narrow. Courts will review a noncompete to ensure it does not interfere with the public interest (as set out in state law/state court decisions) or impose an undue hardship on the employee. This analysis includes reviewing the noncompete agreement for reasonableness as to geography and time. If either is overly broad, the court will not enforce the agreement. For example, a worldwide, five-year noncompete is unlikely to survive. Your noncompete stands a much better chance if the restrictions are narrowly drawn to the minimum necessary to protect the company. A one-year noncompete, limited to the state/geography where the company is based/competes will likely withstand scrutiny.

Provide consideration for the agreement. A noncompete, like any other contract, requires consideration to create a valid, enforceable agreement. If you require employees to sign your noncompete as part of their initial job offer, that is sufficient consideration. If you attempt to require an existing employee to sign a noncompete or else they lose their job, that is not sufficient consideration. If the agreement is part of a promotion, stock grant, special bonus payment, or similar offering, however, then the consideration element is satisfied.

Get it in writing. Relying on common law rights around noncompetition versus a clear contractual obligation is playing with fire. All noncompetes should be set out in writing and signed by both parties. Include a provision that gives the employee time to consult with an attorney to review the agreement before a signature is required (including a place for the employee to initial that section).This will help with enforcement.

Prepare multiple versions if necessary. Utilizing a single noncompete template is a bad idea unless your employees work only in one state or one country and work under similar circumstances; otherwise, be prepared to customize your noncompete template based on the laws of each jurisdiction where your employees work. Avoid using one template and finding out it’s unenforceable somewhere when you actually need to enforce it.

Concede choice of law/forum. Choice of law and choice of forum should get extra attention. If enforcement of your noncompete requires the employee to travel long distances at their expense (time and money) or if it imposes the law of a state or country that conflicts with rights the employee enjoys where he or she lives, you can run into problems. Balance and reasonableness are key.

Provisions to include. In addition to choice of law and forum, there are three basic clauses that you should include in every noncompete agreement:

Injunctive relief. Include a clause that expressly provides for injunctive relief as a remedy in the event of a breach. This clause should also provide that if there is a breach, there is a presumption of irreparable harm and consent to injunctive relief.

Attorney’s fees. Your noncompete should provide for an award of attorney’s fees and costs to the prevailing party.

Savings clause. This clause provides that if a court should render any clause in the noncompete invalid, the remaining contract clauses survive intact.

Use other types of agreements. Consider utilizing other types of agreements that might be less draconian than a noncompete but provide some of the same protections, e.g., nonsolicitation agreements (customers and employees) and nondisclosure agreements (protecting confidential information of the company).

Be prepared to enforce it. Nothing puts people on notice about the consequences of violating a noncompete like knowing you will file a lawsuit to enforce it. If you are going to use noncompete agreements, be prepared to enforce them in court.

Imagine that you are a plaintiff in a lawsuit, and you just settled your case for $1,000,000.[1] Your lawyer takes 40 percent ($400,000), leaving you the balance. Most plaintiffs assume their worst-case tax exposure would be paying tax on $600,000, but today, you could pay taxes on the full $1,000,000. Welcome to the crazy way legal fees are taxed.

In Commissioner v. Banks,[2] the Supreme Court held that plaintiffs in contingent-fee cases must generally recognize income equal to 100 percent of their recoveries. This is so even if the lawyer is paid directly by the defendant, and even if the plaintiff receives only a net settlement after fees. This harsh tax rule usually means plaintiffs must figure a way to deduct those fees.

Until 2018, there were two ways to deduct: above the line or below the line. Below-the-line (also called miscellaneous itemized) deductions, where plaintiffs historically deducted most legal fees, were disallowed for 2018 through 2025.[3] Thus, beginning in 2018, above the line is the only remaining choice, if you qualify. The above-the-line tax deduction is for employment, civil rights, and whistleblower legal fees, and is more important than ever. Qualifying for it means that in our example, at most you are taxed on $600,000.

Physical Injury Recoveries

You might think there would be no tax issues in physical injury cases, where damages should be tax free, but section 104 (the tax exclusion section for physical injury recoveries) applies only to compensatory damages, not to punitive damages or interest. What if a case has some of each?

Example: You are injured in a car crash and sue the other driver. Your case settles for $2 million—50 percent compensatory for physical injuries and 50 percent punitive damages. There is a 40-percent contingent fee. That means you net $1.2 million. However, the IRS divides the $2 million recovery in two and allocates legal fees pro rata. You claim $600,000 as tax free for physical injuries, but you are taxed on $1 million and cannot deduct any of your $800,000 in legal fees.

“Unlawful Discrimination” Recoveries

The above-the-line deduction applies to attorney’s fees paid in “unlawful discrimination” cases. The tax code defines a claim of unlawful discrimination with a long list of claims brought under:

The Civil Rights Act of 1991

The Congressional Accountability Act of 1995

The National Labor Relations Act

The Fair Labor Standards Act of 1938

The Age Discrimination in Employment Act of 1967

The Rehabilitation Act of 1973

The Employee Retirement Income Security Act of 1974

The Education Amendments of 1972

The Employee Polygraph Protection Act of 1988

The Worker Adjustment and Retraining Notification Act

The above-the-line deduction applies to whistleblowers who were fired or retaliated against at work. However, what about whistleblowers who obtain awards outside this context? The deduction applies to federal False Claims Act cases and was later amended to cover state whistleblower statutes as well. It applies to IRS tax whistleblowers and in 2018 was extended to SEC and Commodities Futures Trading Commission whistleblowers.

Catchall Employment Claims

Arguably the most important item in this list is a catchall provision for claims under:

[a]ny provision of federal, state or local law, or common law claims permitted under federal, state or local law, that provides for the enforcement of civil rights, or regulates any aspect of the employment relationship, including claims for wages, compensation, or benefits, or prohibiting the discharge of an employee, discrimination against an employee, or any other form of retaliation or reprisal against an employee for asserting rights or taking other actions permitted by law.[5]

This is broad and should cover employment contract disputes even where no discrimination is alleged.

Civil Rights Claims

The catchall language in section 62(e)(18) also provides for deduction for legal fees to enforce civil rights. This unlawful discrimination deduction is arguably even more important than the deduction for fees relating to employment cases. What exactly are civil rights, anyway? You might think of civil rights cases as those brought under section 1983. However, the above-the-line deduction extends to any claim for the enforcement of civil rights under federal, state, local, or common law.[6] Civil rights is not defined for the purposes of the above-the-line deduction, nor do the legislative history or committee reports help. Some general definitions are broad, indeed, including:

a privilege accorded to an individual, as well as a right due from one individual to another, the trespassing upon which is a civil injury for which redress may be sought in a civil action. . . . Thus, a civil right is a legally enforceable claim of one person against another.[7]

In an admittedly different context (charitable organizations), the IRS itself has generally preferred a broad definition of civil rights. In a General Counsel Memorandum, the IRS stated that it “believe[s] that the scope of the term ‘human and civil rights secured by law’ should be construed quite broadly.” Could invasion of privacy cases, defamation, debt collection, and other such cases be called civil rights cases? Possibly.

What about credit reporting cases? Don’t those laws arguably implicate civil rights as well? Might wrongful death, wrongful birth, or wrongful life cases also be viewed in this way? Of course, if all damages in any of these cases are compensatory damages for personal physical injuries, then the section 104 exclusion should protect them, making attorney’s fee deductions irrelevant.

However, what about punitive damages? In that context, plaintiffs may once again be on the hunt for an avenue to deduct their legal fees. Reconsidering civil rights broadly might be one way to consider fees in the new environment. In any event, the scope of the civil rights category for potential legal fee deductions merits separate treatment in a forthcoming article.

Business Expenses

If sections 62(a)(20) and 62(e) are not fertile grounds for legal fee deductions, is anything else available? Can legal fees be a business expense? Of course they can. Business expense deductions were largely unaffected by the 2017 tax changes, other than the Weinstein provision restricting deductions in confidential sexual harassment cases.[9]

In a corporation, LLC, partnership, or sole proprietorship, business expenses are above-the-line deductions. Of course, one must ask whether one’s activities are sufficient to be considered really in business, and whether the lawsuit really is related to that business. If one can answer both of these questions in the affirmative, all is well.

However, a plaintiff filing his or her first Schedule C as a proprietor for a lawsuit recovery probably may not be convincing. Before the above-the-line deduction was enacted in 2004, some plaintiffs argued their lawsuits were business ventures. Plaintiffs usually lost these tax cases.[10] The repeal of miscellaneous itemized deductions until 2026 may revive such attempts.

Some may push the envelope about what is a trade or business and how their lawsuit is inextricably connected to it. Some plaintiffs may consider filing a Schedule C even if they have never done so before. Schedule C is historically more likely to be audited and draws self-employment taxes.

Capital Gain Recoveries

If your recovery is capital gain, you arguably could capitalize your legal fees and offset them against your recovery. You might regard the legal fees as capitalized or as a selling expense to produce the income. Thus, the new “no deduction” rule for attorney’s fees may encourage some plaintiffs to claim that their recoveries are capital gain, just (or primarily) to deduct or offset their attorney’s fees.

Exceptions to Banks

The remaining ideas in this article address attempting to keep attorney’s fees out of the plaintiff’s income in the first place. Technically, falling within one of the exceptions to the Banks case is not a way of deducting legal fees, but of avoiding the fees as income. In Banks, the Supreme Court laid down the general rule that plaintiffs have gross income on contingent legal fees. General rules have exceptions, however, and the court alluded to situations in which this general 100-percent gross income rule might not apply.

Separately Paying Lawyer Fees

Some defendants agree to pay the lawyer and client separately. Do two checks obviate the income to plaintiff? According to Banks, they do not. Still, separate payments cannot hurt, and perhaps Forms 1099 can be negated in the settlement agreement.

The Form 1099 regulations generally require defendants to issue a Form 1099 to the plaintiff for the full amount of a settlement, even if part of the money is paid to the plaintiff’s lawyer. Even so, a defendant might agree to issue a Form 1099 only to the plaintiff for the net payment. Banks seems to dictate there is gross income anyway, but the plaintiff might feel comfortable reporting only the net.

Fees for Injunctive Relief

The Supreme Court suggested that legal fees for injunctive relief may not be income to the client. If the plaintiff receives only injunctive relief, but plaintiffs’ counsel is awarded large fees, should the plaintiff be taxed on those fees? Arguably not. However, if there is a big damage award with small injunctive relief, will that take all the lawyer’s fees from the client’s tax return? That seems unlikely, although the documents might help finesse it.

Court-Awarded Fees

Court-awarded fees may also provide relief, depending on how the award is made and the nature of the fee agreement. Suppose that a lawyer and client sign a 40-percent contingent-fee agreement providing that the lawyer is also entitled to any court-awarded fees. A verdict for plaintiff yields $500,000, split 60/40. The client has $500,000 in income and cannot deduct the $200,000 paid to his or her lawyer. However, if the court separately awards another $300,000 to the lawyer alone, that should not have to go on the plaintiff’s tax return. What if the court sets aside the fee agreement and separately awards all fees to the lawyer?

Class-Action Fees

There has long been confusion about how legal fees in class actions should be taxed. Historically, there was a difference between the tax treatment of opt-in cases and opt-out cases. In more recent years, however, the trend appears to be away from taxing plaintiffs on legal fees in class actions of both types.

That is fortunate because the legal fees in class actions generally dwarf the amounts plaintiffs take home. It is an over-generalization, but most plaintiffs in most class actions generally assume that they will not be taxed on the gross amount (or even their pro rata amount) of the legal fees paid to class counsel. Optimally, the lawyers will be paid separately under court order.

Statutory Attorney’s Fees

If a statute provides for attorney’s fees, can this be income to the lawyer only, bypassing the client? Perhaps in some cases, although contingent-fee agreements may have to be customized. In Banks, the court reasoned that the attorney’s fees were generally taxable to plaintiffs because the payment of the fees discharged a liability of the plaintiffs to pay their counsel under their fee agreements. In statutory fee cases, a statute (rather than a fee agreement) creates an independent liability on the defendant to pay the attorney’s fees. If the statutory fees were not awarded, the plaintiff may not be obligated to pay any additional amount to his or her attorney.

Accordingly, some attorneys seem to assume that if a statute calls for attorney’s fees, the general rule of Banks can never apply. Arguably, though, more may be needed. If the contingent-fee agreement is plain vanilla, the fact that the fees can be awarded by statute may not be enough to distance the client from the fees. As the Banks decision notes, the relationship between lawyer and client is that of principal and agent. The fee agreement and the settlement agreement may need to address the payment of statutory fees.

Lawyer-Client Partnerships

A partnership of lawyer and client arguably should allow each partner to pay tax only on that partner’s share of the profits. The tax theory of a lawyer-client joint venture was around long before the Supreme Court decided Banks in 2005. Despite numerous amicus briefs, however, the Supreme Court expressly declined to address this long-discussed topic and whether it would sidestep the holding of Banks.

A mere fee agreement is surely not enough to suggest a partnership, but with appropriate documentation, one can argue that the lawyer contributes legal acumen and services, whereas the client contributes the legal claims. Lawyer purists will note the ethical rules that suggest this cannot be a true partnership because lawyers are generally not allowed to be partners with their clients. Yet, tax law is unique and sometimes at odds with other areas of law.

Could a lawyer-client partnership agreement provide that it is a partnership to the maximum extent permitted by law? Partnership nomenclature and formalities matter, and lawyer-client partnerships rarely seem to be attempted with conviction. A partnership tax return with Forms K-1 to lawyer and client might be difficult for the IRS to ignore. So far, however, lawyer-client partnerships do not look terribly promising.[11]

Conclusion

Returning to our $1,000,000 recovery with $400,000 in fees, no plaintiff will think it is fair to pay taxes on $400,000 paid directly to his or her lawyer. Increase these numbers, and emotions may run higher still. In the old days, alternative minimum tax and phased-out deductions often limited the efficacy of legal-fee deductions. There was plenty of grousing about those rules, but it was relatively rare for them to result in truly catastrophic tax positions. Nevertheless, there were a few cases in which plaintiffs lost money after tax.[12] Today, entirely disallowed legal fee deductions are less likely to be easily endured. Some plaintiffs may aggressively plan or report around this unjust landmine. They may try to gerrymander their settlement agreements to avoid receiving gross income on their legal fees. If plaintiffs cannot credibly argue that they avoided the gross income, they may go to new lengths to try to deduct or offset the fees. The bigger the numbers and the higher the contingent-fee percentage, the more creative and assertive the plaintiff may be. Good luck out there!

[9]See Tax Cuts and Jobs Act, Pub. L. No. 115-97, § 13307 (2017); see also Robert W. Wood, Taxing Sexual Harassment Settlements and Legal Fees in a New Era, 158 Tax Notes 4, 545 (Jan. 22, 2018).

[10]See Alexander v. Comm’r, 72 F.3d 938 (1st Cir. 1995).

[11] Allum v. Comm’r, T.C. Memo 2005-117, aff’d, 231 F. App’x 550 (9th Cir. 2007), cert. denied, 128 S. Ct. 303 (2007).

[12]See Spina v. Forest Preserve District of Cook County, 207 F. Supp. 2d 764 (N.D. Ill. 2002), as reported in 2002 National Taxpayer Advocate Report to Congress, at 166; see also Adam Liptak, Tax Bill Exceeds Award to Officer in Sex Bias Case, N.Y. Times, Aug. 11, 2002, at 18.

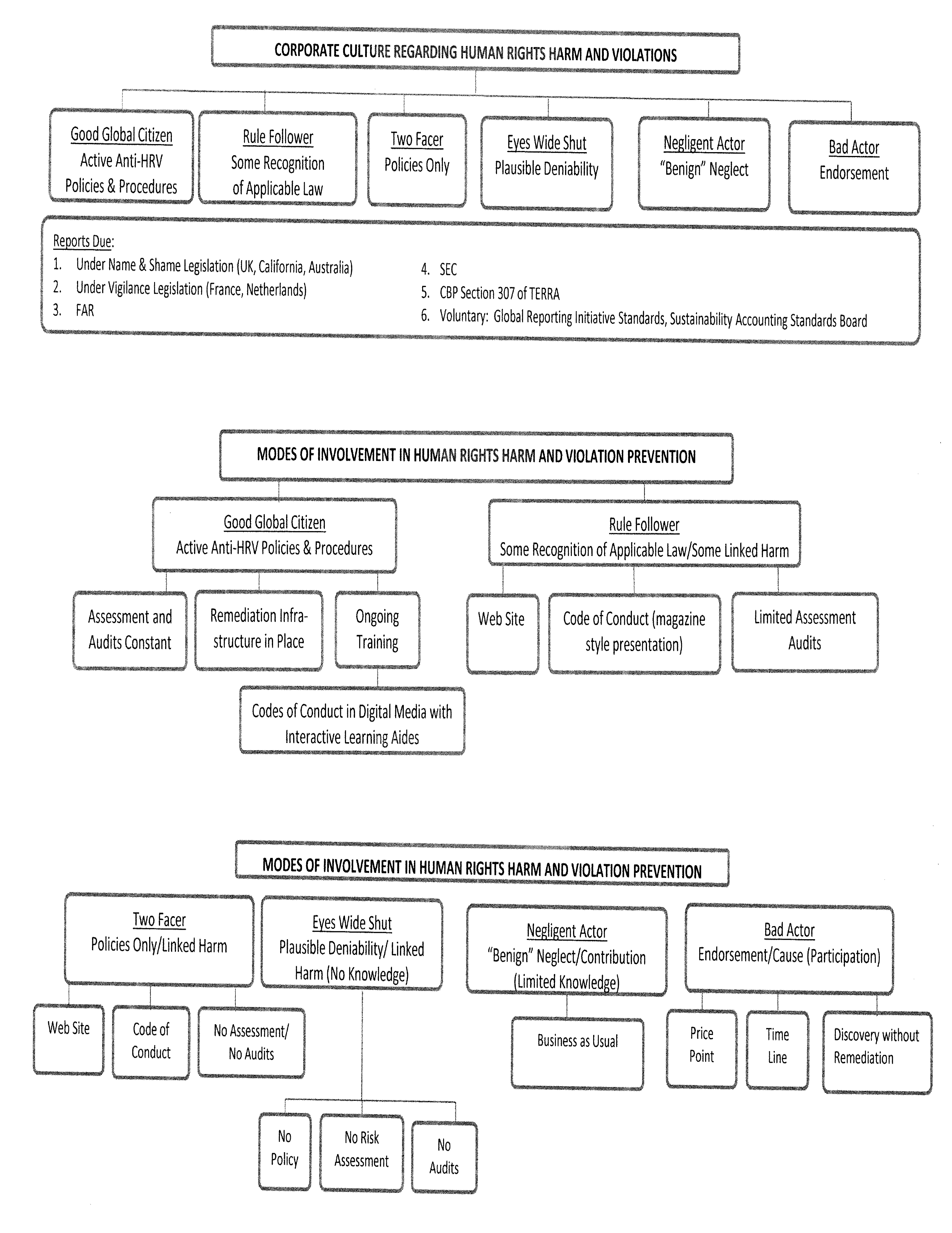

Most companies and the boards that govern them like to think their operations and supply chains are free of human rights abuses, yet of the 40 million estimated people enslaved worldwide, 16 million are working in forced labor within company operations and supply chains. Millions more work under dangerous and sometimes brutal conditions, toiling for up to 19 hours a day and subject to physical abuse at the hands of their supervisors. The eighth edition of the List of Goods Produced by Child Labor or Forced Labor and the 17th annual edition of the Findings on the Worst Forms of Child Labor published in September 2018 by the U. S. Department of Labor’s Bureau of International Labor Affairs (ILAB) highlight specific industry sectors in which child labor or forced labor persists. Abused workers can be found around the world, including within the United States. According to the human rights group Walk Free Foundation, an estimated 400,000 people are believed to be trapped in trafficking and modern slavery in the United States. If for no reason other than brand protection, there is a need for immediate proactive corporate initiatives in this context. To eradicate modern slavery, the C-suite must be encouraged by business lawyers to actively engage in supporting meaningful upstream and downstream change in identifying and remediating modern slavery.

The federal Trafficking Victims Protection Act of 2000 (TVPRA), 18 U.S.C. §1589(a)(4) (originally enacted as Victims of Trafficking and Violence Protection Act, Pub. L. No. 106-386, §112, 114 Stat. 1464, 1487 (2000)), defines labor trafficking as “the recruitment, harboring, transportation, provision, or obtaining of a person for labor or services, through the use of force, fraud, or coercion for the purpose of subjection to involuntary servitude, peonage, debt bondage, or slavery.” 22 U.S.C. §7101(9).

The reality is that publishing a policy or two on the company website does not accomplish anything to tackle modern slavery or other abuses of labor standards. The growing development of legislative and investor focus on human rights issues is pushing larger companies to report on what, if anything, they are doing to tackle these problems at every tier of their supply chain. The United Kingdom’s Home Office estimates between 9,000 to 11,000 companies are required to report under the UK Modern Slavery Act alone. The reporting requirements recognize that modern slavery cannot be addressed without direct, private-sector participation. The work necessary for coordination of the efforts of the company’s internal legal, compliance, and procurement departments, however, can be daunting. Corporate resistance and real challenges encountered in drafting human rights policies and contract provisions, including greater exposure to the risk of litigation, must be addressed.