At any time during 2022, did you: (a) receive (as a reward, award, or payment for property or services); or (b) sell, exchange, gift, or otherwise dispose of a digital asset (or a financial interest in a digital asset)?

The guidance describes a digital asset as a digital representation of value that is recorded on a cryptographically secured, distributed ledger. It lists as common digital assets:

convertible virtual currency and cryptocurrency,

stablecoins, and

non-fungible tokens (NFTs).

Every taxpayer filing Form 1040, Form 1040-SR, or Form 1040-NR must check either the “Yes” or “No” box. Do not leave this question unanswered.

Should I Answer “Yes” or “No”?

To help taxpayers understand how to answer the question, the IRS provides examples of when the “Yes” box should be checked and when the “No” box should be checked. Normally, taxpayers should answer “Yes” if they:

received digital assets as payment for property or services provided;

transferred digital assets for free (without receiving any consideration) as a bona fide gift;

received digital assets resulting from a reward or award;

received new digital assets resulting from mining, staking, and similar activities;

received digital assets resulting from a hard fork (a branching of a cryptocurrency’s blockchain that splits a single cryptocurrency into two);

disposed of digital assets in exchange for property or services;

disposed of a digital asset in exchange or trade for another digital asset;

sold a digital asset; or

otherwise disposed of any other financial interest in a digital asset.

A key point for taxpayers to remember is that using digital assets to purchase a good or pay for a service during the taxable year requires the “Yes” box to be checked. While taxpayers generally will know when they have engaged in a transaction that involves a digital asset, it may not be obvious (or may be easy to overlook) when they receive a digital asset as an award under a loyalty program. For example, a taxpayer may use an online financial services product, such as a credit card, that awards digital assets for using the service. If digital assets are awarded during the taxable year, the taxpayer should check the “Yes” box.

Possibly the most helpful guidance provided by the IRS is when to check the “No” box. Taxpayers who own digital assets during the taxable year but who do not engage in any transactions involving digital assets should check the “No” box. Taxpayers also can check the “No” box if their activities were limited to one or more of the following:

holding digital assets in a wallet or account;

transferring digital assets from one wallet or account they own or control to another wallet or account they own or control; or

purchasing digital assets using U.S. or other real currency, including through electronic platforms such as PayPal and Venmo.

While purchasing digital assets with U.S. or other real currency allows the “No” box to be checked, as noted above, using digital assets to purchase a good or service requires the “Yes” box to be checked.

Digital Asset Received as Compensation. If an employee is paid with digital assets, the employee must report the value of assets received as wages. The employer should provide this value on the Form W-2 furnished to the employee. If an individual works as an independent contractor and is paid with digital assets, the independent contractor must report the value of the digital asset as income on Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship). It would appear that the value of the digital asset at the time it is received is the amount of income that must be reported, even if the value of the digital asset is higher or lower at the time the income tax return for the individual is filed. Schedule C also is used by anyone who sold, exchanged, or transferred digital assets to customers in connection with a trade or business.

Additional Information

In addition to the recently released guidance, more information is provided on page 15 of the Tax Year 2022 1040 (and 1040-SR) Instructions. The IRS also has a set of frequently asked questions and other details on its webpage on Digital Assets.

While the utility of digital assets is much debated, there is little debate over whether engaging in transactions with digital assets creates challenging tax compliance issues for taxpayers.

On February 1, 2023, the Centers for Medicare and Medicaid Services (“CMS”) will issue its final rule on the method for conducting Medicare Advantage audits and calculating overpayments. As part of its 2023 final rule, CMS will eliminate the application of a fee-for-service adjuster (“FFSA”), which reduced the amount of the extrapolated overpayments determined to be owed in risk adjustment data validation (“RADV”) audits, and replace it with a retroactive method of determining extrapolated overpayments.[1]

The Medicare Advantage RADV final rule raises serious issues as to whether it falls within the narrow circumstances under which retroactive rulemaking applies—that is, whether CMS’s corrective adjustment of costs “is necessary to comply with statutory requirements” or whether “failure to apply the change retroactively would be contrary to the public interest.”[2] The implications for the Medicare Advantage program as a whole are significant. Pricing uncertainties affecting the Medicare Advantage bid process, and the potential negative effect on Medicare Advantage plans’ financial reporting treatment of liabilities, may affect the availability or the cost of plan benefits—and could even potentially affect the decision of insurers to remain in the Medicare Advantage market.

The New Standard: Retroactive Rulemaking

In its prior final rule in 2012, CMS recognized the need to use the FFSA to account “for the fact that the documentation standard used in RADV audits to determine a contract’s payment error (medical records) is different from the documentation standard used to develop the Part C risk-adjustment model (FFS claims).”[3] The FFSA was intended to ensure that the amount due in a RADV audit took into account the difference between audit review standards and the errors resulting from unsupported fee-for-service diagnostic codes, creating a permissible level of payment errors and limiting RADV audit recovery to payment errors above the set level.[4]

In the 2023 final rule, instead of using the FFSA, CMS, through its rulemaking authority, will be using a new substantive standard for the extrapolation of overpayments: authorizing the audit of earlier payment periods extending as far back as the 2011 plan year to recoup amounts paid to insurers in those earlier periods.[5] Thus, the audit methodology imposes retroactive rulemaking,[6] despite the fact that courts have recognized that there is a presumption against statutory retroactivity: “[t]he legal effect of conduct should ordinarily be assessed under the law existing at the time that the conduct took place.“[7]

It remains to be seen whether the 2023 Medicare Advantage rule will meet the narrow circumstances under which retroactive rulemaking is permitted.[8] CMS did not cite any prior regulation or statute as a basis for its retroactive method of extrapolating overpayments in RADV audits. In its final rule, it simply stated that “based on longstanding case law and best practices from HHS [Health and Human Services] and other federal agencies,” it had a right to change the extrapolation methods that are “historically a normal part of auditing practice throughout the Medicare program.”[9]

Effects of New Rule

The retroactive RADV rule will change the standard under which earlier payments were made, creating new financial obligations in the current periods.[10] Due to the elimination of the FFSA factor that offset extrapolated amounts and the resulting increased audit recoveries, the change will create uncertainty in the market in two ways. First, it will affect the plan bid process, as plans will be required to estimate potential rebates or premiums based on increased audit recoveries arising from the retroactive application of a different audit methodology. Second, it will affect the financial reporting treatment associated with higher risk-adjusted liabilities.[11]

Rebate Payments to Plan Enrollees

To the extent the calculation of overpayments under the new standard causes the plan’s medical loss ratio to be out of formula with the Affordable Care Act’s 85/15% requirement, plans would be required to pay unexpected increased rebates to enrollees.[12] The amount of the additional rebate would be calculated using a methodology that was not in place during the audited year, relating to a patient population with different actuarial risks than the current one. The pricing distortions and financial risk triggered by noncompliance with medical loss ratios will be magnified due to the lack of a set timetable for resolving RADV audit disputes and the limited scope of appellate challenges permitted.[13] Although there are deadlines by which the insurers must file requests for appeal or reconsideration of hearing officers’ decisions, the hearing officials’ decisions are not subject to any deadlines, and the final review by the CMS administrator is discretionary and unappealable.[14] It is unlikely that appeals of RADV audits would be exhausted before bids were due for subsequent years or a plan’s medical loss reports were due.

Compounding the uncertainty is the inconsistency between two CMS rules pertaining to RADV audit liabilities. Under the 2023 RADV rule, auditors can recover overpayments from the audit of plan years extending back to 2011. However, the financial reporting side of the RADV audit process limits plan liability. The rule pertaining to the reporting of medical loss ratios—the ratio that moves upward or downward based on RADV audit results—limits adjustments to the period from 2017 forward.[15]

Increased Premiums

If the due date for submitting bids to CMS for the next year’s Medicare Advantage contract and the RADV repayment date fall within the same time frame, the insurer would have no choice but to shift the financial risk of the RADV audit results to Medicare Advantage enrollees in the form of increased premiums. In other words, plan enrollees in 2023 could potentially be required to pay a higher premium based on an obligation relating to a patient pool with different actuarial risks.[16] This practice will result in competitive disadvantages and increased volatility in the marketplace. The obvious impact will be that insurers not audited will be able to submit lower Medicare Advantage bids and will be able to charge enrollees lower premiums, leading to a shift in enrollee participation in plans.

Financial Reporting Issues due to Unexpected Charges to Plan Capital Accounts

Where a RADV obligation is calculated under the new standard and falls due in the middle of a plan year, outside of the bid process, the increased liability cannot be shifted as a cost to enrollees in the form of increased premiums. The plans would have no choice but to account for the increased obligation as an additional charge assessed against plan capital accounts.[17]

The financial obligation arising from overpayments determined as part of the audit process could create unexpected consequences at the state level. Recording those additional liabilities may result in the insurer not maintaining its adjusted state statutory capital and surplus levels within state-defined limits,[18] as set out in the National Association of Insurance Commissioners health risk-based capital report.[19] This could potentially trigger regulatory action resulting from questions about the insurer’s financial solvency.[20]

Conclusion

The Medicare Advantage RADV final rule most certainly will be challenged as retroactive rulemaking. Its significant impact on plan pricing and financial reporting will affect both insurer and plan enrollee decision-making.

Medicare and Medicaid Programs; Policy and Technical Changes to the Medicare Advantage, Medicare Prescription Drug Benefit, Program of All-Inclusive Care for the Elderly (PACE), Medicaid Fee-For-Service, and Medicaid Managed Care Programs for Years 2020 and 2021; Extension of Timeline to Finalize a Rulemaking, 87 Fed. Reg. 65,723 (Nov. 1, 2022). RADV refers to risk adjustment data validation, which is the process of verifying diagnosis codes submitted for payment by Medicare Advantage insurers to provide clinical support for the diagnoses. The fee-for-service model reimburses providers by procedures performed. The Medicare Advantage and Medicare fee-for-service models differ in that Medicare Advantage risk adjusts a capitated rate to allow plans that accept patient populations with chronic conditions, requiring the expenditure of more health care resources. Reimbursement under the Medicare Advantage model is diagnosis driven. ↑

Social Security Act, 42 U.S.C. § 1395hh, sec. 1871(e)(1)A). ↑

Ctrs. for Medicare & Medicaid Servs., Notice of Final Payment Error Calculation Methodology for Part C Medicare Advantage Risk Adjustment Data Validation Contract-Level Audits 4–5 (2012). ↑

Contra Azar v. Allina Health Servs., 139 S. Ct. 1804, 1811 (2019) (rulemaking only applied prospectively); Regions Hosp. v. Shalala, 522 US 448 (1998) (rule adjusting base-year cost for inflation was limited to affecting reimbursement for future years and for those cost-reporting periods within the three-year window for auditing cost reports—no new reimbursement principles were applied to prior periods); Bowen v. Georgetown Univ. Hosp., 488 U.S. 204 (1988) (recoupment of amounts previously paid to hospitals applying new rule retroactively is impermissible). ↑

Landgraf v. USI Film Prods., 511 U.S. 244, 265 (1994). ↑

Azar, 139 S. Ct. 1804; Shalala, 522 U.S. 448; Bowen, 488 U.S. 204. ↑

Ctrs. for Medicare & Medicaid Servs., Medical Loss Ratio, https://www.cms.gov/CCIIO/Programs-and-Initiatives/Health-Insurance-Market-Reforms/Medical-Loss-Ratio (last visited Jan. 19, 2023). “The Affordable Care Act requires health insurance issuers to submit data on the proportion of premium revenues spent on clinical services and quality improvement, also known as the Medical Loss Ratio (MLR). . . . The Affordable Care Act requires insurance companies to spend at least 80% or 85% of premium dollars on medical care, with the rate review provisions imposing tighter limits on health insurance rate increases.” To the extent that a plan’s administrative costs exceed the 15 percent ratio, it must pay a rebate to its customers. ↑

Insurers may not appeal the Health and Human Services (“HHS”) secretary’s medical record review methodology or RADV payment methodology. 45 C.F.R. § 422.311 (c)(3). ↑

The insurer must file a written request with CMS for an appeal of the RADV audit report (the medical record review determination or the payment error calculation) within sixty days of its issuance; there is no deadline for the issuance of a written report by the reconsideration officer. The insurer must file a written request for a RADV hearing within sixty days after the reconsideration officer’s report; however, there is no deadline for the holding of the hearing or issuance of any decision. The hearing officer’s decision is subject to a discretionary review by a CMS administrator. If the administrator elects to review the hearing decision, the decision by the CMS administrator must be made within sixty days of acknowledging the decision to review the hearing officer’s decision. The decision of the CMS administrator is final and not subject to appeal. 42 C.F.R. § 422.311. ↑

Ctrs. for Medicare & Medicaid Servs., Medical Loss Ratio (MLR) Annual Reporting Form: Filing Instructions for the 2021 MLR Reporting Year 28–29, https://www.cms.gov/files/document/2021-mlr-form-instructions.pdf (last visited Jan. 19, 2023). Line 1.10 states that HHS-RADV adjustments and other RADV charges do not include any estimates of the 2021 benefit year or of any years prior to 2017. This is contrary to the CMS rule relating to RADV recoupment of overpayments extrapolated under the new standard for plan years dating back to 2011. ↑

The world has moved online, and if your law firm doesn’t have an online presence, you’re going to get left behind. You don’t have to create profiles for every social media platform or create advertising for search engine results pages, but the transformation of business enterprise means you at least need a website for your law firm. When potential clients are seeking out a firm to help them, your web pages will display in search engines and direct clients to you.

Creating a law firm website does take some time and dedication, and it’s important to create useful pages that are representative of your business. Knowing what to include can be challenging, especially because different law firm websites may present different information and prioritize different pages. Even so, we have some tips to keep in mind to help make your website as effective as possible.

Why Do I Need a Law Firm Website?

Often, potential clients seek a law firm out for themselves, searching the internet without the guidance of recommendations or referrals. To have a chance of acquiring these new clients, your firm needs a website to direct them to your business and stand out from the competition. This gives potential clients the information they need to know about your firm and encourages them to get in contact with your team to learn about your services.

Your website also provides an opportunity for you to create the first impression of your business, build your brand image, and communicate your values to potential clients. For those who have no awareness of your firm, your landing pages set the tone. Before a potential client speaks to any member of your team, your website already has the chance to communicate your firm’s principles and who you are through the content you include.

Source: Pexels.

What to Include in Your Law Firm Website

Homepage

In any website design or redesign, you need to pay attention to your homepage, as this is the landing page most clients will arrive at. This needs to establish your law firm name and any essential information that potential clients need to know. From here, it should be easy to navigate to other pages on your website with clearly displayed links or buttons. Your homepage should also give clients an impression of your brand through your logo, images, and color scheme.

About Us

Clients navigating to this page of your website want to know more about your firm and the people within it. Generally, “about us” pages give an overview of a business’s history leading to what you do today. You may also want to use this page to introduce key staff at your firm, including job titles or a short description of their roles. This helps clients to feel more familiar with your firm as they gain some background knowledge, helping to build their trust.

Services

Law firms can cover a range of areas of practice, so including a page or pages on your website laying out your specialties can help direct the right clients to you. Your services could be covered with one page, briefly explaining what each of these includes. Alternatively, if you want to go into more detail, it may be useful to have a page for each separate service or area of expertise available.

Resources

An optional page to include is your resources. This could include templates or reports, showing your expertise and a sample of what your firm does. If you’re interested in starting a blog, this could also be located within your resource pages to provide helpful information for clients and keep your website relevant. Regularly uploading blog posts shows your website is updated and can help your pages to show up in more search engine results.

Source: Pixabay.

Reviews

It’s important to show previous client reviews and testimonials. Reading these can be influential for potential clients deciding whether to use your firm or not. You may want to display reviews on your homepage, so viewers can immediately see what the experience with your business is like. Testimonials can also be included on your about us page, presenting how clients view your firm and the services they have used, or on pages for individual attorneys.

Contact Information

If you want potential clients to become actual clients, they need a way of contacting you. This page should be easy to find on your website, as ultimately your aim is to generate new leads. Typically, contact information should include your firm’s main email address and phone number, and the location of your offices. You can also include links to your social media profiles or enable potential clients to set up an online meeting with a member of your team using cloud communication solutions.

Terms and Conditions

Regulations about how you use and store the data from your website will depend on where your firm is based. Having terms and conditions on your website allows clients to be clear on how you use their information and what they agree to by browsing your pages. You can also provide a privacy policy here, setting out how you use the information and data gathered from your website. This shows your transparency and professionalism.

Other Tips to Keep in Mind for Your Law Firm Website

After you’ve built a basic website for your law firm, you should review your pages to ensure they’re designed to a high standard. This can help to improve the user experience, leaving potential clients with a positive impression of your firm and making them more likely to use your services. You may want to keep the following tips in mind to help you design professional and effective web pages for your law firm’s website.

Source: Pexels.

Create a Brand Image

Having the same color scheme, fonts, and presentation style across your pages helps your website to appear professional and unified. Communicate your brand image to web designers, such as by using a graphic design proposal from PandaDoc, to ensure this is tied into images and visuals on your website. Your brand image can go beyond your pages, using the same palettes and styles for social media posts, files, and presentations to make your firm easily recognizable.

Keep It Simple

It can be tempting to keep adding to your website, but this can make it confusing and convoluted. The purpose of your website isn’t to give clients all the information they could need, but to direct them to your firm and encourage them to get in touch. Having this focus can help your website design prioritize the essentials, avoiding overloading clients with information. If they need to know more, they can always call your number or send an email.

Use Intuitive Design

Intuitive design for your website means your pages are structured and presented to be easy for clients to navigate. Group related pages under headings that make sense, and use buttons or marked links to take clients to the pages they want. Creating a sitemap may help in designing your website, listing where each page can be found.

Optimize for Mobile

More and more, clients are using mobile devices to search online and find law firms. Make your website mobile friendly to allow clients to easily find and interact with your pages. This involves ensuring buttons and links are big enough to select on a mobile screen, and adapting your page design to present well. Check how your website looks on mobile and test the various pages, noting where changes need to be made to improve the user experience.

Source: Pexels.

Use SEO

Search engine optimization (SEO) helps ensure that your website appears at the top of search engine results pages. The higher your ranking, the more clients you attract as they don’t have to look hard to find your website. Make sure your pages include keywords in your headings as well as throughout your copy. Particularly on your blog pages, aim to include internal links to your other pages to make them more noticeable to search engines.

Start Designing Your Law Firm’s Website Today

What your law firm website looks like and includes is up to you. The website should accurately depict your business and give potential clients an overview of who you are and what you do, while encouraging them to get in contact with you. How you do this may vary from other law firms, as each business will reach out to potential clients in different ways.

Once your website is live, keep reviewing it and making improvements. What makes a good website changes as the requirements of clients evolve, so look for trends and incorporate them into your website. This could be through adding newer content, refreshing pages with different images, or working on the user experience to attract new clients to your firm.

In the current environment, financing take-private transactions by private equity (PE) sponsors has been uniquely challenging. Volatility, inflation, rising interest rates, and geopolitical instability have all contributed to making equity and debt financing both more difficult to put together and more expensive. As such, typical private equity financing structures are being replaced with novel and more bespoke financing arrangements.

Despite the uncertain macro environment, private equity remains active, and there is significant dry powder available to be deployed. While fundraising has softened and aggregate capital raised declined in 2022, private equity powerhouses still managed to successfully close on big flagship funds. As PE players get accustomed to the new normal, 2023 is poised to see a resurgence in financial sponsor buying, but likely on new terms and utilizing new structures.

Private Equity Sponsors Are Less Willing to Write Large Equity Checks

Financial sponsors are less willing to write large equity checks to finance leveraged buyouts (LBOs). Unlike the beginning of 2022, when sponsors were willing to underwrite the full equity financing, private equity shops are now less likely to speak for the entire equity check and take on the syndication risk themselves. This development has been accentuated by the need for larger equity checks, as capacity for leverage in the market has shrunk dramatically and equity financing often now comprises a larger portion—sometimes north of 50%—of the overall sources and uses for a deal.

Club deals, which reduce individual equity commitments, are becoming more common, especially in sizable LBOs. For example, Hellman & Friedman partnered with Permira in June 2022 to lead a consortium of investors in buying Zendesk for $10.2 billion. In another notable deal in the software space, Datto was acquired by Kaseya for $6.2 billion, with funding from an equity consortium led by Insight Partners, with significant investment from TPG and Temasek.

As such, in large take-private transactions, careful consideration should be given to which private equity players are able to write the equity check necessary to execute the transaction on their own, versus which will need a partner. When running an auction and deciding when and how to pair up potential general partners, target companies and their advisors should be thoughtful about the potential impact of partnering arrangements both on the price a bidding consortium would be willing to pay for the company, as well as on the overall competitive dynamics of the sales process.

Sovereign Wealth Funds and Public Pension Funds Are Increasingly Playing a Key Role in Private Equity Transactions

Sovereign wealth funds (SWFs) have been very active in take-private transactions, and virtually no LBO of a meaningful size can be executed in the current environment without some level of SWF participation. The SWFs of Saudi Arabia, Singapore, Qatar, and the United Arab Emirates are on the list of desired limited partners (LPs)/co-investors of virtually every top-tier financial sponsor looking at a sizable LBO.

Canadian public pension funds have also become some of the world’s largest investors in private equity and are often on the list of requested LPs/co-investors. Many of them focus on investments in the infrastructure space, where they can generate stable returns commensurate with the expected payouts under pension plans.

While SWFs and public pension funds previously participated in private equity transactions passively, through their LP interests in PE funds, they have increasingly been coming in as co-investors alongside private equity firms, in roles with varying degrees of board and other governance rights. For example, in December 2022, Advent International agreed to acquire Maxar Technologies for $6.4 billion, in a transaction financed with $3.1 billion equity commitments from funds advised by Advent and a separate $1 billion minority equity investment by the British Columbia Investment Management Corporation.[1]

Allocating LPs to bidders in a sell-side process is nowadays equally important as general partner (GP) partnering decisions, as LP access can be particularly relevant to the ability of certain PE sponsors to put forward fully financed bids, especially in mega deals. As such, putting together the right GP/LP investor groups can be essential for the successful outcome of auction processes, and decisions as to when to allow financial sponsors to talk to LPs—and which LPs they can have access to—carry significant weight.

In addition, the identity of LPs, the size of co-investor stakes, and the constellation of governance rights given to co-investors can dictate the scope of governmental clearances needed to close a deal, how long it will take to get them, and whether there is risk that they will not be obtained. This is something that can clearly weigh in the favor of—or, conversely, detract from the attractiveness of—any bid and should be given due diligence and factored in when making key strategic decisions over the course of auction processes.

Currently, Traditional Lending Markets Are Effectively Shut Down for Large LBOs

The syndication of the debt financing for the LBO of Citrix marked a watershed moment in traditional lending markets. For all intents and purposes, the big banks are not currently open for business when it comes to big LBOs.

In January 2022, Vista and Evergreen, an affiliate of Elliott Investment Management, agreed to acquire Citrix in a $16.5 billion LBO—the largest LBO of the year, setting aside Elon Musk’s purchase of Twitter. At the time, Vista and Evergreen had a $15 billion fully committed debt package ($16 billion counting the revolver) underwritten by a group of bulge bracket banks, led by Bank of America, Credit Suisse, and Goldman Sachs.

The debt was priced before the markets started souring and interest rates started rising in steep increments, and the banks had a difficult time offloading the debt. According to news reports, the Citrix bonds and loans were sold at big discounts to face value, and the underwriting banks ended up with more than $600 million in losses (and some junior debt remains unsold). Some commentators went as far as to label the Citrix debt sale “the point of no return” and a “bloodbath.”[2]

The story of the Twitter acquisition financing is not that different. According to Bloomberg, in November 2022, Wall Street banks were sitting on more than $40 billion of buyout and acquisition debt that they were not able to sell following the dramatic turn in credit conditions earlier in 2022.[3] Notwithstanding certain sales and block trades at the end of 2022, much of this LBO debt hangover still remains on bank balance sheets—which includes an estimated $12.5 billion of loans tied to the buyout of Twitter, as well as loans in connection with the acquisitions of Nielsen, Brightspeed, and Tenneco—and has significantly reduced banks’ appetite for more LBO financing in the near term.[4]

Direct Lenders and Private Credit Are Taking the Place of Traditional Underwriters

The void created by big banks sitting on the sidelines of LBOs has been filled by direct lenders and other sources of private capital, particularly in the software and technology sectors. For example, a Blackstone-led group of direct lenders provided a record $5 billion loan for the Zendesk deal,[5] and a private debt club led by Blue Owl Capital provided a $2.5 billion loan to finance Vista’s $8.4 acquisition of Avalara.[6] Unlike traditional banks, who seek to place and sell committed acquisition financing to the debt market, direct lenders are in the business of holding the debt and are, unlike traditional banks, not under pressure to sell it.

Historically, direct lenders would often finance transactions on their own or in small groups. In recent deals, however, particularly for the larger LBOs, consortiums of direct lenders may include upwards of fifteen lenders. Direct lenders are credit focused and are known to do a deeper dive in diligence, as they are making the loans with the expectation of carrying them on their balance sheets until maturity. Direct lending debt packages may also be more expensive and contain bespoke features (such as a blend of callable and non-callable debt) designed to deliver lenders their desired returns. As a result, ironing out the details of a debt financing package can be more involved than in a traditional syndicated term facility and/or bridge to bonds. Direct lenders also have flexibility to provide alternative forms of private capital, notably preferred equity (typically combined with a direct lender debt financing or with a financing led by the traditional banks), which can give buyers greater flexibility, especially if rating agencies are willing to assign equity credit to the alternative financing.

Because of this, from the sell-side standpoint, it is important to ensure from the outset that the company has control over potential bidders contacting debt financing sources and that potential buyers cannot lock up debt financing sources in exclusivity arrangements without the company’s consent. In many deals, especially larger ones, competing private equity bidders need to go to the same universe of direct lenders (subject to customary “tree” and information barrier arrangements) to finance their bids, and locking up any debt providers can impede the competitiveness of an auction.

In addition, target companies and their advisors should be thoughtful about when to allow private equity firms to contact debt financing sources. Given the number of parties that would be brought under the tent, the risk of leaks should be considered and balanced against the need of private equity buyers to get perspectives from lenders to put forward firm bids and the need of lenders to have time to do their diligence and go through their investment committee processes to be able to execute binding financing commitments.

Auctions Need to Be Carefully Orchestrated from Beginning to End to Deliver the Best Value for Target Companies

For the reasons described above, from the outset of a sales process, target companies should ensure that they have full control over when potential buyers can contact equity and debt financing sources, who they can join forces with, and the basis on which they can engage with potential co-investors and lenders. These terms are often set at the NDA phase of a process and can set the stage for the entire auction. Some of the most crucial inflection points for the successful outcome of a sell-side process are the decisions regarding partnering, with the when, who, and how carrying significant consequences for the end result of an auction.

We wish to recognize, with immense appreciation, the assistance of Daria Butler.

Financial Technology (fintech) is a catch-all term to describe new technology used to improve and automate financial services. Although the concept has existed for some time, breakthroughs in blockchain and other distributed ledger technology, artificial intelligence, quantum computing, and biometrics have accelerated the rate of change. This recent evolution has created an influx of a broad range of startups with diverse business models looking to gain market share or offer new products or services.[1]

Similar to other industries that have reached this stage in their development cycles, fintech will likely experience an increase in M&A activity as the industry consolidates and incumbent companies look to capitalize on emerging disruptive technology to improve the financial services they provide through a buy-or-build model. Deal lawyers need to be keenly aware of industry-specific risks to engineer transactions that maximize value and ensure that their clients receive a commensurate share of the gains.

Mechanisms to Reduce Transaction Costs in M&A Deals

Representations and warranties (reps and warranties)—along with their associated disclosure schedule, indemnifications, covenants, conditions to consummate the deal, and earn-outs—are ubiquitous in M&A transactions as means to contractually reduce information asymmetry, efficiently allocate risk, and minimize moral hazards between the buyer and seller. In the hands of a skilled transactional lawyer, these tools and mechanisms have the potential not only to sway the allocation of gains from a transaction in favor of their client but to increase the deal’s value net legal fees by reducing transaction costs and helping to close the valuation gap between the parties.[2] As such, deal lawyers can play an integral role in the fintech ecosystem’s development by helping to facilitate value-creating transactions and the efficient use of capital in the industry.

Along with information provided in the diligence process, representations (statements of facts about a business’s past or present operations) and warranties (promises about future business operations) help minimize information gaps between the buyer and seller in a transaction. To enforce the reps and warranties, acquisition agreements typically contain an indemnification clause in which the breaching party compensates the non-breaching party for losses or damages sustained from the breach. Drafted carefully, indemnity provisions create an incentive structure for the parties to accurately disclose material information to each other, allowing the parties to allocate risk efficiently.

Additionally, the parties to a transaction ordinarily enter into a set of covenants in which the parties promise to take or not to take certain actions before and after closing to preserve the anticipated value of the deal gleaned during the diligence process. Unless a deal is structured as a simultaneous sign and close, many acquisitions will have a significant gap between when the acquisition agreement is signed and when the transaction is closed. Covenants help mitigate the risks between signing and closing and the risks following the consummation of the transaction by incentivizing the parties to refrain from taking unusual risks that might jeopardize the value of the deal.

Lastly, acquisition agreements generally contain a set of conditions that must occur before the parties are obligated to close the deal. Two customary pre-closing conditions are (1) that the parties remain in compliance with the pre-closing covenants and (2) that the reps and warranties remain true and accurate as of the closing date. Additionally, the indemnification clause typically includes breaches of the conditions as a cause for compensation. The pre-closing conditions, along with the indemnification clause, provide a powerful incentive for the parties not to breach the terms of the agreement while the transaction is being consummated and help to reduce transactional costs.

Although deal lawyers have many tools to help reduce transactional costs and facilitate agreement on key issues, parties often disagree on the prospective value of the target business, creating a barrier to what would otherwise be a value-creating transaction. To help bridge the valuation gap, earn-outs or deferred payments provide a valuable tool to help the parties reach an agreement. Earn-outs, when appropriately structured, can benefit both parties, minimizing risk and providing an incentive for management to continue working diligently to achieve agreed-upon benchmarks. As such, the seller has the opportunity to receive the full value for its business, and the buyer can protect itself and ensure that the asset performs as anticipated.

The reps and warranties, disclosure schedules, indemnification provisions, and closing conditions work in tandem in M&A deals to reduce transaction costs by helping to minimize information asymmetry between the negotiating parties and allowing them to efficiently allocate risks, price the deal, and plan for future operations. Along with these mechanisms, deal lawyers have various levers at their disposal to calibrate a party’s risk exposure—particularly knowledge, materiality, scope, and time qualifiers. These mechanisms and levers are essential for transactions in sectors fraught with risk and uncertainty.

The Fintech Industry’s Idiosyncratic Risks

The framework above of the mechanisms and levers deal lawyers use to facilitate efficient capital asset transfer is by no means exhaustive. Rather, this framework illustrates the potential for transactional lawyers to add value to deals and the fintech ecosystem by engineering efficient transactions to help foster synergy and economies of scale in the fintech industry.

The fintech ecosystem is vast and encompasses an extensive range of businesses offering various products and services, ranging from digital payment platforms, robo-advisors, non-fungible tokens, and digital currencies to digital lending platforms. The variety of idiosyncratic risks in the fintech industry is equally broad, including regulatory uncertainty, fintech companies’ heightened operational risks stemming from handling consumer financial data, the volatility associated with certain crypto assets, cybersecurity risks, and unique intellectual property risks. These risks can create tremendous friction in the deal-making process; however, well-crafted deal documents can help mitigate these risks and facilitate the efficient transfer of fintech assets.

For instance, cybersecurity and data breach issues are prevalent in the fintech industry, giving rise to data privacy risks. Reps and warranties from the seller regarding IT and data security policies, historical breaches, and compliance with regulatory obligations (along with indemnifying the buyer for breaches of those reps and warranties) are instrumental to reducing information asymmetry between the parties and efficiently allocating data privacy risks associated with handling sensitive customer information.

Further, buyers of fintech assets should consider including in the deal documents disclosures of and indemnification from the use of open source software in the development of business technologies of the seller. This can mitigate the risk that the source codes of the seller’s products derived from an open source software could be required to be distributed or disclosed to the general public, which could materially reduce the value of the fintech asset.

The deluge of fintech activity has garnered an influx of regulatory attention at the federal, state, and international level,[3] as evidenced by the President’s recent Executive Order 14067 on Ensuring Responsible Development of Digital Assets (EO).[4] The EO provides an excellent example of the litany of regulatory risks in the fintech industry, as it requires a number of federal agencies to submit reports on various issues that directly impact fintech companies’ operations. The issues covered include consumer and investor protection, data privacy and security, preventing illicit finance (AML/CFT/KYC), financial inclusion and stability, and central bank digital currencies (CBDCs). Notably, the EO does not enact any explicit policies but rather establishes a coordinated, interagency process to deliberate the issues.

It will take some time for the federal government to operationalize a coordinated approach toward regulating digital assets. Additionally, state and international regulators add another layer of uncertainty and complexity to the fragmented fintech regulatory regime. The lack of regulatory clarity in fintech provides a prime opportunity for deal lawyers to add extraordinary value to transactions through the private ordering of regulatory risks.

Illustratively, the investor protection regulatory regime of digital assets has been in a state of flux as the SEC and CFTC attempt to provide regulatory guidance on the characteristics of digital assets that will deem a product a security or a commodity—a factor that could have a substantial impact on the value proposition of a project. However, the principle-based definition of securities does not bode well for bright-line rules. Central to the analysis are the nuanced and fact-intensive “reasonable expectation of profits” and “from the efforts of others” prongs of the Howey test.[5]

Ordinarily, the seller will have more knowledge and information about the regulatory status of a business, whether through interactions with regulators or advice previously received from financial and legal advisers—information that would be difficult or expensive for the buyer to obtain and would have a significant bearing on the valuation of an asset. Carefully crafted reps and warranties coupled with a set of bespoke indemnity provisions can help reduce the information asymmetry between the buyer and seller to allocate the risks between the two parties appropriately and efficiently price the asset. Additionally, innovative use of earn-out provisions can be extremely useful to allocate regulatory risk among the parties efficiently—for example, making part of the consideration contingent on obtaining an SEC no-action letter.

Undoubtedly, the evolving fintech regulatory regime will tremendously impact fintech companies’ operational risks and create endogenous risks within the fintech industry. The EO prominently features the specter of a potential deployment of a US-issued CBDC. It is difficult to determine if the US will eventually launch a CBDC or its design function. However, the possibility of a US Federal Reserve-issued CBDC (US CBDC) for retail consumption creates competitive risks for privately developed payment systems and stablecoins. The design function for a potential US CBDC would have a consequential impact on the fintech ecosystem; particularly of interest would be whether or not the US CBDC undermines the two-tiered banking system and whether the US CBDC is interoperable with other forms of digital currencies.

A US CBDC has the potential to spur or stifle private economic innovation. Even improvements to the payment rails of our current Federal Reserve System can create risks for the value proposition of private payment system projects. Deal lawyers will need a deep understanding of the policy priorities of key regulators to help clients navigate the risks government action or inaction creates in the fintech ecosystem. Concretely, deal lawyers can play a vital role in helping clients manage the risk of acquiring a fintech asset susceptible to increased regulatory scrutiny, which could result in a material loss of value.

Lastly, many M&A transactions’ projected value derives from the patentability of a product. However, fintech products stemming from blockchain technology on a peer-to-peer network to validate transactions create endemic impediments to clearing the Alice/Mayo two-part test for patent subject matter eligibility. Particularly, the likelihood is high that a claimed invention derivative of blockchain technology will be deemed directed at an abstract idea, which the Supreme Court has held is not patentable as an implicit exception to the four statutory categories of invention pursuant to 35 U.S.C. §101. Although a claimant can overcome a judicially recognized exception if it recites additional features that amount to significantly more than the abstract idea, in light of the proliferation of Satoshi Nakamoto’s white paper, the code supporting blockchain technology is “well known in the art,” casting a hurdle for novel and non-obvious applications.[6]

The United States Patent and Trademark Office (USPTO) has granted numerous blockchain patents. However, prosecuting a patent in the blockchain technology space is laden with risk. Although the USPTO has provided guidance on issues related to patent subject matter eligibility deriving from the Alice/Mayo test, applying the test in practice has been murky. Deal lawyers can play an instrumental role in helping allocate the risk associated with patent issues when structuring transactions to help bring the parties to closing.

Conclusion

Fintech is revolutionizing the way we transfer value and conduct commerce. Commensurately, the industry has attracted an enormous amount of capital and has surpassed a $3 trillion market cap. Along with the considerable capital inflow, the fintech industry has garnered the attention of regulators at the federal, state, and international level. As illustrated, the increased regulatory scrutiny and market dynamics engender significant risks and friction in deal-making, creating an opportune environment for deal lawyers to add tremendous value not just for their clients, but for the fintech ecosystem as a whole. Beyond having a keen understanding of deal structures, and the fintech industry’s idiosyncratic risks and market dynamics, transactional lawyers need impeccable judgment, foresight, and ingenuity to become trusted advisers when helping clients structure efficient transactions in a constantly evolving industry full of risks and opportunities.

Tumultuous, exasperating, difficult, nerve-wracking, and frustrating are all apt descriptions of the 2022 SPAC market. We’ve summarized some of its ups and downs in our year in review blog post from October and have touched on them again in our December podcast with Doug Ellenoff.

In this article, we’ll examine the hard data, which, in some cases, is yielding surprising and—dare we say it—positive trends and conclusions.

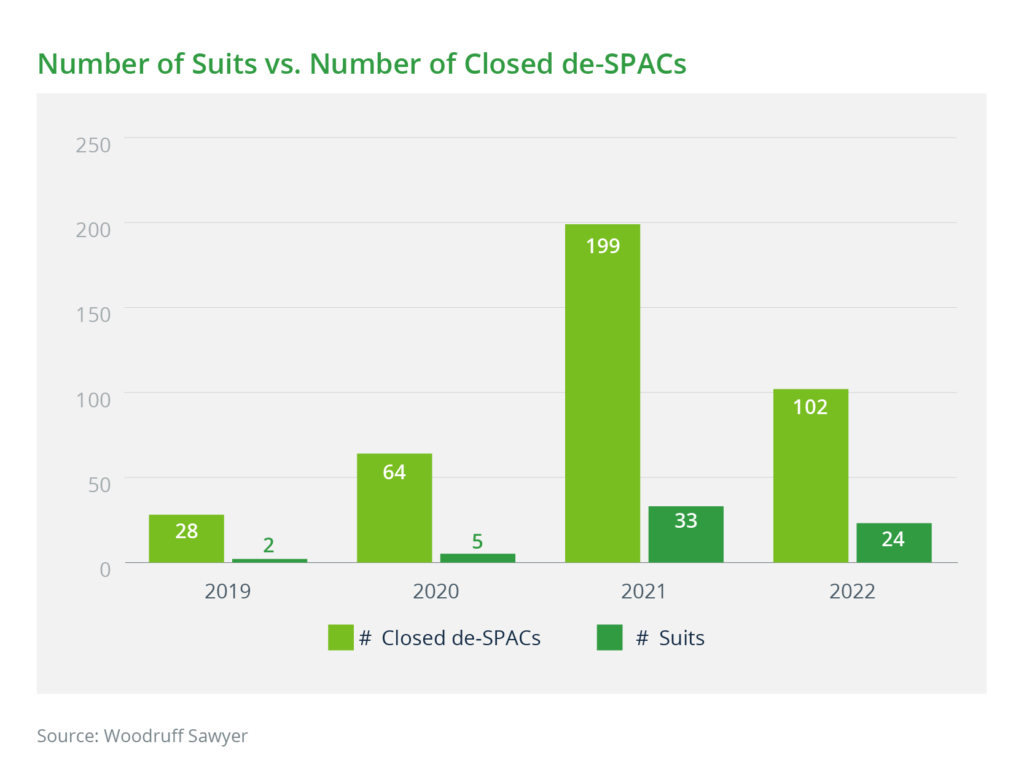

SPAC Lawsuits by the Numbers

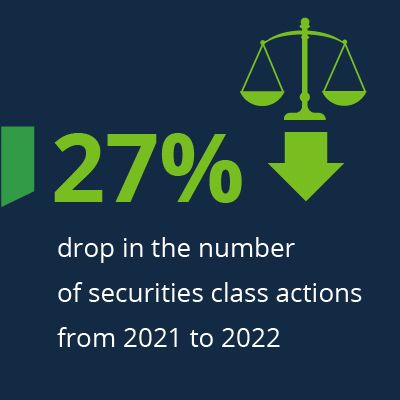

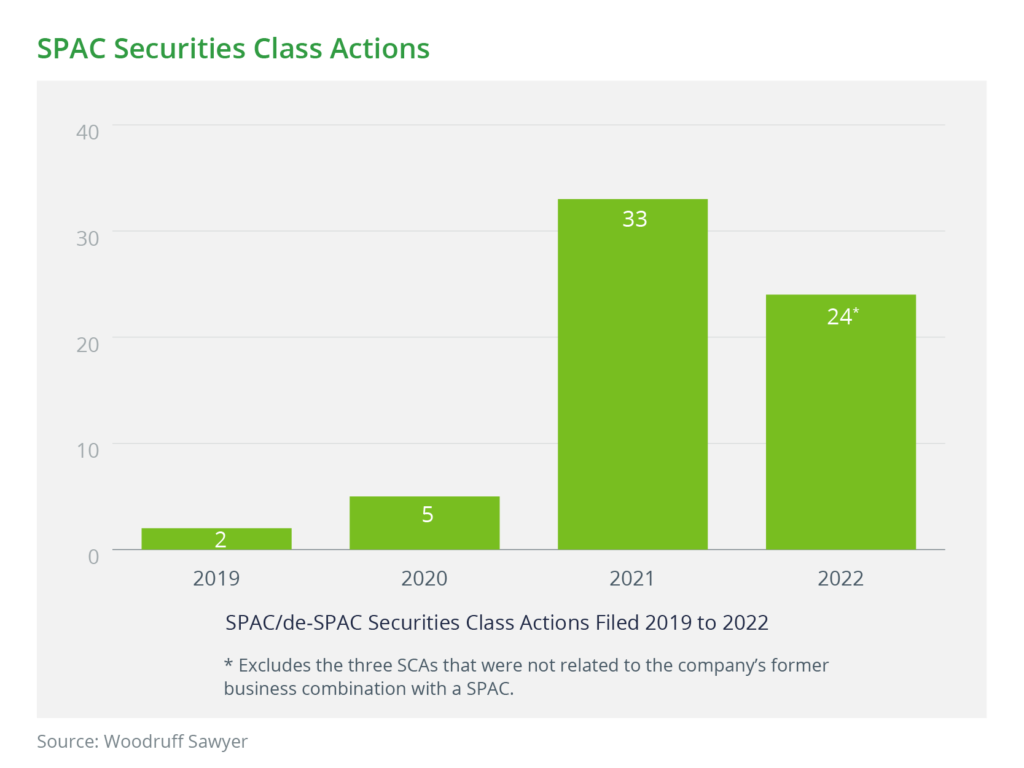

In 2021, there were 199 closed de-SPAC transactions, a number that is almost double the 102 de-SPACs that closed in 2022. In 2021, we observed 33 securities class actions (SCAs), which were filed following 2020, a year with only 64 closed de-SPACs. Based on the average time after the merger (nine months) or the SPAC IPO (22 months) that it takes for an SCA to materialize, we were expecting a much higher number of SCAs in 2022. But, in fact, only 24 SCAs were filed in 2022—a 27% decline from 2021 numbers.

Reasons for Decline in SCAs

What could be causing the decline in the number of SPAC securities class action lawsuits? First is the increased sophistication of SPAC market participants, including SPAC teams and their advisors, over the last two years. This sophistication grew out of both new, more experienced teams and advisors entering the market and out of the increased experience of all those teams and advisors as the SPAC rush of 2020 and 2021 progressed. Many ended up handling more SPAC transactions, both on the IPO and the de-SPAC side, than they ever had before, and, naturally, they learned from previous missteps. This is the so-called self-correction that we referred to in our previous posts and podcasts.

The second reason for decreased litigation volume is the overall decline of the financial market in 2022. Many companies, including those that went public via a traditional IPO and a SPAC, have been experiencing disappointing performance. When the entire market is hurting, it is difficult for a plaintiff’s attorney to claim that one particular team or merger did particularly badly.

The third reason could be the proposed SEC rules regarding SPACs, which came out in March 2022. Even though these rules are still not finalized, many adopted them as a playbook and quickly adjusted their disclosures and transactions to comply.

SPAC Litigation Compared to SPAC Activity

Taking a look at the number of SCAs and the number of de-SPACs in each year leads to the interesting graph below. Although some SPACs and their targets were sued prior to the completion of the merger, the majority of SPAC-related SCAs occur post-merger. It typically takes a few months—nine months on average—after the merger occurs for a lawsuit to be brought. Understanding the lag between a SPAC merger and a lawsuit, it is interesting to see the decline not only in the absolute number of SCAs from 2021 to 2022 but in the number of SCAs relative to the number of completed mergers in each of those years.

Funky Suits

Of course, the SPAC SCA is not the only type of lawsuit that exists. We saw quite a few new types of lawsuits against SPACs in 2021 and a few more novel fact patterns that resulted in disputes in 2022. For example, we saw a few skirmishes around a merger termination fee when the SPAC team decided to keep the fee without sharing it with its investors (e.g., FAST Acquisition Corp., Concord Acquisition, and Pioneer Merger Corp.).

Other types of unusual suits that we had not seen many of in the past include:

A suit by an executive of Digital World Acquisition Corp., a SPAC tied to Donald Trump, alleging fraud at the SPAC and asserting that the executive was frozen out of the deal.

A suit against a parent of Quantum Fintech Acquisition’s target for sabotaging the target’s deal with the SPAC.

There have also been a few derivative (and some direct) actions filed against the D&Os of a SPAC for breaches of fiduciary duties in proceeding with a merger that later turned out to be unsuccessful. The usual themes for a derivative suit, which is typically filed in tandem with an SCA, include rushing into a transaction, failing to conduct proper due diligence, entering into a deal outside of the SPAC’s targeted industry, and the SPAC omitting information relating to potential dilutive effects of the merger.

Likelihood of Getting Sued

One of the questions we often get from clients is focused on the likelihood of their team or venture getting sued. The answer to this question is meant to assist the teams in deciding on the amount or type of the directors’ and officers’ (D&O) insurance they will ultimately purchase. The answer is not simple, but some recent data we collected may be instructive.

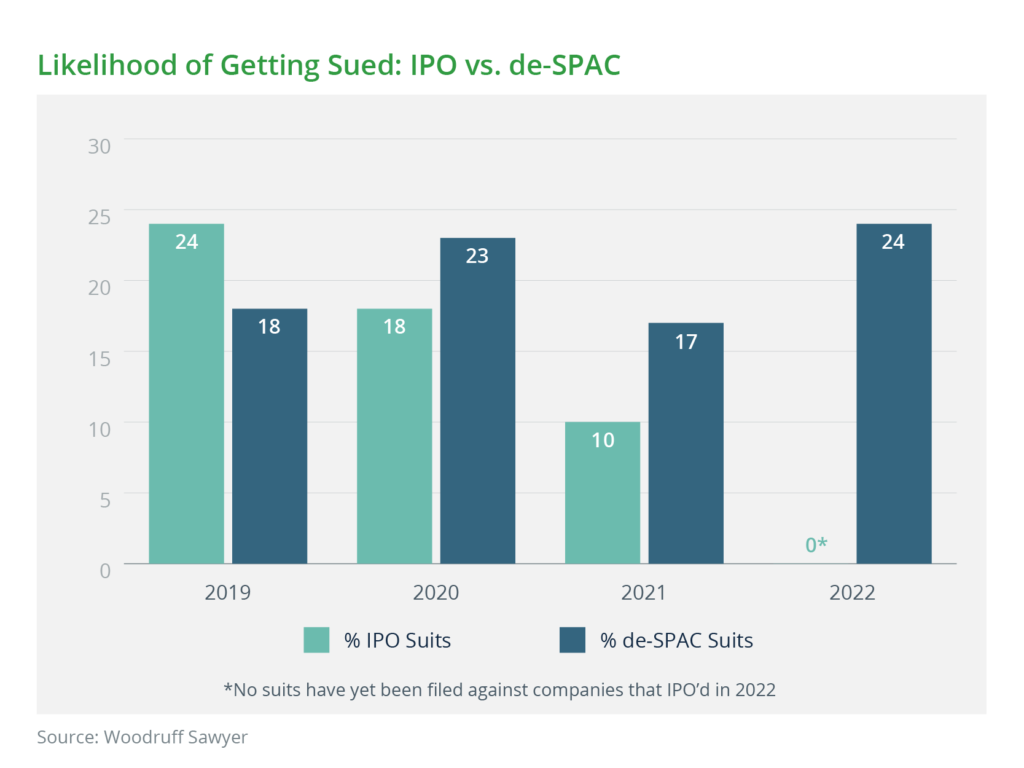

Companies that go public via a traditional IPO are more likely to get sued than mature public companies, and companies merging with a SPAC are more likely to get sued than those going public via a traditional IPO.

As a rough estimate, one can expect about 3% of companies that have been public for 10 years to become subject to an SCA. That number is significantly higher for newly IPO’d and de-SPACed companies. The reason is simple—new public companies are more likely to stumble out of the gate.

An interesting risk question is whether there is a difference in likelihood of a lawsuit for companies going public via a traditional IPO and those choosing the SPAC route. The answer is yes, and the graph below illustrates that difference.

Although there is indeed an increased risk of a lawsuit for companies going public via a SPAC rather than a traditional IPO, that differential in risk is not enormous.

Settlements

Now let us turn from lawsuits to settlements. There have been very few publicly disclosed settlements, and some of them did not stem from an SCA, so it is very difficult to draw conclusions about trends. The ones that made the news include:

Triterras:SCA settlement of $9 million in April 2022. The action was filed after a short seller report raised issues with disclosures about a related party.

Multiplan: A direct-action breach of fiduciary duty claim that settled for $33.75 million in November 2022. After a short seller report raised issues with the company’s largest customer, the suit was filed in Delaware. The judge denied the motion to dismiss, and the parties settled.

TradeZero: Private action settlement of $5 million in December 2022. A SPAC (Dune Acquisition) entered into a merger agreement with TradeZero. The merger fell apart, and Dune sued TradeZero.

It is worth remembering that outside of the actual settlement amounts, some of which were covered by a D&O insurance policy in the above cases, the defendants had to also pay substantial attorney fees. When deciding on the limit of a D&O policy, it is worth factoring in the potential costs of the attorney fees, which will be due whether or not the lawsuit ends up being frivolous or ultimately gets dismissed.

Regulatory Enforcement Actions

The other piece of the risk puzzle is, of course, the risk of regulatory enforcement actions and investigations. With the SEC taking an openly hostile stance towards SPACs in 2022, many of us expected to see a barrage of SPAC-related investigations and enforcement actions. That expectation has not yet been realized. While there have been a few investigations reported, there have been fewer than a handful of enforcements. Here are some examples that made the headlines:

Momentus: Settlement total of $8.04 million in July 2021. The SEC alleged that Momentus and the founder misled Stable Road, the SPAC with which it planned to merge, about its technology and national security issues and that Stable Road had failed to perform its due diligence to identify those issues.

Nikola: Settlement total of $125 million in December 2021. The enforcement was preceded by a short seller report and an SCA and centered around misleading statements about Nikola’s products, technical advancements, and commercial prospects.

Perceptive Advisors: Settlement of $1.5 million in September 2022. This was the SEC’s first enforcement action against an investment adviser. The SEC charged the adviser with violating the Investment Advisers Act in connection with its involvement with SPACs.

Gordon: Administrative charges settled against CEO in 2019 for $100,000. The SEC charged Benjamin Gordon, the former CEO of Cambridge Capital Acquisition Corporation, a SPAC, with failing to conduct appropriate due diligence to ensure that the SPAC’s shareholders voting on the merger were provided with accurate information concerning the target’s business prospects.

An interesting way to think about these settlements and enforcement actions is through the lens of the enterprise value of the SPAC business combinations that were completed in the last few years. The total expenditures on private settlements and government enforcement actions run in the millions of dollars and constitute a tiny fraction (likely no more than 0.05%) of the billions of dollars in enterprise value of closed de-SPACs.

Now it is true that SEC typically takes several months—if not longer—to bring and conclude an enforcement action. Considering that the SPAC market went into overdrive in late 2020 and two years have already passed since then, it is interesting that the SEC’s enforcement division has not been able to locate more examples of situations worth pursuing. Could it be that aside from the less than a handful of egregious cases that have been flagged thus far, the rest of the SPAC market teams and deals are operating within regulatorily acceptable parameters?

Update on the D&O Insurance Market

All of the above data is interesting not only in an academic sense. It has real implications for the risk and risk mitigation decisions that SPAC sponsors, their target companies, investors, and deal teams make. Those decisions inevitably involve decisions on the size and structure of each outfit and team’s directors and officers (D&O) insurance. Higher risk yields lower availability of coverage and higher premiums. But aside from the risk itself, the availability and premiums are also dictated by the state of the overall insurance market.

After many months of an almost impossibly hard SPAC D&O market, substantially diminished deal volume both in the SPAC world and the traditional IPO world has caused many carriers to reconsider their stance. In the last few months, we have witnessed a palpable easing of terms and even of pricing. Of course, carriers are keeping a close eye on each new case and enforcement action. However, if litigation and enforcement trends continue to hold at the current level or decline further, we are likely to enjoy a period of reasonable D&O insurance pricing for SPACs in 2023.

An earlier version of this article appeared in the Woodruff Sawyer SPAC Notebook.

The past three years have been fraught with challenges for law firms and early-career attorneys. Demand for legal services has continued to expand, and the need for legal talent to help meet that demand has been at an all-time high. The market for associates has been incredibly hot with escalating salaries, big signing bonuses, and the offer of more flexibility around where associates can work than ever. However, firms have struggled with managing and developing attorneys in a remote and hybrid workplace. In a profession that leans heavily on an apprenticeship model for development, many senior practitioners are spending less time in the office and have not significantly shifted the way that they work with their junior counterparts to match the development that would have happened in a pre-pandemic, principally in-person work environment.

The lag in associate professional development (and consequential poor work product and less than ideal professional conduct) has not been met with the consequences and repercussions that those now in partnership and leadership would have experienced when they were junior attorneys.

And recent surveys say that many of these well-paid, flex-working, and highly sought-after early-career attorneys are not happy. They report feeling isolated and not being meaningfully connected with peers and colleagues in this remote work environment. They do not see how the work they are doing relates to the bigger picture and the career they want for themselves.

Today it is more important than ever for associates to take the lead in the progress of their professional and career development. With a looming recession, we are already seeing firms making cuts. Here, we review things associates can do now to improve their experience at work and ensure they avoid being on the list of people considered for layoffs if (when) things slow down.

Take ownership of your work and seek to add value

As an associate, you’ve been told to think of the firm’s partners as your clients. This means that you should be thinking about how your work can make a partner’s life easier. When you are given an assignment, avoid treating the work just as a task to be completed so you can move on to another task. Start to think like a partner; understand how the assignment fits into the larger client strategy, and take ownership of the work you are assigned. Look at deadlines and plan your time accordingly, be proactive, and ensure what you are working on is seen all the way through. “Your ownership shouldn’t end when you send a draft to the partner in an email,” said Vanessa Widener, managing partner and civil litigation attorney at Anderson, McPharlin & Conners LLP in California. “I get so many emails every day, it is likely I may not see something right away, so an associate that follows up stands out as a go-getter and is highly appreciated.”

To be an appreciated team member, learn partners’ styles and preferences. When it comes to communication, ask at the onset how they prefer to be communicated with: Do they want you to just call when you have a question, send a text, ask via email, schedule time to discuss? Do they have a writing style you can learn from their redlined drafts? Do they prefer single spaces after sentences, or do they avoid using adjectives or adverbs? “The associates that I enjoy working with the most write intentionally ‘for me,’” said Mark T. Cramer, shareholder in Buchalter’s Los Angeles office and chair of the class action practice group. “They know what edits I am going to make; they know if they start a sentence with ‘however’ I am going to change it to ‘but,’ so they use ‘but’ when they write for me. It shows me that they care and they are learning, and that really differentiates them.”

Communication is key when seeking to add value. The partner (and most definitely the client) won’t be happy to learn you spent ten hours researching something that the partner has the answer to on their desk. Managing expectations and facilitating regular communication are necessary to provide the level of service that will make you stand out. If you are unsure about something, ask a senior person, but do not wait and do nothing. “I’d rather rein someone in than have to prod them like a wet noodle,” said Cramer.

Add value by anticipating what needs to happen next. Josh Wurtzel, civil litigation partner at Schlam Stone & Dolan in New York, suggests: “If a motion to dismiss comes in, don’t wait for the partner. If you haven’t heard from anyone, read through everything, then make a call to the partner, give your suggestions on how you think it should be approached, and offer to write the first draft opposition.” When you are asked to do research, go the extra step and come back with what the law is and how it applies to the case, along with your recommendations for the approach moving forward. “Even if your suggestions are not 100% on point, people appreciate and recognize the value add and effort in that situation,” said Wurtzel.

Express your interest to learn, improve, and grow

Associates I work with sometimes worry that they will be perceived as overzealous or bothersome if they ask for help or feedback from the senior people they work with. I hear the opposite complaint from the partners I work with: If they notice the absence of questions and follow-up, they interpret it as either the associate feels confident, or they don’t care about improving. “If you are working on something that takes a good amount of time, make sure you talk with the partner to understand how your assignment fits in the bigger picture of what the strategy and objectives are for the client,” said Pooja Nair, partner and business litigator at Ervin Cohen and Jessup in Beverly Hills. “Expressing interest in learning should always be well received because ultimately the partner knows the work product will be better if you have a better understanding of the situation.” Make a point to ask questions and get feedback on your work. After a motion or contract is finalized, you should reach out to the partner to schedule a conversation to discuss and better understand the changes made and why they were made.

Identify areas where you would like to improve your skills, and then find professionals in your organization who have mastered those skills. “You can reach out to someone and say, ‘I hear you are amazing at depositions; I would love to sit in, I won’t bill for it,’ or ‘I think you are a fantastic writer; I would really love to work with you on something,’” suggests Cramer. It is likely the attorney will be flattered, and this kind of interaction will further develop the relationship. Plus, you will learn something you’re interested in, and the attorney you work with will likely feel invested in your success.

Build relationships

A huge benefit of regular physical proximity with colleagues is the opportunity to build familiarity and communicate often, which leads to connection and meaningful relationship-building. In other words, people at work get to know you and like you, and you get to know and like the people you work with. These relationships are avenues to improved learning of legal skills along with the inner workings and politics of a law firm and are critical in building a professional support system and ultimately true friendships. “Some of my best friends are people that I have met through work and have gotten to know over the last twenty-five years,” said Cramer.

With fewer in-person interactions available organically at law firms because of reduced in-office work expectations, as well as different preferences and changed habits around socializing in the office, associates need to take an expressly active role in creating opportunities to connect with peers and colleagues. To expedite these interactions, use technology to initiate relationships, so that when you do connect in person you can get the most out of those exchanges. Research the experienced people at your firm and identify things that you admire in their experience, background, or practice. Then you can reach out with a note like, “I am very interested in working with (X category of clients/Y type of matters/Z type of extracurriculars), and I see that you have had a lot of success in that area. If you are open to it, I would love to share some of my objectives and strategies around building my practice in that direction and would really appreciate hearing your thoughts. Are you available for a video call next Thursday or Friday?”

If you are working with a partner or a peer who is in the same region you are, suggest meeting in person for lunch/breakfast/drinks so you can get to know them a bit better. If you are attending a professional social event, invite a peer you would like to know better to come with you. Find out if a senior colleague you are working with on something is available to discuss the matter in person the next time they are in the office.

There are plenty of opportunities to connect in routine interactions, too. When you start calls or emails to review client matters, ask the partner about their weekend or their experience at that conference you know they attended. Look for opportunities to connect about something besides the work at hand. Mention the volunteer work or extracurriculars you are participating in, and share things that you care about. Show up to the events the firm puts together. Interactions at these events will be even more successful if you have made those initial introductions via email beforehand. Plus, you never know who you might end up talking to and about what. There are opportunities to connect in person that will start or bolster significant relationships that would not be possible otherwise, so be sure to show up so you can take advantage of them.

Develop unique expertise/knowledge that makes you essential

Wurtzel says the best way to ensure that your firm would not consider letting you go is to make yourself indispensable. “Be a critical person on the matter. Know all of the facts of the case—the procedural history, read all the deposition documents. Be on top of deadlines with a clear sense of where the case is going.”

Being of value to partners also means knowing how to effectively and efficiently solve their problems. If you know who internally to go to for help because they are good (paralegals, secretaries, other attorneys) and who it’s best to avoid because they will not be helpful, and where to find templates, and how to utilize and leverage the technology available, you can accurately estimate timelines and will be highly appreciated.

Look for a niche or distinctive expertise you can develop. There are a multitude of reasons why attorneys benefit when they build a niche expertise, and one of them is that when you are the go-to person at a firm for a specific type of matter or issue, it adds value for the firm’s clients and a benefit to the attorneys that will make it more likely they will want to make sure you stay at the firm.

Be visible

There is science behind the saying “out of sight, out of mind,” with a multitude of studies showing that physical and psychological distance are directly related. Attorneys who have not experienced the benefits that come with regularly working in close physical proximity with peers and colleagues may not recognize that they are losing out on opportunities to grow professionally. It is important to be a highly visible presence if you want to be known, recognized, and valued at your firm.

Building your reputation and visibility may happen by spending time in the office, but it is important to be increasingly intentional to get the most benefit out of now-reduced face time. Many associates report that when they go into the office no one is there, or the few people who are there are working with their doors closed. Associates can get more out of working in the office if they let people know that they are interested in connecting. Maximize your opportunities for face time, and schedule your days in the office around when your colleagues and peers will be there.

Be present and visible in video meetings; that means keeping your camera on, even if not everyone does. Moving to video instead of in-person meetings creates efficiency, but it is wise to treat these meetings with the same intention and objectives you would an in-person meeting. People should see you and hear you. Contribute, ask questions, and use the chat section to connect on a more personal level.

Use your growing niche to get exposure. “People notice when an associate takes the initiative to write or get involved outside of the firm; when it is clear an associate sees themselves as a leader,” said Nair. Nair started her career at a big firm and made a concerted effort to get involved in professional organizations outside of the firm. “Do things collaboratively with the firm, giving the firm exposure. Big firms will allow for that and eventually will encourage it, especially when it yields new or additional revenue. Beyond the short-term value for the firm, it’s vital that associates build their reputations for the long-term benefits to their careers.”

Cramer advises that when work eases up, associates should do things proactively to be visible or to improve themselves. “A dream day for me would be if a competent person came to me and said, ‘I am very interested in working on a class action advertising matter—do you have anything I can work with you on?’ And if I don’t at the moment, they suggest that we collaborate on an article and they take the lead on a draft. We’d get to work on something together, and it could likely lead to another thing… new work, attending a conference together, or another article.” Educate your colleagues on your expertise by sharing articles you’ve written and presentations you are giving on LinkedIn and internal channels, and be sure to bring it up in the conversations you are actively scheduling.

Be productive and professional

Treating partners like clients demonstrates your skill and ability to work with actual clients. Be sure to err on the side of being overly professional, especially in your communication. In emails, use greetings and sign-offs, complete sentences, and accurate grammar. Dress professionally if you are going to be on a video call or in-person meeting with colleagues; show up as if a client were going to be there.

Presentation is important, and revenue is essential. When a firm is preparing to make cuts, it is likely they will review hours billed to assess who is pulling their weight and creating economic value for the firm. If your hours are low, leadership will wonder if there is a reason none of the partners want to give this person work, or they may assume that partners are assigning the person work and this person is just not working enough.

Associates today can’t afford to wait for their firms to take the lead in their professional development. If you want to build a successful and fulfilling legal practice, you need to be more proactive and intentional than any associate before you. And as a junior professional interested in optimizing the experience of working at a law firm, you must prove you have what it takes to be a good lawyer and a valuable partner, and you must adapt to the professional expectations of the firm partners and clients. Even if markets don’t shift and demand for legal services continues to increase, when you take the actions mentioned here, you will gain better, more fulfilling work; make valuable connections and friendships; and advance more quickly in your career.

Technology companies in the payments space should pay close attention to the Federal Reserve’s (the Fed’s) upcoming launch of a long-awaited new payment system, the FedNow Service. The system will change the consumer payments landscape by providing a new instant payment alternative to existing retail payment rails.

It is rare for the U.S. central bank to build a wholly new payment rail, and importantly, the federal government has also announced its backing for instant payment systems. The FedNow Service promises to both pose challenges to fintech companies whose business models depend on activity over existing payments rails and offer key new opportunities to innovators in the space. These new drivers and risks will be important considerations for many players in the market and critical to their success.

The Fed’s Instant Payments Platform

An instant payment is a new type of payment from one bank account to another, where the recipient receives final funds in near real time, enabled by immediate interbank settlement of the payment. This means there is no buildup in interbank obligations, and end users can instantly send and receive money. This is an improvement to payments via credit or debit cards and automated clearinghouse (ACH), which come with higher costs or delays to receiving final funds.

FedNow, expected to launch between May and July of this year, will be the central bank’s new core instant payment infrastructure. It will process retail payments in real time, twenty-four hours a day, 365 days a year, with funds made available immediately for use by the payment recipient. Eligibility to participate in the new system will generally be limited to U.S. banks; these banks, in turn, would offer instant payment services to individuals and businesses. The new system is a much-needed upgrade to the national infrastructure for retail payments, which is currently closed on weekends and can at times take several days before funds are available. The Fed’s ultimate aim is to give consumers and merchants faster access to their funds and greater flexibility to manage cash flow, at low cost and with reduced payment risk.

A key milestone was the Fed’s October 2022 publication of the legal terms and conditions governing FedNow transfers, which contain granular legal details about the service. These terms reveal important shifts to the status quo and critical ways the FedNow Service will impact the competitive outlook for retail payments, especially for fintech companies.

Challenges and Opportunities for Technology Companies