Much has been written about authenticity in the fields of business and leadership, but by comparison, not so much in the legal field. Yet, for all the reasons authenticity is discussed in those fields, it is equally central to the practice of law. It fosters relationships, encourages collaboration, builds trust, and differentiates you from others.

Research shows that when we cater to others and hide who we are, it is cognitively and emotionally draining, which can undermine performance. And when we don’t know the preferences and expectations of our audience, we are more anxious, which also can hurt performance.[1] When I started to think about how to bring authenticity to my practice, I thought of preparation for trial and, in particular, Federal Rule of Evidence 901—Authenticating or Identifying Evidence. The essence of the rule is in the first part: to authenticate an item of evidence, the proponent must produce evidence sufficient to support a finding that the item is what the proponent claims it is. What does that mean when it is applied to a person? At a basic level, I think of it as demonstrating that you are who you are. That’s not to say that “authenticity” should be an excuse to do only what is comfortable or to be completely unfiltered in any professional setting. Just as I would think through carefully what documents or testimony I would use or elicit to meet the standard under Rule 901, I also have to think through what personal qualities I have that would make me a better lawyer. Here, I identify four ways to bring authenticity to the practice of law.

Start with Being Self-Aware

Having a better understanding of yourself helps to create more relevant and motivating goals. If this were a trial, I would begin with a list of issues that need to be proven in order to prevail. Start making that list. What are the top five priorities for you professionally and personally? What are your personality traits? Keep in mind that we all have multiple versions of ourselves that show up depending on the context. Just as knowing your case inside and out is an important step toward success for a client, knowing yourself is equally important. If you are concerned that you have blinders on, then solicit feedback from colleagues and family members as you would from mock jurors. Others’ perception of you is an equally important part of the picture.

Effective Vulnerability Can Build Trust

By being vulnerable at the right time in the right situation, you can build trust and strengthen connections. Once, during jury selection for a case pending in the federal court in Connecticut, I watched a trial attorney from Texas ask—in a thick “Texan” drawl—whether potential jurors would give his client a fair chance and not be biased against the trial team’s “Texas-ness.” His delivery of his difference and vulnerability was very effective in turning around a potential distraction.

Humans are hard-wired to read each other’s expressions. Research shows that observing someone who is injured will trigger the brain’s “pain matrix.”[2] Similarly, observing someone who is suppressing their feelings triggers physiological reaction in the observer.[3] Research also shows that we are particularly sensitive to signs of trustworthiness.[4] Finding the right context and the right method of delivery is not easy, but accepting the idea that vulnerability leads to trust and being curious about what context and method of delivery may be effective is a good first step.

Identify Values for Your Team

Throughout a trial, key pieces of evidence need to be made clear to the jury. Those key pieces of evidence are based on a thorough understanding of the facts and the law. The same applies to identifying and communicating core values to a team. Having a diverse team means thoughtfully addressing the challenges of working with people of different backgrounds. In fact, a study using fMRI to observe adults randomly assigned to two groups, one “leopards” and the other “tigers,” showed that even randomly assigned groups displayed in-group biases.[5] If we are hardwired to pick up on differences, then shared values can act as a unifying thread that anchors a team toward a common goal.

Practice Active Listening

During trial, it is important to listen carefully to testimony. On cross-examination, the testimony may not be the same as the testimony obtained in a deposition, so unexpected answers may be potential areas for impeachment or further exploration. And on direct examination, the testimony may not be the same as you had prepared the witness to deliver, so unexpected answers may need to be remedied. Outside of trial, active listening is equally important but often difficult to do. Most people fall into four listening styles: (1) the analytical listener who aims to analyze a problem from a neutral starting point; (2) the relational listener who aims to build connection and understand the emotions underlying a message; (3) the critical listener who aims to judge the content of the conversation and reliability of the speaker; and (4) the task-focused listener who shapes a conversation towards efficient transfer of important information.[6] Each style is effective, and developing the ability to shift between different styles can help improve listening and achieve conversational goals.

Properly authenticating documents during trial is a learned process that pays off in better results the more you practice. The same can be said for practicing authenticity in work and in life.

Gino, Francesca, Research: It Pays to Be Yourself, Harvard Business Review, Feb. 13, 2020. ↑

Lamm C, Nusbaum HC, Meltzoff AN, Decety J (2007) What Are You Feeling? Using Functional Magnetic Resonance Imaging to Assess the Modulation of Sensory and Affective Responses during Empathy for Pain. PLOS ONE 2(12): e1292. https://doi.org/10.1371/journal.pone.0001292. ↑

Dirks, KT, and Ferrin, DL (2002) Trust in leadership: Meta-analytic findings and implications for research and practice. Journal of Applied Psychology 87(4): 611–628. https://doi.org/10.1037/0021-9010.87.4.611. ↑

Public companies in a number of sectors have recently experienced a significant decline in their share prices. In addition, the conflict in Ukraine and macroeconomic factors continue to impact the economy. Nevertheless, the labor market remains tight, and companies are struggling to retain talent. This goal can be undermined when stock options awarded during better times are “underwater” and have therefore lost much of their incentive value. Pressure can quickly mount on boards and management to address this mismatch by “repricing” such underwater options.

This is not the first time that a large number of public companies have faced this challenge. The need to conduct repricings occurs during prolonged downturns or sector realignments. There were a total of 264 stock option repricings announced between 2004 and 2009.[1] This included high-profile companies, such as Alphabet (then Google), Intel, Starbucks, and Williams Sonoma.[2] Since that time, generally favorable market conditions have made repricings less common, with only a handful occurring each year. It is therefore of particular importance that companies facing this challenge understand the lessons and practices from earlier waves of repricings.

1. Structuring Repricings

1.1. One-for-One Exchanges

Option repricings were traditionally effected by the relatively simple mechanic of lowering the exercise price of underwater options to the then-prevailing market price of a company’s common stock. This was achieved either by amending the terms of the outstanding options or by canceling the outstanding options and issuing replacement options. The majority of repricings that occurred during the 2001 and 2002 market downturn were one-for-one option exchanges. At that time, the majority of new options had the same vesting schedule as the canceled options, and only a minority of companies excluded directors and officers from repricings.

Two developments have made one-for-one option exchanges and inclusion of directors and officers the exception rather than the norm:

In 2003, the New York Stock Exchange (“NYSE”) and the Nasdaq Stock Market (“Nasdaq”) adopted a requirement that public companies seek shareholder approval of option repricings absent express permissive language in the relevant plan. As a result, a large number of companies faced the need to ask (often unhappy) shareholders to provide employees with a benefit that the shareholders themselves would not enjoy. Since that time, the influence exerted by proxy advisors—ISS and Glass Lewis in particular—and large institutional shareholders on the outcome of repricing votes has made it difficult for companies to receive shareholder approval of one-for-one option exchanges due to the perceived unfairness to shareholders.

Stock option grants were not accounted for as an expense on a company’s income statement until the adoption of Financial Accounting Standards Board Accounting Standards Codification Topic 718 (“ASC 718”) and its predecessor (Statement of Financial Accounting Standards No. 123(R)) in 2005. As a result, there was a limited accounting impact from a significant grant of replacement stock options if a company waited six months and one day from the prior grant, giving stock options a distinct advantage over other forms of equity compensation. ASC 718 now requires the expensing of employee stock options over the implied service term (the vesting period of the options). As a result, the accounting cost of a one-for-one option exchange can be very significant.

1.2. Value-for-Value Exchanges

Companies seeking to reprice their options now generally undertake a “value-for-value” exchange. A value-for-value exchange affords option holders the opportunity to cancel underwater options in exchange for an immediate re-grant of new options at a ratio of less than one-for-one with an exercise price equal to the market price of such shares.

Value-for-value exchanges are more acceptable to shareholders compared to one-for-one exchanges and are a prerequisite for proxy advisor support. A value-for-value exchange results in less dilution to public shareholders than a one-for-one exchange because it allows the reallocation of a smaller amount of equity to employees, which shareholders generally perceive as being fairer under the circumstances. In addition, the accounting implications of a value-for-value exchange are significantly more favorable than a one-for-one exchange. Under ASC 718, the accounting cost of new options (amortized over their vesting period) is the fair value of those grants less the current fair value of the canceled (underwater) options.

As a result, companies generally structure an option exchange so that the value of the new options for accounting purposes—based on Black-Scholes or another option pricing methodology—approximates or is less than the value of the canceled options, thereby making it “value-neutral.” If the fair value of the new options exceeds the fair value of the canceled options, that incremental value is recognized as an expense over the remaining service period of the option.

1.3. Use of Restricted Stock or RSUs

A common variation of the value-for-value exchange is the cancellation of all options and the grant of restricted stock or restricted stock units (“RSUs”) with the same or a lower economic value than the options canceled. Restricted stock is stock that is subject to a substantial risk of forfeiture at grant but vests upon the occurrence of continued employment. Restricted stock is nontransferable while it is forfeitable. RSUs are economically similar to restricted stock but involve the promise to issue the shares or an equivalent cash value at a time that is concurrent with or after vesting.

The US tax rules applicable to restricted stock are different from those applicable to RSUs. Although the taxation of restricted stock is generally postponed until the stock becomes vested (with the grantee treated as receiving ordinary income equal to the fair market value of the underlying stock on the vesting date), the grantee of restricted stock may elect to be taxed in the year of grant rather than waiting until vesting. If this election is made pursuant to Section 83(b) of the Internal Revenue Code (the “Code”), the grantee is treated as receiving ordinary income equal to the fair market value of the underlying stock on the date of the grant, rather than on the date of vesting. Future appreciation is taxed as capital gain (rather than as ordinary income) when the grantee disposes of the shares after vesting. There is no ability to make Section 83(b) elections with respect to the grant of RSUs, which are taxed upon delivery of the shares following vesting of the RSUs. Outside the United States, many companies grant RSUs to their non-US employees because RSUs generally permit deferral of taxation until delivery of the shares of stock underlying the RSU, whereas there may be different tax consequences for restricted stock in a non-US jurisdiction upon grant.

One benefit of both restricted stock and RSUs is that such awards ordinarily have no purchase or exercise price and provide immediate value to the grantee. Consequently, the exchange ratio will generally result in less dilution to existing stockholders than an option-for-option exchange. In addition, at a time when institutional investors and proxy advisors may advocate greater use of restricted stock and RSUs, usually with performance vesting conditions for executives, either alone or together with stock options and stock appreciation rights (“SARs”),[3] such an exchange can be part of a shift in the overall compensation policy of a company. Finally, because restricted stock and RSUs ordinarily have no exercise price, there is no risk that they will subsequently go underwater if there is a further drop in a company’s stock price. This is an important consideration in a volatile market.

Income which certain officers recognize from the new restricted stock and RSU grants will be subject to the annual deduction limit of Section 162(m) of the Code, to the extent applicable. Section 162(m), in general terms, limits to US $1 million per year the deductibility of compensation to a public corporation’s CEO, CFO, and the next top three highest-compensated officers who served at any time during the corporation’s taxable year, as well as employees who were subject to Section 162(m) in a tax year beginning after 2016.[4]

1.4. Repurchase of Underwater Options for Cash

Instead of an exchange, a company may simply repurchase underwater options from employees for an amount based on Black-Scholes or another option pricing methodology. The repurchase of underwater options generally involves a cash outlay by the company, the amount of which will vary based on the extent to which the shares are underwater and the extent to which such repurchase is limited to fully vested options. Such a repurchase would reduce the number of options outstanding as a percentage of the total number of common shares outstanding (referred to as the “overhang”), which is generally beneficial to a company’s capital structure. If a company repurchases its underwater options for cash rather than replacing them with other equity awards, the company will also need to consider how to provide future retention value to the employees.

1.5. Treatment of Directors and Officers

Due to the guidelines of proxy advisors and the expectations of institutional investors, it can be advisable to exclude directors and executive officers from repricings that require shareholder approval. Nevertheless, because directors and officers often hold a large number of options, excluding them can undermine the goals of the repricing, and may lead to executive retention and motivation issues. Due in part to these practical concerns, a majority of recent repricings have included directors and officers despite the risk of an adverse vote. As an alternative to exclusion, companies could permit directors and officers to participate on less favorable terms than other employees and could consider seeking separate shareholder approval for the participation of directors and officers to avoid jeopardizing the overall program. Where the method of repricing or the intention behind the implementation of a new program reflects a shift in the overall compensation policy of a company, such as the exchange of options for restricted stock or RSUs, proxy advisors and institutional investors are more likely to acquiesce in the inclusion of directors and executive officers.

1.6. Key Repricing Terms

The following are key items that a company conducting a repricing will need to consider:

Exchange Ratio. The exchange ratio for an option exchange represents the number of options that must be tendered in exchange for one new option or other security. This must be set appropriately to encourage employees to participate and to satisfy shareholders. In order for a repricing to be value-neutral, there will usually be a number of exchange ratios, each addressing a different range of option exercise prices.

Option Eligibility. The company must determine whether all underwater options, or only those that are significantly underwater and/or were granted before a certain date, are eligible to be exchanged. This will depend on shareholder perceptions and proxy advisor guidelines, as well as the volatility of the company’s stock and the company’s expectations of future increases in share price. In addition, if employees in countries other than the United States hold underwater options, the company will need to consult with its advisors to determine if there are any issues (e.g., adverse tax consequences to either the company or the employee) that would result if such employees were eligible to participate in the exchange, and it may elect to exclude employees in certain non-US countries.

New Vesting Periods. A company issuing new options in exchange for underwater options must determine whether to grant the new options based on a new vesting schedule, the old vesting schedule, or a schedule that provides some other vesting mechanic between these two alternatives. Practices in this regard are quite varied, although a new vesting schedule is most common in order to garner shareholder support.

2. Shareholder Approval

2.1. NYSE and Nasdaq Requirements

Under NYSE and Nasdaq rules, a company listed on the NYSE or Nasdaq must first obtain shareholder approval of material amendments to equity compensation plans, including a proposed repricing, unless the equity compensation plan under which the options in question were issued expressly permits the company to reprice outstanding options.[5] Nasdaq rules define a material amendment to include any change to an equity compensation plan to “permit a repricing (or decrease in exercise price) of outstanding options… [or] reduce the price at which shares or options to purchase shares may be offered.”[6] Similarly, NYSE rules state that “any repricing of options will be considered a material revision of a plan.”[7] Under NYSE rules, a plan that does not contain a provision specifically permitting the repricing of options will be considered to prohibit repricing.[8] Nasdaq requires companies to use “explicit terminology” to clearly illustrate the possibility of repricing.[9] Therefore, if a plan itself is silent as to repricing, any repricing of options under that plan will be deemed to be a material revision, requiring shareholder approval. In addition, under NYSE rules, any attempt to delete or limit a plan’s provision prohibiting the repricing of options requires shareholder approval.[10]

The NYSE and Nasdaq define a repricing as involving any of the following:[11]

lowering the strike price of an option after it is granted;

canceling an option at a time when its strike price exceeds the fair market value of the underlying stock in exchange for another option, restricted stock, or other equity, unless the cancellation and exchange occurs in connection with a merger, acquisition, spin-off, or other similar corporate transaction; or

any other action that is treated as a repricing under generally accepted accounting principles.

It should be noted that neither the NYSE nor Nasdaq rules prohibit the straight repurchase of options for cash. Nasdaq has provided an interpretation stating that the repurchase of outstanding options for cash by means of a tender offer does not require shareholder approval even if an equity compensation plan does not expressly permit such a repurchase.[12] In reaching this conclusion, Nasdaq noted that the consideration for the repurchase was not equity. As noted below, however, some proxy advisors still require shareholder approval for a cash repurchase program.

Shareholder approval of a repricing will likely be required for most domestic companies listed on the NYSE or Nasdaq since few companies’ equity incentive plans expressly permit a repricing. As discussed below, this is because the existence of such a provision, or a decision to conduct a repricing without shareholder approval, would result in proxy advisors recommending a vote against the compensation committee and possibly other board members. A discussion regarding the exception available to foreign private issuers is provided below.

2.2. Proxy Advisors and Institutional Investors

The leading proxy advisors, ISS and Glass Lewis, have taken a clear position on repricing provisions in equity compensation plans. The detailed voting guidelines on this topic published by ISS and by Glass Lewis have remained unchanged over the last several years. ISS uses an “equity plan scorecard” model that considers a range of positive and negative factors to evaluate equity incentive plan proposals.[13] Under this approach, ISS will recommend a case-by-case vote on equity plans “depending on a combination of certain plan features and equity grant practices.”[14] However, ISS guidelines indicate that certain overriding, or “egregious,” features trigger an outright negative recommendation on the plan. Specifically, it will recommend a vote against a proposal if “[t]he plan would permit the repricing or cash buyout of underwater options without shareholder approval (either by expressly permitting it—for NYSE and Nasdaq listed companies—or by not prohibiting it when the company has a history of repricing—for non-listed companies).”[15] ISS considers the following to constitute a repricing: (i) the amendment “of outstanding options or SARs to reduce the exercise price of such outstanding options or SARs”; (ii) the cancellation of “outstanding options or SARs in exchange for options or SARs with an exercise price that is less than the exercise price of the original options or SARs”; (iii) the cancellation of “underwater options in exchange for stock awards”; or (iv) “cash buyouts of underwater options.”[16]

Glass Lewis will consider the company’s past history of option repricings and express or implied rights to reprice when making its voting recommendations and will recommend a vote against all members of a company’s compensation committee if the company repriced options without shareholder approval within the past two years.[17] Against this background, most companies are likely to seek shareholder approval for a repricing even if it is not required under their equity compensation plans.

Glass Lewis states that it has great skepticism with respect to option repricings, indicating that a repricing or option exchange program may only be acceptable “if macroeconomic or industry trends, rather than specific company issues, cause a stock’s value to decline dramatically and the repricing is necessary to motivate and retain employees.”[18] In such a circumstance, Glass Lewis will support a repricing if:

officers and board members cannot participate in the program;

the exchange is value-neutral or value-creative to shareholders using very conservative assumptions;

the vesting requirements on exchanged or repriced options are extended beyond one year;

shares reserved for options that are reacquired in an option exchange will be permanently retired so as to prevent additional shareholder dilution in the future; and

management and the board make a cogent case for needing to motivate and retain existing employees, such as being in a competitive employment market.[19]

Similarly, ISS has previously stated that an option exchange “creates a gulf between the interests of shareholders and management, since shareholders cannot reprice their stock” and therefore it “should be the last resort for management to use as a tool to re-incentivize employees.”[20] According to ISS, only deeply underwater options should be eligible for an exchange program.[21] “Repricing underwater options after a recent precipitous drop in the company’s stock price demonstrates poor timing and warrants additional scrutiny.”[22] Therefore, as a general matter, the threshold “exercise price of surrendered options should be the 52-week high for the stock price.”[23] ISS cautions that this general rule should be considered along with other factors, such as “the timing of the request, whether the company has experienced a sustained stock price decline that is beyond management’s control,”[24] and whether “[g]rant dates of surrendered options [are] far enough back (two to three years) so as not to suggest that repricings are being done to take advantage of short-term” declines in the company’s current stock price.[25]

2.3. Treatment of Canceled Options

Upon the occurrence of a repricing, equity compensation plans generally provide for one of two alternatives: (1) the shares underlying repriced options are returned to the plan and used for future issuances; or (2) such shares are redeemed by the company and canceled so as to no longer be available for future grants. A company’s equity compensation plan should make clear which alternative it will use. In the case of an option repricing that results in the return of canceled shares to a company’s equity incentive plan, ISS considers the total cost of the equity plan and whether the issuer’s three-year average burn rate is acceptable in determining whether to recommend that shareholders approve the repricing.[26]

2.4. Proxy Solicitation Methodology

Companies seeking shareholder approval for a repricing face a number of hurdles, not the least of which would be the fact that shareholders suffered from the same decrease in share price that caused the options to become underwater. It should also be noted that brokers are prohibited from exercising discretionary voting power (i.e., voting without instructions from the beneficial owner of a security) with respect to implementation of, or a material revision to, an equity compensation plan.[27] Therefore, the need to convince shareholders of the merits of a repricing is magnified, as is the influence of proxy advisors and institutional shareholders.

The solicitation of proxies from shareholders by a domestic reporting company is governed by Section 14(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the rules thereunder. Item 10 of Schedule 14A contains the basic disclosure requirements for a proxy statement used by a domestic issuer to solicit approval of a repricing. Pursuant to these requirements and common practice, issuers generally include the following items of disclosure:

A description of the option exchange program, including a description of who is eligible to participate, the securities subject to the exchange offer, the exchange ratio, and the terms of the new securities.

A table disclosing the benefits or amounts, if determinable, that will be received by or allocated to (1) named executive officers, (2) all current executive officers as a group, (3) all current directors who are not executive officers as a group, and (4) all employees, including all current officers who are not executive officers, as a group.

A description of the reasons for undertaking the exchange program and any alternatives considered by the board.

The accounting treatment of the new securities to be granted, and the US federal income tax consequences.

It is important that companies ensure that their disclosure includes a clear rationale for the repricing to satisfy the disclosure requirements sought by proxy advisors and necessary to persuade shareholders to vote in favor of the repricing.[28]

Rule 14a-6 under the Exchange Act permits a company that is soliciting proxies solely for certain specified limited purposes in connection with its annual meeting (or a special meeting in lieu of an annual meeting) to file a definitive proxy statement with the Securities and Exchange Commission (the “SEC”) and commence its solicitation immediately. The alternative requirement would be to file a preliminary proxy statement first and wait ten days while the SEC determines whether it will review and comment on the proxy statement. A proxy statement containing a repricing proposal should be filed with the SEC in preliminary form and then in definitive form after ten days if there is no SEC review. This is because the purposes for which a proxy statement can be initially filed in definitive form are limited to the following solely in connection with an annual meeting: (1) the election of directors; (2) the election, approval, or ratification of accountants; (3) a security holder proposal included pursuant to Rule 14a-8; (4) the approval, ratification, or amendment of a “plan” (a “plan” is defined in Item 402(a)(6)(ii) of Regulation S-K as “any plan, contract, authorization or arrangement, whether or not set forth in any formal document, pursuant to which cash, securities, similar instruments, or any other property may be received”); (5) certain specific proposals related to investment companies and Troubled Asset Relief Program financial assistance recipients; and (6) an advisory vote on executive compensation, or for a vote on the frequency of the advisory vote on executive compensation. Repricing proposals could be viewed as seeking approval of an amendment to a company’s plan to permit the repricing and approval of the terms of the repricing itself. Nevertheless, the better interpretation is that approval of the terms of a particular repricing is separate from an amendment to the plan to permit repricing, since the repricing terms would generally still be submitted for shareholder approval due to proxy advisor requirements even if the plan permitted repricing. Accordingly, companies should initially file proxy statements for a repricing in preliminary form.

3. Tender Offer Rules

3.1. Application of the Tender Offer Rules

US tender offer rules are generally implicated when the holder of a security is required to make an investment decision with respect to the purchase, modification, or exchange of that security. One might question why a unilateral reduction in the exercise price of an option would implicate the tender offer rules since there is no investment decision involved by the option holder. Indeed, many equity incentive plans permit a unilateral reduction in the exercise price of outstanding options, subject to shareholder approval, without obtaining the consent of option holders on the basis that such a change is beneficial to them. In reality, however, the likelihood of a domestic company being able to conduct a repricing without implicating the tender offer rules is minimal for the reasons set forth below.

Because of the influence of proxy advisors and institutional shareholders, most option repricings involve a value-for-value exchange consisting of more than a mere reduction in exercise price. A value-for-value exchange requires a decision by option holders to accept fewer options or to exchange existing options for restricted stock or RSUs. This is an investment decision requiring the solicitation and consent of individual option holders.

A reduction in the exercise price of an incentive stock option (“ISO”) would be considered a “modification” akin to a new grant under applicable tax laws.[29] The new grant of an ISO restarts the holding periods required for beneficial tax treatment of shares purchased upon exercise of the ISO. The holding periods require that the stock purchased under an ISO be held for at least two years following the grant date and one year following the exercise date of the option. The resulting investment decision makes it difficult in practice to effect a repricing that includes ISOs without seeking the consent of ISO holders, since they must decide if the benefits of the repricing outweigh the burdens of the new holding periods.

The SEC staff has suggested that a limited option repricing/exchange with a small number of executive officers would not be a tender offer. In such an instance, the staff position is that an exchange offer to a small group is generally seen as equivalent to individually negotiated offers, and thus not a tender offer. Such an offer, in many respects, would be similar to a private placement. The SEC staff believes that the more sophisticated the option holders, the more the repricing/exchange looks like a series of negotiated transactions. However, the SEC staff has not provided guidance on a specific number of offerees, so this remains a facts-and-circumstances analysis based on both the number of participants and their positions and sophistication.[30]

Not all equity incentive plans involve issuing ISOs, and thus the attendant ISO-related complexities will not always apply. As a result, foreign private issuers and domestic companies that have not granted ISOs and are simply reducing the exercise price of outstanding options unilaterally may also be able to avoid the application of the US tender offer rules. Foreign private issuers are discussed in more detail below.

3.2. Requirements of the US Tender Offer Rules

The SEC views a repricing of options that requires the consent of the option holders as a “self-tender offer” by the issuer of the options. Self-tender offers by companies with a class of securities registered under the Exchange Act are governed by Rule 13e-4 thereunder, which contains a series of rules designed to protect the interests of the targets of the tender offer. While Rule 13e-4 applies only to public companies, Regulation 14E applies to all tender offers. Regulation 14E is a set of rules prohibiting certain practices in connection with tender offers and requiring, among other things, that a tender offer remain open for at least twenty business days.

In March 2001, the SEC issued an exemptive order providing relief from certain tender offer rules that the SEC considered onerous and unnecessary in the context of an option repricing.[31] Specifically, the SEC provided relief from complying with Rule 13e-4(f)(8)(i) (the “all holders” rule) and Rule 13e-4(f)(8)(ii) (the “best price” rule). As a result of this relief, issuers are permitted to reprice/exchange options for only certain selected employees. Among other things, this exception allows issuers to exclude directors and officers from repricings. Furthermore, issuers are not required to provide each option holder with the highest consideration provided to other option holders.[32]

3.3. Pre-commencement Offers

The tender offer rules regulate the communications that a company may make in connection with a tender offer. These rules apply to communications made before the launch of a tender offer and while it is pending. Pursuant to these rules, a company may publicly distribute information concerning a contemplated repricing before it formally launches the related tender offer, provided that the distributed information does not contain a transmittal form for tendering options or a statement of how such form may be obtained. Two common examples of company communications that fall within these rules are the proxy statement seeking shareholder approval for a repricing and communications between the company and its employees at the time that proxy statement is filed with the SEC. Each such communication is required to be filed with the SEC under cover of a Schedule TO with the appropriate box checked to indicate that the content of the filing includes pre-commencement written communications.

3.4. Tender Offer Documentation

An issuer conducting an option exchange will be required to prepare the following documents as exhibits to a Schedule TO Tender Offer Statement:

the offer to exchange, which is the document pursuant to which the offer is made to the company’s option holders and which must contain the information required to be included therein under the tender offer rules;

the letter of transmittal, which is used by the option holders to tender their securities in the tender offer; and

other ancillary documents, such as the forms of communication with option holders that the company intends to use and letters for use by option holders to withdraw a prior election to participate.

The offer to exchange is the primary disclosure document for the repricing offer and, in addition to the information required to be included by Schedule TO, focuses on informing security holders about the benefits and risks associated with the repricing offer. The offer to exchange is required to contain a “summary term sheet” that provides general information—often in the form of frequently asked questions—regarding the repricing offer, including its purpose, eligibility of participation, duration, and how to participate. It is also common practice for a company to include risk factors disclosing economic, tax, and other risks associated with the exchange offer. The most comprehensive section of the offer to exchange is the section describing the terms of the offer, including the purpose, background, material terms and conditions, eligibility to participate, duration, information on the stock or other applicable units, interest of directors and officers with respect to the applicable units or transaction, procedures for participation, tax consequences, legal matters, fees, and other information material to the decision of a security holder when determining whether or not to participate in such offer.

The offer to exchange, taken as a whole, should provide comprehensive information regarding the securities currently held and those being offered in the exchange—including the difference in the rights and potential values of each. The disclosure of the rights and value of the securities is often supplemented by a presentation of the market price of the underlying stock to which the options pertain, including historical price ranges and fluctuations, such as the quarterly highs and lows for the previous three years. The offer to exchange may also contain hypothetical scenarios showing the potential value risks/benefits of participating in the exchange offer. These hypothetical scenarios illustrate the approximate value of the securities held and those offered in the exchange at a certain point in the future, assuming a range of different prices for the underlying stock. If the repricing is part of an overall shift in a company’s compensation plan, the company should include a brief explanation of its new compensation policy.

3.5. Launch of the Repricing Offer

The offer to exchange is transmitted to employees after the Schedule TO has been filed with the SEC. While the offer is pending, the Schedule TO and all of the exhibits thereto (principally the offer to exchange) may be reviewed by the SEC staff, who may provide comments to the company, usually within five to seven days of the filing. The SEC’s comments must be addressed by the company to the satisfaction of the SEC, which usually requires the filing of an amendment to the Schedule TO, including amendments to the offer to exchange. Generally, no distribution of such amendment (or any amendments to the offer to exchange) will be required.[33] This review usually does not delay the tender offer and generally will not add to the period that it must remain open.

Under the tender offer rules, the tender offer must remain open for a minimum of twenty business days from the date that it is first published or disseminated. For the reasons noted below, most option repricing exchange offers are open for less than thirty calendar days. If the consideration offered or the percentage of securities sought is increased or decreased, the offer must remain open for at least ten business days from the date such increase or decrease is first published or disseminated. The SEC also takes the position that if certain material changes are made to the offer (e.g., the waiver of a condition), the tender offer must remain open for at least five business days thereafter.[34] At the conclusion of the exchange period, the repriced options, restricted stock or RSUs will be issued pursuant to the exemption from registration provided by Section 3(a)(9) of the Securities Act of 1933, as amended (the “Securities Act”) for the exchange of securities issued by the same issuer for no consideration.

3.6. Conclusion of the Repricing Offer

The company is required to file a final amendment to the Schedule TO setting forth the number of option holders who accepted the offer to exchange.

4. Certain Other Considerations

4.1. Tax Issues

Incentive Stock Options. If the repricing offer is open for thirty days or more with respect to options intended to qualify for ISO treatment under US tax laws, those ISOs are considered newly granted on the date the offer was made, whether or not the option holder accepts the offer.[35] If the period is for less than thirty days, then only ISO holders who accept the offer will be deemed to receive a new grant of ISOs.[36] As discussed above, the consequence of a new grant of ISOs is restarting the holding period required to obtain beneficial tax treatment for shares purchased upon exercise of the ISO.[37] As a result of these requirements, repricing offers involving ISO holders should generally be open for no more than thirty days.

To qualify for ISO treatment, the maximum fair market value of stock with respect to which ISOs granted to an employee may first become exercisable in any one year is US $100,000.[38] For purposes of applying this dollar limitation, all ISOs granted to the employee are taken into account; the stock is valued when the option is granted, and ISOs are taken into account in the order in which they were granted.[39] Whenever an ISO is canceled pursuant to a repricing, any options and shares scheduled to become first exercisable in the calendar year of the cancellation would continue to count against the US $100,000 limit for that year.[40] To the extent that the new ISO becomes exercisable in the same calendar year as the cancellation, the canceled options and shares (referenced in the immediately preceding sentence) reduce the number of shares that can receive ISO treatment (because the latest grants are the first to be disqualified).[41] Where the new ISO does not start vesting until the next calendar year, however, this will not be a concern.

Section 409A Compliance. If the repricing occurs with respect to nonqualified stock options (i.e., options that are not ISOs), such options need to be structured so as to be exempt from (or in compliance with) Section 409A of the Code. Section 409A comprehensively codifies the federal income taxation of nonqualified deferred compensation. Section 409A generally provides that unless a “nonqualified deferred compensation plan” complies with various rules regarding the timing of deferrals and distributions, all amounts deferred under the plan for the current year and all previous years become immediately taxable, and subject to a 20% penalty tax and additional interest, to the extent the compensation is not subject to a “substantial risk of forfeiture” and has not previously been included in gross income. Nonqualified stock options are usually structured to be exempt from Section 409A. One of the conditions for this exemption is that the option have an exercise price at least equal to the fair market value of the underlying stock on the option grant date. A reduction in the option exercise price that is not below the fair market of the underlying stock value on the date of the repricing should not cause the option to become subject to Section 409A. Instead, such repricing of an underwater option is treated as the award of a new stock option that is exempt from Section 409A.[42] While foreign private issuers may enjoy certain relief from the US tender offer rules as described below, there is no similar relief from US tax considerations for US taxpayers. This is most important where foreign private issuers’ home country rules allow for the grant of options with exercise prices below fair market value. In such case, care should be taken to ensure that grantees who are US taxpayers receive awards that comply with Section 409A.

4.2. Plan Grant Limitation

It should also be noted that a repriced option will count against any per-person grant limitations (typically an annual limit on the maximum number of shares which may be granted to an individual) in the applicable equity plan.

4.3. Accounting Treatment

Accounting considerations are a significant factor in structuring a repricing. Before the adoption of ASC 718 in 2005, companies often structured repricings with a six-month hiatus between the cancellation of underwater options and the grant of replacement options. The purpose of this structure was to avoid the impact of variable mark-to-market charges. Under ASC 718, however, the charge for the new options is not only fixed upfront but is for only the incremental value, if any, of the new options over the canceled options. As discussed above, in a value-for-value exchange, a fewer number of options or shares of restricted stock or RSUs will usually be granted in consideration for the surrendered options. As a result, the issuance of the new options or other securities can be a neutral event from an accounting expense perspective.

4.4. Section 16

The replacement of an outstanding option with a new option having a different exercise price and a different expiration date involves a disposition of the outstanding option and an acquisition of the replacement option, both of which are subject to reporting under Section 16(a). However, the disposition of the outstanding option will be exempt from short-swing profit liability under Section 16(b) pursuant to Rule 16b-3(e) if the terms of the exchange are approved in advance by the issuer’s board of directors, a committee of two or more nonemployee directors, or the issuer’s shareholders. It is generally not a problem to satisfy these requirements. Similarly, the grant of the replacement option or other securities is subject to reporting but will be exempt from short-swing profit liability pursuant to Rule 16b-3(d) if the grant was approved in advance by the board of directors or a committee composed solely of two or more nonemployee directors, or was approved in advance or ratified by the issuer’s shareholders no later than the date of the issuer’s next annual meeting, or is held for at least six months.

5. Foreign Private Issuers

5.1. Relief from Shareholder Approval Requirement

Both the NYSE[43] and Nasdaq[44] provide foreign private issuers with relief from the requirement of stockholder approval for a material revision to an equity compensation plan by allowing them instead to follow their applicable home-country practices. As a result, if the home-country practices of a foreign private issuer do not require shareholder approval for a repricing, the foreign private issuer is not required to seek shareholder approval under NYSE or Nasdaq rules.

Both the NYSE and Nasdaq require an issuer following its home-country practices to disclose in its annual report on Form 20-F an explanation of the significant ways in which its home-country practices differ from those applicable to a US domestic company.[45] Alternatively, companies listed on the NYSE may disclose such home-country practices on the issuer’s website, in which case the issuer must provide in its annual report the web address where the information can be obtained.[46] Under Nasdaq rules, the issuer is required to submit to Nasdaq a written statement from independent counsel in its home country certifying that the issuer’s practices are not prohibited by the home country’s laws.[47]

Many foreign private issuers disclose that they will follow their home-country practices with respect to a range of corporate governance matters, including the requirement of shareholder approval for the adoption or any material revision to an equity compensation plan. These companies are not subject to the requirement under NYSE or Nasdaq rules of obtaining shareholder approval for a repricing. Companies that have not provided such disclosure and wish to avoid the shareholder approval requirements when undertaking a repricing will need to consider carefully their historic disclosure and whether such an opt-out poses any risk of a claim from shareholders.

5.2. Relief from US Tender Offer Rules

Foreign private issuers also have significant relief from the application of US tender offer rules if US option holders hold 10% or less of the company’s outstanding options.[48] Under the exemption, assuming the issuer’s actions in the United States still constitute a tender offer, the issuer would be required to take the following steps:

file with the SEC under the cover of a Form CB a copy of the informational documents that it sends to its option holders. This informational document would be governed by the laws of the issuer’s home country and would generally consist of a letter to each option holder explaining why the repricing is taking place, the choices each option holder has, and the implications of each of the choices provided;

appoint an agent for service of process in the United States by filing a Form F-X with the SEC; and

provide each US option holder with terms that are at least as favorable as those terms offered to option holders in the issuer’s home country.

A more limited exemption to the US tender offer rules also exists for foreign private issuers where US investors hold 40% or less of the options that are subject to the repricing. Under this exception, both US and non-US security holders must receive identical consideration. The minimal relief is intended merely to minimize the conflicts between US tender offer rules and foreign regulatory requirements and provides little actual relief in the context of an option repricing.

6. Alternative Strategies

There have been surprisingly few deviations from the repricing approaches described above. In the past, Microsoft and Google used different and more innovative methods to address the issue of underwater employee stock options, thereby providing an alternative to a traditional repricing. To date, other companies have not followed suit, but it is possible that others will consider these approaches in the future.

In 2007, Google implemented a program that afforded its option holders (excluding directors and officers) the ability to transfer outstanding options to a financial institution through a competitive online bidding process managed by Morgan Stanley. The bidding process effectively created a secondary market in which employees can view what certain designated financial institutions and institutional investors are willing to pay for vested options. The value of the options is therefore a combination of their intrinsic value (i.e., any spread) at the time of sale plus the “time value” of the remaining period during which the options can be exercised (limited to a maximum of two years in the hands of the purchaser). As a result of this “combined” value, Google believed that underwater options would still retain some value. This belief is supported by the fact that in-the-money options were sold at a premium to their intrinsic value.

Google’s equity incentive plan was drafted sufficiently broadly to enable options to be transferable without the need for Google shareholder approval to amend the plan. Many other companies’ plans would likely limit transferability of options to family members. Accordingly, most companies seeking to implement a similar transferable option program will likely need to obtain shareholder approval to do so. Note that ISOs become nonqualified stock options if transferred. The only options Google granted following its IPO were nonqualified stock options and, accordingly, the issue of losing ISO status did not arise. Finally, notwithstanding the benefits that Google’s transferable option program offers, it did not prevent the company from effecting a one-for-one option exchange and incurring a related stock-based compensation expense of US $460 million over the life of the new options.

In 2003, Microsoft implemented a program that afforded employees holding underwater stock options a one-time opportunity to transfer their options to JPMorgan in exchange for cash.[49] The program was implemented at the same time that Microsoft started granting restricted stock instead of options, and it was open on a voluntary basis to all holders of vested and unvested options with an exercise price of US $33 or more (at the time of the implementation of the program, the company’s stock traded at US $26.50). Employees were given a one-month election period to participate in the program, and once an employee chose to participate, all of that employee’s eligible options were required to be tendered. Employees who transferred options were given a cash payment in installments, dependent upon their continued service with Microsoft.

The methods used by Google and Microsoft require consideration of tax and accounting implications and required the filing of a registration statement under the Securities Act in connection with short sales made by the purchasers of the options to hedge their exposure. To date, these methods have not been adopted by other companies, and it is to be expected that most companies will continue to conduct more conventional repricings to address underwater options.

7. Summary

The current market realignment has not yet continued for long enough to generally justify a significant number of repricings. Trends over the last decade have shown a tendency to avoid repricing when possible. Continued examples of market resilience and feasibility of alternative compensation practices have subsided the widespread occurrence of repricings. Nevertheless, while underwater option repricings may not rise to the levels following the financial crisis of 2008, companies will likely always require the ability to reprice underwater options upon certain market fluctuation or individual corporate circumstances, especially those that last for longer periods in tight labor markets.

See David F. Larcker, Allan L. McCall, and Gaizka Ormazabal, “Proxy Advisory Firms and Stock Option Repricing,” Journal of Accounting and Economics 56 (November–December 2013): 149–169. ↑

SARs are essentially net options, and provide for the delivery, in cash or shares (as applicable), of an amount equal to the spread (i.e., the excess of fair market value of the stock over exercise price) upon exercise. Broker-assisted cashless exercises of options have an economic effect similar to that of SARs but technically involve the payment of the exercise price to the issuer with a loan or other assistance from the broker. ↑

Prior to the enactment of the Tax Cut and Jobs Act of 2017 (the “2017 Tax Act”), “covered employees” subject to Section 162(m) included a public corporation’s CEO and its three highest paid officers (other than the CEO and CFO) who were serving as of the last day of the tax year. The 2017 Tax Act expanded the group of covered employees and provided that for tax years beginning on or after January 1, 2018, covered employees include the CEO, CFO, and the three highest paid officers serving at any time during the tax year, as well as any employee who was a covered employee for a tax year beginning after 2016. The 2017 Tax Act also eliminated the performance-based compensation exemption for equity awards granted after November 2, 2017. ↑

The New York Stock Exchange Listed Company Manual, Section 303A.08; Nasdaq Stock Market Listing Rules, Rule 5635(c); Nasdaq Interpretive Material IM-5635-1; and NYSE American LLC Company Guide Section 711 and related commentary. ↑

Nasdaq Stock Market Listing Rules, Rule 5635(c); and Nasdaq Interpretive Material IM-5635-1. ↑

The New York Stock Exchange Listed Company Manual, Section 303A.08; and NYSE American LLC Company Guide Section 711 and related commentary. ↑

The New York Stock Exchange Listed Company Manual, Section 303A.08. ↑

Nasdaq Stock Market Listing Rules, Rule 5635(c); and Nasdaq Interpretive Material IM-5635-1. ↑

The New York Stock Exchange Listed Company Manual, Section 303A.08. ↑

The New York Stock Exchange Listed Company Manual, Section 303A.08; Nasdaq OMX Listing Center, Nasdaq “Frequently Asked Questions.” ↑

It is worth noting that Item 402 of Regulation S-K requires that any repricing of an option held by a director or named executive be disclosed in a company’s annual proxy statement for the election of directors. See also Securities and Exchange Commission, Division of Corporation Finance, Current Issues and Rulemaking Projects Quarterly Update (March 31, 2001), Part II. ↑

For ISO purposes, a modification is any change in the terms of the option that gives the optionee additional benefits under the option, regardless of whether the optionee actually benefits from such change. Treas. Reg. § 1.424-1(e)(4). ↑

Exemptive Order, Securities and Exchange Act of 1934, “Repricing.” ↑

An issuer must satisfy a number of requirements to be eligible for the relief: (1) the issuer must be eligible to use Form S-8, the options subject to the exchange offer must have been issued under an employee benefit plan as defined in Rule 405 under the Securities Act, and the securities offered in the exchange offer will be issued under such an employee benefit plan; (2) the exchange offer must be conducted for compensatory purposes; (3) the issuer must disclose in the offer to purchase the essential features and significance of the exchange offer, including risks that option holders should consider in deciding whether to accept the offer; and (4) except as exempted in the order, the issuer must comply with Rule 13e-4. ↑

If the terms of the offer change (e.g., the option exchange ratio is changed) or other material changes are made to the disclosure in the offer to exchange, a supplement may need to be prepared, mailed to stockholders, and filed with the SEC as part of a Schedule TO amendment. This rarely occurs in an option repricing. ↑

If such change is made at a time when more than five business days remain before the expiration of the tender offer, no extension of the tender offer would be needed. If such change is made in the five-business-day period preceding the scheduled expiration of the tender offer, an extension would be necessary. ↑

Comcast Corporation implemented a similar program with JPMorgan in 2004. In that case, due to the structure of the option plan, Comcast repurchased the options and issued new options to JPMorgan with exercise prices and times to maturity identical to the repurchased options.↑

The Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency (collectively, the “Regulators”) issued a joint “Statement on LIBOR Transition” (the “2020 Statement”)[1] on November 30, 2020. The stated purpose of the 2020 Statement was to “encourage banks to transition away from [USD] LIBOR as soon as possible.”[2] Included in the 2020 Statement was guidance that the Regulators believe that “entering into new contracts that use USD LIBOR as a reference rate after December 31, 2021, would create safety and soundness risks and will examine bank practices accordingly.”[3] As a result, the Regulators have urged banks to “cease entering into new contracts that use USD LIBOR as a reference rate as soon as practicable and in any event by December 31, 2021.”[4]

On October 20, 2021, a new “Joint Statement on Managing the LIBOR Transition” was issued by the Regulators together with the Consumer Financial Protection Bureau, the National Credit Union Administration, and the State Bank and Credit Union Regulators (the “2021 Statement,” and together with the 2020 Statement, the “Regulators’ Joint Statements”)[5]. The 2021 Statement offered additional guidance on the interpretation of the term “new contracts” and specified that the term would include “an agreement that (i) creates additional LIBOR exposure for a supervised institution; or (ii) extends the term of an existing LIBOR contract.”[6] Additionally, the statement clarified that new draws under already existing committed credit facilities would not be viewed as new contracts for the purpose of the guidance under the Regulators’ Joint Statements.[7]

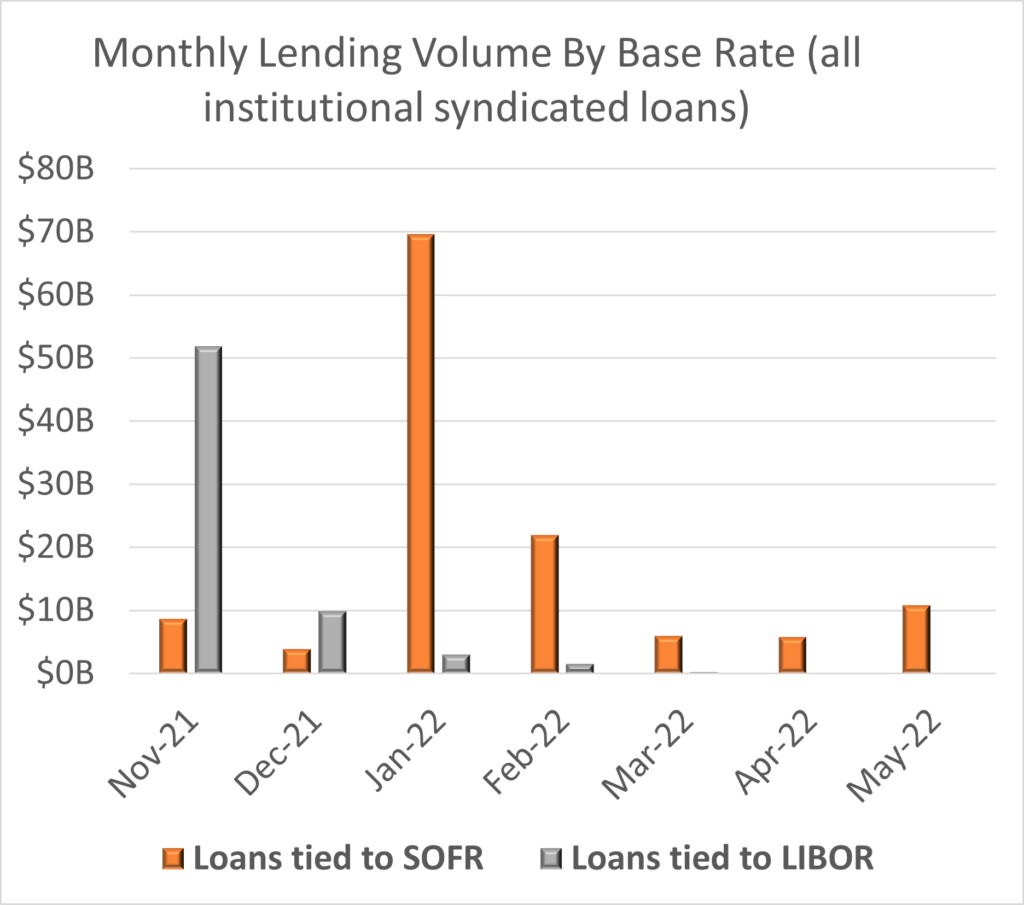

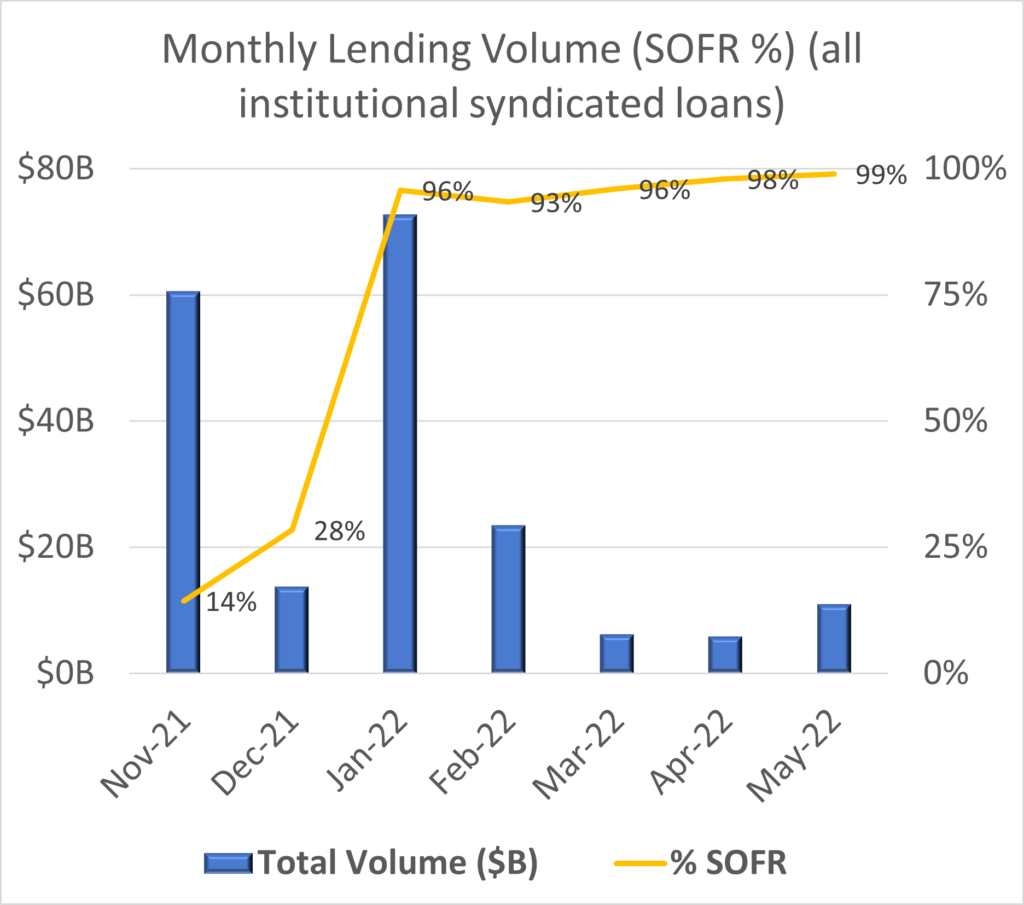

As a result of the Regulators’ Joint Statements, the vast majority of syndicated loan agreements that have closed on or after January 1, 2022, have used interest rate benchmarks other than LIBOR, primarily SOFR. From statistics provided by LevFinInsights (graphs representing these statistics are reproduced below), the pivot from LIBOR to SOFR in the institutional syndicated loans market has been drastic. While over 70% of institutional syndicated loans that launched in December 2021 still referenced LIBOR, less than 5% of institutional syndicated loans that launched in January 2022 reference LIBOR. The move to SOFR has continued in a similar split in the months that have followed since the beginning of 2022, with approximately 99% of institutional syndicated loans that launched in May 2022 referencing SOFR.

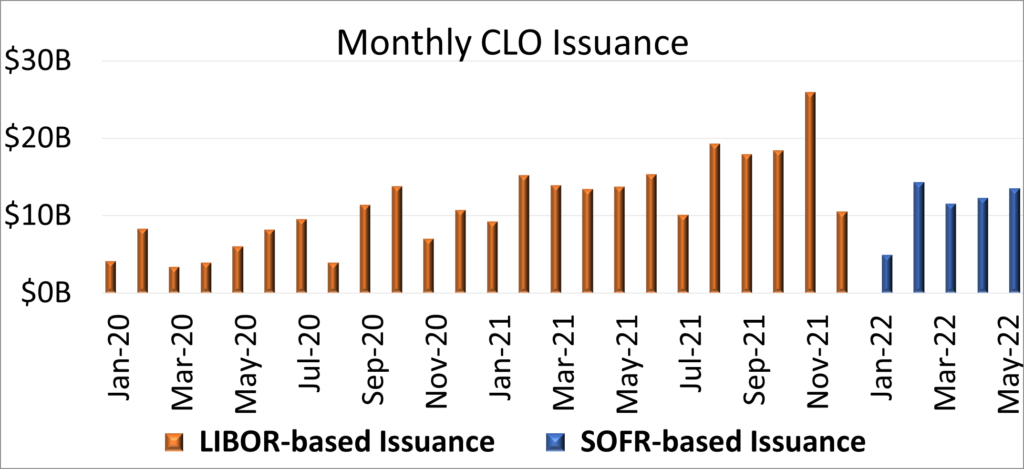

The mechanics of the new SOFR-based institutional syndicated loans impact not only the regulated bank institutions (which are typically the parties that act as lead arranger and administrative agent of the credit facilities), but also institutional lenders (typically collateralized loan obligations (CLOs) and Debt Funds that become lenders under the credit facilities and are interested in trading the loans efficiently). Like the regulated banks, which are largely responding to the Regulators’ Joint Statements in moving credit facilities they help arrange away from LIBOR, the institutional lenders also appear to be eager to move to the new SOFR-based lending world. From statistics provided by Refinitiv (a graph representing these statistics is reproduced below), almost all the CLO notes issued in 2021 referenced LIBOR but almost all the CLO notes issued in 2022 reference SOFR.

As the market for SOFR-based credit agreements has continued to evolve over the course of the first half of 2022, market participants (lead arrangers, administrative agents, lenders, and borrowers) have continued to explore issues that are affected by the new SOFR-based credit agreements. Among specific topics of interest, participants have focused on:

the variance among the non-LIBOR referencing syndicated credit agreements (Term SOFR vs. Daily Simple SOFR vs. BSBY vs. any other credit sensitive rates);

interest rate benchmarks used for incremental facilities in legacy deals;

credit spread adjustments in newly originated credit agreements;

interest period variations;

trading mechanics of SOFR-based loans; and

LIBOR remediation and what impact the new SOFR-based credit agreements may have on Early Opt-in Elections and refinancing/repricings of existing LIBOR loans.

We briefly discuss the latest developments in each of these areas of focus below.

(i) Variance in Interest Rate Benchmarks

Because the Regulators have only encouraged the transition away from LIBOR, a number of interest rate benchmarks have arisen as potential replacements for LIBOR in loan agreements.

The most prominent of such benchmarks is SOFR, which stands for the Secured Overnight Financing Rate. SOFR has been recommended by the Alternate Reference Rates Committee (the “ARRC”)[8] as its preferred alternative reference rate since June 22, 2017.[9] Unlike LIBOR, SOFR is an overnight rate and in its pure form can present operational challenges for certain regular loan market activities, such as prepayments and loan trading. Therefore, SOFR’s use as Daily Simple SOFR in credit agreements has mostly been limited to bilateral or pro rata investment grade facilities that do not normally trade.

A related benchmark, which offers a forward-looking term rate (just as LIBOR is), is Term SOFR. Term SOFR rates “provide an indication of the forward-looking measurement of overnight SOFR, based on market expectations implied from derivatives markets.”[10] CME Group publishes Term SOFR for interest periods of one month, three months, six months and 12 months, and each of CME Group’s rates have been formally recommended by the ARRC for use as replacement rates to LIBOR.[11] Due to the forward-looking nature of Term SOFR rates and the fact Term SOFR has the same operational characteristics as LIBOR, Term SOFR has been the most widely used benchmark in the new syndicated loan agreements that have closed since the beginning of 2022. The same rate has been used in CLO issuances as well.

Other SOFR-based variations are available, such as SOFR compounded in advance using the Federal Reserve Bank of New York’s 30-, 90- and 180-day averages or SOFR compounded in arrears; however, these rates have not received widespread usage in the U.S. syndicated loan market.

Certain other potential benchmarks have been developed as potential replacements to USD LIBOR. These benchmarks all have in common the inclusion of a “credit sensitive component,” which more closely mirrors LIBOR in a time of credit stress. The most prominent of the credit sensitive rates are the Bloomberg Short Term Bank Yield Index (“BSBY”) and the American Interbank Offered Rate (“Ameribor”). Each rate is calculated using a proprietary formula and includes a means of capturing bank credit spreads. While the credit sensitive rates more closely resemble LIBOR than either SOFR or Term SOFR, none of them have been formally recommended by the ARRC and they are also not used as fallback or originating benchmark rates in CLO issuing indentures. As a result, there has been a comparatively low inclusion of such rates in broadly syndicated loan agreements. The credit sensitive rates are most likely to be used in certain regional U.S. bank bilateral or pro rata club syndicated transactions.

Lastly, especially in the first quarter of 2022, there were a few transactions that still used USD LIBOR at origination. These transactions were usually either (i) transactions evidenced by credit agreements that became effective in 2022 but were already committed before the start of 2022; or (ii) “fungible” incremental facilities to existing USD LIBOR credit agreements.

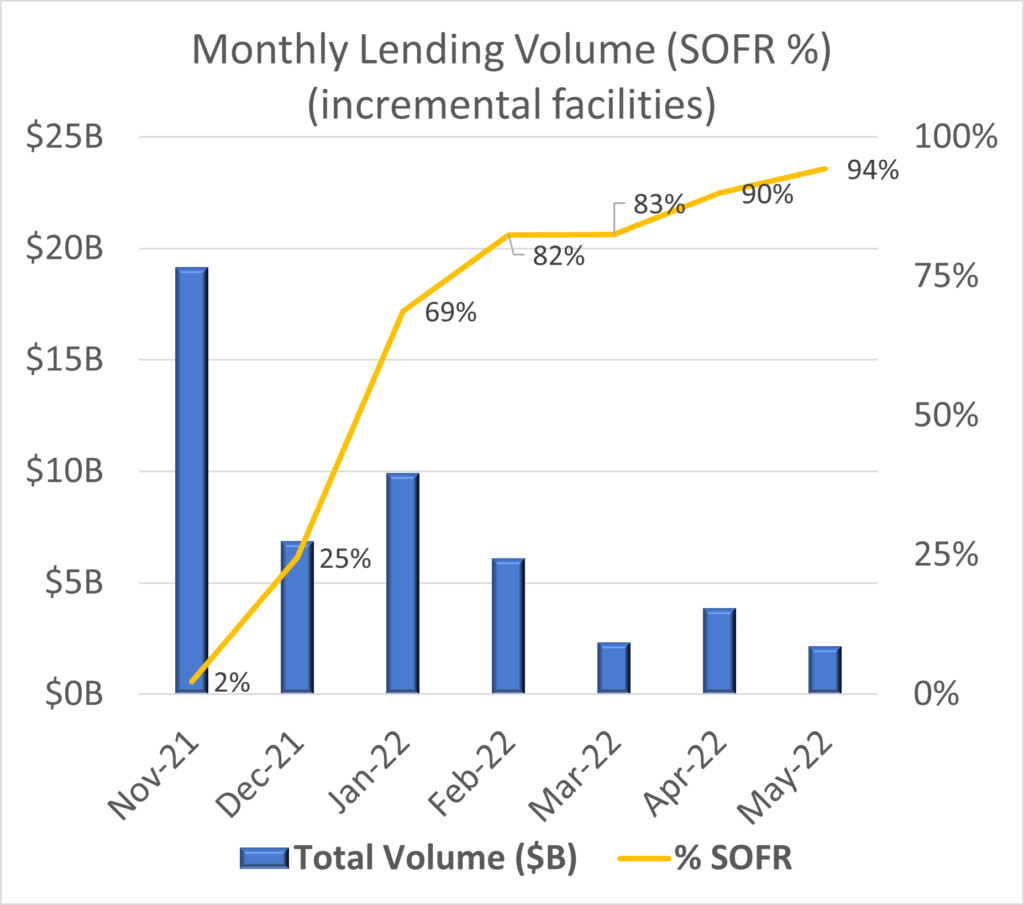

(ii) Interest Rate Benchmarks Used for Incremental Facilities in Legacy USD LIBOR Credit Agreements

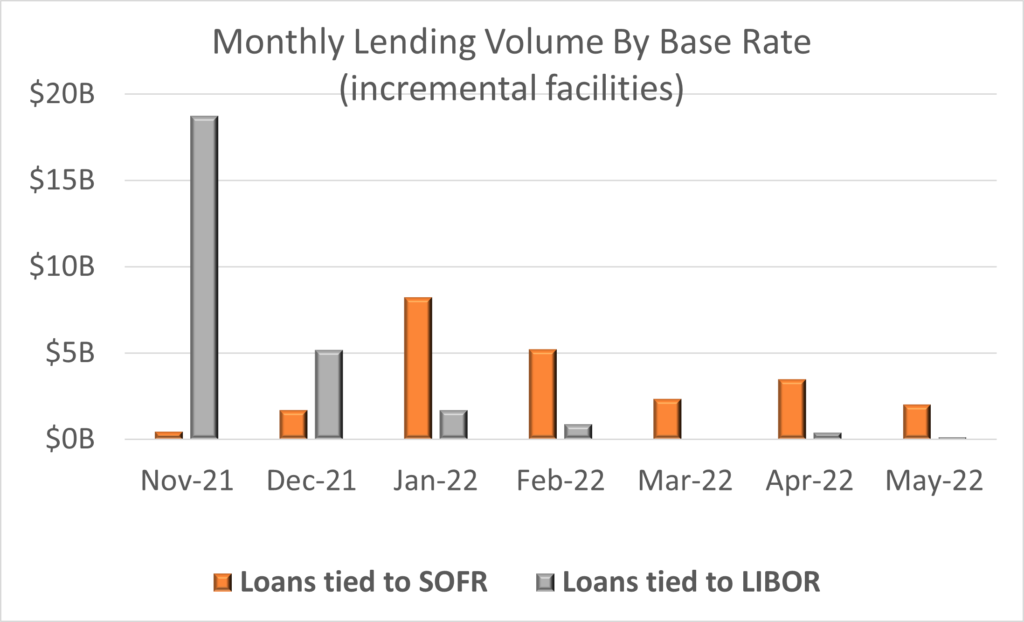

During the first quarter of 2022 there were a minority of incremental facilities (also referred to interchangeably as accordions or add-ons) that were originated using USD LIBOR. From statistics provided by LevFinInsights (graphs representing these statistics are reproduced below), the pivot from LIBOR to SOFR in incremental facilities has been somewhat less drastic than in newly originated credit facilities, although a large majority still use SOFR rather than LIBOR.

While an incremental facility is viewed by many to fit squarely into the definition of a “new contract” used in the 2021 Statement, there are perhaps a few reasons why the use of USD LIBOR in incremental facilities is a “gray” area, especially for those incrementals that were originated in the early part of 2022.

First, incremental facilities are usually much smaller in size than the existing credit facility that exists in the original credit agreement. Given this, it is advantageous and sometimes essential that the new incremental loan be “fungible” with and trade together with the existing credit facility. Without fungibility, given the smaller size, it would be difficult to ensure liquidity in the incremental loan, and the ultimate impact is likely to be a higher interest rate charged to the borrower. The new incremental loan would not be fungible if it uses a SOFR-based interest rate while the existing credit facility continues to use a LIBOR-based interest rate. While an obvious answer may be to amend or refinance the entire credit facility, that is not feasible for all borrowers and can lead to much greater overall transaction costs. With this in mind, one argument that can be made for a LIBOR-based incremental loan is that such a LIBOR origination prevents a disruption to the leveraged loan market with respect to those borrowers that would incur increased transaction costs, and thus complies with the overall goal of regulators not to disrupt the market during LIBOR transition.

Another argument that can be made is that an incremental facility ultimately uses the same loan documentation as the original credit agreement. As such, the new incremental loans would switch from LIBOR to a replacement rate at the same time that the original credit agreement would switch pursuant to its LIBOR replacement mechanics. The new incremental loan would not require a separate amendment to achieve the transition of the entire facility.

Finally, some in the market have taken the position that an incremental facility is not a “new contract,” as the mechanics for the increase are contained in the existing loan agreement. In other words, the borrower is just activating a provision in their loan agreement that already exists, and therefore the requirement to move to USD LIBOR is not required pursuant to the 2021 Statement.

(iii) Credit Spread Adjustments in Newly Originated Credit Agreements

The size of the credit spread adjustment has been the most contentious and heavily negotiated term in SOFR-originated credit agreements. While SOFR is a rate that broadly measures the cost of borrowing cash overnight collateralized by Treasury securities,[12] LIBOR is a rate that averages the rates at which large banks could fund themselves on the wholesale, unsecured funding market.[13] Due to the unsecured nature of the transactions that LIBOR measures, the LIBOR rate is generally higher than SOFR; additionally, LIBOR historically has had larger upward fluctuations in times of economic stress. To capture the difference between the rates over different interest periods (e.g., one month, three months), both the ARRC and ISDA recommended the use of a five-year median spread adjustment,[14] which compares the median LIBOR and Compounded SOFR figures over the five-year period from March 2016 to March 2021. The exact amounts that should be added to one-month, three-month and six-month SOFR contracts (whether of the Daily Simple, Daily Compounded, or Term SOFR variety) using this method are 0.11448%, 0.26161%, and 0.42826%, respectively.[15] These amounts will be added in all contracts that transition from LIBOR to Term SOFR or Daily Simple SOFR relying on the ARRC hardwired fallback mechanics or pursuant to the federal Adjustable Interest Rate (LIBOR) Act.[16]

While it would be consistent to have newly originated SOFR credit agreements use the same credit spread adjustments as will be used for fallback purposes, there is no requirement on market participants to do so. The most recent data shows that switching from LIBOR to Term SOFR plus the ARRC and ISDA recommended credit spread adjustment would lead to a very slightly lower interest rate for borrowers that use one-month interest periods to borrow, while borrowings of three-month and six-month interest periods would result in larger increases to interest rates. The interest rate savings on one-month interest periods are especially modest when considering that due to the rising interest rate environment, more borrowers are likely to choose longer interest periods in order to “lock in” their interest rate for a longer period. However, as both LIBOR and Term SOFR move differently, the differences between these rates (and whether LIBOR or Term SOFR adjusted by adding the ARRC and ISDA recommended credit spread adjustments results in a higher or lower interest rate) fluctuates regularly.

The below table illustrates recent data by showing a “point in time” comparison as of June 23, 2022, between LIBOR, Term SOFR, and Term SOFR adjusted by adding the ARRC and ISDA recommended credit spread adjustments.

June 23, 2022, Comparison of LIBOR, Term SOFR, and Adjusted Term SOFR

LIBOR

Term SOFR

Term SOFR + ARRC/ISDA CSA

1 month

1.62357%

1.49738%

1.61186%

3 months

2.19729%

2.01322%

2.27483%

6 months

2.83529%

2.56366%

2.99192%

From the start of 2022, the newly originated SOFR-based credit agreements have included a mixture of different credit spread adjustments. On one side of the spectrum there are credit agreements that do not appear to add any credit spread adjustment to the Term SOFR rates.[17] On the other side of the spectrum, some credit agreements have adopted the ISDA- and ARRC-recommended credit spread adjustments. The other two most popular options picked by market participants are: (i) adding a flat 0.10% credit spread adjustment across all interest periods; or (ii) adding 0.10%, 0.15%, and 0.25% credit spread adjustments for one-month, three-month, and six-month interest periods respectively. The flat 0.10% credit spread adjustment is more frequently adopted in investment grade or other “pro rata” credit facility agreements that are largely not traded in the secondary loan market. The formulation that includes 0.10%, 0.15%, and 0.25% credit spread adjustments for one-month, three-month, and six-month interest periods respectively is more frequently adopted in leveraged loan credit facility agreements than investment grade credit facility agreements. It is worth noting that if we reference the June 23, 2022, data, both the flat 0.10% and the 0.10%, 0.15%, and 0.25% credit spread adjustment formulations would lead to lower interest rates for borrowers across each of one-month, three-month, and six-month interest periods.

It remains to be seen if, after the LIBOR transition period has ended, some credit agreements will continue to reference a credit spread adjustment to SOFR or whether margin pricing will simply evolve to take into consideration a SOFR benchmark instead of a credit sensitive benchmark.

(iv) Interest Period Variations

The ARRC endorsement of the 12-month CME Term SOFR rate on May 19, 2022[18] resolves one of the open questions of whether or not parties to a credit agreement could include a 12-month interest period. The remaining interest periods that are frequently included in LIBOR-based credit agreements but are not published by the CME as Term SOFR interest periods are one-week and two-month term rates.

With respect to a two-month interest period, we have not seen SOFR-originated credit agreements that include this interest period. For those credit agreements that originated using LIBOR and included a two-month interest period, administrative agents could interpolate the two-month interest period rate using the published one-month and three-month LIBOR rates if permitted pursuant to the terms of the credit agreement.[19] Those credit agreements that contain certain ARRC-based LIBOR transition mechanics allow the administrative agent to remove the two-month interest period. The earlier credit agreements that did not include such a mechanic are still likely not to include the two-month interest period in the LIBOR transition amendment agreed by the parties. Many administrative agents have already notified borrowers that two-month interest periods are not available under their facilities as of the end of 2021.

With respect to the one-week interest period, there have been a few SOFR-originated credit agreements that have retained a quasi-one-week interest period. The most common alternatives used in the market either allow the borrower to make interest payments weekly using the Daily Simple SOFR rate or use the one-month Term SOFR published rate as the reference for the one-week interest period.[20] Failing these mechanics, a borrower could still prepay and reborrow the loan on a weekly basis, but this option can only be used in revolving credit facilities and the borrower risks incurring breakage costs as well as having to remake the representations and warranties in the credit agreement each week upon the new drawing. For LIBOR-based credit agreements, the ability to interpolate a one-week LIBOR rate will depend on the wording of any interpolation mechanics. The results are likely to be similar as with respect to the two-month interest period with the one-week interest period most frequently dropped.

(v) Trading Mechanics of SOFR-Based Loans and the Secondary Trading Market

Historically, secondary trading of loans in the institutional market has been evidenced using the LSTA forms of Confirmation (whether the LSTA Distressed Trade Confirmation or the LSTA Par/Near Par Trade Confirmation), and recently a similar form has been developed by the LSTA for primary allocations (the LSTA Primary Allocation Confirmation) (collectively referred to as “LSTA Trade Confirmations”). Each of the LSTA Trade Confirmations incorporates a Standard Terms and Conditions document that, among other terms, includes a concept for when and how interest on a loan that is earned by a lender may be passed to a prospective lender during the period of time that passes after the parties have agreed to trade the loan but before such loan trade has settled. This concept includes a defined term for “Cost of Carry,” which has historically used LIBOR to calculate what is owed among the parties.

As noted above, since the start of 2022, both new syndicated credit agreements that evidence the loans that are being traded, as well as the indentures that evidence the notes that are used by the institutional lenders to fund themselves, are using SOFR to calculate interest. In line with this move to SOFR, the LSTA updated the LSTA Trade Confirmations and related Standard Terms and Conditions on December 1, 2021, to reference Daily Simple SOFR instead of LIBOR. This change more closely aligns the secondary trading documents with the relevant credit agreements.

(vi) Remediation of Legacy LIBOR Credit Agreements