Technology companies in the payments space should pay close attention to the Federal Reserve’s (the Fed’s) upcoming launch of a long-awaited new payment system, the FedNow Service. The system will change the consumer payments landscape by providing a new instant payment alternative to existing retail payment rails.

It is rare for the U.S. central bank to build a wholly new payment rail, and importantly, the federal government has also announced its backing for instant payment systems. The FedNow Service promises to both pose challenges to fintech companies whose business models depend on activity over existing payments rails and offer key new opportunities to innovators in the space. These new drivers and risks will be important considerations for many players in the market and critical to their success.

The Fed’s Instant Payments Platform

An instant payment is a new type of payment from one bank account to another, where the recipient receives final funds in near real time, enabled by immediate interbank settlement of the payment. This means there is no buildup in interbank obligations, and end users can instantly send and receive money. This is an improvement to payments via credit or debit cards and automated clearinghouse (ACH), which come with higher costs or delays to receiving final funds.

FedNow, expected to launch between May and July of this year, will be the central bank’s new core instant payment infrastructure. It will process retail payments in real time, twenty-four hours a day, 365 days a year, with funds made available immediately for use by the payment recipient. Eligibility to participate in the new system will generally be limited to U.S. banks; these banks, in turn, would offer instant payment services to individuals and businesses. The new system is a much-needed upgrade to the national infrastructure for retail payments, which is currently closed on weekends and can at times take several days before funds are available. The Fed’s ultimate aim is to give consumers and merchants faster access to their funds and greater flexibility to manage cash flow, at low cost and with reduced payment risk.

A key milestone was the Fed’s October 2022 publication of the legal terms and conditions governing FedNow transfers, which contain granular legal details about the service. These terms reveal important shifts to the status quo and critical ways the FedNow Service will impact the competitive outlook for retail payments, especially for fintech companies.

Challenges and Opportunities for Technology Companies

The Fed’s launch of FedNow this year is significant because it will enable banks of any size to offer convenient instant payments with nationwide reach. This will alter the retail payments landscape in three critical ways:

FedNow will challenge some major players in the payments industry: Instant payment systems like FedNow may ultimately prompt companies that depend on revenue from activity over existing payment rails, such as fintechs and partner banks that rely on credit or debit card interchange fees, to rethink their business models. It will similarly impact established nonbank providers of peer-to-peer payment services, such as dominant fintech companies that offer alias-based payment services (which allow senders to more conveniently make payments using only the email address or cell phone number of the recipient, without having to know their bank account information). Understanding the relative strengths and limitations of instant payments will be critical for both types of entities to adapt.

In addition, emerging digital asset payment rails, such as stablecoins and cryptocurrencies, may appear risky compared to payments over FedNow. To address this problem, it will be even more critical for companies offering these digital asset-based products to adopt robust legal foundations, risk-based measures to ensure regulatory compliance, and appropriate controls to manage operational risk.

FedNow will offer a fast, low-cost payment rail for digital platforms: The Fed’s legal terms and conditions for FedNow generally limit eligibility to banks, but e-commerce merchants and other digital marketplaces that have accounts with banks participating in FedNow can also take advantage as recipients of instant payments. If these merchants and marketplaces enable an instant payment option that a customer can select when purchasing goods or services online, they would have a significantly lower-cost alternative to traditional credit and debit card rails.

Digital wallet companies and payment platforms could similarly leverage instant payments via FedNow to improve customer offerings. Consumers and businesses will be able to immediately fund and defund wallet balances at low cost. For example, they can instantly move funds sitting in a digital wallet to an interest-bearing or wealth management account to more efficiently manage money, or immediately fund the wallet to make an in-store purchase without a card.

Likewise, electronic billing and pay vendors should take note that bill pay is among the core use cases the Fed has pitched for FedNow. Instant settlement of bill payments means that consumers and businesses can conveniently move money immediately from their own accounts to biller accounts, at any time.

Fintech companies will have a new central bank platform to provide innovative consumer and enterprise services: The Fed’s approach to designing and growing FedNow is new and envisions an efficient, open platform for technology companies to innovate and create ancillary services, end-user interfaces, and back-end processing support. A range of fintech companies and service providers (such as payment processors, mobile and online banking platform providers, payment hubs and gateways, and bill pay service providers) can take advantage of this early opportunity to contribute to the Fed ecosystem’s development.[1]

Why This Matters

Importantly, the U.S. Department of the Treasury has endorsed the adoption of instant payment systems in its recently issued report on “The Future of Money and Payments,” encouraging U.S. government agencies to use instant payment systems where appropriate. As history has shown with the growth of ACH payments, participation by U.S. government agencies in a payment system drastically amplifies that system’s ability to scale and reach ubiquity.[2] While it may take time for consumers and businesses to change deep-rooted payments behavior, the government’s support makes FedNow and instant payments well worth watching—not just for banks that are eligible for the service, but also payment processors, end-user interface providers, and other fintech companies.

Takeaways

There is a critical role for technology companies in the growing U.S. instant payments space: by rolling out the end-user interfaces needed to make instant payments convenient and safe, by offering the processing services that many banks rely on, or by integrating instant payments into platforms and products that drive the digital economy. Fintech companies that intend to take advantage of the faster movement of money through this new national payment rail will need a solid understanding of the service’s key features, the areas available to innovate and offer tailored functionality within the bounds of FedNow’s legal terms, and, importantly, the regulatory compliance obligations and their interplay with payments law, such as the Uniform Commercial Code.

The Fed itself has recognized the importance of the contributions of highly motivated and engaged technology companies and service providers in its outreach campaigns. Among other things, the Fed has created an Ecosystem Accelerator Group to promote engagement with these service providers and a Service Provider Showcase to connect service providers with FedNow banks. ↑

Indeed, Treasury notes in its report: “In settings where appropriate, U.S. government agencies should consider and support the use of instant payment systems. The U.S. government sends and receives millions of payments per day. Use of instant payment systems by U.S. government agencies could promote the expedient distribution of disaster, emergency or other government-to-consumer payments, potentially providing more rapid support for underserved communities.” ↑

The key challenge for regulating crypto assets is whether they can be classified as commodities or securities and, hence, whether the U.S. Securities and Exchange Commission (“SEC”) and/or the Commodity Futures Trading Commission (“CFTC”) has oversight. The collapse of FTX has highlighted the need to set clear guidelines on how the CFTC and SEC should divide the regulation of crypto assets.[1] Following the collapse of FTX, the CFTC’s chairman, Rostin Behnam, said that the CFTC had limited authority for enforcement action because it lacks direct oversight.[2] He stated the “CFTC does not have direct statutory authority to comprehensively regulate cash digital commodity markets.”[3] Behnam asked for “bills that contemplate shared responsibility for the CFTC and the SEC” so that “the SEC would utilize its existing authority and reporting regime requirements for all security tokens, while the CFTC would apply its market-based rules for the more limited subset of commodity tokens, which do not have the same characteristics as security tokens.”[4] Classification of crypto assets and subsequent regulation are important factors in the market. This article demonstrates that market participants’ classification of crypto assets as securities (or not) has been consistent with SEC and CFTC enforcement actions, with the notable exception of Ripple (“XRP”).

Ripple’s price movement following the SEC’s 2017 disclosure of the guidelines to identify crypto assets that are securities was in line with Bitcoin and Ethereum—crypto assets that the SEC has ruled are not securities.[5] Iconomi and other crypto assets with equity-like features experienced a more pronounced price decline than Ripple following the SEC’s guidelines disclosure. Despite arguments by industry participants that Ripple was “very unlikely” to be identified as a security by the SEC because “there is no expectation of profit (dividends or payouts) expected for Ripple holders,” the agency filed a lawsuit against Ripple in December 2020 for allegedly conducting an unregistered securities offering.[6] Ripple’s status as a commodity or security, and whether the SEC or industry players are correct about it, will soon be resolved as a court decision is expected soon.[7]

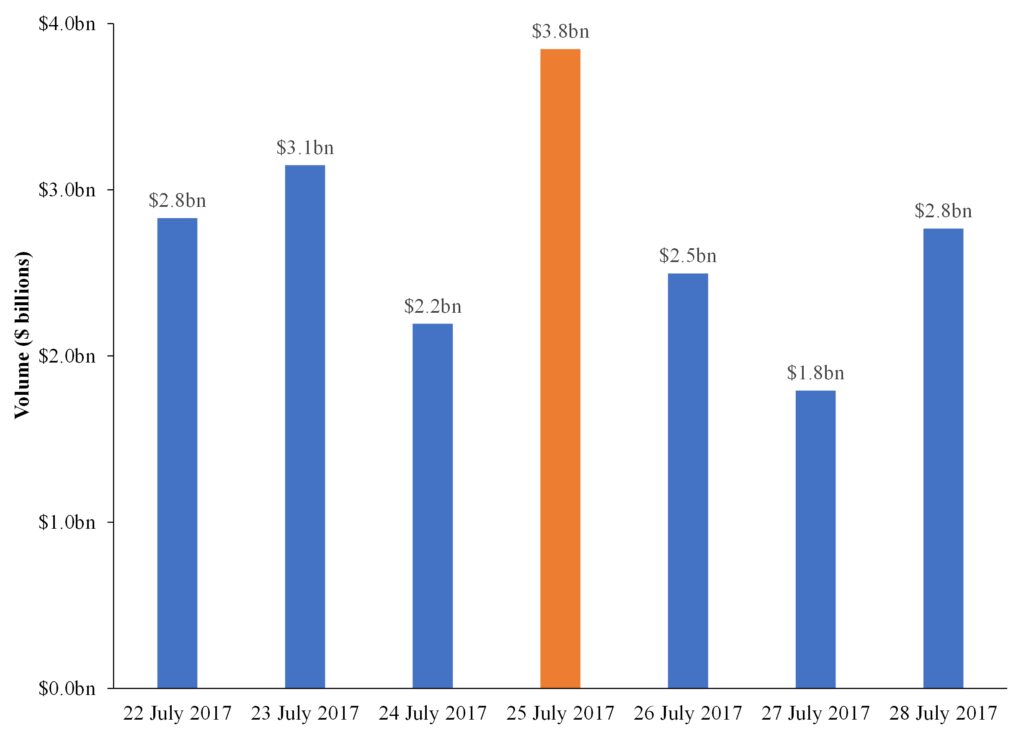

On July 25, 2017, the SEC issued an investigative report concluding that tokens sold by a decentralized autonomous organization that used blockchain technology were securities (“the DAO report”). The DAO report identified for the first time a crypto asset as a security and outlined the factors the agency would consider in determining whether crypto assets are securities. In the DAO report, the SEC stated that a key feature of a security is being an investment of money in which the investor has an expectation of profits based on the efforts of others regardless of whether the securities “are distributed in certificated form or through distributed ledger technology.”[8] The release of the DAO report had a notable impact on the crypto market, which we examine in this article to compare the regulatory decisions to the views of market participants regarding the classification of the crypto assets. The figure below presents the volume of crypto assets trading in the days immediately before and after the DAO report was issued. Daily trading volume increased from $2.2 billion the day prior to the report disclosure to $3.8 billion the day that the report was released, about a 75% increase.

Volume of Crypto Trading Following the Release of the DAO Report

The impact of the DAO report on the prices of crypto asset differed in that some prices remained stable while others dropped by more than 20% in a single day. In the discussion that follows, we demonstrate that the price of crypto assets reacted to the DAO report in a manner consistent with the market’s views about the type of crypto asset at issue. That is, the prices of certain crypto assets dropped notably for tokens that were viewed by market participants as likely to be securities, while the reaction of other assets was less noticeable or completely absent.

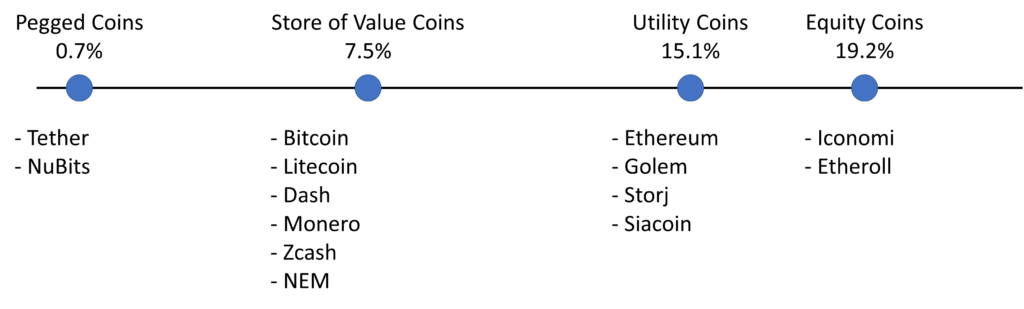

In analyzing market views regarding the classification of the crypto assets, we relied on two articles by Steemit, among other sources. The 2017 Steemit article “Is Your Crypto Digital Gold, Gas, or Something Else?” classified several crypto assets into four categories: pegged coins, store of value coins, utility coins, and equity coins.[9] We examined the crypto assets considered in the Steemit article and their classification to examine the price reaction to the DAO report on various crypto assets. The prices for crypto assets identified as pegged coins remained stable. Pegged coins are crypto assets that aim to peg their market value to some other assets, including the US dollar or the price of gold.[10] The prices for crypto assets identified as equity coins declined by about 20% following the DAO report. Equity coins are crypto assets that grant ownership rights to the token holders from profits generated by a project or product.[11] Iconomi is an example of a crypto asset identified as an equity coin, based on its white paper, which asserts that “ICN tokens represent ownership of the ICONOMI platform, allowing their holders to receive dividends and vote on ICONOMI related issues.”[12] Price declines for crypto assets that are considered to be store of value or utility tokens were not as pronounced. The purpose of store of value coins is to serve as a medium for transactions.[13] Utility coins are meant to offer additional network utility by providing access to resources to build block-chain-based applications or to execute smart contracts or provide access to remote computing power.[14]

The figure below presents the average price decline on the date that the DAO report was released across all crypto assets which were classified in the Steemit article. It is unlikely that pegged coins and store of value coins would be classified as securities “given their strong currency-like characteristics,” and “it is equally apparent” that equity coins are securities.[15] The Steemit article stated that it is less clear whether utility coins are securities or not.[16] The price decline of the coins classified as utility coins following the DAO report is consistent with the market’s view on the classification of the crypto assets. The average price decline was only 0.7% for the pegged coins and 7.5% for store of value coins, but it was 15.1% for utility coins and 19.2% for equity coins.

Price Decline Following the Release of the DAO Report by Type of Crypto Asset as Classified by the Steemit Article

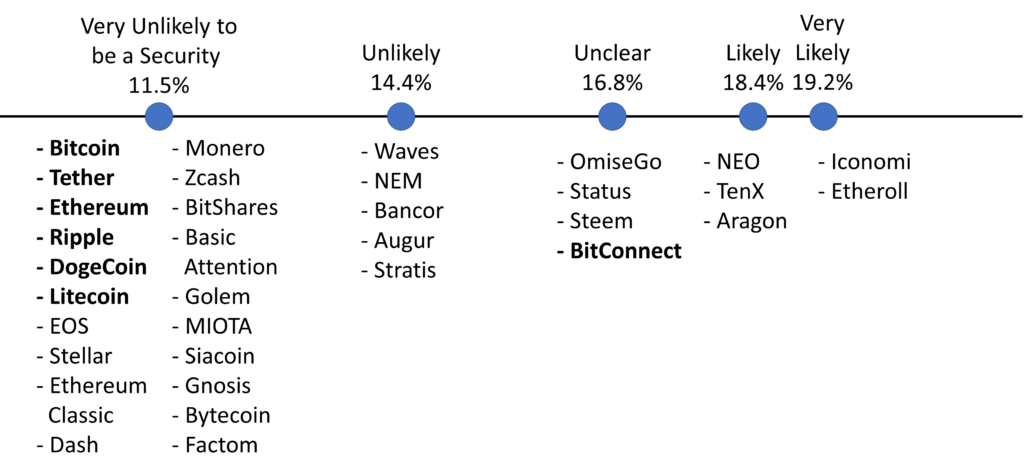

A second 2017 Steemit article, “Which Cryptocurrencies Will Be Regulated by the SEC/CFTC?” categorized a larger set of crypto assets as very unlikely, unlikely, unclear, likely, and very likely to be classified as securities per the SEC.[17] The figure below presents the average price decline on the date that the DAO report was released across all rating categories established in the second Steemit article. The price decline following the DAO report is again consistent with the market’s view on the likelihood of crypto assets being classified as securities by the SEC. The price decline was 11.5% for crypto assets classified as very unlikely to be deemed securities, 14.4% for unlikely, 16.8% for unclear, 18.4% for likely, and 19.2% for very likely.

Differences in Price Decline Following the Release of the DAO Report as Classified by the Steemit Article

The figure above lists the crypto assets under each rating category as identified in the second Steemit article. We identify in bold the subset of crypto assets that were later included in an enforcement action by the CFTC or the SEC. Bitcoin, Tether, Ethereum, DogeCoin, and Litecoin were included in enforcement actions by the CFTC, which oversees commodities and derivatives. Each had been classified by the Steemit article as very unlikely to be deemed securities.

Ripple and BitConnect were included in enforcement actions by the SEC, which oversees securities.[18] While BitConnect was given an unclear rating by the second Steemit article, Ripple received a very unlikely chance of being classified as a security by the SEC. Regarding BitConnect, the Steemit article stated:

It’s somewhat difficult to find information on how this coin works. We have not been able to find a white paper describing it. We suspect it would be considered a security as its purpose is to earn interest by paying it back to BCC developers, but it is very unclear.[19]

Regarding Ripple, the Steemit article said, “At this time there is no expectation of profit (dividends or payouts) expected for Ripple holders. It is used as a value holder for transactions in the Ripple ecosystem.”[20]

Conclusion

Since the DAO report release, the CFTC and SEC have conducted numerous enforcement actions. The agencies’ decisions on whether particular crypto assets were securities have been generally consistent with the market price reaction of the crypto assets following the DAO report with the notable exception of Ripple. Following the DAO decision, the market classified Ripple as “very unlikely” to be considered a security, and its price movement was in line with other crypto assets that were not considered securities using the same market classification, including Bitcoin and Ethereum.[21] Nevertheless, on December 22, 2020, the SEC charged Ripple with conducting a $1.3 billion unregistered securities offering. [22] The SEC argued there was no significant use for Ripple other than as an investment. The agency argued that the first potential use Ripple claimed for the token—to serve as a universal digital asset for banks to transfer money—never materialized. The SEC further argued that to date, the only product that permits Ripple use for any purpose is on-demand liquidity (“ODL”). ODL allows for cross-border payments to be settled in seconds, not days.[23] The SEC claimed, however, that ODL has gained little traction and that “ODL transactions comprised no more than 1.6% of XRP’s trading volume during any one quarter.”[24] The SEC has repeatedly clarified that “merely calling a token a ‘utility’ token or structuring it to provide some utility does not prevent the token from being a security.”[25] Both Ripple and the SEC submitted reply briefs in the ongoing lawsuit on December 2, 2022, and a court decision nears regarding whether Ripple can avoid the lawsuit.[26]

As more information is disclosed about the various crypto assets, one can examine the price reaction to regulatory and litigation rulings to evaluate the likelihood that assets will be classified as securities, as reflected by the views of market participants.

The authors are with NERA Economic Consulting. The views in this article represent those of the authors and not NERA. Please do not cite without permission from the authors.

Why Congress Needs to Act: Lessons Learned from the FTX Collapse:Hearing Before the S. Comm. on Agric., Nutrition, & Forestry 117th Cong. (Dec. 1, 2022) (testimony of Rostin Behnam, Chairman, Commodity Futures Trading Comm’n). ↑

The Ripple price dropped by 8.7% following the DAO report, similar to the 7% decline for Bitcoin and the 9.7% decline for Ethereum and less pronounced than the 23.2% price decline for Iconomi. While Iconomi was deemed an equity coin by the Steemit article, Bitcoin was categorized as a store of value coin, and Ethereum was identified as a utility coin that also has store of value coin features. ↑

The Roles of the SEC and CFTC: Hearing Before the S. Committee on Banking, Hous., & Urb. Affs. 115th Cong. (Feb. 6, 2018) (testimony of Jay Clayton, Chairman, Sec. & Exch. Comm’n). ↑

This article is the first in a new series from the American Bar Association Business Law Section’s Rule of Law Working Group, exploring the intersections between business and the rule of law from a client perspective and discussing how attorneys can support businesses’ rule of law missions. The Business and the Rule of Law Client Diaries Series is looking for more businesses to feature. Readers working for businesses interested in the rule of law are welcome to get in touch.

1. Tell us about your company: Who are your founders? What is their vision for the company and, perhaps, the company’s vision for the world?

Jussi Vento, Volument Co-Founder and CMO: Volument is an insight-led, privacy-friendly web analytics tool designed to help anyone create more engaging content and curate better online experiences. We want to transform web analytics and make it accessible to everyone, not just experts.

Volument was started to solve a very specific problem: the internet is suffering from privacy issues, clutter, and bad usability choices. (Usability is a measure of how well a specific user in a specific context can use a product or design to achieve a defined goal.) Web analytics tools are supposed to improve usability. Instead, a fairly untested obsession with personal identity has led to data analysts stockpiling personal data without any clear goal in mind—adding to online clutter and undermining online privacy. We want to hit the reset button on web analytics to make it work for, rather than against, the internet.

Volument is a Finnish company. The idea for Volument came to Tero Piirainen when he counted the number of different report views inside Google Analytics. He felt frustrated by the poor user interface, information overflow, and significant privacy concerns. After creating jQuery Tools and Riot.js and co-founding Flowplayer and Muut, Tero set out to build a web analytics tool he didn’t hate. Lauri Heiskanen joined him as the company’s backend guru and second founder. Tero and I connected around a shared frustration with the impact that web analytics was having on the overall health of the internet. Tina Nayak joined as our fourth founder and CEO, infusing her passion for user-centered business development into everything we do. The four founders share a frustration with products that put marketing before design, an interest in helping people at all levels within an organization understand users and their needs, and a commitment to leaving the marketplace (and the internet) a little better off than when we found it by disrupting practices that don’t serve businesses or consumers.

2. When does law come into your thinking or your plans? How do you rely on the law/the rule of law?

Volument aims to make legal compliance with privacy regulations simple for start-ups and for small and medium enterprises; we are innovating to help people and businesses comply with data protection regulations. So law and the rule of law are very important to the work that we do. Law plays a huge role in helping us advance our aims–as much as a product like ours works to enhance legal compliance.

3. What is your business’s engagement with the rule of law, sustainability, and/or important social issues?

We see ourselves as a mission-driven business. We like to think that we are building a better way to understand how people interact with websites and ultimately make the internet a better place. We don’t necessarily use big-ticket ideas to describe what we do, so we don’t talk about “rule of law,” “sustainability,” or “DEI” too often. At the same time, if you attend any of our meetings, you will see a diverse team that expresses a genuine passion for equity and inclusion. Equally, we might not list “upholding the rule of law” as an action item on meeting agendas—but certainly we talk a lot about how conventional web analytics tools are gaming the internet against small businesses and everyday people and how we can fix that.

The meat and potatoes of all of the big ideas listed in the question matter deeply to us. Creating a more inclusive, safe, diverse, and sustainable digital world drives all aspects of the work we do—from the design choices we make, to the people we hire, to the other companies we partner with.

Oddly, it’s not a given that we will necessarily look to lawyers to help us advance our mission or broader social aims. We enjoy working with lawyers who can make the connection between the causes that drive our work and more theoretical concepts. We rely on our lawyers to understand our mission and broader aims, so that they can help guide us through the legal aspects of making our vision a reality. It also helps when lawyers know how to speak a language that we care about, one that encourages us to seek them out when we want to advance important causes.

Often, lawyers might miss the connection between the values that drive us and broader concepts, like the rule of law or democracy. Those kinds of lawyers are more interested in talking to us about bare-bones compliance and what we can and cannot do. So whether or not we get lawyers involved really depends on the kinds of lawyers we are engaging with.

4. How do you engage with lawyers, and at what stage of innovation? What part of your vision do you share with lawyers?

Law comes in right away for us because of the compliance-driven aspects of our mission. But lawyers, not necessarily. Lawyers and the law can be intimidating. So sometimes getting lawyers involved too early in any process can feel like more trouble than it is worth. Lawyers can be challenging to engage with because they use a lot of legal jargon. They also tend to assume that entrepreneurs don’t understand the law, which can be frustrating.

Trust is very important for us when we engage with lawyers. We tend to engage with lawyers throughout the course of the development of our products and services—especially for a product like Volument that aims to support laws. But we don’t always get what we need from a single lawyer. We talk to scholars, experts, regulators, and practitioners to work to build our own understanding of the issues. And that’s what we are looking for most often, to build our own understanding.

When we find lawyers who can see the underlying potential that all laws have for improving the business environment, we hold on to them. Especially for a product like ours, we want to understand not just the “what” of the law, we also want to understand the “why” of the law. Why are data protection regulations framed the way they are? What is the law trying to improve here? How is the law trying to make business work better? How is the law trying to make society function better? Using a more practical example, we would be interested in knowing not just that the law requires cookie banners but why cookie banners are required at all. We have asked many lawyers that question. To be honest, the quality of the answers varied—and even regulators gave us answers that were either plainly wrong or largely unsatisfying. Only a few lawyers were able to have a conceptual conversation with us about why a law exists and how it functions.

5. What advice would you give business lawyers on the best ways to partner with you to advance the causes you care about?

It’s always great if a lawyer understands the market. This feels like it should be non-negotiable, but it’s not something we find that we can take for granted. So for one, understand the market, and not just the Market with a capital “M” or general market conditions, but the ins and outs of the specific niche we are competing in—what is the product, who are our competitors, what will the market look like five or ten years from now.

Second, try to understand what it is that a business cares about, beyond the jargon of both law and business. It is important for lawyers to understand that entrepreneurs don’t necessarily chase profit. We think it’s more accurate to say that entrepreneurs chase dreams, and these dreams might have the potential to turn a profit—but the dreams themselves are rarely about profit. Profit is a currency; it’s a flex that innovators can use to communicate value. We can take our profit margins to capital markets to tell bankers and investors: look, we are doing something; something is happening. Help us. But it would be dangerous to imagine that profit is something that innovators use to describe their goals or measure the effectiveness of their products.

From an entrepreneur’s perspective, profit flows naturally from value. If you can think of a way to make something, anything, better than it was before, people will probably pay you for it. So it’s the people who are obsessed with tinkering and improving things who build profitable companies. It’s that drive to add value, to make things better, that really drives success.

We would advise lawyers to share in that drive to make things better, advise us from that drive, and keep that underlying drive in mind at all times. This might help them more easily connect important concepts that drive the law to the practical tasks of running a business day-to-day.

6. Any last comments?

Volument is beta-testing our web analytics tools. We are gradually inviting people to try our platform. If you’re interested to find out how Volument works you can sign up for early access on our website, or just reach out to me on LinkedIn (Jussi’s LinkedIn Profile) or email us at [email protected]. A single web analytics tool cannot ensure full legal compliance, especially when used alongside more conventional products and services. But Volument can help ensure that web analytics isn’t what holds back compliance.

A new Iowa Business Corporation Act was enacted last year. Like Iowa’s current corporation statute (the “Act”), the legislation (HF 844) is based on the Model Business Corporation Act (“MBCA”) developed by the Corporate Laws Committee of the American Bar Association.

The MBCA is the basis for the corporation statutes in the majority of states. Various updates to the MBCA have occurred from time to time, and Iowa has adopted amendments to the Iowa Business Corporation Act as a result.

In 2016, the ABA Corporate Laws Committee published a new edition of the MBCA. It is the first comprehensive revision since 1984 (which Iowa adopted in 1989). The 2016 edition is in part a restatement of the MBCA that includes all amendments made since the previous version, but it also makes stylistic and editorial changes that are clarifying and adds important and useful provisions based on developments in corporate law around the United States. The Corporate Laws Committee of the Business Law Section of The Iowa State Bar Association met over a three-year period to work on proposed legislation for Iowa that resulted in the new Act.

Highlights of the New Act

Remote-only meetings of shareholders

The new Act includes a provision allowing for remote-only shareholder meetings. The previous Act did not include such a provision. During the recent pandemic, Iowa business corporations had to rely on the governor’s emergency proclamations to conduct remote-only shareholder meetings. The new Act provides that unless the bylaws require a meeting of shareholders to be held at a place, the board of directors may determine that any meeting of the shareholders need not be held at a place and may instead be held solely by means of remote communication, provided that the corporation implements measures to: (1) verify that each person participating remotely as a shareholder is a shareholder; and (2) provide that shareholders have a reasonable opportunity to participate in the meeting, including an opportunity to communicate, and to read or hear the proceedings substantially concurrently with such proceedings, and to vote on matters.[1]

The new Act also amends other Iowa entity statutes, including Iowa’s nonprofit corporation statute, cooperative statutes, and insurance statutes, to allow for remote-only member or policyholder meetings.[2] The remote-only meeting provisions for the different types of entities (including business corporations) became effective upon enactment of the new Act.[3]

Ratification of defective corporate actions

From time to time, a corporation may determine that, due to a misjudgment or oversight, certain actions may have been invalid. This could occur where there was an over-issuance of shares beyond the amount authorized in the articles of incorporation or where a transaction is within the corporation’s power but there was a failure of authorization as a result of procedural misstep. The new Act includes a ratification process that allows corporations to validate defective actions retroactively while fully protecting shareholder rights.[4] The goal of these provisions is to protect the parties’ reasonable expectations as well as the shareholders’ rights and interests while securing compliance with Iowa’s corporate law. The ratification of defective corporate acts can be adjudicated by the courts as well as accomplished by the corporation itself. This process has proved to be extremely helpful to corporations in other states, including Delaware.

Director duties and liability/liability shield

Iowa’s current Act provides a description of the duties of directors, required standards of conduct, and standards of liability; these remain unchanged in the new Act.[5] The effect of such a liability shield was the focus of a recent Iowa Supreme Court decision (Meade v. Christie, 974 N.W.2d 770 (Iowa 2022)), which is discussed in Stanley Keller’s article on recent decisions relevant to the MBCA. In addition, the previous Act authorized a corporation to include in its articles a provision that limits or eliminates monetary liability for any actions or failures to act subject to limited exceptions.[6] The new Act retains these provisions and authorizes an additional liability shield. Under the new Act, a corporation may include a provision in the articles of incorporation that eliminates or limits any duty of a director to offer the corporation the right to a corporate or business opportunity before it can be pursued or taken by the director or other person.[7] This provision is consistent with developments in LLC law and reflects an increasingly contractual or enabling approach to business law. Such a provision might be useful, for instance, with regard to a private equity investor that desires to have a nominee on the board but conditions its investment on limitation or elimination of the corporate opportunity doctrine because of the uncertainty about its application on account of the investor’s investments in multiple enterprises and specific industries. This provision also may be helpful in the situation of a joint venture or closely held corporation where the participants want to be sure that the corporate opportunity doctrine would not apply to their activities outside of the joint venture.[8]

Officer’s duty to inform

Iowa Code section 490.842 continues to set forth the standards of conduct for officers, including the circumstances in which the persons on whom an officer may rely in discharging his or her duties. Under the new Act, the section is amended to require that an officer: (1) inform the superior officer to whom the officer reports, or the board of directors or the board committee to which the officer reports, of information about the affairs of the corporation known to the officer, within the scope of the officer’s functions, and known to the officer to be material to such superior officer, board, or committee; and (2) inform the officer’s superior officer, or another appropriate person within the corporation, or the board of directors, or a board committee, of any actual or probable material violation of law involving the corporation or material breach of duty to the corporation by an officer, employee, or agent of the corporation, that the officer believes has occurred or is likely to occur. A similar requirement is recognized in agency law[9] and already imposed on directors.[10]

Forum selection provision in bylaws

Under the new Act, a corporation is able to include in its bylaws a requirement that internal corporate claims be brought exclusively in a specified court or courts of Iowa or in any other chosen jurisdictions with which the corporation has a reasonable relationship.[11] Still, such a provision may not prohibit bringing internal corporate claims in courts in Iowa, nor may it require such claims to be determined by arbitration. The term “internal corporate claim” is defined broadly to mean any of the following: (1) any claim that is based on a violation of a duty under the laws of Iowa by a current or former director, officer, or shareholder in such capacity; (2) any derivative action brought on behalf of the corporation; (3) any action asserting a claim arising pursuant to any provision of the Act, the articles of incorporation, or bylaws; and (4) any action asserting a claim governed by the internal affairs doctrine that is not included above. A forum selection provision can be an effective way for corporations to reduce litigation costs and enable Iowa courts to interpret Iowa law in the first instance.

Judicial determination of corporate offices and review of elections and shareholder votes

Under the previous Act, there was no provision for judicial review of elections and shareholder votes and determination of corporate offices. Under a section added by the new Act, the Iowa District Court has authority to determine the following issues: (1) the results or validity of an election, appointment, removal, or resignation of a director or officer of the corporation; (2) the right of an individual to serve as a director or officer; (3) the result or validity of any vote by shareholders; (4) the right of a director to membership on a board committee; (5) the right of a person to nominate or an individual to be nominated for election or appointment as a director, and (6) other comparable rights under the corporation’s articles or bylaws.[12]

Domestication and conversion

The previous Act included provisions allowing for the conversion of a business corporation into another type of entity as well as the conversion of another entity into an Iowa business corporation. The new Act revises and relocates provisions authorizing conversion transactions, and it adds sections authorizing domestication, a procedure by which a foreign corporation can become an Iowa corporation or an Iowa corporation can change its jurisdiction of incorporation, assuming in each case the law of the other jurisdiction also authorizes the procedure.[13]

Medium-form mergers

The previous Act included provisions for merger of a business corporation with another corporation or eligible entity, subject to shareholder approval. It also included a provision allowing for a merger without a shareholder vote when the acquiring entity owns more than ninety percent of the outstanding shares of the entity to be acquired. The new Act adds a provision to permit a “two-step” merger without a shareholder vote following a tender offer if sufficient shares are owned after the tender offer—namely, those owned before and as a result of the tender—to have approved the merger (typically, approval by a majority of the outstanding shareholder votes entitled to be cast).[14]

Corporate records and reports

The previous Act provided rights to shareholders to inspect records. The new Act includes a comprehensive revision of the chapter on that subject to modernize shareholder access to information while protecting interests of the corporation. The organization of this chapter is improved and more comprehensive; importantly, the board can condition inspection upon agreement to confidentiality restrictions.[15]

Benefit corporations

The new Act includes provisions allowing for the incorporation of benefit corporations in Iowa as well as the election of existing Iowa business corporations to become benefit corporations.[16] Unlike an ordinary business corporation, which has been held to have shareholder primacy as a focus,[17] a benefit corporation provides an option to mandate the interests of other stakeholders that are “known to be affected by the business of the corporation” to be at the same level as shareholders.[18] The new Act contemplates pursuit “through the business of the corporation [of] the creation of a positive effect on society and the environment” as well as any other public purpose set forth in the articles of incorporation.[19] Important in the analysis is not just what the corporation does but how it conducts its business and operations.[20] The new Act includes provisions addressing the duties imposed on directors, required “benefit” reporting, and conditions for bringing any shareholder action.[21] With the new Act, Iowa joins the nearly forty jurisdictions that have enacted benefit corporation statutes.

Official Comment

An important benefit of the MBCA is the Official Comment that may be used by practitioners and courts in interpreting and applying in practice various provisions and requirements in the MBCA. The 2016 Revision of the MBCA includes a new set of updated Comments. The Official Comment for prior editions of the MBCA is now out-of-date.

Unique IBCA provisions remain in statute

The new Act tracks the 2016 MBCA but continues to be tailored to reflect Iowa’s experience and preferences. As a result, the new Act includes non-MBCA provisions. These include the community interest provision that allows directors to consider interests other than shareholders’ interests when evaluating a tender offer or proposed business combination,[22] the provision on business combinations with interested stockholders,[23] the foreign-trade zone corporation provision,[24] provisions on names and reinstatement following administrative dissolution,[25] and provisions on filing of biennial reports.[26]

Secretary of State business filings

In other states, including Delaware, the secretary of state’s office allows for pre-filing clearance review of documents as well as expedited filing services for a fee. These services are extremely beneficial to businesses of all types. Although not part of the MBCA, HF 844 includes provisions establishing these services with the Iowa Secretary of State’s office.

Conclusion

With the new Act, Iowa has a comprehensive and modernized statute that should enhance Iowa’s business climate and serve clients and their counsel well. In addition, by updating the Iowa Business Corporation Act, Iowa is able to continue to take advantage of a useful body of law that develops around the United States that will help increase the certainty and efficiency of corporate actions and corporate transactions.[27]

This article originally appeared in the Winter 2022 issue of The Model Business Corporation Act Newsletter, the newsletter of the ABA Business Law Section’s Corporate Laws Committee. Read the full issue and previous issues on the Corporate Laws Committee webpage. It was adapted there from an article that was first published in “The Iowa Lawyer” (August 2021) and is reprinted with permission from The Iowa State Bar Association.

The views expressed in this article are solely those of the author and not Nyemaster Goode, P.C. or its clients. No legal advice is being given in this article.

Iowa Code §490.709. All Iowa Code citations are to citations in the new Act which, with the exception of the remote-only meeting provisions, become effective January 1, 2022. ↑

The opioid epidemic that has gripped this country for decades has spurred more than 2,000 lawsuits and led to billions of dollars in damages. AmerisourceBergen Corporation (the “Company”), one of the “big three” wholesale pharmaceutical distributors, has paid over $6 billion in damages and incurred over $1 billion in legal fees in connection with its role in the crisis. In Lebanon County Employees’ Retirement Fund et al., v. Collis, et al., the Company’s stockholders sought to hold the Company’s directors and officers personally liable for those damages and fees. 2022 Del. Ch. LEXIS 358 (Del. Ch. Dec. 22, 2022).

The Defendants moved to dismiss the action, claiming that because the action was derivative the Plaintiffs were required, but failed, to satisfy the rigorous “demand futility” requirement of Court of Chancery Rule 23.1. Plaintiffs argued that demand was futile because each of the Defendants faced a substantial likelihood of liability. Id. at *40–49.

On December 22, 2022, Vice Chancellor Laster issued an opinion dismissing the action. While there is a plethora of cases addressing demand futility, the Court’s opinion in this case is notable because of the high-profile nature of the allegations, and the fact that the Court dismissed the case notwithstanding its finding that the allegations would ordinarily be sufficient to survive a motion to dismiss.

Plaintiffs’ first argument was that the Defendants breached their fiduciary duty of care by ignoring several red flags that demonstrated the Company was not in compliance with federal regulations that required pharmaceutical distributors to maintain effective controls against the diversion of opioids to improper channels (known as “Anti-Diversion Policies”). Id. at *3.

The Court considered each of the red flags (which included the Company’s receipt of subpoenas and information requests from the attorneys general of forty-one states and numerous United States Attorneys’ offices; internal audit reports that raised questions about the Company’s compliance structure; congressional investigations and conclusions that found the Company failed to meet its reporting obligations; and the Company’s involvement in [and settlement of] several lawsuits regarding its compliance practices) and concluded that they would ordinarily be sufficient to overcome a motion to dismiss. Id. at *40–49. In fact, the Court held that the allegations demonstrated that the Defendants “did not just see red flags; they were wrapped in them.” Id. at *48.

That holding, however, did not end the Court’s analysis. The Court then looked to the United States District Court for the Southern District of West Virginia’s decision in City of Huntington v. AmerisourceBergen Corp. (2022 U.S. Dist. LEXIS 117322 [S.D. WV, 2022]), which held that the Company’s Anti-Diversion Policies were appropriate. Based on that holding, the Court found that the Defendants did not face a substantial likelihood of liability because it was impossible to infer that the Company failed to comply with its anti-diversion obligations. Id. at *50–51.

Plaintiffs’ second argument was that the Defendants caused the Company to put profitability over its compliance obligations by: (i) revising its oversight policy to make it harder for a sale to be deemed suspicious, and providing less oversight to sales to smaller and more profitable pharmacies; and (ii) entering into agreements with a large pharmacy chain that was under investigation by the DEA. The Court again concluded that the allegations in the complaint were sufficient to overcome the motion, however; because the West Virginia Court determined that the Company’s Anti-Diversion Policies were adequate, and therefore did not violate the law, the Court could not infer that the Defendants faced a substantial threat of liability for their conduct. Id. at *56.

While Vice Chancellor Laster’s decision provides helpful recitations of law, perhaps the most important theme is one that has been echoed by the Delaware Chancery Court for years—that equity is not a plug-and-play concept, and the Court may be required to consider the larger picture.

Providing the correct debtor name on a financing statement is a critical part of the process of perfecting security interests under Article 9 of the Uniform Commercial Code (“UCC”). This article will review fundamental debtor name concepts and special debtor name concerns, and identify a number of traps for the unwary attorney.

The purpose of filing financing statements is to provide notice of the claimed security interests. The ability of a UCC financing statement to serve its notice function depends on whether an interested party can locate the record. This is where the debtor name becomes particularly important.

Filing office search systems are designed to retrieve UCC records by debtor name. These systems generally report only exact matches to the name searched after the filing office has applied its standard search logic. With the way these systems are designed to operate, any error, omission, or variation in the debtor name, no matter how small, can prevent a search of the correct debtor name from locating the record.

The UCC recognizes the importance of accurate debtor names in this process by providing specific rules for different types of debtors in UCC Section 9-503(a). The code also provides harsh consequences for the secured party when a financing statement does not comply with the debtor name rules. With one exception, a financing statement that fails to sufficiently provide the debtor name in accordance with Section 9-503(a) will render the financing statement seriously misleading and not effective under Section 9-506(b).

The exception occurs when a search of the filing office records on the correct name of the debtor, using the jurisdiction’s standard search logic, if any, would disclose the record. In such cases, the insufficient debtor name does not render the financing statement seriously misleading. Unfortunately, the search logic test provides little protection. The search logic used by most jurisdictions will only disregard minor variations in punctuation, ending noise words, a leading “the”, and spacing. Even these general search logic steps differ somewhat from state to state.

Debtor Names for Organizations and Series of Entities

With so much riding on correct debtor names, one might expect that those who file UCC records would strictly comply with the Section 9-503(a) name rules. Many filers do so, but such compliance can be a challenge. To arrive at the correct debtor name, the filer must often disregard distractions that could lead them astray. If the debtor is a registered organization, for example, the financing statement must provide the name stated to be the name of the organization in the public organic record. “Public organic record” is a defined term in Article 9 and generally refers to the formation documents that state the name of the entity. However, other public records, including tax returns, certificates of good standing, and other official sources, often contain multiple variations of an entity’s name. Unless the filer understands what constitutes the public organic record and resists the temptation offered by other potential name sources, there is a substantial risk of error.

Another challenge for filers is what name to provide on the financing statement for an increasingly popular type of debtor: the series of an entity. In recent years several states have enacted legislation that permits limited liability companies and other entities to create series. A series has no existence apart from the entity under which it was formed. However, a series can have its own members, assets, and liabilities. A series can also contract, sue or be sued, and have a liability shield from the obligations of other series or the parent company.

There continues to be uncertainty regarding what name to provide for the debtor when the security interest is granted by the series of an entity. Much depends on the particular state law under which the series was formed. Filers must take care to determine what debtor name could be correct for a series debtor and list that name or any potentially correct names as separate debtors on the financing statement.

Names for Individual Debtors

Since the 2010 Amendments to UCC Article 9 were enacted across the country, determining the correct name of an individual debtor has been easier. Generally, the financing statement must provide the name indicated on the debtor’s driver’s license or, if permitted by applicable state law, the non-driver’s identification card. Nevertheless, there are still plenty of traps for the unwary, such as how to extract an unusual name from the driver’s license or what to do if the debtor lacks the designated identification documents.

Final Thoughts

The foregoing discussion represents the greatest concerns for attorneys who file UCC records, but there are other types of debtors as well. The debtor name requirements when the collateral is held in a trust or administered by a decedent’s personal representative, for example, are not always intuitive, leading to a number of common errors. Likewise, filers often struggle when the debtor doesn’t have a name, such as with an unnamed, as might be the case with an unnamed general partnership or similar entity.

In summary, strict compliance with the UCC Article 9 debtor name rules is always important. Those who file UCC records should provide the name required by UCC Section 9-503(a) exactly as it appears on the designated source document, including matching the spelling, spacing, and punctuation. If there is any doubt as to what Section 9-503(a) requires for the correct name, the filer should provide one or more name variations to ensure that whatever a court later decides was correct is contained on the financing statement.

This article is based on a CLE program that took place during the ABA Business Law Section’s 2022 Hybrid Annual Meeting. To learn more about this topic, view the program as on-demand CLE, free for members.

A lawsuit filed by the U.S. Securities Exchange Commission (“SEC”) against Ripple Labs, Inc. (“Ripple Labs”), creator of the popular cryptocurrency token known as XRP, represents a turning point for the cryptocurrency and wider blockchain-technology industries in their relationship with regulators. As a significant part of the SEC’s cryptocurrency enforcement campaign, the agency’s case against Ripple could have substantial implications for the SEC’s authority over digital assets in general, with important impacts on U.S. blockchain network operations.

Absent clear legislative measures by Congress, the SEC has stepped into the regulatory void as the blockchain industry has roiled with a series of bankruptcies and controversies in recent months. In November, the prominent cryptocurrency exchange FTX filed for bankruptcy after reports suggested liquidity and solvency questions for the firm. Later in the month, crypto lender BlockFi—for which FTX was a substantial creditor—initiated its own bankruptcy proceedings, citing liquidity concerns stemming from the FTX matter. Amidst such crypto asset market mayhem, the SEC recently warned U.S. companies that they may have disclosure obligations regarding the impacts the crypto market downturn has had or may have had on their business.[1]

In SEC v. Ripple, the parties have now completed briefing on summary judgment in the case, which lies at the convergence of cryptocurrency, blockchain technology, and the scope of the SEC’s regulatory authority—namely, whether digital asset tokens, in a variety of market conditions and circumstances, can be considered “investment contracts” subject to federal securities laws. That dry, legalistic question lies at the heart of the SEC’s authority here: If so, such assets arguably fall under the SEC’s regulatory authority; if not, they do not. With closing briefs due before Christmas 2022, a resolution is expected sometime in the first quarter of 2023.

Without a federal law adequately addressing blockchain regulation, regulators and market participants have had to consult the history books to determine when a crypto asset may be a security. In the landmark case SEC v. W.J. Howey Co., 328 U.S. 293 (1946), the U.S. Supreme Court devised a test to determine when an investment contract is present in any contract, scheme, or transaction. Under the “Howey Test,” the following characteristics must be present for an investment contract to be evidenced: (1) an investment of money (2) in a common enterprise (3) with a reasonable expectation of profits (4) derived from the efforts of others. While subsequent case law has refined the Howey Test and its application, the essence remains the same.

Of course, the Ripple matter is not the SEC’s first attempt at regulating blockchain products, and one recent win for the agency—in SEC v. LBRY—could bolster its arguments on summary judgment. Still, the agency’s grasp on the blockchain industry is far from secure, as Congress continues to weigh legislation that could clarify the government’s approach to these products.

The three sections of this article examine these aspects of the Howey–digital asset issue in turn. In the first section of this article, we briefly discuss the facts and outcome of the SEC’s win against LBRY Inc. and how that ruling implicates the same issue in the SEC’s battle against Ripple. From there, we dive into SEC v. Ripple by outlining each side’s arguments with respect to the Howey test. Finally, we discuss the extent the whole issue could be annulled if Congress passes legislation clarifying the regulatory boundaries surrounding cryptocurrency and blockchain technologies, even after a ruling in Ripple.

SEC v. LBRY Inc.: A Potential Roadmap for the SEC

In November, the Howey–digital asset issue received attention in a now-resolved matter—SEC v. LBRY, Inc.

LBRY, Inc. runs a popular “open-source” and “community-driven” digital content marketplace (the “LBRY Network”) that offers a blockchain-based alternative to platforms such as YouTube, Spotify, and Instagram.[2] Part of the LBRY Network’s advertised appeal as an alternative content-creation platform was that content creators are never at risk for demonetization or de-platforming since the LBRY protocol is decentralized. Central to this scheme was the LBRY Credit or “LBC,” which was created as a means to incentivize network transaction validation (also known as “mining”).[3] The token could be spent on the LBRY Network to publish content, tip content creators, purchase paywalled content, or purchase advertisement boosts.[4]

In March 2021, the SEC brought an enforcement action in New Hampshire federal court alleging that LBRY Inc. had sold LBC to U.S. investors to fund LBRY’s business and build its product—a violation of the same federal securities registration requirements at issue in SEC v. Ripple.

LBRY Inc. had two responses. First, it argued that LBC functions as a digital currency that is an essential component of the LBRY Network, which was already fully developed and launched prior to any offer or sale of LBC. Second, LBRY Inc. asserted that the SEC’s attempt to treat LBC as a security violated its right to due process because the SEC did not give LBRY Inc. fair notice that its LBC offerings were subject to the securities laws.[5] To support its positions, LBRY Inc. indicated that the SEC’s prior enforcement actions focused only on digital assets offered in Initial Coin Offerings, or “ICOs,” and never against a fully developed product like the LBRY Network.

On November 7, 2022, Judge Peter Barbadoro of the U.S. District Court for the District of New Hampshire granted the SEC’s motion for summary judgment against LBRY Inc., holding that the company had offered and sold LBC as a security in violation of the registration provisions of the federal securities laws. The judge further noted that LBRY Inc. was in “no position” to claim that it lacked fair notice of the application of those laws, concluding that LBRY did not offer “any persuasive reading of Howey that would cause a reasonable issuer to conclude that only ICOs are subject to the registration requirement.”[6]

The ruling could have important implications for Ripple because it lends theoretical support to the SEC’s position, although the SEC v. LBRY Inc. ruling is limited to a single district court with fact-specific holdings. Consistent with LBRY Inc.’s arguments, the ruling in that case marked a departure for the SEC, as every prior enforcement action had focused on issuers of digital tokens who had conducted ICOs. Like LBC, the XRP tokens at issue in Ripple were not issued through an ICO.

Similarities also exist in the conduct of the LBRY and Ripple Labs executive teams. In a Reddit post, LBRY Inc. had stated that the company “reserved 10% of all LBRY Credits to fund continued development and provide profit for the founders. Since Credits only gain value as the use of the protocol grows, the company has an incentive to continue developing this open-source project.”[7] Judge Barbadoro’s summary judgment decision noted that because LBRY Inc. retained its own tokens, reasonable purchasers could understand that decision as a signal that “[the purchaser] too would profit from holding LBC as a result of LBRY’s assiduous efforts.” Furthermore, “by intertwining LBRY’s financial fate with the commercial success of LBC, LBRY made it obvious to its investors that it would work diligently to develop the [LBRY] Network so that LBC would increase in value.”[8]

Similarly, the SEC has asserted in its action against Ripple Labs that the company’s co-founder and current chair Christian Larsen and CEO Bradley Garlinghouse—both named defendants in the matter—structured and promoted XRP sales to finance the company’s business and “also effected personal unregistered sales of XRP totaling approximately $600 million.”[9]

While the SEC v. LBRY Inc. ruling is limited to a single district court, the SEC’s victory in Ripple may be a harbinger of a looming regulatory crackdown against the broader cryptocurrency industry that would be given the go-ahead if the SEC wins its case versus Ripple Labs. And the implications for market actors can, of course, be dramatic: In a Twitter thread posted weeks after the summary judgment decision, LBRY wrote, “LBRY Inc. will likely be dead in the near future…the company itself has been killed by legal and SEC debts…[although] the LBRY protocol and blockchain will continue.”[10]

Ripple’s Battle with the SEC

Ripple Labs is a software company that dubs itself the “leading provider of crypto-enabled solutions for businesses,” the strategy for which includes use of its own XRP blockchain and native cryptocurrency token under the same name to facilitate cross-border payments, cryptocurrency liquidity, and the implementation of central bank digital currencies.[11] Ripple first launched its XRP blockchain and native cryptocurrency token in June 2012. At one point, XRP was the third largest cryptocurrency in terms of market capitalization, although since then it has fallen to sixth, at around $17.6 billion as of January 4.[12]

In December 2020, the SEC filed a complaint in the Southern District of New York arguing that Ripple Labs, along with its Chairman and CEO, had violated Sections 5(a) and 5(c) of the Securities Act of 1933 by engaging in the unlawful offer and sale of securities.[13] In September 2022, both sides filed for summary judgment, asking the court to decide whether XRP qualifies as a security and thus needs to be regulated pursuant to the Securities Act.

The SEC’s complaint alleges that, beginning in 2013, Ripple Labs, Larsen, and Garlinghouse raised funds through the sale of XRP in an unregistered securities offering. The agency also alleges that Ripple Labs distributed billions of XRP in exchange for non-cash considerations, like labor and market-making services.[14]

The SEC posits that Ripple Labs’ offering and sale of XRP straightforwardly qualify as an investment contract under the Howey Test. While the SEC deems numerous features of Ripple’s offering significant, the primary features of the agency’s argument are as follows. The SEC argues that the first prong of the Howey Test is met because purchasers obtained XRP through cash and non-cash considerations (and so made an investment of money). The SEC argues that the second prong is met—that the investment is in a common enterprise—because Ripple Labs pooled funds obtained from purchases of XRP to fund and build its operation, which includes financing the development of XRP use cases. As to this factor, the SEC also cites the fact that XRP’s price rises and falls for all investors together equally. In effect, the SEC is attempting to establish the presence of vertical and horizontal commonality, which, in Howey case law, has been a manner to distinguish when a common enterprise is present. Vertical commonality is evinced either strictly by the fortunes of the investor being interwoven with and dependent upon the efforts and success of those seeking the investment or broadly by the success of an investor depending on a promoter’s expertise. Alternatively, horizontal commonality focuses on the relationship between investors in which their funds are pooled into a common enterprise.

In regards to the third and fourth prongs of the Howey Test, wherein investors are led to a reasonable expectation of profits derived from the efforts of others, the SEC contends that Ripple openly touted the token as an investment and took publicly advertised measures to ensure rising demand for XRP. According to the agency, Ripple Labs “gave specific details of the efforts it would undertake to find ‘uses’ for XRP, to attract others to the ‘ecosystem,’ to manage the supply of XRP, to get platforms to list XRP, and to develop uses for the ledger.”[15] Further, the SEC focuses on the fact that XRP lacked a notable use, beyond mere speculative investment, well past its 2013 launch date. Ripple Labs originally announced that XRP would be a “universal digital asset” that would allow banks to transfer money, a promise which never actualized. Yet only five years after XRP’s launch, in 2018, did XRP have a product that permitted its use, Ripple Labs’ own On-Demand Liquidity Product (“ODL”), which targeted “money transmitter” businesses rather than individuals as potential users. Between October 2018 and June 2020, only 15 money transmitters were signed up to use ODL, and ODL transactions never amounted to more than 1.6% of XRP’s quarterly trading volume.

Whereas LBRY Inc. challenged the SEC as to only part of the Howey Test—the matter of whether purchasers were led to a reasonable expectation of profits derived from the efforts of others—the Ripple Defendants challenge the SEC on all four prongs of the Test.

When it comes to the first prong, Ripple Labs, Larsen, and Garlinghouse (“Ripple Defendants”) contend that, in many cases, there was no investment of money because Ripple Labs gave away more than two billion XRP tokens to charities and various grant recipients. Further, the Ripple Defendants argue that the second prong is not met—that there is no common enterprise—because Ripple Labs is not engaged in a profit-seeking business venture of which, according to Howey, must be present for the second prong to be met.[16] The XRP Ledger, the Ripple Defendants point out, is decentralized and thus incapable of being controlled or managed by Ripple Labs. The Ripple Defendants also deny that horizontal and vertical commonality are present along similar lines (in addition to other circumstances), while also maintaining that vertical commonality is insufficient as a criterion for the second prong to be met even if established. The Ripple Defendants’ point regarding the company’s own control or lack thereof over the XRP Ledger dovetails well not only with the second prong but with the third and fourth: The decentralized nature of XRP, Defendants argue, prevents its purchasers from relying on Ripple Labs’ efforts for profit.

However, the Ripple Defendants’ main argument on the third and fourth prongs relies on the fact that Ripple Labs was never under any contractual obligation to promote XRP. In essence, Defendants claim that an investment contract cannot be present if there is no contract at all. Expanding on this point, the Ripple Defendants broadly argue that XRP lacks the “essential ingredients” of an investment contract, as interpreted by the courts since Howey, which the Ripple Defendants argue (1) involve an actual contract, (2) impose post-sale obligations on the promoter, and (3) entitle the purchaser to receive a profit, and that XRP lacks all of these characteristics.

In response, the SEC asserts that Defendants are relying on a “made up” test that ignores federal securities laws:

[T]hese common law contract terms are not required to satisfy Howey’s ‘expectation of profits’ inquiry. This part of the test is about expectations, not about commitments, a point supported by far more than just ‘out-of-circuit cases.’[17]

Could It All Be for Nothing?

In LBRY and the still-pending Ripple case, the SEC is attempting to clarify its authority over blockchain matters. But a federal proposal could eradicate the issue entirely in the near future. In June, Senators Kirsten Gillibrand (D-NY) and Cynthia Lummis (R-WY) introduced the Responsible Financial Innovation Act[18] (“RFIA”) in the Senate, which, among other things, aims to establish a comprehensive regulatory framework for digital assets in order to address the Howey–digital asset issue.[19]

The RFIA introduces a new category of digital assets called “ancillary assets” to the Securities Exchange Act that would encompass “investment contracts.” The new category would be treated as “commodities” under the Commodity Exchange Act (“CEA”), rather than securities, and thus be subject to the regulatory authority of the Commodity Futures Trading Commission, or CFTC. Title III of the RFIA defines an “ancillary asset” as:

an intangible, fungible asset that is offered, sold, or otherwise provided to a person in connection with the purchase and sale of a security through an arrangement or scheme that constitutes an investment contract, as that term is used in section 2(a)(1) of the Securities Act of 1933 (15 U.S.C. 77b(a)(1)).[20]

While unlikely to become law before the congressional session adjourns on January 3, 2023, the RFIA represents a potential yet long-anticipated legislative answer to problems created by regulatory gaps pertaining to the cryptocurrency and broader blockchain technology industries. And the bill—or another like it—could solidify the regulatory landscape in place of the SEC’s ad hoc approach thus far.

Securities and Exchange Commission Litigation Release No. 25573, “SEC Granted Summary Judgment Against New Hampshire Issuer of Crypto Asset Securities for Registration Violations.” SEC, November 7, 2022, available at: https://www.sec.gov/litigation/litreleases/2022/lr25573.htm. ↑

Securities and Exchange Commission Press Release 2020-338, “SEC Charges Ripple and Two Executives with Conducting $1.3 Billion Unregistered Securities Offering.” SEC, December 22, 2020, available at: https://www.sec.gov/news/press-release/2020-338. ↑

SEC v. Ripple Labs, Inc., et al. 1:20-cv-10832-AT-SN. Defendants’ Reply in Support of Motion for Summary Judgment. December 2, 2022, available at: https://fingfx.thomsonreuters.com/gfx/legaldocs/gkvlwgobopb/SECURITIES%20CRYPTO%20RIPPLE%20brief.pdf. See Howey; this claim is a reference to the following (emphasis added): “A common enterprise managed by respondents or third parties with adequate personnel and equipment is therefore essential if the investors are to achieve their paramount aim of a return on their investments. Their respective shares in this enterprise are evidenced by land sales contracts and warranty deeds, which serve as a convenient method of determining the investors’ allocable shares of the profits. The resulting transfer of rights in land is purely incidental. Thus all the elements of a profit-seeking business venture are present here. The investors provide the capital and share in the earnings and profits; the promoters manage, control and operate the enterprise. It follows that the arrangements whereby the investors’ interests are made manifest involve investment contracts, regardless of the legal terminology in which such contracts are clothed.” ↑

SEC v. Ripple, Inc., et al. SEC’s Reply Memorandum in Support of Motion for Summary Judgment, supra note 15. ↑

Attorney Kathleen McLeroy has been selected as the 2022 recipient of the American Bar Association (ABA) Business Law Section’s Jean Allard Glass Cutter Award. The award is presented to an exceptional woman business lawyer who has made significant contributions to the profession and the Business Law Section, achieved professional excellence in her field, and advanced opportunities for other women in the profession and Business Law Section.

Kathleen paved her own path to becoming an accomplished trial lawyer. She began her career as bank loan officer where she gained business expertise and insight into a banking client’s perspective. Today, as a shareholder at Carlton Fields, P.A., Kathleen represents commercial banks, mortgage holders, property owners, insurers, and real estate developers in disputes. She has extensive experience resolving disputes as a litigator, mediator, and arbitrator. In addition, she works with judgement holders to enforce and collect domestic and international judgements. Her business acumen and legal expertise supply her clients with astute legal advice to meet their business goals and needs. Kathleen earned her MBA at Louisiana State University and JD from Washington and Lee University School of Law.

Kathleen McLeroy, 2022 Jean Allard Glass Cutter Award Recipient.

According to Law360, women constitute only 23% of equity partners at law firms—Kathleen is one such equity partner. Her hard work representing her clients and pro bono clients alike exemplifies how she has overcome hurdles within the legal profession. Her path to becoming an equity partner was no simple feat as she dedicated thousands of billable and nonbillable hours in her profession; she continues be a pillar of representation for women at the equity partner level. Her peers agree that Kathleen is a committed leader.

Kathleen’s devotion to the legal field extends beyond her clients, as she represents individuals on pro bono matters ranging from landlord-tenant disputes to mortgage foreclosure actions. Kathleen spends countless hours improving access to justice for those who cannot afford legal representation. For example, she represented an elderly client faced with excessive fees that were unrelated to the relevant loan instruments. Kathleen spent countless hours reviewing documents and understanding every detail of the case before justice could be served to her pro bono client. She worked tirelessly for thirteen months to reinstate the client’s mortgage, as the client was the head of household for her daughter; her son, who has a disability; and two grandchildren. Kathleen’s advocacy plays a pivotal role in her career within her local community and extends throughout the United States. She champions the rights of her pro bono clients and associations.

When Kathleen was the president of the Bay Area Legal Services (BALS), she increased and diversified the organization’s funding, which led to improved technology and staff. Most notably, she ran a successful campaign to raise $500,000 for the BALS’s endowment. She has also chaired the ABA Business Law Section’s Pro Bono Committee, served on the ABA Commission on Interest on Lawyer’s Trust Accounts, and was a member of the inaugural board of directors for the Florida Justice Technology Center (FJTC). Her leadership in the area of IOLTA resulted in a Florida Supreme Court mandate—since emulated nationwide—requiring that IOLTA monies be used to fund civil legal services and be paid interest rates commensurate with those offered to non-IOLTA depositors.

While her accomplishments are evidenced by Kathleen’s numerous speaking engagements, published articles, and awards received, the arduous labor behind the scenes is not captured through the same lens. Kathleen received the Florida Bar Foundation’s 2016 Medal of Honor Award, which is the Foundation’s highest award. She has also been recognized as a Florida Super Lawyer by Super Lawyers Magazine from 2011 to 2022; been noted as one of the Best Lawyers in America, Bankruptcy and Creditor Debtor Rights/Insolvency and Reorganization Law, Commercial Litigation from 2019 to 2022; and received the William Reece Smith Jr. Public Service Award from Stetson University College of Law in 2017, to name only a few of her accolades. She has blazed a trail in her legal career as a litigator, mediator, and arbitrator and is the well-deserving 2022 recipient of the ABA Business Law Section’s Jean Allard Glass Cutter Award.

The Great Recession taught an important lesson: if economic pressures prevent your organization from buying new software, then be on the lookout for an audit of your existing software licenses. Software vendors have seized upon noncompliance issues as leverage in convincing reluctant customers to buy new products.

For the past fifteen years, we have advised clients on how to manage software audits, even litigating when necessary. Over time, we’ve seen audits become consistently more sophisticated—employing well-known consulting firms, elaborate and tricky reporting mechanisms, and vendor-friendly scripts or automated review processes.

In part one of this two-part article series, we delved into the steps of a software audit and tips for managing audits. Now, in part two, we will explore ways to improve your license agreements to limit audits or avoid them entirely.

Part Two – Contractual Strategies to Mitigate the Risk of Software Audits

By Andrew Geyer and Christina Edwards

Drafting the Scope of the License to Align with Your Anticipated Use

When preparing and negotiating your license agreements, it is critical that the license grant is comprehensive, accurate, and clear. This process must be supported by a business team with a thorough understanding of who will be using the licensed product, why the organization is procuring the licensed product, and what purpose it is intended to serve.

Intended Users